Anti-corrosion Coatings Market Report by Technology (Solvent-based, Water-based, Powder, and Others), Material (Acrylic, Alkyd, Polyurethane, Epoxy, Zinc, and Others), Application (Oil and Gas, Marine, Building and Construction, Automotive and Rail, Aerospace and Defense, and Others), and Region 2026-2034

Anti-corrosion Coatings Market Size:

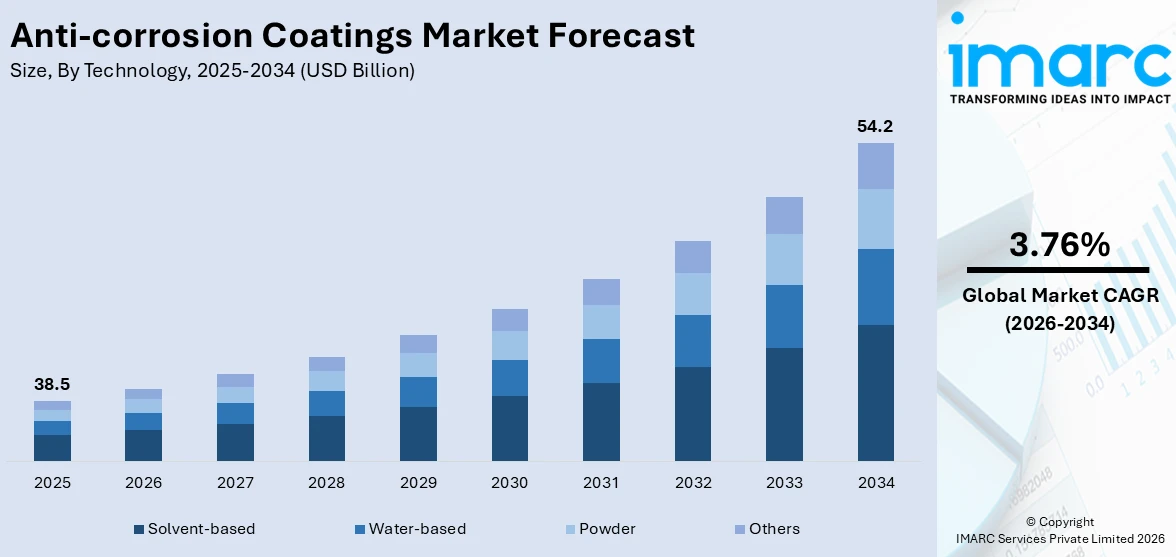

The global anti-corrosion coatings market size reached USD 38.5 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 54.2 Billion by 2034, exhibiting a growth rate (CAGR) of 3.76% during 2026-2034. Asia-Pacific dominates the market, driven by increasing infrastructure development and rapid advancements in coating technologies. The market is also experiencing robust growth due to the expanding item demand in the marine, automotive, and aerospace industries and the rising product utilization in the oil and gas sector.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

|

Market Size in 2025

|

USD 38.5 Billion |

|

Market Forecast in 2034

|

USD 54.2 Billion |

| Market Growth Rate 2026-2034 | 3.76% |

At present, rapid industrial growth and infrastructure development are catalyzing the demand for anti-corrosion coatings that prolong the lifespan of equipment and building materials subjected to severe conditions. The shipping and marine industry is a significant driver, as vessels, terminals, and offshore facilities need safeguarding from constant exposure to moisture, seawater, and chemicals. The automotive and aerospace industries are driving the demand, as manufacturers utilize advanced coatings to boost durability, lower maintenance expenses, and extend the lifespan of valuable components. Increasing environmental regulations are motivating industries to adopt sustainable solutions like waterborne, powder, and high-solid coatings that reduce volatile organic compound (VOC) emissions while providing robust protection. Furthermore, innovations in technology, such as the creation of nano-coatings and smart coatings with self-repairing features, are generating new possibilities.

To get more information on this market Request Sample

Anti-corrosion Coatings Market Trends:

Expanding oil and gas exploration projects

Rising oil and gas exploration projects are positively influencing the market, as equipment and infrastructure in this sector are constantly exposed to harsh environments, such as saltwater, chemicals, and extreme temperatures. Pipelines, storage tanks, rigs, and offshore platforms require durable protective coatings to prevent corrosion, leaks, and costly downtime. Anti-corrosion coatings extend asset life, reduce maintenance costs, and ensure safety in high-risk operations. With increasing exploration in deepwater and unconventional reserves, the demand for high-performance coatings that offer superior resistance and durability is rising. The need to optimize operational efficiency and comply with stringent safety standards is further strengthening the adoption of anti-corrosion coatings. As the oil and gas sector continues to thrive worldwide, the reliance on anti-corrosion coatings is growing. As per the IMARC Group, the global oil and gas market is set to attain USD 72.6 Billion by 2033, exhibiting a CAGR of 15.21% from 2025-2033.

