Air Brake System Market Size, Share, Trends and Forecast by Component, Type, Vehicle Type, and Region, 2026-2034

Air Brake System Market Size, Share, Trends & Forecast (2026-2034)

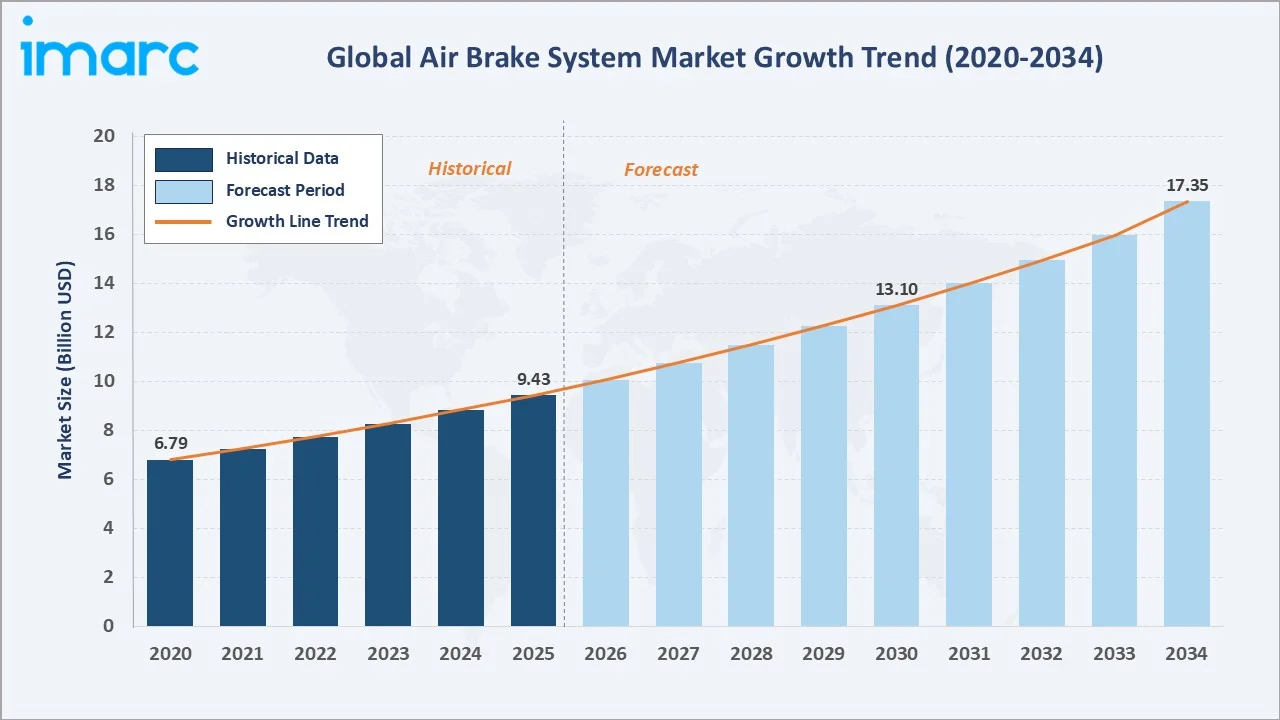

The global air brake system market size reached USD 9.43 Billion in 2025 and is projected to reach USD 17.35 Billion by 2034, exhibiting a CAGR of 6.80% during 2026-2034. Growing commercial vehicle production, stricter safety regulations, and expanding rail infrastructure are the primary growth forces shaping this market.

