Anything-as-a-Service Market Size, Share, Trends and Forecast by Service Area, Industry, and Region 2026-2034

Global Anything-as-a-Service Market Size, Share, Trends & Forecast (2026-2034)

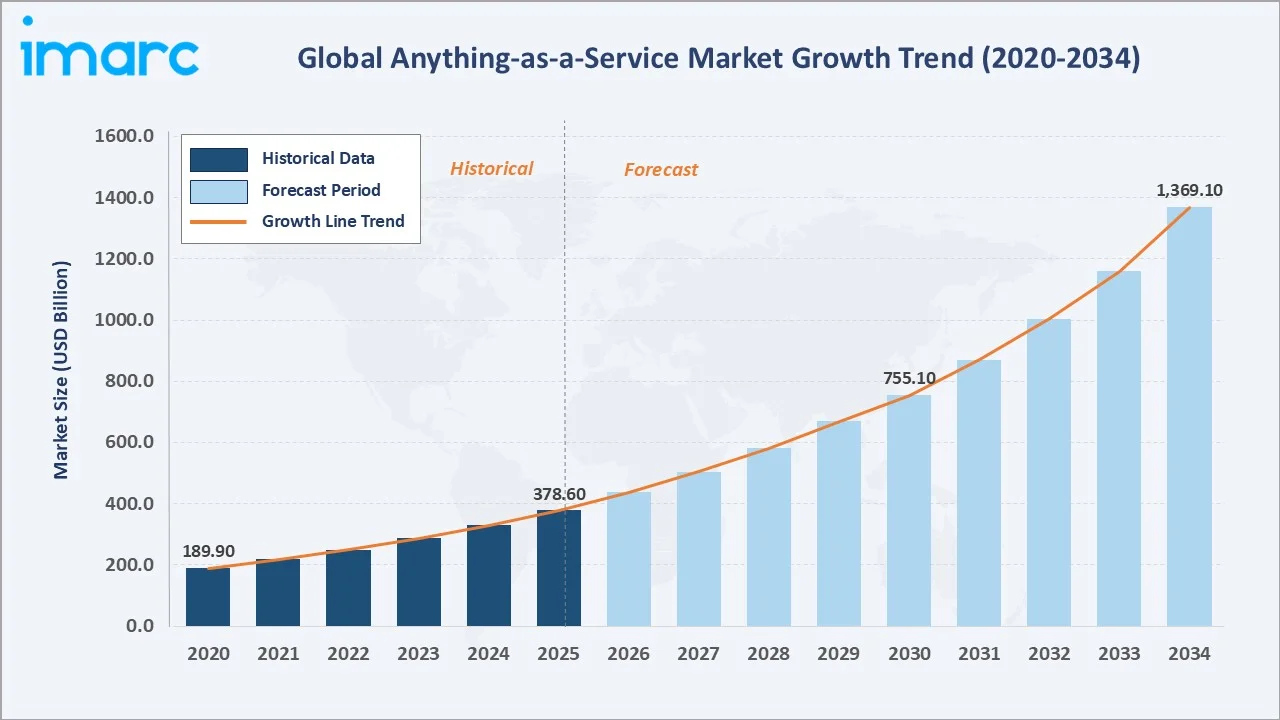

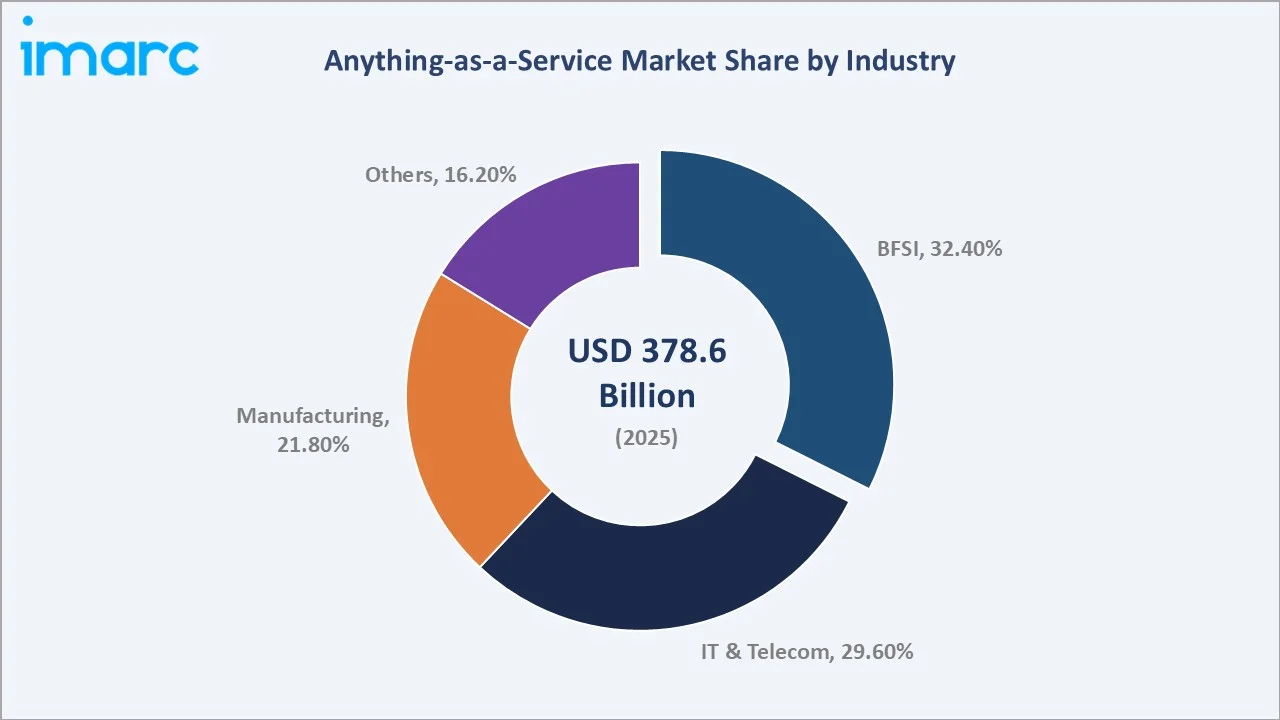

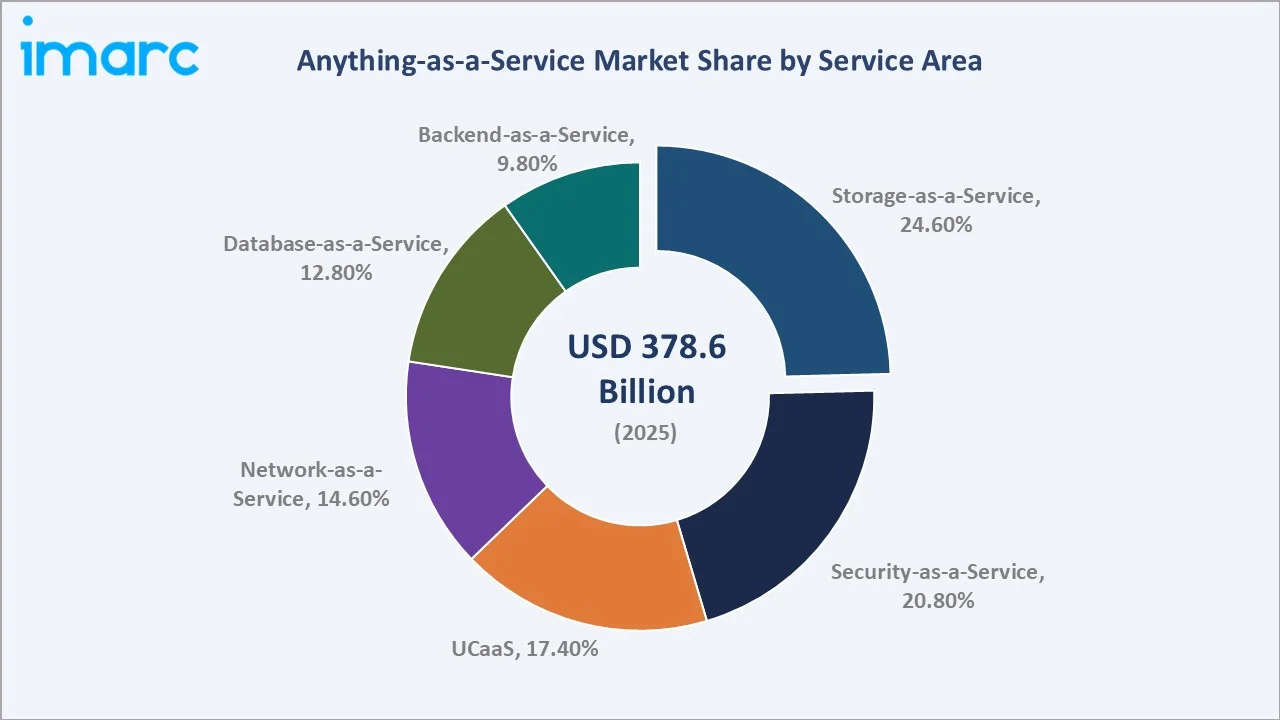

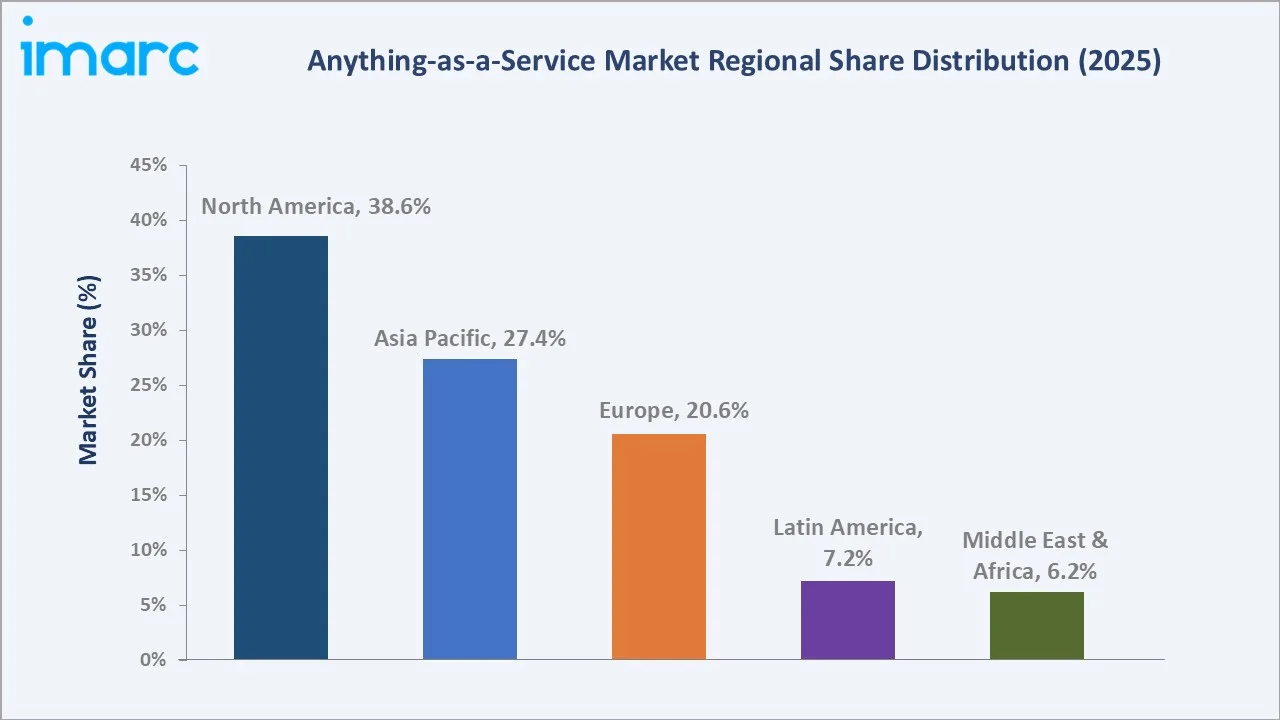

The global anything-as-a-service market size reached USD 378.6 Billion in 2025 and is projected to reach USD 1,369.1 Billion by 2034, exhibiting a CAGR of 14.8% during the forecast period 2026-2034. Accelerating enterprise cloud migration, exponential data growth requiring scalable storage and database solutions, surging cybersecurity investments, and the large-scale digitalization of BFSI, IT & Telecom, and manufacturing operations are driving the anything-as-a-service market growth. BFSI leads industry adoption at 32.4% in 2025, while Storage-as-a-Service accounts for 24.6% of the service area segment. North America commands 38.6% of global revenue in 2025, the world's largest regional anything-as-a-service market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 378.6 Billion |

|

Forecast Market Size (2034) |

USD 1,369.1 Billion |

|

CAGR (2026-2034) |

14.8% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (~18.2% CAGR) |

|

Leading Industry Segment |

BFSI (32.4%, 2025) |

|

Leading Service Area |

Storage-as-a-Service (24.6%, 2025) |

The global anything-as-a-service market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by cloud-native adoption, AI-integrated XaaS platforms, and 5G-enabled digital infrastructure.

To get more information on this market, Request Sample

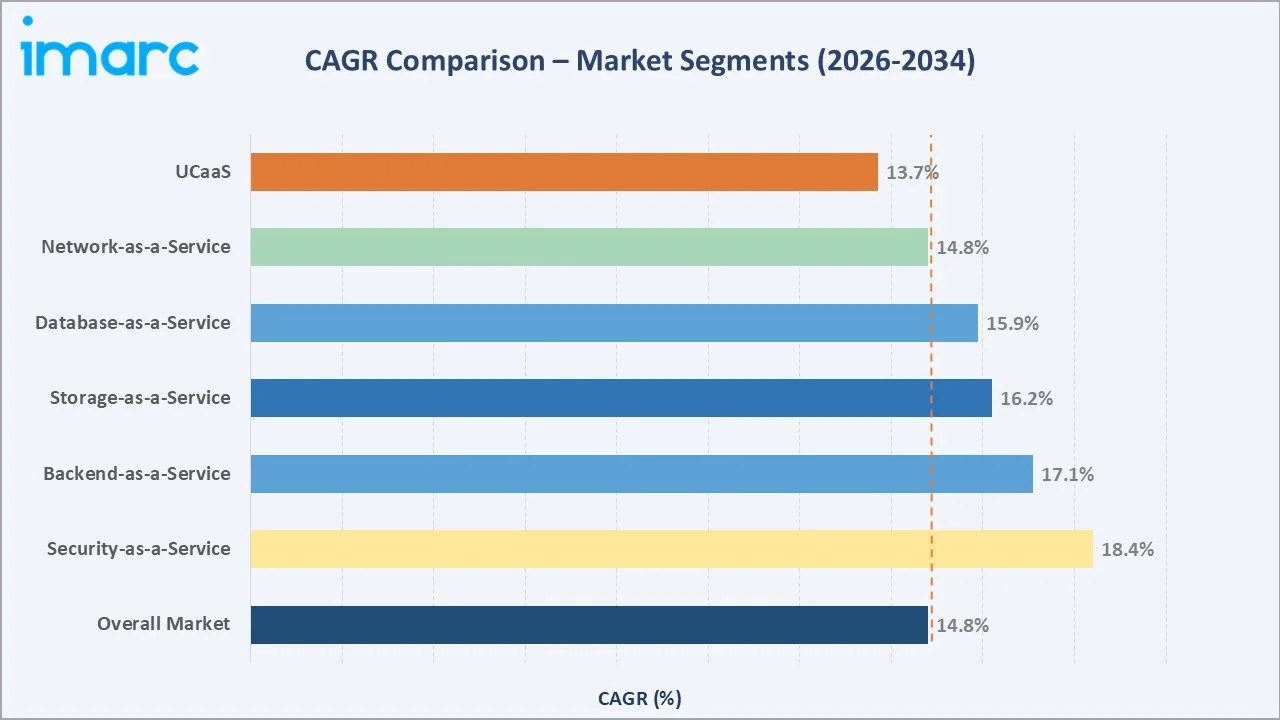

Segment-level CAGR comparisons highlighting Security-as-a-Service and Backend-as-a-Service as the two fastest-growing service area sub-categories within the global anything-as-a-service industry analysis through 2034.

Executive Summary

The global anything-as-a-service market is undergoing a fundamental structural shift driven by the convergence of enterprise cloud adoption, AI integration, and subscription-based IT economics across all major industries. Valued at USD 378.6 Billion in 2025, the market is forecast to reach USD 1,369.1 Billion by 2034 at a CAGR of 14.8%.

BFSI commands the largest industry share at 32.4% in 2025, propelled by banks and insurers deploying cloud-native infrastructure for core banking modernization, real-time fraud analytics, and digital payments at scale. IT & Telecom follows at 29.6%, driven by telecom operators virtualizing network functions via NaaS and UCaaS to reduce OPEX by 25–35%. Storage-as-a-Service represents the largest service area at 24.6%, reflecting exponential data volume growth, while Security-as-a-Service at 20.8% benefits from surging demand for zero-trust network access and AI-powered cloud security operations centers.

North America leads with 38.6% of global revenue in 2025, anchored by the mature hyperscaler ecosystem of AWS, Microsoft Azure, and Google Cloud. Asia Pacific at 27.4% is the fastest-growing region, driven by rapid cloud adoption in India, China, and Southeast Asia. The competitive landscape is moderately consolidated at the hyperscaler tier, with the top three providers collectively commanding ~60% of global anything-as-a-service revenue, while niche specialists in security, communications, and database-as-a-service compete vigorously in high-growth sub-segments.

Key Market Insights

|

Insight |

Data |

|

Largest Industry Segment |

BFSI – 32.4% share (2025) |

|

Second Largest Industry Segment |

IT & Telecom – 29.6% share (2025) |

|

Leading Service Area |

Storage-as-a-Service – 24.6% share (2025) |

|

Fastest Growing Service Area |

Security-as-a-Service (~18.4% CAGR, 2026-2034) |

|

Leading Region |

North America – 38.6% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (~18.2% CAGR, 2026-2034) |

|

Top Companies |

AWS, Microsoft, Google, IBM, Oracle, Cisco |

Key Analytical Observations Supporting The Above Data:

- BFSI's 32.4% dominance in 2025 reflects the sector's aggressive cloud-native core banking migrations, with global financial institutions deploying DBaaS and SECaaS to meet Basel IV and GDPR compliance mandates simultaneously while reducing IT infrastructure OPEX.

- Storage-as-a-Service leads at 24.6% in 2025, fuelled by enterprise data volumes growing at ~23% annually, with hyperscaler object storage pricing declining ~15% per year, compelling even cost-sensitive SMEs to migrate from on-premises NAS to cloud storage.

- Security-as-a-Service at 20.8% is the highest-growth service area (~18.4% CAGR), reflecting enterprises' transition from hardware-based firewalls and SIEM platforms to cloud-delivered CASB, ZTNA, and AI-powered threat intelligence architectures.

- North America's 38.6% leadership in 2025 is underpinned by the world's highest enterprise cloud penetration rate, with an estimated 72% of Fortune 500 companies operating multi-cloud anything-as-a-service environments as of 2025.

- Asia Pacific at 27.4% represents the fastest-growing regional opportunity, with India's Digital India initiative, China's 14th Five-Year Plan cloud targets, and Southeast Asia's expanding digital economy collectively driving anything-as-a-service demand at an accelerated pace through 2034.

