Artificial Turf Market Size, Share, Trends and Forecast by Material, Application, Distribution Channel, and Region 2026-2034

Artificial Turf Market Size, Share, Trends & Forecast (2026-2034)

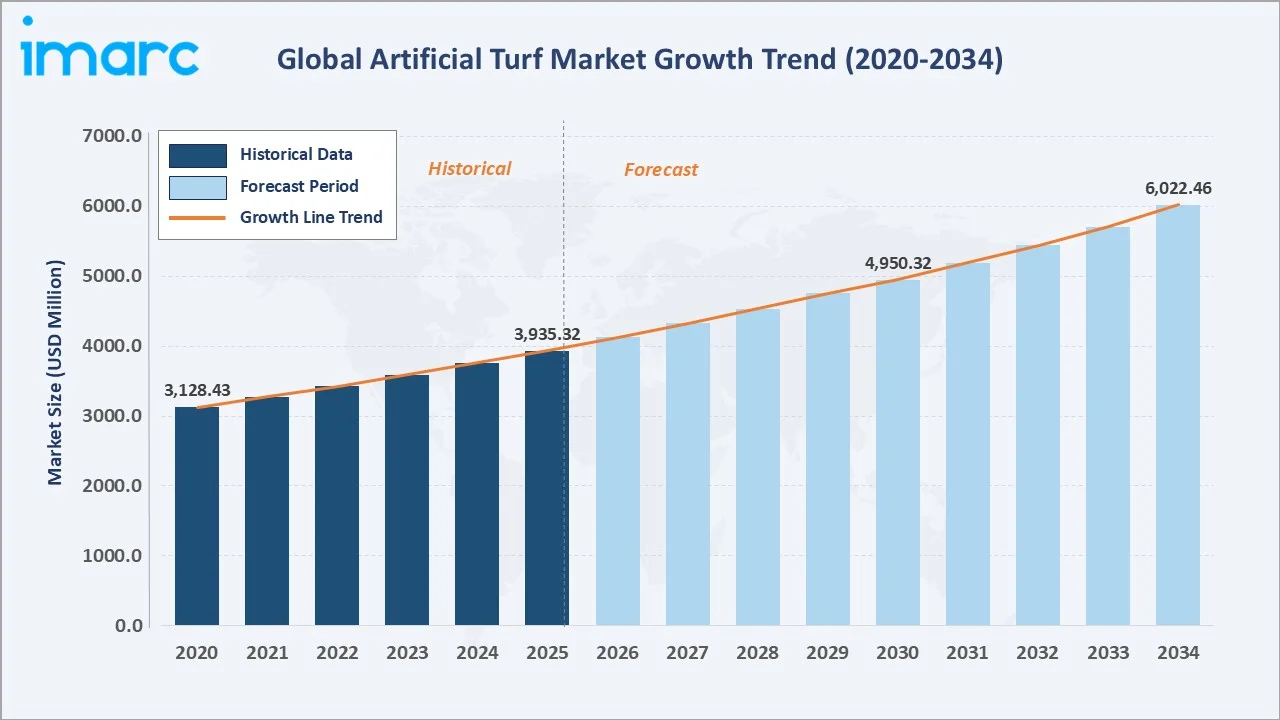

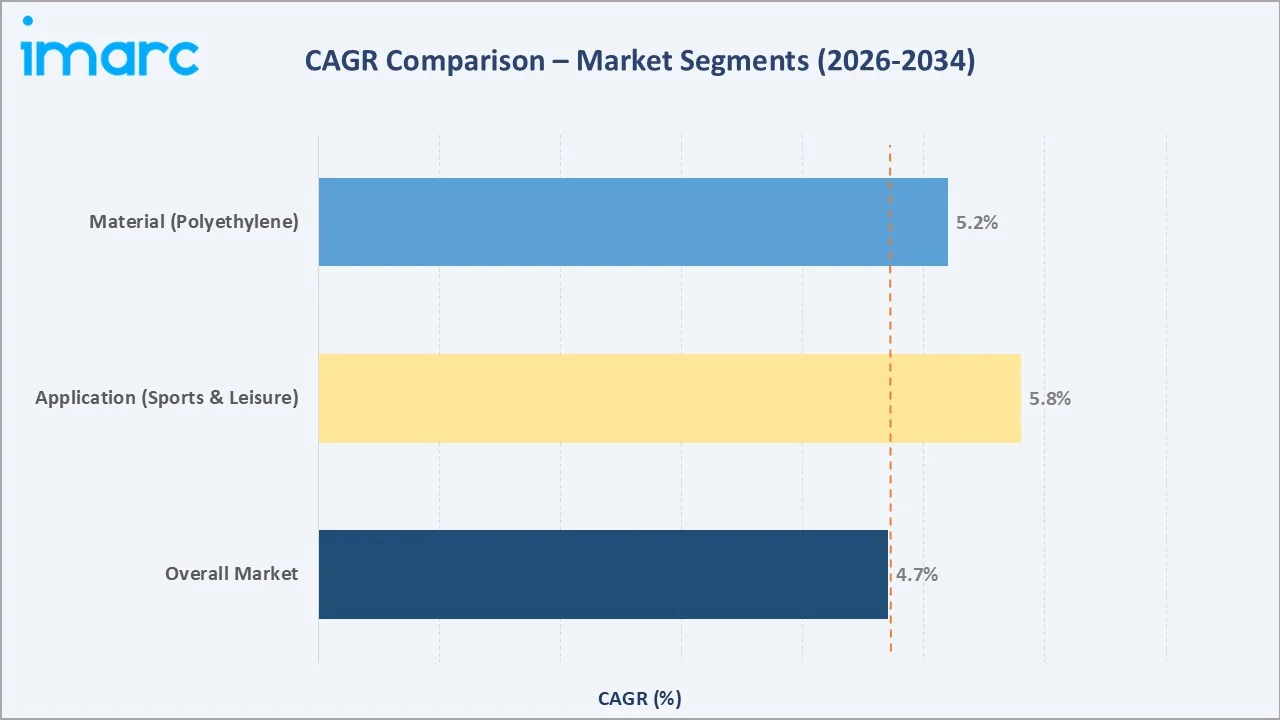

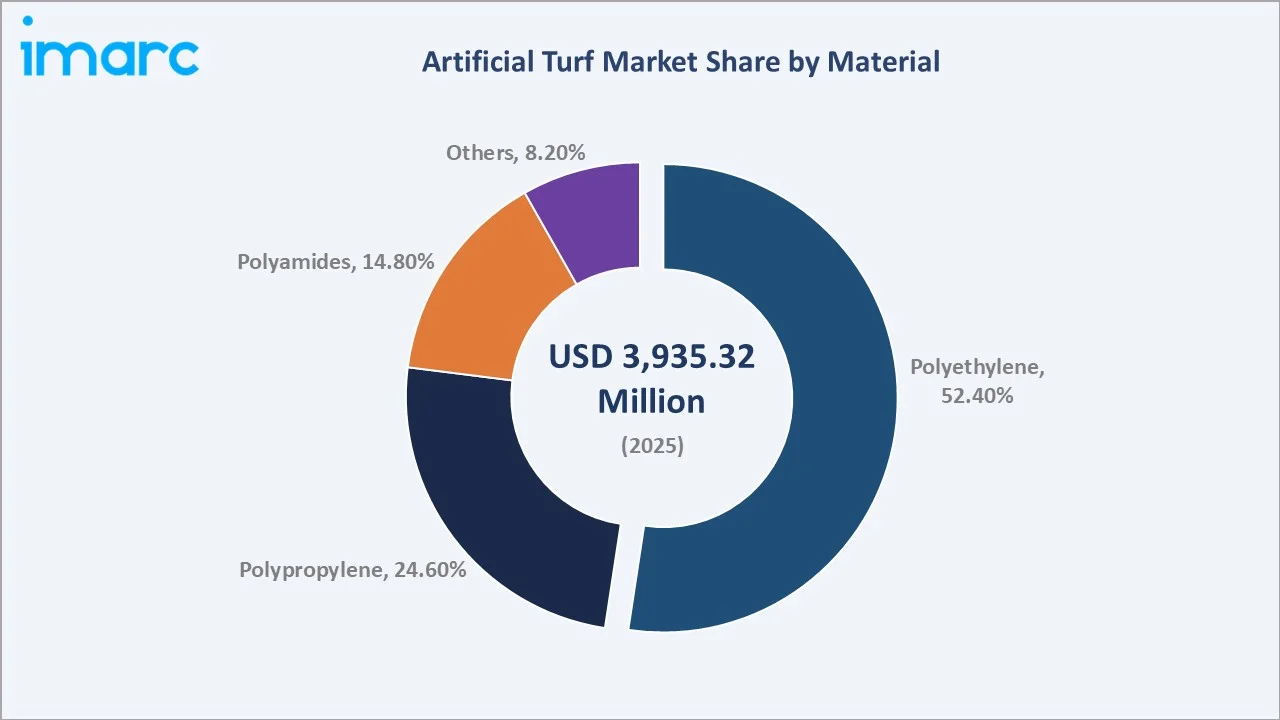

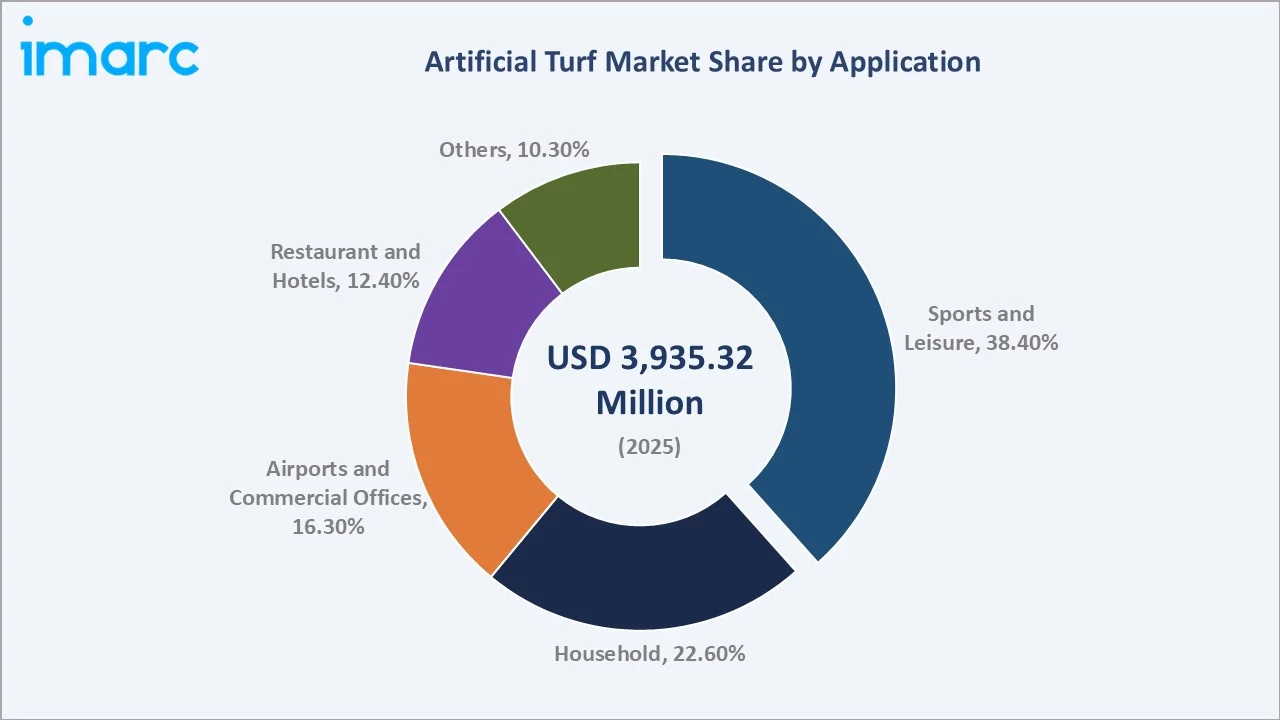

The global artificial turf market reached USD 3,935.32 Million in 2025 and is projected to reach USD 6,022.46 Million by 2034, growing at a CAGR of 4.70% during 2026-2034. Rising demand for low-maintenance, durable outdoor surfaces, rapid urbanization, and growing investments in sports infrastructure are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3,935.32 Million |

|

Forecast Market Size (2034) |

USD 6,022.46 Million |

|

CAGR (2026-2034) |

4.70% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

