Amino Acids Market Size, Share, Trends and Forecast by Type, Raw Material, Application, and Region, 2026-2034

Global Amino Acids Market Size, Share, Trends & Forecast (2026-2034)

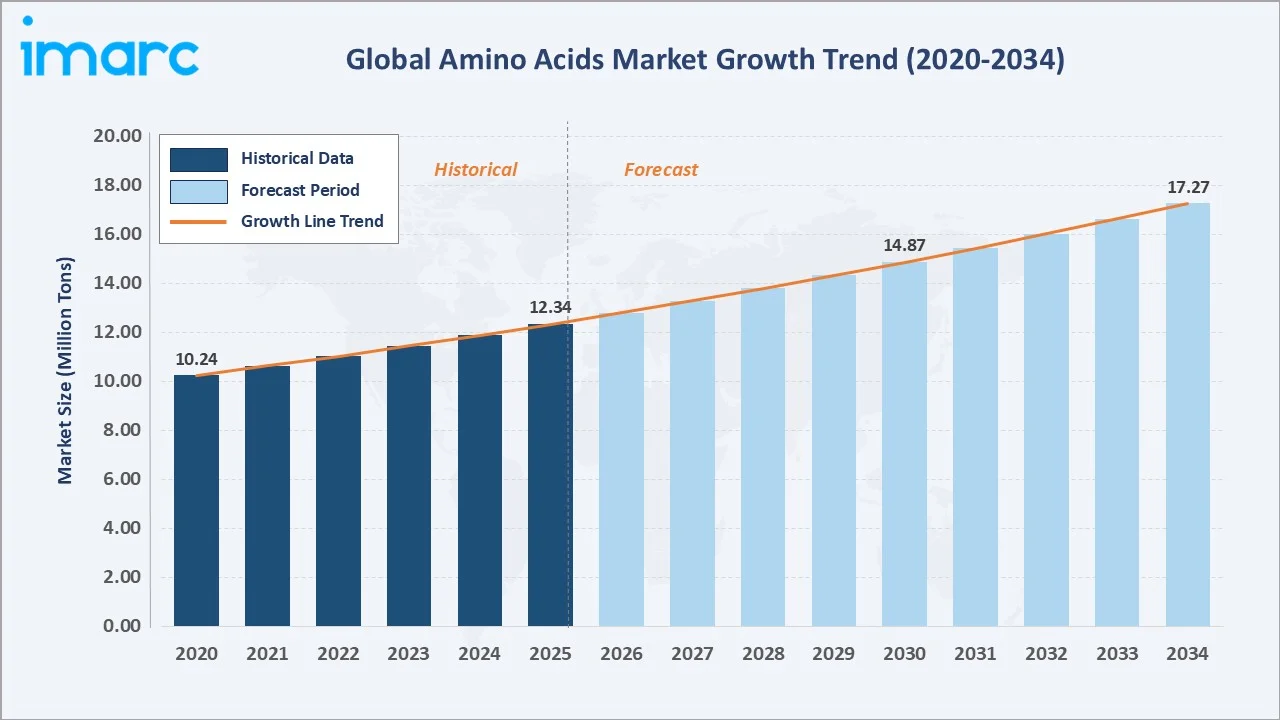

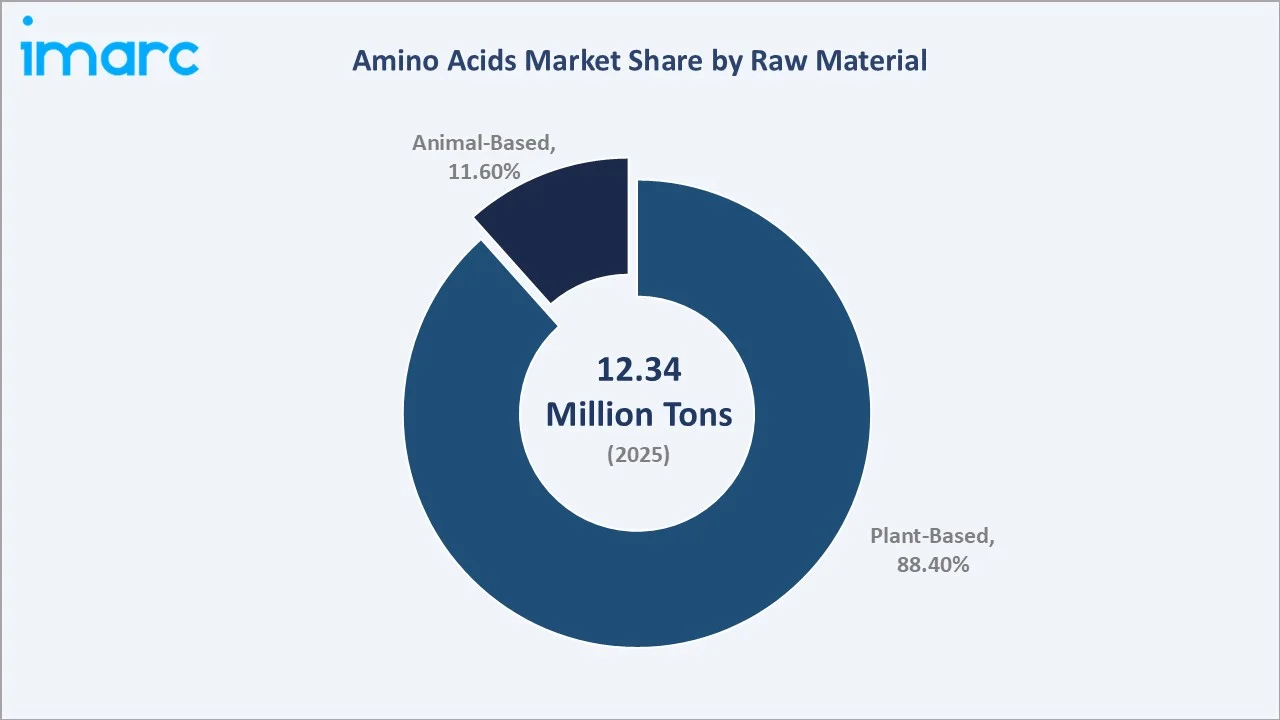

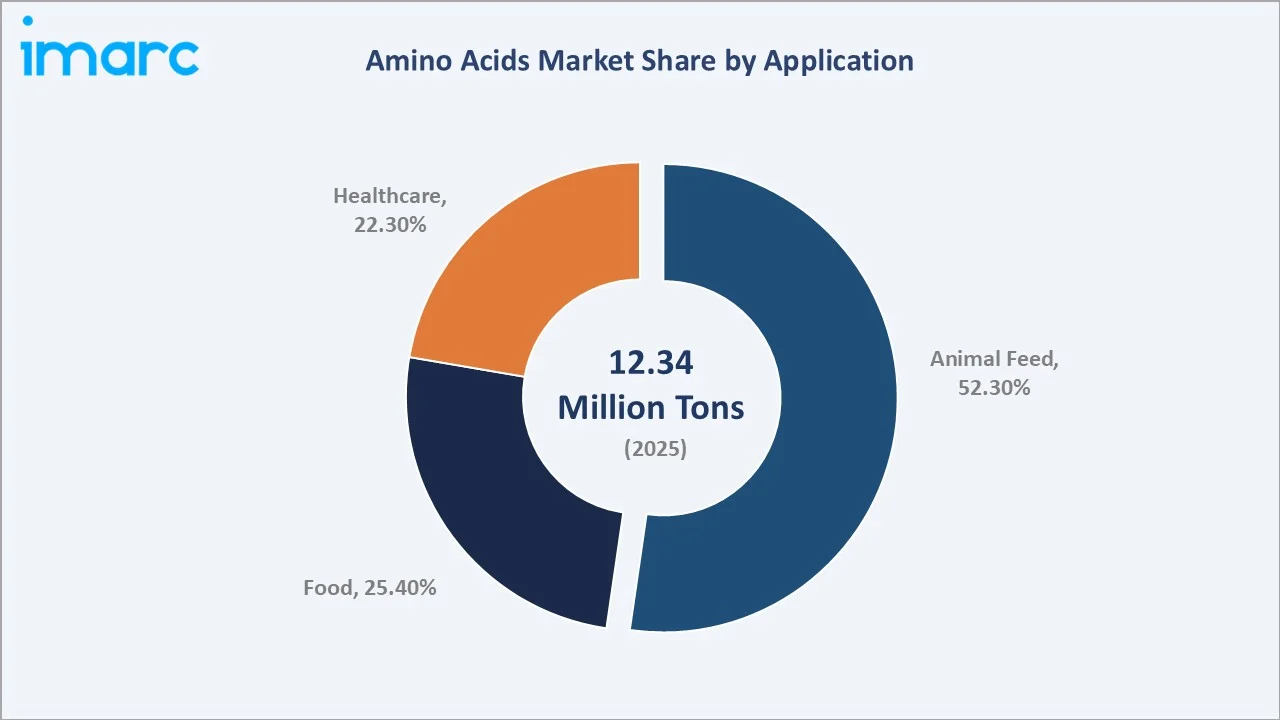

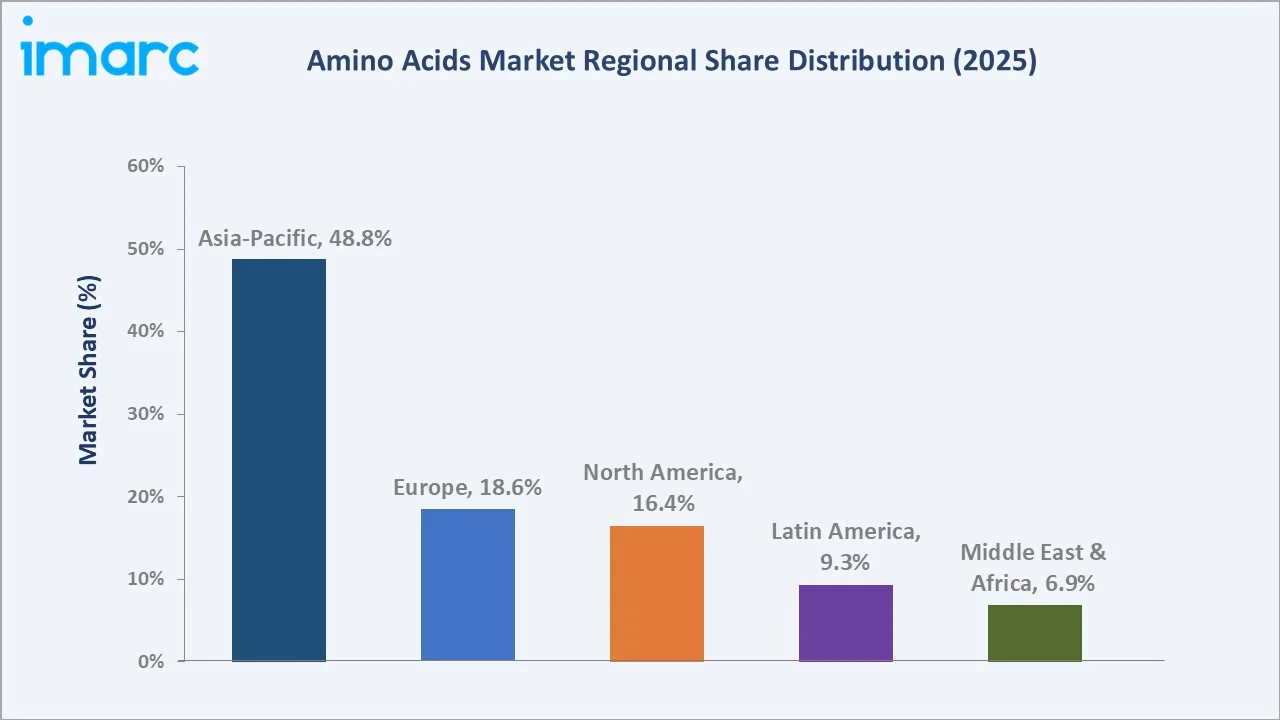

The global amino acids market size reached 12.3 Million Tons in 2025 and is projected to reach 17.3 Million Tons by 2034, exhibiting a CAGR of 3.80% during 2026-2034. The market growth is underpinned by surging demand from animal nutrition, the rising health-conscious consumer base seeking protein-enriched foods, and accelerating pharmaceutical-grade amino acid applications. Plant-based raw material dominates supply, accounting for 88.4% of production in 2025. Animal Feed leads application at 52.3%, reflecting the critical role of essential amino acids in modern livestock farming. Asia-Pacific commands 48.8% of global revenue in 2025, driven by China's expanding agri-food processing sector and India's fast-growing nutraceuticals industry.

Market Snapshot

|

Metric |

Volume |

|

Market Size (2025) |

12.3 Million Tons |

|

Forecast Market Size (2034) |

17.3 Million Tons |

|

CAGR (2026-2034) |

3.80% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (48.8% share, 2025) |

|

Fastest Growing Region |

Middle East & Africa (Est. CAGR ~4.5%) |

|

Leading Raw Material |

Plant-Based (88.4%, 2025) |

|

Leading Application |

Animal Feed (52.3%, 2025) |

The chart below illustrates the global amino acids market growth trajectory from 2020 through 2034, contrasting consistent historical expansion against a sustained forecast curve powered by protein economy trends, biotechnology innovations, and emerging-market feed demand.

