Arteriovenous Fistula Devices Market Report by Type (AVF Creation Devices, AVF Monitoring Devices, AVF Maintenance Devices), End User (Hospitals, Ambulatory Surgical Centers, Dialysis Centers), and Region 2026-2034

Market Overview:

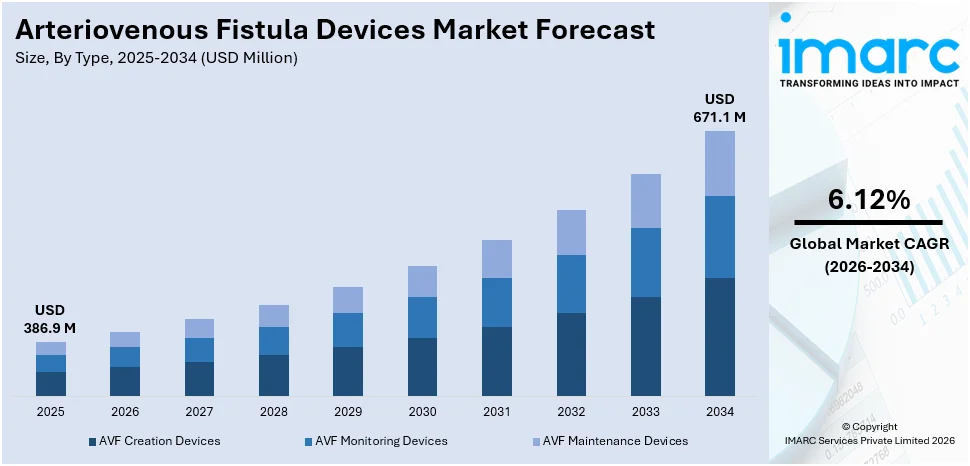

The global arteriovenous fistula devices market size reached USD 386.9 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 671.1 Million by 2034, exhibiting a growth rate (CAGR) of 6.12% during 2026-2034. The escalating awareness among patients, healthcare professionals, and caregivers about the benefits of AV fistulas, the growing preferences for hemodialysis in elderly patients due to their better long-term outcomes, and the development of patient-centric AVF devices are some of the major factors propelling the market.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 386.9 Million |

| Market Forecast in 2034 | USD 671.1 Million |

| Market Growth Rate (2026-2034) | 6.12% |

Arteriovenous fistula devices are surgical constructs created to facilitate long-term access to the circulatory system, often for dialysis in patients with end-stage renal disease. A direct connection is established between an artery and a vein, typically in the patient's arm, creating a high-flow, low-resistance pathway that allows for repeated access without causing undue trauma to the blood vessels. The elevated blood flow causes the vein to thicken and enlarge, providing a robust site for needle insertion during dialysis procedures. This arteriovenous fistula (AVF) is preferred over other vascular access methods due to lower complications such as infection and clotting. It's a living part of the patient's body, providing reliable access with proper care and maintenance. As medical devices, AVFs are crucial for the viability and efficiency of hemodialysis treatments, improving patient outcomes and quality of life.

To get more information on this market Request Sample

The rising awareness among patients, healthcare professionals, and caregivers about the benefits of AV fistulas majorly drives the global market. Educational initiatives by healthcare organizations and patient advocacy groups are promoting AVFs as the gold standard for vascular access in hemodialysis patients. Along with this, the elderly population is more susceptible to kidney-related diseases and often requires renal replacement therapies. As the global population continues to age, the demand for AVF devices is increasing, as they are the preferred vascular access for hemodialysis in elderly patients due to their better long-term outcomes. In addition, improving reimbursement policies and support from government healthcare programs in many countries have made AVF creation more financially accessible to patients. Favorable reimbursement encourages healthcare providers to recommend AVF devices as the primary choice for vascular access. Apart from this, collaboration between medical device manufacturers and healthcare providers has led to the development of patient-centric AVF devices, further impacting the market. Moreover, the integration of technologies in dialysis systems improving compatibility with AVF devices, and enhancing overall treatment efficacy and patient outcomes is creating a positive market outlook.

Arteriovenous Fistula Devices Market Trends/Drivers:

Growing Prevalence of Chronic Diseases

The increasing prevalence of end-stage renal disease (ESRD) and chronic kidney disease (CKD) is a significant market driver for arteriovenous fistula devices. ESRD and CKD are chronic conditions that lead to the loss of kidney function, necessitating renal replacement therapies, including hemodialysis. As the global population ages and the incidence of lifestyle-related diseases such as diabetes and hypertension rise, the number of individuals suffering from CKD and ESRD is escalating. Arteriovenous fistulas (AVFs) are considered the preferred vascular access for hemodialysis due to their superior long-term patency and lower infection rates compared to other access types. As the demand for renal replacement therapies rises, the need for reliable and efficient AVF devices increases. Manufacturers in the market strive to develop technologically advanced and durable AVF devices to meet the growing requirements of the dialysis patient population.

Rising Preference for AV Fistulas over Other Vascular Access Devices

The growing preference for AV fistulas over other vascular access devices, such as arteriovenous grafts and central venous catheters, is a significant driver propelling the market forward. AV fistulas have shown superior long-term outcomes, including lower rates of infection, thrombosis, and hospitalization compared to alternative access methods. Along with this, healthcare providers and regulatory bodies across the globe are recognizing the clinical benefits of AV fistulas and are increasingly recommending them as the first-choice vascular access for hemodialysis. Additionally, the cost-effectiveness of AVF devices, as they eliminate the need for frequent replacements and associated complications, further supports their preference. As healthcare systems and payers aim to enhance patient outcomes and reduce the overall cost burden, the shift toward AV fistulas is accelerating on the global level.

Advancements in Arteriovenous Fistula Device Technology

The continuous advancements in medical technology are another crucial driver for the arteriovenous fistula device market. In recent years, there has been significant progress in AVF device design, materials, and manufacturing processes. These innovations have resulted in improved functionality, increased longevity, and enhanced biocompatibility of AVF devices. One of the key innovations is the development of biocompatible materials that reduce the risk of thrombosis, stenosis, and infection at the fistula site. Additionally, the integration of imaging technologies has enabled better preoperative planning, leading to more successful AVF creation procedures. Furthermore, advancements in minimally invasive surgical techniques have reduced patient discomfort and recovery time, making AVF creation a more attractive option for patients and healthcare providers alike. As technology continues to evolve, it is expected that AVF devices will become even more efficient, contributing to the expansion of the market.

Arteriovenous Fistula Devices Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global arteriovenous fistula devices report, along with forecasts at the global, regional, and country levels from 2026-2034. Our report has categorized the market based on type and end user.

Breakup by Type:

- AVF Creation Devices

- Surgical Instruments

- Vascular Grafts

- Angioplasty Balloons

- Others

- AVF Monitoring Devices

- Doppler Ultrasound

- Pressure Monitoring Systems

- Others

- AVF Maintenance Devices

- Central Venous Catheters

- Stents

- Others

AVF creation devices dominates the market

The report has provided a detailed breakup and analysis of the market based on the type. This includes AVF creation devices (surgical instruments, vascular grafts, angioplasty balloons, and others), AVF monitoring devices (doppler ultrasound, pressure monitoring systems, and others), AVF maintenance devices (central venous catheters, stents, and others). According to the report, AVF creation devices represented the largest segment.

The market drivers for AVF creation devices in the arteriovenous fistula (AVF) devices industry are primarily fueled by the increasing prevalence of end-stage renal disease (ESRD) and chronic kidney disease (CKD) globally. As the incidence of these conditions rises due to factors, such as an aging population and lifestyle-related diseases, the demand for reliable vascular access for hemodialysis, such as AVFs, is growing. Additionally, technological advancements in AVF creation devices, including the development of biocompatible materials and minimally invasive surgical techniques, further enhance their appeal to healthcare providers and patients. Furthermore, the preference for AVF procedures over other vascular access methods, driven by superior long-term outcomes and cost-effectiveness, boosts the adoption of AVF creation devices, propelling the market forward.

On the contrary, AVFs are the preferred vascular access for hemodialysis, and their long-term success heavily relies on regular monitoring to detect potential complications early. AVF monitoring devices enable healthcare providers to assess blood flow, detect stenosis, thrombosis, or infections promptly, and intervene when necessary, reducing the risk of AVF failure and associated complications. In addition, the increasing prevalence of end-stage renal disease (ESRD) and the rising adoption of AVF procedures contribute to the demand for efficient and accurate AVF monitoring devices, ensuring optimal patient outcomes and further driving the market.

Breakup by End User:

Access the comprehensive market breakdown Request Sample

- Hospitals

- Ambulatory Surgical Centers

- Dialysis Centers

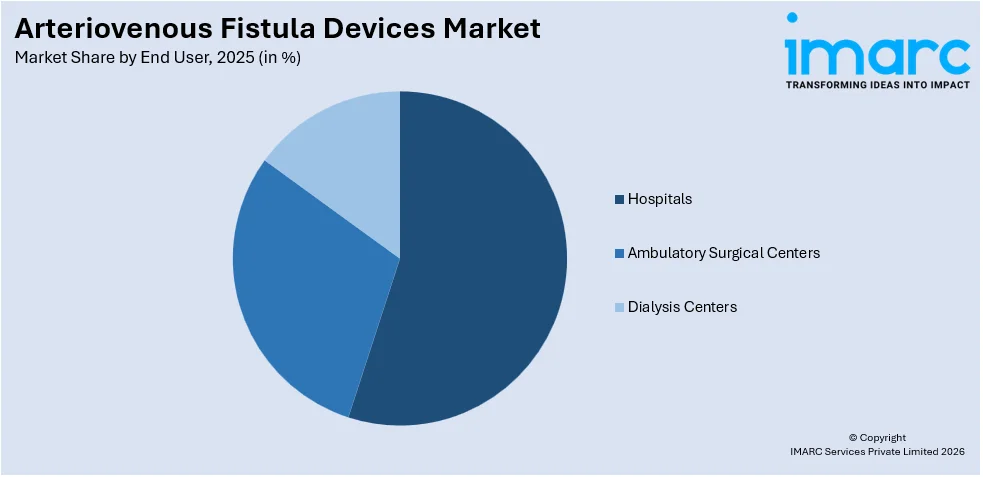

Hospitals hold the largest share in the market

A detailed breakup and analysis of the market based on the end user has also been provided in the report. This includes hospitals, ambulatory surgical centers, and dialysis centers. According to the report, hospitals accounted for the largest market share.

The hospital end use segment in the arteriovenous fistula (AVF) devices industry is driven by the rising prevalence of chronic kidney disease (CKD) and end-stage renal disease (ESRD). This is leading to an increased demand for renal replacement therapies, such as hemodialysis, where AVFs are the preferred vascular access. As hospitals play a critical role in providing hemodialysis treatments, their demand for AVF devices is directly influenced by the growing number of patients requiring such procedures. In confluence with this, hospitals typically have specialized nephrology departments and skilled healthcare professionals who can efficiently perform AVF creation and monitoring procedures. Moreover, the centralization of dialysis services in hospitals offers cost-effectiveness and streamlined patient management, further promoting the adoption of AVF devices in hospital settings.

On the other hand, the increasing trend towards outpatient care and the preference for minimally invasive procedures have led to a rising number of AVF creation and monitoring procedures being performed in ASCs. Patients often prefer the convenience and shorter recovery time associated with ASCs, which boosts the demand for AVF devices in these settings. In confluence with this, advancements in AVF device technology and surgical techniques have made it feasible to carry out AVF procedures in ASCs safely and effectively, further driving their adoption.

Breakup by Region:

- North America

- United States

- Canada

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Others

- Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America exhibits a clear dominance, accounting for the largest arteriovenous fistula devices market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America represented the largest market.

The arteriovenous fistula (AVF) devices industry in North America is driven by the high prevalence of end-stage renal disease (ESRD) and chronic kidney disease (CKD) in the region. The aging population and the increasing incidence of diabetes and hypertension contribute to the growing prevalence of kidney-related conditions, leading to a higher number of patients requiring hemodialysis with AVF as the preferred vascular access. In addition, North America influences a well-established healthcare infrastructure with advanced medical facilities, skilled healthcare professionals, and access to cutting-edge technologies. This conducive environment fosters the development and adoption of innovative AVF devices, supporting the market's growth. Moreover, a strong focus on patient-centric care and the continuous advancements in AVF device technology further drive the growth of the arteriovenous fistula devices industry in North America.

On the contrary, Asia Pacific is estimated to expand further in this domain due to the region's large and aging population, along with an escalating prevalence of diabetes and hypertension. Additionally, improvements in healthcare infrastructure and the growing awareness about advanced treatment options are driving the adoption of AVF devices. Along with this, the region's rapid economic growth has increased healthcare spending, providing patients with better access to renal replacement therapies with AVF as the preferred vascular access.

Competitive Landscape:

The global arteriovenous fistula devices market is experiencing significant growth due to the growing investments in research and development to design and develop innovative AVF devices. This includes exploring new materials, refining device designs for improved biocompatibility and functionality, and integrating advanced technologies to enhance monitoring and treatment outcomes. Along with this, companies are conducting clinical trials and studies to assess the safety and efficacy of their AVF devices to help gather data to support regulatory approvals is significantly supporting the market. In addition, establishing distribution networks, obtaining regulatory approvals, and developing partnerships with local healthcare providers are positively influencing the market. Apart from this, the rising number of mergers, acquisitions, and partnerships among the companies is favorably impacting the market. Furthermore, innovations aimed to improve the ease of use for healthcare professionals during AVF creation and monitoring procedures are contributing to the market.

The report has provided a comprehensive analysis of the competitive landscape in the global arteriovenous fistula devices market. Detailed profiles of all major companies have also been provided. Some of the key players in the market include:

- B. Braun SE

- Becton Dickinson and Company

- Fresenius Medical Care AG & Co. KGaA

- Laminate Medical Technologies

- Medtronic plc

- Poly Medicure Ltd.

Arteriovenous Fistula Devices Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered |

|

| End Users Covered | Hospitals, Ambulatory Surgical Centers, Dialysis Centers |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, and Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | B. Braun SE, Becton Dickinson and Company, Fresenius Medical Care AG & Co. KGaA, Laminate Medical Technologies, Medtronic plc, Poly Medicure Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global arteriovenous fistula devices market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global arteriovenous fistula devices market?

- What is the impact of each driver, restraint, and opportunity on the global arteriovenous fistula devices market?

- What are the key regional markets?

- Which countries represent the most attractive arteriovenous fistula devices market?

- What is the breakup of the market based on the type?

- Which is the most attractive type in the arteriovenous fistula devices market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the arteriovenous fistula devices market?

- What is the competitive structure of the global arteriovenous fistula devices market?

- Who are the key players/companies in the global arteriovenous fistula devices market?

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the arteriovenous fistula devices market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global arteriovenous fistula devices market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the arteriovenous fistula devices industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade