Aircraft Health Monitoring System Market Size, Share, Trends and Forecast by Component, Subsystem, End-User, Installation, Fit, Operation Time, Operation Type, and Region 2026-2034

Global Aircraft Health Monitoring System Market Size, Share, Trends & Forecast (2026-2034)

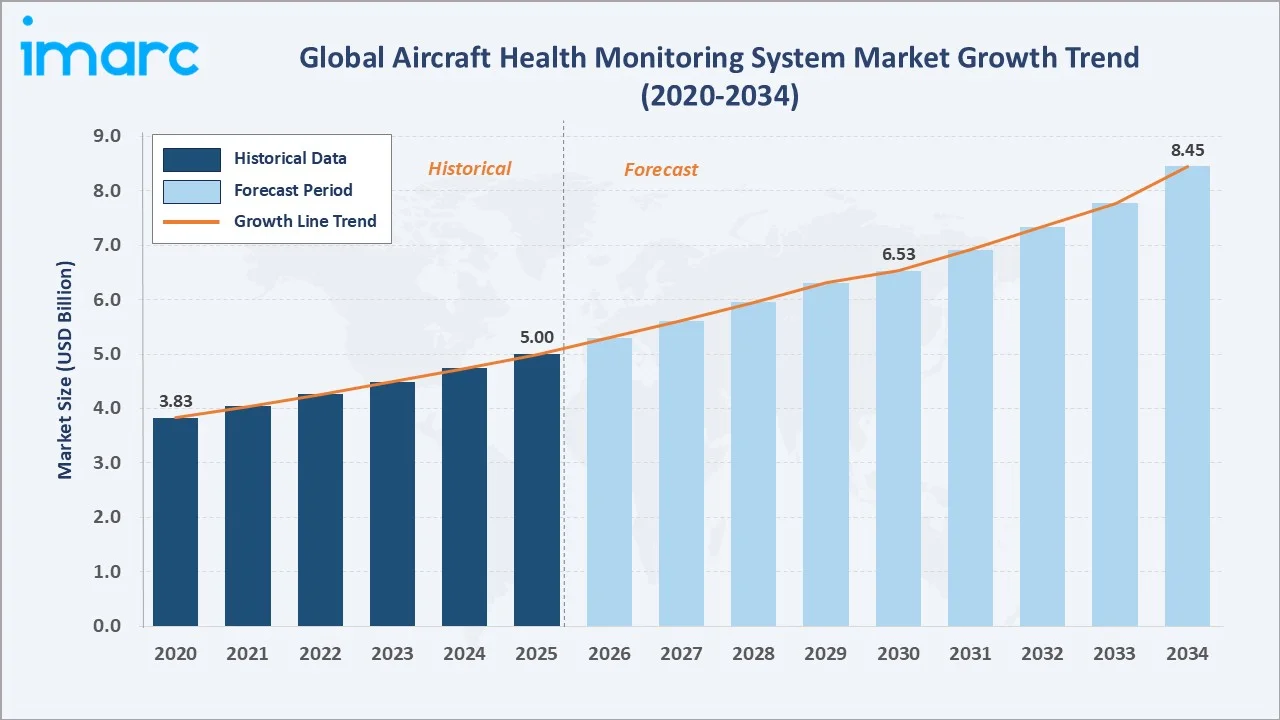

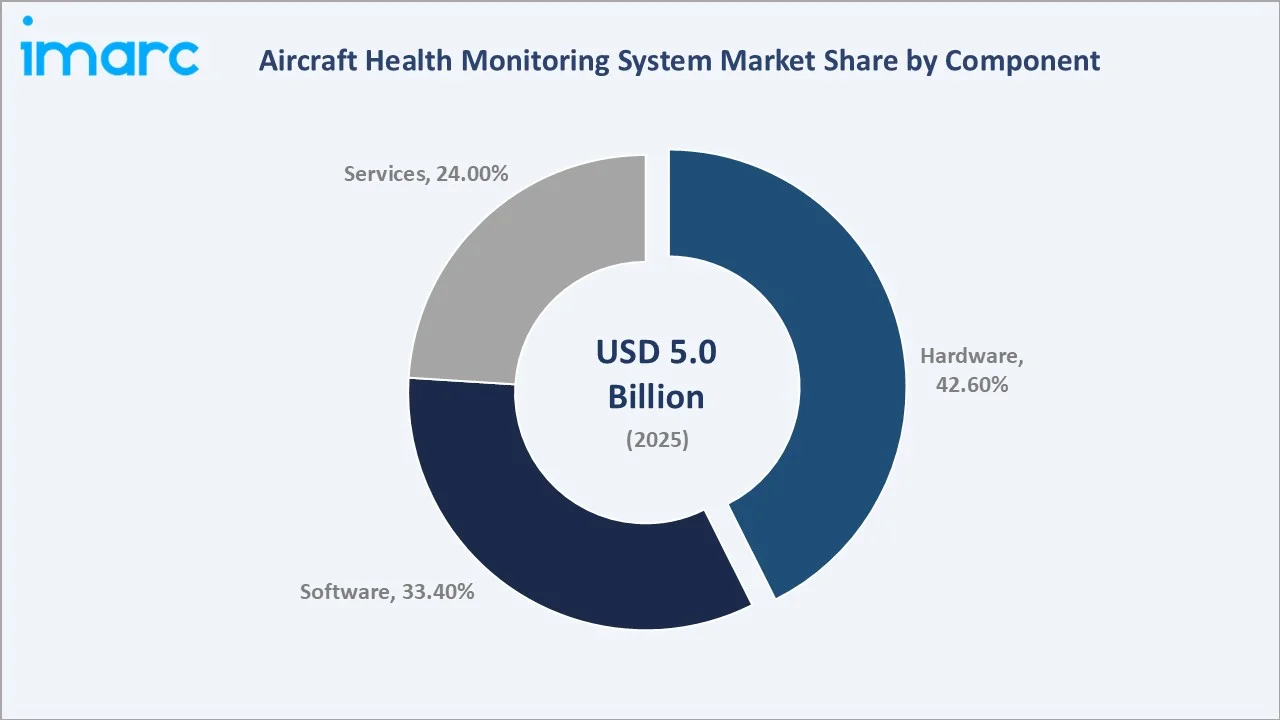

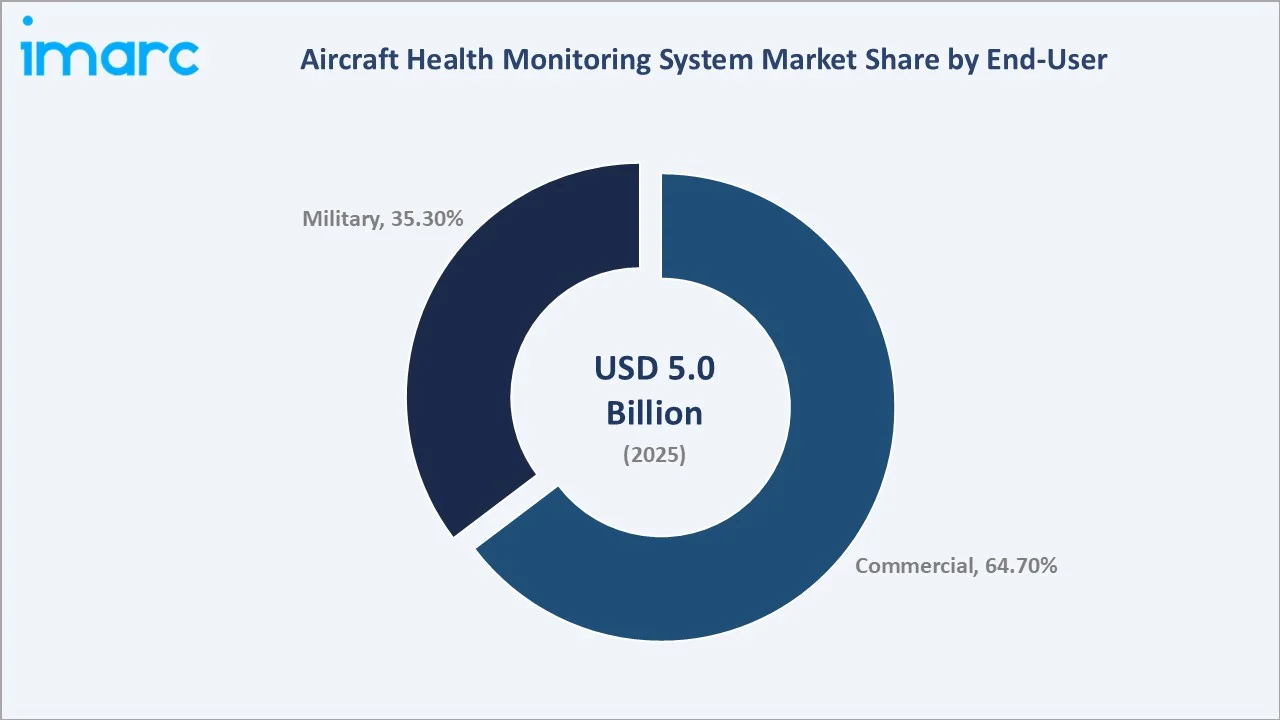

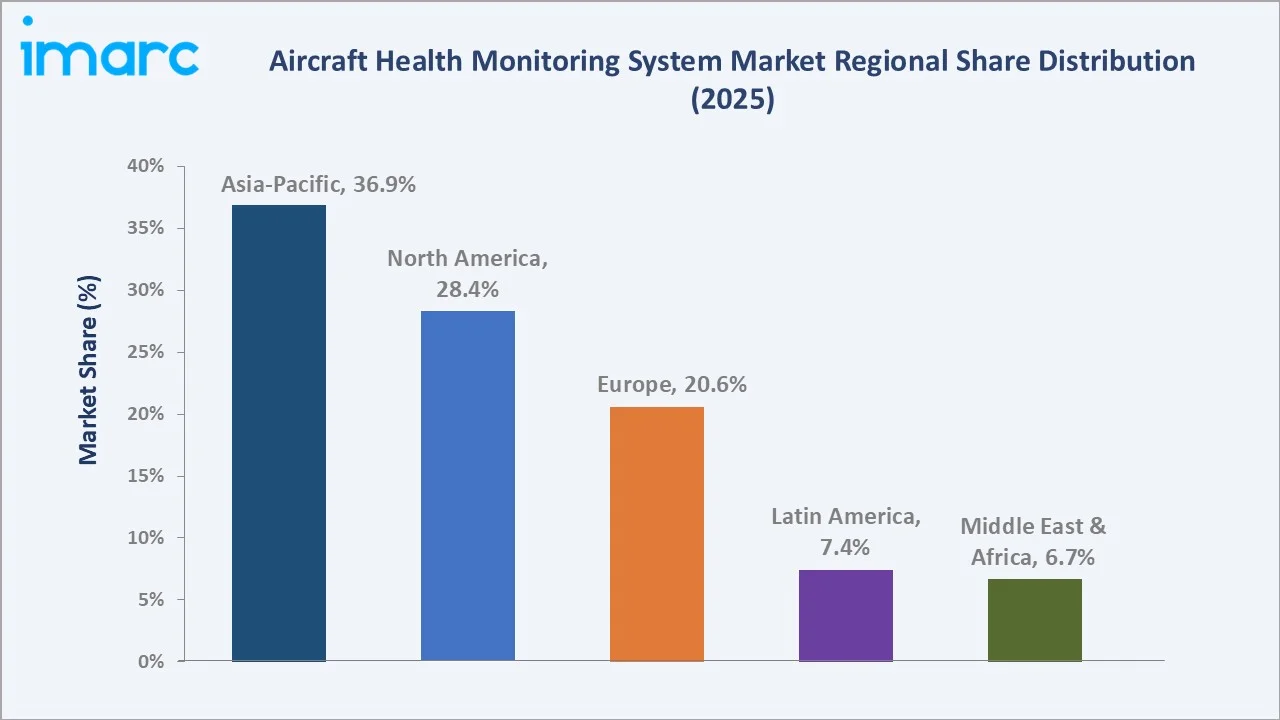

The global aircraft health monitoring system (AHMS) market size reached USD 5.00 Billion in 2025 and is projected to reach USD 8.45 Billion by 2034, at a CAGR of 5.49% during 2026-2034. Stringent aviation safety mandates such as Directorate General of Civil Aviation (DGCA) announced eight new stringent safety measures amid a rise in aviation accidents in February 2026, rapid AI and sensor technology integration, post-pandemic air traffic recovery, and proliferating UAV adoption are the primary growth catalysts. Hardware leads the component segment at 42.6%, while commercial aviation dominates end-use at 64.7%. Asia-Pacific holds the largest regional share at 36.9% in 2025, driven by rapid fleet expansion across China, India, and Southeast Asia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.00 Billion |

