Antisense & RNAi Therapeutics Market Size, Share, Trends and Forecast by Technology, Route of Administration, Application, and Region, 2026-2034

Antisense & RNAi Therapeutics Market Size and Share:

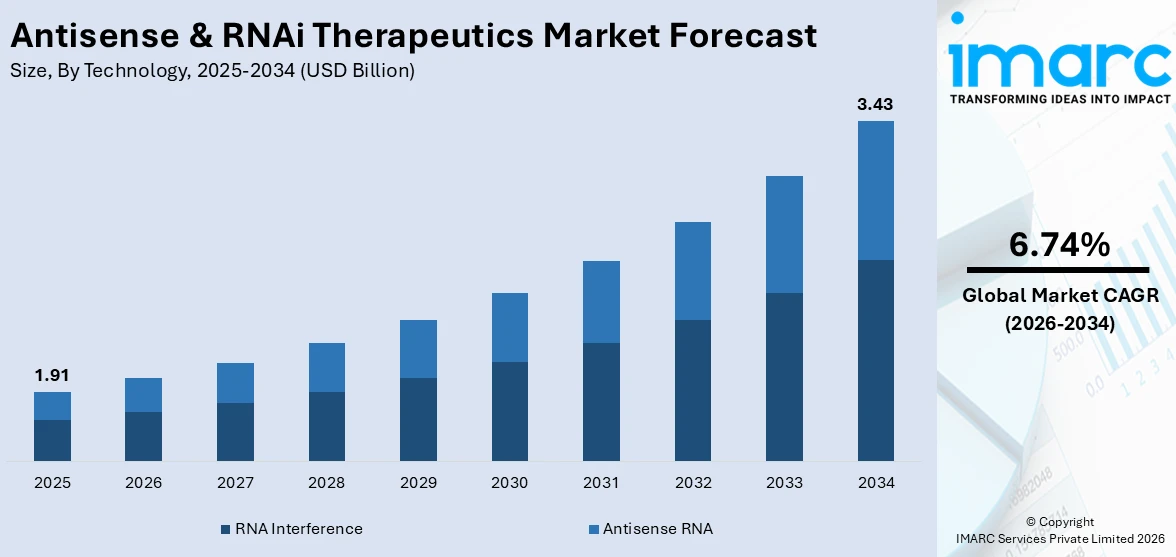

The global antisense & RNAi therapeutic market size was valued at USD 1.91 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 3.43 Billion by 2034, exhibiting a CAGR of 6.74% from 2026-2034. North America currently dominates the market, holding a market share of 40% in 2025. The region benefits from advanced biotechnology infrastructure, significant public and private research investment, a favorable regulatory environment enabling expedited therapy approvals, and high prevalence of genetic disorders among the population, all contributing to the antisense & RNAi therapeutics market share.

The global antisense & RNAi therapeutics market is experiencing robust expansion driven by several compelling factors. The rising global incidence of genetic, metabolic, and chronic diseases is generating unprecedented demand for targeted gene-silencing therapies that address molecular root causes rather than symptoms. Advancements in oligonucleotide chemistry, particularly the introduction of phosphorothioate backbones and chemical modifications, have significantly enhanced drug stability, specificity, and bioavailability. Growing scientific understanding of RNA biology is expanding the therapeutic landscape to previously untreatable conditions. Global investments in biopharmaceutical research and development are accelerating the identification of novel therapeutic targets. The ongoing proliferation of clinical trials investigating antisense oligonucleotide and RNAi platforms across multiple indications is broadening their applicability. The shift toward personalized medicine, driven by genomic profiling technologies, is also creating tailored treatment opportunities, reflecting positive antisense & RNAi therapeutics market outlook for this specialized and rapidly advancing modality.

