Agricultural Haying and Forage Machinery Market Size, Share, Trends and Forecast by Machinery Type, Sales Channel, and Region 2026-2034

Agricultural Haying and Forage Machinery Market Size, Share, Trends & Forecast (2026-2034)

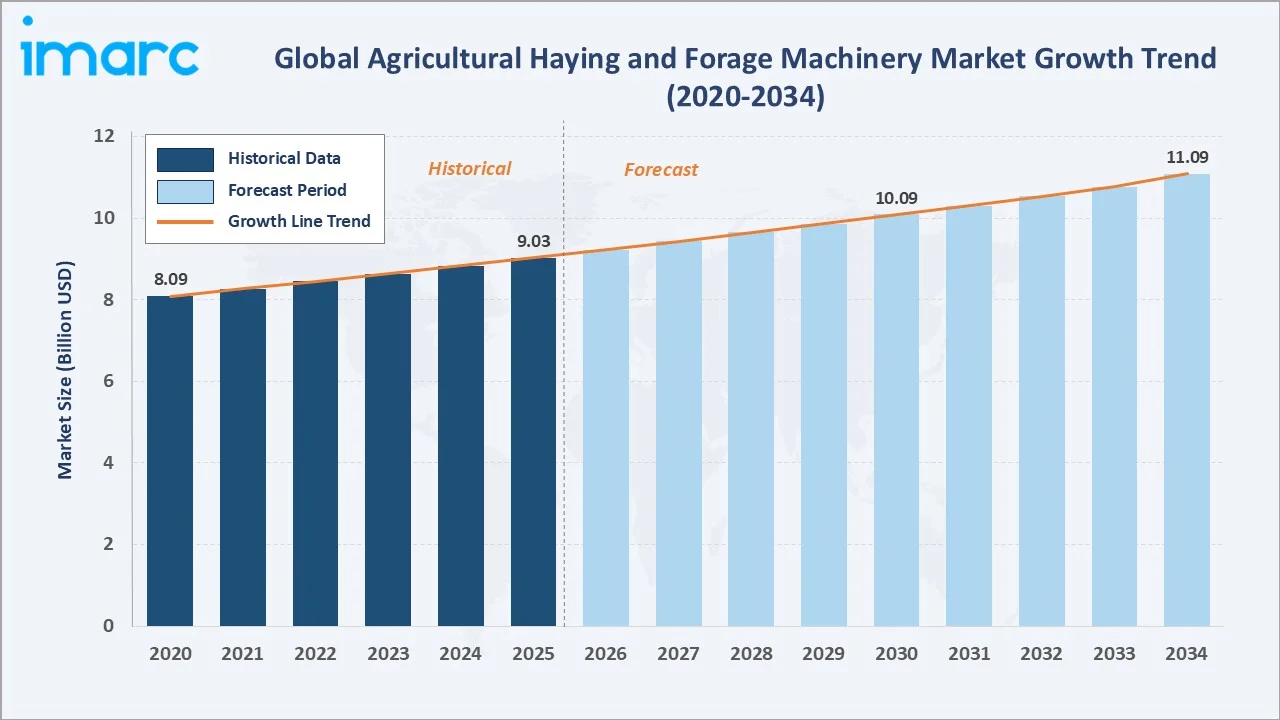

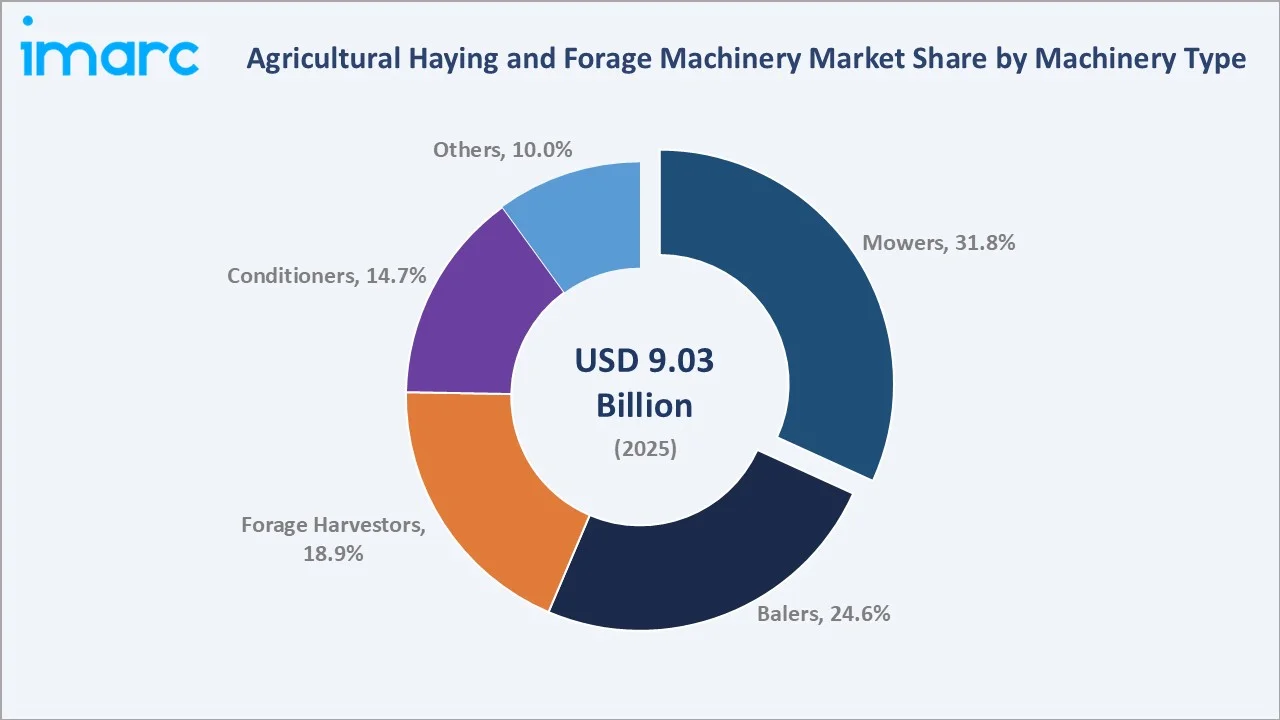

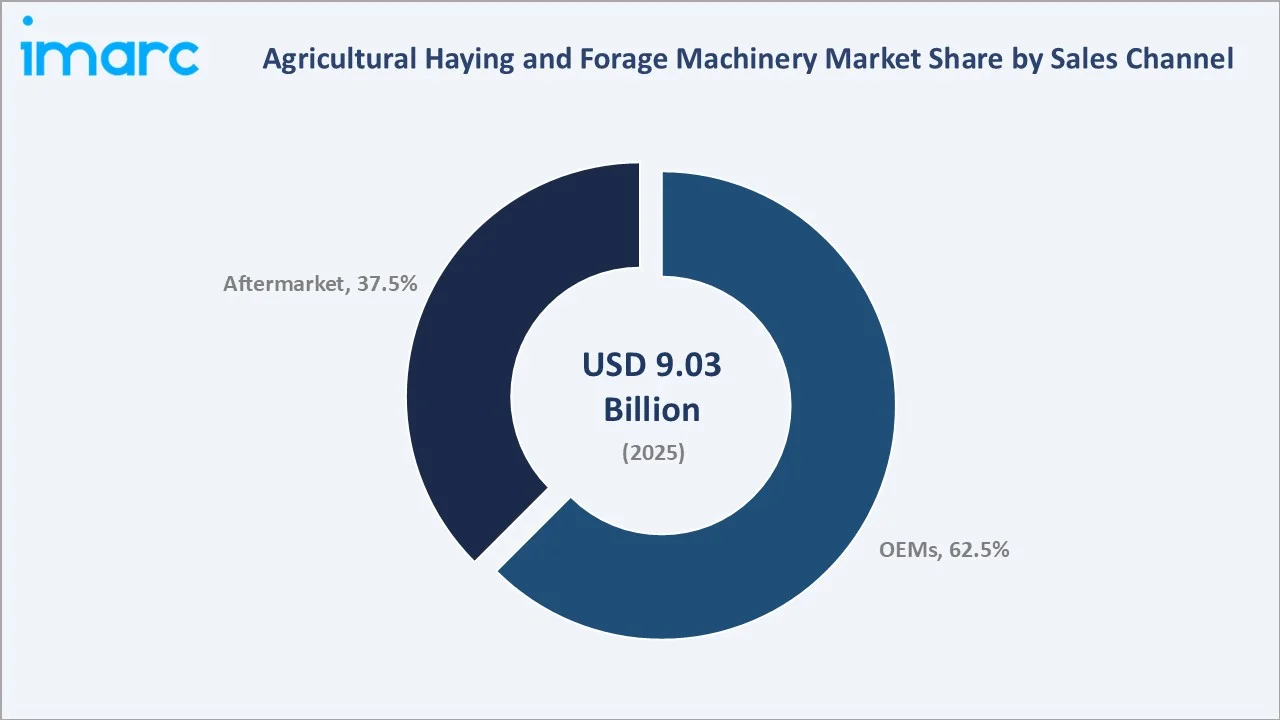

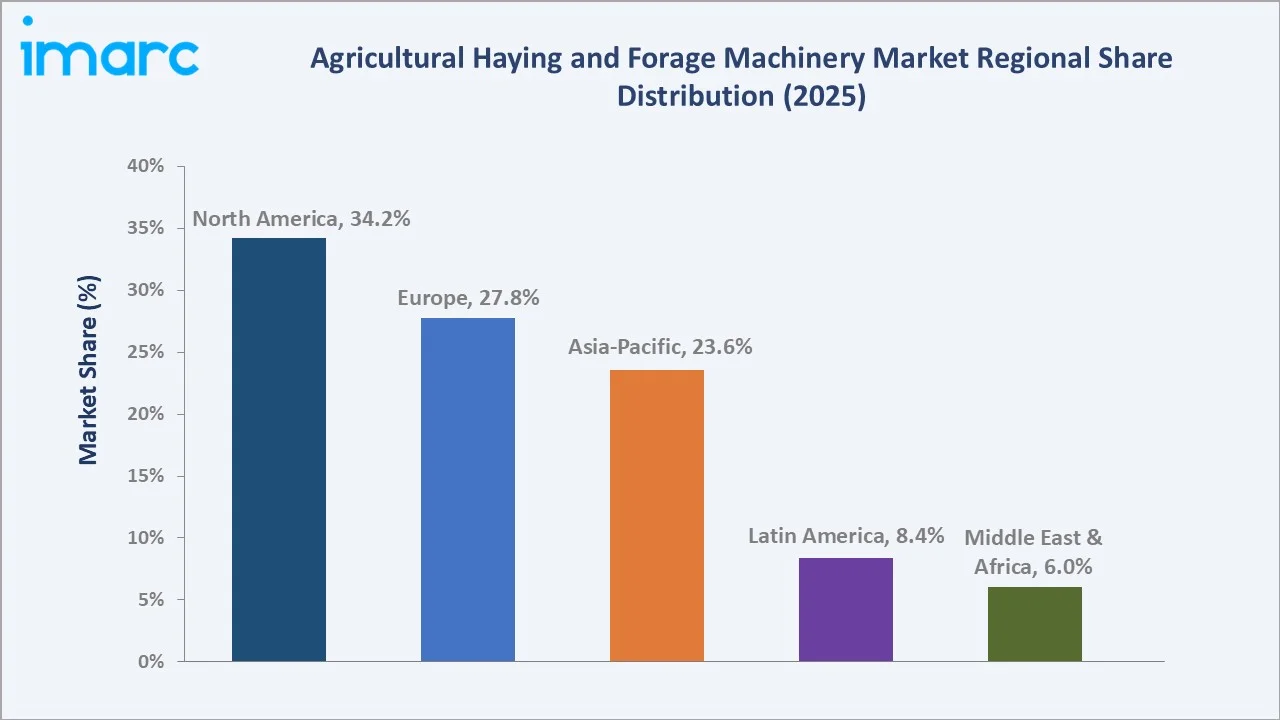

The agricultural haying and forage machinery market was valued at USD 9.03 Billion in 2025 and is projected to reach USD 11.09 Billion by 2034, exhibiting a CAGR of 2.23% during 2026-2034. Rising livestock and dairy production, steady replacement of aging haying fleets, and increasing demand for quality forage are the primary drivers shaping the market growth.

