Aluminium Powder Market Size, Share, Trends and Forecast by Technology, End-Use, Raw Material, and Region 2026-2034

Global Aluminium Powder Market Size, Share, Trends & Forecast (2026-2034)

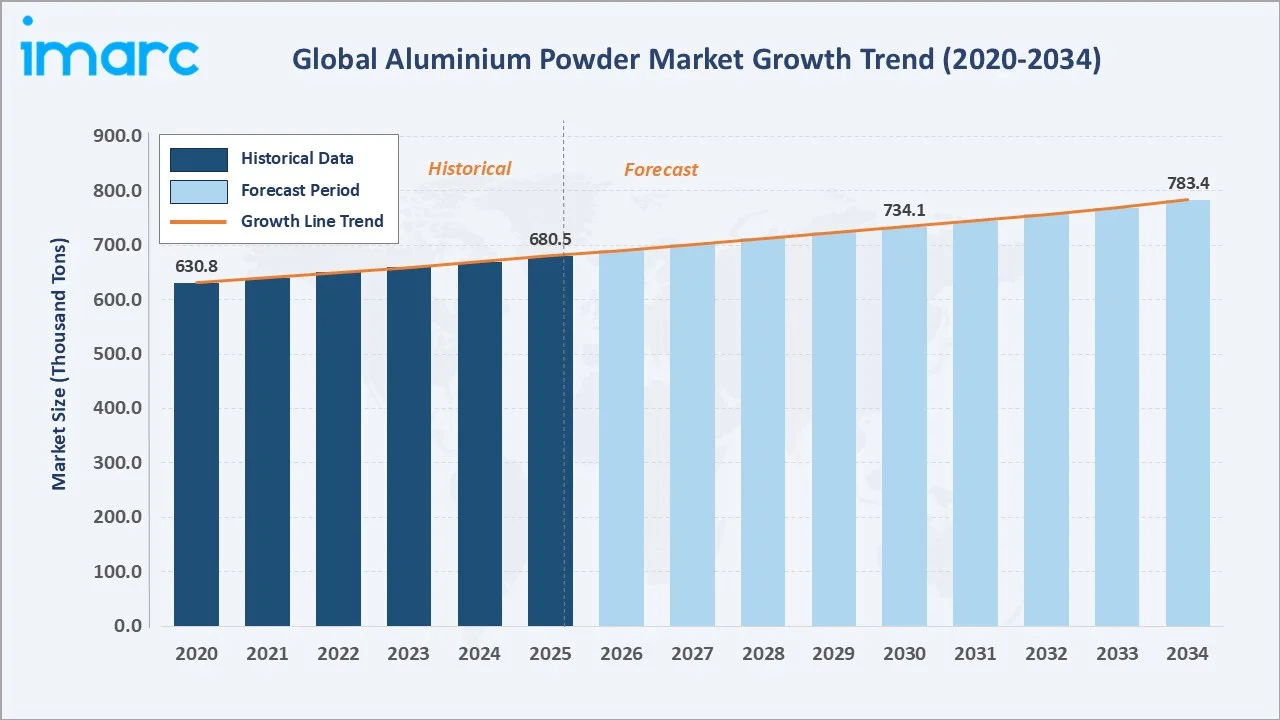

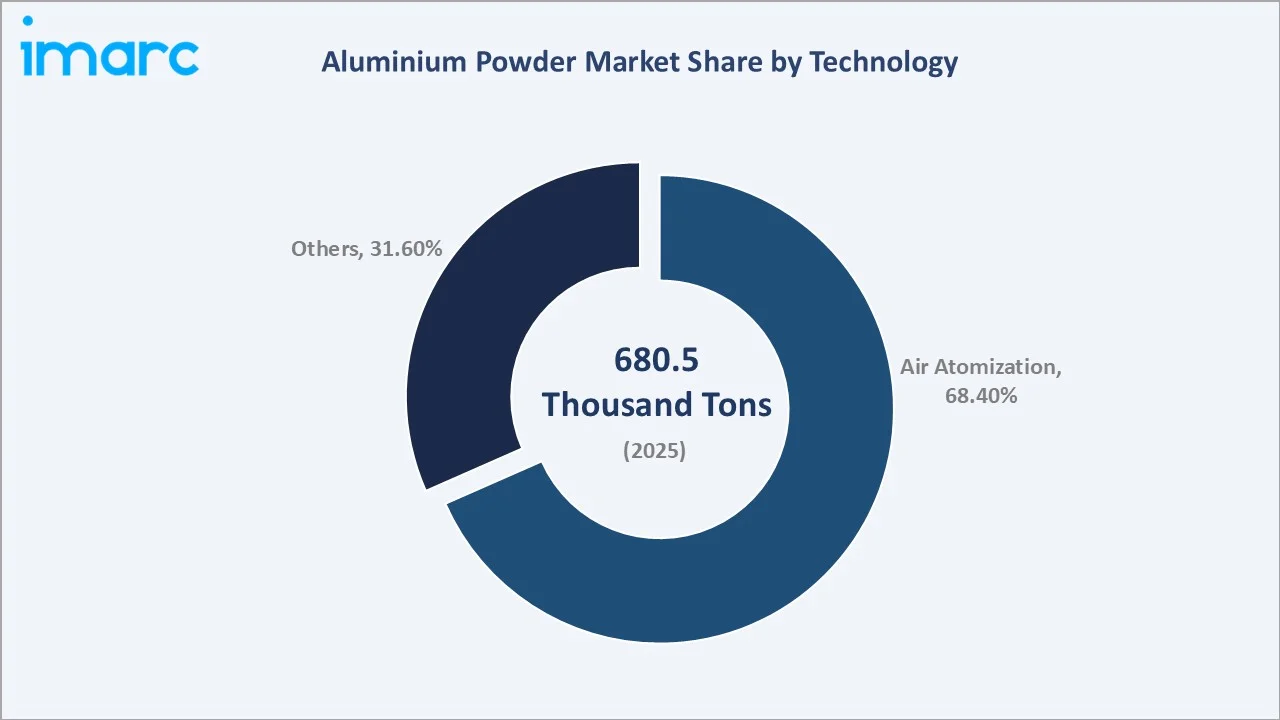

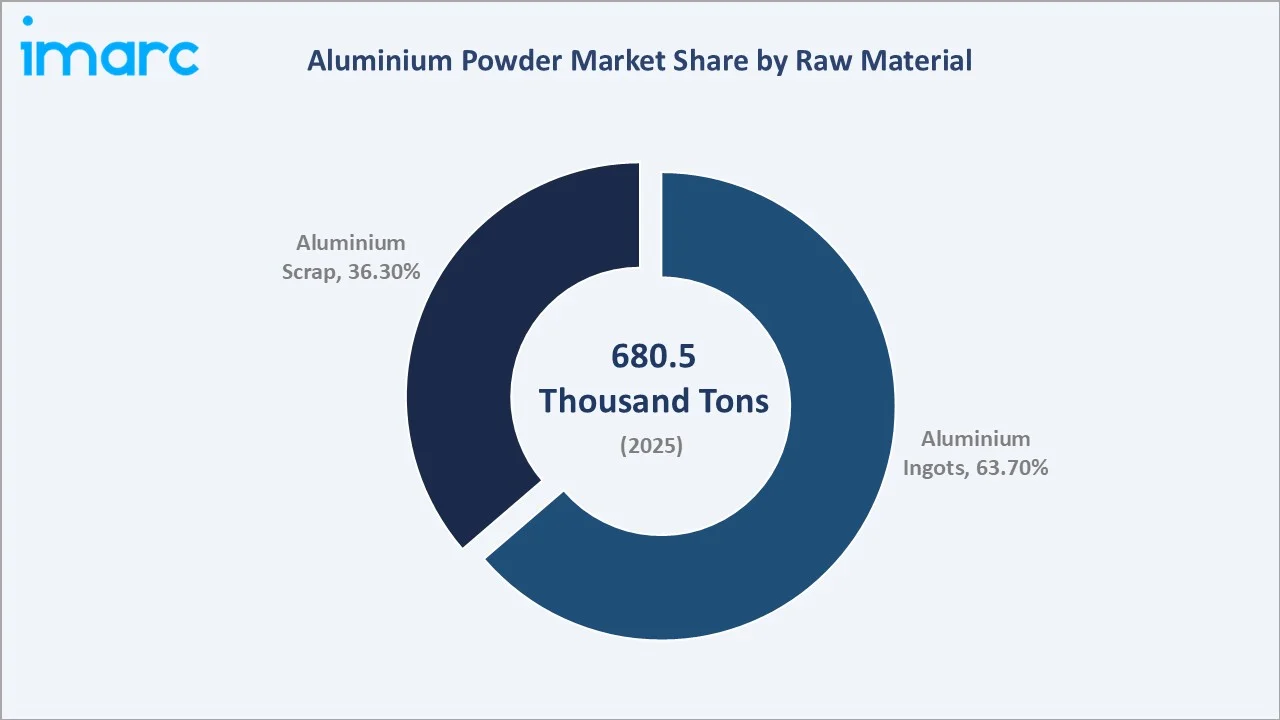

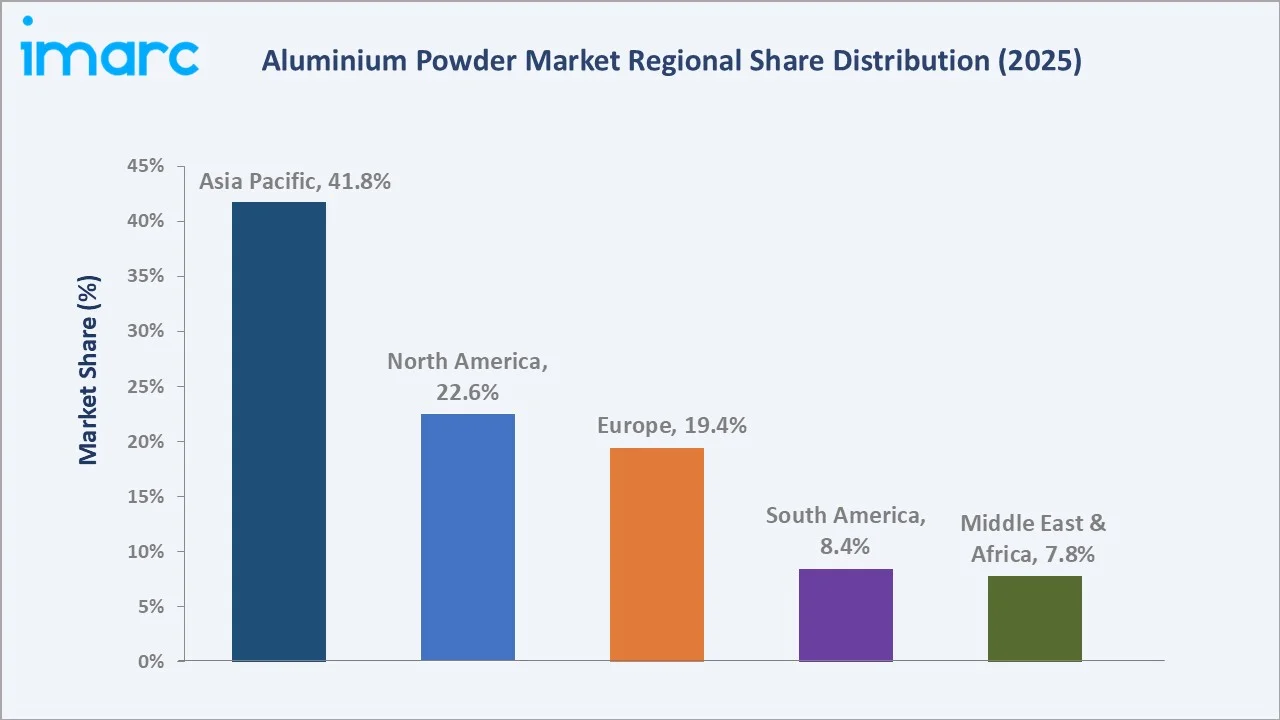

The global aluminium powder market reached a volume of 680.5 Thousand Tons in 2025 and is projected to reach 783.4 Thousand Tons by 2034, expanding at a CAGR of 1.5% during 2026-2034. Demand is driven by rising aerospace and defence spending, automotive lightweighting mandates, rapidly scaling additive manufacturing applications, and rising production, with annual world production of aluminum powders amounts to over 100,000 metric tons. Air atomization technology dominates at 68.4% of production volume (2025), while aluminium ingots remain the primary raw material at 63.7%. Asia Pacific leads all regions with a 41.8% volume share.

