Argentina Dairy Farming Market Size, Share, Trends and Forecast by Product Type, Production Method, and Region, 2026-2034

Argentina Dairy Farming Market Summary:

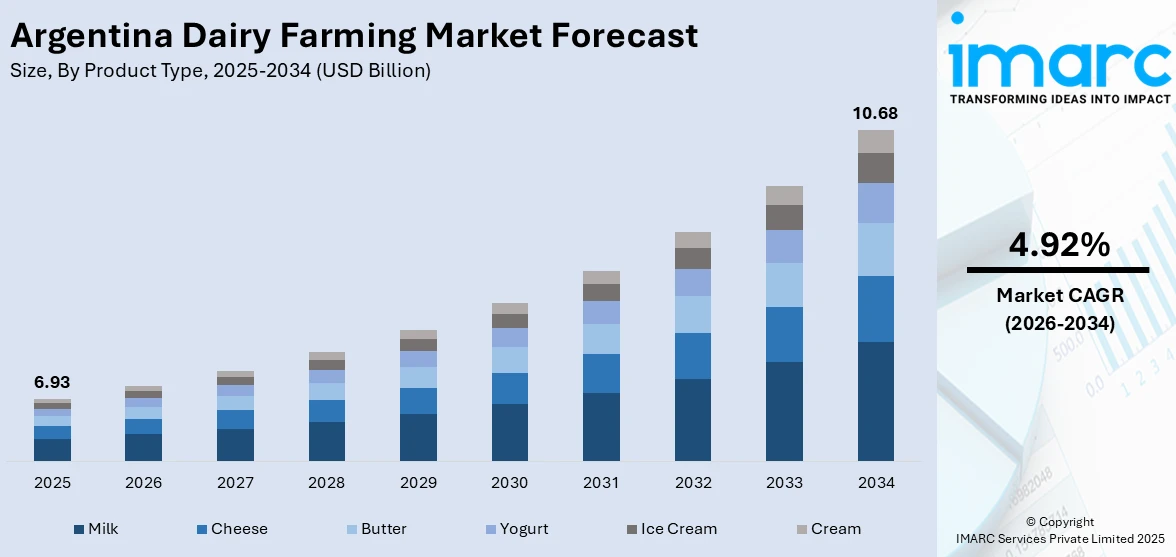

The Argentina dairy farming market size was valued at USD 6.93 Billion in 2025 and is projected to reach USD 10.68 Billion by 2034, growing at a compound annual growth rate of 4.92% from 2026-2034.

The Argentina dairy farming market is experiencing renewed momentum as the sector recovers from recent production challenges and benefits from favorable policy reforms. Strengthening producer profitability, expanding export opportunities, and growing domestic consumption are driving the market forward. Advancements in farm-level productivity, improved herd management practices, and modernization of processing infrastructure are supporting the long-term development of the industry, positioning Argentina as a competitive force in the global dairy trade and reinforcing the Argentina dairy farming market share.

Key Takeaways and Insights:

- By Product Type: Milk dominates the market with a share of 48.7% in 2025, owing to its fundamental role in daily nutrition, extensive domestic consumption base, and strong demand from processing industries for powder and fluid milk products across the country.