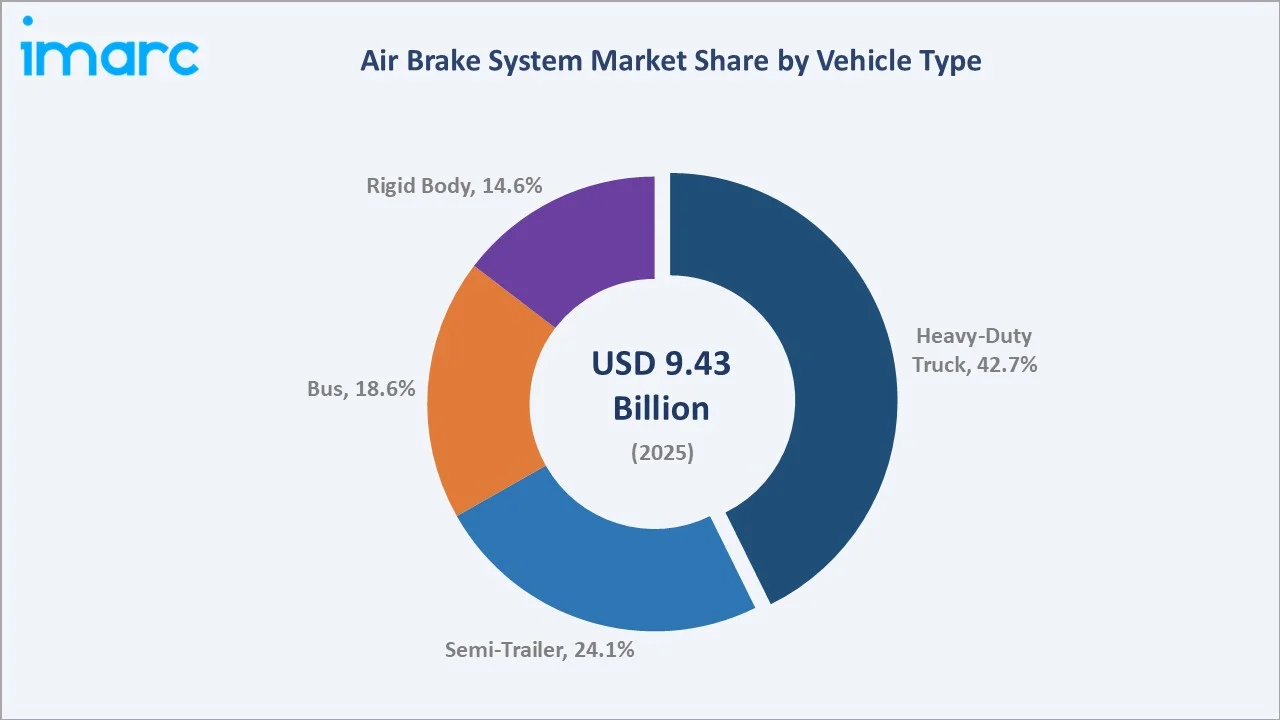

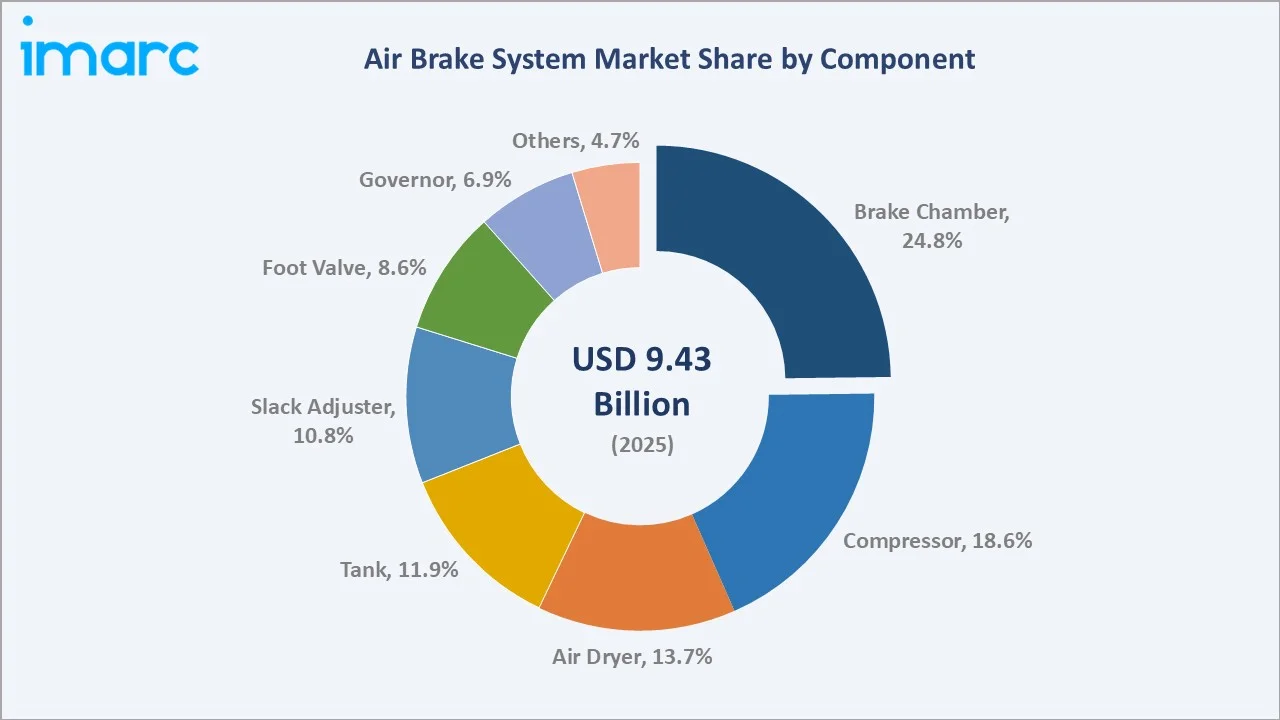

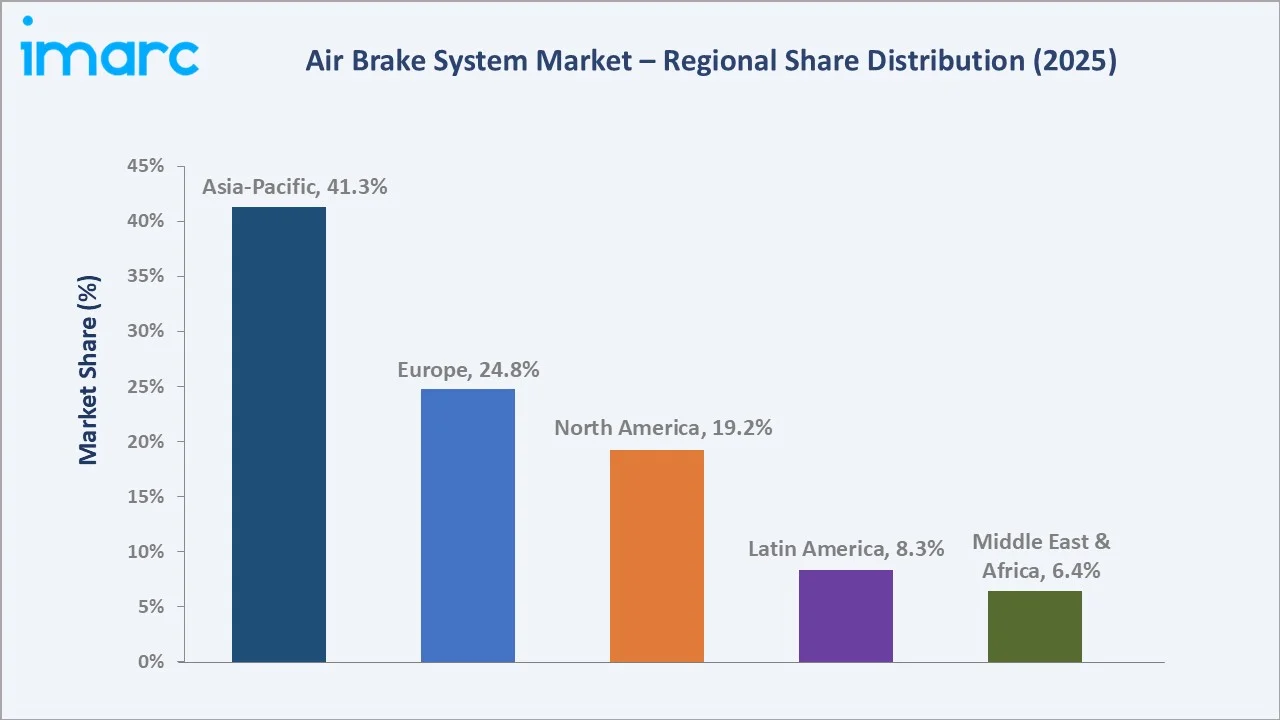

Heavy-Duty Truck leads vehicle type segmentation at 42.7% in 2025, driven by freight transportation expansion. Brake Chamber commands 24.8% component share. Asia-Pacific dominates the regional landscape with a 41.3% share underpinned by robust commercial vehicle manufacturing and rail infrastructure investment across China, India, and South Korea.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 9.43 Billion |

|

Forecast Market Size (2034) |

USD 17.35 Billion |

|

CAGR (2026-2034) |

6.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Vehicle Type |

Heavy-Duty Truck (42.7% share, 2025) |

|

Leading Component |

Brake Chamber (24.8% share, 2025) |

|

Leading Region |

Asia-Pacific (41.3% share, 2025) |

The air brake system market growth from 2020 through 2034 reflects consistent demand driven by global freight expansion, rising safety mandates, and technological advances. The forecast to USD 17.35 Billion by 2034 captures commercial vehicle production growth, railway electrification projects, and accelerating adoption of advanced braking technologies worldwide.

To get more information on this market, Request Sample

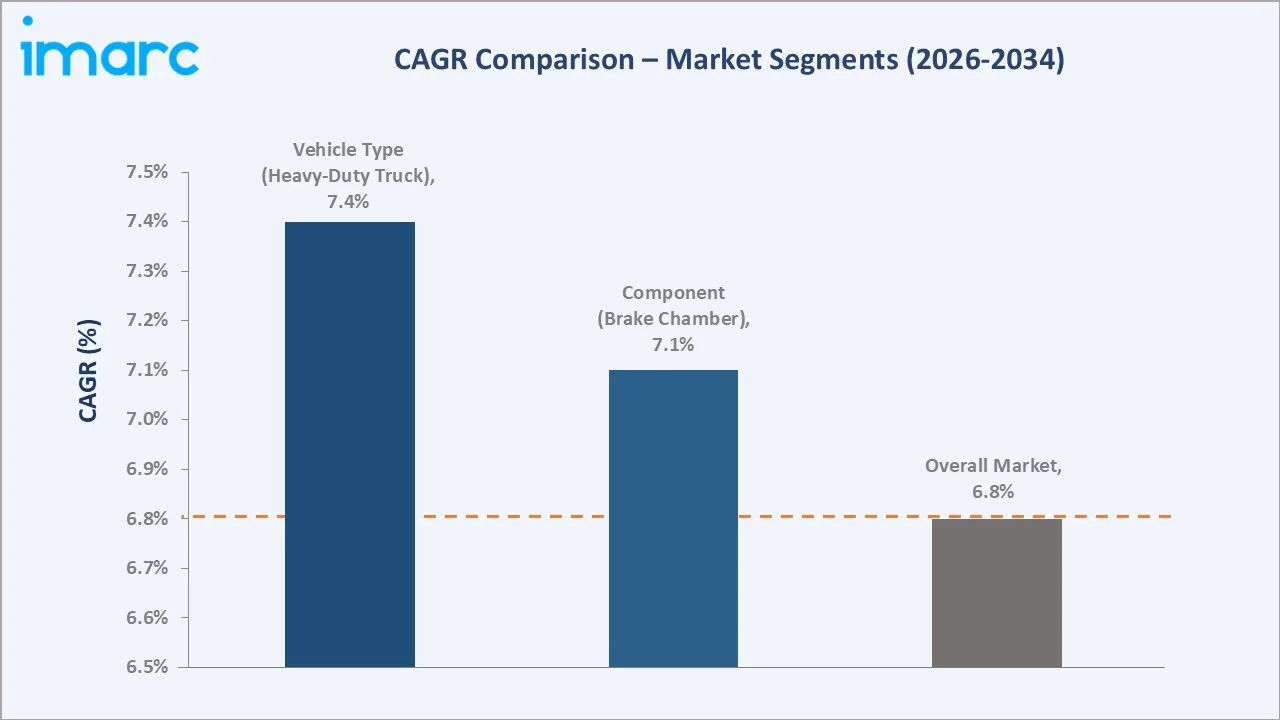

The CAGR trajectories across key vehicle type and component sub-segments highlight Heavy-Duty Truck at approximately 7.4% CAGR and Brake Chamber at approximately 7.1% CAGR as the fastest-growing categories within the air brake system market through 2034.

Executive Summary

The air brake system market is on a sustained growth trajectory from USD 9.43 Billion in 2025 to USD 17.35 Billion by 2034. The market encompasses air disc and drum brake systems deployed across heavy-duty trucks, semi-trailers, buses, rigid body vehicles, and railway applications worldwide.

Heavy-Duty Truck leads at 42.7% in 2025, owing to its critical role in long-haul freight transportation, logistics networks, and commercial fleet operations. Semi-Trailer (24.1%) supports intermodal transportation and distribution networks across North America, Europe, and Asia-Pacific regions.

Brake Chamber commands 24.8% component share in 2025, driven by its fundamental role in converting air pressure into mechanical braking force. Compressor (18.6%) and Air Dryer (13.7%) reflect sustained demand for system reliability across high-utilization commercial vehicle fleets globally.

Asia-Pacific dominates at 41.3% in 2025, supported by rapid commercial vehicle manufacturing expansion in China and India, growing rail infrastructure investment, and rising road freight activity. Europe follows at 24.8%, with North America at 19.2%, driven by stringent vehicle safety regulations and mature commercial fleet replacement cycles.

Key Market Insights

|

Insight |

Data |

|

Largest Vehicle Type |

Heavy-Duty Truck – 42.7% share (2025) |

|

Leading Component |

Brake Chamber – 24.8% share (2025) |

|

Leading Region |

Asia-Pacific – 41.3% share (2025) |

|

Second Largest Region |

Europe – 24.8% share (2025) |

|

Top Companies |

Knorr-Bremse AG, ZF Friedrichshafen AG, SAF-HOLLAND SE, Brakes India, and others |

- Heavy-Duty Truck at 42.7%: dominates because long-haul freight and logistics networks depend on reliable compressed air braking. Rising e-commerce-driven trucking demand and stricter regulatory requirements for heavy vehicle safety systems sustain capital investment in advanced air brake systems globally.

- Brake Chamber commands 24.8%: share because it is the core actuating component in every air brake assembly. Growing commercial fleet sizes, rising vehicle utilization rates, and mandatory brake safety inspection programs sustain consistent replacement and aftermarket demand across all major regions.