Market Snapshot

|

Metric |

Value |

|

Market Volume (2025) |

680.5 Thousand Tons |

|

Forecast Market Volume (2034) |

783.4 Thousand Tons |

|

CAGR (2026-2034) |

1.5% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest and Fastest Region |

Asia Pacific (41.8%, 2025, CAGR ~2.0%, 2026-2034) |

The aluminium powder market volume from 2020 through 2034, expanded from 630.8 Thousand Tons in 2020 to 680.5 Thousand Tons in 2025, anchored at 734.1 Thousand Tons in 2030 before reaching 783.4 Thousand Tons by 2034.

To get more information on this market, Request Sample

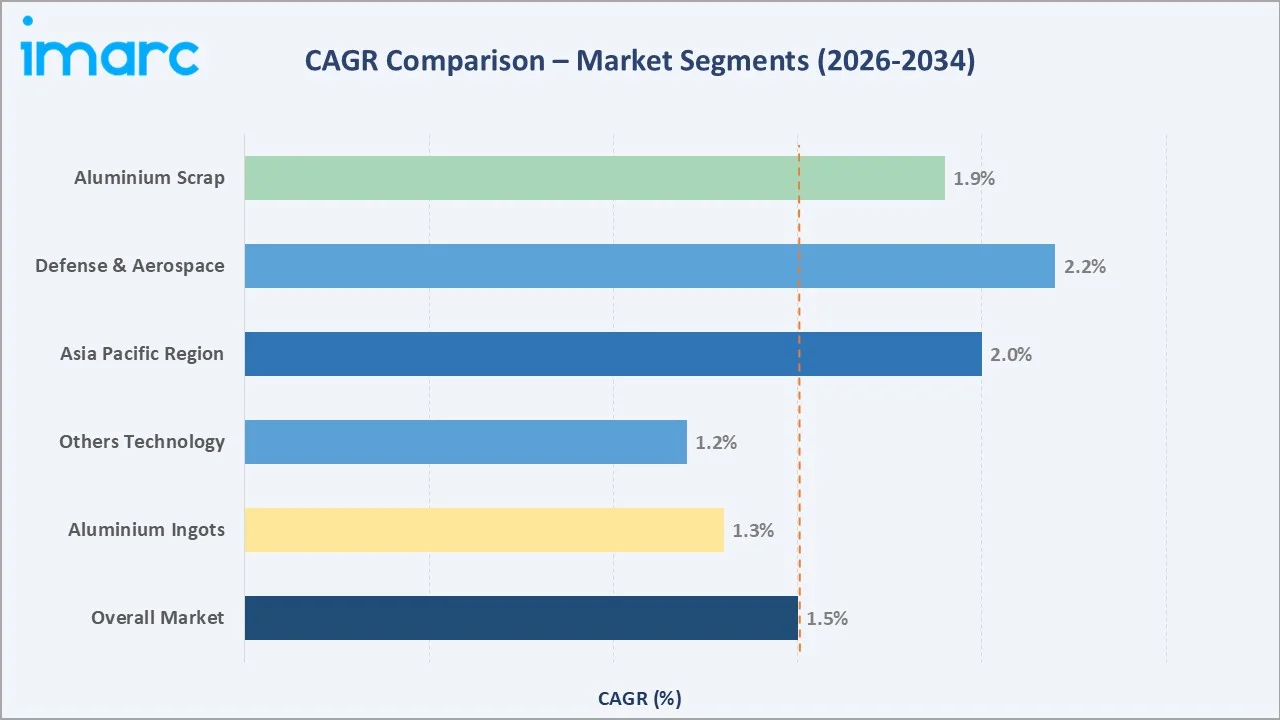

The overall market CAGR is 1.5%, the aluminium scrap segment is growing at a CAGR of 1.9%, and the Asia Pacific region is growing at 2.0% CAGR.

Executive Summary

The global aluminium powder market exhibits steady, end-use-demand-driven growth across a diversified application base. From 630.8 Thousand Tons in 2020, the market volume grew to 680.5 Thousand Tons in 2025, registering consistent gains anchored by construction, explosives, and chemical industry demand in the Asia Pacific. The forecast period (2026–2034) targets 783.4 Thousand Tons, with growth momentum increasingly driven by rising aluminium production, with 5,713 thousand metric tons of aluminium produced by February 2026, high-value applications, aerospace-grade powder for additive manufacturing, nano-aluminium for solid propellants, and aluminium powder as a prospective hydrogen carrier for clean energy applications.

Air atomization remains the technological backbone of production at 68.4% share (2025), prized for producing consistent spherical particles across the 10–150 micron range required by most industrial applications. Aluminium scrap-based production at 36.3% is the fastest growing raw material segment at ~1.9% CAGR through 2034, driven by circular economy policies in Europe and cost optimization by producers managing aluminium commodity price cycles.

Asia Pacific commands a 41.8% volume share (2025), led by China’s construction explosives demand and India’s rapidly expanding defence and aerospace manufacturing base. North America follows at 22.6%, anchored by Alcoa’s domestic production and the U.S. defence industrial base’s demand for MIL-SPEC aluminium powder grades. Europe at 19.4% benefits from stringent ATEX-certified production standards that create barriers to entry while supporting premium pricing for specialty grades.

Key Market Insights

|

Insight |

Data |

|

Dominant Technology |

Air Atomization – 68.4% share (2025) |

|

Leading Raw Material |

Aluminium Ingots – 63.7% share (2025) |

|

Leading and Fastest Region |

Asia Pacific – 41.8% volume share (2025) |

Key Analytical Observations Supporting The Above Data:

- Air atomization dominates at 68.4% (2025): The process produces highly spherical particles with controlled particle size distribution (D50 of 10–150 microns), critical for flowability in additive manufacturing and consistent burn rates in explosives.