The United States has emerged as a major region in the antisense & RNAi therapeutics market owing to many factors. The country hosts a dense network of world-class biotechnology companies, academic research institutions, and government-funded programs that collectively advance RNA-based therapeutic discovery. A robust regulatory framework administered by the FDA actively supports innovation through expedited pathways including Fast Track, Breakthrough Therapy Designation, and Accelerated Approval, enabling quicker clinical translation of oligonucleotide candidates. High patient awareness and participation in clinical trials supports pipeline development across rare genetic, neurodegenerative, and oncological indications. In 2025, Alnylam Pharmaceuticals, Inc., a top company in RNAi therapeutics, revealed its intention to expand its advanced manufacturing plant located in Norton, Massachusetts. The Company is set to invest $250 million to develop what is expected to be the industry's first fully dedicated, proprietary facility for siRNA enzymatic-ligation manufacturing. This investment is anticipated to greatly increase capacity, considerably lower production costs, and enable Alnylam to assist future launches within its expanding pipeline of possible new treatments

To get more information on this market Request Sample

Antisense & RNAi Therapeutics Market Trends:

Technological Advancements in Drug Delivery Systems

The rapid evolution of drug delivery technologies is a key factor propelling this therapeutic field. Lipid nanoparticles have emerged as the gold standard for delivering short interfering RNA and antisense oligonucleotides into target cells, improving cellular uptake and reducing nuclease-mediated degradation. GalNAc-siRNA conjugate platforms have revolutionized hepatic targeting, enabling precise delivery to liver cells at substantially lower doses compared to earlier formulations. These innovations have improved the therapeutic index of RNA-based medicines, enabling subcutaneous administration regimens that enhance patient compliance. Advanced chemical modifications including phosphorothioate linkages, 2’-O-methyl groups, and locked nucleic acid motifs have further extended the half-life and potency of oligonucleotide therapeutics. Research efforts in 2025 are increasingly focused on expanding delivery systems beyond the liver to reach muscle tissue, the central nervous system, and lung cells. Artificial intelligence is being integrated into oligonucleotide sequence design to improve target selectivity and minimize off-target effects.

Rising Prevalence of Genetic and Chronic Diseases

The escalating global burden of genetic, rare, and chronic diseases is significantly supporting the antisense & RNAi therapeutics market growth. Conditions such as Huntington’s disease, hereditary transthyretin amyloidosis, spinal muscular atrophy, and various hereditary cancers lack effective treatments using conventional pharmaceutical approaches, creating sustained demand for nucleic acid-based gene-silencing therapies. Antisense oligonucleotides and RNAi platforms offer a unique therapeutic advantage by selectively silencing disease-causing genes at the mRNA level, providing targeted intervention for conditions driven by aberrant protein expression. The growing aging global population is amplifying the prevalence of age-related genetic and degenerative disorders, expanding the addressable patient base for these therapeutics. According to the National Institutes of Health (NIH), over 7,000 rare diseases have been identified, with approximately 80% having a genetic origin, collectively affecting an estimated 300 million people worldwide. This enormous unmet medical need continues to generate strong research investments and robust pipeline expansion, reflecting growing antisense & RNAi therapeutics market trends across multiple therapeutic indications globally.

Favorable Regulatory Landscape for Novel Therapies

The supportive global regulatory environment represents a significant enabler of the antisense & RNAi therapeutics market forecast. Regulatory agencies including the FDA in the United States and the European Medicines Agency have implemented specialized mechanisms to accelerate the development and approval of novel nucleic acid therapeutics. Programs such as Orphan Drug Designation, Breakthrough Therapy Designation, Fast Track approval, and Priority Review vouchers provide meaningful incentives for companies to invest in antisense and RNAi development, particularly for rare and underserved disease areas. These designations reduce development timelines and associated costs, enabling smaller biotechnology firms to compete effectively alongside large pharmaceutical organizations. Accelerated pathways have facilitated a steady stream of approvals in this class, reinforcing commercial confidence in these modalities. In March 2025, the U.S. FDA approved Qfitlia (fitusiran), a subcutaneous siRNA therapeutic for hemophilia A or B, marking the sixth Alnylam-discovered RNAi medicine to receive U.S. market clearance and demonstrating the accelerating pace of regulatory advancement. This milestone reinforces investor confidence in the Antisense & RNAi Therapeutics sector’s long-term potential.

