Architectural Hardware Market Size, Share, Trends and Forecast by Application, End User, and Region, 2026-2034

Architectural Hardware Market Size and Share:

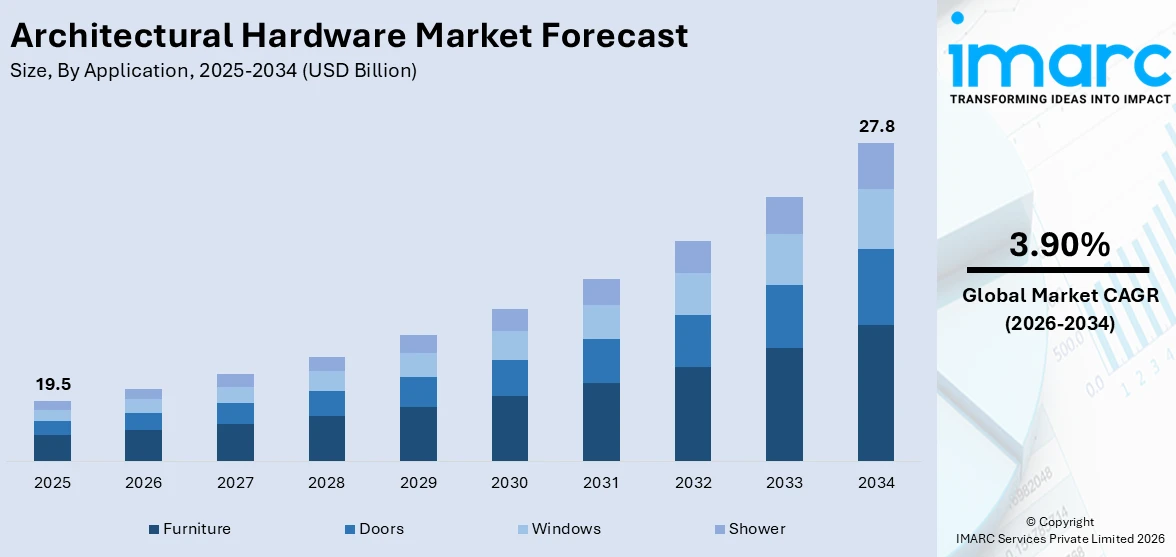

The global architectural hardware market size was valued at USD 19.5 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 27.8 Billion by 2034, exhibiting a CAGR of 3.90% from 2026-2034. North America currently dominates the market, holding a market share of 29% in 2025. The region benefits from well-established construction and real estate sectors, high consumer spending on home improvement and renovation projects, stringent building safety codes that mandate high-quality hardware, and a mature residential market driving consistent demand for architectural hardware, contributing to the architectural hardware market share.

The global architectural hardware market is being driven by significant growth in construction and infrastructure development activities worldwide. Rapid urbanization, particularly in developing economies, is fueling demand for residential, commercial, and industrial structures, thereby increasing the consumption of door hardware, window fittings, furniture components, and shower accessories. Moreover, escalating safety and security concerns are prompting building owners and developers to invest in advanced locking systems, reinforced hinges, and durable door closers that comply with evolving regulatory standards. The growing trend of home renovation and interior remodeling, influenced by shifting aesthetic preferences and rising disposable incomes, is further catalyzing demand for premium architectural hardware products. Additionally, increasing investment in smart city projects and sustainable construction practices globally is creating new opportunities for the architectural hardware market growth and innovation across product categories.

The United States has emerged as a major region in the architectural hardware market owing to many factors. The country's robust construction sector continues to sustain substantial demand for high-quality architectural hardware across residential, commercial, and institutional applications. According to the US Census Bureau, private residential construction spending reached a seasonally adjusted annual rate of approximately USD 913.9 billion in October 2025, reflecting steady investment in housing development and renovation[DA1] . Additionally, the increasing adoption of smart home technologies, including connected locking systems and automated door hardware, is accelerating product upgrades in both new builds and existing structures. Stringent building codes enforced across states mandate the use of certified, fire-rated, and ADA-compliant hardware, driving sustained demand for specialized products that promote the market outlook across the country.