Mowers lead the machinery type segment at 31.8%, OEMs dominate the sales channel segment at 62.5%, and North America commands a 34.2% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.03 Billion |

|

Forecast Market Size (2034) |

USD 11.09 Billion |

|

CAGR (2026-2034) |

2.23% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

| Largest Region |

North America (34.2%, 2025) |

| Second Largest Region |

Europe (27.8%, 2025) |

| Leading Machinery Type |

Mowers (31.8%, 2025) |

| Leading Sales Channel |

OEMs (62.5%, 2025) |

The agricultural haying and forage machinery market expanded from USD 8.09 Billion in 2020 to USD 9.03 Billion in 2025, supported by mechanization, fleet renewal, and steady forage demand. Anchored at USD 10.09 Billion in 2030, the forecast to USD 11.09 Billion by 2034 reflects a mature, replacement-led market with selective growth in emerging regions.

To get more information on this market, Request Sample

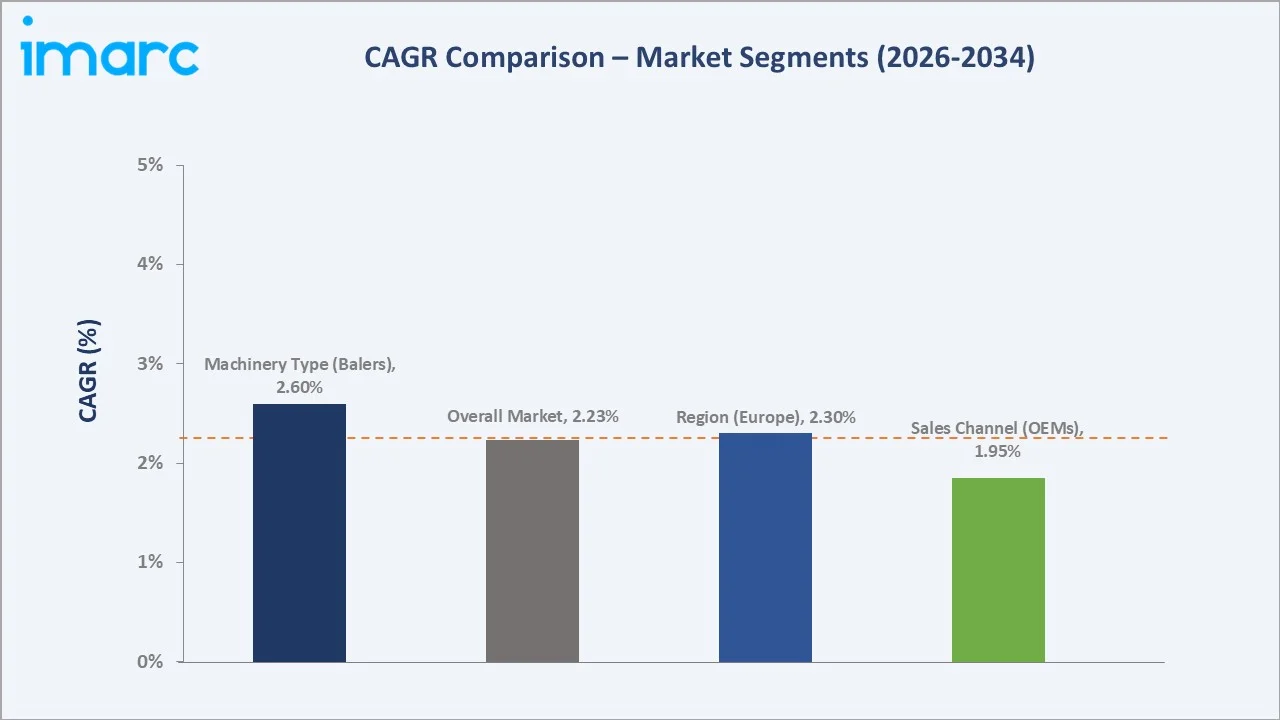

CAGR trajectories across machinery type and sales channel sub-segments show forage harvesters, balers, and aftermarket expanding faster than the overall 2.23% market CAGR, driven by silage demand, larger operations, and an aging installed base requiring parts and service.

Executive Summary

The agricultural haying and forage machinery market is on a steady growth path from USD 8.09 Billion in 2020 to USD 11.09 Billion by 2034. Haymaking has shifted toward larger, faster, and more automated machines as farms consolidate and labor tightens. Rising livestock and dairy output keeps demand for quality forage firm. Fleet replacement and mechanization in developing regions further support stable, replacement-led demand across the segment.