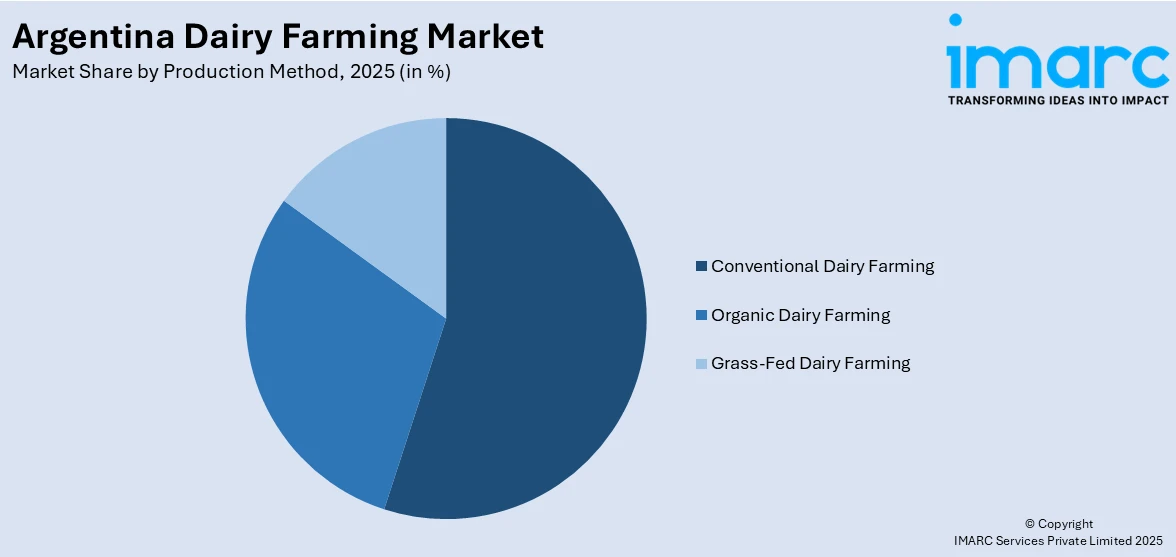

- By Production Method: Conventional dairy farming leads the market with a share of 67.9% in 2025. This dominance is driven by established pasture-based systems across the Pampas region, cost-effective production models, and widespread adoption of proven feeding and breeding practices.

- By Region: Buenos Aires Region represents the largest region with 41.5% share in 2025, driven by the concentration of major dairy processing facilities, favorable agro-climatic conditions, and proximity to key consumer and export distribution networks.

- Key Players: Key players drive the Argentina dairy farming market by expanding processing capacities, investing in precision agriculture technologies, enhancing product quality and export compliance, and forming strategic alliances to strengthen supply chain efficiency, boost producer profitability, and ensure consistent product availability across domestic and international markets.

To get more information on this market Request Sample

The dairy farming market in Argentina is developing well, with the conjunction of government reforms, improved farm economics, and growing consumer demand all coming together to provide a very encouraging environment for growth. A key catalyst in this development has been the strong production recovery of the sector, which has been supported by favorable policy measures and sustained profitability that has enabled producers to reinvest in operational efficiency and herd expansion. The removal of export duties further raised competitiveness, decreasing trade barriers and improving Argentina's position in global dairy markets. The expanding processing infrastructure, enhancing cold chain logistics, and increasing focus on product quality standards add to a more resilient and efficient dairy ecosystem. These, along with the increase in demand from other nations for Argentine dairy products, support the long-term expansion of the market.

Argentina Dairy Farming Market Trends:

Accelerating Per-Cow Productivity Through Genetic Advancement

Argentina's dairy sector is witnessing a significant shift toward higher per-cow output as producers adopt advanced genetic programs and precision feeding strategies. Despite a decline in total herd numbers, milk production has risen substantially due to improved animal genetics and management practices. Advanced crossbreeding programs across key dairy provinces are achieving strong yields while maintaining robust butterfat and protein content, reflecting the sector's growing emphasis on component-driven value creation. This focus on quality over quantity is reshaping the Argentina dairy farming market growth and strengthening the country's competitiveness in value-added dairy exports.

Expansion of Technology-Driven Farm Management

The operations of Argentine dairy farms are increasingly embracing the use of precision livestock farming solutions that include rumination collars, health monitoring technology, and data-enabled feed optimization tools. These cutting-edge technological solutions have enabled Argentine dairy farms to improve animal welfare, diagnose health problems, and enhance feed conversion efficiency. Major Argentine dairy farms in major provinces are using wearable sensor technology and real-time health monitoring technology to monitor animal behavior, optimize feeding patterns, and boost overall productivity. The growing adoption of precision livestock farming technology is enabling Argentine dairy farms to cut costs, improve milk quality parameters, and benefit from future efficiency gains.