Antisense & RNAi Therapeutics Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global antisense & RNAi therapeutics market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on technology, route of administration, and application.

Analysis by Technology:

- RNA Interference

- siRNA

- miRNA

- Antisense RNA

RNA Interference holds 60% of the market share. RNA interference operates through small interfering RNA (siRNA) and microRNA (miRNA) molecules that engage the RNA-induced silencing complex (RISC) to achieve targeted gene silencing at the post-transcriptional level. This mechanism provides unparalleled precision in suppressing disease-causing gene expression, making it particularly effective for conditions where a specific pathogenic protein must be inhibited. The siRNA pathway has been the basis for several FDA-approved medicines, demonstrating proven clinical efficacy across hepatic, hematological, and neurological indications. Key advantages of RNAi over antisense approaches include greater potency at lower doses and catalytic activity within the RISC complex, enabling repeated cycles of gene silencing. Ongoing research into extra-hepatic delivery is expected to unlock new application areas including neurology, oncology, and muscle diseases, further solidifying the dominant position of RNA interference within this expanding market.

Analysis by Route of Administration:

- Intravenous Route

- Subcutaneous Route

- Intrathecal Route

- Pulmonary Delivery

- Intraperitoneal Injection

- Others

Intravenous Route leads the market with a share of 26%. The intravenous route enables systemic delivery of antisense oligonucleotides and RNAi therapeutics, facilitating rapid distribution throughout the bloodstream for conditions requiring broad biodistribution. Intravenous administration is particularly relevant for oncological and hematological applications where systemic circulation is essential for reaching tumor cells and blood-borne targets. Lipid nanoparticle-encapsulated RNAi therapeutics such as patisiran, the first FDA-approved siRNA drug, were initially formulated for intravenous delivery, establishing a strong clinical precedent for this administration route. The well-established hospital infusion infrastructure globally supports broad adoption of intravenous RNA therapeutics in developed healthcare markets. This route remains essential for the clinical management of conditions requiring rapid therapeutic effect or systemic distribution. Although newer formulations are transitioning toward subcutaneous delivery for improved patient convenience, the intravenous route retains a significant and well-validated position across multiple RNA therapeutic indications globally.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

