Amniotic Membrane Market Size, Share, Trends and Forecast by Product, Application, End User, and Region, 2026-2034

Amniotic Membrane Market Size and Share:

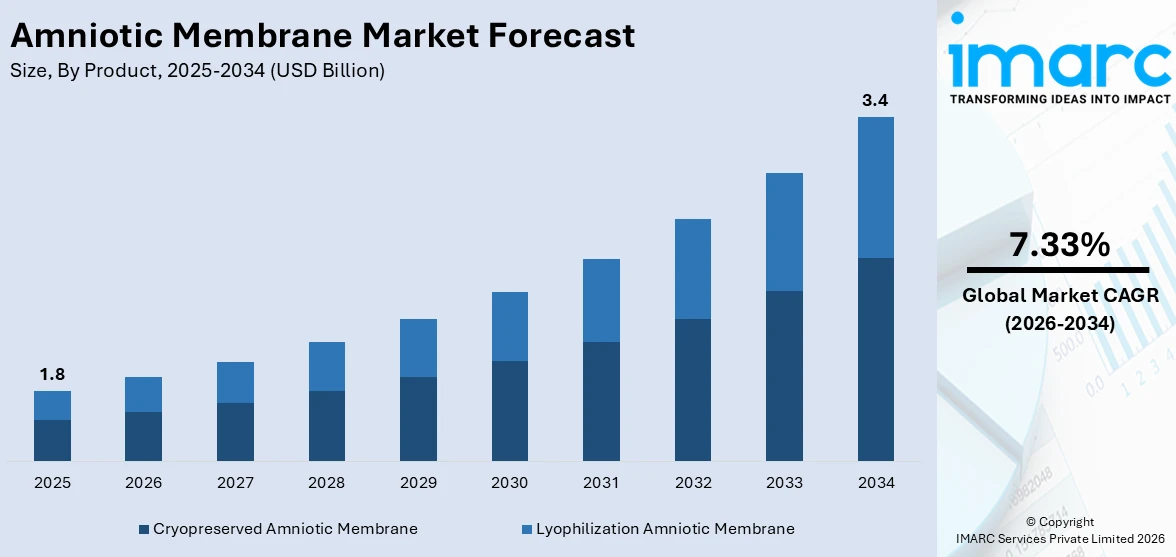

The global amniotic membrane market size was valued at USD 1.8 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.4 Billion by 2034, exhibiting a CAGR of 7.33% during 2026-2034. North America currently dominates the market, holding a significant market share of around 37.6% in 2025. The market is driven by increasing applications in regenerative medicine, ophthalmology, and wound care due to its anti-inflammatory, anti-scarring, and healing properties. Rising cases of ocular disorders, burns, and diabetic foot ulcers, coupled with growing awareness among clinicians about the clinical benefits of amniotic grafts, are boosting demand. Additionally, advancements in tissue preservation techniques, expanding healthcare infrastructure, and rising adoption of amniotic products in surgical procedures are augmenting the amniotic membrane market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 1.8 Billion |

|

Market Forecast in 2034

|

USD 3.4 Billion |

|

Market Growth Rate (2026-2034)

|

7.33% |

The market is experiencing notable expansion due to the widening scope of regenerative medicine applications and the incorporation of amniotic-derived products in aesthetic procedures. Additionally, the increasing awareness regarding the wound-healing benefits of cryopreserved and lyophilized membranes is also encouraging demand. Moreover, strategic collaborations between biopharmaceutical firms and tissue banks are supporting product innovations and wider clinical access. The shift toward outpatient and ambulatory care is contributing significantly to the demand for amniotic membrane products. As surgical procedures increasingly transition to non-hospital settings, the need for efficient, biologically compatible wound-healing solutions has risen. Industry reports project a 4% annual growth rate in the ambulatory surgery center (ASC) market between 2017 and 2027 in the United States. This expansion aligns with the broader adoption of amniotic membranes in procedures such as ophthalmic surgeries, dermatological interventions, and soft tissue repair, where rapid recovery and reduced complications are prioritized. The convenience and efficacy of amniotic-based grafts make them well-suited for integration within ASC treatment protocols.

To get more information on this market Request Sample

In the United States, the market is benefiting from the steady adoption of advanced wound management solutions across outpatient and specialty care clinics. Furthermore, heightened clinical interest in biologic dressings for managing diabetic foot ulcers and ocular surface disorders is supporting demand growth. One of the significant emerging amniotic membrane market trends is robust research funding and a highly structured regulatory environment, which are accelerating the clinical adoption of novel applications. For instance, the biggest public funder of biomedical research worldwide is the National Institutes of Health, which is a United States federal agency. The NIH spends the majority of its around USD 48 Billion funding on medical research with the goal of enhancing quality of life and reducing the prevalence of illness and disability. The proliferation of biotechnology startups specializing in placental tissue processing is introducing innovative delivery formats. Enhanced clinician training and awareness campaigns by industry players are also contributing to the expanding utilization of amniotic membrane therapies nationwide.

Amniotic Membrane Market Trends:

Increasing Demand for Regenerative Medicine

The rising prevalence of several chronic conditions like diabetes and rheumatoid arthritis, leading to chronic wounds and ulcers is increasing the need for effective treatment methods. The World Health Organization (WHO) reported that the number of people living with diabetes increased from 200 million in 1990 to 830 million in 2022. Amniotic membranes offer an innovative solution and stimulate the healing process. Apart from this, the growing global geriatric population, which is highly susceptible to various health conditions is driving the need for treatments that promote faster healing and tissue regeneration. Furthermore, the increasing adoption of amniotic membranes in various medical specialties like orthopedics and dental medicine is positively impacting the amniotic membrane market outlook. Moreover, the ability of the amniotic membrane to facilitate cellular growth and decrease inflammation is driving its adoption in other regenerative treatments.

Technological Advancements in Medical Procedures

The integration of advanced technologies is resulting in the development of amniotic membranes with increased efficiency and efficacy. Modern techniques ensure that essential growth factors and healing properties are maintained, enhancing their applicability in various medical domains. The compatibility of the amniotic membrane with cutting-edge treatments, such as stem cell therapies and three-dimensional (3D) bioprinting, is offering a favorable market outlook. Stem cell treatments, in particular, are seeing increased adoption due to strong clinical evidence supporting their effectiveness. For instance, in multiple sclerosis, patients who received autologous hematopoietic stem cell transplants experienced a 19% improvement in disability over five years, compared to just a 4% improvement in those receiving medication alone. These integrations allow for more personalized and effective treatments and enhance the quality of patient care. Apart from this, improved preservation methods allow for longer shelf life and wider distribution, which is increasing its adoption across various regions and healthcare systems. This, in turn, is contributing to amniotic membrane market growth.

Supportive regulatory environment

Regulatory bodies of various countries are recognizing the therapeutic value of the amniotic membrane and implementing clear and well-defined guidelines for the extraction, processing, preservation, and application of amniotic membranes. These guidelines ensure uniformity in practices and uphold the quality of products. Apart from this, regulatory authorities are actively monitoring the market to ensure compliance with all relevant rules and standards. Regular inspections, audits, and reporting requirements help maintain trust and integrity in the industry. Furthermore, they are offering supportive policies, which include grants, incentives, and public-private partnerships that encourage research and development in the field. As such, in 2025, MTF Biologics awarded over USD 1 Million in grants for allograft translational research. Notable recipients include Dr. Derrick Wan, exploring umbilical cord amnion and chorion allografts for wound healing, and Dr. Sameer Shakir, studying amniotic membrane in cleft lip/palate treatments. Collaborative efforts with research institutions can drive innovation and bring novel products and therapies to market.

Amniotic Membrane Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global amniotic membrane market, along with forecasts at the global, regional, and country levels from 2026-2034. The market has been categorized based on product, application, and end user.

Analysis by Product:

- Cryopreserved Amniotic Membrane

- Lyophilization Amniotic Membrane

Cryopreserved amniotic membrane leads the market with around 64.5% of market share in 2025. It has a long shelf life, and it allows hospitals and clinics to maintain an inventory without the risk of degradation. It also offers ease of storage, simplifies logistics, and reduces waste. Additionally, it aids in maintaining the biological integrity of the amniotic membrane and enhancing the therapeutic effectiveness of the membrane. This ability to retain the natural healing properties is attracting healthcare providers. Apart from this, regulatory bodies are recognizing the benefits of cryopreservation and are actively providing supportive guidelines and approvals. This support from regulatory authorities is promoting the adoption of cryopreserved amniotic membranes across different regions.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Surgical Wounds