To get more information on this market Request Sample

Architectural Hardware Market Trends:

Growing Adoption of Smart Hardware

The integration of smart technology into architectural hardware is reshaping the industry by enhancing security, convenience, and connectivity. Smart locks, sensor-driven door systems, and automated window hardware are gaining significant traction across both residential and commercial applications, driven by the broader adoption of smart home ecosystems. Building owners and property managers increasingly prefer hardware solutions that offer keyless entry, remote access control, and real-time monitoring through smartphones and centralized platforms. The proliferation of Internet of Things connectivity and compatibility with voice-activated assistants supports this transition from traditional mechanical hardware to electromechanical and digital systems. For instance, the global smart lock market was valued at approximately USD 2.7 billion in 2024, with North America accounting for the largest revenue share, underscoring the growing consumer preference for connected security solutions. The demand for smart hardware is further amplified by rising urbanization and heightened security awareness, positioning technology-enabled products as a transformative force in the architectural hardware market forecast.

Emphasis on Sustainable Building Materials

Sustainability has become a central consideration in the architectural hardware industry, with manufacturers and builders prioritizing eco-friendly materials and energy-efficient designs. The increasing enforcement of green building certifications and environmental regulations is compelling hardware producers to adopt recyclable metals, low-emission coatings, and responsibly sourced raw materials. Corrosion-resistant stainless steel and anodized aluminum are becoming the materials of choice, reducing environmental impact while enhancing product longevity. This shift aligns with the global movement toward sustainable construction, where every component of a building is evaluated for its environmental footprint. For instance, the global green building materials market size reached USD 374.7 Billion in 2024. Looking forward, IMARC Group expects the market to reach USD 739.9 Billion by 2033, exhibiting a growth rate (CAGR) of 7.85% during 2025-2033, highlighting the strong demand for sustainability-oriented construction practices. Hardware manufacturers are increasingly developing products that support energy-efficient building envelopes and contribute to certifications such as LEED and BREEAM, driving the architectural hardware market trends in product innovation.

Expansion of Furniture Hardware Innovations

The furniture hardware segment is witnessing a wave of innovative product introductions that are redefining design possibilities and user convenience. Manufacturers are developing advanced fittings, drawer systems, soft-close mechanisms, and modular hardware solutions that cater to evolving lifestyle preferences and space-efficient living environments. The demand for customizable, aesthetically appealing, and functionally superior furniture hardware is rising as consumers seek personalized interior solutions. This trend is particularly strong in urban markets where compact living spaces necessitate space-optimizing storage and multi-functional furniture designs. For instance, in March 2025, Hettich, a global leader in furniture fittings, officially launched FurnSpin in the United States, a revolutionary system that enables cabinets to rotate 180 degrees, combining luxury design with unprecedented functionality. This innovation exemplifies the broader industry shift toward creating hardware that transforms traditional furniture into dynamic, space-saving solutions, reinforcing the importance of ongoing research and development investments across the sector.

Architectural Hardware Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global architectural hardware market, along with forecast at the global, regional, and country levels from 2026-2034. The market has been categorized based on application and end user.

Analysis by Application:

- Furniture

- Doors

- Windows

- Shower

Furniture holds 32% of the market share. Furniture hardware encompasses a broad range of fittings, including drawer runners, cabinet hinges, sliding mechanisms, handles, and soft-close systems that are integral to the functionality and aesthetics of modern furniture. The growing consumer preference for modular and customizable furniture designs, driven by urbanization and compact living spaces, is sustaining robust demand for advanced furniture fittings. Additionally, the rising focus on premium interior design and home renovation activities is encouraging consumers to invest in high-quality, durable, and visually appealing furniture hardware, creating a positive architectural hardware market outlook. Manufacturers are responding with innovations that combine ergonomic convenience with design flexibility, such as rotating cabinet systems and illuminated drawer platforms. For instance, in May 2025, Hettich presented its future-ready furniture innovations at Interzum 2025, showcasing the slimline Avosys hinge, the SAH 500 heavy-duty cabinet suspension bracket, and dynamic LED illumination upgrades for its AvanTech YOU drawer system, highlighting the industry's continued investment in advanced furniture hardware solutions.