To get more information on this market, Request Sample

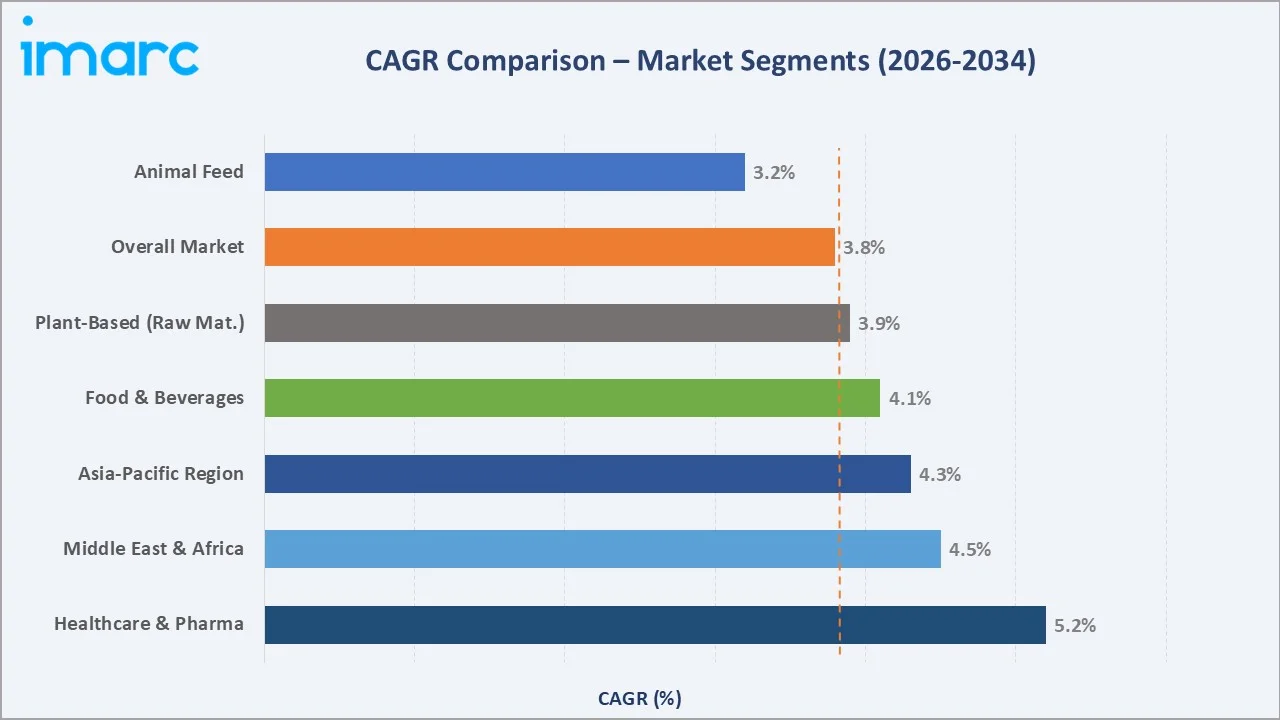

The CAGR comparison below highlights Healthcare & Pharma and Middle East & Africa as the fastest-growing sub-categories, both outpacing the overall market CAGR of 3.80%, with Healthcare & Pharma projected at 5.2% and MEA at 4.5% through 2034.

Executive Summary

The global amino acids market is undergoing a sustained transformation, driven by the convergence of plant-based nutrition, precision animal husbandry, and pharmaceutical biotechnology. Volumed at 12.3 Million Tons in 2025, the market is forecast to grow at a CAGR of 3.80% to reach 17.3 Million Tons by 2034. According to the International Feed Industry Federation, compound feed production in 2023 was approximately 1 billion 295 million metric tons, Essential amino acids such as lysine, methionine, and threonine enhance livestock growth and feed-conversion efficiency by improving protein utilization and reducing nutrient waste, typically resulting in double-digit performance gains.

Animal Feed remains the dominant application, claiming 52.3% of total market volume in 2025. The sector benefits from intensifying livestock production, aquaculture expansion, and growing demand for leaner, higher-protein outputs in Asia and Latin America. The food segment, at 25.4% share in 2025, is fuelled by consumer trends toward functional foods, sports nutrition, and clean-label protein enrichment.

Asia-Pacific dominates with 48.8% market share in 2025, led by China's large-scale fermentation-based amino acid manufacturing ecosystem and India's expanding animal husbandry and supplement sectors. Europe holds 18.6%, driven by stringent regulatory standards and premium nutraceutical demand. North America accounts for 16.4%, underpinned by a large protein supplement industry and sophisticated pharmaceutical R&D base.

Key Market Insights

|

Insight |

Data |

|

Largest Application |

Animal Feed – 52.3% share (2025) |

|

Leading Raw Material |

Plant-Based – 88.4% share (2025) |

|

Leading Region |

Asia-Pacific – 48.8% revenue share (2025) |

|

Second Region |

Europe – 18.6% revenue share (2025) |

|

Market Volume (2034) |

17.3 Million Tons |

|

Top Companies |

Ajinomoto, ADM, CJ CheilJedang, Evonik, Fufeng Group, Kyowa Kirin |

Key Analytical Observations Supporting the Above Data:

- Animal Feed dominance at 52.3% in 2025 reflects the amino acid industry's structural dependence on the livestock and aquaculture sectors, where methionine, lysine, and threonine are indispensable nutritional inputs.

- Plant-Based raw material's 88.4% share as corn, cassava, and soy enable cost-efficient fermentation-based amino acid production, replacing petrochemical synthesis for most commodity amino acids.

- Asia-Pacific's 48.8% global dominance in 2025 reflects China's role as both the world's largest producer and consumer of amino acids, with Fufeng Group and Meihua Holdings operating mega-scale fermentation plants.

- Healthcare's 22.3% share and accelerating growth trajectory reflects biopharmaceutical pipeline expansion, with amino acids used as buffers, excipients, and active ingredients in next-generation biologics.

- Middle East & Africa is emerging as a high-growth region, supported by expanding livestock investments, rising protein demand, and government-led food security programs that are creating new demand centers for feed additives and amino acids.

Global Amino Acids Market Overview

Amino acids are organic compounds composed of nitrogen, carbon, hydrogen, and oxygen, functioning as the fundamental building blocks of proteins. Commercially, more than 20 amino acids hold industrial significance, ranging from feed-grade products such as lysine, methionine, and threonine to pharmaceutical-grade amino acids including glutamine, arginine, and taurine. Production is primarily dominated by microbial fermentation, which accounts for most of the global output, followed by chemical synthesis and enzymatic processes, each offering varying levels of purity, scalability, and cost efficiency.

