Asia Pacific Electric Vehicle Charging Station Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application, and Country 2026-2034

Asia Pacific Electric Vehicle Charging Station Market Size, Share, Trends & Forecast (2026-2034)

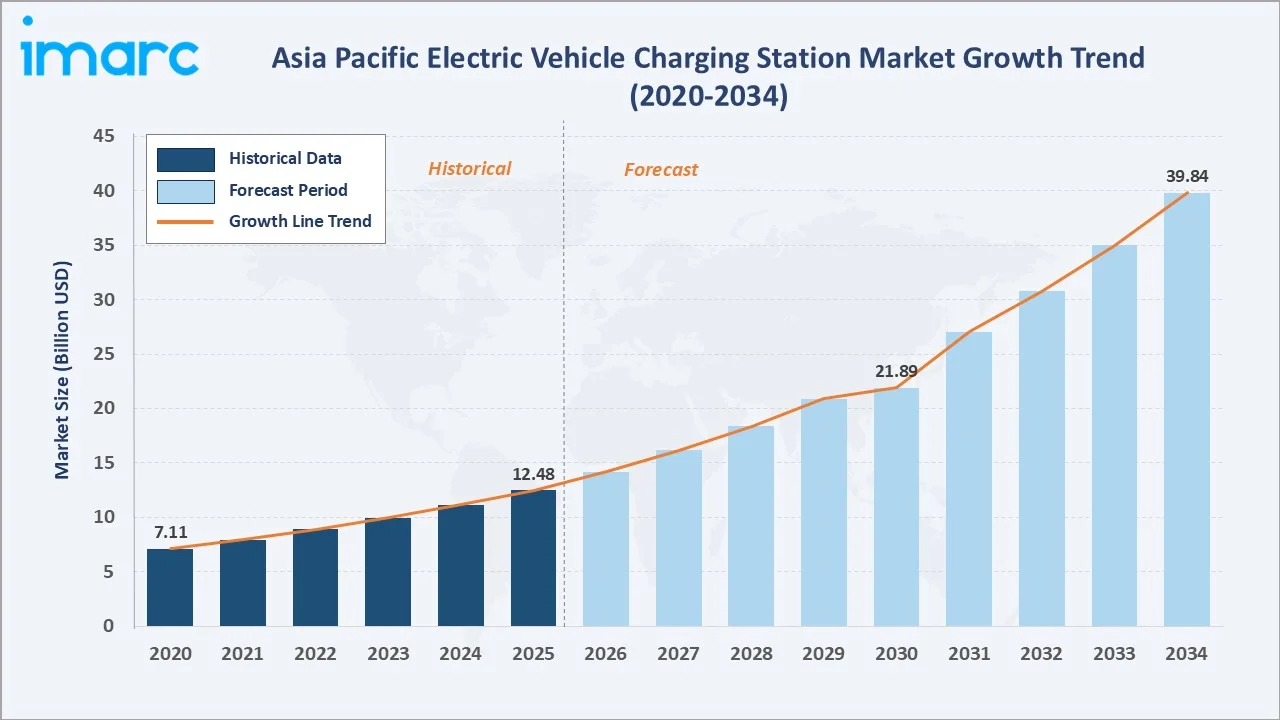

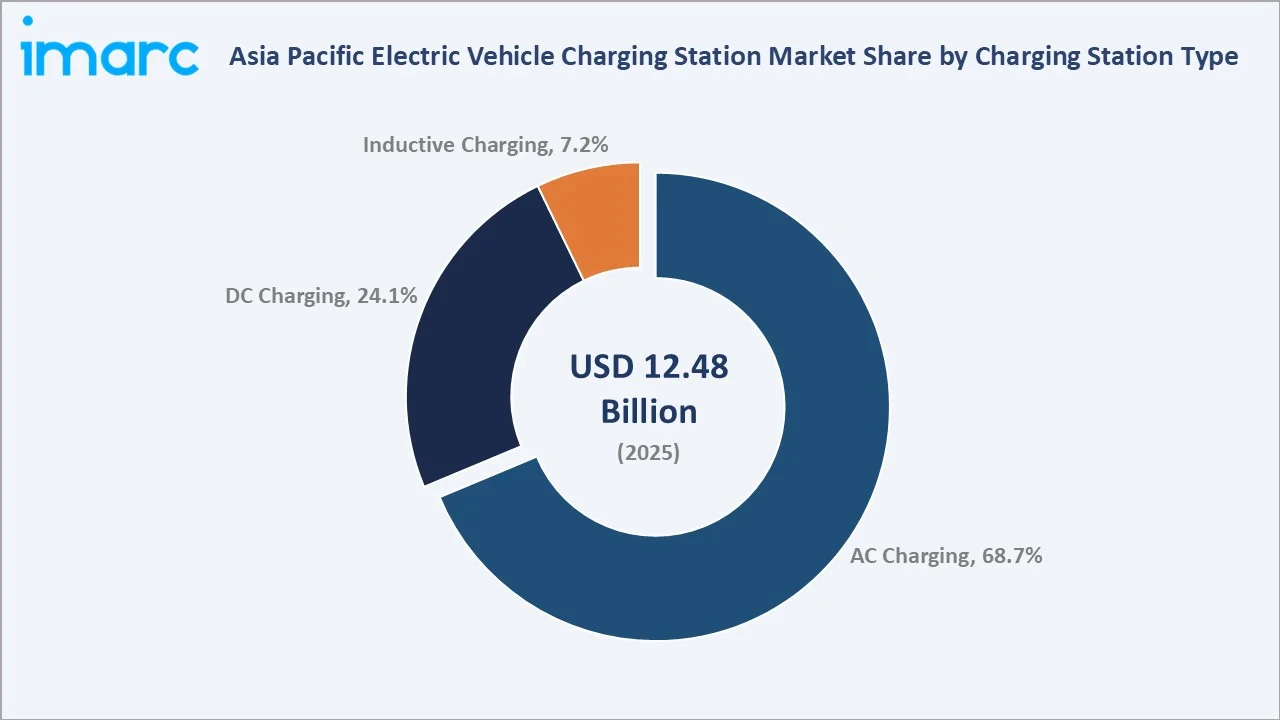

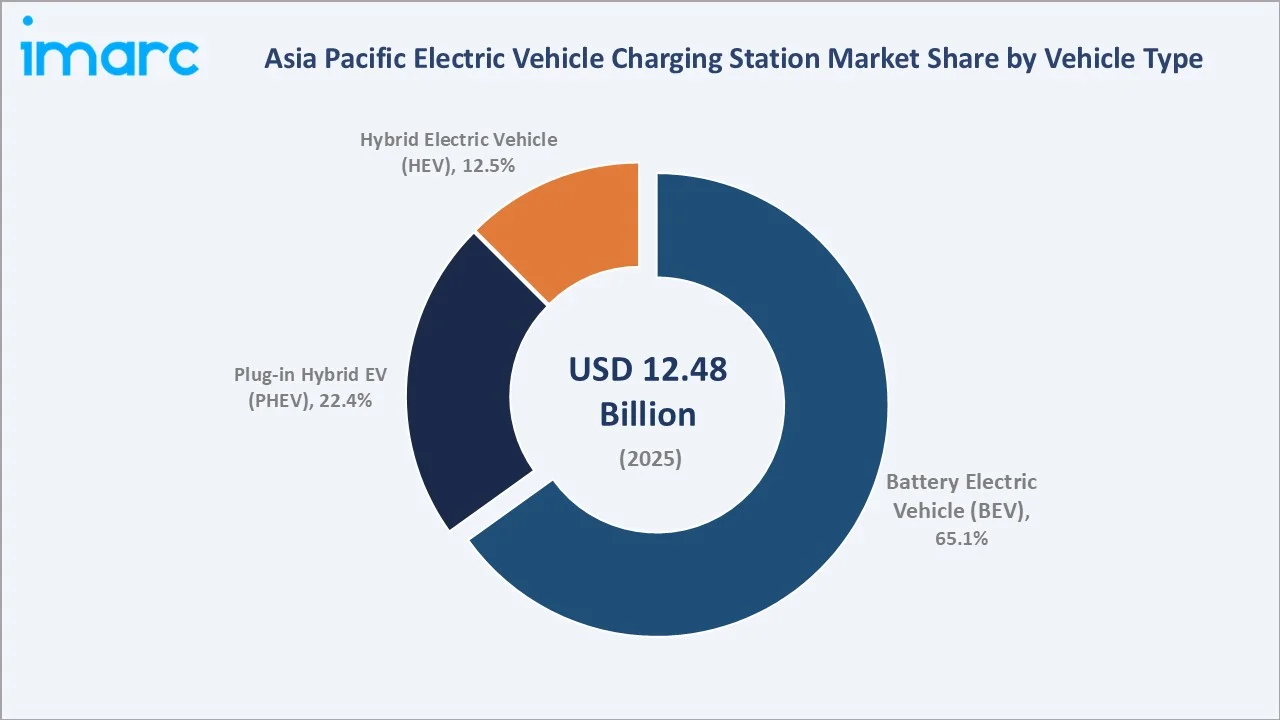

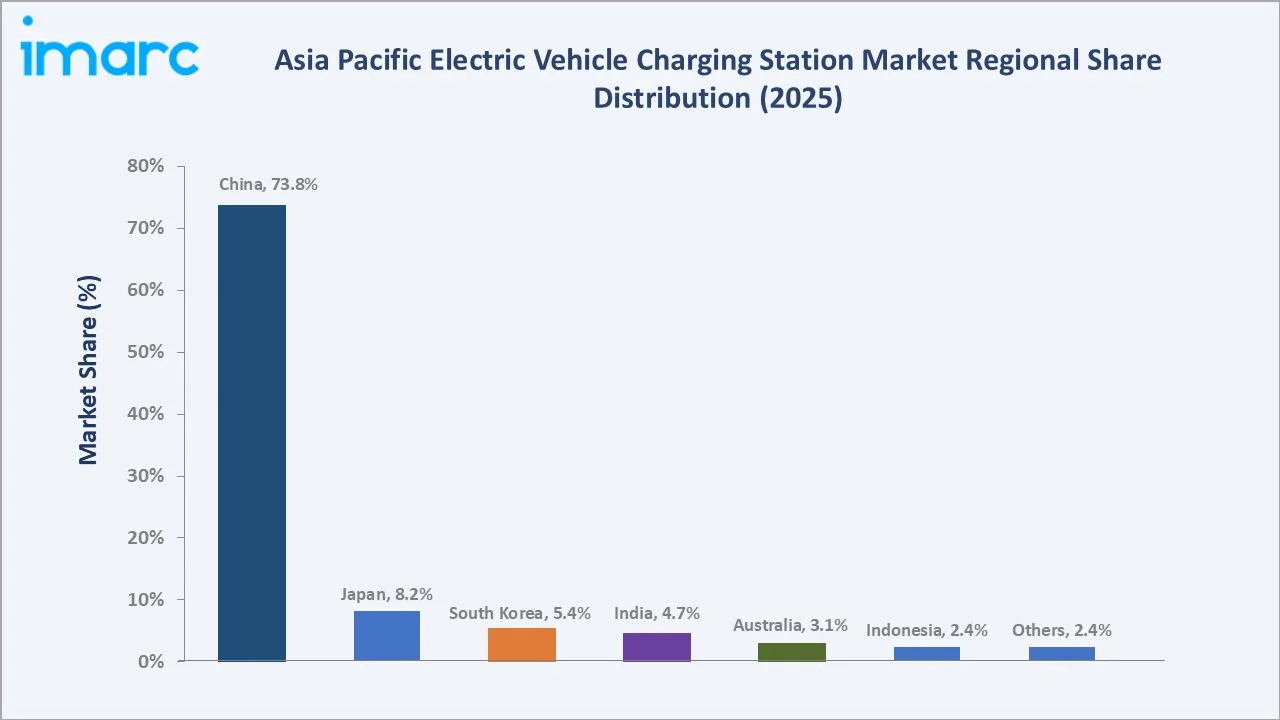

The Asia Pacific electric vehicle charging station market reached USD 12.48 Billion in 2025 and is projected to reach USD 39.84 Billion by 2034, growing at a CAGR of 11.90% during 2026-2034. The market is driven by rapid EV adoption, supportive government policies, and increasing investments in charging infrastructure development. Rising urbanization and expansion of public and private charging networks are further accelerating market growth. As of March 2026, India deployed more than 29,000 public EV charging stations across the country, reflecting the rapid expansion of charging infrastructure to support electric mobility. AC charging dominates the charging station type segment, with a 68.7% share in 2025. Battery electric vehicles (BEV) lead vehicle type demand at 65.1%. China commands 73.8% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.48 Billion |

|

Forecast Market Size (2034) |

USD 39.84 Billion |

|

CAGR (2026-2034) |

11.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Charging Station Type |

AC Charging (68.7%, 2025) |

|

Dominant Vehicle Type |

BEV (65.1%, 2025) |

|

Leading Country |

China (73.8%, 2025) |

The market expanded from USD 7.11 Billion in 2020 to USD 12.48 Billion in 2025, anchored at USD 21.89 Billion in 2030, and forecast to reach USD 39.84 Billion by 2034. China's extraordinary pace of EV charging deployment was the defining market growth force of the 2020-2025 period. COVID-19 supply chain disruptions temporarily slowed charger hardware deliveries in 2021-2022, but government infrastructure stimulus packages and pent-up EV demand accelerated the market recovery strongly from 2023.