Mowers dominate the machinery type segment at 31.8% in 2025, supported by frequent cutting cycles and broad applicability. OEMs lead the sales channel segment at 62.5%, driven by factory-fitted machines, dealer financing, and bundled technology. North America commands 34.2%, led by large-scale hay and dairy operations and high mechanization activities across the United States and Canada. As per IMARC Group, the United States dairy market size was valued at USD 252.57 Billion in 2025.

Key Market Insights

|

Insight |

Data |

| Leading Machinery Type | Mowers - 31.8% share (2025) |

| Second Largest Machinery Type | Balers - 24.6% share (2025) |

| Leading Sales Channel | OEMs - 62.5% share (2025) |

| Second Largest Sales Channel | Aftermarket - 37.5% share (2025) |

| Leading Region | North America - 34.2% share (2025) |

| Second Largest Region | Europe - 27.8% (2025) |

| Top Companies | Deere & Company, CNH Industrial N.V., AGCO Corporation, KUBOTA Corporation, Vermeer Corporation |

Key Analytical Observations Expanding On The Data Above:

- Mowers dominance at 31.8% is driven by frequent first-cut operations and broad applicability across hay and silage. Disc and drum mowers remain core tools for nearly every haymaking operation, supporting steady replacement demand.

- Balers at 24.6% hold the second position, supported by round and large square baling for hay, straw, and silage. Demand for higher-density bales continues to favor larger, more capable machines.

- OEMs leadership at 62.5% reflects the prevalence of factory-fitted machines, dealer financing, and bundled precision technology. At AGRITECHNICA 2025, AGCO Corporation presented its full-line forage offering, including the Fendt Katana forage harvester.

- Aftermarket at 37.5% is sustained by a large and aging installed base requiring blades, belts, tines, and routine service, providing a resilient and recurring revenue stream for suppliers.

- North America at 34.2% leads on large-scale hay and dairy operations, high mechanization, and a strong fleet-replacement culture across the United States and Canada.

Agricultural Haying and Forage Machinery Market Overview

Agricultural haying and forage machinery covers equipment used to cut, condition, rake, bale, and harvest grass and fodder crops. Core categories include mowers, balers, forage harvesters, and conditioners used in hay and silage production.

The ecosystem integrates raw-material and component suppliers, OEM manufacturers, dealer and distribution networks, custom and contract operators, and farmers and livestock producers, together supported by parts, service, and aftermarket providers across regional markets.

Market Dynamics

To evaluate market opportunities, Request Sample

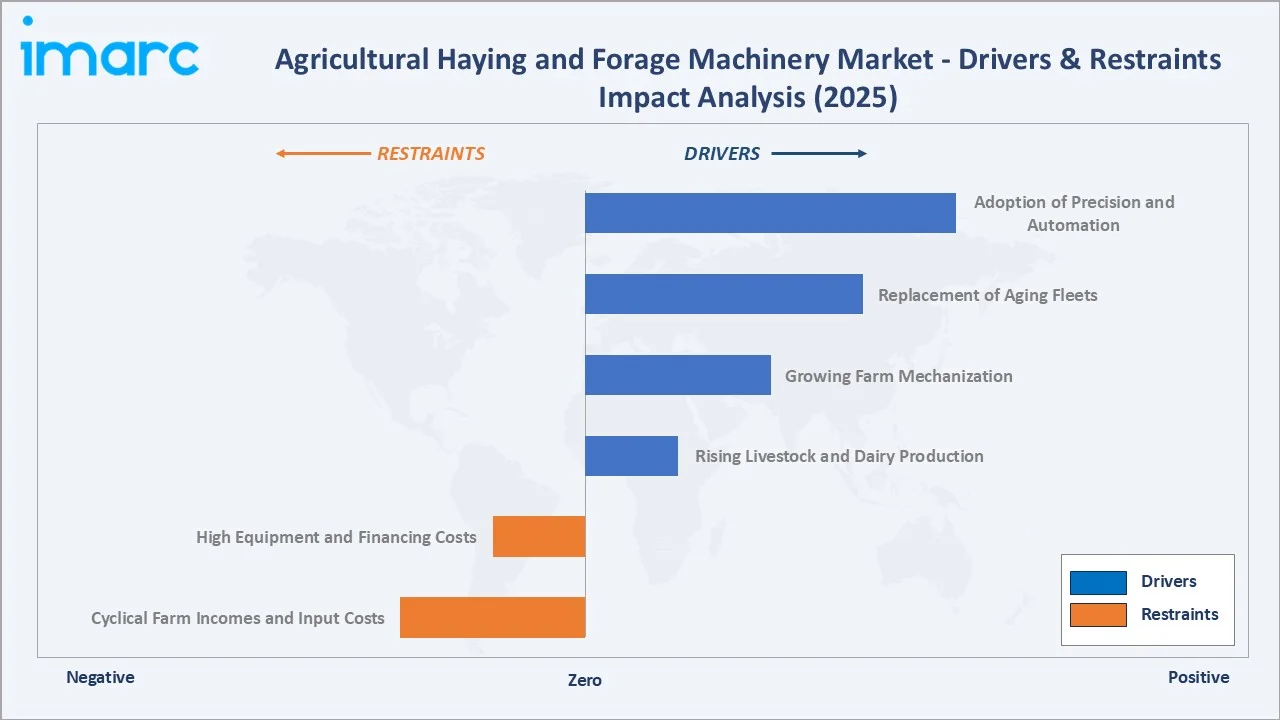

Market Drivers

- Rising Livestock and Dairy Production: Growing global demand for meat and dairy supports steady forage production, sustaining demand for mowing, baling, and harvesting equipment across livestock-intensive regions. In India, the total meat output reached 10.50 Million Tons for the period 2024-25.