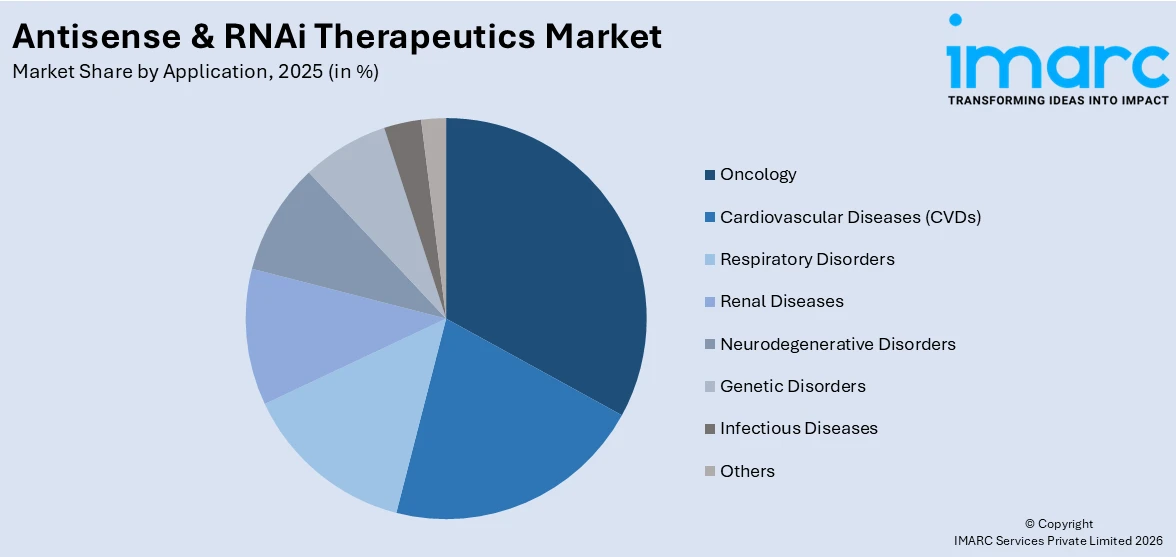

- Oncology

- Cardiovascular Diseases (CVDs)

- Respiratory Disorders

- Renal Diseases

- Neurodegenerative Disorders

- Genetic Disorders

- Infectious Diseases

- Others

Oncology dominates the market, with a share of 31%. The application of antisense oligonucleotides and RNAi therapeutics in oncology represents one of the most dynamic and rapidly growing segments in this field. Cancer, by its nature, is driven by aberrant gene expression, making it an ideal candidate for nucleic acid-based gene-silencing approaches. RNAi and antisense technologies enable selective suppression of oncogenes, resistance pathways, and immune evasion mechanisms that drive tumor growth and survival. Multiple RNAi-based oncology programs are currently advancing through clinical development pipelines, targeting genes such as VEGF, kinesin spindle protein, and various tumor-specific mRNAs. The growing understanding of cancer genomics, driven by next-generation sequencing, is identifying novel targetable sequences for antisense and RNAi drug design. This persistent unmet need across solid and hematological cancers continues to propel the Antisense & RNAi Therapeutics sector’s oncology-focused applications.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 40% of the share, enjoys the leading position in the market. The region’s dominance is underpinned by exceptional biotechnology infrastructure, world-class academic research institutions, substantial public and private sector R&D investment, and a regulatory environment that actively facilitates the development and commercialization of novel nucleic acid therapeutics. The United States in particular is home to pioneering companies that led the development of the world’s first approved antisense and RNAi medicines. High patient awareness, widespread reimbursement coverage, and strong healthcare spending collectively drive demand for advanced therapies across genetic, neurological, and cardiovascular indications. In 2025, variouspharmaceutical and biotechnology companies were actively working on antisense oligonucleotide programs in the United States, as reported by clinical pipeline analyses, highlighting the region’s exceptional research density. Canada also contributes to regional growth through government-funded biotechnology initiatives and a growing base of RNA therapeutics startups, further reinforcing North America’s leading regional position within the global landscape.

Key Regional Takeaways:

United States Antisense & RNAi Therapeutics Market Analysis

The United States is the world’s largest individual market for antisense & RNAi therapeutics, driven by a unique combination of scientific leadership, regulatory innovation, and healthcare infrastructure. The country’s biotechnology ecosystem, centered in regions such as Greater Boston, the San Francisco Bay Area, and Research Triangle Park, houses the largest concentration of RNA therapeutics companies globally. The National Institutes of Health (NIH) continues to direct substantial funding toward foundational RNA biology and clinical translation research, supporting a robust pipeline of investigational oligonucleotide therapies. Favorable reimbursement policies for approved specialty therapeutics, including orphan drugs, enable broad commercial uptake of high-cost RNA medicines across patient populations. The FDA’s commitment to novel therapy pathways, evidenced by multiple Breakthrough Therapy and Fast Track designations for antisense and RNAi candidates, significantly accelerates development timelines. In April 2025, the FDA granted Fast Track designation to BIIB080, an investigational antisense oligonucleotide targeting tau protein, for Alzheimer’s disease treatment, reflecting the agency’s supportive stance toward advanced nucleic acid medicines. The country’s large patient population with rare genetic disorders, neurological diseases, and oncological conditions continues to generate consistent demand for innovative gene-silencing therapies throughout the forecast period.

