Argentina Aerospace Market Size, Share, Trends and Forecast by Type, Size, End User, Operation, and Region, 2026-2034

Argentina Aerospace Market Summary:

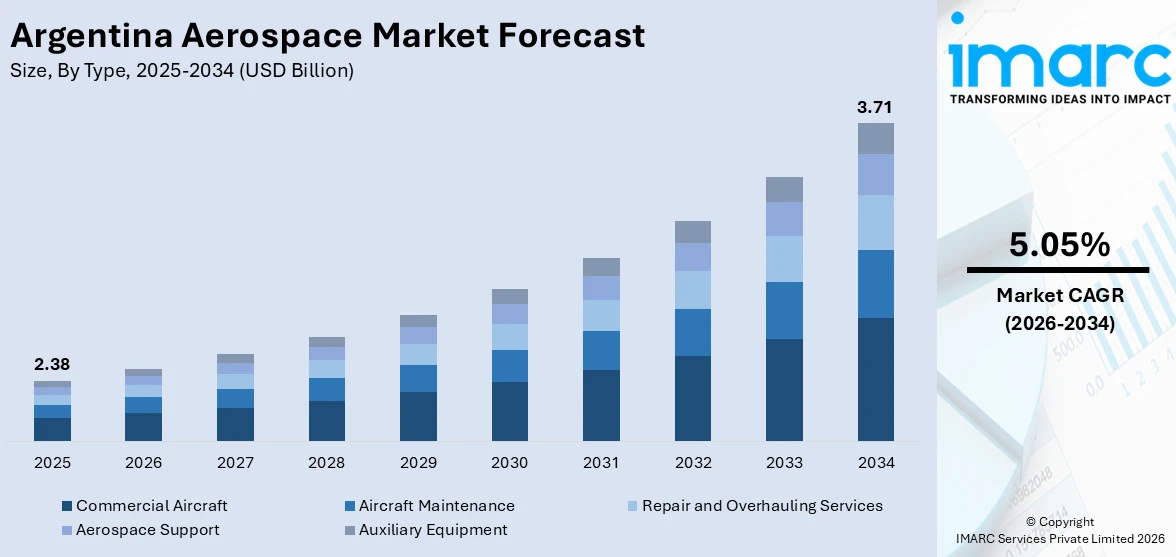

The Argentina aerospace market size was valued at USD 2.38 Billion in 2025 and is projected to reach USD 3.71 Billion by 2034, growing at a compound annual growth rate of 5.05% from 2026-2034.

The market is driven by increasing commercial air passenger traffic supported by aviation deregulation and open skies policies, growing government investments in military modernization and strategic defense procurement programs, and expanding maintenance, repair, and overhaul capabilities across the country. Rising demand for fleet renewal among domestic and regional carriers, advancements in indigenous aircraft manufacturing and design, strategic international defense partnerships, and broader regional air connectivity improvements are further strengthening the Argentina aerospace market share.

Key Takeaways and Insights:

-

By Type: Commercial aircraft dominates the market with a share of 44.6% in 2025, driven by expanding airline fleet renewal programs, rising passenger volumes, and growing demand for fuel-efficient aircraft across domestic and international routes.

-

By Size: Narrow body leads the market with a share of 62.3% in 2025, owing to their operational versatility on high-demand domestic routes, lower operating costs, and growing carrier preference for single-aisle fleet modernization.