- Aluminium Ingots lead raw materials at 63.7% (2025): Primary aluminium ingots deliver superior purity, essential for aerospace, defence, and electronic applications where contaminant levels must meet strict specification limits. The rising consumption, with the inventory of aluminium ingots at major domestic consumption hubs, stood at 468,000 metric tonnes as of Jun 30, 2025, driving the segment growth.

- Asia Pacific’s 41.8% volume share (2025): China alone accounts for approximately 55–60% of Asia Pacific demand, driven by ammonium nitrate fuel oil (ANFO) explosive consumption in mining, aluminium-based aerated concrete (AAC) block production, and growing automotive parts manufacturing requiring sintered aluminium powder components.

Global Aluminium Powder Market Overview

Aluminium powder is a finely divided form of aluminium metal produced through atomization of molten aluminium or mechanical milling of aluminium foil and flake. Products range from coarse industrial-grade powders (>100 micron) used in construction, explosives, and chemical applications to ultra-fine spherical powders (<10 micron) manufactured to MIL-SPEC standards for solid rocket propellants and precision additive manufacturing. The aluminium powder market sits within the broader non-ferrous metal powder industry, which serves as a critical input across aerospace, defence, automotive, construction, and advanced manufacturing industries globally.

The global aluminium consumption in 2024 is 72.6 metric tons, with aluminium powder representing a high in total aluminium consumption. Macroeconomic drivers are multifaceted; defence spending growth, infrastructure construction in Asia, automotive lightweighting regulatory mandates, and industrial digitization through additive manufacturing all create distinct demand vectors with differing growth rates and price sensitivity profiles.

