Aerospace 3D Printing Market Report by Offerings (Materials, Printers, Software, Services), Printing Technology (Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Selective Laser Melting (SLM), Selective Laser Sintering (SLS), and Others), Platform (Aircraft, Unmanned Ariel Vehicles (UAV), Spacecraft), Application (Engine Component, Space Component, Structural Component), End Use (OEM, MRO), and Region 2026-2034

Market Overview:

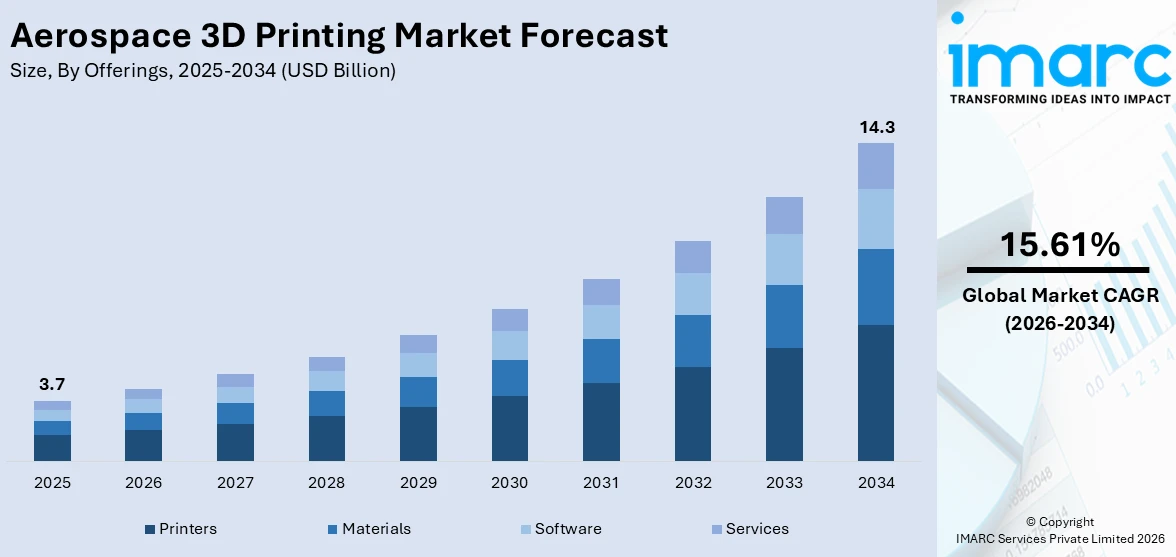

The global aerospace 3D printing market size reached USD 3.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 14.3 Billion by 2034, exhibiting a growth rate (CAGR) of 15.61% during 2026-2034. The growing demand for lightweight and fuel-efficient aircraft, increasing initiatives in reducing carbon emissions from aircraft, and rising investments by governing agencies of various countries in strengthening their defense sector are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3.7 Billion |

| Market Forecast in 2034 | USD 14.3 Billion |

| Market Growth Rate (2026-2034) | 15.61% |

Aerospace 3D printing refers to the process of manufacturing various three-dimensional components of aircraft using 3D printers. It is an additive manufacturing procedure wherein a composite material is deposited layer-by-layer via a 3D printer to create a durable aircraft structure. It also helps engineers and designers create innovative prototypes by making numerous customizations according to their requirements. It does not generate any excess or surplus products that often occur with series production and consequently assists in preventing the wastage of raw materials.

To get more information on this market Request Sample

At present, the increasing demand for aerospace 3D printing, as it is effective, efficient, and a time-saving process, represents one of the crucial factors impelling the market growth. Besides this, the rising construction of airports to increase the number of daily flights and connect various locations around the world is propelling the growth of the market. In addition, governing agencies of various countries are investing in strengthening their defense and military sectors by incorporating efficient fighter jets. Apart from this, the growing utilization of commercial drones for managing traffic, taking photographs, and surveillance purposes is offering a favorable market outlook. Additionally, the increasing popularity of 3D printing, as it offers opportunities to customize prototypes and produce components at cheaper prices, is supporting the growth of the market.

Aerospace 3D Printing Market Trends/Drivers:

Rising demand for light-weight aircraft components positively influencing demand for aerospace 3D printing

There is an increase in the production of light-weight aircraft components as they help enhance the efficiency of an aircraft. They also contribute to the green aviation concept, which is programmed to reduce aviation emissions causing global warming and imparting various other negative impacts on the environment. Light-weight aircraft components are manufactured by aerospace 3D printing, which assists in reducing the overall mass, increasing energy efficiency, and reducing fuel consumption rates of aircraft or planes. Furthermore, as they minimize the carbon footprint, provide higher structural strength to airplanes, and offer better safety performance, their demand is increasing in the aerospace industry.

Increasing utilization of composite materials impelling market growth

Composite materials are substances formed by combining two or more components with different properties without dissolving or blending them into each other. They comprise carbon fiber, aramid-reinforced epoxy, polyamide, and polypropylene. They are widely employed in the aerospace industry to manufacture various aircraft and spacecraft components via aerospace 3D printing. They help in reducing the overall weight of various aircraft parts, providing efficient tensile strength, and enhancing the performance of aircraft and spacecraft. They are primarily employed in 3D printing technology to boost specific properties of the printed components, such as stiffness, heat resistance, and durability. Furthermore, as composite materials decrease thermal expansion coefficients by increasing particle content, their demand is increasing for aerospace 3D printing purposes.

Rising automation of manufacturing processes augmenting market growth

At present, there is an increase in the automation of manufacturing processes, as it saves time and prevents the occurrence of unnecessary errors. Companies are transforming their conventional manufacturing processes into automated manufacturing processes to conduct the entire procedure with the help of software instead of employing people to do the job. Similarly, aerospace companies are investing in aerospace 3D printing, which is an additive process used for producing various light-weight and durable parts of aircraft and spacecraft. Aerospace 3D printing is an automated process where the 3D printer is managed by computer-aided design (CAD) software to create three-dimensional parts spontaneously.

Aerospace 3D Printing Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global aerospace 3D printing market report, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on offerings, printing technology, platform, application, and end use.

Breakup by Offerings:

- Materials

- Printers

- Software

- Services

Printers hold the largest market share

The report has provided a detailed breakup and analysis of the aerospace 3D printing market based on the offerings. This includes materials, printers, software, and services. According to the report, printers represented the largest segment. Printers used for aerospace 3D printing are primarily 3D printers that print three-dimensional aircraft structures layer by layer. They are capable of manufacturing complex feature components with high stability and enhanced performance. They are used to print jet engine parts, wing brackets, fuel chambers, and interiors of aircraft and spacecraft.

Materials utilized in aerospace 3D printing comprise metals, including titanium, aluminum, steel, and nickel-based alloys. They also include thermoplastics, such as polycarbonate (PC), acrylonitrile butadiene styrene, nylon/polyamide, fiber, and continuous fiber-reinforced thermoplastic composites, that offer superior fatigue resistance, chemical resistance, and tensile strength.

Aerospace 3D printing relies on computer-aided design (CAD) software to manufacture three-dimensional object models in precise shapes and sizes. They provide instructions needed to build a prototype or product by depositing accurate amounts of materials onto a substrate known as a print bed.

Breakup by Printing Technology:

- Direct Metal Laser Sintering (DMLS)

- Fused Deposition Modeling (FDM)

- Continuous Liquid Interface Production (CLIP)

- Selective Laser Melting (SLM)

- Selective Laser Sintering (SLS)

- Others

Fused deposition modeling (FDM) represents the commonly used printing technology in aerospace 3D printing

The report has provided a detailed breakup and analysis of the aerospace 3D printing market based on printing technology. This includes direct metal laser sintering (DMLS), fused deposition modeling (FDM), continuous liquid interface production (CLIP), selective laser melting (SLM), selective laser sintering (SLS), and others. According to the report, fused deposition modeling (FDM) represented the largest segment. Fused deposition modeling (FDM) refers to a 3D printing technology that creates parts from plastic filaments by melting them and depositing them in layers. It creates parts by precisely depositing melted material layer-by-layer in a path defined by the CAD model.

Direct metal laser sintering (DMLS) is an industrial metal 3D printing procedure that builds fully functional metal prototypes and production parts in seven days or less. It uses a carbon dioxide laser with high power for sintering the metallic powder material required for prototyping.

Continuous liquid interface production (CLIP) refers to a proprietary 3D printing method that falls under the general process of vat polymerization and shares many similarities with stereolithography (SLA) and digital light processing (DLP) printing. It functions by selectively exposing a liquid photopolymer resin to an ultraviolet (UV) light source and solidifying it into parts.

Selective laser melting (SLM) uses a high power-density laser to entirely melt and fuse metallic powders to create net-shape parts with near full density.

Breakup by Platform:

- Aircraft

- Unmanned Ariel Vehicles (UAV)

- Spacecraft

Aircraft dominates the market

The report has provided a detailed breakup and analysis of the aerospace 3D printing market based on the platform. This includes aircraft, unmanned ariel vehicles (UAV), and spacecraft. According to the report, aircraft represented the largest segment. Aerospace 3D printing is widely utilized in producing aircraft components, as it facilitates faster manufacturing without causing errors in the process. It also enables manufacturers to create aircraft parts and prototypes at cheaper costs and make numerous customizations according to their requirements.

Aerospace 3D printing is employed for the manufacturing of various integral components of unmanned aerial vehicles (UAVs), which are used for surveillance purposes. It also reduces the weight and slash material utilized in solid drone components and provides abundant opportunities to customize the prototype.

Spacecrafts are also manufactured by aerospace 3D printing, as it offers decisive advantages. It also helps in completely reimagining and reinventing various parts of a spacecraft.

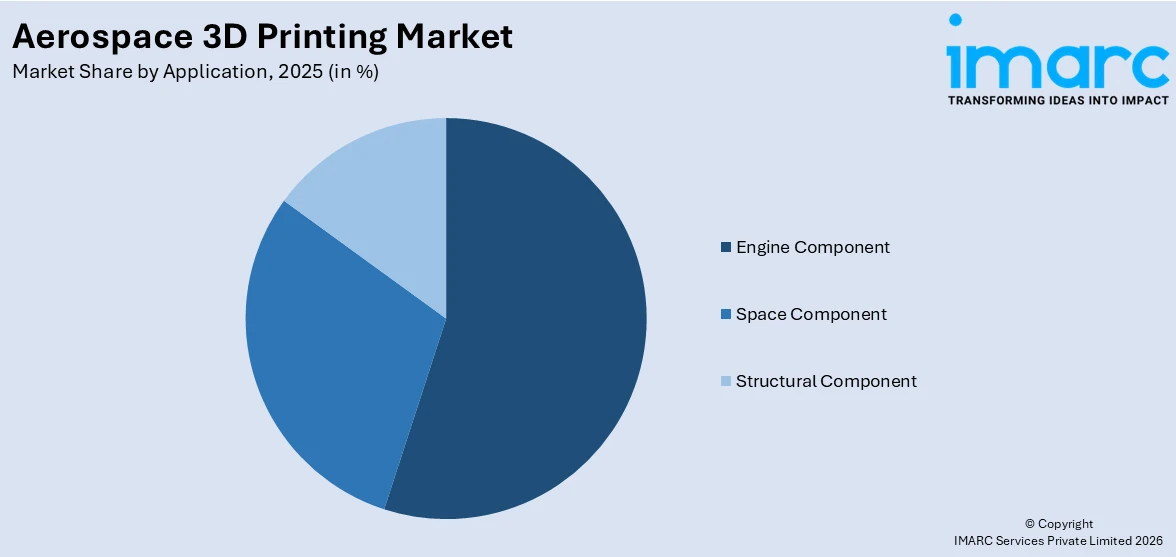

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Engine Component

- Space Component

- Structural Component

Engine component holds the majority of the share

The report has provided a detailed breakup and analysis of the aerospace 3D printing market based on the application. This includes the engine component, space component, and structural component. According to the report, engine component represented the largest segment as it does not require molds or tools and can create part prototypes faster and at lower prices. It effectively accelerates the designing and development process of engine components. Furthermore, it helps in optimizing the functions and increasing fuel efficiency in engines.

Aerospace 3D printing is adopted for the manufacturing of various space components, as it provides manufacturers complete flexibility for prototyping aerospace components.

Structural components are manufactured with the help of aerospace 3D printing as it provides complete flexibility to manufacturers for prototyping various structural parts. Aerospace 3D printing also assists in reducing wastage of raw materials and manufactures light-weight designs of structural components.

Breakup by End Use:

- OEM

- MRO

Aerospace 3D printing is widely utilized in MRO

The report has provided a detailed breakup and analysis of the aerospace 3D printing market based on the end use. This includes OEM and MRO. According to the report, MRO represented the largest segment as it is required for smoothly running the facilities and the production process of a manufacturing company.