Analysis by End User:

Access the comprehensive market breakdown Request Sample

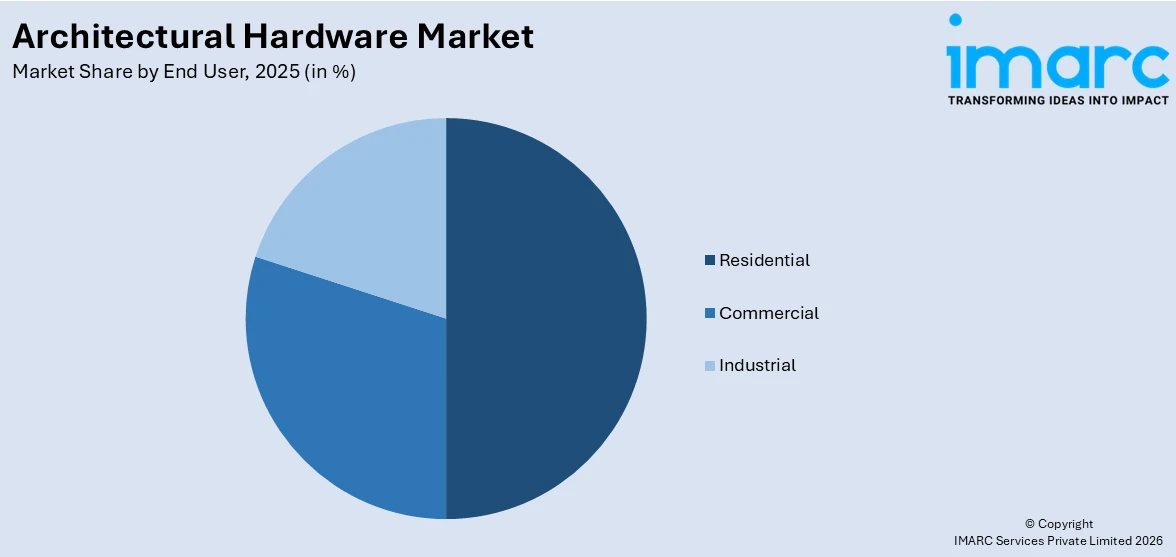

- Residential

- Commercial

- Industrial

Residential leads the market with a share of 50%. The residential segment dominates the architectural hardware market, driven by sustained demand for door hardware, window fittings, furniture components, and shower accessories across new housing construction and home renovation projects worldwide. Rising homeownership rates, increasing disposable incomes, and evolving consumer preferences for aesthetically superior and functionally advanced hardware solutions are fueling growth in this segment. Moreover, the expanding adoption of smart home technologies in residential properties is driving demand for connected locks, automated door closers, and sensor-based window hardware. The growing emphasis on home improvement and interior modernization, particularly in developed markets, further supports consistent residential hardware consumption. Additionally, rapid urbanization and the development of multi-family housing projects are accelerating demand for durable, design-oriented architectural hardware solutions.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America, accounting for 29% of the share, enjoys the leading position in the market. The region's dominance is attributed to its mature construction sector, high standards of building safety, and the widespread adoption of advanced hardware technologies across residential, commercial, and institutional applications. North America benefits from well-established distribution networks, strong consumer spending on home improvement, and stringent regulatory frameworks that mandate the use of certified and fire-rated architectural hardware. The presence of leading global manufacturers and their continuous investment in product innovation further strengthens the regional market. Additionally, the growing trend of smart home integration and energy-efficient building practices is creating sustained demand for technologically advanced hardware solutions. For instance, according to the US Census Bureau, total construction spending in the United States stood at a seasonally adjusted annual rate of approximately USD 2,175.2 billion in October 2025, reflecting the substantial scale of building activity driving hardware demand in the region.

Key Regional Takeaways:

United States Architectural Hardware Market Analysis

The United States represents the largest national market for architectural hardware, supported by its expansive residential housing sector, significant commercial real estate development, and ongoing infrastructure modernization initiatives. The demand for high-quality door locks, hinges, handles, window fittings, and shower accessories is underpinned by stringent building codes enforced at federal and state levels, requiring the use of fire-rated, ADA-compliant, and energy-efficient hardware across all building types. The growing penetration of smart home technologies is driving a rapid transition from traditional mechanical hardware to connected, digitally enabled solutions such as smart locks, automated closers, and sensor-based access control systems. Home renovation and remodeling activities remain a significant demand driver, as homeowners increasingly upgrade their interiors with premium-quality hardware that enhances both functionality and aesthetics. For instance, according to a ConstructConnect forecast published in December 2025, residential construction activity in the United States is projected to advance by 9.7 percent in 2026, driven by improving housing affordability and declining mortgage rates. Furthermore, the growing emphasis on energy-efficient and sustainable building practices is encouraging the adoption of eco-friendly architectural hardware products across new construction and retrofit applications.

Europe Architectural Hardware Market Analysis

Europe represents a significant market for architectural hardware, driven by its well-developed construction sector, stringent energy performance regulations, and strong emphasis on sustainable building practices. The region's commitment to green construction is a key factor shaping hardware demand, as building owners and developers increasingly seek eco-friendly, recyclable, and energy-efficient hardware products that align with certifications such as BREEAM and national building renovation plans. The residential renovation sector is a particularly important growth driver, as aging building stock across major European economies necessitates hardware upgrades and replacements. For instance, the EU construction sector contributes approximately 9% of the European Union's gross domestic product and employs 18 million people[DA3] , underscoring the substantial scale of building activity that sustains hardware demand across the continent. Additionally, the increasing integration of digital technologies, including smart locking systems and automated window hardware, is gaining momentum across European commercial and residential applications, driven by consumer demand for convenience and enhanced security solutions.

Asia-Pacific Architectural Hardware Market Analysis

Asia-Pacific is emerging as a rapidly growing market for architectural hardware, driven by extensive urbanization, large-scale infrastructure development, and rising construction activities across major economies. The region's expanding middle class, growing homeownership aspirations, and increasing investment in residential and commercial real estate are fueling sustained demand for door hardware, window fittings, and furniture components. Government-led housing programs and smart city initiatives in countries such as China and India are further boosting the consumption of architectural hardware products. For instance, the India construction market size was valued at USD 685.0 Billion in 2025 and is projected to reach USD 1,245.7 Billion by 2034, growing at a compound annual growth rate of 6.87% from 2026-2034, reflecting the massive scale of building activity across the region. The adoption of modern hardware technologies, including modular fittings and smart access control systems, is accelerating as developers prioritize quality and functionality in new construction projects.

Latin America Architectural Hardware Market Analysis

Latin America represents a growing market for architectural hardware, supported by increasing urbanization, rising residential construction activities, and expanding infrastructure development across key economies such as Brazil and Mexico. The demand for door hardware, window fittings, and shower accessories is being driven by government housing programs and private real estate investments aimed at addressing housing deficits. For instance, Brazil construction market size reached USD 156.0 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 218.2 Billion by 2034, exhibiting a growth rate (CAGR) of 3.80% during 2026-2034.The growing middle class and improving economic conditions are further encouraging investments in home improvement and commercial building projects, sustaining steady demand.

Middle East and Africa Architectural Hardware Market Analysis

The Middle East and Africa region is witnessing steady growth in the architectural hardware market, driven by large-scale infrastructure projects, urban development initiatives, and the expansion of the hospitality and commercial real estate sectors. Countries in the Gulf Cooperation Council are investing significantly in mega-construction projects, smart city developments, and tourism infrastructure, generating substantial demand for premium-quality hardware. For instance, Saudi Arabia's Vision 2030 program has directed significant capital investment toward diversifying the economy through the construction of new residential, commercial, and entertainment complexes. The increasing adoption of modern building standards and the growing focus on safety and security are further supporting hardware demand.

Competitive Landscape:

The architectural hardware market exhibits a moderately fragmented competitive structure, characterized by the presence of established global corporations alongside numerous regional and local manufacturers. Leading companies are focused on strengthening their market positions through strategic acquisitions, product innovation, and geographic expansion into emerging markets. The transition from traditional mechanical hardware to electromechanical and smart solutions is a defining competitive trend, with major players investing heavily in research and development to introduce connected locks, automated door systems, and sensor-enabled hardware. Additionally, companies are increasingly prioritizing sustainability by adopting eco-friendly materials and manufacturing processes to align with evolving green building standards. Partnerships with construction firms, architects, and technology providers are common strategies to expand distribution channels and enhance solution offerings. Despite the dominance of established players, regional manufacturers continue to compete effectively by offering cost-efficient and customized hardware solutions tailored to local market requirements.

The report provides a comprehensive analysis of the competitive landscape in the architectural hardware market with detailed profiles of all major companies, including:

- Allegion plc

- Assa Abloy AB

- Bohle Ltd.

- CRH plc

- Godrej & Boyce Mfg. Co. Ltd.

- Häfele GmbH & Co KG

- Hettich Holding GmbH and Co. oHG

- HOPPE Holding AG

- Spectrum Brands Inc.

- Taiwan Fu Hsing Industrial Co. Ltd.

Latest News and Developments:

- In February 2026, Angus Capital, a Canadian mid-market private equity firm, acquired Capsol, a niche distributor based in Canada specializing in metal and wood doors, frames, and architectural hardware products.

- In December 2025, ASSA ABLOY completed the acquisition of Sargent and Greenleaf, a United States-based provider of high-quality electronic and mechanical locks founded in 1857. The acquisition is aimed at strengthening ASSA ABLOY's position in the high-security locking solutions segment and expanding its product portfolio in the North American market.

- In October 2025, ASSA ABLOY acquired Metal Products Inc. (MPI), a United States-based manufacturer of custom-made hollow metal doors and frames. MPI, founded in 1980 and based in Corbin, Kentucky, employs approximately 170 people and strengthens ASSA ABLOY's product offering in the Americas region.

Architectural Hardware Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Furniture, Doors, Windows, Shower |

| End Users Covered | Residential, Commercial, Industrial |

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | Allegion plc, Assa Abloy AB, Bohle Ltd., CRH plc, Godrej & Boyce Mfg. Co. Ltd., Häfele GmbH & Co KG, Hettich Holding GmbH and Co. oHG, HOPPE Holding AG, Spectrum Brands Inc., Taiwan Fu Hsing Industrial Co. Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders

- IMARC's report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the architectural hardware market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global architectural hardware market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Architectural Hardware industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Architectural Hardware Market Report

The architectural hardware market was valued at USD 19.5 Billion in 2025.

The architectural hardware market is projected to exhibit a CAGR of 3.90% during 2026-2034, reaching a value of USD 27.8 Billion by 2034.

The architectural hardware market is primarily driven by the growth of global construction and infrastructure development activities, rising urbanization, increasing consumer spending on home improvement and renovation, the growing adoption of smart and connected hardware solutions, escalating safety and security concerns, and the expanding emphasis on sustainable and energy-efficient building materials and practices.

North America currently dominates the architectural hardware market, accounting for a share of 29%. The region benefits from a mature construction sector, stringent building safety codes, high consumer spending on home improvement, and widespread adoption of advanced hardware technologies.

Some of the major players in the architectural hardware market include Allegion plc, Assa Abloy AB, Bohle Ltd., CRH plc, Godrej & Boyce Mfg. Co. Ltd., Häfele GmbH & Co KG, Hettich Holding GmbH and Co. oHG, HOPPE Holding AG, Spectrum Brands Inc., Taiwan Fu Hsing Industrial Co. Ltd., etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)