Aerospace Fasteners Market Size, Share, Trends and Forecast by Product Type, Material Type, Application, Aircraft Type, End-Use Sector, and Region 2026-2034

Global Aerospace Fasteners Market Size, Share, Trends & Forecast (2026-2034)

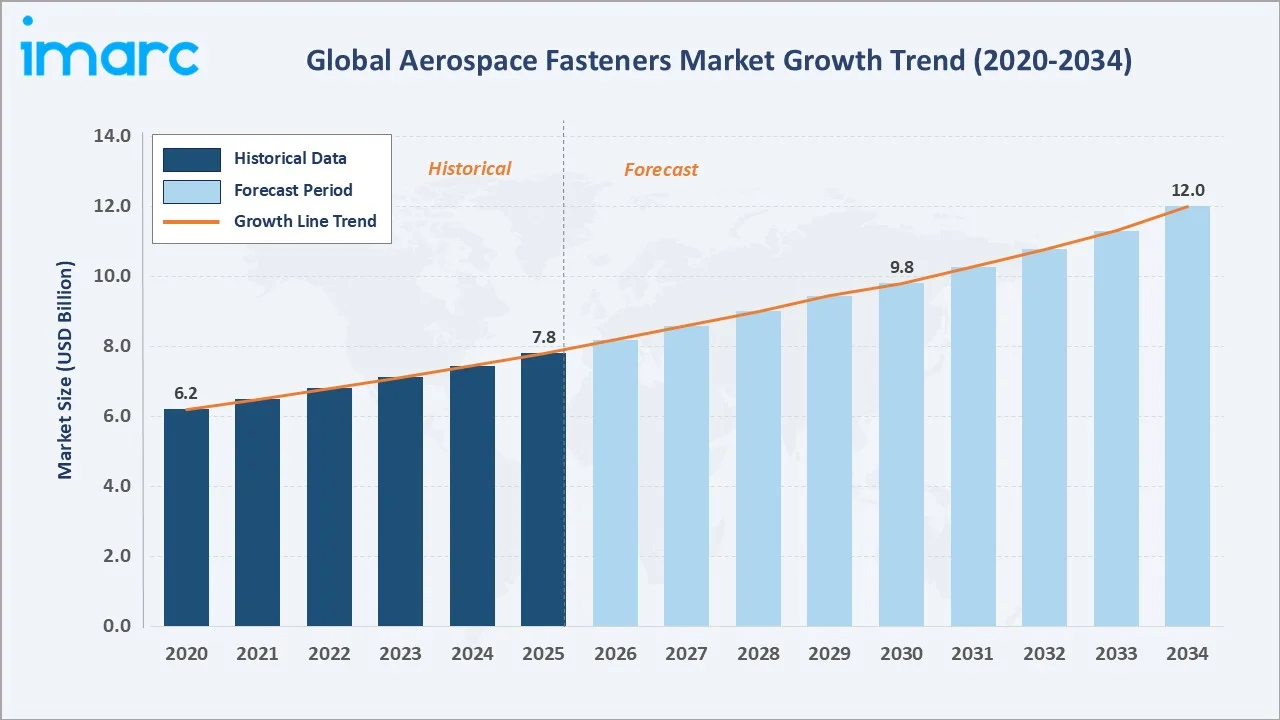

The global aerospace fasteners market reached USD 7.8 Billion in 2025, projected to reach USD 12.0 Billion by 2034 at a 4.70% CAGR .2026-2034 Commercial aviation expansion, defense budgets, and titanium adoption drive growth.