Applications of amino acids span multiple industries, including livestock feed additives that improve protein utilization and animal growth performance, functional food and beverage fortification, sports nutrition products, clinical nutrition such as intravenous parenteral formulations, and pharmaceutical and biologics manufacturing. Market growth is supported by key macroeconomic drivers, including global population growth projected to reach 9.7 billion by 2050 according to United Nations, rising protein consumption across emerging economies, increasing pharmaceutical R&D expenditure exceeding USD 250 billion in 2023 as reported by IQVIA, and continued advances in fermentation biotechnology that have significantly improved production efficiency and reduced manufacturing costs over the past decade.

Applications of amino acids span multiple industries, including livestock feed additives that improve protein utilization and animal growth performance, functional food and beverage fortification, sports nutrition products, clinical nutrition such as intravenous parenteral formulations, and pharmaceutical and biologics manufacturing. Market growth is supported by key macroeconomic drivers, including global population growth projected to reach 9.7 billion by 2050 according to United Nations, rising protein consumption across emerging economies, increasing pharmaceutical R&D expenditure exceeding USD 250 billion in 2023 as reported by IQVIA, and continued advances in fermentation biotechnology that have significantly improved production efficiency and reduced manufacturing costs over the past decade.

Market Dynamics

To evaluate market opportunities, Request Sample

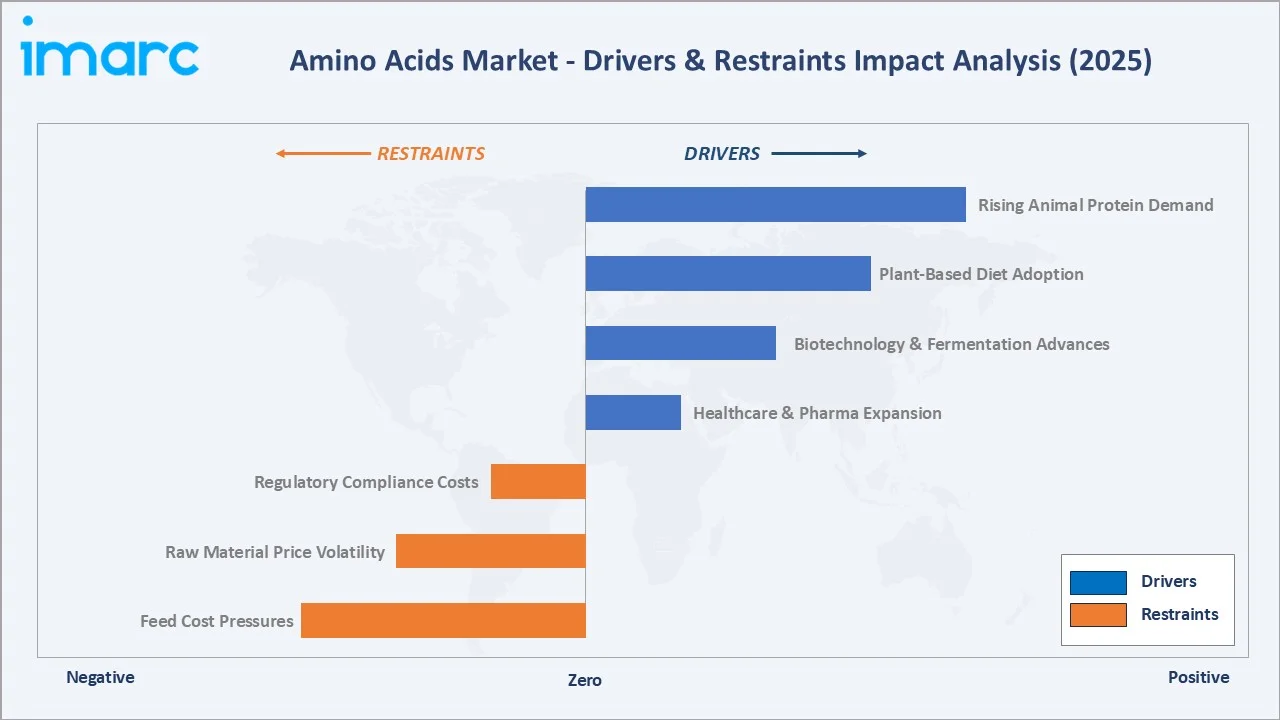

Market Drivers

- Rising Demand from the Animal Feed Sector: Amino acids such as lysine, methionine, and threonine are among the most widely used feed additives, driven by the growing need for precision livestock nutrition. Their supplementation improves feed conversion efficiency, reduces nitrogen emissions, and lowers feed costs, while supporting sustainable livestock production and enhanced animal welfare outcomes.

- Growing Adoption of Plant-Based Diets and Protein Fortification: With 71% of Americans actively trying to increase protein intake in 2024, up from 59% in 2022, demand for amino acid-fortified foods and dietary supplements is accelerating. Plant-based proteins often lack essential amino acids such as lysine, methionine, and tryptophan, increasing demand for amino acid fortification in plant-based formulations and functional foods.

- Advances in Fermentation Biotechnology and Biosynthesis: Most industrial amino acids are now produced using microbial fermentation, which enables large-scale, cost-efficient production with improved yield and purity. Advances in metabolic engineering and microbial strain optimization have significantly improved fermentation productivity, allowing manufacturers such as Ajinomoto and CJ CheilJedang to scale production while reducing manufacturing costs compared to traditional chemical synthesis.

- Expanding Pharmaceutical and Nutraceutical Applications: Amino acids are widely used in clinical nutrition, biologics manufacturing, and pharmaceutical formulations, with growing demand driven by personalized medicine and biologics production. Expanding pharmaceutical and nutraceutical applications, along with increasing use in clinical nutrition formulations, continue to support the rising demand for amino acids across healthcare and life science industries.

Market Restraints

- Raw Material Price Volatility: Corn, cassava, and other carbohydrate feedstocks account for 50–70% of amino acid fermentation production costs, making manufacturers highly sensitive to agricultural commodity price fluctuations. Corn prices have shown significant volatility across recent years, with prices fluctuating due to supply disruptions, weather patterns, and global demand, thereby compressing margins for amino acid producers.

- Stringent Regulatory Requirements: Food-grade and pharmaceutical-grade amino acid production requires compliance with FDA cGMP, GRAS approvals, EFSA food additive regulations (E-numbers), and regional pharmacopoeia standards, significantly increasing validation, documentation, and manufacturing costs.

- Environmental Regulations on Fermentation Waste: Large-scale amino acid fermentation generates wastewater, biomass residues, and ammonium-based by-products, requiring advanced treatment infrastructure. Asia-Pacific, particularly China, dominates global amino acid production (over 56% of global output), and tightening environmental regulations in major production regions are increasing treatment and compliance costs.

Market Opportunities

- Sustainable and Bio-Based Amino Acid Production: Rising sustainability regulations and consumer demand are accelerating bio-based amino acid production using renewable feedstocks and fermentation technologies. Major producers such as BASF and Evonik are expanding low-carbon and sustainable amino acid production initiatives aligned with long-term climate targets.