Global Anything-as-a-Service Market Overview

Anything-as-a-Service is a cloud-based delivery model that enables organizations to access IT capabilities—including compute, storage, networking, security, databases, and communication tools—on-demand via subscription or pay-per-use models, replacing capital-intensive infrastructure with scalable, operational expenditure frameworks. It is widely adopted across industries: BFSI leverages DBaaS and SECaaS for core banking and fraud detection, telecom providers use NaaS for virtualized networks, manufacturers deploy IoT platforms on STaaS and BaaS, healthcare utilizes UCaaS for telemedicine, and governments rely on cloud-native services for digital public infrastructure.

The market’s growth is driven by widespread enterprise cloud adoption, increasing use of hybrid and multi-cloud strategies, rising AI-driven workloads, expansion of 5G and edge computing, and sustainability mandates favoring energy-efficient hyperscale infrastructure, collectively supporting strong long-term growth of the anything-as-a-service market through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

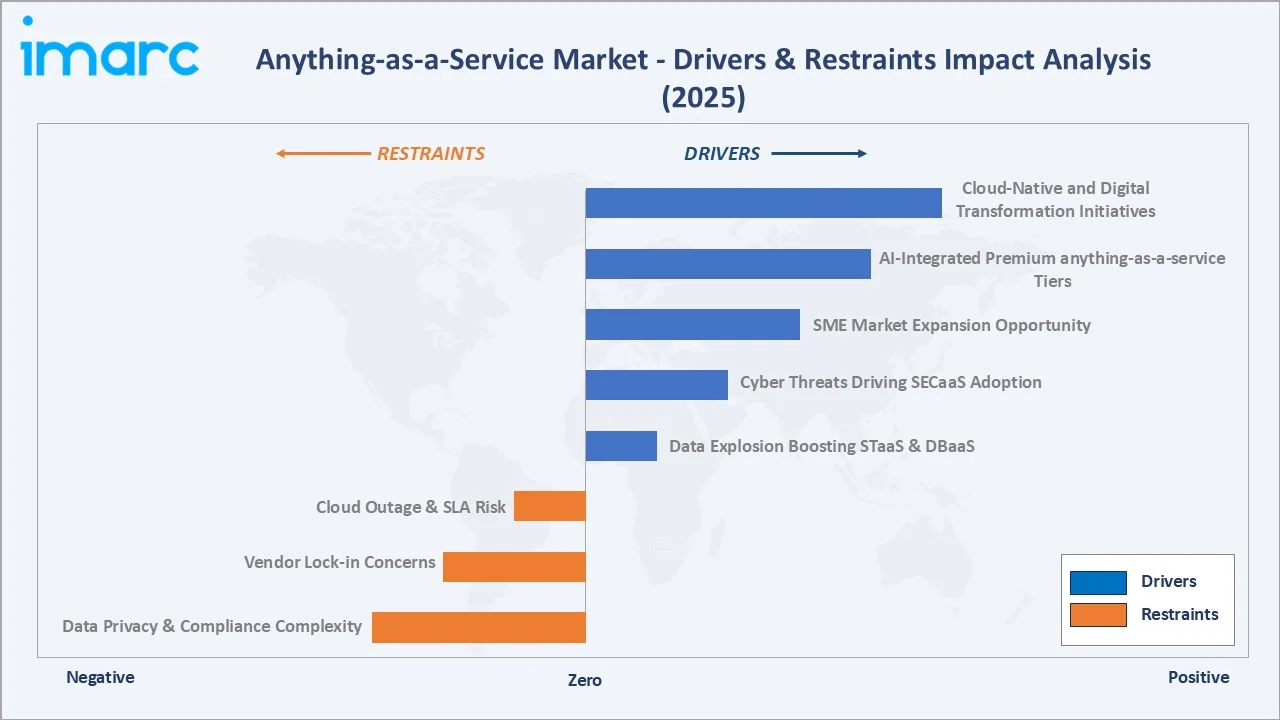

Market Drivers

- Data Explosion Boosting STaaS & DBaaS: Rapid growth in enterprise data—driven by AI, IoT, and digital transformation—is accelerating the shift toward cloud-based storage and database services, with AI workloads creating new high-performance demand tiers.

- Cyber Threats Driving SECaaS Adoption: The rising complexity and frequency of cyber threats are pushing organizations to adopt SECaaS solutions, enabling access to advanced threat detection, CASB, and SIEM capabilities without significant upfront investment.

Market Restraints

- Data Privacy & Compliance Complexity: Diverse data sovereignty regulations across regions increase compliance burdens for anything-as-a-service providers, limiting cross-border cloud adoption in highly regulated industries.

- Vendor Lock-in Concerns: Dependence on proprietary platforms and high data migration costs make enterprises cautious about adopting single-vendor anything-as-a-service solutions for critical workloads.

Market Opportunities

- SME Market Expansion Opportunity: Small and medium enterprises remain underpenetrated in cloud adoption, creating significant growth potential for anything-as-a-service providers through cost-effective, subscription-based offerings.

- AI-Integrated Premium anything-as-a-service Tiers: Integration of AI across anything-as-a-service solutions is enabling advanced capabilities such as intelligent automation and optimization, allowing providers to offer higher-value premium service tiers.

Market Challenges

- Cloud Outage & SLA Risk: Dependence on hyperscaler infrastructure exposes enterprises to service disruption risks, increasing demand for multi-cloud strategies, higher SLA assurances, and automated failover capabilities.

- Cloud Talent Shortage: Limited availability of skilled cloud and cybersecurity professionals creates implementation and management challenges, slowing anything-as-a-service adoption, particularly in emerging markets.