- Growing Farm Mechanization: Mechanization in developing economies and labor shortages in mature markets are encouraging farms to adopt machines for cutting, conditioning, and baling, improving speed and forage quality.

- Replacement of Aging Fleets: A large installed base of older machines in developed regions drives recurring replacement demand as operators upgrade to more efficient and capable equipment.

- Adoption of Precision and Automation: Telematics, moisture sensing, and baling automation are improving efficiency and crop quality. Increasing integration of data-driven monitoring and machine control technologies is enabling operators to optimize forage harvesting operations and reduce field losses.

Market Restraints

- High Equipment and Financing Costs: Elevated machine prices and higher interest rates weigh on purchasing decisions, particularly for smaller operations. Limited access to affordable financing options further constrains equipment replacement and fleet expansion among cost-sensitive farmers.

- Cyclical Farm Incomes and Input Costs: Volatile commodity prices, fluctuating raw-material costs, and uncertain farm incomes can delay capital investment, slowing equipment purchases during weaker farming cycles.

Market Opportunities

- Emerging-Market Mechanization: Rising mechanization across India, Brazil, Africa, and Southeast Asia, alongside expanding dairy and livestock output, is creating new demand for affordable and mid-range haying equipment.

- Precision Haymaking and Service Models: Telematics-enabled machines, contractor and rental models, and value-added service packages offer manufacturers recurring revenue and stronger customer relationships.

Market Challenges

- Seasonality and Short Operating Windows: Haymaking depends on narrow weather windows and seasonal cycles, concentrating sales and utilization into limited periods and creating planning and inventory challenges for suppliers.

- Skilled Labor and Service Constraints: Shortages of skilled operators and technicians can limit equipment uptime and complicate maintenance, particularly for advanced machines requiring specialized support.

Emerging Market Trends

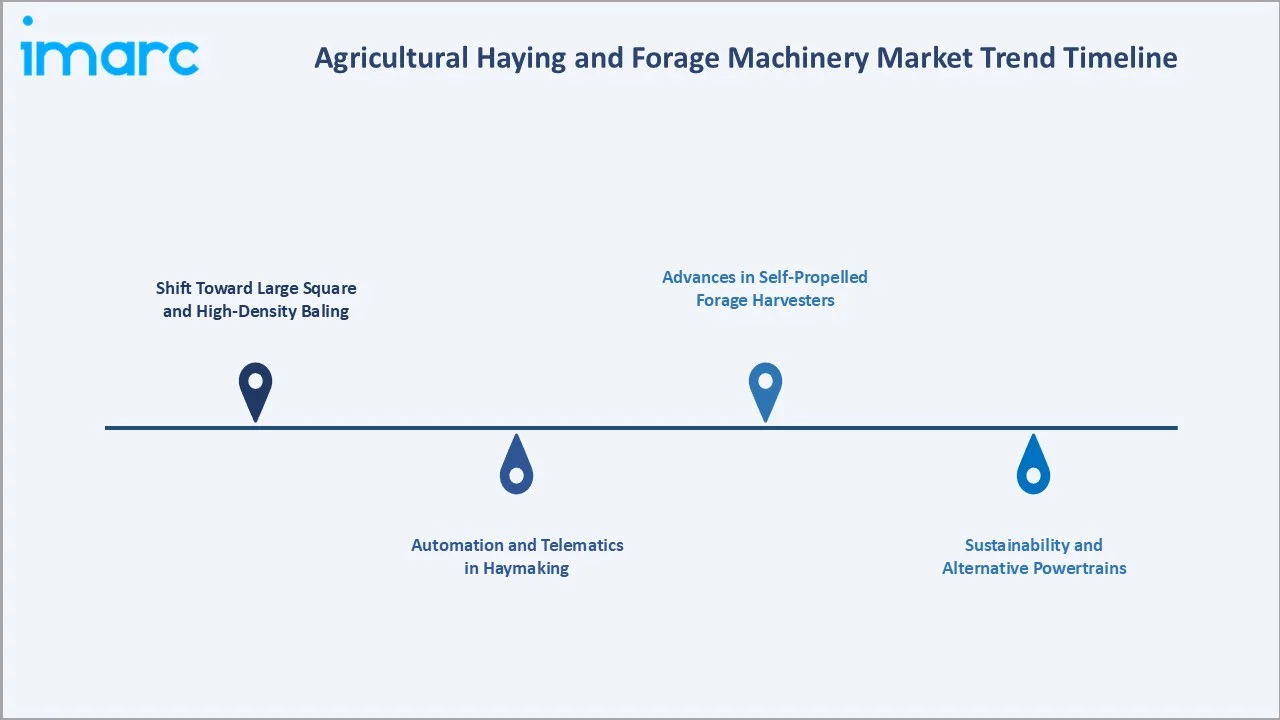

1. Shift Toward Large Square and High-Density Baling

Large square and high-density balers are gaining share as farms and contractors prioritize transport efficiency and storage density. This shift favors larger, higher-capacity machines suited to commercial hay and silage operations.

2. Automation and Telematics in Haymaking

Moisture sensing, automatic bale tying and ejection, and telematics-based fleet monitoring are becoming standard. These features improve forage quality, reduce operator workload, and enable data-driven equipment management.

3. Advances in Self-Propelled Forage Harvesters

Self-propelled forage harvesters continue to advance in capacity, chopping quality, and efficiency for silage operations. Enhanced automation, crop-flow optimization, and real-time performance monitoring technologies are further improving productivity and forage consistency in large-scale harvesting operations.