- Aquaculture Feed Expansion in Asia-Pacific: Global aquaculture production reached 94.4 million tons in 2022–2023 (FAO), with Asia accounting for over 90% of output. Growing shrimp, salmon, and tilapia farming is increasing demand for crystalline amino acids in aquafeed..

- Precision Fermentation and Synthetic Biology Innovations: Precision fermentation technologies are enabling production of high-purity specialty amino acids and bio-based ingredients, supporting premium applications in pharmaceuticals, nutrition, and specialty chemicals with higher margins than commodity amino acids.

Market Challenges

- Intensifying Chinese Production Competition: China dominates global amino acid production, particularly lysine and glutamate, leading to periodic oversupply and price pressure. Increased Chinese capacity expansions during 2022–2024 contributed to declining lysine and feed amino acid prices, compressing margins for global producers.

- Supply Chain Concentration Risk: China accounts for a significant share of global amino acid production, particularly lysine and threonine, creating supply concentration risks. COVID-19 logistics disruptions highlighted vulnerability in global feed supply chains and increased volatility in amino acid availability.

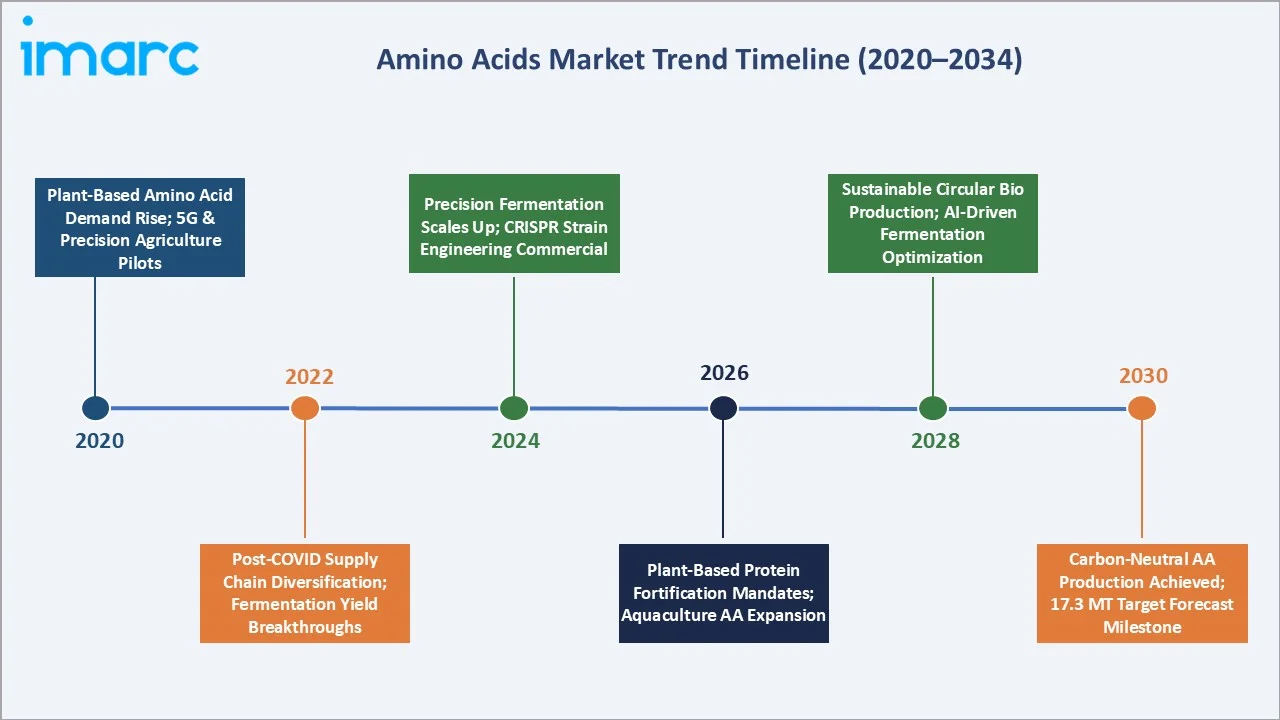

Emerging Market Trends

1. Precision Fermentation Redefining Amino Acid Production Economics

Advanced fermentation using engineered Corynebacterium glutamicum strains is significantly improving amino acid production efficiency. Recent industrial studies indicate lysine titers exceeding 150–180 g/L, compared with 100–130 g/L in conventional fermentation systems, improving yield efficiency and lowering production costs. Continuous strain engineering, metabolic pathway optimization, and process intensification are expected to further reduce manufacturing costs and expand fermentation-based production, accelerating the shift away from legacy chemical synthesis routes through 2030.

2. Plant-Based Protein Fortification Driving Specialty Demand

The global plant-based food market surpassed USD 29 billion in 2023. Plant proteins exhibit well-documented essential amino acid deficiencies – every 100g of pea protein isolate typically requires 200–300mg of supplemental lysine to achieve nutritional completeness, creating a structural, recurring demand that scales directly with plant-based food adoption.

3. Aquaculture Feed Transition Away from Fishmeal

Global aquaculture production is expected to supply over 60% of seafood consumed by humans by 2030 (FAO). The industry's transition from fishmeal-based diets to plant-protein alternatives creates significant digestible amino acid demand gaps. Crystalline methionine and lysine for shrimp and salmon feed, among the highest-growth niches in the forecast period.

4. Personalized Nutrition and Therapeutic Amino Acid Applications

The convergence of clinical nutrition, aging populations, and personalized healthcare is increasing demand for functional amino acid formulations. Therapeutic amino acids such as L-glutamine (gut health), BCAAs (muscle preservation), and metabolic amino acid derivatives are experiencing steady growth in clinical nutrition and dietary supplements.

5. Sustainability and Circular Economy Integration

Sustainability initiatives are becoming increasingly important in amino acid manufacturing. Ajinomoto operates a bio-cycle system that converts fermentation by-products into organic fertilizers and animal feed, supporting circular economy practices and reducing environmental waste. Meanwhile, Evonik is advancing sustainability through emissions reduction targets, renewable energy adoption at selected production sites, and a long-term commitment to carbon neutrality by 2050, positioning sustainability as a competitive differentiator in global amino acid procurement decisions.