Broadening of transportation networks

The expansion of transportation networks, including roads, railways, bridges, ports, and airports, is driving the demand for anti-corrosion coatings, as these large-scale infrastructures are highly susceptible to wear from moisture, chemicals, and environmental exposure. In March 2025, Indian Railways intended to allocate INR 16.7 Lakh Crore by 2031 for infrastructure initiatives, including station improvements, high-speed rail networks, and track electrification. Important initiatives involved the renovation of 1,309 railway stations and the extension of exclusive freight corridors. Steel structures, bridges, and tunnels need protective coatings to maintain durability and reduce costly repairs. In addition, rolling stock, cargo ships, and airport facilities require advanced coatings to extend service life and ensure safety under continuous usage. With government agencies investing heavily in modernizing and expanding transport infrastructure, long-term protection solutions have become a necessity. Anti-corrosion coatings not only enhance durability but also lower maintenance expenses, making them a cost-effective choice for large projects.

Rising defense budgets

Increasing defense budgets worldwide are significantly strengthening the market growth, as military equipment, vehicles, aircraft, and naval assets require long-lasting protection against harsh environmental conditions. As per the 2025 FYDP, the Department of Defense’s (DoD) budget is projected to rise to USD 866 Billion by 2029, marking a total increase of 1.9% from 2025. Defense assets often operate in extreme terrains, ranging from deserts to oceans, where exposure to humidity, salinity, and chemicals accelerates corrosion risks. Anti-corrosion coatings ensure operational readiness, extend the life of high-value defense equipment, and decrease maintenance costs. Naval ships, submarines, and aircraft are especially reliant on advanced coatings to prevent surface degradation. With government agencies prioritizing defense modernization and expanding fleets, the demand for durable and high-performance coatings is increasing. The focus on safety, performance, and lifecycle cost reduction is making anti-corrosion solutions indispensable in defense applications.

Key Growth Drivers of Anti-corrosion Coatings Market:

Technological advancements

Technological advancements are improving performance, sustainability, and application efficiency. Innovations in waterborne, solvent-free, and high-solid coatings are reducing VOC emissions, aligning with environmental standards while maintaining durability. Developments in smart coatings with self-healing and corrosion-sensing capabilities are offering enhanced asset protection in critical industries. Nano-technology has enabled coatings with superior barrier properties, chemical resistance, and thinner layers. Additionally, improvements in application techniques, such as advanced spray systems and robotic coating applications, are enhancing precision and cost-effectiveness. These innovations are expanding the usability of anti-corrosion coatings across oil and gas, marine, automotive, and construction industries. As numerous industries are demanding sustainable and robust solutions, technological progress is fueling strong market growth.

Rising environmental regulations

Environmental regulations are strongly propelling the market growth, as government agencies and regulatory bodies are implementing stringent standards on volatile VOC emissions, waste disposal, and sustainability in industrial processes. Traditional solvent-based coatings are being replaced with eco-friendly alternatives, such as waterborne, powder, and high-solid coatings that minimize environmental impact while maintaining high protective performance. Industries are under increasing pressure to adopt sustainable solutions to ensure compliance and avoid penalties, which has accelerated innovations in green coatings. Additionally, regulations aimed at promoting circular economy practices and asset longevity are supporting the use of durable anti-corrosion coatings that decrease resource wastage. As industries balance operational needs with sustainability goals, the demand for environmentally compliant, high-performance coatings continues to rise.

Increasing demand from power generation sector

Power plants operate in highly challenging environments where equipment and infrastructure are constantly exposed to heat, moisture, and chemicals. Thermal power plants face corrosion risks from high-temperature steam and cooling water systems, while nuclear plants require coatings with superior resistance to radiation and chemical exposure. Similarly, renewable energy facilities, such as wind and hydro power, rely on protective coatings to safeguard turbines, blades, and underwater components against wear and corrosion. Anti-corrosion coatings enhance durability, minimize costly downtime, and extend the service life of critical assets, ensuring uninterrupted energy supply. With the growing global energy demand and expansion of both conventional and renewable power projects, the reliance on advanced protective coatings continues to strengthen.

Anti-corrosion Coatings Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on technology, material, and application.

Breakup by Technology:

- Solvent-based

- Water-based

- Powder

- Others

Solvent-based accounts for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the technology. This includes solvent-based, water-based, powder, and others. According to the report, solvent-based represented the largest segment.

As per the anti-corrosion coatings market trends, solvent-based coatings represented the largest segment due to their superior performance characteristics and versatility. These coatings are favored for their excellent adhesion, durability, and resistance to harsh environmental conditions, making them ideal for protecting infrastructure, marine vessels, automotive parts, and industrial equipment. Moreover, their ability to form robust and protective barriers against moisture, chemicals, and abrasion to ensure prolonged structural integrity and reduce maintenance costs is fostering the market growth. In addition to this, the ongoing innovations that enhance their eco-friendliness without compromising effectiveness are positively impacting the anti-corrosion coatings market size.

Breakup by Material:

- Acrylic

- Alkyd

- Polyurethane

- Epoxy

- Zinc

- Others

Epoxy holds the largest share of the industry

A detailed breakup and analysis of the market based on the material have also been provided in the report. This includes acrylic, alkyd, polyurethane, epoxy, zinc, others. According to the report, epoxy accounted for the largest market share.

Based on the anti-corrosion coatings market outlook, epoxy coatings dominated the market due to their exceptional protective qualities, including high durability, strong adhesion, and superior resistance to chemicals and moisture. They are utilized for a wide range of applications, such as industrial, marine, automotive, and infrastructure projects. Epoxy coatings are effective in harsh environments, as they provide a robust barrier against corrosion to extend the lifespan of metal and concrete structures. Moreover, the versatility of epoxy formulations that allow for customization to meet specific performance requirements, is enhancing the anti-corrosion coatings market growth.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Oil and Gas

- Marine

- Building and Construction

- Automotive and Rail

- Aerospace and Defense

- Others

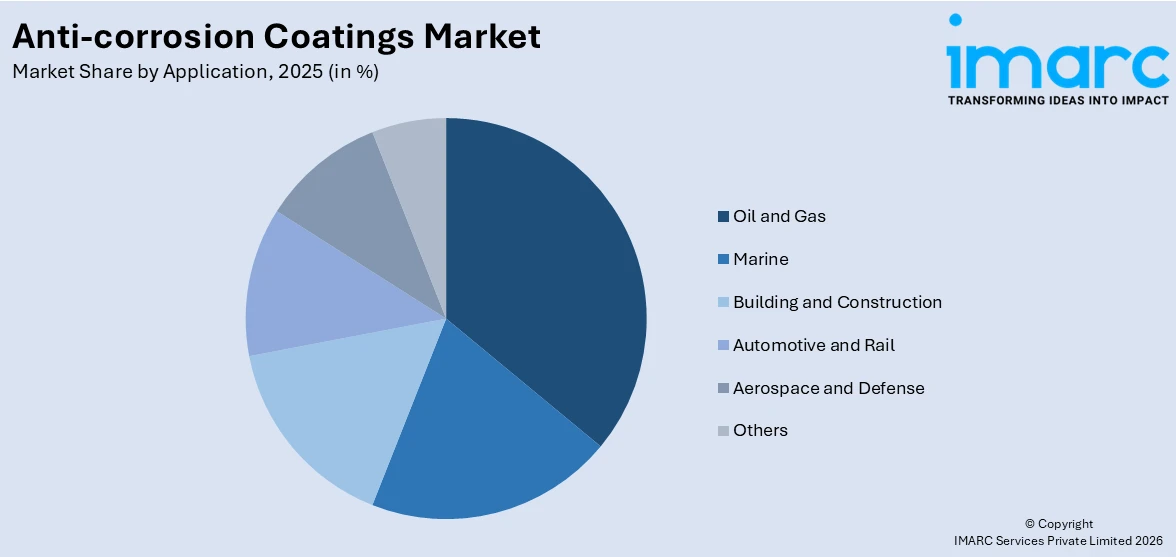

Oil and gas represent the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes oil and gas, marine, building and construction, automotive and rail, aerospace and defense, and others. According to the report, oil and gas represented the largest segment.

According to the anti-corrosion coatings market insights, the oil and gas sector accounted for the largest market share, driven by the industry's critical need for robust corrosion protection in harsh environments. Along with this, the reliance of this sector on extensive infrastructure, including pipelines, storage tanks, refineries, and offshore platforms, that are highly susceptible to corrosion due to constant exposure to seawater, chemicals, and extreme temperatures is fueling the market growth. Anti-corrosion coatings are essential for preventing leaks, spills, and structural failures, thereby ensuring operational efficiency, safety, and regulatory compliance.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

Asia Pacific leads the market, accounting for the largest anti-corrosion coatings market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, Asia Pacific represents the largest regional market for anti-corrosion coatings.

Based on the anti-corrosion coatings market overview, the Asia Pacific region is dominating the market, driven by its rapid industrialization, urbanization, and infrastructure development. Moreover, the burgeoning construction sector, expanding marine and automotive industries, and significant investments in oil and gas exploration and production, necessitating the widespread use of anti-corrosion coatings to protect assets from harsh environmental conditions, are boosting the market growth. Additionally, the imposition of government initiatives and increased spending on public infrastructure projects, coupled with a growing manufacturing base, are fueling the anti-corrosion coatings market demand.

Competitive Landscape:

- The market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the anti-corrosion coatings industry include Akzo Nobel N.V., Ashland, Axalta Coating Systems LLC, BASF SE, Hempel A/S, Jotun, Kansai Paint Co. Ltd., PPG Industries Inc., RPM International Inc., Sika AG, The Sherwin-Williams Company, etc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- The major players in the market are pursuing strategies to strengthen their market position and meet evolving customer needs. They are investing in research and development (R&D) to innovate and enhance their product offerings by focusing on advanced formulations that provide superior protection while being environmentally friendly. Moreover, some companies are expanding their production capacities and geographic reach through strategic acquisitions and partnerships, particularly in high-growth regions. Additionally, they are focusing on developing low-volatile organic compounds (VOC) and water-based coatings, which are gaining popularity for their reduced environmental impact.

Anti-corrosion Coatings Market News:

- March 2025: A study, featured in Progress in Organic Coatings, showed that phosphate- and lignin-doped PEDOT polymers could improve the corrosion resistance of ultraviolet (UV)-cured acrylic coatings, providing an effective and eco-friendly substitute for traditional systems. Coatings containing 20 wt% PEDOT additives demonstrated greater impedance values and superior corrosion resistance compared to those with 60 wt%.

- March 2025: Sherwin-Williams Protective & Marine unveiled a broader range of Global Core products that maintained the similar standard and efficiency benchmarks globally. The updated Global Core coatings consisted of an inorganic zinc primer, an epoxy primer, an epoxy intermediate coat, and a urethane topcoat. These adaptable coatings could be utilized in numerous combinations alongside other products to form multi-layer coating systems aimed at corrosion protection and aesthetics.

- March 2025: Iranian scientists created an innovative nanocomposite coating that efficiently safeguarded magnesium alloys against corrosion, a development that might decrease aircraft weight and enhance fuel efficiency. When the protective layer sustained scratches or damage from environmental influences, the coating automatically detected the impacted region and prevented additional deterioration.

- February 2025: China's COSCO shipping group and Japanese paint firm Kansai Paint teamed up to create zinc-coated containers in a trial of the anti-corrosion technology. Favorable outcomes were observed when the coating was evaluated on a limited selection of Shanghai Universal's refrigerated containers.

- October 2024: A team, co-directed by researchers at Penn State, developed a synthesis method to generate a ‘rust-resistant’ coating with extra features suited for manufacturing quicker and more resilient electronics. The main goal was to enhance the overall quality of the composition and incorporate it into intricate designs.

Anti-corrosion Coatings Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Solvent-based, Water-based, Powder, Others |

| Materials Covered | Acrylic, Alkyd, Polyurethane, Epoxy, Zinc, Others |

| Applications Covered | Oil and Gas, Marine, Building and Construction, Automotive and Rail, Aerospace and Defense, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Akzo Nobel N.V., Ashland, Axalta Coating Systems LLC, BASF SE, Hempel A/S, Jotun, Kansai Paint Co. Ltd., PPG Industries Inc., RPM International Inc., Sika AG, The Sherwin-Williams Company, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global anti-corrosion coatings market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global anti-corrosion coatings market?

- What is the impact of each driver, restraint, and opportunity on the global anti-corrosion coatings market?

- What are the key regional markets?

- Which countries represent the most attractive anti-corrosion coatings market?

- What is the breakup of the market based on the technology?

- Which is the most attractive technology in the anti-corrosion coatings market?

- What is the breakup of the market based on the material?

- Which is the most attractive material in the anti-corrosion coatings market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the anti-corrosion coatings market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global anti-corrosion coatings market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the anti-corrosion coatings market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global anti-corrosion coatings market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the anti-corrosion coatings industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade