Aerial Imaging Market Size, Share, Trends and Forecast by Aircraft Type, Camera Orientation, Application, End Use Sector, and Region, 2026-2034

Global Aerial Imaging Market Size, Share, Trends & Forecast (2026-2034)

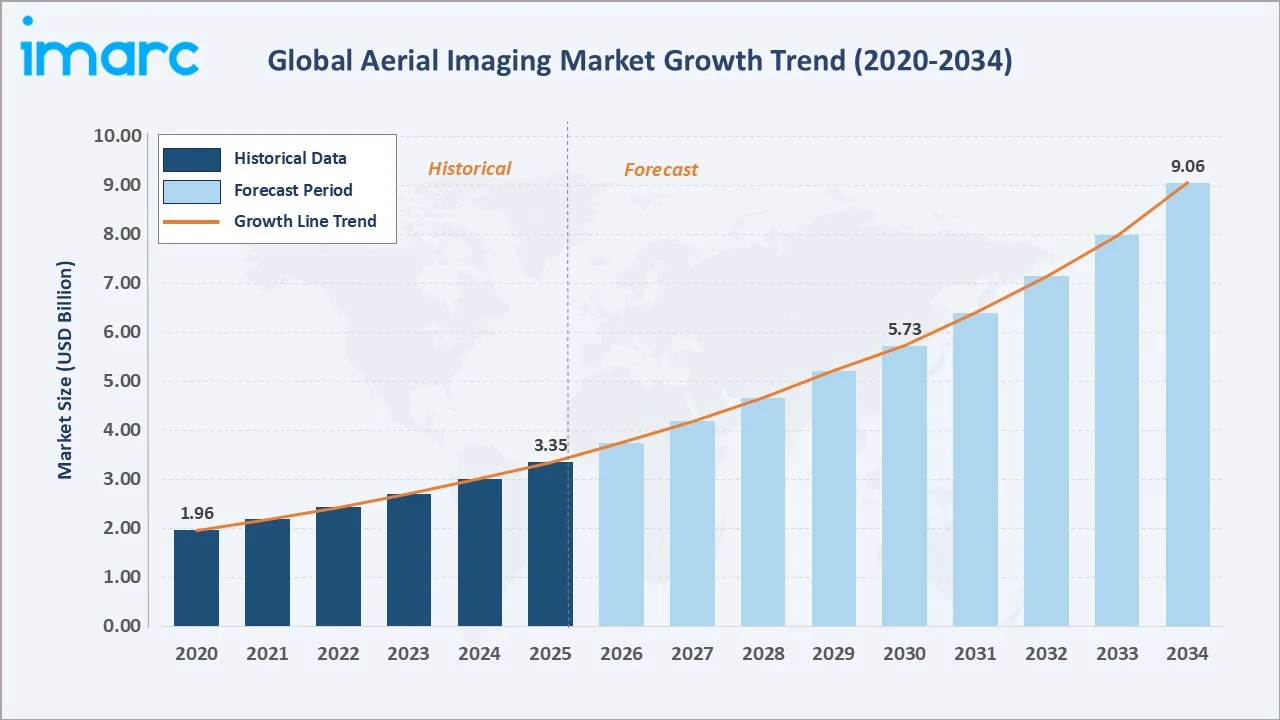

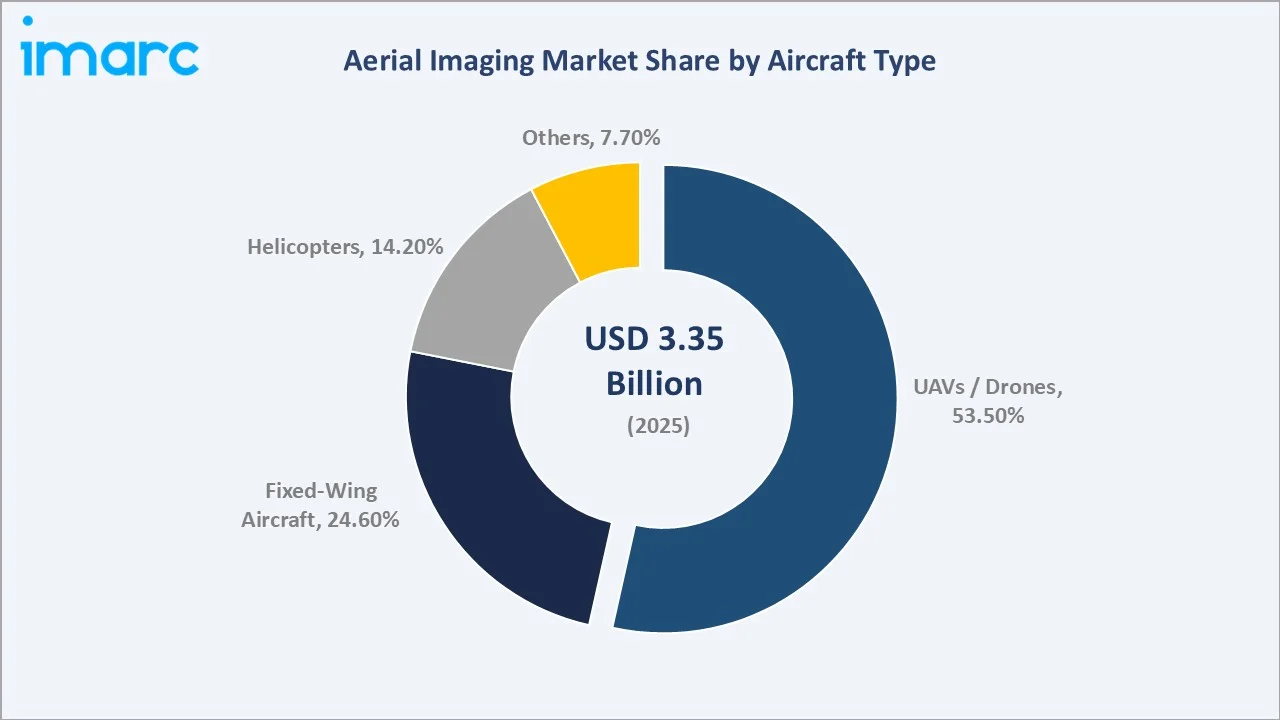

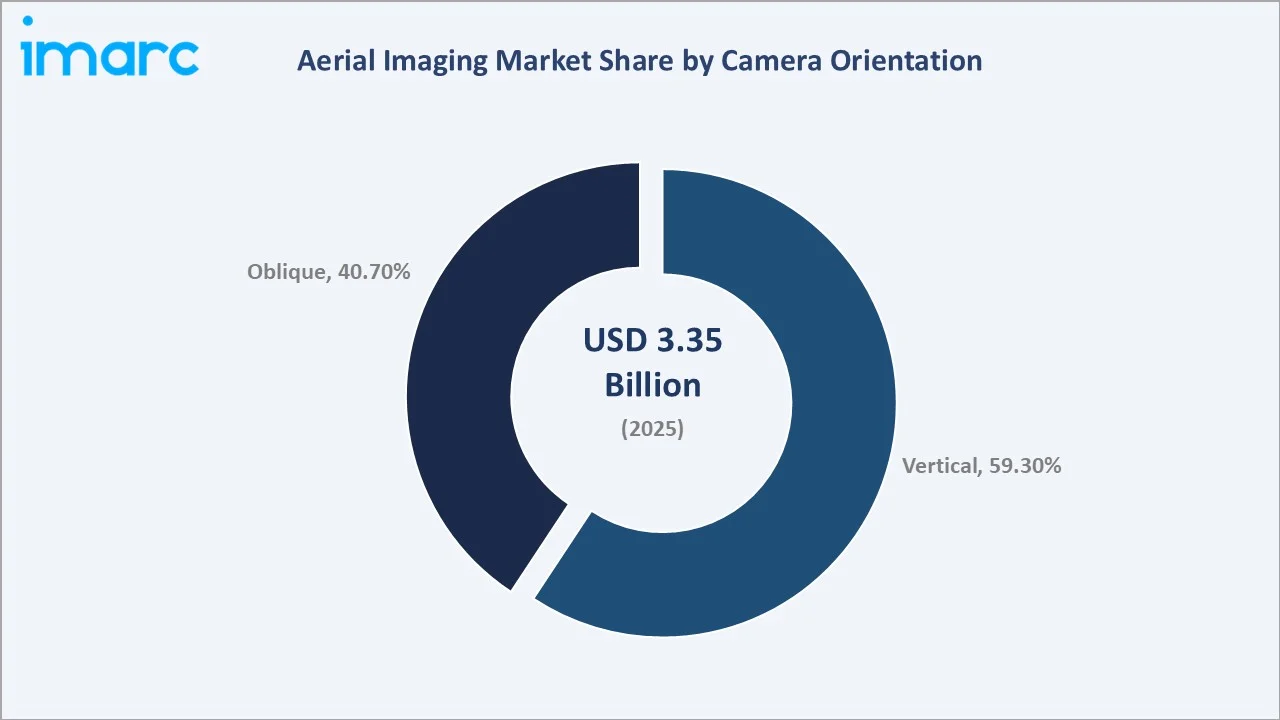

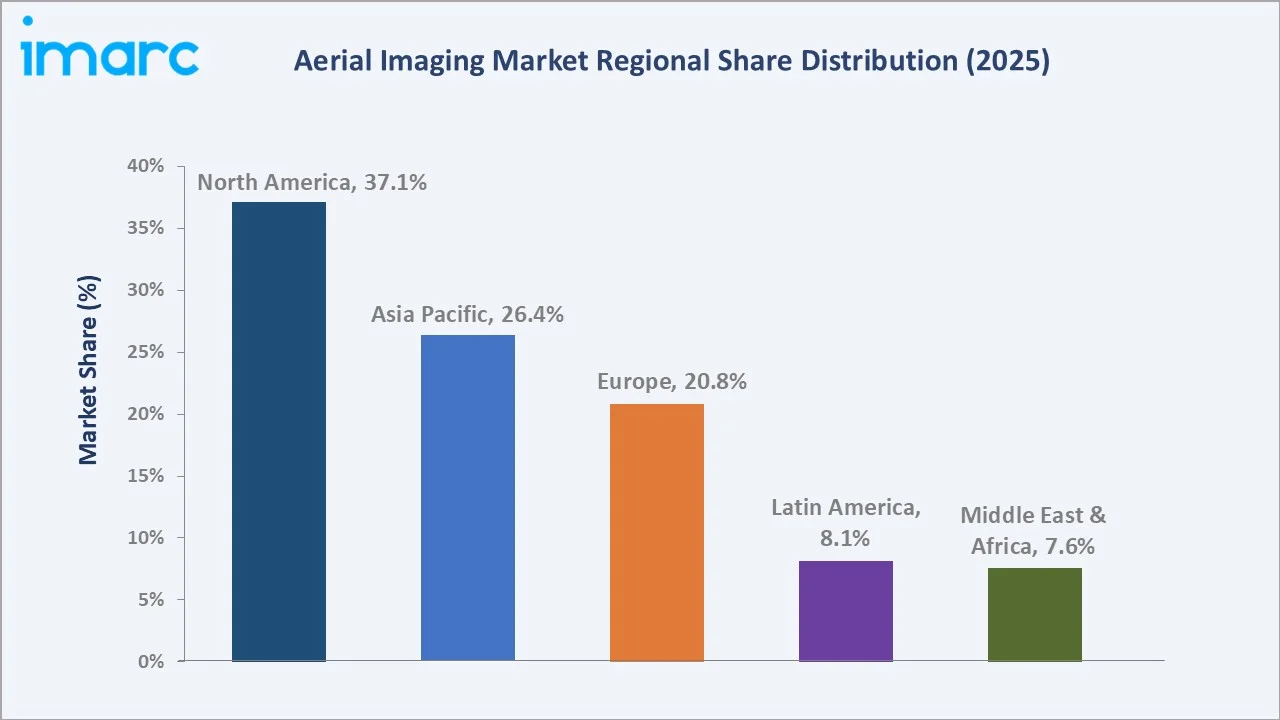

The global aerial imaging market was valued at USD 3.35 Billion in 2025 and is projected to reach USD 9.06 Billion by 2034, growing at a CAGR of 11.35%. Growth is driven by rising UAV/drone adoption in agriculture, defence, and infrastructure, advancements in LiDAR and multispectral sensors, AI-powered analytics, and supportive government regulations. In 2025, UAVs/drones lead the aircraft type segment (53.5%), vertical cameras dominate orientation (59.3%), and North America holds the largest regional share (37.1%).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.35 Billion |

|

Forecast Market Size (2034) |

USD 9.06 Billion |

|

CAGR (2026-2034) |

11.35% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (37.1% share, 2025) |

|

Leading Aircraft Type |

UAVs/Drones (53.5%, 2025) |

|

Leading Camera Orientation |

Vertical (59.3%, 2025) |

The global aerial imaging market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by drone proliferation, AI-driven analytics, and expanded commercial UAV applications across agriculture, construction, and defence sectors.

To get more information on this market, Request Sample

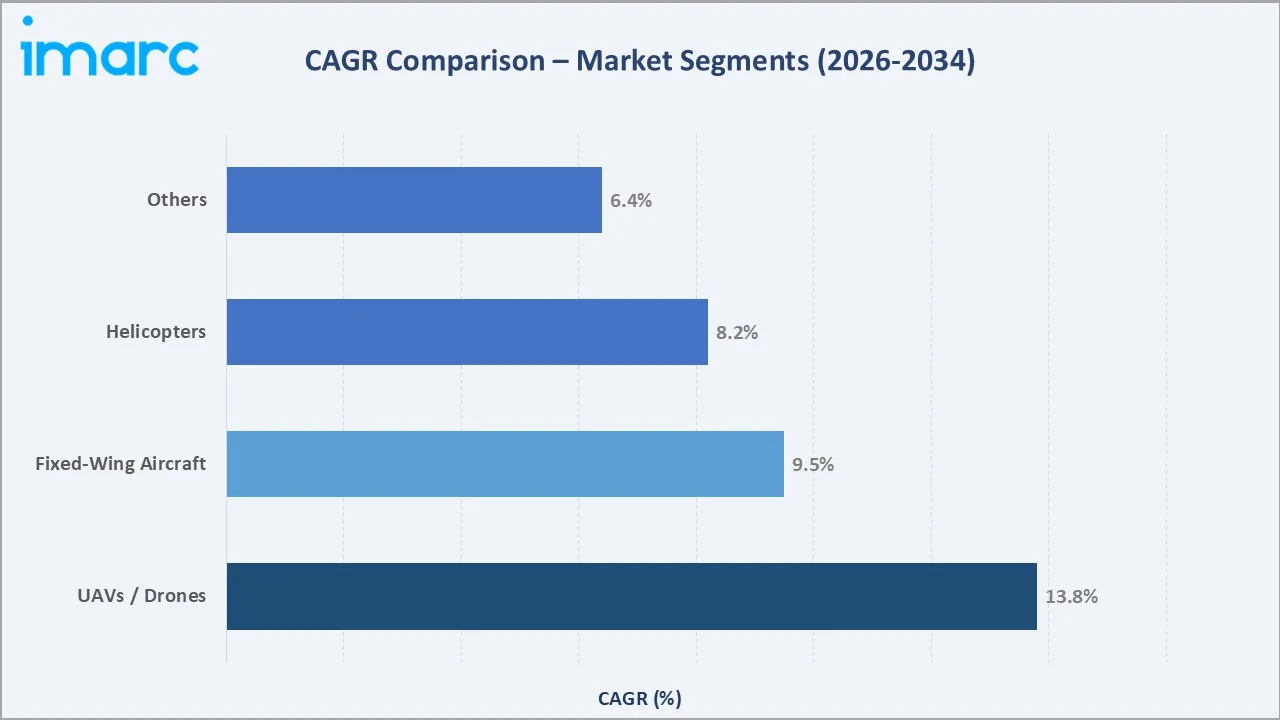

Aircraft type segment CAGR comparisons highlighting UAVs/Drones as the dominant and fastest-growing platform category, followed by Fixed-Wing Aircraft as a significant contributor within the global aerial imaging industry analysis through 2034.

Executive Summary

The global aerial imaging market is undergoing a significant transformation propelled by the convergence of UAV technology, artificial intelligence, and geospatial data analytics. Valued at USD 3.35 Billion in 2025, the market is projected to reach USD 9.06 Billion by 2034, growing at a CAGR of 11.35%. The increasing deployment of drones for precision agriculture, infrastructure inspection, environmental monitoring, and defence surveillance is creating sustained demand across global markets.

UAVs/Drones command the dominant aircraft type share at 53.5% in 2025, driven by their cost-effectiveness, operational flexibility, and compatibility with advanced imaging payloads, including LiDAR, multispectral, and thermal sensors. Their capacity to operate at low altitudes enables the collection of high-resolution, close-range imagery ideal for precision agriculture, construction site monitoring, and land-use assessment. Vertical camera orientation leads the camera orientation segment at 59.3%, underpinned by its critical role in producing orthophotographs, topographic maps, and GIS-ready datasets for urban planning and environmental management.

North America commands a 37.1% global revenue share in 2025, anchored by the United States, where significant government investments in drone technology, supportive FAA regulations, and widespread commercial UAV adoption across agriculture, energy, and construction underpin robust market growth. Asia-Pacific holds 26.4% in 2025, driven by rapid smart city development in China and India, expanding mining operations, and growing deployment of aerial imaging in disaster response. Europe accounts for 20.8%, supported by precision agriculture applications and stringent environmental monitoring requirements.

Key Market Insights

|

Insight |

Data |

|

Largest Aircraft Type |

UAVs/Drones – 53.5% share (2025) |

|

Leading Camera Orientation |

Vertical – 59.3% share (2025) |

|

Leading Region |

North America – 37.1% revenue share (2025) |

|

Second Region |

Asia-Pacific – 26.4% revenue share (2025) |

|

Top Companies |

Fugro N.V., EagleView Technologies, Blom Norway, GeoVantage Inc., Digital Aerial Solutions |

Key Analytical Observations Supporting the Above Data:

- UAVs/Drones' 53.5% dominance in 2025 reflects the industry-wide shift toward cost-effective, flexible aerial platforms capable of carrying advanced multispectral, LiDAR, and thermal imaging payloads across commercial and industrial sectors.

- Vertical camera orientation leads at 59.3% in 2025, driven by demand for precision orthophotography, topographic mapping, and GIS-ready aerial datasets across agriculture, urban planning, and infrastructure management applications.

- North America's 37.1% global dominance in 2025 reflects the region's advanced regulatory environment, substantial defence investments, and high commercial UAV adoption across agriculture, construction, energy, and public safety sectors.

- Asia-Pacific's 26.4% share is rapidly expanding, supported by China's smart city initiatives, India's growing drone manufacturing ecosystem, and rising demand for aerial imaging in resource exploration across the region.

Global Aerial Imaging Market Overview

Aerial imaging captures, processes, and analyzes high-resolution data from airborne platforms such as UAVs, drones, helicopters, and fixed-wing aircraft, equipped with optical, LiDAR, multispectral, hyperspectral, and thermal sensors. It serves applications across agriculture, construction, defence, environmental monitoring, and urban planning, enabling precision agriculture, infrastructure inspection, defence surveillance, disaster response, and smart city development. The ecosystem spans hardware manufacturers, geospatial software and AI analytics providers, regulatory bodies, and government and commercial end-users. Market growth is driven by rising government infrastructure investments, widespread adoption of precision agriculture technologies, and the global democratization of drones as manufacturing costs decline.

Market Dynamics

To evaluate market opportunities, Request Sample

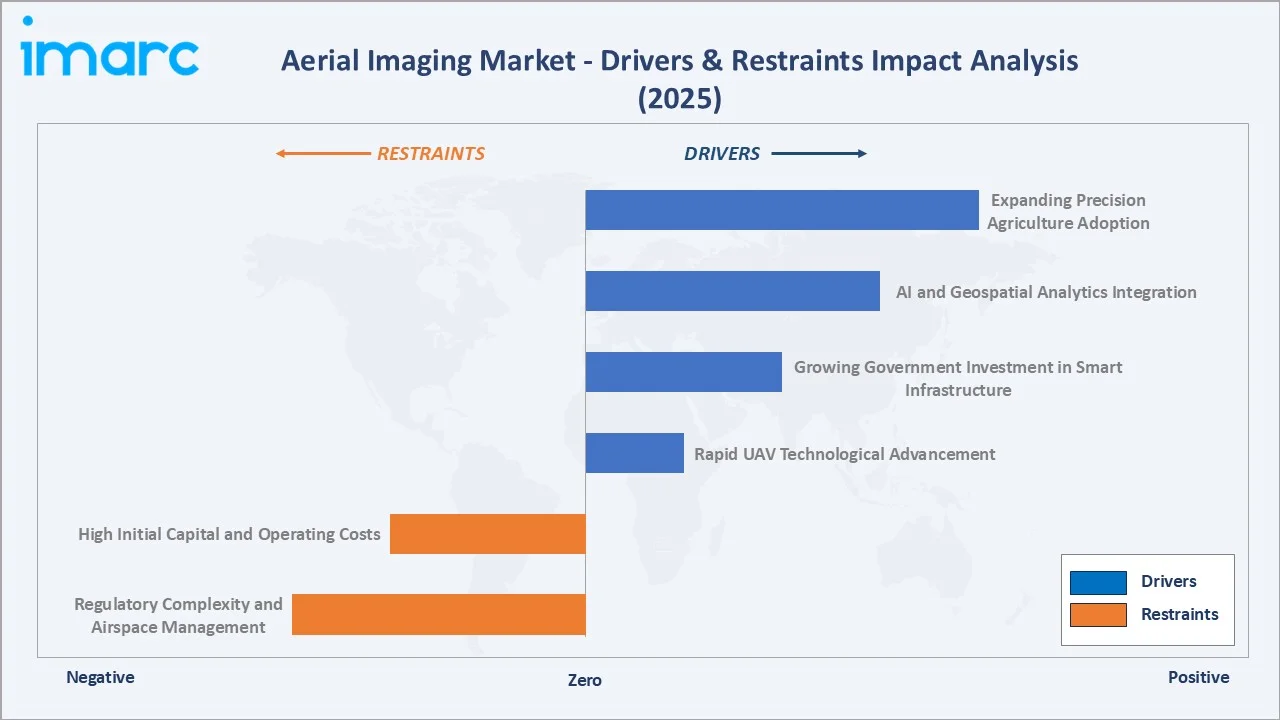

Market Drivers

- Rapid UAV Technological Advancement: Improvements in drone endurance, payload, and autonomous flight are expanding aerial imaging applications. Modern UAVs with AI navigation and automated mission planning can survey thousands of acres per flight, producing structured datasets for GIS analysis.

- Growing Government Investment in Smart Infrastructure: Programs for smart cities, land-use monitoring, disaster management, and environmental protection are driving demand for aerial imaging. Municipal and national agencies increasingly rely on regular aerial surveys for urban planning and infrastructure management.

- AI and Geospatial Analytics Integration: Combining AI-powered image processing with aerial data platforms reduces analysis time and enhances insights. Automated object detection, change detection, and predictive modelling are unlocking new high-value applications in agriculture, construction, and insurance.

- Expanding Precision Agriculture Adoption: Farmers use aerial imaging for crop health monitoring, pest detection, irrigation optimization, and yield improvement.

Market Restraints

- Regulatory Complexity and Airspace Management: Fragmented drone regulations across jurisdictions create compliance challenges for operators, particularly for cross-border and beyond-visual-line-of-sight (BVLOS) operations critical to large-scale aerial imaging deployments.

- High Initial Capital and Operating Costs: Enterprise-grade aerial imaging platforms with LiDAR or hyperspectral payloads require substantial upfront investment, limiting adoption among small and medium-sized operators in emerging markets.

Market Opportunities

- AI-Powered Autonomous Aerial Survey Platforms: The development of fully autonomous drone survey systems capable of executing complex multi-point missions without human intervention represents a significant market expansion opportunity, particularly for large-scale infrastructure inspection and environmental monitoring.

- Climate Monitoring and Environmental Conservation: Growing global emphasis on carbon monitoring, deforestation tracking, and biodiversity assessment is creating new demand streams for aerial imaging services among government agencies, conservation organizations, and sustainability-focused corporations.

- Defence and Border Security Expansion: Rising global defence budgets and security concerns are driving significant investments in aerial surveillance platforms, with the EDGE Group's USD 10 Million investment in ThirdEye drone technology in 2025 exemplifying the growing defence-commercial aerial imaging convergence.

Market Challenges

- Data Privacy and Security Concerns: The collection of high-resolution aerial imagery of urban areas and private properties raises significant privacy concerns, with evolving regulatory frameworks creating compliance uncertainty for commercial operators.