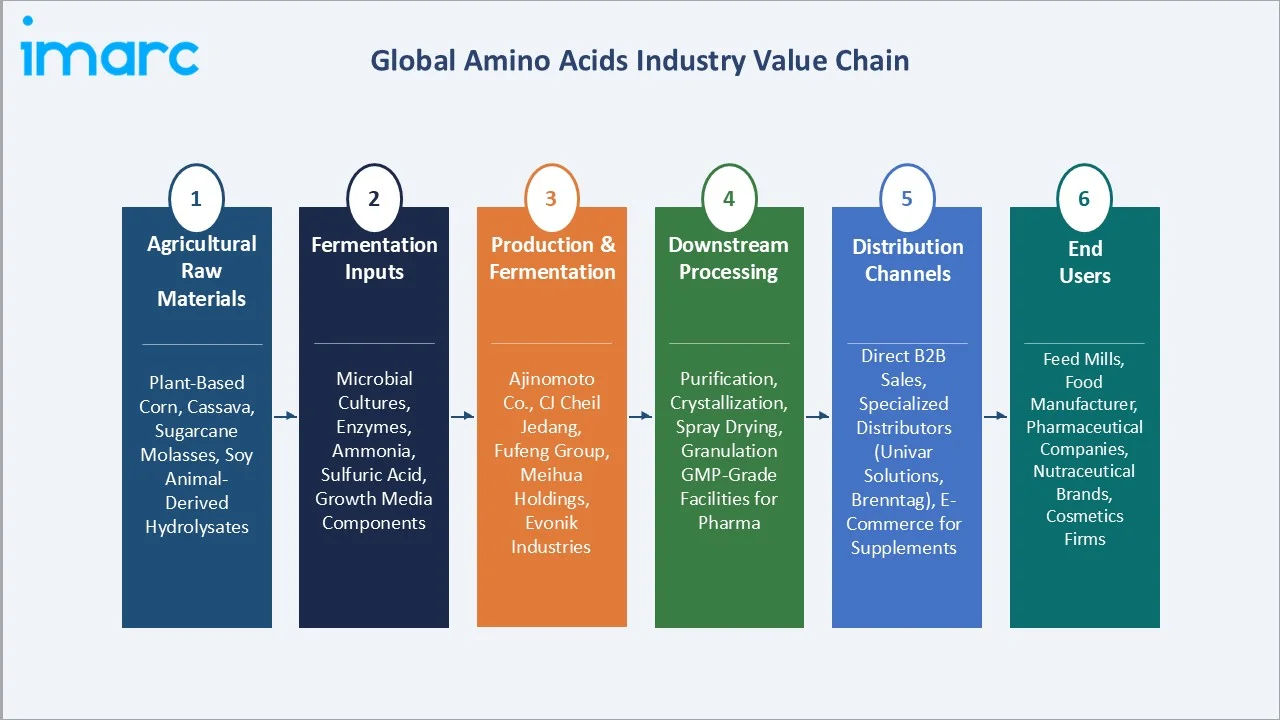

Industry Value Chain Analysis

The amino acids industry value chain spans six integrated stages from agricultural raw material sourcing through end-user consumption. Each stage exhibits distinct margin profiles, competitive dynamics, and technology investment requirements, with fermentation and downstream processing representing the highest-value-added steps.

|

Stage |

Key Players / Examples |

|

Agricultural Raw Materials |

Plant-Based (88.4%): Corn, Cassava, Sugarcane Molasses, Soy; Animal-Derived (11.6%): Hydrolysates |

|

Fermentation Inputs |

Microbial Cultures, Enzymes, Ammonia, Sulfuric Acid, Growth Media Components |

|

Production & Fermentation |

Ajinomoto Co., CJ CheilJedang, Fufeng Group, Meihua Holdings, Evonik Industries |

|

Downstream Processing |

Purification, Crystallization, Spray Drying, Granulation; GMP-Grade Facilities for Pharma |

|

Distribution Channels |

Direct B2B Sales, Specialized Distributors (Univar Solutions, Brenntag), E-Commerce for Supplements |

|

End Users |

Feed Mills, Food Manufacturers, Pharmaceutical Companies, Nutraceutical Brands, Cosmetics Firms |

The production and fermentation stage commands the highest strategic value, integrating substrate supply, microbial biotechnology, and downstream recovery. Chinese producers dominate commodity amino acid manufacturing through economies of scale, while European and Japanese players (Evonik, Ajinomoto, Kyowa Kirin) focus on high-purity, specialty, and pharmaceutical-grade amino acids commanding price premiums over feed-grade products.

Technology Landscape in the Amino Acids Industry

Microbial Fermentation Technology

Microbial fermentation has contributed to 80% of global amino acid production, particularly for lysine, glutamate, and threonine. Advanced fed-batch fermentation using metabolically engineered Corynebacterium glutamicum strains has achieved lysine titers above 200 g/L, with carbon yields approaching 0.6–0.7 g/g glucose under optimized industrial conditions.

Synthetic Biology and Metabolic Engineering

CRISPR-based genome editing and metabolic engineering are enabling microbial production of specialty amino acids such as L-theanine, hydroxyproline, and D-amino acids, previously produced through chemical synthesis. Synthetic biology companies including Ginkgo Bioworks are collaborating with chemical and fermentation manufacturers to develop next-generation high-titer microbial strains, with several specialty amino acid commercialization programs progressing through mid-decade timelines.

Green Chemistry and Enzymatic Synthesis

Enzymatic synthesis methods are increasingly used for high-purity pharmaceutical-grade amino acids, offering improved enantiomeric selectivity compared to chemical resolution routes. Immobilized enzyme and multi-enzyme cascade systems have demonstrated conversion yields above 90–95% and improved operational stability, while also reducing waste generation and solvent consumption. These enzymatic routes support sustainability goals and are gaining adoption in pharmaceutical and nutraceutical amino acid manufacturing

Process Intensification and Downstream Innovation

Advanced downstream technologies including membrane separation, continuous chromatography, and improved crystallization are improving amino acid production efficiency. These innovations reduce energy consumption and enhance product consistency for food- and pharmaceutical-grade applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Glutamic Acids |

43.4% |

2025 |

|

Raw Material |

Plant Based |

88.4% |

2025 |

|

Application |

Animal Feed |

52.3% |

2025 |

|

Region |

Asia Pacific |

48.8% |

2025 |

By Raw Material

Plant-based raw materials dominate the amino acids market, commanding an 88.4% share in 2025. Plant-based feedstocks such as corn, cassava, molasses, and wheat serve as primary carbon sources for industrial amino acid fermentation, particularly for lysine and glutamic acid production. The shift toward biomass-derived sugars has been driven by lower feedstock costs and improved fermentation efficiency, replacing petroleum-based and chemical synthesis routes in most commodity amino acids. Animal-based raw materials, representing 11.6% in 2025, remain relevant for specific high-value amino acid categories.

To access detailed market analysis, Request Sample

By Application

Animal feed leads the amino acids market with a 52.3% volume share in 2025, driven by the essential role of supplemental methionine, lysine, threonine, and tryptophan in optimizing poultry, swine, and aquaculture feed formulations. Modern least-cost feed formulation software – deployed by leading integrators including Tyson Foods, JBS, and Charoen Pokphand Foods – systematically optimizes amino acid supplementation, creating structural, price-inelastic demand.