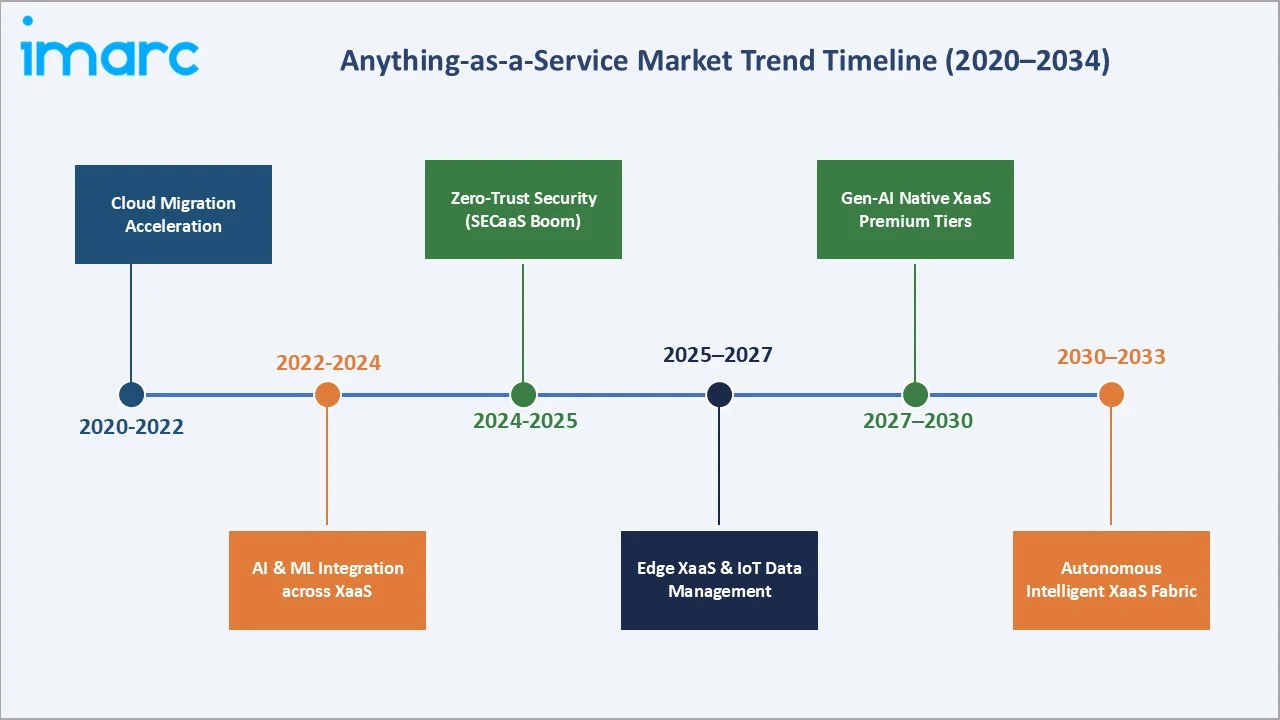

Emerging Market Trends

1. Generative AI Integration Across All Anything-as-a-Service Service Layers

Hyperscalers such as Amazon Web Services, Microsoft, and Google are embedding generative AI into core anything-as-a-service offerings through platforms like Bedrock, Azure AI, and Vertex AI. This is transforming anything-as-a-service from infrastructure delivery into an intelligence-driven platform, with AI-powered databases and automated security operations emerging as high-growth segments.

2. Edge Computing & Distributed Anything-as-a-Service Architectures

The rise of IoT and latency-sensitive applications is accelerating demand for edge-based anything-as-a-service models, including edge NaaS and BaaS. Enterprises are increasingly deploying cloud capabilities closer to data sources to enable real-time processing across manufacturing, healthcare, and autonomous systems.

3. Zero-Trust Security Architecture Driving SECaaS Growth

The shift toward zero-trust architectures is redefining enterprise security, with organizations replacing traditional perimeter-based models with cloud-delivered security services. This transition is positioning SECaaS as a foundational layer in modern IT environments.

4. Telecom Network Virtualization via NaaS

Telecom operators are transitioning from hardware-centric infrastructure to software-defined, cloud-delivered networking models. Technologies such as network function virtualization (NFV) and SD-WAN are enabling scalable NaaS deployments, with providers like Ericsson, Nokia, and Cisco driving ecosystem development.

5. Industry Cloud Platforms & Vertical Anything-as-a-Service Specialization

Cloud providers are launching industry-specific anything-as-a-service platforms tailored to sectors such as healthcare, financial services, and retail. These offerings integrate compliance frameworks, domain-specific AI models, and pre-configured data environments, enhancing the value proposition and increasing customer retention.

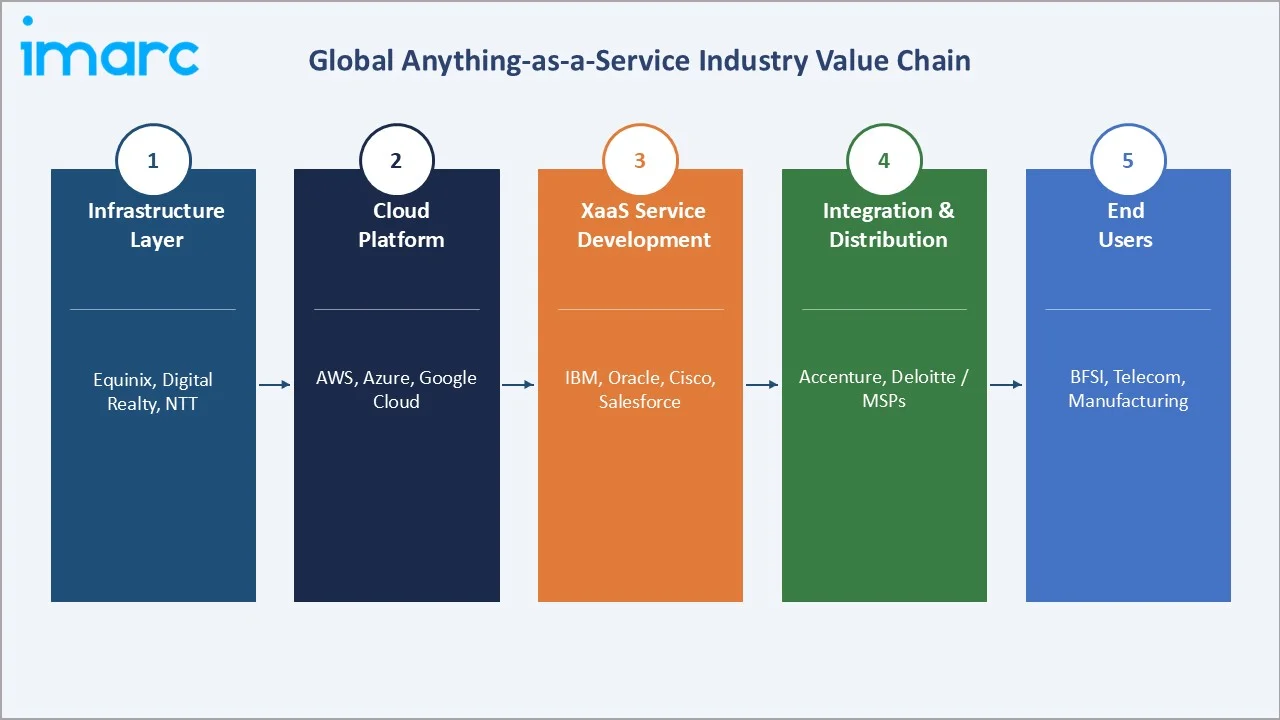

Industry Value Chain Analysis

The anything-as-a-service value chain spans five integrated stages from raw infrastructure provision through end-user consumption. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Infrastructure Layer |

Equinix, Digital Realty, NTT Global Data Centers, Iron Mountain |

|

Cloud Platform Layer |

Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform (GCP) |

|

Anything-as-a-Service Service Development |

IBM, Oracle, Cisco, Salesforce, McAfee (Trellix), Commvault |

|

Integration & Distribution |

Accenture, Deloitte, CDW, Ingram Micro, and regional managed service providers (MSPs) |

|

End Users |

BFSI enterprises, telecom operators, manufacturing conglomerates, SMEs, and government |

Cloud platform providers (AWS, Azure, GCP) occupy the highest strategic value position in the anything-as-a-service value chain, serving simultaneously as infrastructure owners and anything-as-a-service service competitors to the Tier-2 providers built on their platforms. This structural duality creates both co-opetition dynamics and concentration risk for enterprises that are deeply embedded in a single hyperscaler ecosystem.

Technology Landscape in the Anything-as-a-Service Industry

Cloud-Native Architecture: Kubernetes & Containerization

Cloud-native anything-as-a-service delivery is anchored in Kubernetes-based orchestration, enabling automated scaling, workload portability, and multi-tenant isolation across hybrid and multi-cloud environments. Cloud Native Computing Foundation highlights Kubernetes as the de facto standard for container orchestration, supported by a global open-source developer base exceeding millions. Leading hyperscalers, including Amazon Web Services (EKS), Microsoft (AKS), and Google (GKE), provide fully managed Kubernetes services, enabling standardized infrastructure and seamless anything-as-a-service portability.

Software-Defined Networking (SDN) & NaaS Enablement

Software-defined networking abstracts control planes from hardware, enabling programmable and cloud-delivered networking models critical for Network-as-a-Service (NaaS). Platforms such as Cisco Systems (Meraki), VMware (NSX), and Juniper Networks (Mist AI) provide centralized network orchestration and policy automation. These solutions underpin enterprise transitions from legacy MPLS to SD-WAN architectures, enabling scalable, subscription-based network delivery models.

Artificial Intelligence & Machine Learning Integration

AI/ML capabilities are increasingly embedded across anything-as-a-service layers to enhance automation, efficiency, and predictive intelligence. Amazon Web Services (Aurora), Google (AlloyDB), and Microsoft (Azure AI) integrate machine learning for query optimization, anomaly detection, and cost efficiency. Security platforms leverage AI-driven threat detection to significantly reduce detection times compared to traditional SIEM approaches, as outlined in vendor security documentation.

API Economy & Backend-as-a-Service (BaaS) Expansion

API-first architectures are foundational to anything-as-a-service composability, enabling seamless integration across distributed cloud services. Platforms such as Google (Firebase), Amazon Web Services (Amplify), and Supabase provide Backend-as-a-Service capabilities, including authentication, real-time data sync, and serverless compute. API management solutions from Google and Microsoft further reinforce API-driven anything-as-a-service integration strategies.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service Area |

Storage-as-a-Service |

24.6% |

2025 |

|

Industry |

BFSI |

32.4% |

2025 |

|

Region |

North America |

38.6% |

2025 |

By Industry

BFSI commands a 32.4% share in 2025, the largest among all industry verticals. Financial institutions are investing an estimated USD 650 Billion globally in digital transformation in 2025, with cloud-native anything-as-a-service platforms accounting for over 40% of new technology deployments. Core growth drivers include core banking migration to DBaaS, AI-enabled real-time fraud analytics via SECaaS, and digital payment infrastructure built on cloud-native BaaS platforms.

To access detailed market analysis, Request Sample

IT & Telecom at 29.6% in 2025 is driven by telecom operators’ shift to cloud-managed networks. NaaS and UCaaS are replacing capital-intensive infrastructure, reducing network OPEX by 25–35%. Leading operators such as AT&T, Verizon, Deutsche Telekom, and NTT are deploying anything-as-a-service across technology layers. Manufacturing at 21.8% is the fastest-growing vertical, driven by Industry 4.0 adoption, including smart factory IoT data management, supply chain digitization, and connected equipment monitoring via cloud-native anything-as-a-service platforms.

By Service Area

Storage-as-a-Service commands the largest service area share at 24.6% in 2025. Hyperscaler object storage costs have steadily declined, making cloud storage the cost-competitive default for new enterprise data workloads, supported by platforms like Amazon Web Services, Microsoft, and Google. Emerging use cases such as AI training data, regulatory archiving, and media content management are driving new STaaS demand tiers with significantly higher storage volumes than traditional backup workloads.

Security-as-a-Service at 20.8% is the highest-growth service category at ~18.4% CAGR through 2034. Enterprises are transitioning from hardware-based security appliances to cloud-delivered CASB, ZTNA, and AI-powered SIEM platforms. The transition to zero-trust security models is forecast to add USD 42–58 Billion in incremental SECaaS market value by 2034. UCaaS at 17.4% remains structurally supported by permanent hybrid work adoption, with AI-enhanced meeting intelligence and real-time transcription driving average revenue per UCaaS user upward by 15–20% through 2034.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.6% |

Hyperscaler ecosystem leadership; highest enterprise cloud penetration; Fortune 500 multi-cloud anything-as-a-service adoption; FedRAMP-driven government cloud spending |

|

Asia Pacific |

27.4% |

Digital India initiative; China's 14th Five-Year Plan cloud targets; ASEAN digital economy expansion; rapid SME cloud adoption across Southeast Asia |

|

Europe |

20.6% |

GDPR-driven SECaaS demand; EU Digital Decade strategy; industrial NaaS for manufacturing; NIS2 Directive compliance investments |

|

Latin America |

7.2% |

Brazil fintech expansion and LGPD cloud compliance; Mexico manufacturing cloud adoption; SME e-commerce infrastructure growth |

|

Middle East & Africa |

6.2% |

Saudi Vision 2030 cloud investment; UAE smart government initiatives; Africa's mobile-first digital economy driving BaaS and UCaaS demand |

North America commands a 38.6% global revenue share in 2025, the most dominant regional position of any geography in the global anything-as-a-service market. The US alone accounts for approximately 32% of global anything-as-a-service revenue, supported by the world's highest enterprise cloud penetration rate and the headquarters concentration of all five leading anything-as-a-service platform providers.

Asia Pacific at 27.4% is the fastest-growing anything-as-a-service region, with India's cloud market growing at ~23% annually, driven by the Digital India initiative, Jio's hyperscaler ambitions, and the rapid adoption of UCaaS and BaaS among India's 63 million SMEs.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Amazon Web Services Inc. (AWS) |

AWS Cloud / Amazon S3 / Lambda |

Leader |

Broadest anything-as-a-service portfolio; STaaS, DBaaS, BaaS market leader |

|

Microsoft Corporation |

Azure / Microsoft 365 / Sentinel |

Leader |

UCaaS (Teams), SECaaS (Sentinel), enterprise anything-as-a-service suite |

|

Google LLC |

Google Cloud / Workspace / Chronicle |

Leader |

AI-integrated BaaS; strongest analytics anything-as-a-service; Workspace UCaaS |

|

IBM Corporation |

IBM Cloud / QRadar / Cloudant |

Challenger |

Enterprise SECaaS and DBaaS; BFSI vertical focus |

|

Oracle Corporation |

Oracle Cloud Infrastructure (OCI) |

Challenger |

DBaaS leader; autonomous database; ERP-cloud integration |

|

Cisco Systems, Inc. |

Cisco Meraki / Webex / SecureX |

Challenger |

NaaS, UCaaS, SECaaS; dominant enterprise networking anything-as-a-service |

|

Dell Technologies, Inc. |

Dell APEX |

Established |

STaaS and hybrid cloud; on-premise-to-anything-as-a-service bridge solutions |

|

AT&T Inc. |

AT&T Business / AT&T Cybersecurity |

Established |

Carrier-grade NaaS and UCaaS; US enterprise connectivity anything-as-a-service |

|

Telefonaktiebolaget LM Ericsson |

Ericsson Cloud RAN / BSCS |

Emerging |

5G NaaS infrastructure; telecom network virtualization |

|

Juniper Networks, Inc. |

Juniper Mist AI / Juniper Cloud |

Emerging |

AI-driven NaaS; SD-WAN and cloud-managed network services |

The anything-as-a-service competitive landscape is characterized by a small number of global hyperscalers commanding substantial platform share, alongside enterprise software leaders with anything-as-a-service specializations and telecom operators enabling network-layer anything-as-a-service. AWS, Microsoft, and Google collectively account for approximately 58–62% of global anything-as-a-service revenue in 2025, with their competitive moats deepening through AI service integration, global data center footprint, and developer ecosystem flywheel effects.

Key Company Profiles

Amazon Web Services Inc. (AWS)

AWS, a subsidiary of Amazon.com, Inc., is the world's largest cloud platform with over 240 cloud services deployed across 33 geographic regions and 105 availability zones as of 2025.

- Product & Platform Portfolio: Amazon S3 (STaaS), Amazon RDS / DynamoDB / Aurora (DBaaS), AWS Lambda / Amplify (BaaS), AWS Security Hub / GuardDuty (SECaaS), Amazon Chime (UCaaS), AWS Direct Connect (NaaS).

- Recent Developments: In April 2023, Amazon Web Services launched Bedrock, enabling generative AI integration across anything-as-a-service service layers.

- Strategic Focus: AWS centers its strategy on AI service integration across all anything-as-a-service portfolio layers, sovereign cloud expansion for government and regulated enterprise, and developer ecosystem deepening via AWS Marketplace's 12,000+ listed solutions.

Microsoft Corporation

Microsoft’s Intelligent Cloud segment is driven by strong Azure growth and the масштаб adoption of Microsoft 365 across enterprises. The company holds a leading position in the market, supported by the widespread adoption of Microsoft Teams as a core collaboration platform.

-

Product & Platform Portfolio: Microsoft Teams (UCaaS), Azure Sentinel / Defender (SECaaS), Azure SQL / Cosmos DB (DBaaS), Azure Blob Storage (STaaS), Azure Virtual WAN (NaaS), Azure Functions / App Service (BaaS).

-

Recent Developments: In January 2023, Microsoft expanded its partnership with OpenAI through a multi-year, multi-billion-dollar investment to accelerate AI integration across Azure.

-

Strategic Focus: Microsoft pursues an AI-first anything-as-a-service transformation, embedding Copilot capabilities across Teams, Azure, and Defender to create differentiated premium service tiers. The enterprise security consolidation platform strategy positions Sentinel, Defender, and Entra as an integrated SECaaS suite competing directly against point-solution vendors.

Google LLC

Google Cloud has reached sustained profitability, signaling strong enterprise adoption of its anything-as-a-service offerings. Google Workspace anchors its UCaaS and BaaS capabilities, serving a broad global base of business customers and reinforcing its position in cloud-based collaboration and application services.

- Product & Platform Portfolio: Google Cloud Storage (STaaS), BigQuery / Cloud SQL (DBaaS), Chronicle Security (SECaaS), Google Workspace (UCaaS), Firebase / Cloud Run (BaaS), Google Cloud Interconnect (NaaS).

- Recent Developments: In December 2023, Google launched Gemini AI, followed by integration across Google Cloud services through 2024, enabling AI-driven anything-as-a-service capabilities.

- Strategic Focus: Google differentiates via AI-native anything-as-a-service through Gemini model integration, best-in-class data analytics capabilities (BigQuery), and a sustainability commitment to 24/7 carbon-free energy by 2030 – increasingly a procurement criterion for enterprise cloud sourcing decisions.

Market Concentration Analysis

The global anything-as-a-service market exhibits moderate-to-high concentration at the hyperscaler tier. AWS, Microsoft, and Google collectively account for an estimated 58–62% of global anything-as-a-service revenue in 2025, declining marginally from ~65% in 2022 as regional challengers and specialist providers gain share in specific service areas and geographies.

The anything-as-a-service market is led by major players, including IBM and Oracle, while fragmentation remains high in specialized segments. The Security-as-a-Service landscape includes key providers such as CrowdStrike, Palo Alto Networks, Fortinet, Zscaler, and Trellix. The UCaaS market is similarly competitive, with players like Zoom Video Communications, RingCentral, Avaya, 8x8, alongside Microsoft Teams and Cisco Systems Webex.

Consolidation remains strong, highlighted by major acquisitions such as Broadcom’s acquisition of VMware and Cisco Systems’s acquisition of Splunk, reflecting a strategic push by hyperscalers to expand SECaaS and NaaS capabilities through inorganic growth.

Investment & Growth Opportunities

Fastest-Growing Segments

Security-, backend-, and storage-as-a-service segments are emerging as the fastest-growing layers of the anything-as-a-service stack, driven by zero-trust security adoption, developer-first architectures, and AI-led data expansion. Security-as-a-Service leads in strategic importance, supported by SASE convergence and AI-powered SOC platforms, while Backend-as-a-Service and Storage-as-a-Service benefit from serverless computing trends and exponential AI data requirements.

Emerging Market Expansion

Emerging markets are the next major growth frontier. Asia-Pacific—particularly Southeast Asia and India—along with Middle Eastern digital transformation initiatives such as Saudi Arabia’s Vision 2030, represent the largest incremental anything-as-a-service opportunities driven by rapid cloud adoption and digital economy expansion.

Venture & Private Investment Trends

Venture investment trends reinforce this shift, with global funding exceeding tens of billions annually and increasingly concentrated in security and AI-native platforms. AI-integrated anything-as-a-service solutions are attracting disproportionately higher capital, establishing generative AI as the primary competitive differentiation layer across the anything-as-a-service ecosystem.

Future Market Outlook (2026-2034)

The global anything-as-a-service market forecast projects sustained high-growth expansion from USD 378.6 Billion in 2025 to USD 1,369.1 Billion by 2034 at a CAGR of 14.8%, a more-than-three-fold market expansion underpinned by deep enterprise cloud penetration, AI service layer addition across all anything-as-a-service categories, and the structural shift of all enterprise IT delivery models to as-a-service economics.

Three key technology discontinuities will reshape the anything-as-a-service market through 2034. Generative AI integration will redefine all service categories, with AI-enhanced storage, security (AI-SOC), and databases commanding premium pricing. Autonomous, AI-driven network infrastructure (NaaS) will significantly reduce manual operations, shifting pricing toward outcome- and intent-based models.

By 2034, anything-as-a-service will evolve from a utility to a strategic business intelligence platform, led by three ecosystems: the hyperscaler triad—Amazon Web Services, Microsoft, and Google—Chinese cloud providers including Alibaba Cloud, Tencent Cloud, and Huawei Cloud, and a third tier of AI-specialized vertical anything-as-a-service providers offering industry-specific, compliance-integrated solutions at premium price points.

Research Methodology

Primary Research

Primary research included multiple structured interviews (2024–2025) with anything-as-a-service stakeholders—CTOs and cloud architects at Fortune 500 firms, product leaders at anything-as-a-service providers, procurement heads in BFSI and manufacturing, and institutional investors. Insights validated market sizing, segment shares, adoption timelines, and competitive positioning.

Secondary Research

Secondary sources include Gartner Cloud Market reports (2024), IDC Cloud Infrastructure Tracker, Synergy Research Group hyperscaler revenue data, Flexera State of the Cloud Report 2025, ISC² Cybersecurity Workforce Study 2024, PitchBook cloud venture investment data, GSMA Intelligence 5G connectivity forecasts, company annual reports (AWS, Microsoft, Google, IBM, Oracle), and trade publications including CIO Magazine, Cloud Computing News, and TechCrunch.

Forecasting Models

Market size and growth projections were derived using combined top-down and bottom-up forecasting models, incorporating GDP growth rates, IT spending data from Gartner IT Spending Forecast, cloud adoption penetration curves by region and industry, and historical anything-as-a-service segment growth patterns from 2018 to 2025. Scenario analysis (base, optimistic, and conservative cases) was performed to capture macroeconomic uncertainty, supply chain disruptions, and regulatory headwinds.

Report Coverage

|

Attribute |

Details |

|

Market Size (Base Year) |

USD 378.6 Billion (2025) |

|

Market Size (Forecast Year) |

USD 1,369.1 Billion (2034) |

|

CAGR |

14.8% (2026-2034) |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation by Service Area |

STaaS, SECaaS, UCaaS, NaaS, DBaaS, BaaS |

|

Segmentation by Industry |

BFSI, IT & Telecom, Manufacturing, Others |

|

Regional Analysis |

North America, Asia Pacific, Europe, Latin America, MEA |

|

Companies Profiled |

20+, including AWS, Microsoft, Google, IBM, Oracle, Cisco, Dell, AT&T, Ericsson, Juniper |

|

Report Format |

PDF + Excel |

|

Report ID |

SR112026A1326 |

Frequently Asked Questions About the Anything-as-a-Service Market Report

The global anything-as-a-service market was valued at USD 378.6 Billion in 2025, driven by accelerating enterprise cloud migration, rising cybersecurity investment, and growing demand for subscription-based IT service delivery models across BFSI, IT & Telecom, and manufacturing sectors.

The market is projected to reach USD 1,369.1 Billion by 2034, growing at a CAGR of 14.8% during 2026-2034, driven by AI-integrated cloud services, enterprise digital transformation investment, and expanding anything-as-a-service adoption across all industry verticals globally.

BFSI leads with a 32.4% revenue share in 2025, driven by financial institutions deploying cloud-native core banking, real-time fraud analytics via DBaaS and AI, digital payment infrastructure, and regulatory compliance platforms via SECaaS and cloud storage.

Storage-as-a-Service leads with a 24.6% share in 2025, fuelled by exponential enterprise data growth, declining hyperscaler object storage pricing at ~15% annually, and new AI training data repository requirements creating incremental demand beyond traditional backup workloads.

North America leads with 38.6% of global revenue in 2025, supported by the highest enterprise cloud penetration globally, headquarters concentration of AWS, Microsoft, and Google, and structured federal cloud-first policies driving public sector anything-as-a-service adoption.

Key drivers include accelerating enterprise cloud migration, rising cybersecurity threats driving SECaaS demand, exponential data growth fuelling STaaS, 5G network virtualization enabling NaaS, and digital transformation investment exceeding USD 650 Billion annually in BFSI and manufacturing.

Security-as-a-Service is the fastest-growing at ~18.4% CAGR through 2034, driven by zero-trust network access adoption, rising cyberattack frequency, SASE platform convergence, and enterprise migration from hardware-based security to AI-powered cloud security operations.

Leading companies include Amazon Web Services (AWS), Microsoft Corporation, Google LLC, IBM Corporation, Oracle Corporation, Cisco Systems, Dell Technologies, AT&T, Ericsson, and Juniper Networks.

AI integration is creating premium anything-as-a-service service tiers across storage, security, and database categories. AI-SOC platforms reduce threat detection time by 60%; AI-optimized databases cut compute costs by 20–35%; AI-enhanced UCaaS platforms (Copilot, Gemini) drive 35–45% higher average revenue per user versus standard packages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)