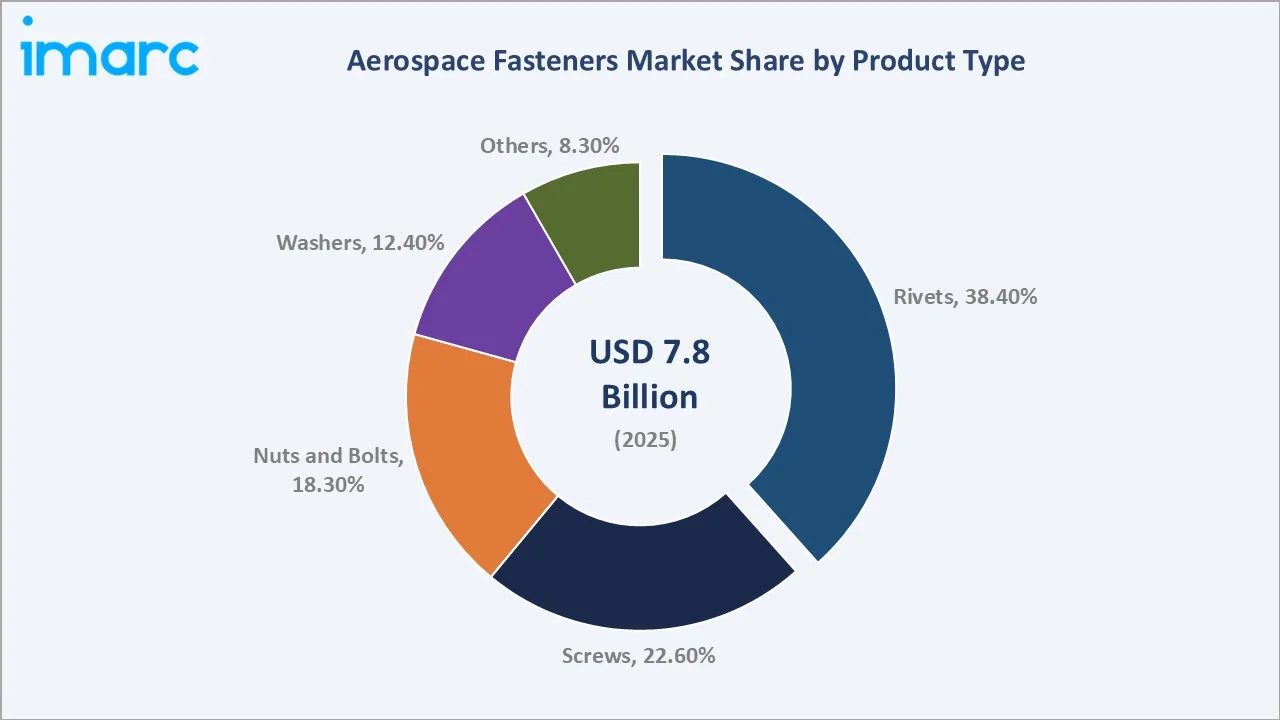

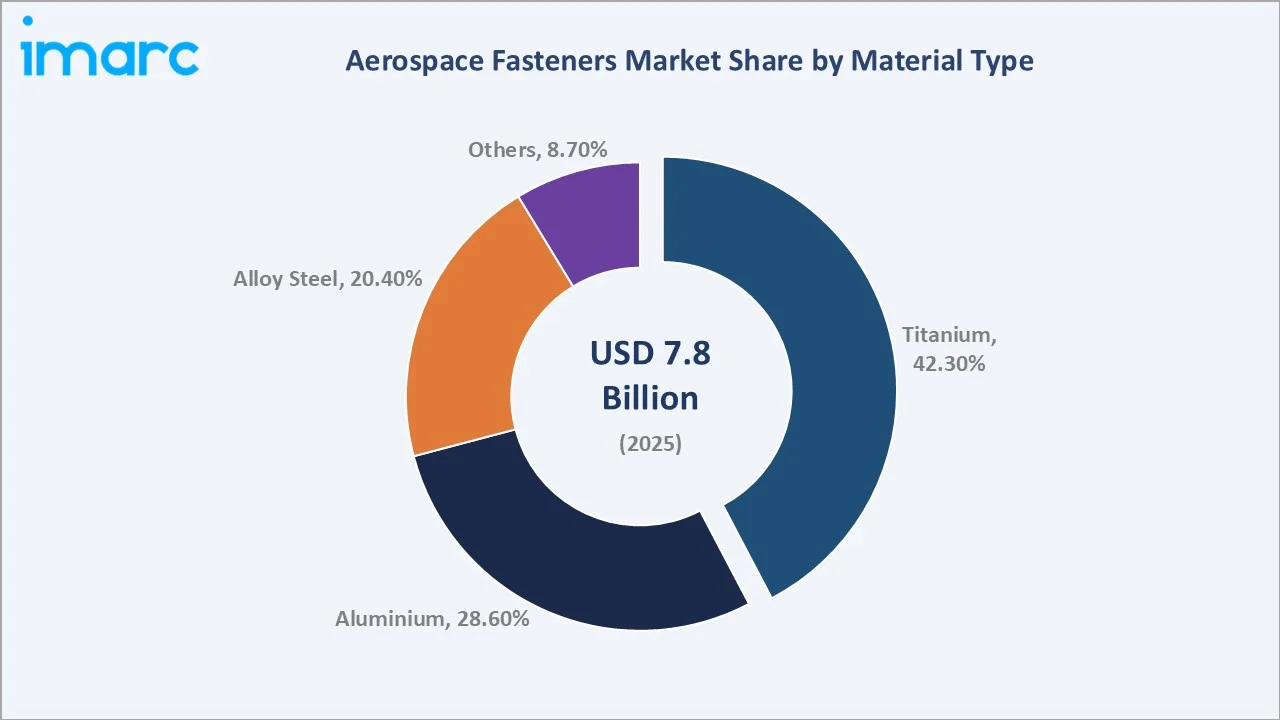

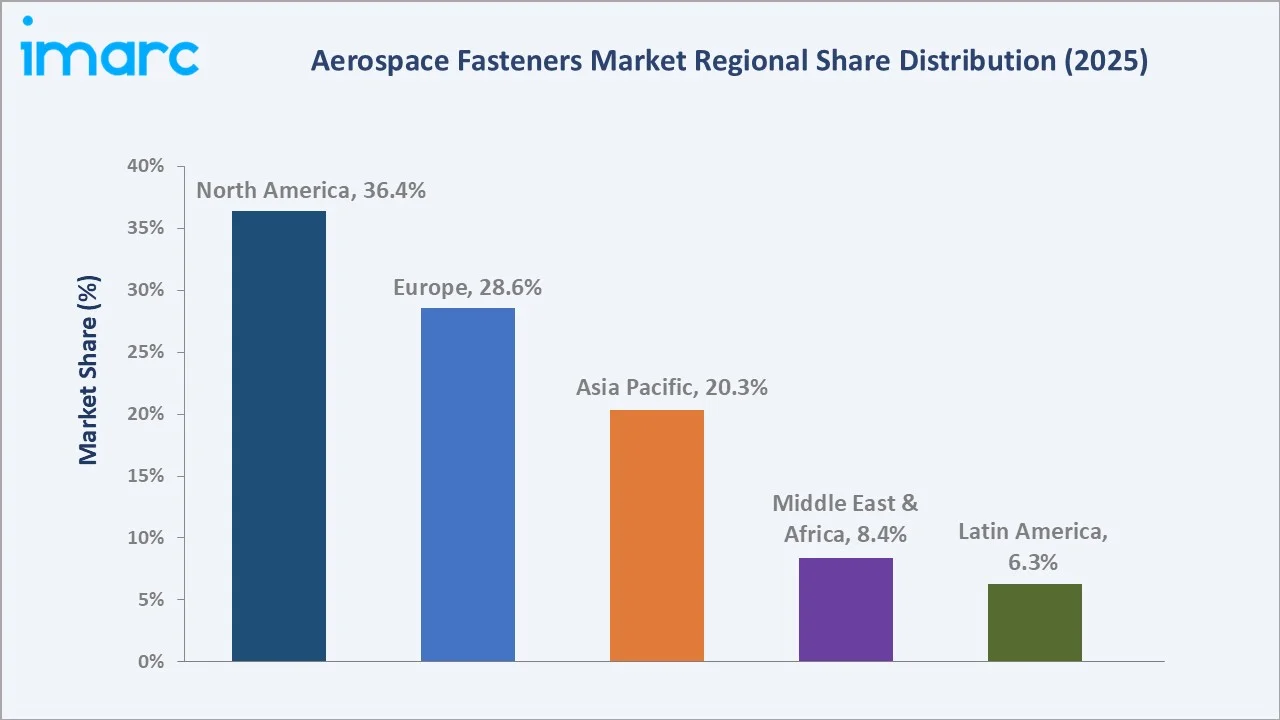

Rivets lead at 38.4%, titanium at 42.3%, and North America commands 36.4% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 7.8 Billion |

|

Forecast Market Size (2034) |

USD 12.0 Billion |

|

CAGR (2026-2034) |

4.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.4% share, 2025) |

| Second Region |

Europe (28.6% share, 2025) |

| Leading Product Type |

Rivets (38.4%, 2025) |

| Leading Material Type |

Titanium (42.3%, 2025) |

To get more information on this market, Request Sample

The market growth trajectory from 2020 through 2034, with historical expansion to USD 7.8 Billion in 2025, reflects aviation-driven demand recovery post-COVID, while the forecast to USD 12.0 Billion in 2034 captures accelerating defense modernization, sustainable aviation, and space exploration investment.