The food segment, at 25.4% in 2025, encompasses Applications include MSG production (glutamic acid), sports nutrition supplements, infant formula enrichment, and functional food fortification.

Regional Market Insights

The amino acids market exhibits strong regional concentration, with Asia-Pacific commanding nearly half of global volume. Diverse growth profiles across regions reflect variations in industrial development, dietary patterns, regulatory frameworks, and biotechnology investment levels.

|

Region |

Share (2025) |

Est. CAGR |

Key Growth Factors |

|

Asia-Pacific |

48.8% |

~4.3% |

China production leadership; India nutraceuticals growth; Southeast Asia feed demand |

|

Europe |

18.6% |

~3.5% |

Premium pharma demand; Evonik & BASF anchoring production; EU sustainability mandates |

|

North America |

16.4% |

~3.2% |

Large supplement industry (USD 67B); sophisticated pharma R&D; poultry/pork feed demand |

|

Latin America |

9.3% |

~4.0% |

Brazil largest poultry exporter; Argentina livestock; Mexico aquaculture expansion |

|

Middle East & Africa |

6.9% |

~4.5% |

GCC food security programs; Sub-Saharan Africa livestock growth at 5–7% annually |

Asia-Pacific dominates the global amino acids market by a wide margin, with China accounts for approximately 62% of Asia-Pacific amino acid production capacity, supported by large-scale fermentation infrastructure and cost-competitive feedstocks. The country hosts some of the world’s largest fermentation-based facilities, including Fufeng operates one of the world’s largest MSG and glutamic acid fermentation complexes in Xinjiang, with annual production capacity exceeding one million tons across glutamic acid and related fermentation product lines, supported by large-scale integrated fermentation infrastructure.

Competitive Landscape

|

Company |

Key Brands |

Market Position |

Core Strength |

|

Ajinomoto Co. Inc. |

AminoScience, AJI-NO-MOTO |

Global Market Leader |

Full-spectrum amino acid portfolio |

|

Evonik Industries AG |

MetAMINO, Biopharma |

Premium Specialty Leader |

Pharma-grade methionine specialist |

|

CJ CheilJedang Corporation |

CJ Feed & Care, CJ BIO |

Strong Challenger |

Feed-grade scale, cost efficiency |

|

ADM |

ADM Animal Nutrition |

Integrated Challenger |

Raw material vertical integration |

|

Fufeng Group Limited |

Fufeng |

Volume Leader (China) |

Low-cost fermentation production |

|

Kyowa Kirin Co. Ltd. |

Kyowa Hakko Bio |

Pharma Specialist |

Pharmaceutical amino acid purity |

|

Meihua Holdings Group |

Meihua |

Large-Scale Fermentation Leader |

High-volume, competitive cost structure |

|

BASF SE |

Luprosil, Luprosil NC |

Industrial Niche Player |

Specialty chemical process expertise |

|

Sumitomo Chemical Co. Ltd. |

Sumitomo Pharma |

Specialty Applications |

Pharma & specialty amino acids |

|

Global Bio-Chem Technology Grp. |

Global Bio-Chem |

Feed-Grade Asian Producer |

Feed-grade supply for Asia Pacific |

The global amino acids market is characterized by a moderately consolidated competitive landscape, with five to six major multinationals commanding approximately 55–60% of global revenue in high-value segments, while dozens of Chinese producers compete for commodity market share. Competitive dynamics differ significantly between feed-grade commodity amino acids (cost-driven, scale-dependent) and pharmaceutical/food-grade specialty products (quality, purity, and regulatory certification-driven).

Key Company Profiles

Ajinomoto Co. Inc.

Ajinomoto, founded in Tokyo in 1909, is the world's largest amino acid company with FY2024 revenues of approximately JPY 1.5 trillion (USD 10 billion). The company's AminoScience business spans feed-grade amino acids, pharmaceutical-grade formulations, food ingredients, and industrial biotechnology, with manufacturing and operational presence across more than over 117 production plants across more than 24 countries. In 2023, Ajinomoto expanded regional marketing initiatives, including educational and consumer engagement campaigns across Southeast Asia to strengthen nutraceutical and functional ingredient positioning. The company continues to develop proprietary fermentation and strain-engineering technologies to enhance yield efficiency and production scalability.

Evonik Industries AG

Evonik's Nutrition & Care division is the global leader in DL-methionine (MetAMINO) and a major supplier of lysine and threonine for animal nutrition. The Antwerp site is one of Evonik's three global methionine production hubs, alongside Mobile, Alabama, and Singapore, with a total annual capacity exceeding 700,000 tons. Evonik's Biopharma Services segment supplies pharmaceutical-grade amino acids and custom fermentation products to biologics manufacturers, with a commitment to a 50% reduction in Scope 1 and 2 GHG emissions by 2030.

CJ CheilJedang Corporation

CJ CheilJedang's CJ BIO division is one of Asia's leading amino acid producers, with global feed-grade amino acid production spanning South Korea, Indonesia, Malaysia, Brazil, China, and the United States. The company maintains strong market positioning in bio-based lysine and continues expanding threonine and tryptophan production capacity. Between 2022 and 2024, CJ CheilJedang invested in fermentation technology and global capacity expansion, reinforcing its strategy of cost competitiveness and supply chain diversification.

Fufeng Group Limited

Fufeng Group is China's largest amino acid producer and one of the world's top fermentation companies. The Xinjiang production complex produces glutamic acid, xanthan gum, and corn-derivative amino acids at multi-million-ton annual scale. Fufeng's integrated corn processing model – capturing value from starch, protein, oil, and fermentation products – provides structural cost advantages versus non-integrated competitors, reinforcing China's global production dominance.

Kyowa Kirin Co. Ltd.

Kyowa Kirin (formerly Kyowa Hakko Bio) is the global authority in pharmaceutical-grade amino acid production, with its Hofu, Japan facility serving as the reference standard for purity and quality in parenteral nutrition and biologic manufacturing. The company supplies high-purity L-glutamine, L-alanine, and branched-chain amino acid formulations to pharmaceutical companies in over 40 countries, maintaining best-in-class quality credentials for the regulated pharmaceutical channel.

Market Concentration Analysis

The global amino acids market exhibits a bimodal concentration structure. In high-value pharmaceutical and food-grade segments, the top 5 players – Ajinomoto, Evonik, CJ CheilJedang, Kyowa Kirin, and BASF – collectively command approximately 60–65% of market revenue, reflecting premium placed on consistent quality, regulatory certification, and technical support capabilities. In feed-grade commodity segments, Chinese producers collectively represent 50–55% of global volume but compete primarily on price.