-

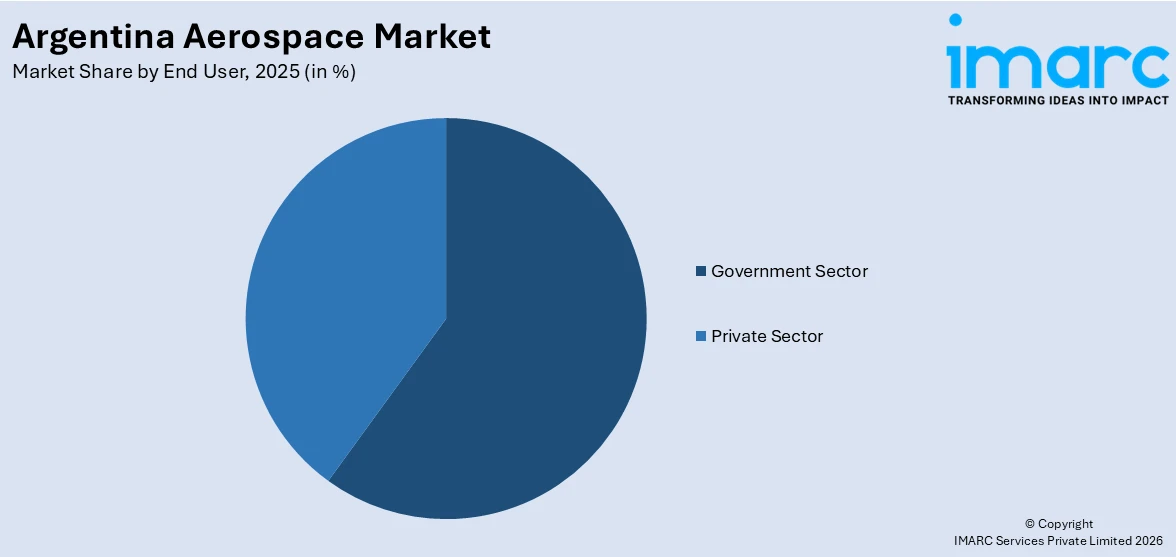

By End User: Government sector represents the largest segment with a market share of 53.1% in 2025, driven by strategic defense modernization initiatives, military aircraft procurement programs, and sovereign aerospace manufacturing investments.

-

By Operation: Manual aircraft dominates the market with a share of 71.4% in 2025, owing to continued reliance on piloted platforms for commercial transport, military operations, and general aviation activities.

-

By Region: Buenos Aires Region leads the market with a share of 36.8% in 2025, driven by the concentration of major airports, airline headquarters, MRO facilities, and defense establishments.

-

Key Players: The Argentina aerospace market features a competitive landscape with domestic manufacturers, state-owned defense enterprises, and international aviation corporations competing across commercial aircraft supply, military equipment procurement, maintenance, repair, and operations (MRO) services, and auxiliary equipment segments.

To get more information on this market Request Sample

The Argentina aerospace market is experiencing a transformative phase, driven by a convergence of commercial aviation expansion, defense modernization, and indigenous manufacturing revival. Government policies emphasizing open skies and aviation deregulation have attracted new international carriers, intensified route competition, and decentralized traffic across the country. According to reports, in June 2025, Argentina replaced extensive airline financial filings with one sworn solvency declaration under Provision 16/2025, simplifying approvals for passenger, cargo, and ramp operators and accelerating aviation market entry. Moreover, the defense sector is undergoing its most significant modernization effort in decades, with strategic fighter aircraft acquisition programs restoring critical military capabilities. Simultaneously, indigenous aerospace manufacturing is being revitalized through training aircraft production, advanced jet trainer programs, and international component supply partnerships. The growing emphasis on self-sufficiency in defense procurement, combined with expanding civil aviation demand and strengthened regional connectivity, is positioning Argentina as an emerging aerospace hub within Latin America.

Argentina Aerospace Market Trends:

Revival of Indigenous Aircraft Manufacturing and Design Capabilities

Argentina is witnessing a resurgence in domestic aircraft production as state-owned manufacturing capabilities are revitalized to reduce foreign dependency. In March 2025, FAdeA advanced the IA-100B Malvina trainer prototype for the Argentine Air Force, reinforcing local design and manufacturing capabilities after years of redevelopment. The country's primary aircraft factory is accelerating production of advanced military trainers, developing new basic training platforms, and expanding civil aviation maintenance certifications. These efforts are complemented by international component manufacturing partnerships and growing participation in global aerospace supply chains.

Expansion of Low-Cost Carrier Operations and Route Decentralization

The Argentina aviation landscape is being reshaped by the rapid expansion of low-cost and ultra-low-cost carriers that are intensifying route competition and broadening air connectivity beyond the traditional hub-and-spoke model centered on the capital. In December 2025, Argentina authorized LATAM to operate domestic routes under “open skies” reforms, allowing foreign airlines to run internal flights without a local subsidiary, boosting competition and connectivity. Aviation deregulation measures have enabled new operators to enter the market, establish direct international connections from provincial airports, and challenge established carriers on high-demand domestic corridors.

Integration of Digital Technologies in Aerospace Operations

Digital transformation is accelerating across Argentina's aerospace sector, with airlines and manufacturers adopting advanced technologies to enhance operational efficiency and passenger experience. Carriers are investing in fleet-wide connectivity solutions, digital flight training systems, and smart maintenance platforms to improve service quality and reduce operational costs. In December 2024, EANA selected Indra’s ManagAir platform to modernize air traffic management across Argentina’s five control centers, integrating advanced automation, 4D trajectory management, and safety networks nationwide. Aerospace manufacturers are incorporating virtual training software and domestically produced avionics into new aircraft platforms, reducing reliance on foreign technology suppliers.

Market Outlook 2026-2034:

The Argentina aerospace market is poised for sustained expansion, supported by continued commercial aviation growth, accelerating defense modernization programs, and the revitalization of indigenous manufacturing capabilities. Rising passenger traffic volumes, ongoing fleet renewal initiatives by domestic and regional carriers, strategic military procurement programs, and strengthening MRO infrastructure are expected to drive higher revenue streams across the forecast period. Increasing international defense cooperation, expanding low-cost carrier operations, growing regional air connectivity, and advancing digital aerospace technologies are anticipated to foster a more competitive, technologically advanced, and sustainable aerospace ecosystem across Argentina. The market generated a revenue of USD 2.38 Billion in 2025 and is projected to reach a revenue of USD 3.71 Billion by 2034, growing at a compound annual growth rate of 5.05% from 2026-2034.

Argentina Aerospace Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Commercial Aircraft |

44.6% |

|

Size |

Narrow Body |

62.3% |

|

End User |

Government Sector |

53.1% |

|

Operation |

Manual Aircraft |

71.4% |

|

Region |

Buenos Aires Region |

36.8% |

Type Insights:

- Commercial Aircraft

- Aircraft Maintenance

- Repair and Overhauling Services

- Aerospace Support

- Auxiliary Equipment

Commercial aircraft dominates with a market share of 44.6% of the total Argentina aerospace market in 2025.

The commercial aircraft is driving growth in Argentina's aerospace market as airlines undertake significant fleet renewal and expansion programs to meet surging travel demand. Rising passenger volumes on both domestic and international routes are fueling orders for modern, fuel-efficient narrow-body and wide-body aircraft. As per sources, in 2025, JetSMART introduced the A320neo in Argentina, adding 222 new flights, boosting domestic and international connectivity across multiple provinces, and supporting fleet modernization and sustainability goals. Open skies policies and aviation deregulation have encouraged new carrier entry and route expansion, intensifying demand for additional commercial aircraft capacity.

The growing presence of low-cost carriers is further expanding the commercial aircraft fleet operating within Argentina. Multiple airlines are introducing newer-generation aircraft with improved fuel efficiency and higher seating capacities to capitalize on expanding domestic and regional demand. Strengthened international connectivity and the emergence of provincial cities as direct international gateways are creating additional requirements for commercial aircraft suited to varying passenger densities. Fleet modernization strategies emphasizing operational cost reduction and enhanced passenger experience are accelerating procurement cycles and sustaining long-term demand across the commercial aviation segment.

Size Insights:

- Narrow Body

- Wide Body

Narrow body leads with a share of 62.3% of the total Argentina aerospace market in 2025.

Narrow body represent the backbone of Argentina's commercial aviation operations, serving the extensive domestic route network and regional connections across South America. These single-aisle aircraft offer significant operational cost advantages that make them ideal for the country's predominantly short-to-medium-haul routes connecting the capital with provincial cities and major tourist destinations. As per sources, in 2025, Flybondi announced a $1.7 billion fleet expansion, ordering 15 Airbus A220-300 and 10 Boeing 737 MAX 10 jets, reinforcing its narrow body operations and supporting growth across domestic and regional routes.

The dominance of narrow bodies is reinforced by the rapid expansion of low-cost carriers, which operate exclusively single-aisle fleets to maximize seat density and minimize unit costs. The domestic market structure, characterized by numerous high-frequency routes connecting major population centers, strongly favors narrow-body operations over wide-body alternatives. Growing passenger volumes on key domestic and regional corridors are prompting airlines to introduce larger narrow-body variants capable of carrying more passengers while maintaining comparable operating economics, further consolidating the segment's leading position within Argentina's aerospace market.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Private Sector

- Government Sector

Government sector exhibits a clear dominance with a 53.1% share of the total Argentina aerospace market in 2025.

The government sector dominance reflects Argentina's strategic commitment to military modernization and sovereign aerospace capability development. The current administration has prioritized defense procurement after decades of underinvestment, with the most significant military acquisition program in recent history now underway. As per sources, in December 2025, Argentina received the first batch of six F‑16 fighter jets under its multi-year procurement program, restoring supersonic capabilities and marking a major milestone in national defense modernization. Strategic fighter aircraft procurement programs are restoring critical combat capabilities that had been absent for nearly a decade following the retirement of previous-generation platforms.

Beyond fighter acquisition, the government maintains substantial aerospace spending through state-owned aircraft manufacturing operations, military maintenance programs, and indigenous defense technology development initiatives. Investments in training aircraft production, advanced jet trainer modernization, unmanned aerial system development, and flight simulator manufacturing underscore the sector's central role in the aerospace market. The administration's stated objective of progressively increasing defense spending as a share of national output is expected to sustain government-driven aerospace demand, supporting continued procurement, infrastructure development, and workforce expansion across the military aerospace value chain.

Operation Insights:

- Manual Aircraft

- Autonomous Aircraft

Manual aircraft leads with a market share of 71.4% of the total Argentina aerospace market in 2025.

Manual aircraft continue to account for most of the aerospace activity in Argentina, spanning commercial aviation, military operations, and general aviation sectors. The country's commercial airline fleet consists entirely of conventionally piloted aircraft, including narrow-body and wide-body jets operating across domestic and international networks, As per sources, the Argentine Air Force conducted the first flight of the IA‑100 Malvina basic trainer, a domestically developed piloted aircraft designed to enhance pilot training and support next-generation fleet readiness.

The sustained dominance of manual aircraft reflects the current regulatory framework, airspace management infrastructure, and operational requirements that favor human-piloted platforms for passenger transport, cargo operations, and defense missions. While autonomous and remotely piloted systems are emerging for surveillance, agricultural, and tactical applications, their market share remains modest relative to conventional manned platforms. The extensive pilot training ecosystem, including specialized military academies, civilian flight schools, and advanced simulator facilities, continues to support Argentina's piloted aircraft operations and reinforces the long-term structural advantage of manual aircraft across the market.

Regional Insights:

- Buenos Aires Region

- Litoral Region

- Northern Region

- Cordoba Region

- Cuyo Region

- Patagonia Region

Buenos Aires Region dominates with a market share of 36.8% of the total Argentina aerospace market in 2025.

Buenos Aires region serves as Argentina's primary aerospace hub, hosting the country's largest international airports, major airline headquarters, and critical aviation infrastructure. The metropolitan area handles most of the country's international and domestic passenger traffic through its principal gateway airports, which serve as the primary connection points for long-haul intercontinental services and regional routes. The region's concentration of private aviation operators, MRO service providers, and defense establishments further reinforces its dominant position within the national aerospace landscape, attracting sustained investment in aviation services and infrastructure.

The region benefits from a well-established ecosystem of aerospace support services, including aircraft leasing companies, ground handling operators, aviation training academies, and regulatory bodies that collectively facilitate efficient aviation operations. Buenos Aires also serves as the administrative center for civil aviation authority functions, airline management operations, and international route coordination activities. The presence of military aviation installations and defense procurement agencies within the region further strengthens its strategic importance, ensuring that Buenos Aires remains the focal point for aerospace decision-making, investment allocation, and operational activity across Argentina.

Market Dynamics:

Growth Drivers:

Why is the Argentina Aerospace Market Growing?

Surging Commercial Air Passenger Traffic and Aviation Deregulation

Argentina's commercial aviation sector is experiencing unprecedented growth, driven by comprehensive deregulation measures and open skies policies that have fundamentally transformed the competitive landscape. The government's decision to liberalize air transport has enabled new domestic and international carriers to enter the market, expand route networks, and offer increasingly competitive fares to travellers. As per sources, Santa Fe airports recorded a 79% increase in domestic flights from Sauce Viejo and a 60% rise in international flights from Rosario, reinforcing the province’s role as a key regional aviation hub. This liberalization has resulted in record passenger volumes across both domestic and international segments, with provincial airports emerging as direct international gateways.

Strategic Military Modernization and Defense Procurement Programs

Argentina is undertaking its most ambitious military modernization program in decades, with aerospace procurement forming a central pillar of national defense strategy. The current administration has prioritized restoring military capabilities that had deteriorated over prolonged periods of underinvestment, focusing on acquiring advanced multirole fighter aircraft, upgrading training platforms, and strengthening maintenance infrastructure. These strategic procurement decisions are generating substantial aerospace market activity across aircraft integration, pilot training, weapons systems deployment, and long-term sustainment programs. The emphasis on building domestic defense industrial capabilities through indigenous manufacturing and international technology partnerships is further expanding government-driven aerospace investment.

Expanding Maintenance, Repair, and Overhaul Service Capabilities

Argentina is progressively developing its domestic MRO ecosystem to reduce reliance on foreign service providers and capture greater value within the national aerospace industry. State-owned and private maintenance facilities are expanding their service portfolios to accommodate newer aircraft types entering the fleet, pursuing international quality certifications, and investing in advanced diagnostic and repair technologies. As per sources, FAdeA renewed its ANAC and Brazil MRO approvals, earned AS9100 and NADCAP certifications, and gained Chile DGAC authorization, enabling it to offer maintenance services for aircraft registered in multiple countries.

Market Restraints:

What Challenges the Argentina Aerospace Market is Facing?

Macroeconomic Instability and Currency Volatility

Argentina's chronic macroeconomic challenges, including high inflation, currency depreciation, and fiscal constraints, create significant headwinds for aerospace market expansion. The volatile economic environment complicates long-term procurement planning, increases the cost of imported aerospace equipment and components, and limits the purchasing power of both government and private sector participants. These conditions make financing arrangements for aircraft acquisitions and infrastructure investments more complex and costly.

Limited Domestic MRO Infrastructure and Supply Chain Gaps

Argentina's maintenance, repair, and overhaul ecosystem remains underdeveloped relative to the sector's growing needs, with many airlines depending on foreign service providers for heavy maintenance activities. The domestic MRO segment lacks the scale and specialization required to service the growing diversity of aircraft types operating across the country. Supply chain gaps in critical spare parts create operational dependencies on international suppliers.

Geopolitical Constraints on Military Equipment Access

Argentina's access to advanced military aerospace technology has been historically constrained by geopolitical factors, particularly long-standing military embargoes stemming from past conflicts. These restrictions have effectively narrowed the country's procurement options for advanced combat platforms and defense systems, limiting flexibility in sourcing equipment from diverse international suppliers. While recent procurement programs have partially addressed these barriers, broader geopolitical dynamics continue influencing acquisition strategies.

Competitive Landscape:

The Argentina aerospace market features a diverse competitive structure encompassing state-owned manufacturers, domestic private operators, and international aerospace corporations. Competition is intensifying across commercial aviation as deregulation attracts new entrants and existing carriers expand their fleet and route portfolios. In the defense segment, strategic procurement decisions are increasingly influenced by geopolitical alliances and technology transfer considerations. Key market participants are focusing on fleet modernization, operational efficiency improvements, MRO capability expansion, and strategic partnerships to strengthen their market positioning. The growing emphasis on indigenous manufacturing and technology localization is reshaping competitive dynamics as domestic capabilities are revitalized to complement international supply relationships.

Recent Developments:

-

In February 2026, TLON Space readied its Aventura I micro-launcher for launch from Malacara Spaceport, near Necochea, Argentina. The two-stage rocket, designed for small payloads to low Earth orbit, seeks to validate flight performance, gather operational data, and strengthen Argentina’s domestic space launch capabilities, marking a key milestone for the startup.

Argentina Aerospace Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Commercial Aircraft, Aircraft Maintenance, Repair and Overhauling Services, Aerospace Support, Auxiliary Equipment |

|

Sizes Covered |

Narrow Body, Wide Body |

|

End Users Covered |

Private Sector, Government Sector |

|

Operations Covered |

Manual Aircraft, Autonomous Aircraft |

|

Regions Covered |

Buenos Aires Region, Litoral Region, Northern Region, Cordoba Region, Cuyo Region, Patagonia Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Argentina Aerospace Market Report

The Argentina aerospace market size was valued at USD 2.38 Billion in 2025.

The Argentina aerospace market is expected to grow at a compound annual growth rate of 5.05% from 2026-2034 to reach USD 3.71 Billion by 2034.

Commercial aircraft held the largest Argentina aerospace market share, driven by expanding airline fleets, rising passenger volumes, fleet modernization programs, and growing demand for fuel-efficient next-generation aircraft across domestic and international routes.

Key factors driving the Argentina aerospace market include surging commercial air passenger traffic supported by aviation deregulation, strategic military modernization and defense procurement programs, revival of indigenous aerospace manufacturing capabilities, and expanding MRO services.

Major challenges include macroeconomic instability and currency volatility affecting procurement budgets, limited domestic MRO infrastructure and supply chain gaps, geopolitical constraints on military equipment access, underdeveloped aerospace workforce pipeline, and dependency on foreign technology suppliers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)