4. Sustainability and Alternative Powertrains

Manufacturers are exploring more efficient engines, alternative fuels, and early electrification to reduce emissions and operating costs. Lighter designs and improved conditioning also support faster dry-down and lower fuel use.

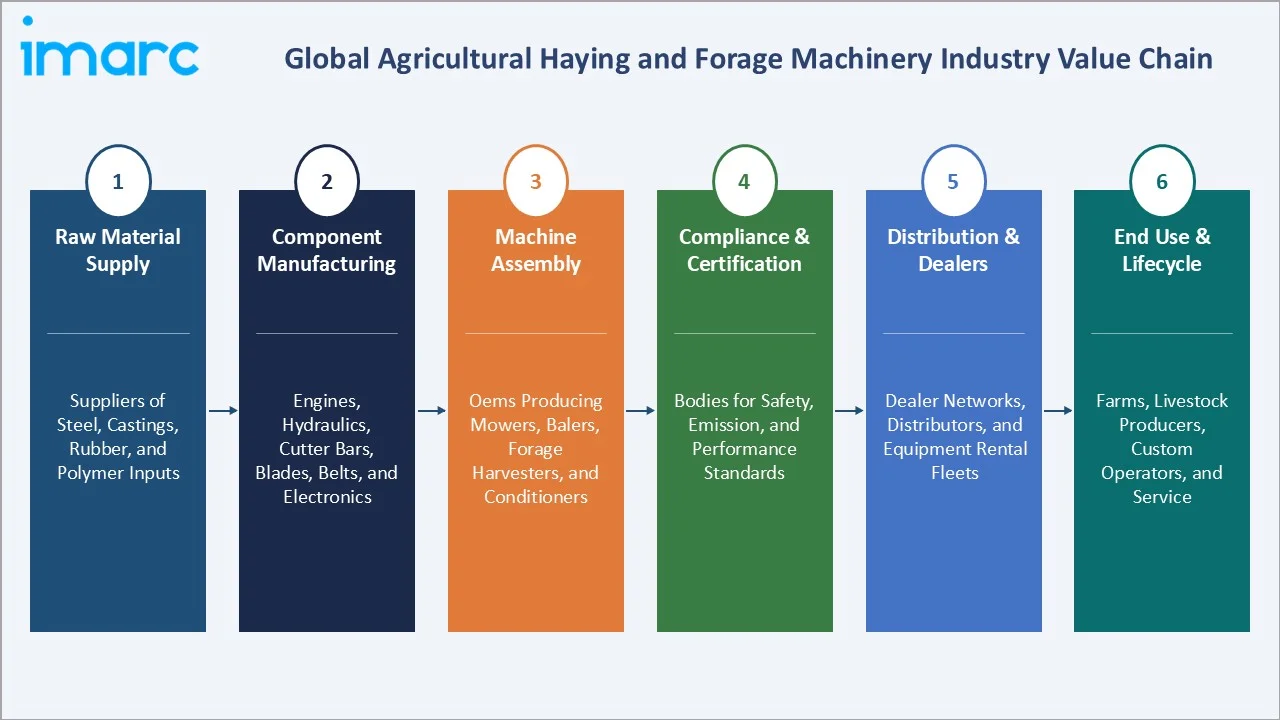

Industry Value Chain Analysis

The agricultural haying and forage machinery value chain spans six stages, from raw-material supply through end use and lifecycle service. Machine assembly and component manufacturing capture the highest value-add, while dealer relationships and after-sales service generate durable downstream advantages.

|

Stage |

Key Players / Examples |

| Raw Material Supply | Suppliers of steel, castings, rubber, and polymer inputs used in machine structures and wear parts |

| Component Manufacturing | Producers of engines, hydraulics, cutter bars, blades, belts, and electronic control systems |

| Machine Assembly | Original equipment manufacturers producing mowers, balers, forage harvesters, and conditioners |

| Compliance & Certification | Bodies administering safety, emission, and performance standards across regional markets |

| Distribution & Dealers | Authorized dealer networks, regional distributors, and equipment rental fleets |

| End Use & Lifecycle | Farms, livestock producers, custom operators, and parts-and-service providers |

Full-line and vertically capable players that combine in-house engineering with broad dealer coverage achieve stronger cost control and service reach than narrower specialists relying on third-party components.

Technology Landscape in the Agricultural Haying and Forage Machinery Industry

Cutting and Conditioning Innovation

Disc and drum mowers, mower-conditioners, and improved conditioning systems are enabling faster cutting and quicker dry-down. Advances in cutter-bar durability and conditioning intensity help preserve crop quality while increasing field speed and capacity.

Baling and Forage Harvesting Technology

Variable-chamber round balers, high-density large square balers, and high-capacity self-propelled forage harvesters are raising throughput and bale quality. Automated tying, ejection, and bale-data capture reduce operator workload and improve consistency.

Smart Connectivity and Precision Farming

Telematics, moisture sensors, GPS guidance, and fleet-management platforms are increasingly integrated into haying machinery. These tools enable real-time monitoring, predictive maintenance, and data-driven decisions that improve uptime and forage quality.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Machinery Type |

Mowers |

31.8% |

2025 |

|

Sales Channel |

OEMs |

62.5% |

2025 |

|

Region |

North America |

34.2% |

2025 |

By Machinery Type

Mowers command a 31.8% majority share in 2025, driven by their essential role in nearly every haymaking operation and frequent replacement cycles. Disc and drum mowers and mower-conditioners remain core to cutting and conditioning across hay and silage production.

To access detailed market analysis, Request Sample

Balers follow at 24.6%, supported by round and large square baling demand. Growing emphasis on efficient forage handling, transportation, and storage is further driving adoption across commercial livestock and hay production operations.