- Asia-Pacific’s 41.3%: regional dominance reflects its unrivalled commercial vehicle production capacity, rapid logistics infrastructure expansion, and large-scale rail electrification programs. China and India are rapidly expanding air brake manufacturing capacity while sustaining demand through advanced vehicle safety regulation adoption.

Air Brake System Market Overview

The air brake system market encompasses pneumatic disc and drum braking solutions deployed across heavy commercial vehicles, buses, semi-trailers, rigid body trucks, and railway rolling stock. Market structure integrates raw material suppliers, component manufacturers, OEM assemblers, distributors, and regulatory bodies ensuring compliance with global vehicle safety standards.

The ecosystem integrates global brake system manufacturers, steel and aluminum suppliers, precision component producers, OEM vehicle assemblers, regulatory agencies, commercial fleet operators, railway authorities, and aftermarket service networks serving transportation, logistics, construction, and public transit sectors worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

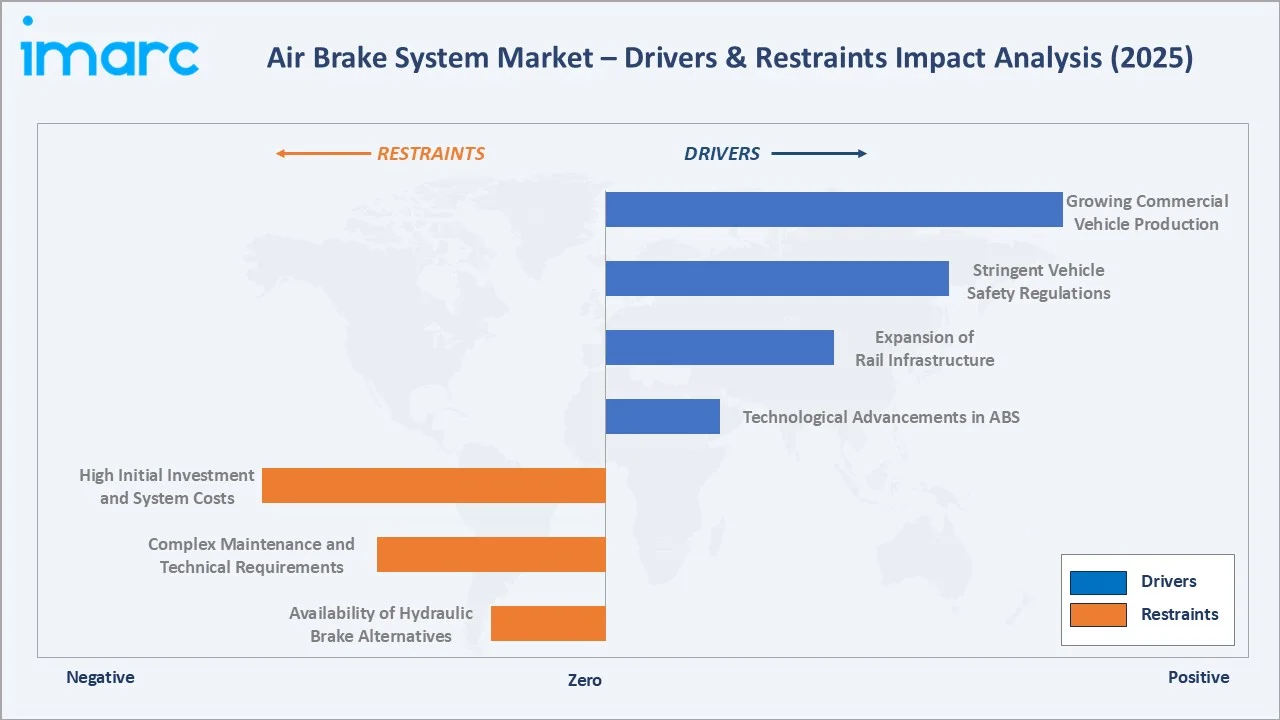

Market Drivers

- Growing Commercial Vehicle Production: Expanding global logistics networks, rising freight volumes driven by e-commerce, and increasing construction activity are fueling commercial vehicle production. Air brake systems are mandatory for heavy trucks and buses, creating sustained OEM demand as vehicle production scales across emerging economies globally.

- Stringent Vehicle Safety Regulations: Governments worldwide are implementing increasingly rigorous braking performance standards for heavy commercial vehicles. Mandatory ABS integration, enhanced braking distance requirements, and regular brake inspection protocols are driving sustained system upgrades and replacement demand across global commercial fleets and railway networks.

- Expansion of Rail Infrastructure: Large-scale rail electrification projects across Asia-Pacific, Europe, and the Middle East are creating significant demand for air brake systems in railway applications. Government investment in high-speed trains, metro systems, and freight rail expansion provides sustained growth impetus for specialized air braking solutions globally.

- Technological Advancements in Braking Systems: Development of electronically controlled air brakes, electro-pneumatic systems, and ADAS integration is expanding the value proposition of air braking technology. Manufacturers developing smart, lightweight, and more reliable systems are capturing premium market segments and commanding higher average selling prices globally.

Market Restraints

- High Initial Investment and System Costs: Air brake systems require substantial component investment and specialized installation expertise compared to hydraulic alternatives. These cost barriers restrict adoption among small fleet operators and commercial vehicle buyers in cost-sensitive emerging markets, limiting penetration rates in developing regions globally.

- Complex Maintenance and Technical Requirements: Air brake systems require regular maintenance of compressors, air dryers, valves, and chambers by trained technicians. Limited availability of qualified service personnel in emerging markets and high maintenance costs create operational challenges, slowing adoption among smaller fleet operators in developing regions worldwide.

- Availability of Hydraulic Brake Alternatives: Hydraulic brake systems offer lower initial costs and simpler maintenance requirements, making them competitive alternatives for light commercial vehicles. Growing performance improvements in hydraulic braking technology provide effective substitutes in market segments where air braking was previously dominant globally.

Market Opportunities

- Electric and Hybrid Commercial Vehicle Integration: The transition to electric and hybrid commercial vehicles creates significant opportunities for adapted air brake system designs. Manufacturers developing regenerative braking-compatible pneumatic systems and electro-pneumatic hybrid solutions are positioned to capture substantial market share as EV commercial fleets expand globally.

