Asia Pacific Aluminum Extrusion Market Size, Share, Trends and Forecast by Product Type, Alloy Type, End Use Industry, and Country, 2026-2034

Asia Pacific Aluminum Extrusion Market Summary:

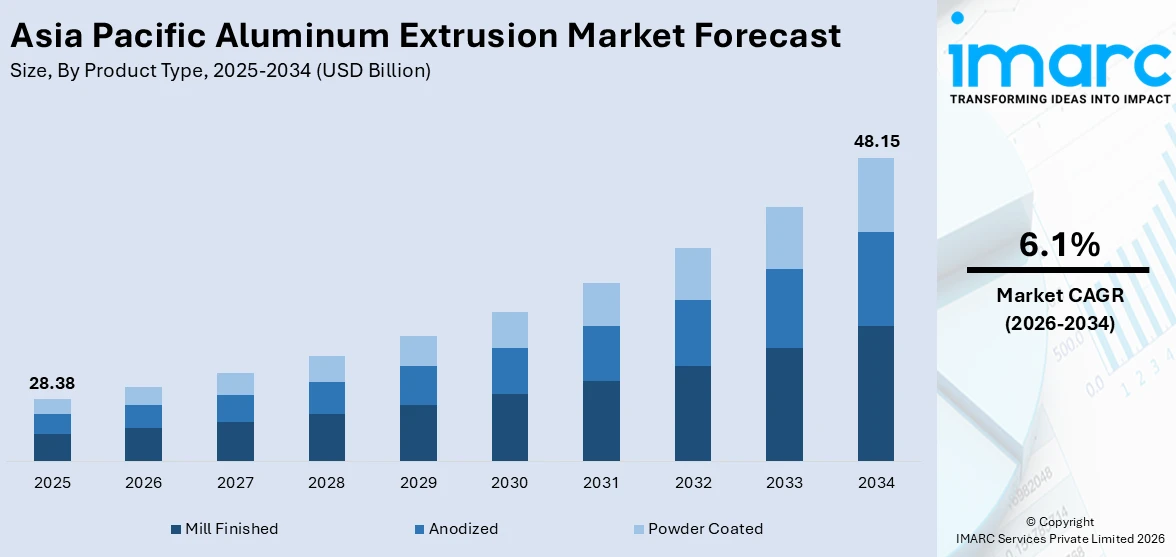

The Asia Pacific aluminum extrusion market size was valued at USD 28.38 Billion in 2025 and is projected to reach USD 48.15 Billion by 2034, growing at a compound annual growth rate of 6.1% from 2026-2034.

The Asia Pacific aluminum extrusion market is witnessing robust expansion driven by rapid urbanization, large-scale infrastructure development, and the rising adoption of lightweight materials across key industries. Surging construction activity in emerging economies, growing automotive production focused on fuel efficiency, and increasing demand from the electrical and electronics sectors are accelerating consumption. Additionally, supportive government policies promoting green building standards and sustainable manufacturing practices are reinforcing regional demand, strengthening the Asia Pacific aluminum extrusion market share.

Key Takeaways and Insights:

- By Product Type: Mill finished dominates the market with a share of 45% in 2025, owing to its versatility, cost-effectiveness, and ease of customization across diverse industrial applications including construction, automotive, and electrical engineering.

- By Alloy Type: 6000 series aluminum alloy leads the market with a share of 30% in 2025, driven by its superior combination of strength, corrosion resistance, machinability, and weldability making it ideal for structural and architectural applications.

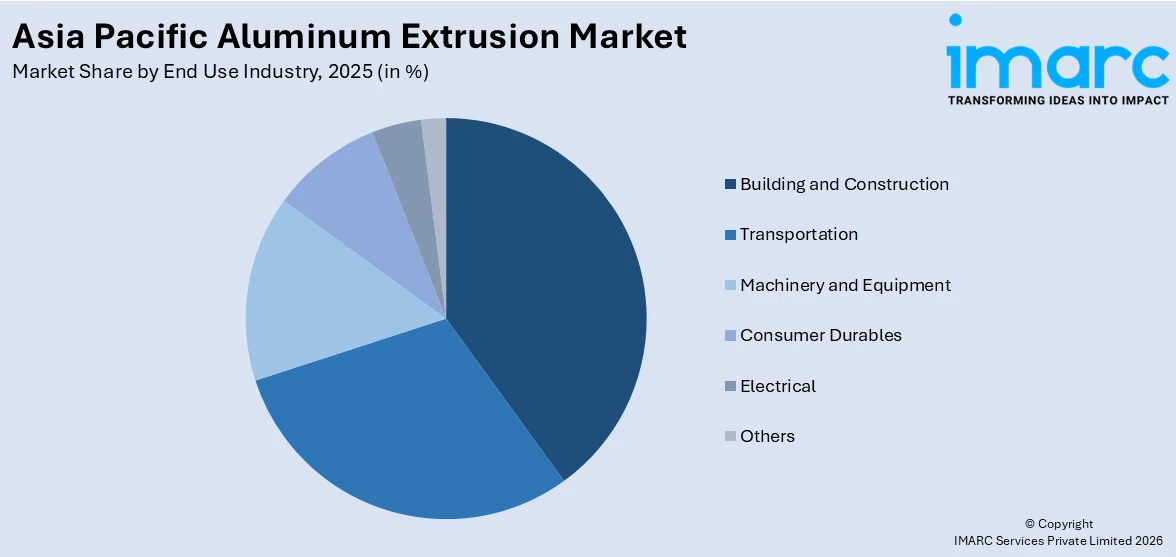

- By End Use Industry: Building and construction represent the largest segment with a market share of 38% in 2025, reflecting the extensive utilization of aluminum extrusions in window frames, curtain walls, roofing systems, and structural frameworks across the region’s expanding urban landscape.

- Key Players: Key players drive the Asia Pacific aluminum extrusion market by expanding production capacities, investing in advanced extrusion technologies, strengthening value-added product portfolios, and forming strategic partnerships to enhance distribution networks and capture growing demand across construction, automotive, and renewable energy sectors.

To get more information on this market Request Sample

The Asia Pacific aluminum extrusion market is advancing as the region continues to experience rapid industrialization, urban transformation, and infrastructural modernization across major economies. Governments are deploying substantial capital toward transportation networks, smart city projects, and renewable energy installations, all of which require high-performance aluminum extrusion products. The automotive sector is increasingly incorporating extruded aluminum components into vehicle chassis, battery enclosures, and structural frames to achieve weight reduction targets and comply with tightening emission standards. Furthermore, expanding applications in solar panel framing, electronic enclosures, and consumer durables are broadening the consumption base. The region’s abundant raw material availability, competitive manufacturing costs, and skilled labor pool continue to attract investment, positioning Asia Pacific as the epicenter of global aluminum extrusion production and consumption.

Asia Pacific Aluminum Extrusion Market Trends:

Rising Adoption of Aluminum Extrusions in Electric Vehicle Manufacturing

The Asia Pacific electric vehicle sector is driving substantial demand for aluminum extrusions, as automakers seek lightweight yet structurally robust materials for battery enclosures, chassis components, and crash management systems. The shift toward electrification necessitates significant weight reduction to maximize driving range and battery efficiency. In August 2024, Hindalco Industries commissioned its new 34,000 TPA extrusion plant in Silvassa, India, specifically designed to cater to the growing electric vehicle sector, underscoring the accelerating integration of aluminum extrusions in next-generation mobility platforms across the region.

Expansion of Green Building Standards Driving Architectural Aluminum Demand

Green building mandates across Asia Pacific are fueling demand for sustainable, recyclable construction materials, with aluminum extrusions emerging as a preferred choice for energy-efficient facades, window systems, and structural applications. The material's corrosion resistance, thermal performance, and recyclability align with evolving sustainability certifications and building codes. Governments across the region are strengthening green building frameworks and environmental compliance standards, encouraging developers and architects to incorporate recyclable, energy-efficient materials into new construction projects, directly stimulating demand for architectural aluminum extrusion products throughout the region.

Integration of Smart Manufacturing and Automation in Extrusion Production

Aluminum extrusion manufacturers across Asia Pacific are embracing Industry 4.0 technologies, including robotic handling systems, predictive maintenance, and precision extrusion control to enhance production efficiency and product quality. The adoption of real-time monitoring, data analytics, and automated quality inspection is reducing operational costs while enabling complex profile designs for specialized applications. Leading producers across the region are investing heavily in automation upgrades, energy-efficient production processes, and advanced extrusion press technologies to improve throughput, reduce waste, and meet the rising demand for high-precision aluminum profiles across construction, automotive, and electronics sectors.

Market Outlook 2026-2034:

The Asia Pacific aluminum extrusion market is poised for sustained expansion throughout the forecast period, underpinned by accelerating infrastructure investments, rising automotive lightweighting requirements, and growing renewable energy installations across the region. Governments in China, India, Japan, and Southeast Asian nations are channeling substantial capital toward urban development projects, high-speed rail networks, and smart city initiatives that rely extensively on aluminum extrusion products for structural and functional components. The transition toward electric vehicles is creating additional demand for specialized extrusion profiles used in battery housings and vehicle frames. Furthermore, advancements in alloy development, surface treatment technologies, and sustainable manufacturing practices are enabling producers to offer higher-value products that cater to increasingly demanding end-use specifications, reinforcing the market’s positive growth trajectory. The market generated a revenue of USD 28.38 Billion in 2025 and is projected to reach a revenue of USD 48.15 Billion by 2034, growing at a compound annual growth rate of 6.1% from 2026-2034.

Asia Pacific Aluminum Extrusion Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Mill Finished |

45% |

|

Alloy Type |

6000 Series Aluminum Alloy |

30% |

|

End Use Industry |

Building and Construction |

38% |

Product Type Insights:

- Mill Finished

- Anodized

- Powder Coated

Mill finished dominates with a market share of 45% of the total Asia Pacific aluminum extrusion market in 2025.

Mill finished aluminum extrusions represent the foundational product category within the Asia Pacific market, valued for their natural surface quality and versatility across multiple end-use applications. These extrusions emerge directly from the extrusion press without additional coating or surface treatment, offering manufacturers the flexibility to apply custom finishes or utilize the profiles in their raw state. The product type’s dominance is reinforced by its cost-effectiveness and suitability for applications where subsequent fabrication or finishing is required.

The widespread preference for mill finished extrusions stems from their adaptability to diverse manufacturing requirements and compatibility with various downstream processing techniques including anodizing, powder coating, and painting. Builders, fabricators, and original equipment manufacturers across the Asia Pacific region frequently select mill finished profiles as base materials for window frames, structural components, heat sinks, and industrial machinery parts. The growing construction activity across developing Asian economies, particularly in residential and commercial building segments, continues to generate substantial demand for these cost-efficient extrusion products, further consolidating their dominant market position throughout the region.

Alloy Type Insights:

- 1000 Series Aluminum Alloy

- 2000 Series Aluminum Alloy

- 3000 Series Aluminum Alloy

- 5000 Series Aluminum Alloy

- 6000 Series Aluminum Alloy

- 7000 Series Aluminum Alloy

6000 series aluminum alloy leads with a share of 30% of the total Asia Pacific aluminum extrusion market in 2025.

The 6000 series aluminum alloy maintains its leading position within the Asia Pacific aluminum extrusion market, driven by its exceptional combination of mechanical properties that make it indispensable across construction, automotive, and electrical applications. Comprising aluminum with magnesium and silicon as primary alloying elements, this series delivers excellent corrosion resistance, high strength-to-weight ratio, superior machinability, and outstanding weldability characteristics. These properties make 6000 series alloys particularly suitable for structural profiles, architectural frameworks, and automotive components requiring both durability and precision.

The continued dominance of 6000 series alloys reflects their alignment with the Asia Pacific region’s industrial requirements, where versatility and performance consistency are paramount. These alloys are extensively utilized in the production of window frames, curtain wall systems, door profiles, and roofing components for the construction sector, while simultaneously serving automotive manufacturers producing lightweight chassis and body structural elements. The alloy’s heat-treatability enables manufacturers to achieve specific temper conditions tailored to diverse application requirements. The expanding electric vehicle manufacturing sector further amplifies demand, as 6000 series extrusions are increasingly specified for battery enclosure frames and vehicle structural reinforcements that require precise dimensional accuracy.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Building and Construction

- Transportation

- Machinery and Equipment

- Consumer Durables

- Electrical

- Others

The building and construction exhibit a clear dominance with a 38% share of the total Asia Pacific aluminum extrusion market in 2025.

Building and construction remains the primary consumption sector for aluminum extrusions in the Asia Pacific region, driven by massive urbanization programs, infrastructure modernization initiatives, and the increasing adoption of sustainable building materials across developing and developed economies. Aluminum extrusions serve critical functions in architectural applications including window frames, curtain walls, structural glazing systems, roofing panels, and facade elements, offering superior durability, aesthetic versatility, and environmental sustainability. The region’s construction sector benefits from substantial government investment in smart city development, affordable housing projects, and commercial infrastructure expansion.

The sector’s dominance is further reinforced by the growing emphasis on green building certifications and energy-efficient construction standards across Asia Pacific nations. Aluminum extrusions contribute to achieving sustainability benchmarks through their inherent recyclability, lightweight characteristics, and ability to enhance building thermal performance when used in high-performance fenestration systems. The material’s resistance to corrosion makes it particularly suitable for the region’s diverse climatic conditions, from tropical Southeast Asian environments to temperate zones in Japan and South Korea. The expanding commercial real estate sector, coupled with ongoing development of transportation hubs, educational institutions, and healthcare facilities, continues to generate sustained demand for construction-grade aluminum extrusion profiles across the region.

Country Insights:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

China is the major market leader in the Asia Pacific market for aluminum extrusions. China controls the majority of market activity in the Asia Pacific market for aluminum extrusions. The country has major manufacturing bases, construction activities, and investments by the government in transportation and energy infrastructure.

The aluminum extrusions market of Japan is a high-value, technology-driven market with substantial demand from segments such as the automobile, aerospace, and electronic device industries. The Japanese automobile industry leads the world in the adoption of aluminum extrusions as a metal material for constructing light-weight automobiles, parts of hydrogen-based fuel cells, and structural components conducive to increased automotive mobility and environmental regulations to reduce emissions.

India's aluminum extrusion market is experiencing accelerated growth, propelled by robust infrastructure development, rapid urbanization, and expanding automotive manufacturing. The country's leading aluminum producers are actively investing in capacity expansion, establishing new extrusion facilities, and upgrading existing production lines to cater to strengthening demand across construction, electric vehicles, and electronics, positioning India as one of the fastest-growing aluminum extrusion markets in the region.

South Korea's advanced car manufacturing and electronics-manufacturing ecosystems escalate the demand for extruded aluminum products. Automakers here have increasingly begun incorporating aluminum extrusions into the platforms of their electric vehicles to cover batteries, structural frames, and thermal management components, while the consumer electronics industry uses precision-extruded profiles for heat dissipation and device housings.

As far as Australian markets are concerned, the manufacturers of aluminum extrusions benefit from strong and sustained investment in residential and commercial building construction, mining infrastructure, and the installation of renewable energy. Specific growth drivers include the country's emphasis on sustainable building practices and energy-efficient construction standards, thereby ensuring consistent demand for architectural aluminum extrusion products-particularly for solar panel framing and modular construction applications.

The aluminum extrusion market is shaping up in Indonesia, on the back of expanding industrialization and growing construction activities, supplemented by governmental infrastructure development programs. The position of the country as a substantial bauxite producer, with rising domestic consumption for construction materials and consumer goods, is presenting favorable conditions for both production capacity expansion and increasing intake for the products of aluminum extrusion.

Market Dynamics:

Growth Drivers:

Why is the Asia Pacific Aluminum Extrusion Market Growing?

Accelerating Urbanization and Large-Scale Infrastructure Development

The Asia Pacific region is experiencing unprecedented urbanization, with hundreds of millions of people transitioning to urban centers across China, India, Indonesia, and Southeast Asian nations. This demographic shift is generating immense demand for residential housing, commercial complexes, transportation networks, and public infrastructure that extensively utilize aluminum extrusions for structural and architectural components. Governments across the region are deploying substantial capital toward smart city initiatives, metro rail expansions, airport modernization, and highway development projects. The construction of energy-efficient buildings incorporating aluminum curtain walls, window systems, and structural frameworks is intensifying as sustainability mandates gain traction. The convergence of population growth, economic development, and infrastructure modernization creates sustained, long-term demand that underpins market expansion across the region.

Growing Automotive Lightweighting Requirements and Electric Vehicle Adoption

The automotive industry across Asia Pacific is increasingly adopting aluminum extrusions as a strategic material for achieving vehicle weight reduction targets and complying with progressively stringent emission regulations. Extruded aluminum components are being integrated into vehicle chassis, body structures, crash management systems, and battery housings, offering superior strength-to-weight ratios compared to traditional steel alternatives. The rapid expansion of electric vehicle manufacturing is amplifying this trend, as reduced vehicle weight directly translates to extended driving range and improved battery efficiency. Japan and South Korea’s established automotive manufacturers are developing advanced aluminum structural platforms, while China’s dominant EV production ecosystem is creating massive demand for specialized extrusion profiles tailored to next-generation electric mobility applications.

Expanding Renewable Energy Infrastructure and Solar Panel Installations

The renewable energy sector across Asia Pacific is emerging as a significant growth driver for aluminum extrusions, particularly through the rapid expansion of solar photovoltaic installations that require durable, corrosion-resistant framing systems. Aluminum extrusion profiles are the preferred material for solar panel mounting structures, racking systems, and module frames due to their lightweight nature, weather resistance, and compatibility with outdoor environmental conditions. Governments across the region are setting ambitious renewable energy targets, stimulating massive investment in solar farm construction and distributed rooftop installations. Press Metal Aluminium Holdings in Malaysia has specifically commissioned its Nilai extrusion plant to cater to the photovoltaic industry, supplying aluminum frames and structural components for solar energy applications, representing the world’s largest solar infrastructure and creating enormous, sustained demand for aluminum extrusion products dedicated to renewable energy applications across the region.

Market Restraints:

What Challenges the Asia Pacific Aluminum Extrusion Market is Facing?

Volatility in Raw Material Prices and Supply Chain Disruptions

The aluminum extrusion industry faces persistent challenges from fluctuating aluminum commodity prices, which are influenced by global economic conditions, geopolitical tensions, trade policies, and energy cost variations. Price volatility directly impacts production costs and profit margins for extrusion manufacturers, creating planning uncertainties and affecting pricing competitiveness. Supply chain disruptions, including fluctuations in bauxite and alumina availability, transportation bottlenecks, and trade restrictions between producing and consuming nations, further compound these challenges, making stable production planning difficult for manufacturers across the region.

Intense Competition from Alternative Materials and Unorganized Sector

Aluminum extrusion manufacturers face competitive pressure from alternative materials including steel, plastics, and composite materials that can substitute aluminum in certain applications. Additionally, the presence of numerous unorganized and small-scale producers, particularly in markets like India and Southeast Asia, creates a highly fragmented competitive environment that exerts downward pressure on pricing and margins. This fragmentation makes it challenging for organized manufacturers to maintain pricing power and market positioning, especially in price-sensitive construction and consumer goods segments.

Environmental Regulations and Energy-Intensive Production Requirements

The aluminum extrusion manufacturing process is inherently energy-intensive, requiring substantial electricity consumption for smelting, billet casting, and extrusion operations. Increasingly stringent environmental regulations across Asia Pacific nations are imposing higher compliance costs on manufacturers through emission reduction mandates, waste management requirements, and energy efficiency standards. These regulatory pressures necessitate significant capital investment in cleaner production technologies, recycling infrastructure, and renewable energy integration, raising operational costs and creating barriers for smaller manufacturers seeking to maintain competitiveness in the evolving regulatory landscape.

Competitive Landscape:

The Asia Pacific aluminum extrusion market has a competitive industry, where large integrated manufacturers along with local industry players are currently operating. The leading industry players of the region are focusing on enhancing their production capabilities, technology, and product range, thereby strengthening their presence. Investment strategies in value-added products, such as precision-engineered products for automotive, aerospace, and electronics segments, are considered significant industry differentiators. Industry players are also focusing on sustainable business strategies, such as low-carbon production, recycle usage, and energy-efficient production, while developing key partnerships for enhancing their presence.

Recent Developments:

- In August 2025, Hindalco Industries received government approval under the Electronics Component Manufacturing Scheme for setting up an aluminum extrusion facility for mobile phone enclosures. The company also secured clearance from Apple to supply aluminum extrusions for iPhone enclosures, with an investment of INR 586 Crore, strengthening its value-added aluminum portfolio for electronics applications.

- In September 2024, Press Metal Aluminium Holdings announced an 80% equity participation in PT Kalimantan Alumina Nusantara in Indonesia, a new alumina refinery expected to be completed by 2027, securing upstream raw material supply for its integrated aluminum extrusion and smelting operations across Southeast Asia.

Asia Pacific Aluminum Extrusion Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Segment Coverage |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Mill Finished, Anodized, Powder Coated |

| Alloy Types Covered | 1000 Series Aluminum Alloy, 2000 Series Aluminum Alloy, 3000 Series Aluminum Alloy, 5000 Series Aluminum Alloy, 6000 Series Aluminum Alloy, 7000 Series Aluminum Alloy |

| End Use Industries Covered | Building and Construction, Transportation, Machinery and Equipment, Consumer Durables, Electrical, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Asia Pacific Aluminum Extrusion Market Report

The Asia Pacific aluminum extrusion market size was valued at USD 28.38 Billion in 2025.

The Asia Pacific aluminum extrusion market is expected to grow at a compound annual growth rate of 6.1% from 2026-2034 to reach USD 48.15 Billion by 2034.

Mill finished dominated the market with a share of 45%, owing to its versatility, cost-effectiveness, and ease of customization across diverse industrial applications including construction, automotive, and electrical engineering sectors.

Key factors driving the Asia Pacific aluminum extrusion market include accelerating urbanization and infrastructure development, growing automotive lightweighting requirements driven by electric vehicle adoption, expanding renewable energy installations, and supportive government policies promoting sustainable construction.

Major challenges include volatility in raw material prices and supply chain disruptions, intense competition from alternative materials and unorganized sector producers, energy-intensive production requirements facing stricter environmental regulations, and fluctuating trade policies affecting cross-border material flows.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)