- Skilled Workforce Shortage: The shortage of qualified drone pilots, geospatial data analysts, and AI integration specialists is constraining the pace of market expansion, particularly in emerging market regions.

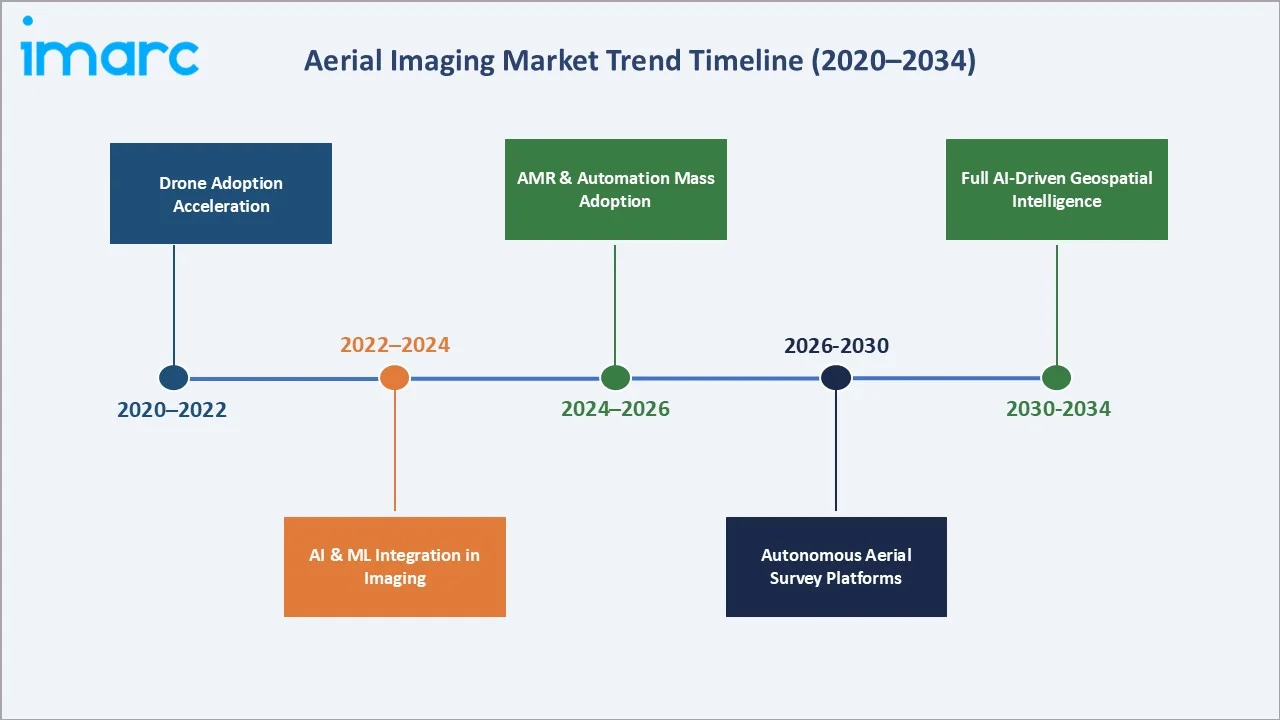

Emerging Market Trends

1. Growing Deployment of UAVs in the Construction Sector

The construction sector is rapidly adopting aerial imaging, with drones used for site mapping, progress monitoring, structural inspection, and safety compliance. Aerial imaging is increasingly a standard tool on construction sites, enhancing scheduling efficiency, cost management, and quality assurance.

2. Tourism and Scenic Aerial Content Creation

The global resurgence of international travel has created a substantial new market for aerial imaging in tourism promotion and destination marketing. According to UN Tourism’s May 2025 World Tourism Barometer, international tourist arrivals (overnight visitors) increased by 5% in Q1 2025 compared with Q1 2024, with over ~300 million travellers crossing international borders in the first three months of 2025 — roughly 14 million more than in the same period of 2024. This reflects continued growth in global travel demand despite economic and geopolitical headwinds.

3. AI and IoT Integration Transforming Aerial Platforms

The integration of artificial intelligence and Internet of Things connectivity into aerial imaging platforms is fundamentally enhancing data capture, transmission, and analysis capabilities. AI-equipped drones can perform real-time image analysis, detecting patterns and anomalies without human intervention, while IoT connectivity enables seamless data exchange with ground-based management systems. In May 2025, Quantum Systems raised €160 million in Series C funding led by Balderton Capital with support from Hensoldt, Airbus Defence and Space, Bullhound, LP&E AG, Porsche SE, and Peter Thiel’s funds, aiming to scale AI-powered drone manufacturing and expand autonomous aerial intelligence across Europe and Asia‑Pacific.

4. Expansion of LiDAR and Multispectral Imaging Applications

Advanced sensors like LiDAR, multispectral, and hyperspectral cameras are extending aerial imaging beyond photography, enabling 3D terrain modelling, detailed vegetation analysis, and precision data collection for agriculture, mining, and environmental monitoring.

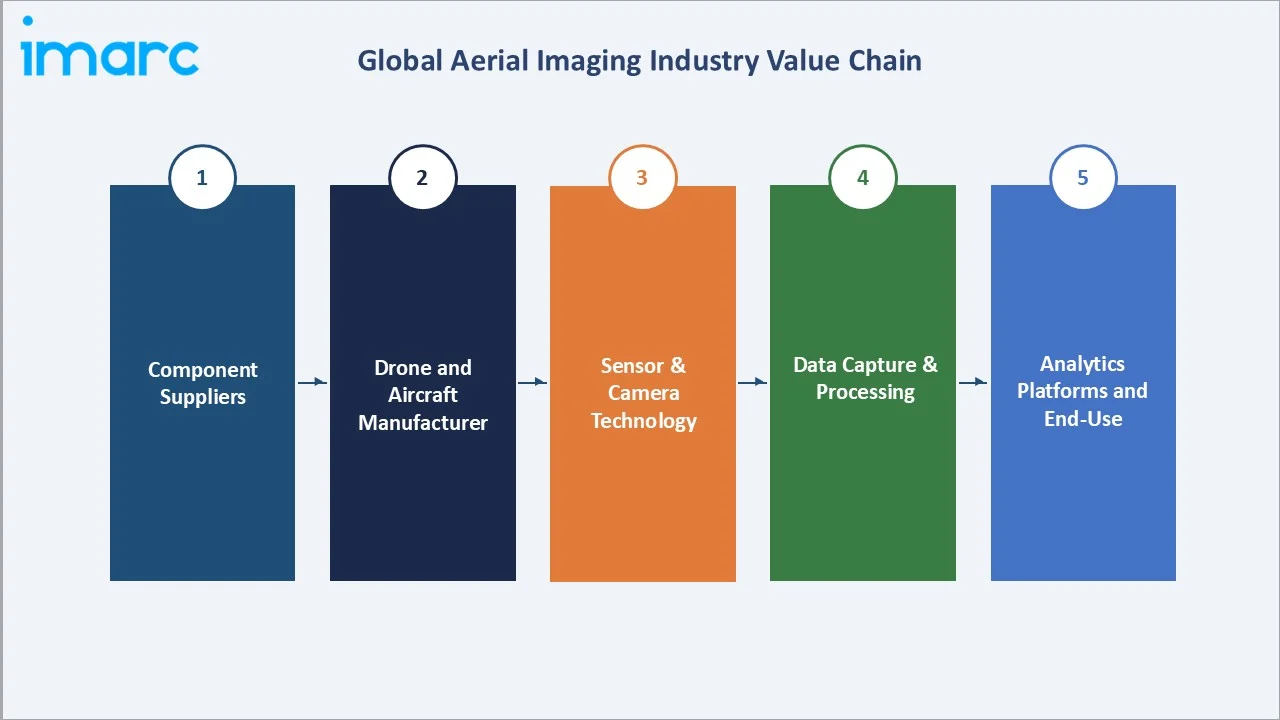

Industry Value Chain Analysis

The aerial imaging industry value chain spans six integrated stages from component supply through end-use delivery, with each stage presenting distinct competitive dynamics and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Component Suppliers |

Sensor manufacturers, battery suppliers, composite materials, and GPS/GNSS module providers |

|

Drone & Aircraft Mfrs |

DJI, Parrot, Autel Robotics, senseFly, Wingtra, Quantum Systems, Textron Aviation |

|

Sensor & Camera Tech |

Teledyne FLIR, Sony, Phase One, Micasense, Velodyne (LiDAR), Trimble, Leica Geosystems |

|

Data Capture Services |

Fugro N.V., EagleView Technologies, Blom Norway, Cooper Aerial Surveys, Kucera International |

|

Analytics Platforms |

Esri (ArcGIS), Pix4D, DroneDeploy, Bentley Systems, Trimble Business Center |

|

End-Use Sectors |

Government agencies, agriculture, construction, defence, energy, media & entertainment |

Geospatial data service providers hold the highest strategic value in the aerial imaging chain, combining hardware, sensors, and analytics into turnkey solutions for clients. However, the rise of affordable drones and cloud-based analytics allows operators to perform data capture and analysis in-house, reducing reliance on traditional full-service survey firms.

Technology Landscape in the Aerial Imaging Industry

UAV and Drone Platform Technologies

Modern aerial imaging drones incorporate advanced flight control systems, extended battery endurance platforms delivering 45-90 minute flight times, hybrid fixed-wing/multirotor designs for large-area coverage, and autonomous mission planning with obstacle avoidance. In January 2025, DJI launched the DJI Flip, a lightweight vlog‑focused drone that captures 48 MP stills and 4K video with an integrated 1/1.3‑inch CMOS sensor, and includes AI subject tracking and intelligent shooting modes — underscoring rapid capability advancement in commercial drone platforms.

Imaging Sensor Technologies

The aerial imaging sensor landscape includes RGB cameras, LiDAR, multispectral/hyperspectral, thermal, and OGI sensors. In May 2025, Teledyne FLIR OEM and AerialOGI launched the AerialOGI‑N, a dual-use OGI module for drone- or handheld-mounted methane and industrial gas detection, advancing specialized aerial sensing capabilities.

AI, Data Processing, and Analytics

Cloud-based photogrammetry and AI-powered analytics convert aerial imagery into actionable geospatial intelligence. Automated object detection and machine learning enable sub-meter mapping, crop health forecasting, and infrastructure assessment, while 5G-enabled UAVs provide real-time data for time-critical applications like disaster response and emergency management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Aircraft Type |

UAVs/Drone |

53.5% |

2025 |

|

Camera Orientation |

Vertical |

59.3% |

2025 |

|

Application |

Geospatial Mapping |

26.8% |

2025 |

|

End Use Sector |

Goverment |

24.3% |

2025 |

|

Region |

North America |

37.1% |

2025 |

By Aircraft Type

UAVs/Drones command a dominant 53.5% majority share in 2025, reflecting the industry-wide standardization of drone platforms as the primary aerial imaging delivery vehicle across commercial and industrial applications. The UAV segment benefits from continuously declining hardware costs, expanding payload compatibility, and the development of automated mission planning software that enables operators to execute complex survey missions with minimal technical expertise. Regulatory frameworks in key markets, including the FAA's Part 107 rules in the United States and EASA's U-Space framework in Europe, have created structured pathways for commercial drone operations, supporting market expansion.

To access detailed market analysis, Request Sample

Fixed-wing aircraft hold 24.6% of the market, favoured for large-area surveys due to endurance and coverage efficiency. Helicopters account for 14.2%, used in manned photography, broadcast, and specialized inspections, while other platforms (balloons, airships, hybrids) make up 7.7% for niche applications.

By Camera Orientation

Vertical camera orientation leads with a 59.3% market share in 2025, driven by its critical role in generating orthophotographs and nadir-view datasets essential for GIS mapping, topographic surveys, and land-use classification. Vertical imaging produces precisely scaled, geometrically corrected outputs directly compatible with standard GIS platforms, including Esri ArcGIS and QGIS, making it the default orientation for professional geospatial data collection across agriculture, urban planning, and environmental monitoring sectors.

Oblique camera orientation accounts for 40.7% and is experiencing faster growth driven by expanding applications in 3D city modelling, real estate marketing, and infrastructure visualization. High oblique imaging provides angled perspectives that reveal building facades and structural details invisible to vertical cameras, while low oblique imaging captures ground-level textures and features valuable for forensic documentation and heritage conservation applications. The growing adoption of multi-camera rigs capturing simultaneous vertical and oblique imagery is further blurring the segment boundary.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

37.1% |

UAV investment, FAA regulations, agriculture, defence, infrastructure, smart city growth |

|

Asia-Pacific |

26.4% |

Smart city development in China/India, mining expansion, disaster response, EV infrastructure |

|

Europe |

20.8% |

Precision agriculture, EU environmental mandates, LiDAR topographic surveys, energy inspection |

|

Latin America |

8.1% |

Precision agriculture, infrastructure investment, forest monitoring, and geospatial analytics growth |

|

Middle East & Africa |

7.6% |

Oil & gas exploration, smart city megaprojects, heritage documentation, defence surveillance |

North America commands a 37.1% global revenue share in 2025, the most dominant regional position in the global aerial imaging market. The United States holds approximately 81.2% of the North American market, anchored by significant government and defence investments in UAV technology. The FAA's evolving regulatory framework for commercial drone operations, including expanded BVLOS authorization pathways, is progressively enabling more sophisticated aerial imaging deployments across the country.

Asia-Pacific, with 26.4% in 2025, is the fastest-growing regional market supported by China's dual role as the world's largest drone manufacturing hub and a rapidly expanding commercial UAV adopter across agriculture and smart city applications. India's drone ecosystem is experiencing significant policy-driven expansion following the PLI scheme for drone manufacturing, while Asia-Pacific mining GDP growth is driving demand for aerial imaging in resource exploration. Latin America, at 8.1%, is growing, supported by precision agriculture investment.

Competitive Landscape

|

Company Name |

Key Platform |

Market Position |

Core Strength |

|

Fugro N.V. |

Fugro GEO |

Leader |

Geospatial data services, offshore & onshore survey expertise, global reach |

|

EagleView Technologies |

EagleView Analytics |

Leader |

AI-powered roof & property analytics, insurance, government data services |

|

Blom Norway (Terratec AS) |

Blom Survey |

Established/Regional |

Aerial mapping, LiDAR, photogrammetry, Scandinavian & European presence |

|

GeoVantage (John Deere) |

GeoVantage Platform |

Niche |

Precision agriculture imagery, crop health monitoring, Deere ecosystem integration |

|

Digital Aerial Solutions |

DAS Platform |

Emerging |

Custom aerial survey services, multi-sensor payloads, and environmental monitoring |

|

Global UAV Technologies |

Scout Platform |

Emerging |

Fixed-wing UAV platforms, beyond-visual-line-of-sight operations, resource sector |

|

Cooper Aerial Surveys |

Cooper Survey |

Emerging |

Traditional aerial photography, film & digital mapping, US market focus |

|

Kucera International |

Kucera Aerial |

Established |

Orthophoto mapping, infrastructure surveying, and US government contracts |

The aerial imaging competitive landscape is characterized by a diverse mix of full-service geospatial data providers, technology-driven drone analytics platforms, and specialized sector-focused operators. Major players are investing in AI and machine learning integration for automated image processing, expanding their cloud analytics capabilities, and forming strategic partnerships with hardware manufacturers to offer end-to-end data intelligence solutions. In December 2024, Nokia and Motorola Solutions launched an AI-powered automated drone-in-a-box solution integrating Nokia Drone Networks with Motorola's CAPE software, enhancing real-time situational awareness for public safety and industrial applications and setting a new benchmark for integrated aerial imaging system deployment.

Key Company Profiles

Fugro N.V.

- Product & Platform Portfolio: Fugro GEO, aerial LiDAR survey services, photogrammetric mapping, environmental remote sensing.

- Recent Developments: In 2025, Fugro expanded its geospatial operations across Asia-Pacific and the Middle East, securing major offshore and energy-related survey projects and deploying advanced geodata acquisition technologies, including airborne LiDAR and remote sensing solutions, for applications such as coastal monitoring and offshore infrastructure assessment.

- Strategic Focus: Fugro's strategy centers on integrating aerial imaging with subsurface and marine geospatial data to offer comprehensive site characterization services for energy transition projects, infrastructure development, and natural disaster risk assessment globally.

EagleView Technologies Inc.

- Product & Platform Portfolio: EagleView Analytics, CogoSystem, Assess Pro, roof intelligence platform, property data analytics.

- Recent Developments: EagleView continued advancing its AI-powered property intelligence capabilities in 2025, leveraging high-resolution oblique aerial imagery and machine learning to enhance automated property assessment, risk analysis, and underwriting workflows for insurance and government applications.

- Strategic Focus: EagleView's strategy focuses on deepening data analytics capabilities for the insurance, government, and construction sectors, leveraging its proprietary oblique aerial imagery archive and AI processing platform to deliver automated property and infrastructure insights at scale.

Global UAV Technologies Ltd.

- Product & Platform Portfolio: Scout fixed-wing UAV platform, beyond-visual-line-of-sight survey systems, resource sector data capture services.

- Recent Developments: In 2025, Canada expanded its BVLOS (Beyond Visual Line of Sight) regulatory framework, introducing new certification pathways that enable operators to conduct long-range drone missions for applications such as pipeline corridor monitoring and remote resource exploration, significantly extending aerial imaging coverage into previously inaccessible regions.

- Strategic Focus: Global UAV's strategy targets the resource extraction sector with high-endurance fixed-wing UAV platforms designed for extended-range missions in remote environments, positioning the company to capture growing demand for aerial imaging in mining, forestry, and energy infrastructure inspection.

Market Concentration Analysis

The global aerial imaging market exhibits moderate concentration among established geospatial service providers and technology-enabled platforms, with the top five companies collectively accounting for approximately 30–38% of global market revenue in 2025. The market is experiencing a bifurcated dynamic: at the enterprise and government tier, consolidation is occurring as complex multi-sensor aerial survey requirements demand significant capital investment, technical expertise, and regulatory certifications that only established players can provide at scale.

Simultaneously, the democratization of drone hardware and cloud-based analytics software is enabling a large number of regional and specialist operators to compete effectively in niche application segments. The commercial UAV services market is particularly fragmented at the small operator level, with thousands of FAA Part 107 certified pilots and regional survey firms serving local markets across agriculture, real estate, and construction inspection. This fragmentation presents both competitive challenges and acquisition opportunities for larger geospatial service providers seeking to expand geographic and sector coverage.

Investment & Growth Opportunities

Fastest-Growing Segments

UAVs/Drones represent the highest-growth aircraft type at an estimated ~13.8% CAGR through 2034, driven by continuous hardware capability improvements, expanding payload options, and the development of autonomous mission execution capabilities. AI-powered aerial analytics is emerging as the fastest-growing technology sub-segment, with automated image processing platforms enabling geospatial insights at scales and speeds that are transforming workflows across agriculture, construction, and environmental monitoring sectors.

Emerging Market Expansion

Asia-Pacific presents the most compelling emerging market opportunity, with India's drone manufacturing PLI scheme, China's smart city expansion program, and Southeast Asia's rapidly growing agricultural drone adoption creating diverse demand growth vectors. The Middle East's smart city megaprojects, including Saudi Arabia's NEOM development, represent significant aerial imaging service demand for topographic mapping, infrastructure monitoring, and construction progress tracking. Latin America's precision agriculture expansion, particularly in Brazil and Argentina, offers growing opportunities for multispectral aerial imaging service providers.

Venture & Private Investment Trends

The aerial imaging sector is attracting significant venture capital and strategic investment. The aerial imaging sector is attracting strong venture capital and strategic investment. In May 2025, Quantum Systems raised €160 million in Series C funding to scale AI-driven drone systems and global expansion. In February 2025, Hidden Level secured USD 65 million in Series C funding to expand its airspace monitoring and drone detection technologies. Additionally, in January 2025, EDGE Group invested USD 10 million in ThirdEye Systems, strengthening AI-based drone detection capabilities. Defence technology convergence with commercial aerial imaging is emerging as a particularly active investment theme.

Future Market Outlook (2026-2034)

The global aerial imaging market forecast projects steady value expansion from USD 3.35 Billion in 2025 to USD 9.06 Billion by 2034 at a CAGR of 11.35%, representing nearly a tripling of market value underpinned by UAV technology proliferation, AI analytics integration, expanding application scope, and growing government and commercial investment across all major global regions.

Three technology trajectories are most likely to reshape the aerial imaging market through 2034. First, fully autonomous aerial survey platforms capable of BVLOS operations at scale will transform large-area data collection economics, reducing cost-per-acre imaging costs by 60–80% for agriculture, forestry, and infrastructure monitoring applications. Second, real-time AI analytics integration will shift the value proposition from data capture to instant intelligence delivery, enabling same-day decision support for crop management, construction scheduling, and emergency response. Third, the convergence of aerial, satellite, and ground-sensor data into unified geospatial intelligence platforms will create comprehensive situational awareness capabilities that extend the aerial imaging market into new sectors, including insurance, financial services, and climate risk assessment.

By 2034, the aerial imaging industry is expected to have completed its evolution from a project-based survey service into a continuous geospatial intelligence subscription economy, with persistent monitoring platforms delivering regular aerial data updates for agriculture, infrastructure, and environmental management clients on automated collection schedules.

Research Methodology

Primary Research

Primary research encompassed structured interviews with aerial imaging industry stakeholders, including drone technology executives, geospatial data service providers, agricultural technology specialists, defence and government procurement officers, and commercial UAV operators. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments across the global aerial imaging value chain.

Secondary Research

Secondary sources include FAA UAS registration and operational data, EASA drone regulation publications, UN Tourism arrival statistics, IEA infrastructure investment reports, India MOSPI mining GDP data, company annual reports and press releases, and trade publications including Inside Unmanned Systems, Commercial UAV News, and GIM International. All statistical data points referenced in this report are sourced from publicly available government and industry publications dated 2024–2025.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating historical aerial imaging adoption rates, UAV shipment data, government investment trends, agricultural technology adoption curves, and macroeconomic growth indicators. Scenario analysis incorporating base, optimistic, and conservative cases was performed to account for regulatory uncertainty and technology adoption pace variability.

Aerial Imaging Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Aircraft Types Covered | Fixed-Wing Aircraft, Helicopters, UAVs/Drones, Others |

| Camera Orientations Covered |

|

| Applications Covered | Geospatial Mapping, Infrastructure Planning, Asset Inventory Management, Environmental Monitoring, National and Urban Mapping, Surveillance and Monitoring, Disaster Management, Others |

| End Use Sectors Covered | Government, Energy, Defense, Agriculture and Forestry, Construction and Archaeology, Media and Entertainment, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Fugro N.V., EagleView Technologies, Blom Norway (Terratec AS), GeoVantage (John Deere), Digital Aerial Solutions, Global UAV Technologies, Cooper Aerial Surveys, Kucera International, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aerial imaging market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aerial imaging market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aerial imaging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Aerial Imaging Market Report

The global aerial imaging market was valued at USD 3.35 Billion in 2025, driven by growing UAV adoption across agriculture, construction, defence, and environmental monitoring sectors.

The market is projected to reach USD 9.06 Billion by 2034, growing at a CAGR of 11.35% during 2026-2034, driven by UAV technology advancement, AI integration, and expanding government and commercial aerial imaging applications.

UAVs/Drones lead the aircraft type segment with a 53.5% share in 2025, driven by their cost-effectiveness, operational flexibility, and compatibility with advanced multispectral, LiDAR, and thermal imaging payloads across commercial and industrial applications.

Vertical camera orientation leads with a 59.3% share in 2025, driven by its critical role in producing GIS-ready orthophotographs and topographic datasets for agriculture, urban planning, and infrastructure management applications.

North America leads with a 37.1% share in 2025, driven by significant U.S. government defence investments, supportive FAA drone regulations, and widespread commercial UAV adoption across agriculture, construction, and public safety sectors.

Key drivers include rapid UAV technology advancement, growing government investment in smart infrastructure and defence, expanding precision agriculture adoption, AI-powered geospatial analytics integration, and the democratization of commercial drone platforms as hardware costs continue to decline globally.

UAVs/Drones represent the fastest-growing aircraft type at an estimated ~13.8% CAGR through 2034, supported by continuous hardware capability improvements, expanding autonomous operation capabilities, and growing adoption across agriculture, construction, and environmental monitoring sectors.

Leading companies include Fugro N.V., EagleView Technologies, Blom Norway (Terratec AS), GeoVantage (John Deere), Digital Aerial Solutions, Global UAV Technologies, Cooper Aerial Surveys, and Kucera International.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)