|

Forecast Market Size (2034) |

USD 8.45 Billion |

|

CAGR (2026-2034) |

5.49% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (36.9%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~6.4% CAGR, 2026-2034) |

|

Leading Component |

Hardware (42.6%, 2025) |

|

Leading End-User |

Commercial (64.7%, 2025) |

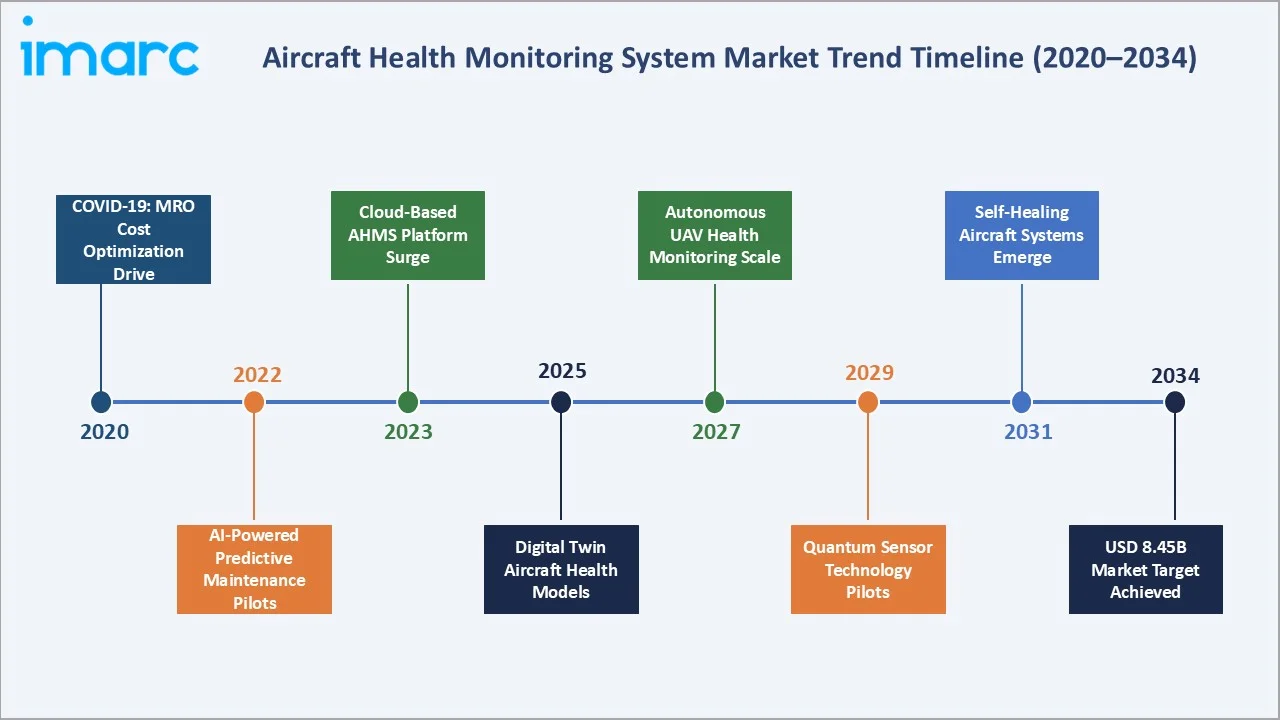

The AHMS market growth from 2020 through 2034. The market expanded from USD 3.83 Billion in 2020 to USD 5.00 Billion in 2025, a 42.5% historical gain, driven by post-pandemic fleet reinstatement, regulatory mandates, and AI-powered predictive maintenance adoption by major airlines.