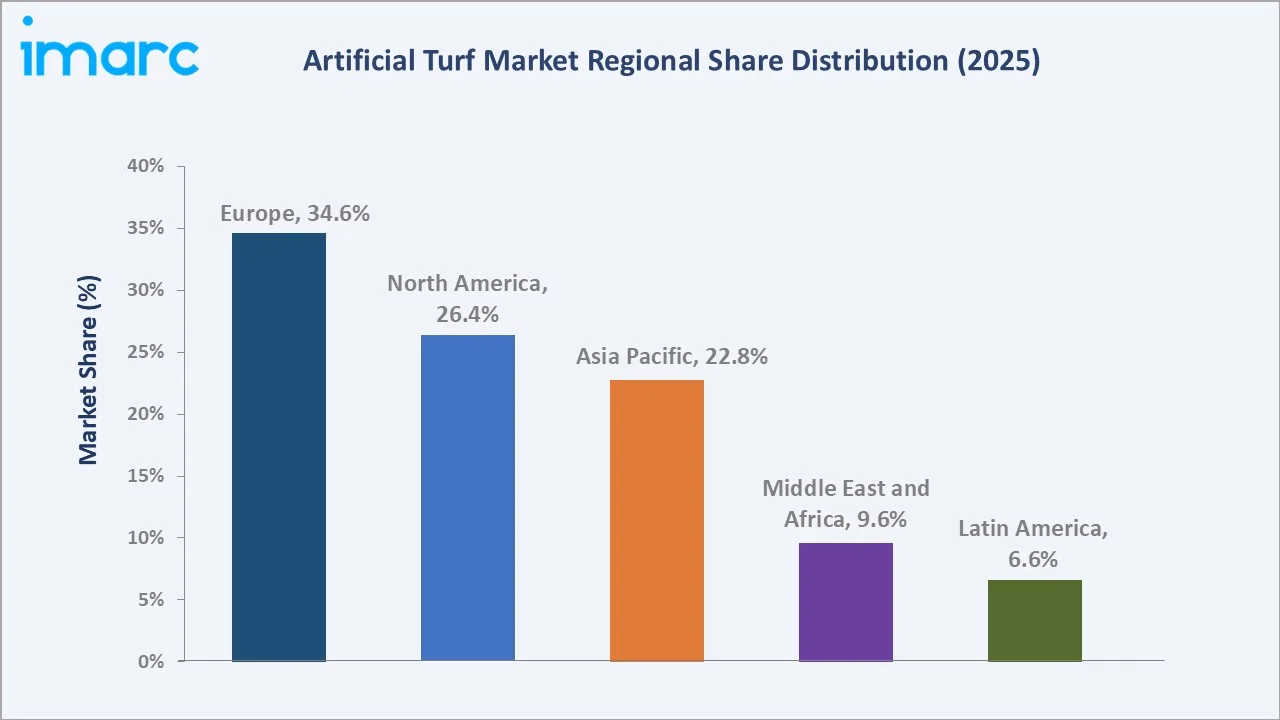

Largest Region |

Europe (34.6% share, 2025) |

|

Fastest Growing Region |

Asia Pacific |

Europe dominates, holding a 34.6% market share in 2025, while the sports and leisure segment leads application demand at 38.4%. Polyethylene remains the dominant material with a 52.4% share. Artificial turf offers numerous advantages over natural grass, including water conservation, reduced maintenance costs, and enhanced performance, making it a preferred choice for sports stadiums, recreational areas, and residential landscapes.

To get more information on this market, Request Sample

With applications spanning various sectors, including sports, landscaping, and commercial use, the market is expected to continue expanding, supported by innovations in eco-friendly materials and increasing adoption in regions with challenging climates or water scarcity.

Executive Summary

The global artificial turf market is on a sustained growth path, underpinned by increasing infrastructure investments, rising sports participation, and the widespread shift from natural grass to synthetic alternatives across commercial, residential, and public applications. The market reached USD 3,935.32 Million in 2025 and is forecast to surpass USD 6,022.46 Million by 2034. This trajectory reflects a healthy CAGR of 4.70% over the forecast period.

Europe leads globally with a 34.6% revenue share in 2025, driven by a strong sports culture and ongoing stadium upgrades across Germany, the UK, and France. Asia Pacific, at 22.8%, represents the fastest-growing opportunity, with China, Japan, and South Korea investing heavily in football and multipurpose facilities. Polyethylene dominates material use at 52.4% due to its softness, UV resistance, and versatility.

Sports and leisure applications command the largest share at 38.4%, followed by household (22.6%) and Airports & Commercial Offices (16.3%). Leading players - including CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), and Polytan GmbH - continue to invest in eco-friendly, recyclable turf systems to align with tightening environmental regulations.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Material) |

Polyethylene – 52.4% share (2025) |

|

Largest Segment (Application) |

Sports and Leisure – 38.4% share (2025) |

|

Leading Region |

Europe – 34.6% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific (urbanization + sports investment) |

|

Top Companies |

CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), Polytan GmbH |

|

Market Opportunity |

Eco-friendly recyclable turf projected at USD 1.2 billion by 2034 |

Key Analytical Observations Supporting The Above Data:

- Polyethylene accounts for 52.4% of the artificial turf market in 2025, preferred for sports pitches and residential lawns due to superior durability, natural aesthetics, and compliance with FIFA quality standards.

- Sports and leisure is the dominant application segment at 38.4% (2025), fueled by rising football, cricket, and rugby participation globally and increased allocation of public budgets toward all-weather pitches.

- Europe holds 34.6% of the global market in 2025, led by Germany, the UK, France, and the Netherlands, all of which have government-mandated sports facility upgrade programs underway.

- Asia Pacific is emerging as the fastest-growing region, driven by China's plan to expand football pitch infrastructure in urban communities over the next 15 years, aiming for full coverage nationwide by 2035.

- Eco-friendly and lead-free artificial turf is gaining regulatory momentum, with the EU's REACH regulation restricting PFAS content in synthetic turf infill materials, reshaping procurement standards from 2024 onward.

Global Artificial Turf Market Overview

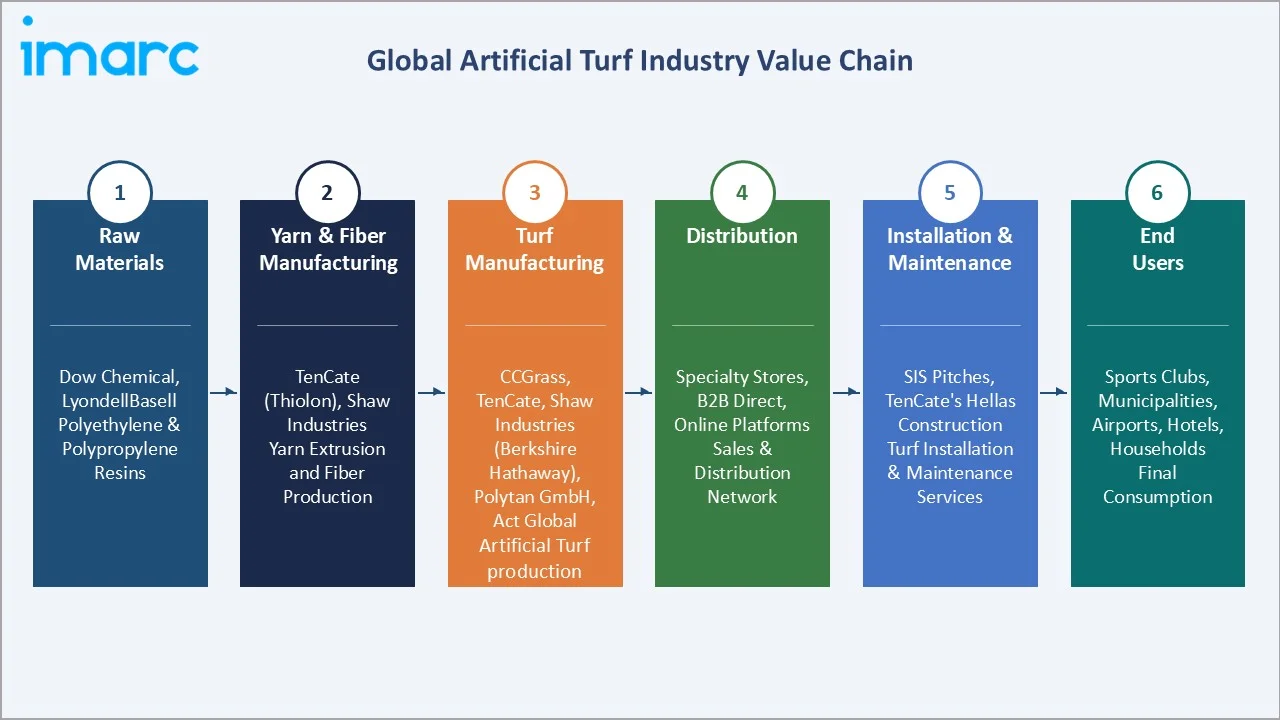

Artificial turf is a synthetic surface material engineered to replicate the appearance and functionality of natural grass. Originally developed for stadium applications in the 1960s, its use has expanded to encompass residential landscaping, commercial interiors, airports, hotels, and public parks. The market ecosystem spans raw polymer producers, yarn manufacturers, backing material suppliers, installation contractors, and infill material providers.

Macroeconomic factors, including rapid urbanization, water conservation mandates, and rising sports participation, are primary growth catalysts. Artificial turf conserves water, eliminates the need for regular maintenance, retains its pristine appearance for years, and remains playable in adverse weather.

Market Dynamics

To evaluate market opportunities, Request Sample

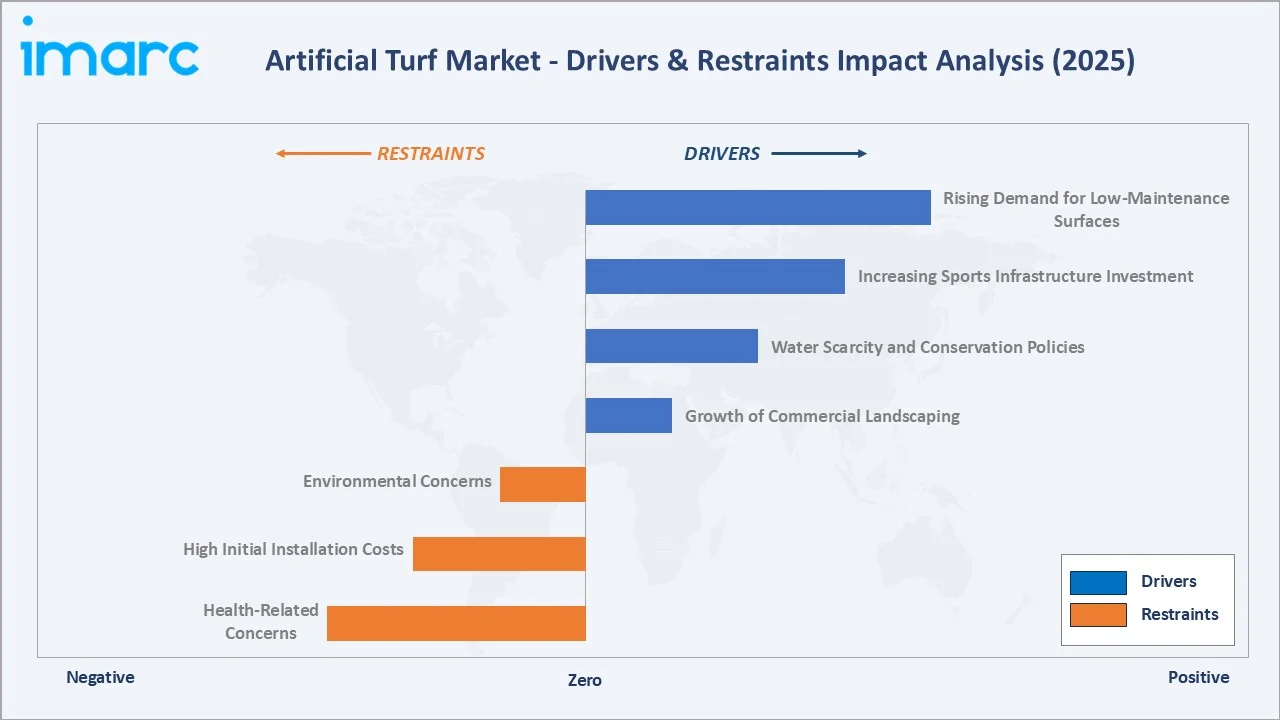

Market Drivers

- Rising Demand for Low-Maintenance Surfaces: Maintenance costs for artificial turf are generally lower, amounting to approximately USD 7,000 over its 25-year lifespan, compared to around $50,000 for natural grass, as per a comparison by Ideal Turf.

- Increasing Sports Infrastructure Investment: The global sports industry revenue is projected to reach approximately USD 623 billion by 2027, with approximately 14% allocated to artificial turf installation across football, hockey, and multi-use facilities.

- Water Scarcity and Conservation Policies: Regions with water stress, including the Middle East, California, and Australia, mandate the use of synthetic turf for public spaces.

- Growth of Commercial Landscaping: Airport and hospitality sectors adopted artificial turf across 18 million sqm of new installations globally in 2024, driven by aesthetic appeal and zero-watering requirements.

These drivers reinforce a self-sustaining growth cycle - government mandates drive institutional adoption, which accelerates cost reductions via manufacturing scale, which in turn expands affordability into residential and SME segments.

Market Restraints

- Environmental Concerns: Non-biodegradable turf systems containing PFAS, crumb rubber infill, and synthetic polymers face increasing regulatory scrutiny. The EU's REACH PFAS restrictions, effective 2025, require significant reformulation investment from manufacturers.

- High Initial Installation Costs: Quality artificial turf installation ranges from USD 6–10 per sq. ft, posing a barrier for small clubs and public institutions in lower-income regions with constrained capital budgets.

- Health-Related Concerns: Studies linking crumb rubber infill to elevated heavy metal exposure have prompted precautionary procurement shifts, particularly in school and children's sports facilities across North America and Europe.

Market Opportunities

- Recyclable and Bio-Based Turf Systems: TenCate launched the first chemical recycling program in the U.S. to break down end‑of‑life synthetic turf into raw materials that can be reused in new products, partnering with Cyclyx International and ExxonMobil. The pilot will process about 50 old turf fields, converting the shredded material into high‑quality feedstock using advanced Exxtend chemical recycling technology.

- Emerging Market Expansion: Africa and South Asia collectively represent an incremental USD 420 Million artificial turf opportunity by 2034, driven by FIFA's Goal program and increasing cricket and football infrastructure development.

- Smart Turf Technology: Embedded IoT sensors in turf systems for temperature monitoring, usage analytics, and maintenance alerts represent a nascent USD 85 Million segment, expected to grow at 18% CAGR through 2034.

Market Challenges

- Disposal and Recycling Infrastructure: According to solid waste industry analysts, discarded artificial turf is projected to generate between 1 million and 4 million tons of waste over the next decade, with no clear disposal solution. This is drawing negative ESG attention from institutional buyers.

- Regulatory Complexity: Diverging standards across the EU, USA (ASTM), and FIFA create compliance cost burdens for manufacturers supplying across multiple geographies, increasing per-product certification costs by up to 22%.

Emerging Market Trends

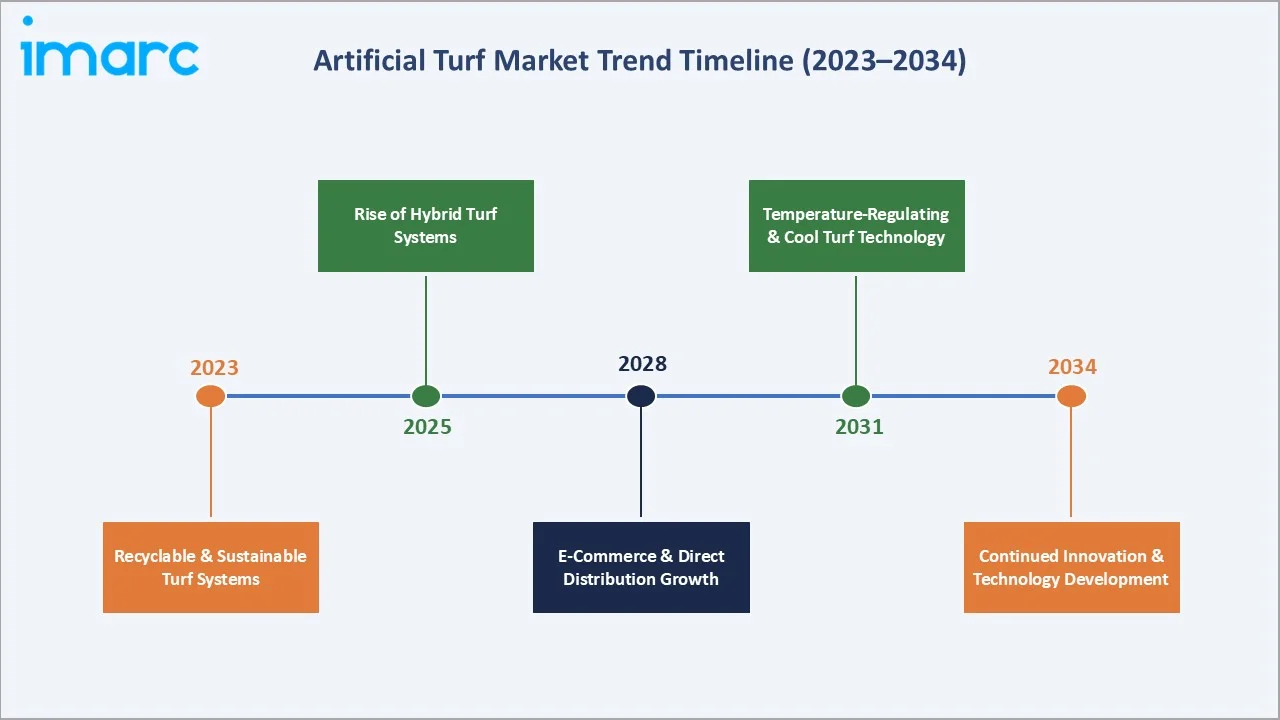

1. Adoption of Recyclable and Sustainable Turf Systems

The market is transitioning toward fully recyclable turf products. In 2023, Shaw Industries partnered with Encina Development Group to recycle over 2 million pounds of waste carpet annually. This trend is accelerating as ESG-aligned procurement policies become standard in European municipalities and FIFA-affiliated stadiums from 2025.

2. Rise of Hybrid Turf Systems

Hybrid surfaces combining natural grass root zones with synthetic fibers gained traction and are now adopted in over 40 elite football stadiums globally. These systems reduce injury risk by 18% compared to pure artificial surfaces while providing year-round durability. Market penetration is estimated to grow from 3.2% in 2025 to 9.8% by 2034.

3. E-Commerce and Direct Distribution Growth

Online and direct-to-consumer turf sales channels grew from 11.3% of total distribution in 2020 to 18.3% in 2025. Platforms offering virtual turf visualization tools, free samples, and self-installation guides are disrupting traditional specialty store channels, particularly in the household segment.

4. Temperature-Regulating and Cool Turf Technology

Surface temperatures on conventional artificial turf can exceed 70°C in direct sunlight. New cool turf technologies using phase-change material infills reduce surface temperatures by up to 20°C. Adoption increased 34% in 2024 across school and public playground installations in hot-climate markets including GCC states and Australia.

Industry Value Chain Analysis

The artificial turf value chain spans raw material extraction through end-consumer installation, with each stage populated by specialized operators whose performance directly influences product quality, sustainability credentials, and installed cost.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Dow Chemical, LyondellBasell (polyethylene/polypropylene resins) |

|

Yarn & Fibre Manufacturing |

TenCate (Thiolon), Shaw Industries (yarn extrusion) |

|

Turf Manufacturing |

CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), Polytan GmbH, Act Global |

|

Distribution |

Specialty Stores, B2B Direct, Online Platforms |

|

Installation & Maintenance |

SIS Pitches, TenCate's Hellas Construction |

|

End Users |

Sports clubs, municipalities, airports, hotels, households |

Technology Landscape in the Artificial Turf Industry

Advanced Fiber Engineering

Polytex Sportbeläge Produktions GmbH owns a patent for a method and material for making artificial turf fibers partially from polymers derived from renewable carbon sources (e.g., bio‑based polyethylene), aiming to produce more sustainable synthetic turf.

Organic and Alternative Infill Materials

Cork, coconut husk, thermoplastic elastomers, and bio-based wax infills are replacing crumb rubber in regulatory-sensitive markets. Organic infill adoption grew 28% in 2024 in school and residential segments, with cost premiums declining from 35% to 18% over 2020–2024 as production scales.

Smart Turf Integration

IoT-embedded pitch management systems providing real-time data on surface compaction, drainage, and temperature are gaining traction. Smart turf systems were deployed across 1,200 professional facilities globally in 2024, with payback periods of 3–4 years via optimized maintenance scheduling.

Recycling Technology

Advanced separation technologies now achieve 95%+ purity in recovering polypropylene backing, polyethylene fibers, and silica sand from decommissioned fields. Recycling capacity is expected to process 85% of European turf waste by 2030, driven by EU extended producer responsibility (EPR) regulations coming into force in 2026.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Material | Polyethylene | 52.4% | 2025 |

| Application | Sports and Leisure | 38.4% | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | Europe | 34.6% | 2025 |

By Material

Polyethylene dominates the material segment with a 52.4% share in 2025 (equivalent to approximately USD 2,062.1 Million). Its dominance reflects superior softness, UV stability, and compatibility with FIFA and World Rugby performance standards.

To access detailed market analysis, Request Sample

Polypropylene holds 24.6% of the market (approx. USD 968.1 Million in 2025), primarily used in cost-sensitive landscaping, residential, and commercial applications where moderate performance suffices. Polyamides account for 14.8% and are favored for high-traffic areas due to exceptional tensile strength, while Others (8.2%) include blended and bio-based materials gaining share in premium eco-segments.

By Application

Sports and leisure leads application demand at 38.4% in 2025 (approx. USD 1,511.2 Million), driven by football, hockey, tennis, and multipurpose pitch installations. The segment benefits from strong institutional funding; FIFA Forward 3.0 (2023–2026) offers up to USD 8 million per member association to support football development, with a strong emphasis on infrastructure such as artificial pitch.

Household applications represent 22.6% (USD 889.4 Million), growing as suburban homeowners adopt artificial lawns to reduce water bills and maintenance time. Airports & commercial offices hold 16.3% share; restaurants and hotels follow at 12.4%, with others at 10.3% comprising healthcare facilities, educational campuses, and event venues.

Regional Market Insights

Europe's market leadership (34.6%, 2025) reflects decades of sports facility investment and strong regulatory alignment. Germany alone has over 9,000 artificial turf pitches, and a new third-generation (3G) artificial grass pitch is planned for each of the five districts in West Yorkshire, representing a potential £5.5 million investment in the region’s health, youth programs, and local clubs.

|

Region |

Share (2025) |

Key Growth Drivers |

Regulatory Impact |

Major Companies |

|

Europe |

34.6% |

Sports culture, stadium upgrades, municipal programmes |

EU REACH PFAS restrictions; EPR (2026) |

Polytan GmbH, TenCate |

|

North America |

26.4% |

School athletic facilities, NFL/MLS stadiums, drought policies |

ASTM F1292 safety standards |

Shaw Industries, FieldTurf |

|

Asia Pacific |

22.8% |

Urbanization, China football push, limited arable land |

National sports infrastructure mandates; import duties |

Taishan and All Victory Grass |

|

Middle East & Africa |

9.6% |

Water scarcity, FIFA Forward programme, tourism venues |

GCC green building codes; FIFA compliance |

SIS Pitches, Condor Group |

|

Latin America |

6.6% |

Football federations, Olympic legacy sites, rising GDP |

CONMEBOL certification requirements |

Forest Group, regional installers |

Asia Pacific is the highest-growth region, with China targeting 70,000 artificial football pitches by 2030 under the national football development plan. South Korea and Japan are integrating artificial turf in urban park redevelopment projects.

Competitive Landscape

The global artificial turf market exhibits a moderately fragmented structure. The top five manufacturers, CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), Polytan GmbH, Act Global, collectively hold approximately 38–42% of global market revenue in 2025. Regional specialists and private-label installers account for the balance, particularly in the Asia Pacific and Latin America.

|

Company Name |

Brand Name |

Market Position |

Core Strength |

|

CCGrass |

CCGrass |

Market Leader |

World's largest turf manufacturer; 140+ country distribution |

|

TenCate |

TenCate / Thiolon |

Market Leader |

Premium fibre technology; FIFA-aligned component supplier |

|

Shaw Industries (Berkshire Hathaway) |

Shaw Sports Turf |

Strong Challenger |

North America market leader; vertical integration |

|

Polytan GmbH (a Sport Group subsidiary) |

LigaTurf, Poligras and Rekortan |

Strong Challenger |

European sports turf; eco-product leadership |

|

Act Global |

Xtreme Turf / ACTurf / UBU |

Challenger |

FIFA, World Rugby, FIH (Fédération Internationale de Hockey) products |

|

Sport Group |

AstroTurf |

Challenger |

Iconic AstroTurf brand; track and field expertise |

|

SIS Pitches |

SIS Pitches |

Niche Player |

Hybrid turf specialist; elite stadium contracts |

Key Company Profiles

CCGrass

CCGrass, headquartered in Nanjing, China, is the world's largest artificial turf manufacturer by production capacity, operating across 5 factory locations. The company supplies to 140+ countries with FIFA Quality Pro and World Rugby Preferred Turf Producer certifications.

- Product Portfolio: Full-spectrum synthetic grass for football, hockey, tennis, landscape, and padel court applications.

- Recent Developments: Expanded European distribution network with 12 new regional warehouses.

- Strategic Focus: Vertical integration expansion; investment in recyclable yarn technology; FIFA partnership extension through 2028.

TenCate

TenCate is a Netherlands-based premium fiber and turf manufacturer, a pioneer of the Thiolon brand. With operations across Europe, the Americas, and the Middle East, the company is recognized for innovation in monofilament fiber technology and sustainable turf systems.

- Product Portfolio: Thiolon Elite performance fibers and XQ technology turf for elite sports.

- Recent Developments: Launched bio-based TenCate Grass Bio yarn in 2024.

- Strategic Focus: Sustainability leadership through recycled content expansion; premium differentiation in elite sports category.

Shaw Industries Group Inc. (Berkshire Hathaway)

Shaw Industries, a Berkshire Hathaway subsidiary headquartered in Dalton, Georgia, is North America's leading artificial turf manufacturer.

- Product Portfolio: Shaw Sports Turf for athletics

- Recent Developments: Recycling partnership with Encina Development Group (2023) to process 2M+ pounds of carpet waste annually.

- Strategic Focus: Sustainability via circular economy commitments; residential segment growth through big-box retail partnerships.

Polytan GmbH

Polytan, headquartered in Burgheim, Germany, is a leading European synthetic sports surface manufacturer with over 50 years of expertise. The company specializes in FIFA-certified artificial turf for football, athletics tracks, and multi-use surfaces, with a strong focus on eco-certifications.

- Product Portfolio: LigaTurf, Poligras, and Rekortan.

- Recent Developments: Achieved Cradle-to-Cradle Silver certification for its LigaTurf RS+ product line in 2024; Polytan supplied the Paris 2024 Olympic hockey turf (Poligras Paris GT zero).

- Strategic Focus: ESG-aligned product development; European market share consolidation; Middle East hospitality segment expansion.

Market Concentration Analysis

The artificial turf market exhibits moderate concentration at the manufacturing level, with the top five global suppliers holding approximately 38–42% of total revenue in 2025. However, a long tail of 800+ regional manufacturers and installation specialists - particularly in China, India, and Latin America - ensures substantial market fragmentation below the top tier.

Consolidation activity is accelerating, driven by sustainability compliance costs and FIFA/World Rugby certification requirements that create barriers to entry for smaller operators. Between 2020 and 2024, seven significant M&A transactions reshaped the competitive map, including Sport Group's integration of AstroTurf. Private equity interest remains elevated, targeting mid-tier manufacturers with certified product portfolios and regional distribution networks.

Investment & Growth Opportunities

Fastest Growing Segments

Recyclable and bio-based turf systems (estimated CAGR 9.2%), smart turf technology (18% CAGR), and hybrid natural-synthetic turf (12% CAGR) represent the three highest-growth investment vectors through 2034. Together, these niches address a total addressable market of approximately USD 480 million by 2030.

Emerging Market Expansion

Sub-Saharan Africa and South Asia collectively represent an incremental USD 420 million opportunity by 2034. Entry via joint ventures with local sports infrastructure developers, alignment with FIFA Forward and AFC Vision program, and government-backed stadium development schemes are the preferred investment modalities.

Venture and Institutional Investment Trends

- Key investment themes include PFAS-free infill technology, robotic turf installation equipment, and satellite-based turf condition monitoring systems.

- Family offices and PE firms are increasingly targeting vertical integration plays - consolidating fibre production, manufacturing, distribution, and installation into single platform companies.

Future Market Outlook (2026-2034)

The global artificial turf market is positioned for sustained, broad-based growth through 2034. From a base of USD 3,935.32 Million in 2025, the market is projected to reach USD 6,022.46 Million by 2034, representing total incremental value creation of USD 2,087.2 Million over the forecast decade.

Regulatory evolution - particularly the EU's PFAS restrictions, FIFA's updated Quality Program 2026, and North American state-level mandates on infill safety- will drive significant product reformulation investment. Manufacturers that achieve certification-ready, eco-compliant product portfolios by 2026 are positioned to capture a disproportionate share of institutional procurement budgets.

Long-term, the market's trajectory is tied to three structural macro-themes: urbanization (creating space-constrained markets where synthetic surfaces are the only viable option), climate change (driving water conservation mandates), and rising global sports participation. Artificial turf sits at the intersection of all three.

Research Methodology

Primary Research

Primary research for this report comprised structured interviews and surveys with over 150 industry participants in 2024–2025, including artificial turf manufacturers, installation contractors, sports facility managers, procurement officers, and end consumers across Europe, North America, and Asia Pacific.

Secondary Research

Secondary research encompassed a systematic review of company annual reports, regulatory filings, FIFA and World Rugby technical documentation, industry databases (Euromonitor, IBISWorld), trade publications (SportsTurf Magazine, Synthetic Turf Council), and publicly available financial data. Over 280 secondary sources were reviewed and triangulated.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting approaches, incorporating macroeconomic indicators, urbanization rates, sports participation indices, and historical market evolution. A base-case CAGR of 4.70% reflects consensus analyst estimates validated against reported manufacturer revenue growth rates.

Artificial Turf Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Materials Covered | Polyethylene, Polypropylene, Polyamides, Others |

| Applications Covered | Household, Sports and Leisure, Restaurant and Hotels, Airports and Commercial Offices, Others |

| Distribution Channels Covered | Direct Sales/B2B, Online Stores, Specialty Stores, Convenience Stores, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), Polytan GmbH (a Sport Group subsidiary), Act Global, Sport Group, SIS Pitches, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the artificial turf market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global artificial turf market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the artificial turf industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Artificial Turf Market Report

The global artificial turf market reached USD 3,935.32 Million in 2025. It is projected to reach USD 6,022.46 Million by 2034.

The artificial turf market is expected to grow at a CAGR of 4.70% during the forecast period from 2026 to 2034, supported by consistent demand from sports, landscaping, and commercial sectors.

Europe leads the market with a 34.6% revenue share in 2025, driven by an established sports culture, high levels of football club infrastructure investment, and government-backed facility upgrade programs in Germany, the UK, and France.

Polyethylene dominates the material segment with a 52.4% share in 2025, valued at approximately USD 2,062.1 Million. Its dominance is driven by superior softness, UV resistance, and compliance with FIFA and World Rugby performance standards.

The sports and leisure segment holds the largest application share at 38.4% in 2025 (approx. USD 1,511.2 Million), driven by rising global sports participation and institutional investment in all-weather playing surfaces.

Key players include CCGrass, TenCate, Shaw Industries (Berkshire Hathaway), Polytan GmbH (a Sport Group subsidiary), Act Global, Sport Group, and SIS Pitches.

Online platforms are increasingly used for artificial turf purchasing, particularly for residential and small-scale commercial projects. E-commerce sales represent a major share, driven by convenience and product variety available to customers.

Key challenges include environmental concerns regarding turf disposal, the high initial installation cost, limited recycling solutions for turf materials, and increasing regulations on microplastics in artificial turf.

Expansion into developing regions such as the Middle East, Asia-Pacific, and Latin America presents significant growth potential, with the market projected to exceed USD 8 billion by 2030s.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)