Original equipment manufacturer (OEM) refers to various companies that specialize in manufacturing components by employing aerospace 3D printing and providing them to other companies who customize the components and incorporate them into their product models. OEMs sell various parts in bulk to organizations that do not own their manufacturing plant yet specialize in assembling the individually bought components and selling their own products.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest aerospace 3D printing market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa.

North America held the biggest market share due to the presence of manufacturing units of various leading aerospace companies in the region. Additionally, the growing investment in space exploration programs, rising production of light-weight modern aircraft parts, and increasing air travel activities are further propelling the growth of the aerospace 3D printing market in the region.

Asia Pacific is estimated to expand further in this domain during the forecast period due to the growing construction of airports, along with rising investments in strengthening the military and defense sector. Apart from this, the increasing utilization of commercial drones for surveillance purposes is bolstering the growth of the market.

Competitive Landscape:

Key players are experiencing a rise in demand for aerospace 3D printing due to the growing production of light-weight aircraft and spacecraft components, along with the increasing automation of manufacturing processes. They are focusing on expanding their additive manufacturing capabilities to seize the opportunities. Leading companies are shifting to 3D printing techniques by eliminating subtractive manufacturing methods in the space sector. They are also planning on improve their manufacturing, designing, and processing technologies to enhance their product quality. Top manufacturers are investing in research activities and focusing on collaborations and mergers with other enterprises to increase their production facilities and sales.

The report has provided a comprehensive analysis of the competitive landscape in the global aerospace 3D printing market. Detailed profiles of all major companies have also been provided. Some of the key players in the global aerospace 3D printing market include:

- 3D Systems Inc.

- EOS GmbH

- General Electric Company

- Hoganas AB

- Markforged

- Materialise NV

- Proto Labs

- SLM Solutions Group AG (Nikon AM. AG)

- Stratasys Ltd.

- The ExOne Company (Desktop Metal)

- VoxelJet AG

Recent Developments:

- In June 2023, 3D Systems Inc. submitted an enhanced proposal to combine with Stratasys and create an additive manufacturing industry leader with an unmatched scale and extremely attractive financial profile.

- In May 2023, EOS GmbH and nTopology announced their plan to proceed with the development of a new implicit interop capability, solving a serious bottleneck in the additive manufacturing (AM) workflow.

- In September 2021, VoxelJet AG, GE Renewable Energy, and Fruanhofer IGCV announced a research partnership to develop the largest 3D printer in the world for offshore wind applications to manage the production of key components of the Halidae-X offshore wind turbine.

Aerospace 3D Printing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Offerings Covered | Materials, Printers, Software, Services |

| Printing Technologies Covered | Direct Metal Laser Sintering (DMLS), Fused Deposition Modeling (FDM), Continuous Liquid Interface Production (CLIP), Selective Laser Melting (SLM), Selective Laser Sintering (SLS), Others |

| Platforms Covered | Aircraft, Unmanned Ariel Vehicles (UAV), Spacecraft |

| Applications Covered | Engine Component, Space Component, Structural Component |

| End Uses Covered | OEM, MRO |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | 3D Systems Inc., EOS GmbH, General Electric Company, Hoganas AB, Markforged, Materialise NV, Proto Labs, SLM Solutions Group AG (Nikon AM. AG), Stratasys Ltd., The ExOne Company (Desktop Metal), VoxelJet AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global aerospace 3D printing market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global aerospace 3D printing market?

- What is the impact of each driver, restraint, and opportunity on the global aerospace 3D printing market?

- What are the key regional markets?

- Which countries represent the most attractive aerospace 3D printing market?

- What is the breakup of the market based on the offerings?

- Which are the most attractive offerings in the aerospace 3D printing market?

- What is the breakup of the market based on the technology?

- Which is the most attractive technology in the aerospace 3D printing market?

- What is the breakup of the market based on the platform?

- Which is the most attractive platform in the aerospace 3D printing market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the aerospace 3D printing market?

- What is the breakup of the market based on the end use?

- Which is the most attractive end use in the aerospace 3D printing market?

- What is the competitive structure of the global aerospace 3D printing market?

- Who are the key players/companies in the global aerospace 3D printing market?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aerospace 3D printing market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global aerospace 3D printing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aerospace 3D printing industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)