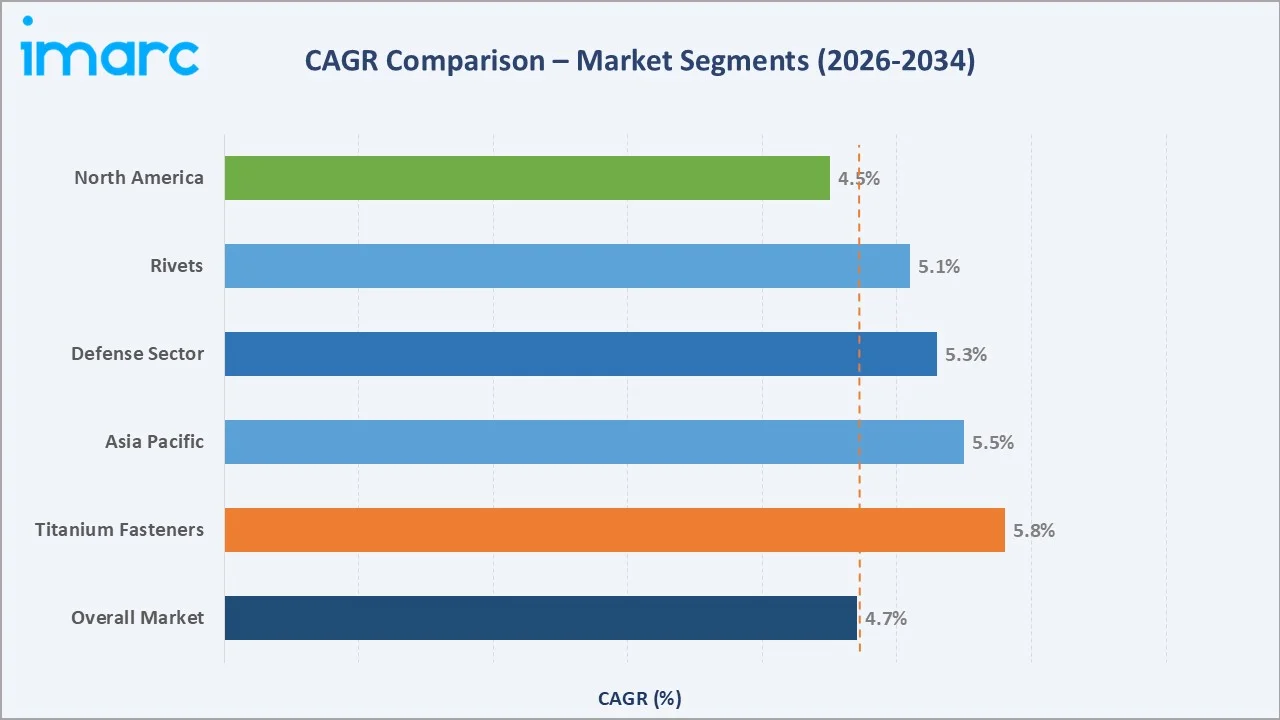

CAGR trajectories across key product, material, and regional sub-segments, with titanium fasteners at ~5.8% CAGR and the defense sector at ~5.3% CAGR, represent the fastest-growing categories within the global aerospace fasteners industry through 2034.

Executive Summary

The global aerospace fasteners market is on a sustained growth trajectory from USD 7.8 Billion in 2025 to USD 12.0 Billion by 2034. Aerospace fasteners are critical structural components deployed across fuselage assembly, control surfaces, engine nacelles, and interior structures, with non-discretionary demand driven by safety certification requirements.

Rivets dominate product type at 38.4% in 2025, owing to their proven performance in airframe assembly and high-volume production economics. Titanium commands 42.3% of material type in 2025, reflecting the aerospace industry's transition toward lightweight, high-strength materials that improve fuel efficiency while maintaining structural integrity under extreme operating conditions.

North America leads at 36.4% in 2025, anchored by Boeing and Lockheed Martin OEM procurement demand and a robust MRO market. Europe (28.6%) follows, driven by Airbus production and defense spending. Asia Pacific (20.3%) is the fastest-growing region, supported by fleet expansion in China, India, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

| Largest Product Type |

Rivets – 38.4% share (2025) |

| Leading Material Type |

Titanium – 42.3% share (2025) |

|

Leading Region |

North America – 36.4% revenue share (2025) |

| Second Region |

Europe – 28.6% revenue share (2025) |

|

Top Companies |

Howmet Aerospace, LISI Aerospace (LISI Group), Stanley Engineered Fastening, CDP Fastener Group, Inc., B&B Specialties, Inc., Aero |

Key Analytical Observations Expanding On The Above Data:

- Rivets at 38.4% in 2025 dominate because they are the fundamental joining technology for aluminium airframe structures. Their shear-load performance, installation speed, and compatibility with automated riveting systems make them the default specification across commercial aircraft fuselage and wing assembly globally.

- Titanium at 42.3% in 2025 leads material type because it delivers the highest strength-to-weight ratio among structural metals, a critical parameter for aerospace fasteners that directly impacts aircraft fuel efficiency. Ti-6Al-4V alloy fasteners are the standard specification for high-stress structural joints.

- North America's 36.4% dominance reflects the combined procurement demand from Boeing's commercial and defense platforms, Lockheed Martin and Northrop Grumman defense programs, and NASA space exploration, creating unparalleled fastener consumption density in a single region.

- Europe at 28.6% in 2025 benefits from Airbus's A320 and A350 production ramp-up, a robust defense industrial base across France, Germany, and the UK, and growing aftermarket demand from one of the world's largest commercial fleet operating regions.

Global Aerospace Fasteners Market Overview

Aerospace fasteners are precision-engineered mechanical joining elements manufactured to exacting aerospace standards including NAS, MS, AN, NASM, and SAE AS9100. Product types include rivets, screws, nuts, bolts, and washers produced from titanium, aluminium alloys, alloy steel, and superalloys to withstand extreme vibration, thermal cycling, and structural loading.

The global ecosystem integrates primary metal producers, forging and precision machining specialists, fastener fabricators, surface treatment providers, certified distribution networks, OEM manufacturers (Boeing, Airbus, Lockheed Martin), MRO operators, and diverse aerospace end-use platforms spanning commercial aviation, military aircraft, rotorcraft, and space launch systems.

Market Dynamics

To evaluate market opportunities, Request Sample

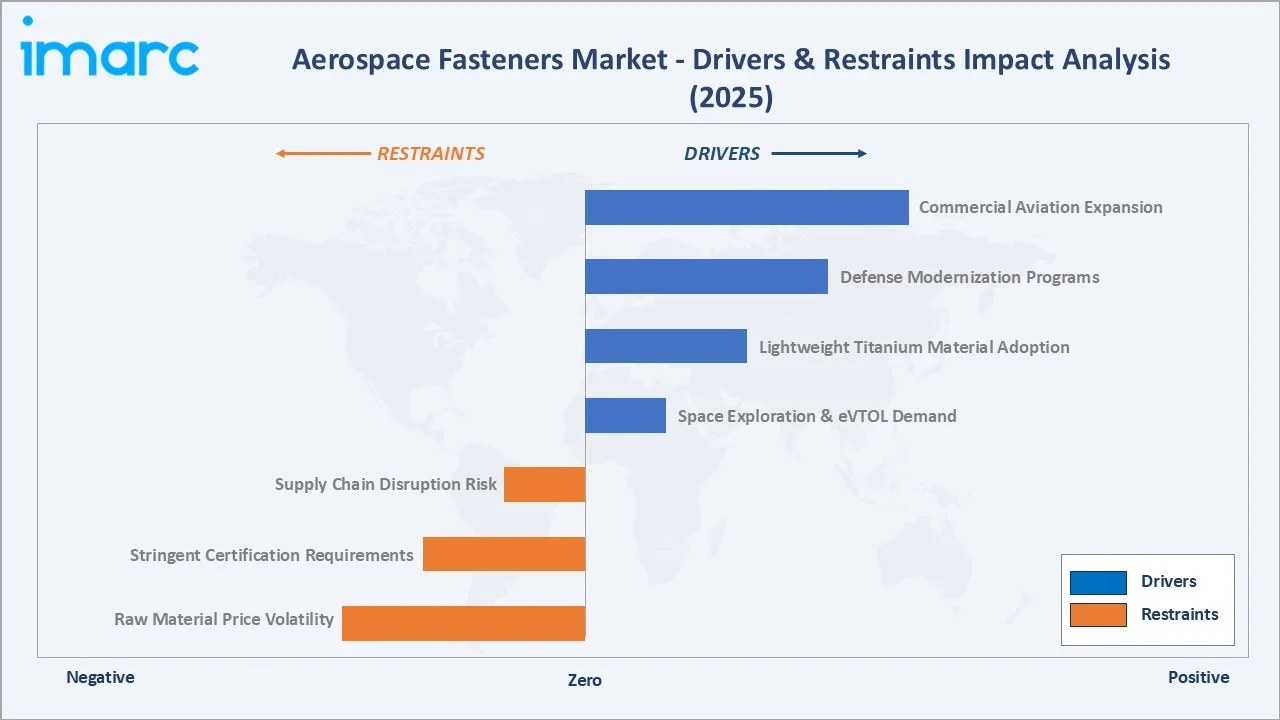

Market Drivers

- Commercial Aviation Expansion: IATA forecasts global air passenger traffic to reach 7.8 billion by 2036. New aircraft deliveries from Boeing and Airbus, with combined backlogs exceeding 12,000 aircraft, generate sustained multi-year fastener procurement demand per airframe.

- Defense Modernization Programs: Global defense spending surpassed USD 2.2 Trillion in 2023, with fighter jet, military transport, and rotorcraft procurement programs across NATO, Indo-Pacific, and Middle Eastern nations driving high-specification fastener demand.

- Lightweight Material Adoption: Increasing composite and titanium content in next-generation aircraft, with the Boeing 787 incorporating 50% composites by weight, necessitates specialized titanium and specialty alloy fasteners compatible with composite panel stress transfer characteristics.

Market Restraints

- Raw Material Price Volatility: Aerospace-grade titanium prices ranged between USD 15–30 per pound from 2024–2025, driven by Russia-Ukraine conflict supply disruptions and tightening export controls, creating input cost uncertainty for fastener manufacturers relying on titanium feedstock.

- Stringent Certification Requirements: AS9100 and NADCAP certification processes require substantial capital investment in testing, inspection, and quality management infrastructure. Recertification after process changes adds production lead time and limits manufacturing flexibility.

Market Opportunities

- Space Exploration and Commercial Launch Markets: The commercial space launch market, driven by SpaceX, Blue Origin, and global new-space entrants, generates demand for specialized fasteners rated for extreme thermal and vibration environments beyond traditional aerospace specifications.

- eVTOL and Advanced Air Mobility (AAM): The eVTOL market, with over 600 AAM concepts in development globally, requires miniaturized, lightweight fastening solutions for novel airframe configurations, representing a high-margin emerging segment for specialized fastener manufacturers.

Market Challenges

- Supply Chain Disruption Vulnerability: The COVID-19 pandemic exposed single-source supplier concentration risks in aerospace fastener supply chains. Titanium supply chain disruptions require OEMs to qualify alternative sources, a process requiring 12–18 months minimum.

- Counterfeit Fastener Risk: The aerospace industry continues to face challenges from counterfeit fasteners entering the supply chain, leading to significant financial losses and safety concerns. Regulatory bodies emphasize strict traceability, quality assurance, and proper material certification to ensure component reliability and compliance.

Emerging Market Trends

1. Additive Manufacturing and Digital Fastener Development

Metal additive manufacturing (AM) is enabling rapid prototyping of complex fastener geometries that are cost-prohibitive in conventional machining. AM-produced titanium fasteners with internal channels for weight reduction are entering qualification testing for advanced defense and space applications.

2. Automated Drilling and Fastening in Aircraft Assembly

Robotic automated fastening systems (RAFS) adopted by Boeing and Airbus reduce installation cycle times by 40–60% versus manual installation. These systems require highly consistent fastener dimensional tolerances, driving demand for precision-machined fasteners from certified suppliers.

3. Smart Fasteners and Structural Health Monitoring

Next-generation smart fasteners integrating embedded sensors for real-time load and fatigue monitoring are advancing from research to early qualification phases. These enable predictive maintenance models that reduce MRO downtime and improve structural airworthiness assurance.

4. Sustainable and Green Aviation Material Requirements

Sustainable Aviation Fuel (SAF) mandates and next-generation hydrogen-powered aircraft programs are influencing fastener material specifications. Hydrogen embrittlement resistance in fasteners for liquid hydrogen fuel systems is becoming a key R&D priority for specialty alloy manufacturers.

Industry Value Chain Analysis

The aerospace fasteners value chain spans six stages from raw metal input through end-use installation and MRO services. Precision machining and certification stages capture the highest value-add margins, while OEM qualification and distribution logistics generate significant working capital requirements favoring well-capitalized integrated manufacturers.

|

Stage |

Key Players / Examples |

| Raw Material Supply | ATI Inc., Carpenter Technology |

| Precision Machining & Forming | PennAero |

| Surface Treatment & Coating | Cadmium plating specialists, anodizing providers, PTFE coating facilities |

| Quality Testing & Certification | NADCAP accredited labs; AS9100 certified quality management systems |

| Distribution & Stocking | Boeing Distribution Services, Inc., regional aerospace distributors |

| End-Use & MRO Services | Commercial airlines, defense MROs, space launch providers, rotorcraft OEMs |

Integrated fastener manufacturers controlling titanium alloy sourcing through to certified distribution, such as Arconic with its alloy processing and precision machining operations, achieve defensible cost positions versus processors relying entirely on spot market procurement.

Technology Landscape in the Aerospace Fasteners Industry

Titanium Alloy Processing and Cold Heading Technology

Cold heading of titanium alloy rod stock into fastener blanks requires specialized tooling capable of withstanding titanium's high work-hardening rate. Advances in carbide die technology and lubrication systems have reduced heading tool replacement frequency by 30–40%, improving production economics for high-volume titanium fastener manufacturing.

Precision CNC Machining and Thread Rolling

Modern aerospace fastener machining uses multi-axis CNC turning centers with in-process gauging achieving dimensional tolerances of ±0.0005 inches. Thread rolling, preferred over thread cutting for fatigue-critical fasteners, induces compressive surface residual stress that improves fatigue life by 20–30% compared to cut threads.

Surface Treatment: Cadmium Replacement and Dry Film Lubrication

Environmental regulations are accelerating the transition from traditional cadmium plating to alternative coatings including zinc-nickel alloy plating, aluminium-rich organic coatings, and ionic liquid deposition systems. These alternatives maintain corrosion performance while eliminating hazardous cadmium waste streams in fastener manufacturing operations.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Rivets | 38.4% | 2025 |

| Material Type | Titanium | 42.3% | 2025 |

| Application | Fuselage | 🔒 | 2025 |

| Aircraft Type | Wide Body Aircraft | 🔒 | 2025 |

| End-Use Sector | Commercial | 🔒 | 2025 |

| Region | North America | 36.4% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Rivets command a 38.4% majority share in 2025 owing to their fundamental role in aluminium alloy airframe assembly. Their single-sided installation capability, high shear strength, and compatibility with automated fastening systems make them the default specification for commercial aircraft fuselage skin panels, floor beams, and structural frame assembly.

Screws at 22.6% in 2025 serve critical joining functions across interior cabin, avionics bay, and access panel applications where removability is required for maintenance access. Nuts and Bolts (18.3%) dominate structural joining in high-load primary structure applications including engine pylon attachment and landing gear structural interfaces.

Washers at 12.4% in 2025 serve as load distribution elements under bolt and nut heads, preventing surface damage to composite panels and ensuring consistent clamp load distribution in metallic joints.

By Material Type

Titanium commands a 42.3% dominant share in 2025, driven by the widespread adoption of Ti-6Al-4V (Grade 5) alloy as the industry standard for high-strength structural fasteners. Its superior strength-to-weight ratio, excellent corrosion resistance, and biocompatibility with composite panel surfaces make it the preferred material for primary structure applications.

Aluminium at 28.6% serves weight-critical interior and secondary structure applications. Alloy Steel (20.4%) delivers the highest tensile strength for landing gear and engine mounts.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

| North America |

36.4% |

Boeing & Lockheed Martin OEM demand; US defense budgets; NASA space programs; commercial MRO |

| Europe |

28.6% |

Airbus production ramp-up; NATO defense spending; offshore wind UAV programs |

| Asia Pacific |

20.3% |

Fleet expansion in China, India; ASEAN aviation growth; domestic defense manufacturing |

| Middle East & Africa |

8.4% |

GCC airline fleet growth; Vision 2030 aviation investment; African mining aviation |

| Latin America |

6.3% |

LATAM Airlines fleet renewal; Brazil Embraer supply chain; regional aviation growth |

North America's 36.4% market dominance in 2025 is anchored by the world's largest and most technologically advanced aerospace industrial base. The US Department of Defense's USD 842 Billion FY2024 budget sustains continuous military aircraft procurement and MRO demand for precision fasteners across all platform categories.

Europe at 28.6% in 2025is primarily driven by Airbus's record order backlog exceeding 8,600 aircraft as of 2024 and the production ramp-up of A320neo and A350 families. Defense aerospace investment across France, Germany, Italy, and the UK adds structural demand from Eurofighter, FCAS, and MGCS next-generation combat aircraft programs.

Competitive Landscape

The global aerospace fasteners market is moderately fragmented, with regional leaders holding strong positions anchored by AS9100 and NADCAP certifications that create meaningful barriers to entry. North American and European markets are served by well-established specialized fastener companies, while Asia Pacific is developing domestic manufacturing capability.

|

Company Name |

Key Products |

Market Position |

Global Strategic Focus |

| Howmet Aerospace | Bolts, Screws, Inserts & Studs, Nuts |

Leader |

Global OEM-direct; titanium & specialty alloy; commercial and defense |

| LISI Aerospace (LISI Group) |

Screws, Bolts, Nuts, Fasteners |

Leader |

Europe & global; widest product range; aerospace structural joining |

| Stanley Engineered Fastening | POP, Nelson, Optia, Tucker |

Challenger |

North America & Europe; blind fastener systems; interior & secondary structure |

| CDP Fastener Group, Inc. | Bolts, Nuts, Screws, Rivets |

Challenger |

North America (US) distributor; mil-spec & commercial fasteners; aerospace, defense & industrial supply chain |

| B&B Specialties, Inc. | SHCS (Socket Head Cap Screw) - series NAS1351 & NAS1352, 6AL-4V Titanium, MP35N, 718 Inconel | Emerging | US manufacturer; NAS-spec socket head cap screws; titanium & superalloy aerospace fasteners |

| Aero | Aerospace Fasteners | Emerging | US East Coast; specialty and obsolete parts; defense MRO support |

Key players include Howmet Aerospace, LISI Aerospace (LISI Group), Stanley Engineered Fastening, CDP Fastener Group, Inc., B&B Specialties, Inc., Aero, and others.

Key Company Profiles

Howmet Aerospace

Howmet Aerospace Inc. is a leading global provider of advanced engineered solutions headquartered in Pittsburgh, Pennsylvania. Its Fastening Systems division is one of the world's largest manufacturers of aerospace fasteners, producing structural blind fasteners, lockbolts, self-locking nuts, and quick-release panel fasteners under widely certified brand families. The company serves all major commercial and defense OEMs globally from manufacturing facilities across the US, UK, France, and Asia Pacific.

- Product Portfolio: The company offers Bolts, Screws, Inserts & Studs, Nuts

- Recent Developments: In February 2020, Arconic Inc. announced that its Board of Directors approved the separation of the company into two independent, publicly traded entities, with the transition scheduled for April 1, 2020. Under this restructuring, the engineered products and forgings businesses—focused on aerospace components and fastening systems—would remain with the existing entity, which would be renamed Howmet Aerospace Inc. Meanwhile, the rolled aluminum products and construction-related operations would form a new company, Arconic Corporation, listed separately on the New York Stock Exchange.

- Strategic Focus: Howmet Aerospace's strategy centers on building a differentiated, mission-critical fastener portfolio through organic investment and targeted M&A — most notably the CAM acquisition, which broadens its offering across precision fasteners, fluid fittings, and engineered components.

LISI Aerospace (LISI Group)

LISI Aerospace, a division of French industrial group LISI, is Europe's leading aerospace fastener manufacturer with operations across France, Germany, UK, USA, and Morocco. The company produces the broadest aerospace fastener product range in Europe, supplying Airbus, Safran, MTU, and Leonardo as primary OEM customers.

- Product Portfolio: The company offers screws, bolts, nuts, fasteners, and others.

- Recent Developments: In January 2021, LISI Aerospace extended its long-term agreement with Boeing to continue supplying a wide range of components for commercial aircraft programs. Under the renewed contract, LISI Aerospace will provide approximately 6,000 different part numbers supporting Boeing’s major aircraft platforms, including the 737, 747, 767, 777, and 787 programs.

- Strategic Focus: LISI Aerospace differentiates through European OEM proximity, comprehensive product range depth, and investment in titanium alloy fastener capabilities aligned with Airbus's increasing composite content and titanium structural requirement trends across its commercial aircraft families.

Stanley Engineered Fastening

Stanley Engineered Fastening, a division of Stanley Black & Decker (NYSE: SWK), is a global leader in precision blind fastening and assembly solutions with an aerospace heritage.

- Product Portfolio: POP, Nelson, Optia, Tucker, and others

- Recent Developments: In December 2025, Stanley Black & Decker entered into an agreement to sell its Consolidated Aerospace Manufacturing (CAM) business to Howmet Aerospace for approximately $1.8 billion in an all-cash transaction, and closed the deal in April 2026. CAM specializes in producing critical aerospace components, including precision fasteners, fittings, and other engineered parts used in both commercial and defense applications.

- Strategic Focus: Stanley Engineered Fastening's aerospace strategy concentrates on its differentiated multi-material blind fastening portfolio, which are uniquely suited to the growing adoption of composite and mixed-material airframe structures in next-generation commercial and defense aircraft. The division targets productivity and total cost of ownership improvements for OEM assembly lines through automated fastening system integration, with Avdel automated speed fastening platforms reducing installation cycle times and FOD risk in high-rate aircraft production environments.

Market Concentration Analysis

The global aerospace fasteners market is moderately fragmented, with no single company holding more than 8–10% of global revenue. North America (36.4%) is served by Arconic, TriMas, and Wesco-distributed supply chains, while European and Asia Pacific markets maintain distinct competitive ecosystems.

Consolidation at the certification tier is more pronounced than global share suggests. NADCAP and AS9100 certifications require 12–18 months of OEM qualification, creating defensible positions. M&A activity is accelerating as industrial conglomerates acquire specialty fastener manufacturers to add certified aerospace capabilities.

Investment & Growth Opportunities

Fastest-Growing Segments

Titanium fasteners at ~5.8% CAGR through 2034 are the highest-growth material segment, driven by composite aircraft structure expansion and commercial aviation fleet renewal. The defense sector at ~5.3% CAGR represents robust, budget-supported procurement growth through the decade.

Emerging Markets

Asia Pacific at ~5.5% CAGR is the fastest-growing region for aerospace fasteners through 2034. China's COMAC C919 program, India's HAL Tejas Mk2 and private MRO sector expansion, and ASEAN airline fleet additions create large-scale fastener demand from a region building domestic manufacturing capability with limited current supply sources.

Venture & Investment Trends

Private equity interest in aerospace fastener distribution consolidation is growing. Smart fastener startups attracting venture capital for sensor-embedded structural monitoring represent an emerging investment theme. Government-funded AM fastener research programs in the US, UK, and France are creating technology transfer pathways for manufacturers.

Future Market Outlook (2026-2034)

The global aerospace fasteners market is forecast to expand from USD 7.8 Billion in 2025 to USD 12.0 Billion by 2034 at a CAGR of 4.70%, adding USD 4.2 Billion in incremental annual value. This reflects OEM production-linked and MRO-driven demand with strong multi-year visibility.

Three forces will shape the industry through 2034: Advanced Air Mobility and eVTOL commercialization requiring novel fastener specifications; hydrogen aircraft programs demanding embrittlement-resistant fasteners; and space launch market growth needing cryogenic-rated precision fastener solutions.

Research Methodology

Primary Research

Primary research encompassed over 45 structured interviews in 2024–2025 with aerospace fasteners industry stakeholders, including OEM procurement specialists, Tier 1 aerostructure suppliers, MRO procurement managers, fastener manufacturer executives, and aerospace industry trade association representatives. Primary data validated market sizing, segment shares, and technology adoption timelines.

Secondary Research

Key secondary sources include FAA Aerospace Forecast (2024–2044), IATA Economic Performance data, Boeing Commercial Market Outlook, Airbus Global Market Forecast, US DoD Budget Justification documents, NASM standards publications, AS9100 standard bodies, SAE International aerospace materials standards, and trade publications including Aviation Week, Aerospace Manufacturing, and AIN publications.

Forecasting Models

Market projections used top-down and bottom-up forecasting models incorporating aircraft production rate forecasts, defense budget trajectories, MRO spending models, and historical fastener content-per-aircraft data. Scenario analysis across base, optimistic, and conservative cases addressed macroeconomic uncertainty.

Aerospace Fasteners Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Rivets, Screws, Nuts and Bolts, Washers, Others |

| Material Types Covered | Aluminium, Alloy Steel, Titanium, Others |

| Applications Covered | Interior, Control Surfaces, Fuselage |

| Aircraft Types Covered | Narrow Body Aircraft, Wide Body Aircraft, Very Large Aircraft, Fighter Jet, Others |

| End-Use Sectors Covered | Commercial, Defense, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered |

Howmet Aerospace, LISI Aerospace (LISI Group), Stanley Engineered Fastening, CDP Fastener Group Inc., B&B Specialties Inc., Aero, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aerospace fasteners market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global aerospace fasteners market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aerospace fasteners industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Aerospace Fasteners Market Report

The global aerospace fasteners market reached USD 7.8 Billion in 2025, reflecting strong demand from commercial aviation recovery, rising defense procurement, and growing space exploration investment globally.

The market is projected to reach USD 12.0 Billion by 2034, growing at a CAGR of 4.70% during 2026-2034, driven by commercial aviation fleet expansion, defense modernization, and emerging eVTOL aircraft platform development.

Rivets lead with a 38.4% product type share in 2025, valued for their structural performance in aluminum airframe assembly, compatibility with automated fastening systems, and proven certification history across commercial aircraft programs globally.

Titanium dominates at 42.3% in 2025, representing the aerospace industry's preferred structural fastener material due to its superior strength-to-weight ratio, corrosion resistance, and composite panel compatibility, driving specification preference across both commercial and defense platforms.

North America commands the leading 36.4% market share in 2025, anchored by Boeing and Lockheed Martin OEM production demand, the US DoD's substantial defense procurement budget, and one of the world's largest commercial aviation MRO markets.

Leading companies include Howmet Aerospace, LISI Aerospace (LISI Group), Stanley Engineered Fastening, CDP Fastener Group, Inc., B&B Specialties, Inc., Aero, and others.

Titanium fasteners are the fastest-growing material segment at ~5.8% CAGR through 2034, driven by increasing composite airframe content, next-generation aircraft structural requirements, and defense platform modernization programs preferring titanium for weight reduction.

Primary applications include airframe fuselage and wing panel assembly, engine nacelle structural joining, control surface attachment, interior cabin and avionics installations, landing gear structural interfaces, and space launch vehicle structural assembly across commercial, defense, and space platforms.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)