- Ophthalmology

- Others

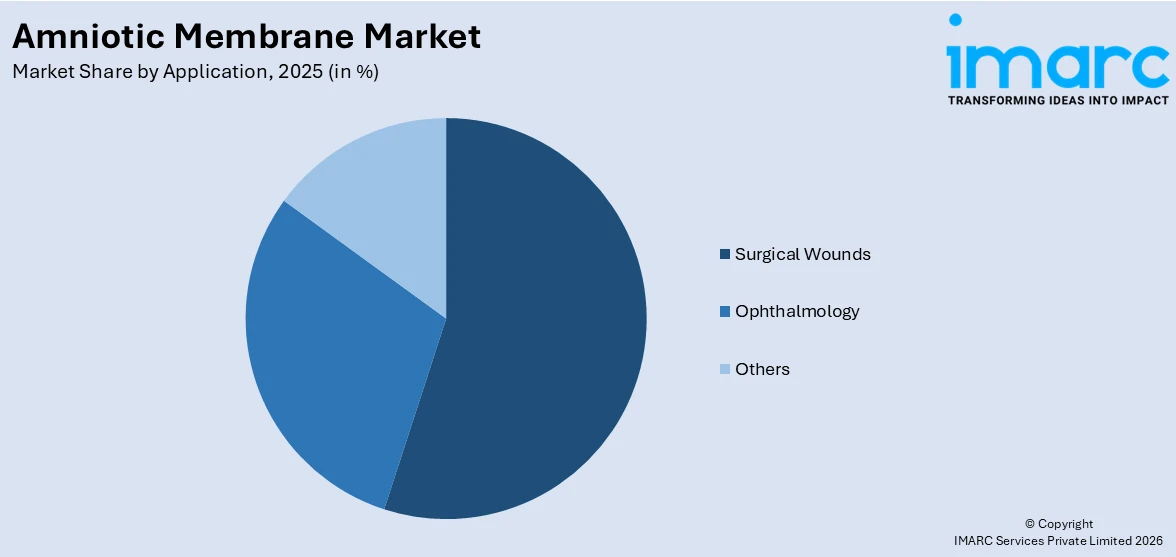

Surgical wounds lead the market with around 45.3% of market share in 2025. Increasing road accidents and major sports injuries are leading to a rise in elective and emergency surgeries across various medical disciplines, which is catalyzing the need for effective wound care. Additionally, technological advancements in surgical procedures are allowing for more complex and numerous surgeries to be performed with optimal efficiency. Apart from this, the rising focus on minimizing post-operative infections and complications is driving the demand for high-quality wound care products. The growing awareness about the importance of infection prevention and control is encouraging healthcare providers and patients to opt for optimal wound care solutions. Furthermore, rising preferences for effective healing without significant scarring is leading to innovations in wound care products specifically designed for surgical wounds.

Analysis by End User:

- Hospitals

- Ambulatory Surgical Centers

- Specialized Clinics

- Research Centers and Laboratory

Hospitals lead the market with around 55% of market share in 2025. Hospitals have specialized medical professionals and skilled staff trained to deal with various medical conditions. They can offer enhanced diagnostic and therapeutic procedures as they are equipped with technologically advanced medical equipment. Apart from this, they provide emergency medical services and handle urgent and life-threatening situations, which is offering a favorable market outlook. Furthermore, many hospitals have established relationships with insurance providers, facilitating easier and more comprehensive coverage for patients, which makes hospital-based care more accessible for many individuals. Moreover, hospitals in various regions receive government funding and support, which ensures the availability of essential healthcare services to the wider population.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

In 2025, North America accounted for the largest market share of over 37.6%. The region is home to leading research institutions and biotechnology companies that actively invest in the research and development (R&D) activities of regenerative medicine, including amniotic membranes. Additionally, the region has a highly developed healthcare system with state-of-the-art facilities and technology, which drives innovation and facilitates the adoption of advanced medical products, such as amniotic membranes. Apart from this, supportive regulatory guidelines for the development, approval, and use of amniotic membrane products in North America is encouraging manufacturers to expand their market reach. Furthermore, collaborations between hospitals, research institutions, and biotechnology companies is enhancing innovation and market penetration in the region.

Key Regional Takeaways:

United States Amniotic Membrane Market Analysis

In 2025, the United States holds a substantial share of around 89.65% of the market share in North America. The market is primarily driven by the increasing demand for advanced wound care solutions due to rising incidences of chronic wounds and burn injuries. According to NCBI, chronic wounds affect approximately 2.5% of the U.S. population, placing significant burdens on both patients and healthcare systems. In line with this, the growing adoption of minimally invasive surgical procedures enhancing the use of amniotic membranes in tissue regeneration, is propelling market growth. Similarly, continual advancements in stem cell therapies and their integration with amniotic membrane applications are contributing to the market's expansion. The increasing prevalence of eye-related conditions such as dry eye disease and corneal injuries is supporting demand for amniotic membrane-based treatments in the market. Industry research indicates that nearly 16 million people in the country are living with dry eye disease (DED). Furthermore, stringent regulatory approvals and the growing recognition of amniotic membranes' therapeutic benefits by healthcare authorities are encouraging wider product usage. The expanding healthcare infrastructure and rising healthcare expenditures in the U.S. are providing a favorable environment for market development. Moreover, the emerging trend of personalized medicine is also augmenting the market progress.