Growing Export Diversification and Market Access

Argentina is actively broadening its dairy export footprint, with products now reaching a wide range of international markets. Whole milk powder remains the primary export product, while cheese shipments are gaining momentum. Argentine dairy exports continue to expand across the Middle East, North Africa, and Latin America, with key destinations emerging as consistent buyers of butter, milk powder, and specialty dairy products. The diversification of export channels, coupled with improved product traceability and compliance with international quality standards, is reinforcing Argentina's growing role as a reliable global dairy supplier.

Market Outlook 2026-2034:

Argentina’s dairy farming industry is projected to register a continuous growth trajectory during the forecast period. Dairy farmers in Argentina are likely to witness significant support from policies that improve their economic conditions. Moreover, growing global as well as local demand is one such factor that is going to propel the Argentina dairy farming industry during the coming years. The permanent abolition of export duties is going to enhance Argentina’s position as a significant participant in the global dairy trade cycle, especially regarding the export of milk powder and cheese. Also, with increased emphasis on precision agriculture and genetic enhancements, the overall dairy farming sector of Argentina is going to witness a quantum jump during the overall forecasting period. Additionally, access to new export markets coupled with increased processing potential is going to enable Argentina to register continuous growth during the near future. The market generated a revenue of USD 6.93 Billion in 2025 and is projected to reach a revenue of USD 10.68 Billion by 2034, growing at a compound annual growth rate of 4.92% from 2026-2034.

Argentina Dairy Farming Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Milk |

48.7% |

|

Production Method |

Conventional Dairy Farming |

67.9% |

|

Region |

Buenos Aires Region |

41.5% |

Product Type Insights:

- Milk

- Cheese

- Butter

- Yogurt

- Ice Cream

- Cream

Milk dominates with a share of 48.7% of the total Argentina dairy farming market in 2025.

Milk remains the cornerstone of Argentina’s dairy sector, driven by its essential role in household nutrition and its critical importance as a raw material for industrial processing. The country’s pasture-based production system supports large-scale fluid milk output at competitive costs, sustaining steady domestic supply. According to the industry report, Argentina’s milk production experienced a notable increase of 10.9% during the first quarter of 2025 compared to the same period in 2024. Rising consumer demand for both pasteurized and ultra-high-temperature processed milk continues to support this segment’s leading position across all distribution channels throughout the country.

The fluid milk segment benefits from an extensive cold chain infrastructure and well-established retail distribution networks that ensure nationwide availability. Argentina's robust processing capacity enables efficient conversion of raw milk into diverse product formats, including pasteurized, ultra-high-temperature, and powdered varieties. Ongoing investments in automated milking and storage technologies are enhancing milk quality, extending shelf life, and improving operational efficiency across the production chain. Growing consumer preference for fortified and specialty milk variants is further expanding product portfolios and supporting premium segment development across urban and semi-urban markets.

Production Method Insights:

Access the comprehensive market breakdown Request Sample

- Conventional Dairy Farming

- Organic Dairy Farming

- Grass-Fed Dairy Farming

Conventional dairy farming leads with a share of 67.9% of the total Argentina dairy farming market in 2025.

Conventional dairy farming dominates Argentina's production landscape, anchored by the country's extensive Pampas grasslands and well-established pasture-based feeding systems. The method leverages cost-effective production models that combine sown pastures with supplemental grain concentrates and maize silage, enabling consistent year-round milk output. The vast majority of the country's dairy production originates from conventional operations that benefit from favorable soil conditions, temperate climate, and decades of accumulated farming expertise. These structural advantages maintain conventional farming as the most economically viable and widely practiced production approach.