To get more information on this market, Request Sample

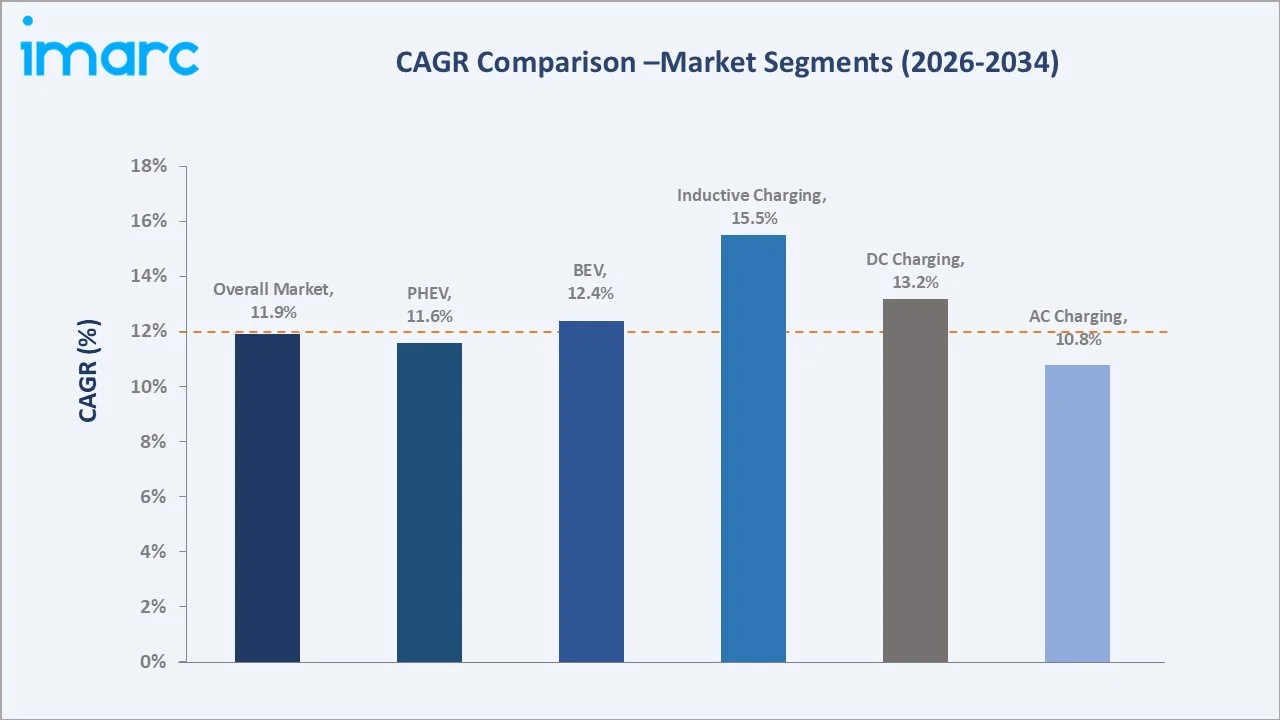

Inductive (wireless) charging grows fastest at ~15.5% CAGR as OEMs integrate wireless charging compatibility in premium models, and public wireless charging pads are deployed at commercial parking, taxi ranks, and autonomous vehicle hubs across China, Japan, and South Korea. The BEV segment grows at ~12.4% CAGR driven by NEV mandate compliance and India's BEV expansion, creating new demand pools across all Asia Pacific sub-markets.

Executive Summary

The Asia Pacific electric vehicle charging station market reached USD 12.48 Billion in 2025, representing one of the largest regional EV charging markets by station count, installation investment, and technology innovation pace. The market encompasses the full spectrum of EV charging technologies from basic Level 1 AC domestic sockets through Level 2 AC wallboxes (7-22 kW), DC fast chargers (20-150 kW), DC ultra-fast chargers (150-480 kW), and emerging inductive wireless charging systems. The market is projected to reach USD 39.84 Billion by 2034.

AC charging at 68.7% dominates through the installed base of residential, workplace, and destination charging points, where Level 2 AC charging (7-22 kW) represents the most cost-effective charging solution for overnight or extended-duration parking scenarios. BEV at 65.1% leads vehicle type demand as pure electric vehicles generate the highest per-vehicle charging infrastructure demand and the highest average charging session value. China, at 73.8%, commands regional market dominance through the combination of scale NEV production, government-mandated infrastructure deployment, and commercial operator network investment at a scale unmatched by any other APAC nation.

Key Market Insights

|

Insight |

Data |

|

Dominant Charging Station Type |

AC Charging - 68.7% share (2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle (BEV) - 65.1% market share (2025) |

|

Leading Country |

China - 73.8% market share (2025) |

|

Market Opportunity |

DC ultra-fast 350 kW hub rollout; V2G grid services; solar-integrated charging parks; India public charging build-out; highway DC fast-charge corridor expansion |

Key Analytical Observations Supporting the Above data:

- AC Charging at 68.7%: AC charging dominates due to its lower installation cost, compatibility with home/workplace charging, and suitability for overnight or long-duration charging. Its wider deployment across residential, commercial, and public locations supports a strong market share.

- Battery Electric Vehicle (BEV) at 65.1%: The BEV segment dominates because battery electric vehicles fully depend on external charging infrastructure, creating higher demand for public, residential, and commercial charging stations. Rapid BEV adoption across China, India, Japan, and South Korea further supports segment growth.

- China at 73.8%: China dominates due to its massive EV fleet, strong government support, and the world’s largest public charging infrastructure network. Rapid urban charging deployment and high BEV sales continue to strengthen its leadership in the Asia Pacific market.

Asia Pacific Electric Vehicle Charging Station Market Overview

The Asia Pacific electric vehicle charging station market encompasses all infrastructure, hardware, software, and services enabling the replenishment of EV battery energy across the region's diverse vehicle fleet, spanning BEVs, PHEVs, and HEVs across passenger cars, commercial vehicles, electric two-wheelers, electric three-wheelers, electric buses, and electric commercial fleet vehicles. Key charging infrastructure categories include AC Level 1, AC Level 2, DC fast charging (20-150 kW), DC ultra-fast charging (150-480 kW), and inductive/wireless charging.