- Aftermarket Service and Component Replacement: The expanding global commercial vehicle fleet creates a growing aftermarket opportunity for air brake component replacement. Rising fleet utilization rates, mandatory safety inspection programs, and increasing focus on predictive maintenance drive sustained demand for high-quality replacement components and system upgrades worldwide.

Market Challenges

- Compliance with Evolving Safety Standards: Air brake system manufacturers must continuously adapt to evolving global safety standards, including FMVSS 121, ECE R13, and emerging Asian regulatory frameworks. Meeting diverse regional requirements while maintaining cost competitiveness creates significant engineering complexity and increases product development timelines globally.

- Supply Chain Disruptions and Raw Material Volatility: Air brake systems rely on steel, aluminum, rubber, and specialized electronic components subject to significant supply chain disruptions and price volatility. Managing these risks while maintaining competitive pricing and reliable delivery schedules presents ongoing operational challenges for manufacturers serving global OEM customers.

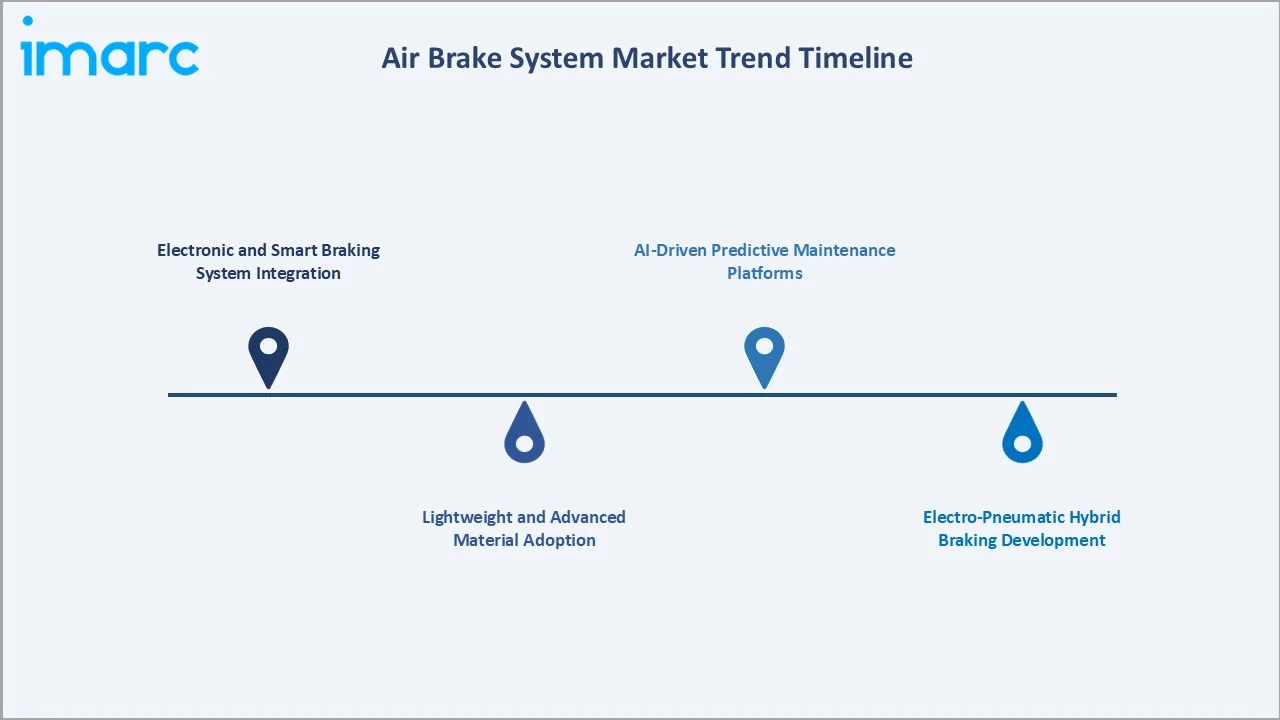

Emerging Market Trends

1. Electronic and Smart Braking System Integration

Advanced electronics, IoT connectivity, and real-time monitoring are transforming air brake operations. Smart systems with electronic brake force distribution, automated brake lining monitoring, and telematics integration are improving safety performance and reducing unplanned maintenance across commercial vehicle fleets globally.

2. Lightweight and Advanced Material Adoption

Manufacturers are developing next-generation air brake components using advanced aluminum alloys, composite materials, and lightweight steel grades to reduce system weight without compromising performance. Weight reduction initiatives driven by fuel efficiency mandates and EV payload optimization are accelerating material innovation across the global brake industry.

3. Electro-Pneumatic Hybrid Braking Development

Transition toward electro-pneumatic braking systems combining traditional compressed air actuation with electronic control is gaining momentum. These systems offer superior response times, improved brake force modulation, and seamless ADAS integration, representing a critical evolution for next-generation autonomous commercial vehicle platforms worldwide.

4. AI-Driven Predictive Maintenance Platforms

Machine learning algorithms and sensor fusion technologies are enabling predictive maintenance for air brake systems. Real-time monitoring of brake chamber pressure, valve response times, and compressor performance allows fleet operators to prevent failures, optimize maintenance schedules, and reduce costly roadside breakdown incidents globally.