Europe Antisense & RNAi Therapeutics Market Analysis

Europe represents the second-largest region in the antisense & RNAi therapeutics market, supported by a mature pharmaceutical industry, strong academic research base, and harmonized regulatory frameworks coordinated by the European Medicines Agency. European countries including Germany, France, the United Kingdom, and Switzerland are home to internationally recognized biotechnology centers and academic institutions that actively contribute to RNA therapeutics innovation. The EMA has implemented favorable regulatory designations, including orphan medicine status and adaptive licensing pathways, to incentivize development of treatments for rare genetic diseases where antisense and RNAi approaches show strong promise. Reimbursement systems across major European markets support patient access to newly approved specialty therapies. High incidence of hereditary transthyretin amyloidosis, Duchenne muscular dystrophy, and rare genetic disorders in European patient populations continues to drive steady clinical demand.

Asia-Pacific Antisense & RNAi Therapeutics Market Analysis

Asia-Pacific is the fastest-growing region in the antisense & RNAi therapeutics market, driven by rapidly expanding healthcare infrastructure, increasing biotechnology investment, and growing patient awareness of advanced gene-silencing therapies. Countries such as China, Japan, South Korea, and India are intensifying domestic research and development capabilities in nucleic acid therapeutics, with several local biotechnology companies pursuing RNAi-based programs. Government initiatives across the region are supporting the development of RNA-based precision medicines as part of broader national biotechnology strategies. According to the World Health Organization (WHO), Asia-Pacific was home to over 4.7 billion people as of 2024, representing one of the world’s largest patient pools for rare, genetic, and chronic diseases requiring advanced therapeutic interventions. The expansion of clinical trial activity and growing regulatory harmonization with international standards are positioning Asia-Pacific as a key growth engine for the global Antisense & RNAi Therapeutics sector.

Latin America Antisense & RNAi Therapeutics Market Analysis

Latin America represents an emerging growth opportunity in the antisense & RNAi therapeutics market, underpinned by a growing patient population, rising healthcare expenditure, and increasing government focus on advanced biopharmaceutical access. Brazil and Mexico lead regional activity, with expanding clinical trial participation and evolving regulatory frameworks being developed to accommodate novel genetic medicines. Growing awareness of rare disease management, supported by patient advocacy organizations and international pharmaceutical partnerships, is enhancing access to approved RNA therapeutics. Moreover, the heightened occurrence of new cancer diagnoses in 2024 is highlighting the significant unmet need for targeted oncology therapeutics including gene-silencing modalities and underscoring the region’s long-term market potential.

Middle East and Africa Antisense & RNAi Therapeutics Market Analysis

The Middle East and Africa market for antisense & RNAi therapeutics is at an early development stage but exhibits meaningful long-term potential. Gulf Cooperation Council countries, particularly Saudi Arabia and the United Arab Emirates, are investing substantially in healthcare infrastructure modernization and advanced pharmaceutical access as part of national economic diversification strategies. Growing awareness of genetic diseases and rare conditions, combined with rising healthcare expenditure, is creating demand for specialized therapies. According to the World Health Organization (WHO), the Middle East and Africa region recorded a major number of new cancer cases in 2024, highlighting growing unmet therapeutic need and creating incremental opportunities for the adoption of innovative antisense and RNAi therapies across the region.