The ecosystem integrates EVCS hardware manufacturers, charging network operators, CPOs, grid utilities and energy providers, EV OEM charging service divisions, software platform providers, and government agencies providing policy mandates and subsidy programmes. Macroeconomic factors include rising disposable incomes, urbanization, fuel cost volatility, and increasing EV affordability.

Market Dynamics

To evaluate market opportunities, Request Sample

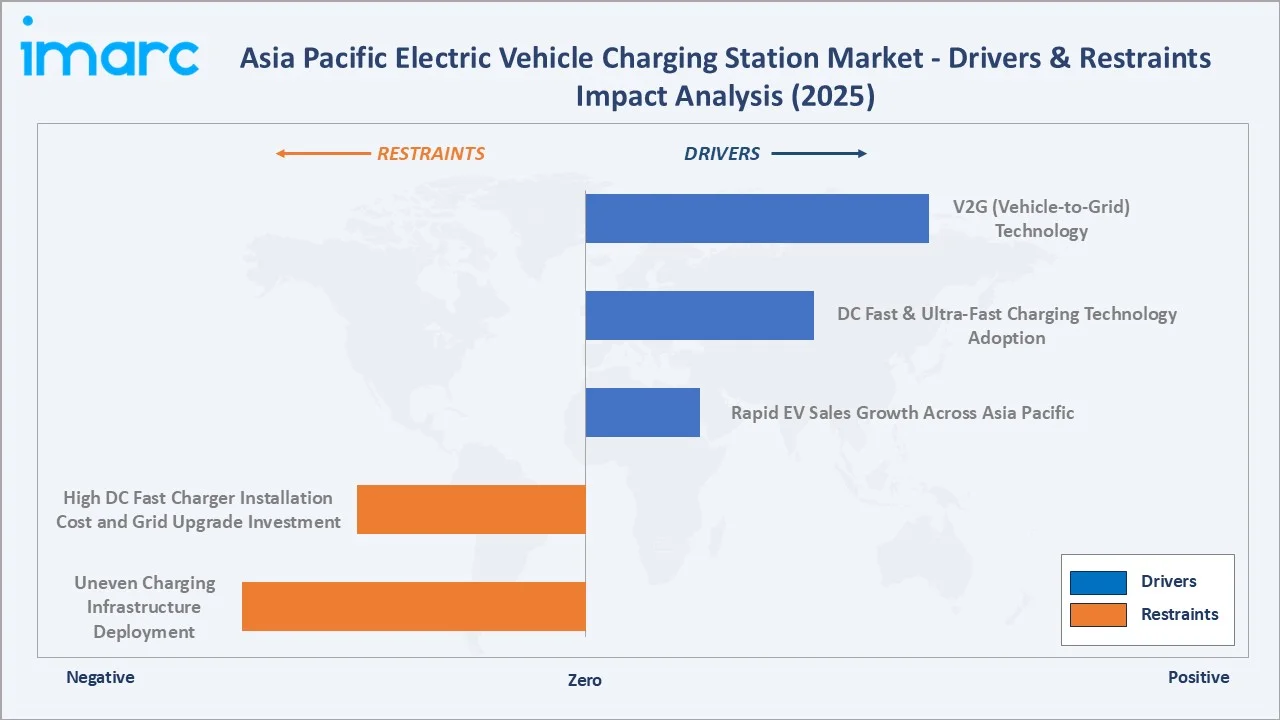

Market Drivers

- Rapid EV Sales Growth Across Asia Pacific: Rapid EV sales growth across Asia Pacific is increasing the number of electric vehicles requiring regular charging infrastructure. Rising EV adoption in countries such as China, India, Japan, and South Korea is accelerating investments in public and private charging networks. India established an ambitious goal to increase EV adoption by 2030, targeting electric vehicles to account for 30% of private car sales, 70% of commercial vehicles, 40% of buses, and 80% of two- and three-wheelers. This is expected to result in nearly 80 million EVs on Indian roads, supported by the government’s “Make in India” initiative aimed at strengthening domestic EV manufacturing and production capabilities. The expansion of the EV fleet and local manufacturing capabilities is expected to boost investments in charging networks and strengthen the Asia Pacific EV charging station market.

- DC Fast and Ultra-Fast Charging Technology Adoption: DC fast and ultra-fast charging technology reduces charging time and improves user convenience. It supports long-distance travel, commercial fleet electrification, and high-traffic public charging locations. As BEV adoption rises, demand for rapid charging networks across highways, cities, and logistics hubs is increasing. This is encouraging stronger investment in advanced charging infrastructure across the region.

- V2G (Vehicle-to-Grid) Technology: V2G (Vehicle-to-Grid) technology enables bidirectional energy flow between EVs and the power grid. It allows EV batteries to store and supply electricity during peak demand periods, improving grid stability and energy efficiency. The technology is encouraging the deployment of smart charging infrastructure and advanced charging stations. Growing renewable energy integration and smart grid initiatives across the Asia Pacific are further supporting V2G adoption.

Market Restraints

- High DC Fast Charger Installation Cost and Grid Upgrade Investment: High DC fast charger installation costs increase upfront investment requirements for operators. These chargers often need grid upgrades, transformer capacity expansion, and advanced power management systems. High land, equipment, and maintenance costs can reduce profitability, especially in low-utilization areas. As a result, deployment of fast-charging networks may slow in some emerging markets.

- Uneven Charging Infrastructure Deployment: Uneven charging infrastructure deployment creates gaps between urban and rural charging availability. While major cities have expanding networks, highways, and smaller towns, remote areas often lack sufficient charging access. This increases range anxiety and limits EV adoption in underserved regions. As a result, charging operators face challenges in achieving balanced network expansion and consistent utilization.

Market Opportunities

- Solar-Integrated EV Charging Parks Creating Green Charging Proposition and Grid Independence: Solar-integrated EV charging parks enable clean energy-based charging and reduce dependence on conventional power grids. These facilities can lower operating costs through renewable energy generation while supporting sustainable mobility goals. They also help improve energy security and reduce grid load during peak demand periods. Growing investments in solar infrastructure and renewable energy policies across the region are further supporting adoption.

- Electric Bus and Commercial Fleet Charging Creating Large-Scale Depot Charging Demand: Electric bus and commercial fleet charging create a strong opportunity by generating demand for large-scale depot charging infrastructure. Fleet operators require reliable, high-capacity chargers to support daily operations, route planning, and vehicle uptime. The growing electrification of buses, delivery vans, taxis, and logistics fleets across the Asia Pacific is increasing investment in dedicated charging hubs. This supports recurring charging demand and creates long-term revenue opportunities for charging station operators.

Market Challenges

- Grid Stability and Power Quality Management Challenges from High-Density DC Fast Charging Clusters: High-density DC fast charging clusters place a heavy load on local grids. Sudden spikes in electricity demand may cause voltage fluctuations, power quality issues, and grid congestion. Operators may need advanced energy management systems, storage solutions, and costly grid upgrades to maintain reliability. These technical and investment requirements can slow large-scale fast-charging deployment.

- Cybersecurity Risks in Connected EV Charging Networks Creating Operational and Regulatory Compliance Requirements: Cybersecurity risks in connected EV charging networks expose chargers, payment systems, and user data to potential cyberattacks. Operators must invest in secure communication protocols, software updates, monitoring systems, and data protection measures. Growing regulatory requirements also increase compliance costs and operational complexity. These risks can slow network expansion and affect consumer trust in public charging infrastructure.

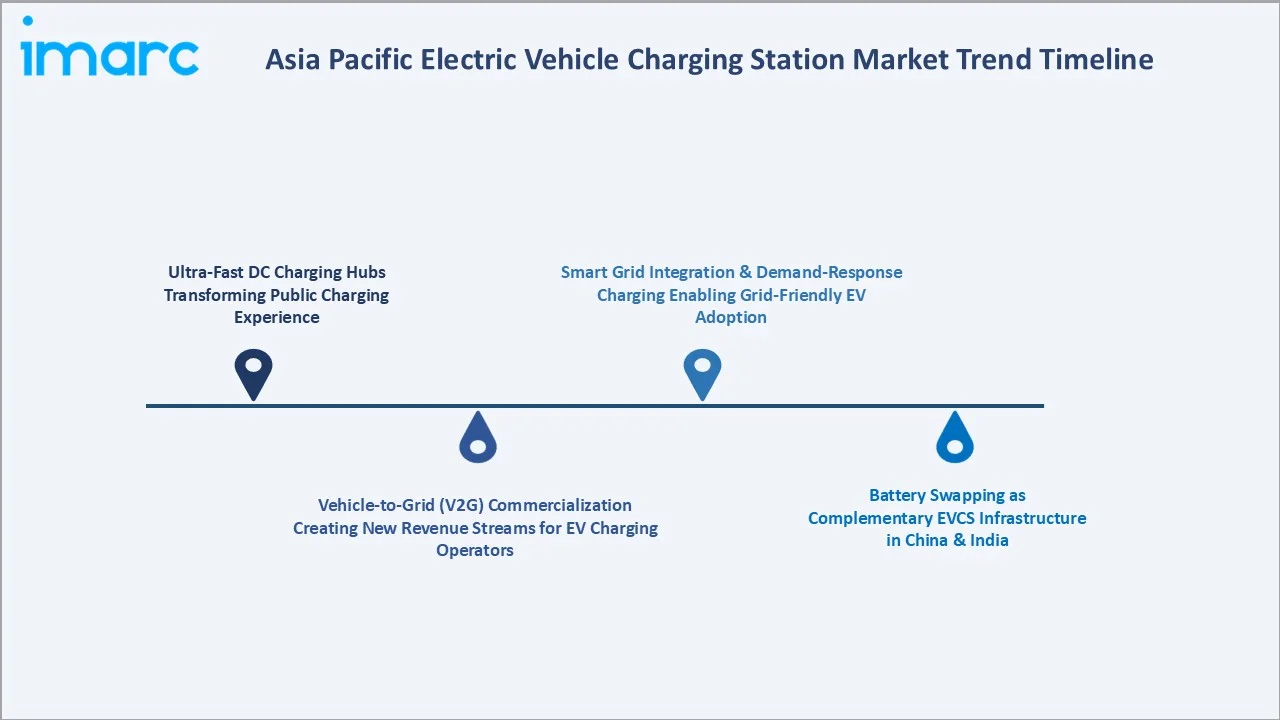

Emerging Market Trends

1. Ultra-Fast DC Charging Hubs Transforming Public Charging Experience

Ultra-fast DC charging hubs significantly reduce charging time and improve user convenience. These hubs support high-power charging for passenger vehicles, commercial fleets, and long-distance travel applications. Their deployment across highways, urban centers, and transit locations is enhancing public charging accessibility. In October 2025, ThunderPlus inaugurated its MegaWatt Ultra-Fast EV Charging Hub at Mutthugadahalli near Bangalore International Airport. Spanning around 28,000 square feet, the facility is among India’s advanced EV charging hubs and offers a total charging capacity of 1 MW. The hub includes multiple charging options, ranging from 7.4 kW AC chargers for regular charging needs to 240 kW DC ultra-fast chargers for rapid charging applications.

2. Vehicle-to-Grid V2G Commercialization Creating New Revenue Streams for EV Charging Operators

V2G commercialization allows EV charging operators to earn revenue from bidirectional energy services. Operators can use connected EV batteries to support peak load management, grid balancing, and renewable energy storage. This creates new business models beyond charging fees, such as energy trading and grid support services. As smart grids expand across the Asia Pacific, V2G-enabled charging stations are becoming more valuable.

3. Battery Swapping as Complementary EVCS Infrastructure in China and India

Battery swapping is emerging as a complementary trend in the Asia Pacific EV charging station market, particularly in China and India, where two-wheelers, three-wheelers, and commercial fleets are rapidly electrifying. The model enables quick battery replacement, reducing charging time and improving vehicle uptime. It also lowers range anxiety and supports high-utilization mobility applications such as delivery and ride-hailing services. This trend is expanding EV infrastructure beyond conventional charging stations and creating additional ecosystem opportunities.

4. Smart Grid Integration and Demand-Response Charging Enabling Grid-Friendly EV Adoption

Smart grid integration and demand-response charging enable charging stations to optimize electricity use based on grid conditions. These systems can shift charging loads to off-peak periods, reducing grid stress and improving energy efficiency. They also support renewable energy integration and enhance grid stability. As EV adoption rises, grid-friendly charging solutions are becoming essential for sustainable infrastructure expansion.