By Sales Channel

OEMs dominate with a 62.5% share in 2025, reflecting the prevalence of factory-fitted machines sold through authorized dealer networks. This channel benefits from financing, warranty support, and bundled precision technology that strengthen customer relationships.

Aftermarket holds 37.5% in 2025, sustained by a large and aging installed base that requires blades, belts, tines, and routine service. This channel provides resilient, recurring revenue and grows steadily alongside fleet aging.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

| North America |

34.2% |

Large-scale hay and dairy operations, high farm mechanization, and steady fleet-replacement demand |

| Europe |

27.8% |

Established livestock sector, strong focus on forage quality, and supportive farm-modernization policies |

| Asia-Pacific |

23.6% |

Rising mechanization, expanding dairy and livestock output, and growing government support for farm equipment |

| Latin America |

8.4% |

Expanding cattle and dairy farming, growing commercial forage production, and increasing equipment access |

| Middle East and Africa |

6.0% |

Gradual farm mechanization, rising fodder demand, and investment in livestock productivity |

North America at 34.2% in 2025 leads the market, supported by large-scale hay and dairy operations, high mechanization, and a strong replacement culture. Well-developed dealer networks and contractor activity further sustain demand across the United States and Canada.

Europe at 27.8% is the second-largest region. Replacement demand, forage-quality requirements, precision-farming adoption, and supportive modernization policies continue to support equipment purchases across the region.

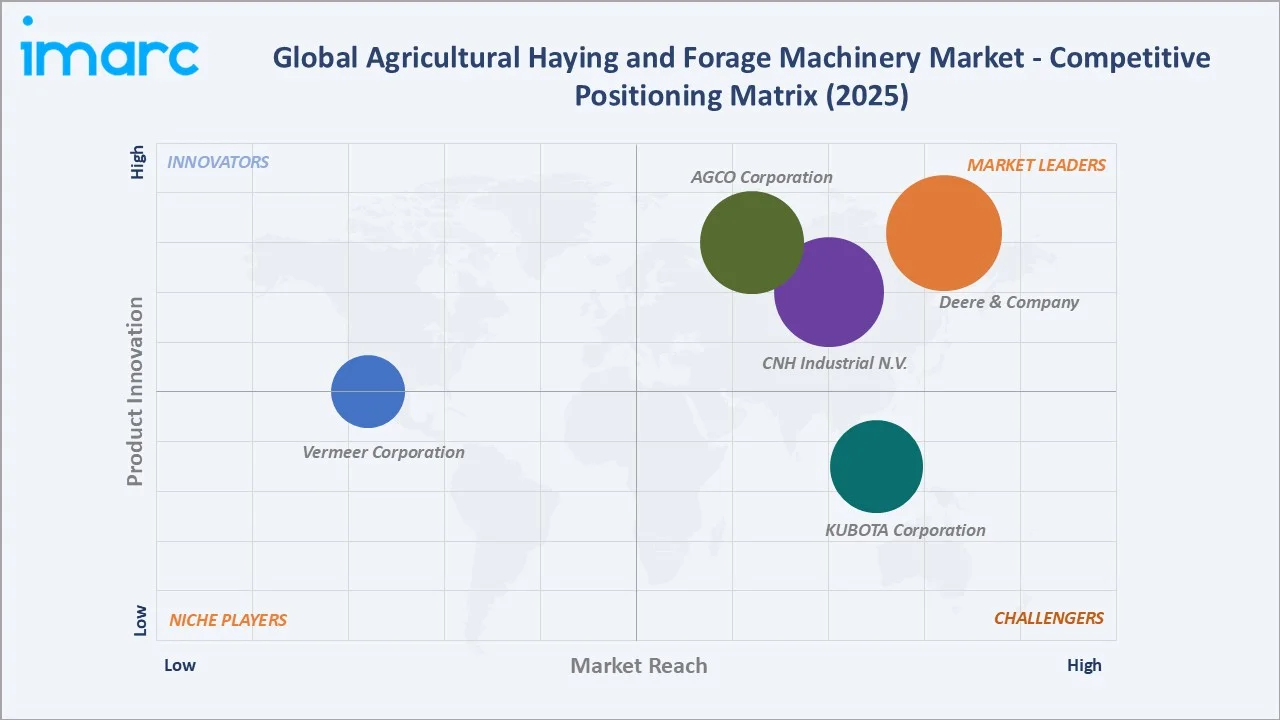

Competitive Landscape

The agricultural haying and forage machinery market is moderately concentrated, with a few global full-line manufacturers leading on brand strength and dealer reach, while specialized players serve specific machine categories and regions. Dealer-network depth and after-sales service form key competitive moats.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

| Deere & Company | John Deere (One Series Round Balers) | Leader | Broad full-line portfolio, dealer-network depth, and precision-technology integration |

| CNH Industrial N.V. |

Case IH |

Leader | Multi-brand coverage, baling and forage innovation, and global distribution |

| AGCO Corporation |

Fendt |

Leader | Full-line hay and forage range with smart-farming technology |

| Kubota Corporation | Kubota, Kverneland (Disc Mowers, Rakes) |

Challenger |

Compact and mid-range machinery with expanding global reach |

| Vermeer Corporation | Vermeer Hay and Silage Balers |

Emerging |

Round-baling focus and durable forage-handling solutions |

Key players in the market include Deere & Company, CNH Industrial N.V., AGCO Corporation, KUBOTA Corporation, and Vermeer Corporation, among others.

Key Company Profiles

Deere & Company

Deere & Company, operating under the John Deere brand, is a leading global manufacturer of agricultural machinery with a comprehensive presence across the haying and forage equipment segment.