Europe Amniotic Membrane Market Analysis

The market in Europe is experiencing growth due to the increasing prevalence of ophthalmic disorders, such as corneal damage and dry eye disease. In accordance with this, the growing elderly population in Europe, which is more susceptible to chronic wounds and degenerative conditions, is propelling market growth. The continual advancements in regenerative medicine, including stem cell therapy, enhancing the use of amniotic membranes in tissue repair and regeneration, are strengthening market demand. Furthermore, the rising number of surgical procedures, particularly in orthopedics and plastic surgery, is encouraging the adoption of amniotic membranes for post-surgical recovery. In 2024, the UK saw a 5% increase in cosmetic surgery, with 27,462 procedures performed. Popular surgeries included breast augmentations (up 6%), liposuction (up 8%), and tr(up 8%), according to the British Association of Aesthetic Plastic Surgeons (BAAPS). The favorable regulatory environment within the European Union, along with approvals for innovative therapies, is fostering market expansion. Similarly, greater awareness of the therapeutic potential of amniotic membranes among healthcare professionals is accelerating market accessibility. Moreover, increasing investments in healthcare infrastructure and research and development (R&D) are expanding the market reach.

Asia Pacific Amniotic Membrane Market Analysis

The Asia Pacific market is advancing attributed to the rising prevalence of chronic conditions, such as diabetic foot ulcers and corneal diseases. An industry research study estimates that the pooled prevalence of diabetic foot ulcers (DFUs) in India is 6.2%. Subgroup analysis showed a higher prevalence in males (14.5%) compared to females (7.7%). In addition to this, increasing healthcare infrastructure investments in emerging economies are contributing to market expansion. Furthermore, the growing acceptance of regenerative medicine and tissue engineering stimulating the use of amniotic membranes in various medical applications, is impelling the market. Similarly, ongoing advancements in medical technologies and surgical techniques improving the efficacy of amniotic membrane products are supporting amniotic membrane market demand. The growing government support through regulatory frameworks and funding encouraging innovation in the field is bolstering market development. Besides this, the increasing focus on wound care, particularly in aging populations, is providing an impetus to the market.

Latin America Amniotic Membrane Market Analysis

In Latin America, the market is progressing propelled by the increasing burden of chronic diseases, such as diabetes and cardiovascular conditions. The International Diabetes Federation (IDF) reported that by 2021, approximately 341 million adults aged 20 to 79 in South and Central America were living with diabetes. The five countries with the highest number of diabetic individuals were Brazil, Colombia, Venezuela, Argentina, and Chile. Similarly, growing healthcare awareness among the population is contributing to greater adoption of regenerative therapies in the market. Additionally, the expansion of medical tourism in countries like Mexico and Brazil augmenting the demand for high-quality medical treatments, is impelling the market. Moreover, the region’s shifting regulatory environment supporting the introduction of innovative amniotic membrane products, is further driving market growth.

Middle East and Africa Amniotic Membrane Market Analysis

The market in the Middle East and Africa is experiencing growth due to the rising prevalence of traumatic injuries and burns. NCBI reported that in 2021, over 42 million people in sub-Saharan Africa were affected by injuries. Nigeria accounted for 16% of this total. Southern sub-Saharan Africa recorded 104 deaths per 100,000 from injuries, twice as high as the rate in western sub-Saharan Africa. Furthermore, the growing adoption of regenerative medicine in the region accelerating the use of amniotic membranes, is fostering market expansion. Additionally, increasing healthcare investments and infrastructure development are enhancing the availability and accessibility in the market. Apart from this, the region’s expanding medical tourism industry promoting the use of cutting-edge treatments, including amniotic membrane-based products, is positively influencing the market.

Competitive Landscape:

The competitive landscape of the market is characterized by ongoing innovations, product segmentation, and increased spending on clinical studies. Players are working to enhance sophisticated preservation technologies and build uses in surgical practices, wound care, and ophthalmic practices. Regulation permits and quality approval remain instrumental for determining credibility as well as attaining market penetration. Hospital, research center, and surgery center partnerships are emerging as new ways of expanding customer bases. Competition also exists on the basis of the type of membrane (cryopreserved or dehydrated), with companies seeking to enhance shelf-life and therapeutic effectiveness. The barriers to entry are moderate, with manufacturing expertise and adherence to safety regulations being the key. According to the amniotic membrane market forecast, competition is expected to intensify as more companies enter the space and existing players broaden their offerings, driven by rising demand for biologics-based therapies and expanding use of amniotic membranes in regenerative medicine.