Investment & Growth Opportunities

- Aquaculture Feed Amino Acids: Rising aquaculture production is increasing demand for digestible methionine, lysine, and threonine in shrimp, salmon, and tilapia diets, supporting premium-margin opportunities above conventional feed-grade amino acids.

- Specialty and Pharmaceutical-Grade Expansion: Growing demand for L-glutamine, BCAAs, and L-carnitine in clinical nutrition and therapeutics supports investments in GMP-certified fermentation capacity, enabling higher-value specialty amino acid production.

- Middle East & Africa Market Entry: Expanding food security initiatives in Saudi Arabia, UAE, and Nigeria create opportunities for partnerships with regional feed producers, enabling early positioning in emerging amino acid demand markets. Example: Saudi Arabia’s Vision 2030 livestock expansion supports rising demand for amino acid-based feed additives.

- Precision Fermentation Ventures: Investments in advanced strain engineering and precision fermentation for specialty amino acids such as ergothioneine, hydroxyproline, and D-amino acids present high-growth commercialization opportunities.

- Carbon-Neutral Production Differentiation: Increasing Scope 3 emission requirements among European and North American buyers are encouraging amino acid producers to adopt low-carbon fermentation processes and secure premium pricing advantages.

Future Market Outlook (2026-2034)

The global amino acids market is positioned for stable, sustained expansion through the forecast period, reaching 17.3 Million Tons by 2034 at a 3.80% CAGR. This growth trajectory reflects a market transitioning from volume-driven commodity competition toward a bifurcated landscape: large-scale, technology-optimized commodity production for animal nutrition on one side, and high-value, precision-fermented specialty amino acids for food, health, and pharmaceutical applications on the other.

Technological advances in synthetic biology are expected to reshape amino acid manufacturing through improved strain engineering and process optimization. AI-enabled metabolic modeling is accelerating fermentation development timelines and enabling faster commercialization of specialty amino acids. Concurrently, increasing regulatory and sustainability expectations are driving investment in bio-based circular production systems. Producers integrating precision fermentation, sustainability initiatives, and pharmaceutical-grade manufacturing capabilities are likely to gain competitive advantages in high-value specialty amino acid segments.

Research Methodology

IMARC Group's amino acids market research employs a comprehensive mixed-methods approach combining primary research, secondary research, and proprietary quantitative modeling to ensure accuracy, comprehensiveness, and actionable relevance.

Primary Research

Structured interviews with C-suite executives, R&D heads, procurement managers, and market experts at amino acid producers, feed mills, pharmaceutical manufacturers, and food companies across 25+ countries. Primary sources constitute approximately 35% of data inputs.

Secondary Research

Analysis of regulatory filings (FDA, EFSA, CFIA), industry association data (IFA, CRN, IFIC), annual reports, patent databases, trade publications (Feed Navigator, Amino Industry Observer), and government trade statistics covering historical market sizing and industry ecosystem mapping.

Quantitative Modeling

Bottom-up market sizing aggregating production capacity data, trade flows (UN Comtrade), consumption statistics, and demand-driver indices across 50+ countries. Top-down validation cross-references aggregate global consumption against macroeconomic indicators including animal protein production growth, nutraceutical market expansion, and pharmaceutical sector growth rates.

Forecasting Methodology

IMARC's proprietary CART (Correlation-Adjusted Regression Trees) forecasting engine incorporates 15+ demand-driver variables to generate probabilistic market size forecasts with ±5% accuracy at the 90% confidence level.

Amino Acids Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million Tons, Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Glutamic Acids, Lysine, Methionine, Threonine, Phenylalanine, Tryptophan, Citrulline, Glycine, Glutamine, Creatine, Arginine, Valine, Leucine, Iso-Leucine, Proline, Serine, Tyrosine, Others |

| Raw Materials Covered | Plant Based, Animal Based |

| Applications Covered | Animal Feed, Food, Healthcare |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | Ajinomoto Co. Inc., Evonik Industries AG, CJ CheilJedang Corporation, ADM, Fufeng Group Limited, Kyowa Kirin Co. Ltd., Meihua Holdings Group, BASF SE, Sumitomo Chemical Co. Ltd., Global Bio-Chem Technology Grp., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the amino acids market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global amino acids market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the amino acids industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Amino Acids Market Report

The global amino acids market reached 12.3 Million Tons in 2025 and is projected to grow at a 3.80% CAGR, reaching 17.3 Million Tons by 2034.

The market is forecast to reach 17.3 Million Tons by 2034, growing from 12.3 Million Tons in 2025, driven by rising demand across animal feed, food, and pharmaceutical applications.

Primary drivers include animal feed sector demand, health and wellness supplement trends, plant-based protein fortification, pharmaceutical biotechnology applications, and advances in fermentation technology reducing production costs.

Asia-Pacific leads the market with a 48.8% revenue share in 2025, driven by China's large-scale fermentation manufacturing base and the rapidly expanding nutraceutical and animal feed industries in India and Southeast Asia.

The global amino acids market is projected to grow at a CAGR of 3.80% during 2026-2034, reflecting stable long-term demand growth driven by diverse end-use applications across feed, food, and healthcare sectors.

Animal Feed holds the largest share at 52.3% in 2025. Essential amino acids including methionine, lysine, and threonine are indispensable for optimizing livestock nutrition and improving feed conversion ratios in commercial operations.

Plant-based materials, primarily corn, cassava, and sugarcane molasses, dominate with 88.4% share in 2025. Fermentation using these agricultural substrates is the most cost-efficient and scalable production method available commercially.

Key companies include Ajinomoto Co. Inc., Evonik Industries AG, CJ CheilJedang Corporation, ADM, Fufeng Group Limited, Kyowa Kirin Co. Ltd., Meihua Holdings Group, BASF SE, Sumitomo Chemical Co. Ltd., and Global Bio-Chem Technology Group.

Key trends include precision fermentation scaling, plant-based protein fortification, aquaculture feed transition, therapeutic amino acid applications in personalized nutrition, and sustainability-driven circular economy production integration.

The market is segmented by type (Glutamic Acids, Lysine, Methionine, Threonine, Phenylalanine, Tryptophan, Citrulline, Glycine, Glutamine, Creatine, Arginine, Valine, Leucine, Iso-Leucine, Proline, Serine, Tyrosine, Others), raw material (plant-based, animal-based), application (animal feed, food, healthcare), and region (Asia-Pacific, Europe, North America, Latin America, MEA).

High-growth opportunities include aquaculture feed amino acids, pharmaceutical-grade specialty products, Middle East & Africa market expansion, precision fermentation technology ventures, and carbon-neutral production differentiation.

Advanced fermentation biotechnology has reduced production costs by 40–60% over a decade. Precision fermentation platforms are enabling commercial specialty amino acid production previously limited to chemical synthesis routes, opening premium market segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)