To get more information on this market, Request Sample

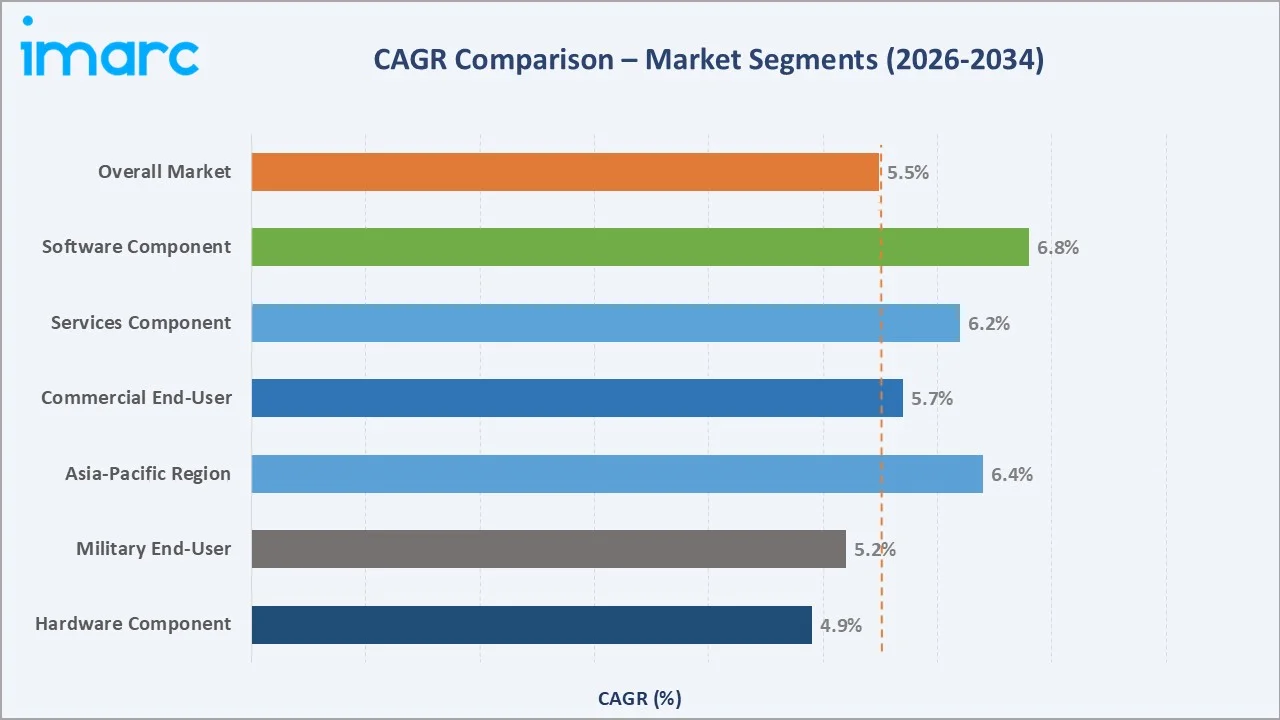

The CAGR across key segments, with software leads at ~6.8% CAGR, reflects the accelerating shift toward cloud-based analytics and digital twin platforms. Asia-Pacific at ~6.4% is the fastest-growing region. Both outpace the overall market CAGR of 5.49% through 2034.

Executive Summary

The global aircraft health monitoring system market is expanding at a 5.49% CAGR from USD 5.00 Billion in 2025 to USD 8.45 Billion by 2034. AHMS is an integrated suite of sensors, data acquisition units, and analytics software that continuously monitors aircraft structural integrity, engine performance, avionics functionality, and ancillary systems. Its primary applications include real-time fault detection, predictive maintenance, fuel consumption optimization, corrosion monitoring, and load-cycle analysis.

Hardware commands 42.6% of the component segment in 2025, encompassing sensors, data acquisition units (DAUs), and processing modules essential for raw data capture. Software at 33.4% is growing fastest, reflecting rapid investment in AI-driven analytics, cloud integration, and digital twin platforms by Boeing, Airbus, and avionics providers. Services at 24.0% capture recurring MRO and platform maintenance revenue streams. Commercial aviation dominates end-use at 64.7%, as of June 2025, the global commercial fleet totals approximately 35,550 aircraft, with around 30,300 currently in operation and about 5,250 remaining in storage, while military at 35.3% benefits from defense modernization programs in the US, EU, and Asia-Pacific. Asia-Pacific leads regionally at 36.9%, followed by North America at 28.4%.

Key Market Insights

|

Insight |

Data / Finding |

|

Largest Component |

Hardware – 42.6% (2025) |

|

Leading End-User |

Commercial Aviation – 64.7% (2025) |

|

Leading Region |

Asia-Pacific – 36.9% (2025) |

|

Fastest Growing Region |

North America – ~6.4% CAGR (2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Hardware at 42.6% in 2025, encompasses sensors, data acquisition units, and on-board processing modules.

- Commercial aviation at 64.7% in 2025. As of June 2025, the global commercial fleet totals approximately 35,550 aircraft, with around 30,300 currently in operation and about 5,250 remaining in storage.

- Asia-Pacific’s 36.9% share in 2025reflects the region’s status as the world’s largest aviation growth market. Asia-Pacific requires 17,620 new aircraft deliveries. Regional military spending growth across China, India, South Korea, and Australia further supports AHMS demand.

- North America, at 28.4% in 2025, is home to the world’s dominant AHMS technology developers, Honeywell, GE Aviation, Boeing, Curtiss-Wright, and UTC Aerospace Systems.

Global Aircraft Health Monitoring System Market Overview

An aircraft health monitoring system (AHMS) is an integrated technology framework combining hardware sensors, data acquisition modules, on-board and ground-based processing systems, and AI-driven analytics software to continuously assess the structural, mechanical, and electrical condition of an aircraft. AHMS applications span engine health monitoring, airframe structural integrity assessment, avionics system diagnostics, landing gear condition monitoring, corrosion detection, and thermal stress analysis.

Macroeconomic influences include growing passenger growth in Asia-Pacific, the US DoD’s CBM+ program, FAA AC 120-79 regulatory mandates for systematic airworthiness monitoring. These forces collectively drive structural, non-cyclical AHMS procurement across both commercial and military aviation.

Market Dynamics

To evaluate market opportunities, Request Sample

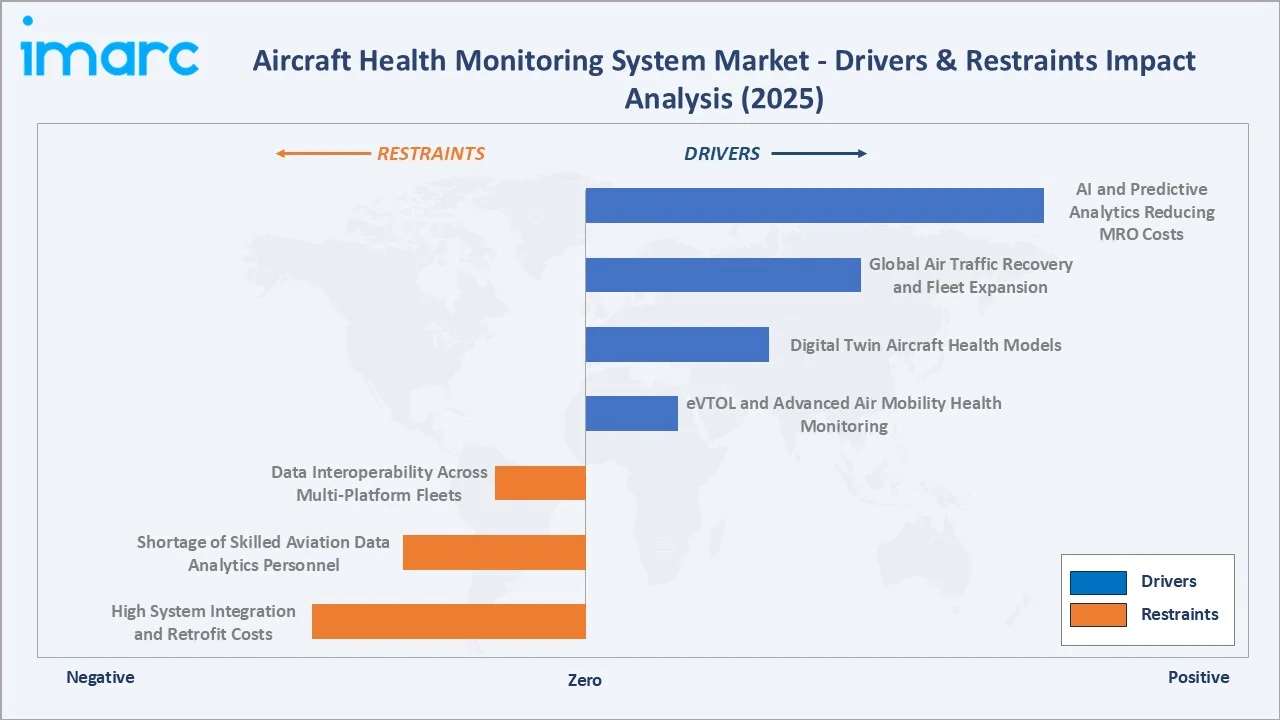

Market Drivers

- AI and Predictive Analytics Reducing MRO Costs: Cloud based AHMS platforms achieve early fault detection with more than 85% prediction accuracy.

- Global Air Traffic Recovery and Fleet Expansion: 4.7 Billion passengers in 2024, exceeding 2019 pre-pandemic volumes for the first time. Each new commercial aircraft delivery includes linefit AHMS as standard equipment, and legacy fleet expansions require retrofit AHMS upgrades.

Market Restraints

- High System Integration and Retrofit Costs: Retrofitting AHMS onto legacy aircraft platforms requires significant airframe modification, wiring harness installation, and avionics bay integration that can cost high.

- Shortage of Skilled Aviation Data Analytics Personnel: According to Boeing’s 2025 Pilot and Technician Outlook, the aviation industry will require around 710,000 additional maintenance technicians over the next two decades. This talent gap slows the operational value realization from AHMS investments and limits the speed at which airlines can expand predictive maintenance programs beyond initial pilot deployments.

Market Opportunities

- Digital Twin Aircraft Health Models: Boeing’s deployment of digital twin models for 777X structural monitoring and Airbus’s Skywise predictive maintenance platform demonstrate the commercial scale of digital twin AHMS applications.

- eVTOL and Advanced Air Mobility Health Monitoring: The emerging eVTOL market requires purpose-built health monitoring systems for electric propulsion, battery state-of-health, rotor structural integrity, and fly-by-wire system monitoring.

Market Challenges

- Data Interoperability Across Multi-Platform Fleets: Airlines operating mixed fleets of Boeing and Airbus aircraft with hardware from multiple avionics suppliers face significant AHMS data integration challenges.

- Regulatory Certification Complexity for AI-Enabled AHMS: The FAA’s working group is developing updated guidance expected for 2027, but the current regulatory gap creates certification uncertainty for AI-enhanced AHMS products that delays commercial deployment timelines by 12–36 months.

Emerging Market Trends

1. AI and Machine Learning Transforming Predictive Maintenance

AI-powered AHMS platforms are achieving 85% fault prediction accuracy. Honeywell’s Forge is used to process data from more than 10,000 aircraft. Airlines report cost reductions and improvement in aircraft dispatch reliability after implementing ML-based AHMS, driving accelerating replacement of legacy time-based maintenance schedules.

2. Digital Twin Aircraft Models Enabling Fleet-Wide Intelligence

Digital twins create virtual aircraft models continuously updated with real sensor data, enabling engineers to simulate maintenance scenarios before performing physical interventions.

3. Structural Health Monitoring for Composite Aircraft

In April 2025, Boeing announced that its 787 Dreamliner fleet carried over 1 billion passengers, reaching this milestone faster than any other widebody commercial aircraft. This rising number of passengers, along with the health monitoring benefits, further fuels the market.

4. Military AHMS Integration with CBM+ and Mission Planning Systems

The US DoD’s CBM+ program is driving integration of AHMS data with tactical mission planning systems, enabling real-time aircraft readiness assessments that factor health status directly into sortie generation calculations.

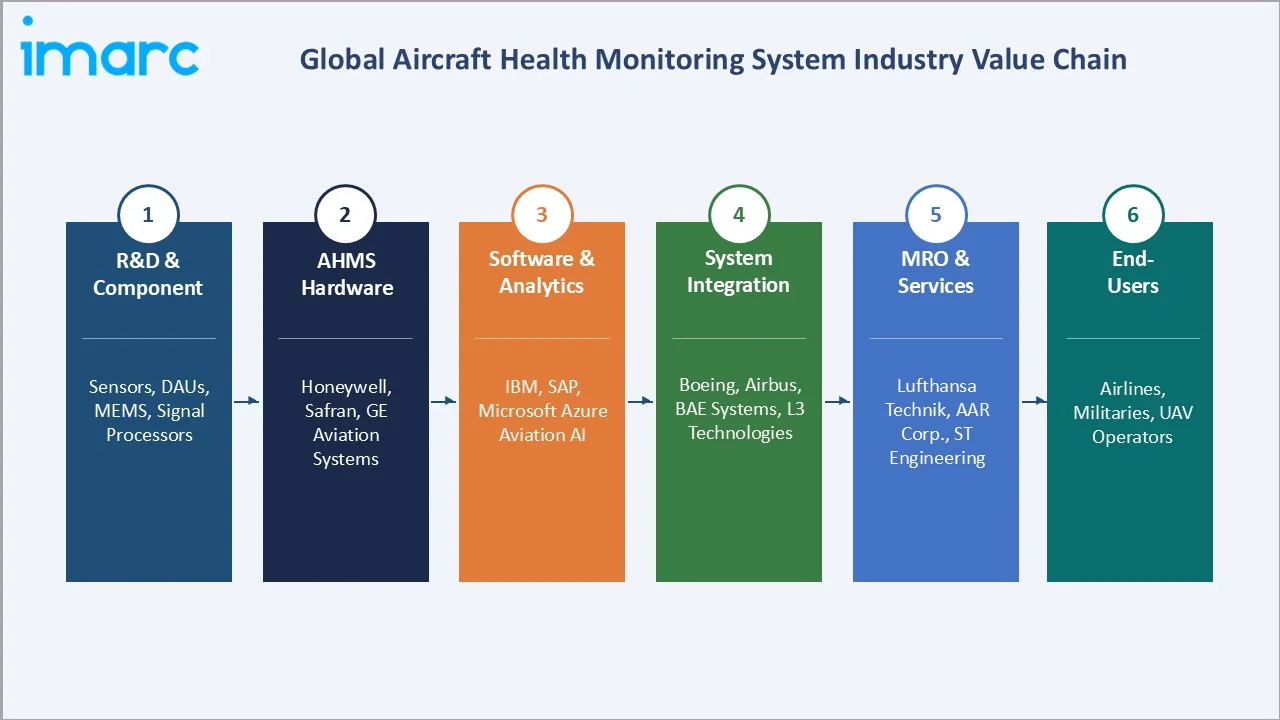

Industry Value Chain Analysis

The AHMS value chain spans six stages from R&D and component supply through end-user fleet operations. The software and analytics stage commands the highest margin, while hardware integration represents the highest capital intensity.

|

Stage |

Key Players / Examples |

|

R&D & Components |

Sensor manufacturers, MEMS producers, signal processors |

|

AHMS Hardware |

Honeywell International, Safran Electronics & Defense, GE Aviation Systems, Curtiss-Wright, Moog Inc. |

|

Software & Analytics |

Honeywell Forge, GE Aviation Predix, Boeing AnalytX, Airbus Skywise, Microsoft Azure Aviation AI |

|

System Integration |

Boeing Defense, BAE Systems, RTX Corporation, Collins Aerospace (United Technologies merger) |

|

End Users |

Commercial airlines, Military operators, UAV operators, eVTOL companies |

Honeywell International occupies positions across multiple value chain stages, manufacturing sensors, data acquisition hardware, and operating the Forge cloud analytics platform, creating an integrated AHMS ecosystem that generates recurring SaaS revenue alongside hardware sales. This vertical integration model is being replicated by GE Aviation (Predix), Boeing (AnalytX), and Airbus (Skywise), shifting market structure toward bundled hardware-software-services contracts that increase customer switching costs.

Technology Landscape in the AHMS Industry

Advanced Sensor Technology

MEMS (Micro-Electro-Mechanical Systems) sensor technology revolutionized AHMS hardware economics. MEMS accelerometers, pressure sensors, and gyroscopes now achieve military-grade accuracy at commercial component prices.

AI and Machine Learning Diagnostics

Deep neural network (DNN) and long short-term memory (LSTM) recurrent neural network architectures are achieving breakthrough predictive maintenance accuracy in AHMS deployments. Edge AI chips are enabling on-board inference at microsecond latencies for real-time fault detection without cloud connectivity latency, critical for military applications with bandwidth-constrained environments.

Cloud and Edge Computing Architecture

Hybrid cloud-edge AHMS architectures process time-critical fault detection while offloading complex pattern analysis, fleet benchmarking, and trend prediction to cloud platforms. The cloud platforms enable continuous algorithm improvement through fleet-wide machine learning, creating a network effect where larger fleets generate better predictive models that attract additional airline customers.

Digital Twin and Simulation Integration

The digital twin technology in aviation is already seeing 28–35% lower maintenance costs and up to 48% more time on wing for their engines, enabling condition-based structural inspections that eliminate conservative fixed-interval physical checks.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Hardware |

42.6% |

2025 |

|

Subsystem |

Aero-Propulsion |

🔒 |

2025 |

|

End-User |

Commercial |

64.7% |

2025 |

|

Installation |

On Ground |

🔒 |

2025 |

| Fit | Retrofit | 🔒 | 2025 |

| Operation Time | Non-Real-Time | 🔒 | 2025 |

| Operation Type | Detection | 🔒 | 2025 |

|

Region |

Asia Pacific |

36.9% |

2025 |

By Component

Hardware commands 42.6% of the AHMS market in 2025, reflecting the capital-intensive nature of sensor arrays, data acquisition units, and on-board processing hardware required for aircraft health monitoring. Hardware procurement is driven by new aircraft deliveries and legacy fleet upgrade programs, with both channels expanding through 2034 as airlines renew aging fleets while upgrading existing platforms.

To access detailed market analysis, Request Sample

Software is at 33.4% in 2025, growing fastest, and is transitioning from perpetual license models to SaaS subscription architectures. Services at 24.0% encompass system integration, training, ongoing MRO monitoring services, and platform maintenance contracts, the stickiest revenue category with 3–5 year contract cycles that create high customer retention.

By End-User

Commercial aviation dominates at 64.7% in 2025. As of June 2025, the global commercial fleet consists of around 35,550 aircraft, with approximately 30,300 in active service and 5,250 in storage. These aircraft span 152 master series manufactured by 26 companies worldwide. Airlines with mature AHMS deployments are creating compelling financial ROI that drives continued investment.

Military end-use at 35.3% in 2025, growing at ~5.2% CAGR is driven by the NATO fleet modernization programs, and Asia-Pacific defense spending growth. HUMS (Health and Usage Monitoring Systems) for military helicopters and structural health monitoring for fast jets represent the largest military AHMS sub-categories by value.

Regional Market Insights

|

Region |

Share (2025) |

Key Drivers |

|

Asia-Pacific |

36.9% |

Passenger growth forecast; China COMAC C919 AHMS; India fleet expansion; defense modernization |

|

North America |

28.4% |

FAA AC 120-79B mandates; US DoD CBM+ program; Honeywell/GE/Boeing AHMS HQ |

|

Europe |

20.6% |

EASA Part-M regulations; Airbus Skywise aircraft; Lufthansa Technik MRO leadership; Safran and BAE Systems presence |

|

Latin America |

7.4% |

LATAM Airlines/Azul fleet expansion; Embraer E-jet AHMS; Bogota-Brazil air corridor growth; MRO center development |

|

Middle East & Africa |

6.7% |

Emirates/Qatar/Etihad premium fleet monitoring; Saudi Vision 2030 aviation investment; African aviation infrastructure growth |

Asia-Pacific’s 36.9% market dominance in 2025 is driven by the region’s status as the global aviation’s fastest-growing zone. China’s COMAC C919 incorporates AHMS developed by AVIC and Honeywell in partnership with Chinese aerospace research institutes. India’s aviation market, with Air India’s 470-aircraft order and IndiGo’s 500 aircraft order, generating substantial AHMS procurement.