The conventional segment continues to evolve through the integration of modern technologies that enhance productivity without fundamentally altering the production model. Producers are increasingly adopting precision feeding protocols, automated health monitoring systems, and improved genetic selection programs within conventional frameworks. In August 2024, the Government of Argentina permanently eliminated export duties on dairy products through Decree 697/2024, significantly improving profitability for conventional dairy operations by reducing trade costs and encouraging reinvestment in farm infrastructure. This policy reform, combined with favorable milk-to-feed ratios and strong domestic demand, is reinforcing the economic competitiveness and long-term viability of conventional dairy farming.

Regional Insights:

- Buenos Aires Region

- Litoral Region

- Northern Region

- Cordoba Region

- Cuyo Region

- Patagonia Region

The Buenos Aires Region exhibits a clear dominance with a 41.5% share of the total Argentina dairy farming market in 2025.

The Buenos Aires Region remains the largest dairy production center, backed by its position as part of the fertile Pampas belt. This area is complemented by an unlimited supply of natural pastures suitable for livestock grazing. The province hosts the best facilities dedicated to dairy processing, with the largest players in the industry having multiple plants, particularly across the region. The presence of the largest consumer base, particularly in the Greater Buenos Aires Metropolis, creates an advantage when it comes to the distribution of fluid milk.

Also, Buenos Aires Region plays an important role as a dairy innovation and genetic improvement center, where high levels of crossbreeding activities are carried out to obtain high yields with strong component content. The region enjoys good infrastructural development in transport facilities that help link dairy producers with bigger retailers across the country and export markets. Strong periods of dairy producers' margins have been useful in improving investment levels in upgrading operations and increasing herd sizes, a factor that has particularly been witnessed with Buenos Aires producers. Continued investments are being made with an aim of improving automation levels, especially for milking, and improving quality control measures to increase competitive advantage for the region.

Market Dynamics:

Growth Drivers:

Why is the Argentina Dairy Farming Market Growing?

Supportive Government Policy Reforms and Trade Liberalization

The dairy farming market in Argentina is currently enjoying a significant impetus as the government implements all-encompassing policy reforms that aim at improving its competitiveness. This step has been initiated as part of a comprehensive policy that aims at reducing the cost burden in the agricultural sector. This is also part of the broader initiative of deregulation that aims at encouraging modernization processes in agricultural sectors. In addition to the liberalization process in the dairy sector, the government has also introduced innovative financial mechanisms that tackle the unique financial challenges facing the dairy farming sector. Specifically, the Bank of Investment and Foreign Trade, commonly referred to as BICE, has introduced financial credit mechanisms that tie loan repayment with the number of liters rather than the number of pesos. This step aims at protecting the farmers from fluctuations in currencies that could otherwise threaten their business during periods of investment.

Rising Domestic Consumption and Market Recovery

Argentina’s domestic dairy consumption is experiencing a meaningful recovery, driven by improving economic conditions and renewed consumer purchasing power. After a period of contraction linked to high inflation and reduced household incomes, dairy product sales across major categories are rebounding significantly. The growing domestic market is providing dairy producers and processors with a stable revenue foundation, reducing dependency on volatile export markets. Expanding urban populations, shifting dietary preferences toward protein-rich foods, and increasing awareness of the nutritional value of dairy products are reinforcing consumption patterns. Retailers are expanding dairy product assortments, including fortified, flavored, and premium variants, to meet evolving consumer expectations. This combination of recovering demand and product diversification is supporting higher capacity utilization across processing facilities and encouraging producers to maintain and expand production levels.

Improving Farm-Level Productivity and Profitability

Argentina's dairy farming sector is undergoing a structural transformation toward greater efficiency and per-cow productivity, creating a powerful growth driver for the overall market. Despite a reduction in total herd numbers, milk output has increased substantially due to improvements in genetics, feeding strategies, and farm management practices. The sector has demonstrated significant gains in individual animal performance, with production volumes rising even as the national herd contracts. Milk quality metrics have also improved, with butterfat and protein content trending upward, enhancing the value of each liter produced. This productivity-driven growth model is enabling Argentine dairy farmers to generate higher revenues from existing or smaller herds, improving overall farm economics and sustainability. The adoption of precision feeding technologies, automated health monitoring systems, and advanced reproductive management tools is accelerating this transition. Extended periods of positive producer margins have given farmers the financial confidence to reinvest in operational improvements and herd development programs. This virtuous cycle of investment, productivity improvement, and profitability enhancement is establishing a stronger foundation for sustained market growth.

Market Restraints:

What Challenges the Argentina Dairy Farming Market is Facing?

Macroeconomic Volatility and Currency-Related Risks

The persistent economic instability in Argentina poses a significant challenge to the dairy farming sector, as frequent currency devaluations, inflationary pressures, and unpredictable fiscal policies create an uncertain operating environment. Peso devaluations cause immediate spikes in dollar-denominated input costs, including feed concentrates, equipment, and fuel, while milk prices adjust much more slowly, compressing producer margins during adjustment periods. This misalignment between rapidly rising costs and slower revenue recovery creates short-term financial pressure that can force smaller operations to reduce production or exit the market entirely.

Accelerating Farm Consolidation and Structural Decline

The Argentine dairy sector is experiencing rapid structural consolidation, with the total number of dairy farms declining dramatically over recent decades as smaller operations exit the industry. This trend disproportionately affects small and medium-sized operations that lack the scale, financial resilience, and access to capital needed to invest in productivity-enhancing technologies. The concentration of production among fewer, larger farms raises concerns about supply chain resilience, regional economic impacts, and the long-term sustainability of rural communities dependent on dairy farming.

Climate Vulnerability and Weather Dependence

Argentina’s predominantly pasture-based dairy farming system remains highly susceptible to climate variability, including droughts, flooding, and temperature extremes that directly affect forage availability and animal productivity. Central Buenos Aires province experienced excessive rainfall and flooding, causing production disruptions and logistical challenges for milk collection. La Niña weather patterns have previously created pasture challenges in southern provinces, while heat stress during summer months reduces milk output and compromises animal welfare. The sector’s dependence on favorable weather conditions introduces inherent uncertainty into production forecasts.

Competitive Landscape:

The Argentina dairy farming market possesses a competitive market structure where integrated players compete against smaller-scale dairy producers in the Pampas Dairy Basins. The prominent players are expanding their processing capabilities, globalization-oriented production facilities, and strategic acquisition activities to strengthen their market share. The major integrated players are differentiating their market position by optimizing their products and supply chains, while the trends of incorporating the latest technology in farming activities and further strengthening the exports and quality compliance of products are altering the competitive scenario. In addition, the focus on differentiating their products, especially those belonging to the value-added segment of the dairy products market, is creating a challenging scene for the milk producers.

Argentina Dairy Farming Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Milk, Cheese, Butter, Yogurt, Ice Cream, Cream |

|

Production Methods Covered |

Conventional Dairy Farming, Organic Dairy Farming, Grass-Fed Dairy Farming |

|

Regions Covered |

Buenos Aires Region, Litoral Region, Northern Region, Cordoba Region, Cuyo Region, Patagonia Region |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Argentina Dairy Farming Market Report

The Argentina dairy farming market size was valued at USD 6.93 Billion in 2025.

The Argentina dairy farming market is expected to grow at a compound annual growth rate of 4.92% from 2026-2034 to reach USD 10.68 Billion by 2034.

Milk dominated the market with a share of 48.7%, driven by its fundamental role in daily nutrition, extensive domestic consumption patterns, strong industrial processing demand for powder and fluid variants, and well-established distribution networks.

Key factors driving the Argentina dairy farming market include supportive government policy reforms including export duty elimination, rising domestic dairy consumption recovery, improving farm-level productivity through genetic advancement and precision farming technologies, and expanding export market access.

Major challenges include persistent macroeconomic volatility and currency devaluation risks, accelerating farm consolidation reducing active operations, climate vulnerability affecting pasture-based production, rising input costs for feed and equipment, and supply chain inefficiencies across the fragmented dairy processing sector.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)