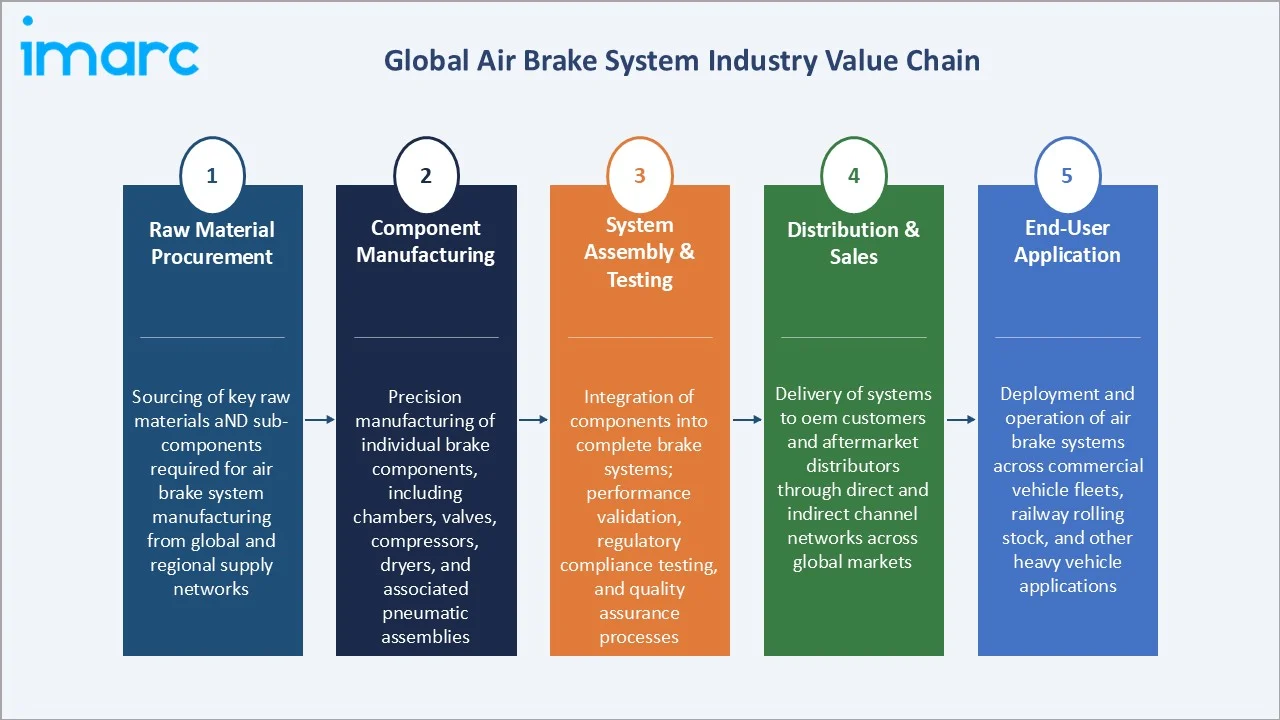

Industry Value Chain Analysis

The air brake system value chain spans five integrated stages from raw material sourcing through end-user operation. Component manufacturers capture primary value through precision engineering, while aftermarket service networks generate growing recurring revenue streams sustaining long-term customer relationships across commercial fleet operators worldwide.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of key raw materials and sub-components required for air brake system manufacturing from global and regional supply networks |

|

Component Manufacturing |

Precision manufacturing of individual brake components, including chambers, valves, compressors, dryers, and associated pneumatic assemblies |

|

System Assembly & Testing |

Integration of components into complete brake systems; performance validation, regulatory compliance testing, and quality assurance processes |

|

Distribution & Sales |

Delivery of systems to OEM customers and aftermarket distributors through direct and indirect channel networks across global markets |

|

End-User Application |

Deployment and operation of air brake systems across commercial vehicle fleets, railway rolling stock, and other heavy vehicle applications |

System assembly and testing stages capture the highest value in the air brake system chain, requiring specialized engineering expertise, regulatory certification knowledge, and sophisticated quality systems. Aftermarket replacement components, service contracts, and fleet management consulting represent growing recurring revenue streams, improving long-term customer retention globally.

Technology Landscape in the Air Brake System Industry

Electro-Pneumatic Braking Technology

Electro-pneumatic systems combining traditional air pressure actuation with electronic control modules enable faster brake response and more precise force modulation. These systems provide the foundation for automated emergency braking and vehicle stability control integration across next-generation commercial vehicle platforms globally.

Advanced Driver Assistance System (ADAS) Integration

Modern air brake systems are increasingly integrated with ADAS platforms including autonomous emergency braking, lane departure warning, and adaptive cruise control. This integration requires sophisticated valve control electronics and sensor fusion capabilities, driving technology investment and creating higher-value product categories for leading manufacturers.

Digital Monitoring and Fleet Telematics

Next-generation air brake systems incorporate embedded sensors transmitting real-time performance data to fleet management platforms. Continuous monitoring of chamber pressure, pushrod travel, and lining wear enables predictive maintenance and remote diagnostics, improving fleet uptime and reducing total cost of ownership for commercial vehicle operators globally.

Lightweight Composite Component Technology

Advanced polymer composites, aluminum alloys, and high-strength steels are enabling significant weight reduction in air brake components without compromising performance or durability. These innovations address commercial vehicle payload optimization requirements and are becoming critical for electric commercial vehicle brake system applications globally.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Brake Chamber |

24.8% |

2025 |

|

Type |

🔒 |

🔒 |

2025 |

|

Vehicle Type |

Heavy-Duty Truck |

42.7% |

2025 |

|

Region |

Asia-Pacific |

41.3% |

2025 |

By Vehicle Type

Heavy-Duty Truck commands a 42.7% majority share in 2025 owing to its essential role in long-haul freight transportation, distribution logistics, and construction material haulage. Regulatory mandates requiring air brake systems on all heavy commercial vehicles above defined gross vehicle weight ratings ensure sustained OEM demand across global truck manufacturing facilities.

To access detailed market analysis, Request Sample

Semi-Trailer (24.1%) reflects growing intermodal freight networks and cross-border logistics expansion. Bus (18.6%) encompasses urban transit, intercity coach, and school bus applications. Rigid Body (14.6%) addresses construction, municipal waste collection, and specialized vocational vehicle applications with mandatory braking compliance requirements globally.

By Component

Brake Chamber dominates at 24.8% in 2025, driven by its fundamental role as the primary actuating mechanism converting air pressure into mechanical braking force. Growing commercial fleet sizes, rising vehicle utilization rates, and mandatory brake safety inspection programs sustain consistent replacement demand across all vehicle categories globally.