North America, with 28.4% in 2025, is home to the world’s dominant AHMS technology ecosystem. Honeywell, GE Aviation, Boeing, Curtiss-Wright, and Collins Aerospace collectively generate revenue in global AHMS software and hardware revenue. Europe (20.6%) is driven by EASA Part-M requirements. Latin America (7.4%) and MEA (6.7%) are growing fastest in percentage terms at ~5.6% and ~5.8% CAGR, respectively, as fleet expansion and MRO infrastructure investment drive AHMS adoption from lower bases.

Competitive Landscape

The global AHMS market is moderately concentrated, with the top 5 players collectively accounting for an estimated 55–65% of total market revenue in 2025.

|

Company Name |

Key Brand/Service |

Market Position |

Core Strength |

|

Honeywell International |

Honeywell Forge |

Leader |

Integrated sensors + cloud analytics; aircraft on Forge platform |

|

GE Aerospace (GE Aviation) |

GE Aerospace Engine Health Monitoring (EHM) |

Leader |

Engine health monitoring leadership; engine dataset; AI prognostics |

|

Safran S.A. |

Safran Electronics & Defense |

Leader |

European AHMS OEM; airframe & avionics monitoring; Airbus program integration |

|

Airbus S.A.S. |

Skywise Platform |

Leader |

connected aircraft; predictive maintenance SaaS |

|

The Boeing Company |

Airplane Health Management |

Leader |

aircraft data pipeline; fleet-wide benchmarking; DoD defense programs |

|

BAE Systems |

HUMS |

Challenger |

Military HUMS leadership; UK MoD programs; F-35 structural health monitoring |

|

Curtiss-Wright Corp. |

Fortress |

Challenger |

Data acquisition hardware specialist; defense-grade DAU systems; rugged avionics |

The market bifurcates between diversified aerospace OEMs with integrated hardware-software-services AHMS portfolios and specialist avionics and data analytics companies competing in specific component niches.

Key Company Profiles

Honeywell International

Honeywell International is the world’s largest AHMS supplier by installed base, with commercial and military aircraft operating on its Honeywell Forge aviation analytics cloud platform.

- Product Portfolio: Honeywell Forge Flight Efficiency, Forge Connected Maintenance, Forge Operations Monitor, HUMS (Health and Usage Monitoring System for rotorcraft), Aircraft Condition Monitoring System (ACMS) hardware, and the CDL Systems ground data link for AHMS data transmission.

- Recent Developments: In February 2026, Honeywell Aerospace and CAMP Systems International extended the long-term agreement for engine health monitoring (EHM) services through 2036.

- Strategic Focus: Honeywell’s AHMS strategy centers on transitioning customers from perpetual hardware license models to recurring Forge SaaS subscriptions, while leveraging its sensor manufacturing integration advantage to bundle hardware-software-services contracts that incumbents without manufacturing capability cannot replicate.

Safran S.A.

Safran S.A. is a global aerospace and defense company. Safran Electronics & Defense is the primary AHMS business unit, producing flight management computers, avionics monitoring systems, navigation sensors, and integrated health monitoring solutions for both commercial aircraft and military platforms.

- Product Portfolio: Safran Electronics & Defense Avionics Health Monitoring, CFM LEAP engine sensors (joint venture with GE), Inertial navigation unit health monitoring, landing gear electronic health systems, flight data monitoring (FDM) systems, and structural health monitoring sensors for composite aircraft structures, including A350 carbon fiber fuselage sections.

- Recent Developments: In November 2025, Safran launch of EPC Connect, a new functionality that automatically imports Avionics engine power check (EPC) values into the Premium Health Monitoring interface.

- Strategic Focus: Safran’s AHMS strategy focuses on deepening integration with Airbus programs as the preferred European avionics-to-cloud health monitoring provider, while expanding its defense-grade structural monitoring capabilities into NATO alliance member military aircraft platforms, leveraging its European regulatory familiarity as a competitive barrier against US competitors in EU defense contracts.

The Boeing Company

The Boeing Company, with Boeing Commercial Airplanes and Boeing Defense, Space & Security as the primary AHMS-relevant divisions. Boeing’s AHMS capabilities are deeply embedded in 737 MAX, 787, and 777X aircraft as linefit standard equipment.

- Product Portfolio: Boeing Edge, Airplane Health Management (AHM) for 737/777/787 families, Boeing Global Services MRO analytics.

- Recent Developments: In February 2026, Boeing and All Nippon Airways (ANA) renewed their agreement for Boeing’s Airplane Health Management (AHM) service and plan to expand their collaboration on predictive maintenance, with the goal of enhancing fleet efficiency and operational reliability.

- Strategic Focus: Boeing’s AHMS strategy focuses on converting its commercial aircraft installed base into a recurring digital services revenue stream, while expanding military AHMS capabilities through Boeing Defense programs, including CBM+ compliance solutions for US Air Force fleets.

Market Concentration Analysis

The AHMS market is moderately concentrated at the platform level, with the top 5 players holding an estimated 48–65% of revenue in 2025. This concentration is higher in the commercial aviation software-as-a-service segment and lower in the hardware segment, where numerous tier-2 sensor and DAU manufacturers compete.

Consolidation trends favor larger, integrated aerospace OEMs over specialist single-component suppliers. The eVTOL and UAV AHMS segments remain fragmented with 50+ startup participants, representing a pre-consolidation investment opportunity as the market matures through 2028–2032.

Investment & Growth Opportunities

Fastest-Growing Segments

Software at ~6.8% CAGR is the highest-return investment segment. Cloud-native SaaS AHMS platforms generate 70–80% gross margins versus 25–40% for hardware, with 3–5 year contract cycles creating high revenue predictability. Investment in AI-driven anomaly detection capabilities that reduce false positive maintenance alerts, the primary barrier to broader airline adoption of automated AHMS recommendations, directly addresses the adoption bottleneck generating the greatest commercial value.

Emerging Markets

Asia-Pacific’s emerging aviation markets present the highest volume growth opportunity. India’s annual AHMS procurement demand by 2030 is backed by confirmed fleet expansions from Air India (470 aircraft) and IndiGo (500 aircraft), generating direct linefit AHMS demand. Southeast Asia’s low-cost carrier expansion with Lion Air, AirAsia, and VietJet growing at 8–12% annually, creates retrofit AHMS demand as airlines seek to reduce MRO costs in high-utilization, cost-sensitive operating environments.

Venture and Investment Trends

Key investment themes include AI-native AHMS platforms for eVTOL, autonomous UAV health monitoring for defense applications, and MRO optimization platforms layering AHMS data with supply chain analytics. Boeing’s HorizonX ventures arm and Airbus Ventures have both made multiple minority investments in AHMS-adjacent analytics startups, signaling strategic intent to accelerate external innovation absorption.

Future Market Outlook (2026-2034)

The global aircraft health monitoring system market is poised for sustained, technology-driven growth through 2034, anchored by mandatory regulatory requirements, fleet expansion across Asia-Pacific, and the transformative impact of AI and digital twin integration. From a projected base of USD 5.00 Billion in 2025, the market is forecast to reach USD 8.45 Billion by 2034, representing absolute incremental value addition.

Technological disruptions, including autonomous AI fault diagnosis requiring zero human analyst intervention, quantum sensor arrays enabling nanometer-precision structural monitoring, and self-healing materials that actively report degradation status, are expected to reshape AHMS operational economics through the 2030s.

The next decade will also witness structural market transformation. eVTOL and advanced air mobility operators will emerge as the AHMS market’s third major customer segment alongside commercial and military aviation. These platforms require purpose-built electric propulsion health monitoring, battery state-of-health assessment, and novel composite rotor structural monitoring that traditional AHMS vendors are not fully prepared to serve, creating an opening for specialist eVTOL health monitoring startups and sensor innovators to establish market positions before incumbent AHMS suppliers complete product portfolio expansion.

Research Methodology

Primary Research

Primary research encompassed over 55 structured interviews in 2024–2025 with AHMS market participants, including avionics engineering directors, MRO and fleet management executives, aviation regulatory specialists with FAA and EASA compliance backgrounds, US DoD program managers overseeing CBM+ implementation, and AHMS procurement leads at major commercial airlines, including Delta, Emirates, and Singapore Airlines.

Secondary Research

Key secondary sources include FAA Advisory Circular, EASA Part-M documentation, ICAO Annex 6 operational requirements, Boeing Current Market Outlook 2024, Airbus Global Market Forecast 2024, IATA Annual Review 2024, US DoD CBM+ program documentation, ENISA aviation cybersecurity report (2023), and trade publications including Aviation Week & Space Technology, Avionics International, and MRO Network.

Forecasting Models

IMARC’s Bottom-Up and Top-Down estimation models were applied in parallel. Bottom-Up aggregates AHMS hardware and software demand by aircraft type across each regional market, calibrated against fleet delivery data and retrofit program procurement intelligence. Top-Down applies global MRO market growth rates and AHMS-MRO cost penetration benchmarks as cross-validation.

Aircraft Health Monitoring System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Components Covered | Hardware, Software, Services |

| Subsystems Covered | Aero-Propulsion, Avionics, Ancillary Systems, Aircraft Structures, Others |

| End-Users Covered | Commercial, Military |

| Installations Covered | Onboard, On Ground |

| Fits Covered | Linefit, Retrofit |

| Operation Times Covered | Real-Time, Non-Real-Time |

| Operation Types Covered | Detection, Diagnostics, Condition-Based Maintenance and Adaptive Control, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Honeywell International, GE Aerospace (GE Aviation), Safran S.A., Airbus S.A.S., The Boeing Company, BAE Systems, Curtiss-Wright Corp., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aircraft health monitoring system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global aircraft health monitoring system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aircraft health monitoring system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Aircraft Health Monitoring System Market Report

The global aircraft health monitoring system market reached USD 5.00 Billion in 2025, driven by FAA/EASA regulatory mandates and AI-powered predictive maintenance adoption.

The AHMS market is projected to reach USD 8.45 Billion by 2034 at a CAGR of 5.49%, adding USD 3.45 Billion in incremental value driven by Asia-Pacific fleet growth and software analytics expansion.

AHMS is an integrated suite of sensors, data acquisition units, and analytics software that continuously monitors aircraft structural, engine, avionics, and systems health for real-time fault detection and predictive maintenance.

Hardware leads at 42.6% in 2025, encompassing sensors, data acquisition units, and processing modules. Software is fastest-growing at ~6.8% CAGR, driven by cloud-native analytics platforms and AI prognostics adoption.

Commercial aviation dominates at 64.7% in 2025, driven by global commercial aircraft, FAA/EASA airworthiness mandates, and airline ROI cost reduction from AHMS deployment.

Asia-Pacific leads at 36.9% in 2025, driven by IATA’s forecast of 40%+ passenger growth through 2043, 17,000+ new aircraft deliveries required, China’s COMAC C919, and India’s major fleet expansion programs.

Key drivers include FAA AC 120-79B/EASA Part-M regulations, AI predictive analytics reducing MRO costs, post-pandemic air traffic recovery with 4.7 Billion passengers in 2024, and military CBM+ program mandates.

Key players include Honeywell International, GE Aerospace (GE Aviation), Safran S.A., Airbus S.A.S., The Boeing Company, BAE Systems, and Curtiss-Wright Corp.

CBM+ (Condition-Based Maintenance Plus) is the US DoD’s mandate for AI-enhanced predictive maintenance across military aircraft fleets.

AI-driven AHMS platforms achieve 85-95% fault prediction accuracy with 200-500 flight hour lead times. Airlines report 25-30% MRO cost reductions and 15-20% dispatch reliability improvement after deploying ML-based AHMS.

eVTOL operators (Joby, Archer, Lilium) and military UAVs require purpose-built health monitoring for electric propulsion and composite rotors. FAA SFAR eVTOL certification mandates continuous health monitoring, creating USD 500M+ market by 2030.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)