- Product Portfolio: A broad hay and forage range, including mowers, balers, and forage harvesting equipment, supported by an extensive dealer network and integrated precision-technology tools.

- Recent Developments: In September 2025, John Deere introduced the V452M round baler, headlining an updated VR and CR round baler lineup with baling automation and enhanced features for heavy crop and silage conditions.

- Strategic Focus: A broad full-line portfolio, deep dealer-network coverage, and leadership in precision-agriculture integration across its haying and forage equipment.

CNH Industrial N.V.

CNH Industrial N.V. is a global agricultural and construction equipment manufacturer that serves the haying and forage market through its established agricultural machinery brands.

- Product Portfolio: A wide range of hay and forage equipment, including balers, mower-conditioners, windrowers, and forage harvesters, delivered through a broad multi-brand and global distribution network.

- Recent Developments: The company continues to invest in and modernize its hay and forage equipment portfolio, with ongoing updates aimed at improving productivity, bale quality, and connectivity for livestock and forage operations.

- Strategic Focus: Multi-brand coverage, continued baling and forage innovation, and broad global distribution.

AGCO Corporation

AGCO Corporation is a global designer, manufacturer, and distributor of agricultural machinery and precision-ag technology, with a strong position in the haying and forage equipment segment.

- Product Portfolio: A full hay and forage line, including mowers, tedders, rakes, balers, and forage harvesters, complemented by integrated smart-farming and precision-agriculture solutions.

- Recent Developments: The company continues to expand and enhance its hay and forage offering, with ongoing product updates and the integration of smart-farming technologies across its equipment range.

- Strategic Focus: A full-line hay and forage range supported by smart-farming technology and a global brand and dealer footprint.

Market Concentration Analysis

The agricultural haying and forage machinery market is moderately concentrated, with a small group of global full-line manufacturers, including Deere & Company, CNH Industrial N.V., AGCO Corporation, KUBOTA Corporation, and Vermeer Corporation, holding a substantial combined share alongside specialized regional players.

Barriers to entry include the scale required for dealer networks, sustained research and development, brand trust, and after-sales service capability. These factors favor well-capitalized incumbents with broad portfolios and established distribution.

Consolidation continues through brand-portfolio expansion, technology bundling, and dealer consolidation. Scale advantages in manufacturing, distribution, and service reinforce the competitive position of established full-line players.

Investment & Growth Opportunities

Fastest-Growing Segments

Forage harvesters and balers are expected to grow faster than the overall 2.23% market CAGR through 2034, supported by silage demand and larger operations. Aftermarket at 37.5% also expands steadily as the aging installed base drives parts and service needs.

Emerging Markets

Asia-Pacific is the highest-growth region, with rising mechanization and expanding dairy output. India, Brazil, and parts of Africa represent significant untapped opportunities as affordability and equipment access improve.

Venture & Investment Trends

Investment is concentrated in precision haymaking, telematics, automation, and more efficient or alternative powertrains. Service-based and contractor models are also attracting interest as manufacturers seek recurring revenue streams.

Future Market Outlook (2026-2034)

The agricultural haying and forage machinery market is forecast to expand from USD 9.03 Billion in 2025 to USD 11.09 Billion by 2034 at a CAGR of 2.23%, adding roughly USD 2.06 Billion in incremental value over the forecast period.

Four forces will shape the market through 2034: continued mechanization in emerging regions, automation and telematics adoption, steady fleet replacement in mature markets, and a gradual shift toward more sustainable and efficient machines.

By 2034, developed markets are expected to remain replacement-led and technology-driven, while emerging regions provide the strongest incremental growth. Full-line manufacturers with deep dealer networks and strong service capability are positioned to lead.

Research Methodology

Primary Research

Primary research included interviews with equipment manufacturers, dealers, custom and contract operators, and farm and livestock producers, validating market sizing, regional demand, machinery-type splits, and sales-channel dynamics across the forecast period.

Secondary Research

Secondary sources included government agricultural statistics, industry associations, equipment-manufacturer annual reports, investor presentations, press releases, and trade publications covering haying and forage machinery and broader farm-equipment trends.

Forecasting Models

Market forecasts combined top-down and bottom-up models using farm mechanization rates, livestock and forage output, fleet age and replacement cycles, and equipment pricing. Scenario analysis addressed farm-income cycles and input-cost variation.

Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage | Machinery Type, Sales Channel, Region |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Vermeer Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Agricultural Haying and Forage Machinery Market Report

The market was valued at USD 9.03 Billion in 2025, supported by rising livestock and dairy production, farm mechanization, and steady replacement of aging haying fleets across regions.

The market is projected to grow at a 2.23% CAGR from 2026 to 2034, reaching USD 11.09 Billion, driven by mechanization, fleet renewal, and emerging-market demand.

Mowers lead at 31.8% in 2025, driven by their essential cutting role. Their widespread use across hay and forage production cycles makes them a foundational equipment category for both livestock and commercial farming operations.

OEMs dominate at 62.5% in 2025 through factory-fitted machines and dealer networks. Aftermarket holds 37.5%, sustained by parts and service for an aging fleet.

North America commands 34.2% in 2025, led by large-scale hay and dairy operations. High mechanization levels, extensive forage cultivation, and strong replacement demand for advanced equipment continue to support the region’s market leadership.

Leading players include Deere & Company, CNH Industrial N.V., AGCO Corporation, KUBOTA Corporation, and Vermeer Corporation.

Growth is driven by rising livestock and dairy production, farm mechanization, replacement of aging fleets, and increasing adoption of precision and automation technologies in haymaking.

High equipment and financing costs, cyclical farm incomes, volatile input costs, seasonality, and shortages of skilled operators and technicians can constrain equipment purchases and utilization.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)