Market Dynamics

To evaluate market opportunities, Request Sample

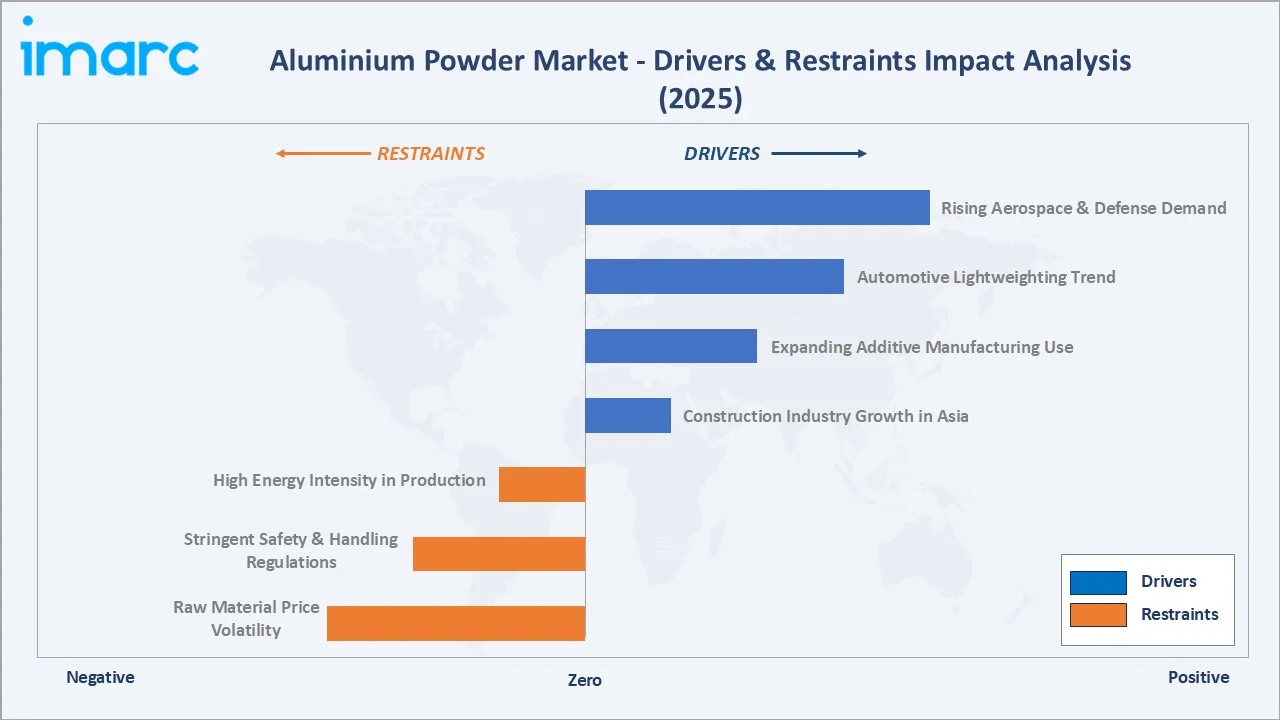

Market Drivers

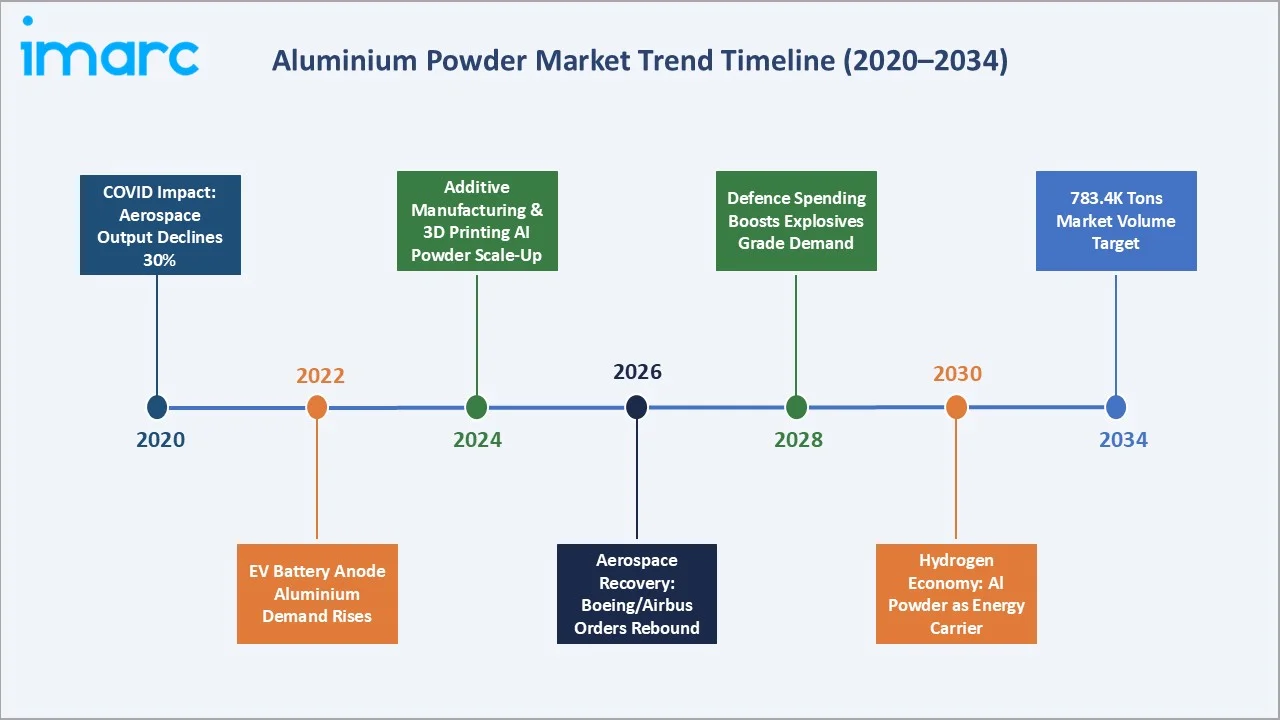

- Rising Aerospace and Defence Spending: Global defence budgets reached USD 2.2 trillion in 2023, a 9% increase, with NATO members accelerating military procurement.

- Automotive Lightweighting and Sintered Parts: Euro 7 emissions standards (2025) and U.S. CAFE 2026 targets mandate weight reduction in passenger vehicles.

- Additive Manufacturing Scale-Up: Aerospace AM parts production is growing at 22% annually, with AlSi10Mg and AlSi12 powder bed fusion alloys as the dominant aluminium grades.

- Construction Growth in Asia Pacific: Autoclaved Aerated Concrete (AAC) block production, a major aluminium powder application, is growing rapidly in China and India.

Market Restraints

- Raw Material Price Volatility: Aluminium LME pricing reached USD 2,800 in 2025, directly impacting powder production costs. Aluminium powder carries a manufacturing premium over ingot price, making cost management critical.

- Stringent Safety and Handling Regulations: Aluminium powder is classified as a combustible dust under OSHA 29 CFR 1910.272 and an explosive atmosphere risk under EU ATEX Directive 2014/34/EU. Compliance requires substantial capital investment in explosion-proof facilities, nitrogen inerting systems, and static electricity controls.

Market Opportunities

- Nano-Aluminium for Advanced Energetics and Propulsion: Nano-aluminium powder (< 100 nm particle size) offers less times the burn rate of micron-scale grades, enabling more compact solid rocket motors and enhanced energetic formulations.

- Emerging Market Infrastructure Demand: South America and Middle East & Africa growing rapidly, outpacing the global average. Mining expansion in Chile and Peru, Saudi Vision 2030 construction programs, and Sub-Saharan Africa infrastructure investment create incremental demand for industrial and explosives-grade aluminium powder.

Market Challenges

- Substitution Threats in Some Applications: In certain coatings and pigment applications, aluminium powder faces substitution pressure from zinc flake, silver-coated particles, and carbon-based conductive materials.

- Quality Certification Complexity: Aerospace and defence customers require powder qualification per AS9100, AMS (Aerospace Material Specifications), and in some cases MIL-DTL specifications with lot-by-lot certification.

Emerging Market Trends

1. Additive Manufacturing Creating Premium Powder Tier

Laser Powder Bed Fusion (LPBF) and Directed Energy Deposition (DED) processes require aluminium powder with a D50 of 15–45 microns. These specifications exclude most industrial-grade production and require dedicated atomization lines with inert gas environments.

2. Aluminium Scrap-Based Production Circular Economy Expansion

EU’s Critical Raw Materials Act (2024) and Corporate Sustainability Reporting Directive create regulatory pressure on industrial users to source materials with documented recycled content.

3. Defence Sector Demand Surge Post-2022

NATO countries’ post-2022 defence spending acceleration is generating the largest backlog of ammunition and energetics orders since the Cold War. Aluminium powder consumption in solid propellants, incendiary ammunition, and illuminating flares is growing.

4. Hydrogen Economy Positioning

Several European energy companies and academic consortia are advancing aluminium powder as a storable, transportable fuel that generates hydrogen on demand via reaction with water (2Al + 3H₂O → Al₂O₃ + 3H₂).

5. AI-Driven Particle Size Optimization in Atomization

Leading producers are deploying machine learning models to optimize atomization process parameters in real time, adjusting gas pressure, melt temperature, and nozzle geometry to achieve target particle size distributions within ±5% of specification.

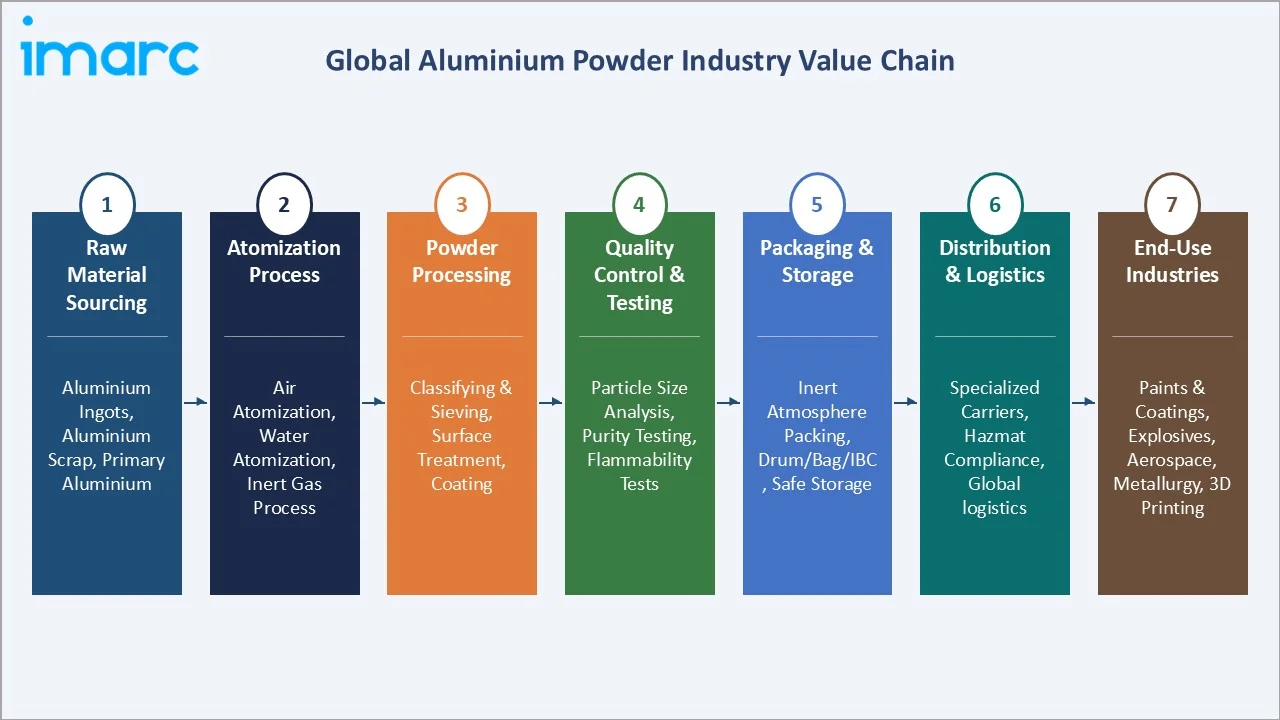

Industry Value Chain Analysis

The aluminium powder industry value chain extends from bauxite mining and primary smelting through to highly specialized end-use manufacturing applications. Each stage involves distinct technical capabilities, capital requirements, and regulatory compliance frameworks.

|

Stage |

Key Players / Examples |

|

Bauxite Mining & Alumina Refining |

Alcoa, Rio Tinto, Norsk Hydro, UC RusAL, Chalco (China) |

|

Aluminium Ingot & Scrap Supply |

Ingot producers, scrap collectors, metal recyclers worldwide |

|

Aluminium Powder Manufacturing |

Toyal America, AMG Alpoco, MEPCO, Valimet |

|

Quality Testing & Certification |

ISO 9001/14001, ISO/IEC 17025 accredited labs, customer QC approval |

|

Distribution & Trading |

Industrial distributors, chemical traders, export agents, brokers |

|

End-Use Industries |

Automotive, aerospace/defence, construction, explosives, chemicals, additive mfg. |

The aluminium powder manufacturing stage captures the highest value-added layer in the chain, with premium specialty grades for aerospace and defence commanding 10–20× the price per kilogram of commodity construction-grade powder. Distribution and logistics represent the most operationally complex layer due to combustible dust safety regulations governing storage, transportation, and handling at every point in the supply chain.

Technology Landscape in the Aluminium Powder Industry

Air Atomization Technology

Air atomization, the dominant production method at 68.4% market share (2025), forces molten aluminium through a nozzle into a high-velocity air stream, shattering the melt into fine droplets that solidify as spherical powder particles.

Inert Gas Atomization for Aerospace Grades

Nitrogen and argon gas atomization is used for aerospace-grade aluminium alloy powders (AlSi10Mg, AA6061, AA2024) where oxygen content must remain below 0.1% and particle morphology must meet LPBF machine requirements.

Nano-Aluminium Synthesis

Aluminium nanoparticles are produced via wet mechanical milling, with the particle size of nano-aluminium powder being about 10 nm under optimized conditions. Nano-aluminium offers dramatically higher surface area and reaction rates, critical for energetic formulations, propellants, and thermite compositions.

Market Segmentation Analysis

By Technology

Air atomization dominates with 68.4% market share (2025). The process’s versatility, energy efficiency versus gas atomization, and ability to produce consistent industrial-grade powder at scale make it the preferred technology for construction, explosives, and chemical applications.

To access detailed market analysis, Request Sample

Other technologies at 31.6% (2025) include gas atomization (aerospace and AM grades), mechanical milling (pigment and flake), and electrolytic production (ultra-fine grades). Gas atomization is the fastest-growing technology segment at ~2.5% CAGR through 2034, driven by additive manufacturing demand growth exceeding 20% annually in aerospace applications.

By Raw Material

Aluminium ingots command 63.7% market share (2025). Primary ingot feedstock enables production of high-purity powder (99.5%+ Al) meeting exacting specifications for aerospace, defence, and advanced manufacturing. The inventory of aluminium ingots at major domestic consumption hubs stood at 468,000 metric tonnes as of June 30, 2025.

Aluminium scrap holds 36.3% market share (2025) and is growing at ~1.9% CAGR through 2034, slightly faster than ingot-based production. Over 100 Mt (million metric tons) of aluminium are currently produced annually, of which ~35% comes from scrap while ~40% has already been scrapped somewhere during production.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

41.8% |

China construction boom, India defence aluminium, SE Asia automotive growth, Japanese precision parts |

|

North America |

22.6% |

U.S. aerospace MRO demand, additive manufacturing adoption, explosives (ANFO) production, defence contracts |

|

Europe |

19.4% |

Germany automotive lightweighting, Nordic defence, UK construction, EU additive manufacturing adoption |

|

South America |

8.4% |

Brazil mining and construction demand; Argentina explosives sector; Chile copper-related chemical use |

|

Middle East & Africa |

7.8% |

UAE construction and defence; Saudi Vision 2030 industrial growth; South Africa mining explosives |

Asia Pacific’s 41.8% volume share (2025) is anchored by China’s extraordinary construction and mining industry consumption. China’s annual AAC block production, India’s growing base, with defence aluminium powder demand growth, driven by Make in India Indigenization programs, is the most dynamic sub-regional growth opportunity.