Competitive Landscape:

The antisense & RNAi therapeutics market is characterized by a dynamic competitive environment comprising established pharmaceutical leaders, dedicated RNA therapeutics companies, and innovative biotechnology entrants. Leading players maintain competitive positions through proprietary delivery platform technologies, extensive patent portfolios covering oligonucleotide chemistry and target sequences, and robust clinical pipelines spanning multiple disease indications. Strategic alliances between large pharmaceutical companies and specialized RNA biotechnology firms have become a defining feature of the competitive landscape, enabling shared expertise in drug development and commercialization. Companies are increasingly leveraging conjugate delivery technologies, particularly GalNAc-siRNA systems, to differentiate their product candidates through improved potency, selectivity, and dosing convenience. Manufacturing scale-up has emerged as a key competitive dimension, with major players investing in proprietary production platforms to reduce costs and support pipeline expansion. Ongoing competition for orphan drug designations and breakthrough therapy status provides an additional avenue for differentiation in this specialized and rapidly evolving market.

The report provides a comprehensive analysis of the competitive landscape in the antisense & RNAi therapeutics market with detailed profiles of all major companies, including:

- Alnylam Pharmaceuticals Inc.

- Arbutus Biopharma Corporation

- Arrowhead Pharmaceuticals Inc.

- Benitec Biopharma Ltd.

- Bio-Path Holdings Inc.

- Dicerna Pharmaceuticals Inc. (Novo Nordisk A/S)

- Ionis Pharmaceuticals Inc.

- OliX Pharmaceuticals Inc.

- Phio Pharmaceuticals Corp.

- Sarepta Therapeutics Inc.

- Silence Therapeutics

- Sirnaomics Inc.

Antisense & RNAi Therapeutics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered |

|

| Route of Administrations Covered | Intravenous Route, Subcutaneous Route, Intrathecal Route, Pulmonary Delivery, Intraperitoneal Injection, Others |

| Applications Covered | Oncology, Cardiovascular Diseases (CVDs), Respiratory Disorders, Renal Diseases, Neurodegenerative Disorders, Genetic Disorders, Infectious Diseases, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Alnylam Pharmaceuticals Inc., Arbutus Biopharma Corporation, Arrowhead Pharmaceuticals Inc., Benitec Biopharma Ltd., Bio-Path Holdings Inc., Dicerna Pharmaceuticals Inc. (Novo Nordisk A/S), Ionis Pharmaceuticals Inc., OliX Pharmaceuticals Inc., Phio Pharmaceuticals Corp., Sarepta Therapeutics Inc., Silence Therapeutics, Sirnaomics Inc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the antisense & RNAi therapeutics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global antisense & RNAi therapeutics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the antisense & RNAi therapeutics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Antisense & RNAi Therapeutics Market Report

The antisense & RNAi therapeutics market was valued at USD 1.91 Billion in 2025.

The antisense & RNAi therapeutics market is projected to exhibit a CAGR of 6.74% during 2026-2034, reaching a value of USD 3.43 Billion by 2034.

The market is driven by the rising prevalence of genetic and chronic diseases globally, advancements in oligonucleotide drug delivery technologies including lipid nanoparticles and GalNAc conjugates, supportive regulatory frameworks offering expedited approval pathways, growing personalized medicine adoption, and sustained biopharmaceutical research and development investments targeting previously unmanageable rare and inherited conditions.

North America currently dominates the antisense & RNAi therapeutics market, accounting for a share of 40%. The region benefits from advanced healthcare infrastructure, robust biotechnology R&D investment, favorable FDA regulatory pathways for novel nucleic acid therapies, and a high concentration of pioneering pharmaceutical and biotechnology companies consistently driving global antisense & RNAi therapeutics market leadership.

Some of the major players in the antisense & RNAi therapeutics market include Alnylam Pharmaceuticals Inc., Arbutus Biopharma Corporation, Arrowhead Pharmaceuticals Inc., Benitec Biopharma Ltd., Bio-Path Holdings Inc., Dicerna Pharmaceuticals Inc. (Novo Nordisk A/S), Ionis Pharmaceuticals Inc., OliX Pharmaceuticals Inc., Phio Pharmaceuticals Corp., Sarepta Therapeutics Inc., Silence Therapeutics, Sirnaomics Inc., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)