The report provides a comprehensive analysis of the competitive landscape in the amniotic membrane market with detailed profiles of all major companies, including:

- Amnio Technology LLC

- Amniox Medical Inc. (TissueTech Inc.)

- Genesis Biologics

- Human Regenerative Technologies LLC

- Integra LifeSciences Holdings Corporation

- Katena Products Inc.

- MiMedx Group

- Next Biosciences

- Skye Biologics Holdings LLC

- Smith & Nephew plc

- Surgenex LLC

- Ventris Medical LLC

- Wright Medical Group N.V. (Stryker B.V.).

Latest News and Developments:

- January 2025: BioStem Technologies launched the BR-AM-DFU clinical trial to evaluate Vendaje, an amniotic membrane-based product, for treating non-healing diabetic foot ulcers. The study aims to showcase the effectiveness of BioREtain technology in advanced wound care.

- October 2024: BioLab Holdings launched the Tri-Membrane Wrap, a robust amniotic skin substitute designed to protect deep wounds in difficult-to-cover areas. Its triple-layer Amnion-Chorion-Amnion tissue offers increased tensile strength, allowing for suturing.

- June 2024: Axogen launched Avive+ Soft Tissue Matrix, a resorbable, multi-layer amniotic membrane allograft designed to protect and separate tissues during the critical phase of peripheral nerve healing. This product complements Axogen's portfolio, addressing nerve injuries and enhancing patient outcomes in surgical nerve protection and repair.

- May 2024: BioTissue introduced the CAM360 AmnioGraft, a cryopreserved amniotic membrane for treating dry eye disease and other ocular surface conditions. Using proprietary SteriTrek technology, CAM360 is shelf-stable, hydrated, and provides anti-inflammatory, anti-scarring, and anti-angiogenic benefits. It also supports corneal nerve regeneration and epithelial healing.

- April 2024: SimpliGraft and SimpliMax, amniotic membrane allografts intended for both acute and chronic wounds, have been commercially launched by Xtant Medical. These dehydrated, irradiated membrane sheets provide protective coverage.

Amniotic Membrane Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Cryopreserved Amniotic Membrane, Lyophilization Amniotic Membrane |

| Applications Covered | Surgical Wounds, Ophthalmology, Others |

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Specialized Clinics, Research Centers and Laboratory |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Amnio Technology LLC, Amniox Medical Inc. (TissueTech Inc.), Genesis Biologics, Human Regenerative Technologies LLC, Integra LifeSciences Holdings Corporation, Katena Products Inc., MiMedx Group, Next Biosciences, Skye Biologics Holdings LLC, Smith & Nephew plc, Surgenex LLC, Ventris Medical LLC and Wright Medical Group N.V. (Stryker B.V.), etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the amniotic membrane market from 2020-2034.

- The amniotic membrane market research report provides the latest information on the market drivers, challenges, and opportunities in the global market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the amniotic membrane industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Amniotic Membrane Market Report

The amniotic membrane market was valued at USD 1.8 Billion in 2025.

The amniotic membrane market is projected to exhibit a CAGR of 7.33% during 2026-2034, reaching a value of USD 3.4 Billion by 2034.

The market is driven by the rising demand for regenerative medicine, increasing prevalence of chronic wounds and burns, growing number of ophthalmic surgeries, and advancements in tissue preservation techniques. Rising awareness regarding amniotic membrane benefits and its wide applications in surgical wound care and stem cell research are also contributing to market growth.

North America currently dominates the amniotic membrane market with a market share of around 37.6%. The dominance is fueled by the advanced healthcare infrastructure, increased adoption of innovative wound care products, rising surgical procedures, favorable reimbursement policies, and strong presence of key market players investing in R&D and clinical trials.

Some of the major players in the amniotic membrane market include Amnio Technology LLC, Amniox Medical Inc. (TissueTech Inc.), Genesis Biologics, Human Regenerative Technologies LLC, Integra LifeSciences Holdings Corporation, Katena Products Inc., MiMedx Group, Next Biosciences, Skye Biologics Holdings LLC, Smith & Nephew plc, Surgenex LLC, Ventris Medical LLC and Wright Medical Group N.V. (Stryker B.V.), among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)