North America’s 22.6% share (2025) reflects the U.S.’s leadership in defence and aerospace aluminium powder consumption. The U.S. defence industrial base is the world’s largest consumer of military-specification aluminium powder for solid propellants, pyrotechnics, and incendiary formulations. Europe at 19.4% (2025), operates the world’s most technically advanced aluminium powder industry in terms of specialty grade development.

Competitive Landscape

The global aluminium powder market is moderately fragmented, with no single producer controlling more than 15–18% of global volume. The top three producers, Alcoa, RusAL, and AMG Critical Materials, collectively account for approximately 35–40% of global production capacity.

|

Company Name |

Brand / Product Line |

Market Position |

Core Strength |

|

Alcoa Corporation |

Industrial grade aluminium powder |

Market Leader |

World’s leading integrated aluminium company, a bauxite/alumina/aluminium metal producer |

|

RusAL |

G-00 smelter-grade alumina |

Market Leader |

One of the world’s largest aluminium producer |

|

Toyal America Inc. |

Aluminum Alloy Powders for Additive Manufacturing and Cold Spray, Atomized Aluminum Powders, and Aluminum Powders and Aluminum Nitride for Thermal Management |

Strong Challenger |

Subsidiary of Toyo Aluminium; premium aluminium pigment and powder |

|

AMG Critical Materials N.V. |

Gas Atomized Aluminum Powders, Air atomized Aluminum Powders, Aluminum Alloys & Flux Powders (AMG Alpoco) |

Specialist Leader |

Military and explosives-grade aluminium powder expertise |

|

THE METAL POWDER COMPANY LIMITED (MEPCO) |

Atomized Aluminium Powder, Spherical Aluminium Powder, Aluminium Alloy Powder, Ferro Aluminium Powder, Leafing Aluminium Powder, Non-Leafing Aluminium Powder, Colored Aluminium Powder, Aluminium Powder For Pesticides, Aluminium Powder For Light Weight Concrete, Aluminium Powders For Fireworks, Slurries (Civil Explosives), Defence Applications |

Established |

India’s leading aluminium powder manufacturer, cost-competitive supply for explosives and construction in Asia |

|

Kymera International |

Aluminium Alloyed Powder and Pre-Mixed Powder |

Emerging Global |

Advanced metal powder specialist, additive manufacturing and aerospace-grade Al powder |

|

VALIMET, Inc. |

VALIMET’s Spherical Aluminum Powders |

Niche Specialist |

U.S.-based precision atomized Al powder; defence, propellants, and pyrotechnics specialty grades |

|

Eckart GmbH (ALTANA) |

STANDART, METALURE |

Established |

German premium aluminium pigment and powder, coatings, inks, and specialty chemicals |

Regional fragmentation is high in Asia Pacific, where dozens of Chinese domestic producers compete primarily on price for industrial-grade markets. Competitive differentiation in the premium tier is driven by particle size consistency, purity certification, ATEX compliance, and aerospace qualification credentials.

Key Company Profiles

Alcoa Corporation

Alcoa is one of the world’s largest aluminium producers, with aluminium powder as part of its broader value-added products portfolio.

- Product Portfolio: EcoSource (Alumina).

- Recent Developments: In February 2026, the Australian Federal Government granted Alcoa Corporation the modernised framework of mining activities in the Western Australian region.

- Strategic Focus: Decarbonization of primary aluminium production; ELYSIS inert anode technology development targeting zero-carbon smelting; specialty alloy and value-added product mix expansion for automotive and aerospace.

RusAL

RusAL is one of the world’s largest primary aluminium producer. The company is headquartered in Moscow, Russia, with major production assets across Siberia, Ural, and the Krasnoyarsk region.

- Product Portfolio: G-00 smelter-grade alumina.

- Recent Developments: In February 2026, RUSAL introduced an innovative composite material for 3D printing. The new metal matrix composite, RS-770K, boasts a tensile strength 30% higher than the strongest aluminum powder alloys, paving the way for advancements in additive manufacturing for high-performance applications.

- Strategic Focus: Asian market penetration for powder exports; green aluminium certification leveraging Siberian hydropower advantage; downstream value-added product mix expansion to reduce commodity metal price exposure.

Toyal America Inc.

Toyal America is the North American subsidiary of Toyo Aluminium K.K. (Japan), specialising in aluminium paste, pigment, and powder products.

- Product Portfolio: Aluminum Alloy Powders for Additive Manufacturing and Cold Spray, Atomized Aluminum Powders, and Aluminum Powders and Aluminum Nitride for Thermal Management.

- Recent Developments: Expanded North American production capacity for aerospace AM powder, launched Toyal PCAF-certified low-carbon aluminium pigment products for automotive OEMs.

- Strategic Focus: Aerospace AM powder market capture through L-PBF qualification programs; automotive OEM paint specification dominance in North America; sustainability certification for automotive supply chain ESG compliance requirements.

AMG Critical Materials N.V.

AMG Alpoco is a subsidiary of AMG Critical Materials N.V., specializing in the production of aluminium powder for pyrotechnics, explosives, rocket propellants, and industrial applications.

- Product Portfolio: Gas Atomized Aluminum Powders, Air atomized Aluminum Powders, Aluminum Alloys & Flux Powders.

- Recent Developments: Secured multi-year UK Ministry of Defence aluminium powder supply contract, qualified new grades for NATO solid propellant programs under NSPA framework agreements.

- Strategic Focus: Defence and military propellants market leadership; MIL-SPEC qualification expansion into European NATO defence programs; nano-aluminium capacity development for next-generation energetic formulations and emerging hydrogen carrier applications.

Market Concentration Analysis

The global aluminium powder market is moderately fragmented. The top five producers collectively account for approximately 38–42% of global production capacity by volume. This level of concentration is below the thresholds for oligopoly but above the highly fragmented norm for commodity chemicals, reflecting the technical barriers of atomization investment and safety certification requirements.

