Asia Pacific Chitosan Market Size, Share, Trends and Forecast by Grade, Source, Application, and Country, 2026-2034

Asia Pacific Chitosan Market Summary:

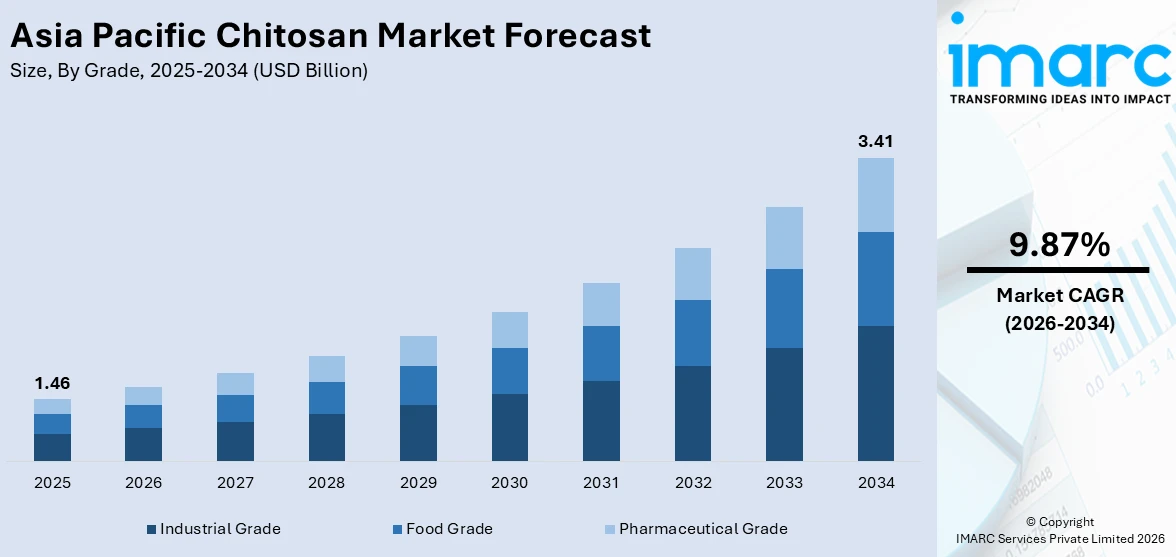

The Asia Pacific chitosan market size was valued at USD 1.46 Billion in 2025 and is projected to reach USD 3.41 Billion by 2034, growing at a compound annual growth rate of 9.87% from 2026-2034.

The Asia Pacific chitosan market is experiencing robust expansion, driven by surging demand across water treatment, agriculture, pharmaceuticals, and food processing sectors. Rapid industrialization, growing environmental awareness, and tightening effluent regulations are compelling industries to adopt bio-based solutions. Expanding aquaculture activities provide abundant raw material supply, while government support for sustainable alternatives further accelerates growth. These combined dynamics are broadening the Asia Pacific chitosan market share across diverse end-use sectors throughout the region.

Key Takeaways and Insights:

- By Grade: Industrial grade dominates the market with a share of 52% in 2025, owing to its versatile applicability in water treatment, agriculture, and industrial processing, where high-volume consumption drives sustained demand across the region.

- By Source: Shrimp leads the market with a share of 40% in 2025, supported by the region's extensive shrimp aquaculture industry, which generates abundant shell waste as a low-cost, readily available feedstock for chitosan extraction.

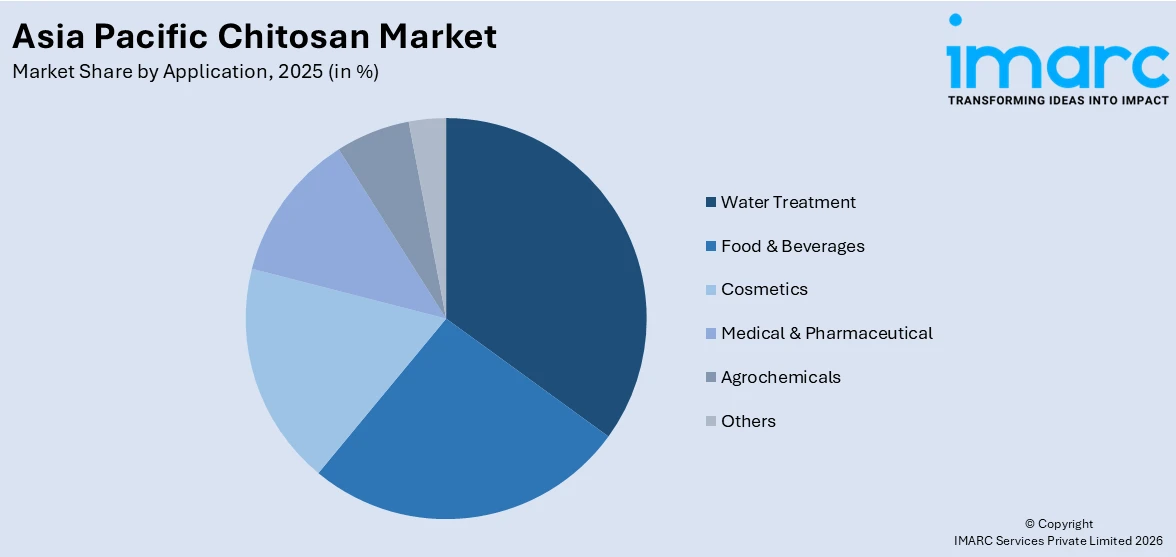

- By Application: Water treatment represents the largest segment with a market share of 31% in 2025, reflecting escalating demand for effective, eco-friendly coagulants and flocculants to address mounting industrial effluent and municipal wastewater management challenges.

- Key Players: Key players in the Asia Pacific chitosan market are expanding production capacities, investing in purity enhancement technologies, and forging strategic partnerships with end-use industries. Their focus on regulatory compliance, application diversification, and competitive pricing is strengthening market penetration and accelerating chitosan adoption across pharmaceutical, agricultural, and environmental sectors.

To get more information on this market Request Sample

The Asia Pacific chitosan market is gaining significant momentum as industries across the region pivot toward sustainable, bio-derived materials. Chitosan, derived primarily from crustacean shell waste, is emerging as a critical input across a broad spectrum of applications, ranging from municipal and industrial water purification to precision agriculture, active pharmaceutical formulations, and functional food ingredients. Regulatory frameworks mandating reduced chemical usage in food production and water treatment are further catalyzing adoption. Pharmaceutical applications are gaining traction due to chitosan's biocompatibility, mucoadhesive properties, and drug delivery potential. Meanwhile, agricultural adoption is accelerating as farmers seek bio-stimulant alternatives to synthetic agrochemicals. These structural drivers, combined with growing research investment and expanding processing infrastructure, are positioning Asia Pacific as the global epicenter of chitosan production and consumption.

Asia Pacific Chitosan Market Trends:

Rising Adoption in Agricultural Bio-stimulants

Growing farmer awareness about soil health and sustainable crop nutrition is accelerating the use of chitosan-based bio-stimulants across Asia Pacific. Governments across the region are actively promoting reduced reliance on synthetic fertilizers through national agriculture sustainability programs, creating a supportive regulatory environment for bio-derived crop inputs. Streamlined registration pathways for bio-stimulant products are enabling faster commercial entry of chitosan-based formulations into agricultural markets. This regulatory support, coupled with demonstrable yield improvement outcomes in rice, wheat, and horticultural crops, is broadening chitosan adoption and supporting Asia Pacific chitosan market growth.

Expansion of Pharmaceutical and Nutraceutical Applications

The pharmaceutical sector is increasingly leveraging chitosan's biocompatibility, biodegradability, and mucoadhesive properties for advanced drug delivery systems, wound healing films, and encapsulation matrices. Regional research institutions are actively developing novel chitosan derivatives, exploring applications across targeted therapeutics, controlled-release formulations, and tissue engineering scaffolds. This sustained research momentum is stimulating investment across pharmaceutical-grade chitosan production and progressively refining the purity standards required for regulated end-use applications. As clinical interest in chitosan-based therapeutics deepens, manufacturers are prioritizing high-deacetylation, low-endotoxin grades that meet the stringent quality benchmarks demanded by pharmaceutical regulators across Japan, South Korea, and Australia.

Integration into Eco-friendly Packaging Solutions

Surging regulatory and consumer pressure to eliminate single-use plastics is driving demand for chitosan-based biodegradable films and coatings in the food packaging sector. Governments across Asia Pacific are enacting extended producer responsibility frameworks and plastic reduction mandates, incentivizing brands and manufacturers to adopt sustainable packaging alternatives that meet both performance and environmental compliance requirements. Chitosan's natural antimicrobial properties, film-forming capability, and full biodegradability make it a technically viable and commercially attractive biopolymer for food contact applications. As retail chains and food processors seek credible alternatives to synthetic barrier materials, chitosan-cellulose composite formats are gaining traction, reinforcing chitosan's role as a scalable solution within the region's rapidly evolving sustainable packaging landscape.

Market Outlook 2026-2034:

The market for chitosan in the Asia Pacific is expected to show strong and sustained growth prospects over the course of the forecast period, driven by accelerating product uptake in water treatment, pharmaceuticals, agriculture, and food packaging segments. Escalating regulatory requirements for eco-friendly industrial products, aquaculture-related supply chain development, and research investments in chitosan derivatives are all strengthening the market’s growth fundamentals. New markets such as biomedical scaffolds, precision fermentation, and smart coatings for agriculture will also create new demand vectors for the product. Countries such as China, India, and Japan are focusing on developing indigenous bio-material processing industries, further strengthening the market’s production ecosystem. The market generated a revenue of USD 1.46 Billion in 2025 and is projected to reach a revenue of USD 3.41 Billion by 2034, growing at a compound annual growth rate of 9.87% from 2026-2034.

Asia Pacific Chitosan Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Grade |

Industrial Grade |

52% |

|

Source |

Shrimp |

40% |

|

Application |

Water Treatment |

31% |

Grade Insights:

- Industrial Grade

- Food Grade

- Pharmaceutical Grade

Industrial grade dominates with a market share of 52% of the total Asia Pacific chitosan market in 2025.

Industrial grade chitosan commands the largest revenue contribution owing to its broad utility across water treatment, textiles, paper manufacturing, and industrial wastewater management applications. Its comparatively relaxed purity specifications reduce production costs, making it commercially accessible for large-scale industrial operations. The proliferation of manufacturing industries across China, India, Vietnam, and Indonesia has created substantial demand for cost-effective, bio-based flocculants and process additives, reinforcing industrial grade's dominant position within the regional market and driving consistent volume uptake from diverse end-use segments.

The accessibility and versatility of industrial grade chitosan make it the preferred choice for environmental applications, particularly in effluent treatment plants managing heavy metal removal and suspended solids reduction. As regulatory frameworks across Southeast Asia tighten permissible discharge standards for industrial effluents, manufacturers are increasingly transitioning from conventional chemical coagulants to chitosan-based alternatives. In 2024, Vietnam's Ministry of Natural Resources and Environment introduced stricter wastewater discharge thresholds for textile dyeing facilities, accelerating the uptake of industrial grade chitosan as a compliant, biodegradable treatment solution.

Source Insights:

- Shrimp

- Crab

- Squid

- Krill

- Others

Shrimp leads with a share of 40% of the total Asia Pacific chitosan market in 2025.

Shrimp shells represent the most abundantly available and cost-efficient feedstock for chitosan extraction across Asia Pacific, owing to the region's position as the world's leading shrimp aquaculture producer. Countries including China, Vietnam, India, Thailand, and Indonesia collectively generate millions of metric tons of shrimp processing waste annually, providing a continuous and scalable raw material base. The well-established collection and processing infrastructure surrounding shrimp processing facilities enables efficient chitin extraction and deacetylation, supporting commercially viable chitosan production at competitive price points.

The widespread availability of shrimp shells also benefits from relatively standardized chitin content and deacetylation characteristics, enabling processors to achieve consistent product quality across industrial and food grade specifications. Integration between shrimp processors and chitosan manufacturers is deepening across Vietnam and India, where by-product valorization policies incentivize zero-waste aquaculture processing. In 2023, the Government of India's Department of Fisheries announced expanded financial support under the Pradhan Mantri Matsya Sampada Yojana for aquaculture waste processing infrastructure, directly benefiting shrimp-sourced chitosan producers.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Water Treatment

- Food & Beverages

- Cosmetics

- Medical & Pharmaceutical

- Agrochemicals

- Others

Water treatment represents the leading segment with a market share of 31% of the total Asia Pacific chitosan market in 2025.

Water treatment holds the dominant application position in the Asia Pacific chitosan market, driven by escalating industrial effluent volumes, deteriorating water quality in rapidly urbanizing economies, and tightening environmental regulations. Chitosan functions as a highly effective natural coagulant and flocculant, efficiently removing heavy metals, dyes, suspended solids, and phosphates from industrial and municipal wastewater streams. Its biodegradability and non-toxic profile offer significant advantages over conventional synthetic coagulants such as aluminum sulfate, making it increasingly favored within environmentally regulated industrial sectors throughout China, India, and Southeast Asia.

Regulatory pressure from environmental protection bodies across the region is driving a structural shift toward bio-based treatment chemicals, as authorities tighten permissible discharge thresholds for textile, leather, and industrial manufacturing facilities. Compliance obligations are compelling procurement teams to transition away from conventional synthetic coagulants toward biodegradable alternatives that satisfy both performance and environmental standards. Municipal water authorities are increasingly evaluating chitosan for drinking water purification, drawn by its ability to reduce microbial contamination without introducing persistent chemical residues into treated water supplies. These dual demand streams, from industrial effluent compliance and municipal water quality improvement, are reinforcing water treatment's position as the leading application segment and sustaining consistent volume uptake of industrial grade chitosan across the region.

Country Insights:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

China represents the largest producer and consumer of chitosan in the region, supported by its vast crustacean processing industry, extensive manufacturing infrastructure, and strong domestic demand from water treatment, agriculture, and pharmaceutical sectors driving sustained market expansion.

Japan maintains a mature chitosan market characterized by high-value pharmaceutical, cosmetic, and functional food applications. Strong regulatory frameworks, advanced processing capabilities, and consumer preference for natural, biocompatible ingredients sustain consistent demand for premium-grade chitosan across specialized industry segments.

India represents a high-growth chitosan market underpinned by its expansive aquaculture base, rapidly expanding agrochemical sector, and increasing investments in water treatment infrastructure. Government programs supporting bio-based agricultural inputs and fisheries by-product valorization are accelerating domestic chitosan production and consumption.

South Korea demonstrates robust chitosan demand driven by its globally recognized cosmetics and personal care industry, alongside an active pharmaceutical research sector. Growing interest in bio-derived functional ingredients and biomedical applications is sustaining premium-grade chitosan consumption across innovation-focused end-use segments.

Australia sustains steady chitosan demand across pharmaceutical, agricultural, and food safety applications. Stringent environmental regulations, strong consumer preference for natural ingredients, and growing adoption of bio-based crop protection products are collectively supporting consistent market development throughout the country.

Indonesia is an emerging chitosan market benefiting from its rapidly expanding shrimp and crab aquaculture industry, which generates abundant feedstock for domestic production. Rising industrial effluent regulations and growing agricultural modernization initiatives are progressively stimulating chitosan adoption across key end-use sectors.

Market Dynamics:

Growth Drivers:

Why is the Asia Pacific Chitosan Market Growing?

Stringent Environmental Regulations Driving Water Treatment Demand

Across Asia Pacific, governments are implementing increasingly rigorous water quality and industrial effluent standards, compelling manufacturing industries, municipalities, and utility operators to adopt effective bio-based treatment alternatives. Chitosan's natural coagulation and heavy metal chelation capabilities position it as a highly effective substitute for conventional synthetic chemicals in water purification applications. Countries including China, India, Vietnam, and Indonesia have progressively strengthened their environmental protection frameworks, with regulations targeting textile, leather, mining, and food processing industries specifically requiring demonstrable reductions in chemical oxygen demand and heavy metal discharge. These mandates are structurally increasing demand for eco-compliant treatment inputs. In China, the Ministry of Ecology and Environment's revised Pollutant Discharge Standards for key industrial sectors introduced tighter effluent quality benchmarks that have accelerated the transition toward bio-based coagulants. India's National Green Tribunal has similarly intensified enforcement of effluent treatment compliance among small and medium industries, broadening the addressable market for industrial grade chitosan. These regulatory catalysts are expected to generate sustained, compliance-driven demand growth throughout the forecast period.

Thriving Aquaculture Sector Ensuring Sustainable Raw Material Supply

Asia Pacific's position as the world's dominant aquaculture producer provides the chitosan industry with a reliable, large-scale, and cost-effective supply of crustacean shell waste as primary feedstock. The region accounts for the overwhelming majority of global shrimp and crab farming and processing output, with China, Vietnam, India, Thailand, and Indonesia collectively operating thousands of commercial processing facilities that generate shell waste streams suitable for chitin extraction. This deeply integrated supply chain reduces raw material acquisition costs and supports competitive pricing for downstream chitosan production. Government-backed aquaculture development programs are further expanding processing capacity. Vietnam's National Aquaculture Development Strategy extended through 2030 targets increased output from value-added seafood processing, directly expanding shell waste availability. In India, the Pradhan Mantri Matsya Sampada Yojana scheme, which allocated INR 20,050 Crore toward fisheries sector development, supports infrastructure for aquaculture by-product processing that strengthens chitosan feedstock availability. The alignment of aquaculture expansion with bio-material demand creates a structural supply advantage unique to the Asia Pacific region.

Growing Adoption Across Agriculture and Food Safety Applications

The accelerating transition toward sustainable agricultural practices and clean-label food production is generating substantial new demand for chitosan across the Asia Pacific region. In agriculture, chitosan functions as a bio-stimulant that enhances plant immunity, promotes root development, and activates natural defense mechanisms, reducing dependence on synthetic pesticides and fertilizers. Government initiatives across India, China, and Southeast Asia promoting integrated pest management and organic certification are creating favorable conditions for chitosan-based crop input adoption. In food processing and packaging, chitosan's antimicrobial and film-forming properties are increasingly leveraged to extend shelf life and reduce reliance on synthetic preservatives. The growing prevalence of food safety regulations and consumer preference for natural ingredients is catalyzing commercial interest. These concurrent demand streams across agriculture and food are expanding chitosan's addressable market beyond its traditional industrial applications.

Market Restraints:

What Challenges the Asia Pacific Chitosan Market is Facing?

High Production and Purification Costs for Specialty Grades

The production of pharmaceutical and food grade chitosan requires multi-stage purification processes involving repeated deacetylation, demineralization, and deproteinization steps, significantly increasing manufacturing costs. This cost intensity restricts the scalability of high-purity chitosan supply, limiting accessibility for smaller manufacturers and creating pricing pressure that challenges market expansion in cost-sensitive segments. The gap between industrial and specialty grade production economics remains a persistent structural constraint that suppresses broader adoption across regulated application sectors, particularly in developing economies where procurement budgets are limited.

Seasonal and Geographic Variability in Feedstock Availability

Despite Asia Pacific's large aquaculture base, chitosan feedstock availability is subject to seasonal fluctuations tied to shrimp and crab harvesting cycles, as well as geographic concentration of processing facilities. This variability creates supply chain inconsistencies that can disrupt production continuity and contribute to price volatility for raw chitin. Producers reliant on spot procurement face challenges in maintaining consistent output quality and volume, particularly during off-harvest periods, complicating contractual supply commitments to industrial and pharmaceutical customers with continuous processing requirements.

Competition from Synthetic and Alternative Natural Coagulants

Despite chitosan's environmental advantages, established synthetic coagulants such as polyaluminum chloride and ferric sulfate continue to dominate water treatment procurement due to their lower unit costs, proven performance documentation, and well-entrenched supply relationships. Additionally, alternative bio-based coagulants derived from plant extracts are emerging as competing options. This competitive landscape limits chitosan's rate of substitution in water treatment and industrial processing applications, particularly in markets where buyer decision-making is primarily cost-driven and awareness of chitosan's superior biodegradability profile remains limited among procurement professionals.

Competitive Landscape:

Asia Pacific chitosan market has a competitive environment with the presence of large-scale producers, biochemical industry players, and aquaculture processing companies. Large-scale producers of chitosan are investing in expanding their production capacity, improving the efficiency of the production process, and developing diverse product offerings for the expanding pharmaceutical, agricultural, and industrial-grade chitosan markets. The competition in the Asia Pacific chitosan market is rising, with players in the region focusing on meeting the expanding domestic demand while exploring the export markets. Key players in the Asia Pacific chitosan market are focusing on the following areas: developing partnerships with aquaculture companies for the procurement of raw materials, improving the purity of chitosan for the expanding pharmaceutical-grade chitosan market, and developing chitosan derivatives for specialty applications. The players in the Asia Pacific chitosan market are seeking regulatory approvals for premium-priced pharmaceutical and food-grade chitosan for the Japanese, Korean, and Australian markets.

Asia Pacific Chitosan Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Grades Covered | Industrial Grade, Food Grade, Pharmaceutical Grade |

| Sources Covered | Shrimp, Crab, Squid, Krill, Others |

| Applications Covered | Water Treatment, Food & Beverages, Cosmetics, Medical & Pharmaceuticals, Agrochemicals, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Asia Pacific Chitosan Market Report

The Asia Pacific chitosan market size was valued at USD 1.46 Billion in 2025.

The Asia Pacific chitosan market is expected to grow at a compound annual growth rate of 9.87% from 2026-2034 to reach USD 3.41 Billion by 2034.

Industrial grade dominated the market with a share of 52%, driven by extensive use in water treatment, textile processing, and agriculture, where high-volume consumption and cost efficiency requirements favor industrial-specification chitosan across multiple end-use industries in the region.

Key factors driving the Asia Pacific chitosan market include tightening environmental regulations, rapid aquaculture industry expansion, growing pharmaceutical and nutraceutical adoption, increasing agricultural bio-stimulant demand, and rising consumer preference for natural, biodegradable ingredients across food, cosmetics, and packaging sectors.

Major challenges include high purification costs for specialty grades, seasonal feedstock supply variability, competition from established synthetic coagulants, limited awareness of chitosan's benefits among industrial procurement professionals, and regulatory complexity for pharmaceutical-grade product approvals across multiple regional jurisdictions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)