Compressor (18.6%) serves as the critical pressure generation component sustaining the entire pneumatic braking circuit. Air Dryer (13.7%) reflects growing demand for moisture removal systems. Tank (11.9%), Slack Adjuster (10.8%), Foot Valve (8.6%), Governor (6.9%), and Others (4.7%) complete the comprehensive component ecosystem supporting global commercial vehicle operations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

41.3% |

Strong commercial vehicle production base; growing railway infrastructure investment; expanding logistics and freight networks |

|

Europe |

24.8% |

Stringent vehicle safety regulations; well-established OEM manufacturing base; rising adoption of advanced braking technologies |

|

North America |

19.2% |

Federal safety compliance mandates; robust freight trucking demand; growing trailer and heavy vehicle production volumes |

|

Latin America |

8.3% |

Expanding commercial fleet base; increasing freight activity; growing regulatory enforcement of vehicle safety standards |

|

Middle East & Africa |

6.4% |

Infrastructure development programs; commercial vehicle fleet modernization; growing construction and industrial sector demand |

Asia-Pacific's 41.3% market dominance in 2025 is driven by rapid commercial vehicle manufacturing expansion, large-scale government investment in railway networks, and growing logistics infrastructure requirements. The region's manufacturing cost advantages and large domestic consumption base sustain investment in air brake system production capacity across key markets.

Europe, at 24.8% in 2025, is anchored by stringent ECE R13 braking compliance requirement driving continuous system upgrades across the continent's sophisticated commercial vehicle fleet. North America at 19.2% maintains robust demand through FMVSS 121 federal safety standards, strong freight trucking activity, and growing Class 8 truck production volumes.

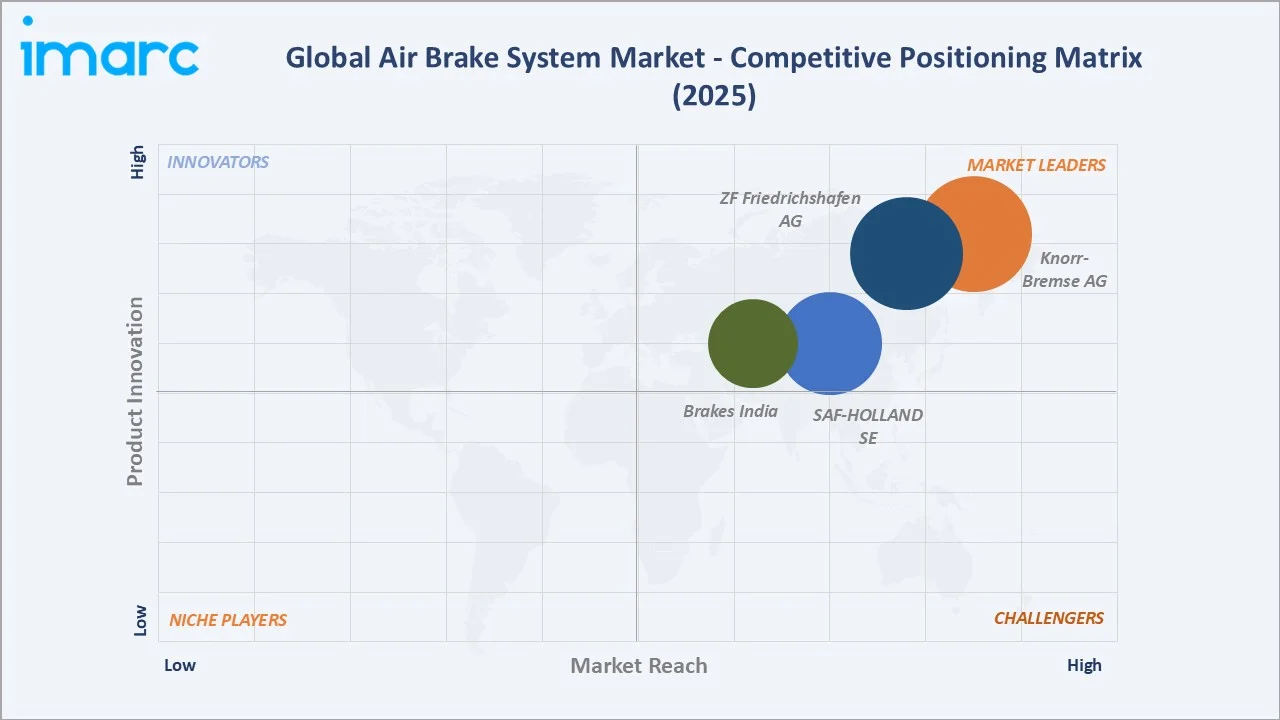

Competitive Landscape

The air brake system market is moderately concentrated, with global majors and specialized brake technology providers collectively commanding the largest market shares. International manufacturers leverage engineering expertise, regulatory certification portfolios, and global service networks to maintain competitive advantage across vehicle OEM customers worldwide.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

Knorr-Bremse AG |

EconX Calipers, Brake Pads, Brake Discs, SYNACT disc brakes |

Leader |

Advancing electro-pneumatic systems; expanding ADAS-integrated braking for autonomous commercial vehicles |

|

ZF Friedrichshafen AG |

Air Brake Systems, Anti-Lock Braking System (ABS), Electronic Braking System (EBS), Conventional Braking Components |

Leader |

Advancing integrated vehicle safety systems; developing autonomous braking for next-generation commercial fleets |

|

SAF-HOLLAND SE |

P89 Air Disc Brakes, Air suspensions |

Leader |

Deliver integrated brake-and-suspension systems |

|

Brakes India |

Air Disc Brake |

Leader |

Expanding export market presence; investing in R&D for international-grade braking technology development globally |

Key players include Knorr-Bremse AG, ZF Friedrichshafen AG, SAF-HOLLAND SE, Brakes India, and others.

Key Company Profiles

Knorr-Bremse AG

Knorr-Bremse AG is a global technology leader in braking systems for rail and commercial vehicles, headquartered in Munich, Germany. The company's air brake portfolio spans pneumatic, electro-pneumatic, and electronic braking systems serving commercial vehicle OEMs, railway operators, and aftermarket distributors.

- Product Portfolio: EconX Calipers, Brake Pads, Brake Discs, SYNACT disc brakes

- Strategic Focus: Knorr-Bremse is executing a dual strategy of advancing electro-pneumatic capabilities for autonomous commercial vehicles while expanding its digital services platform for predictive maintenance. The company is investing in AI-powered brake monitoring systems and strengthening its global service network to capture growing aftermarket revenue streams globally.

ZF Friedrichshafen AG

ZF Friedrichshafen AG is a global technology company supplying systems for passenger cars, commercial vehicles, and industrial technology, with a significant air brake system portfolio following integration of WABCO's commercial vehicle braking business. ZF's braking division serves major truck and bus OEMs with advanced pneumatic and electro-pneumatic solutions globally.

- Product Portfolio: Air Brake Systems, Anti-Lock Braking System (ABS), Electronic Braking System (EBS), Conventional Braking Components

- Strategic Focus: ZF is advancing its integrated vehicle safety systems strategy, combining braking, steering, and chassis control technologies for fully automated commercial vehicle applications. The company is investing heavily in brake-by-wire technology development and building electro-pneumatic braking expertise for autonomous freight vehicle platforms serving global logistics operators.

Market Concentration Analysis

The air brake system market is moderately concentrated, with global manufacturers including Knorr-Bremse AG and Wabtec Corporation holding significant shares through broad product portfolios, regulatory certifications, and global service capabilities. European and North American manufacturers dominate premium OEM segments, while Asian manufacturers are gaining share in cost-sensitive aftermarket categories globally.

At the component level, brake chamber and compressor segments drive concentration metrics, reflecting the technology differentiation between precision-engineered OEM components and standardized aftermarket alternatives. Geographic manufacturing concentration in Germany, the United States, and increasingly China creates supply chain considerations that global OEM customers manage through multi-supplier sourcing strategies.

Investment & Growth Opportunities

Fastest-Growing Segments

Heavy-Duty Truck represents the highest-growth vehicle type segment through 2034 at approximately 7.4% CAGR, capturing rising freight transportation demand and mandatory air brake regulations. Brake Chamber leads component growth at approximately 7.1% CAGR, driven by expanding commercial fleet sizes, rising replacement rates, and regulatory inspection requirements globally.

Emerging Markets

Asia-Pacific and Latin America are emerging as significant investment frontiers. India and China are rapidly expanding domestic air brake manufacturing capacity, while Southeast Asian commercial vehicle markets are increasingly adopting advanced braking technologies to meet tightening safety regulations and growing freight transportation requirements across the region.

Venture & Investment Trends

Strategic investors are increasing capital allocation to air brake technology companies focused on electro-pneumatic systems, digital monitoring platforms, and EV-adapted braking solutions. Government transportation infrastructure programs across Asia and Europe are catalyzing private capital mobilization in commercial vehicle safety technology and advanced braking system manufacturing expansion.

Future Market Outlook (2026-2034)

The air brake system market is forecast to expand from USD 9.43 Billion in 2025 to USD 17.35 Billion by 2034 at a CAGR of 6.80%, driven by commercial vehicle production growth, expanding railway infrastructure programs, and rising vehicle safety regulation enforcement across all major global markets through the forecast horizon.

Three structural forces will shape the market through 2034: commercial vehicle fleet expansion driven by global freight demand will sustain OEM braking system procurement; tightening vehicle safety regulations across Asia, Latin America, and Africa will accelerate system upgrades; and electro-pneumatic technology advancement will reshape the product value mix and drive average selling price improvement across leading manufacturers globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with air brake system manufacturers, commercial vehicle OEM procurement managers, fleet operators, railway maintenance technicians, and regulatory compliance specialists. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the air brake system industry globally.

Secondary Research

Key secondary sources include FMVSS 121 and ECE R13 regulatory documentation, vehicle safety agency publications, annual reports from key manufacturers, trade publications including Commercial Carrier Journal and FleetOwner, academic research on pneumatic braking technology, and market intelligence databases covering commercial vehicle and railway sectors globally.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating commercial vehicle production data, railway infrastructure investment pipelines, regulatory compliance timelines, and equipment replacement cycle analysis. Scenario modelling encompassed base, optimistic, and conservative cases through the 2034 forecast horizon.

Air Brake System Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Compressor, Governor, Tank, Air Dryer, Foot Valve, Brake Chamber, Slack Adjuster, and Others |

| Types Covered | Air Disc Brake, Air Drum Brake |

| Vehicle Types Covered | Rigid Body, Heavy-Duty Truck, Semi-Trailer, Bus |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Knorr-Bremse AG, ZF Friedrichshafen AG, SAF-HOLLAND SE, Brakes India, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Air Brake System Market Report

The global air brake system market reached USD 9.43 Billion in 2025, reflecting sustained demand driven by commercial vehicle production growth, rising freight transportation requirements, and stricter vehicle safety regulations mandating air braking systems across heavy commercial vehicles globally.

The market is projected to reach USD 17.35 Billion by 2034, growing at a CAGR of 6.80% during 2026-2034, driven by expanding commercial vehicle fleets, railway infrastructure growth, electro-pneumatic technology adoption, and tightening vehicle safety regulation enforcement across major emerging economies worldwide.

Heavy-Duty Truck leads the market with a 42.7% share in 2025, driven by long-haul freight transportation, logistics network expansion, and mandatory air brake requirements for vehicles above defined gross vehicle weight thresholds. This segment is expected to maintain leadership position through 2034 globally.

Brake Chamber commands the largest component share at 24.8% in 2025. Its role as the primary actuating mechanism in every air brake assembly, combined with growing fleet sizes, mandatory inspection programs, and regular replacement requirements, sustains its market leadership through the forecast period.

Asia-Pacific dominates with a 41.3% share in 2025, underpinned by rapid commercial vehicle manufacturing expansion, large-scale railway infrastructure investment, and growing logistics demand. The region is expected to maintain its leadership position through the 2034 forecast horizon globally.

Key market drivers include growing global commercial vehicle production driven by freight demand, stringent vehicle safety regulations mandating air braking systems, expanding railway infrastructure investment across Asia and Europe, and technological advancements enabling smart, lightweight, and electronically integrated braking systems globally.

Major challenges include high initial system investment costs limiting adoption in emerging markets, complex maintenance requirements demanding specialized technicians, evolving multi-regional regulatory compliance requirements, supply chain disruptions affecting raw material availability, and growing competition from improved hydraulic braking alternatives globally.

Leading companies in the air brake system market include Knorr-Bremse AG, ZF Friedrichshafen AG, SAF-HOLLAND SE, Brakes India, and others.

Key emerging technologies include electro-pneumatic braking systems enabling seamless ADAS integration, AI-powered predictive maintenance platforms using real-time sensor data, brake-by-wire technology for autonomous commercial vehicles, lightweight composite component materials, and IoT-enabled smart brake monitoring systems improving fleet safety management globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)