The Chinese domestic market represents the most fragmented sub-market. This fragmentation prevents Chinese producers from building global brand equity but creates intense price competition in commodity grades that pressures margins for international producers competing in Asia Pacific markets. The Chinese market’s fragmentation is expected to consolidate gradually as environmental and safety regulation enforcement tightens.

Investment & Growth Opportunities

Fastest Growing Segments

Aerospace and defence-grade aluminium powder (CAGR ~4–6%), additive manufacturing aluminium alloy powders (CAGR ~18–22%), and nano-aluminium for energetics (CAGR ~12–15%) represent the three highest-margin investment vectors through 2034. These combined segments command 5–20× the price of commodity industrial grades, allowing producers to grow revenues significantly faster than the overall market’s 1.5% volume CAGR.

Emerging Market Expansion

India’s defence aluminium powder market growth, as the government mandates domestic procurement under the Defence Acquisition Procedure 2020. Saudi Arabia’s military industrialization program (SAMI) and UAE’s EDGE Group are building domestic defence manufacturing capability that will require locally sourced or in-country produced aluminium powder for ammunition, which favours international producers willing to invest in joint ventures.

Venture Investment Trends

Venture and growth capital investment in metal powder technologies, with additive manufacturing feedstock companies attracting the largest share. Hydrogen-carrier aluminium powder companies are raising Series A funding based on green energy storage market projections.

- Key investment themes: Gas-atomized AM aluminium powder capacity, nano-aluminium for clean energy, scrap-based circular production, and premium aerospace qualification programs yielding 10–20× commodity price premiums.

- Strategic partnership focus: Aluminium powder producers forming JVs with aerospace AM users, defence primes, and clean energy developers to create captive demand anchors.

Future Market Outlook (2026-2034)

The global aluminium powder market is forecast to grow steadily from 680.5 Thousand Tons in 2025 to 783.4 Thousand Tons by 2034, an absolute volume addition of 102.9 Thousand Tons at a 1.5% CAGR. This moderate headline growth rate masks significant structural divergence within the market. Commodity grades for construction, industrial chemicals, and standard explosives will grow at 0.8–1.2% annually, constrained by substitution pressures and Chinese overcapacity.

Between 2026 and 2030, the dominant transformation will be the codification of additive manufacturing aluminium powder as a distinct product category with its own qualification standards, customer specifications, and supply chain dynamics separate from conventional powder markets. The 2030–2034 period will be shaped by whether aluminium powder hydrogen energy carrier technology achieves commercial scale deployment. Producers with green aluminium credentials and ATEX-certified logistics are best positioned to capture this potential new application segment.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 120+ industry stakeholders in 2025, comprising aluminium powder production executives, metallurgical engineers, procurement managers from defence and aerospace OEMs, distributors, and industry analysts covering the metal powder sector across North America, Europe, and Asia Pacific. Primary data validated production volumes, market share estimates, and emerging technology adoption dynamics.

Secondary Research

Secondary research encompassed aluminium industry statistical sources, including IAI (International Aluminium Institute), IFA trade statistics, industry publications (Metal Powder Report, International Journal of Powder Metallurgy), company annual reports, Wohlers Report on additive manufacturing, defence procurement databases, import/export trade data, and patent filing records across 25 countries. Over 240 secondary sources were reviewed and synthesized.

Forecasting Models

Market volume forecasts were developed using a bottom-up end-use demand aggregation approach, modelling aluminium powder consumption within each application segment (construction, explosives, automotive, aerospace, chemicals, additive manufacturing, others) based on end-use industry growth projections. Key inputs include global construction output, defence budget trajectories, automotive production volumes, and AM adoption rate curves.

Aluminium Powder Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | ‘000 Tons |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Air Atomization, Others |

| End-Uses Covered | Industrial, Automotive, Chemical, Construction, Explosives, Defence and Aerospace, Others |

| Raw Materials Covered | Aluminium Ingots, Aluminium Scrap |

| Regions Covered | Asia Pacific, Europe, North America, South America, Middle East and Africa |

| Companies Covered | Alcoa Corporation, RusAL, Toyal America Inc., AMG Critical Materials N.V. , THE METAL POWDER COMPANY LIMITED (MEPCO), Kymera International, VALIMET, Inc., Eckart GmbH (ALTANA), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the aluminium powder market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global aluminium powder market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the aluminium powder industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Aluminium Powder Market Report

The global aluminium powder market reached 680.5 Thousand Tons in 2025 and is projected to reach 783.4 Thousand Tons by 2034, growing at a CAGR of 1.5%.

Asia Pacific dominates with 41.8% volume share (2025), driven by China's construction AAC block production, mining explosives demand, and India's growing defence manufacturing base.

Air atomization dominates with 68.4% market share (2025), preferred for industrial, explosives, and construction grades due to cost efficiency and consistent spherical particle production.

Aluminium ingots lead with 63.7% share (2025), essential for high-purity aerospace and defence grades. Scrap-based production at 36.3% is the faster growing segment at ~1.9% CAGR.

Key players include Alcoa Corporation, RusAL, Toyal America Inc., AMG Critical Materials N.V., THE METAL POWDER COMPANY LIMITED (MEPCO), Kymera International, VALIMET, Inc., and Eckart GmbH (ALTANA).

Major end-uses include construction (AAC blocks), explosives (ANFO), automotive sintering, aerospace/defence propellants, chemical reactions, coatings/pigments, and additive manufacturing (3D printing).

Key trends include additive manufacturing premium powder demand, hydrogen energy carrier research, defence spending acceleration, AI-driven process optimization, and circular economy scrap-based production growth.

Key challenges include combustible dust safety regulations (ATEX/OSHA), aluminium LME price volatility, Chinese commodity producer competition, energy costs, and long aerospace qualification timelines (12–24 months).

China's AAC block construction demand and mining explosives (ANFO) account for approximately 55–60% of Asia Pacific consumption. India’s defence procurement growth adds 6–8% annual incremental demand from 2024 onward.

Top opportunities include aerospace-grade AM powder capacity, MIL-SPEC defence supply, nano-aluminium for hydrogen energy carriers, and low-carbon certified powder for European automotive OEM supply chains.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)