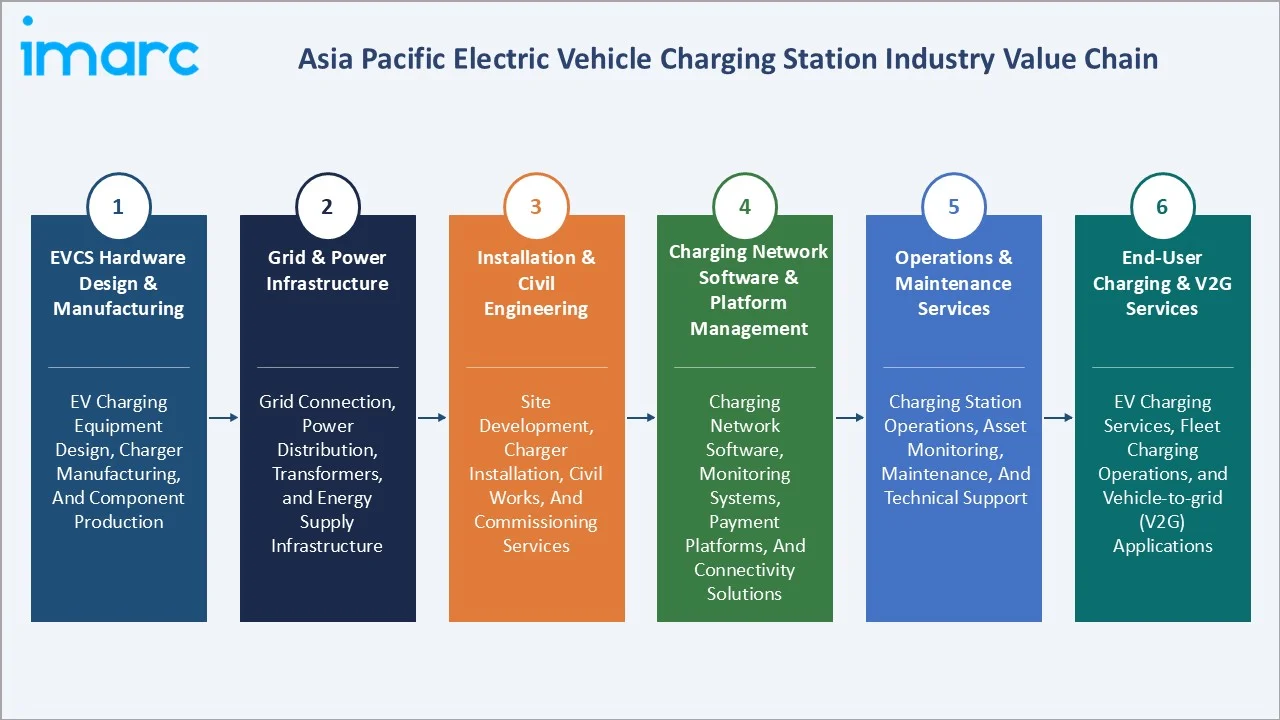

Industry Value Chain Analysis

The Asia Pacific EV charging station value chain integrates EVCS hardware design and manufacturing, grid and power infrastructure, civil installation and engineering, network software and billing management, operations and asset management, and end-user charging and V2G services. This dual-revenue structure rewards vertically integrated operators with hardware margin plus services revenue versus pure hardware manufacturers capturing only the initial hardware sale value.

|

Stage |

Key Participants |

|

EVCS Hardware Design & Manufacturing |

EV charging equipment design, charger manufacturing, and component production |

|

Grid & Power Infrastructure |

Grid connection, power distribution, transformers, and energy supply infrastructure |

|

Installation & Civil Engineering |

Site development, charger installation, civil works, and commissioning services |

|

Charging Network Software & Platform Management |

Charging network software, monitoring systems, payment platforms, and connectivity solutions |

|

Operations & Maintenance Services |

Charging station operations, asset monitoring, maintenance, and technical support |

|

End-User Charging & V2G Services |

EV charging services, fleet charging operations, and Vehicle-to-Grid (V2G) applications |

The network software and billing management tier is increasingly the highest-margin component of the EV charging value chain. The V2G services tier remains nascent but carries transformative commercial potential.

Technology Landscape in the Asia Pacific Electric Vehicle Charging Station Industry

AC Level 2 Charging Technology

AC Level 2 charging technology provides cost-effective and widely accessible charging solutions for residential, workplace, and public locations. It offers moderate charging speeds suitable for overnight and daily charging needs, supporting large-scale EV adoption. The technology requires lower installation costs compared to DC fast chargers, enabling wider deployment. Its compatibility with smart charging and energy management systems further supports the development of connected charging infrastructure.

DC Fast Charging Power Electronics

DC fast charging power electronics enable high-power and ultra-fast charging capabilities. Advanced components such as power converters, rectifiers, and energy management systems improve charging efficiency, reduce charging time, and support higher voltage platforms. These technologies are essential for commercial fleets, highways, and high-traffic charging hubs. Their development is accelerating the deployment of next-generation fast-charging infrastructure across the region. Ultraviolette and Bolt.Earth announced that its interoperable Type-6 DC fast-charging network, launched through a strategic partnership in March 2026, surpassed 130 installed chargers across India. This exceeds the original deployment target of 50 chargers by more than double and was achieved ahead of schedule.

Smart Charging and OCPP Protocol

Smart charging and OCPP (Open Charge Point Protocol) enable interoperability, remote monitoring, and intelligent energy management. OCPP allows seamless communication between charging stations and network management platforms from different providers. Smart charging optimizes charging schedules, balances grid load, and supports demand-response programs. These technologies are improving operational efficiency and supporting the development of connected grid-integrated charging ecosystems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

68.7% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

65.1% |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Country |

China |

73.8% |

2025 |

By Charging Station Type

AC charging leads at 68.7% (2025). AC charging encompasses residential Level 2 wallboxes, workplace charging stations, commercial destination charging at retail and hospitality properties, and street-side community charging in urban residential areas. AC charging's commercial dominance reflects the installed base concentration at residential and workplace locations where charging time is not the constraining factor.

To access detailed market analysis, Request Sample

DC charging grows at ~13.2% CAGR through the 2026-2034 forecast period as highway DC fast charging corridor investment accelerates across APAC and urban commercial fast charging hubs proliferate. Inductive charging at 7.2% represents the premium wireless charging segment growing at ~15.5% CAGR as OEM wireless charging integration and commercial wireless pad deployment expand.

By Vehicle Type

Battery electric vehicle (BEV) leads at 65.1% (2025). BEV's dominant position reflects both the growing BEV fleet size and the above-average per-vehicle charging infrastructure demand that BEV creates versus PHEV and HEV.

PHEV at 22.4% represents plug-in hybrid charging demand primarily through AC Level 2 residential and workplace charging for overnight battery replenishment. HEV at 12.5% includes non-plug-in hybrid vehicles using compatible public AC charging as an opportunistic amenity at locations where AC Level 2 charging is available alongside parking.

Regional Market Insights

|

Country |

Share (2025) |

Key EV Charging Station Market Drivers & Characteristics |

|

China |

73.8% |

Driven by its extensive EV fleet, large public charging network, and strong government support for EV infrastructure development. |

|

Japan |

8.2% |

Driven by EV adoption initiatives, smart charging deployment, and investments in advanced charging technologies and energy integration systems. |

|

South Korea |

5.4% |

Supported by growing EV penetration, fast-charging network expansion, and government-backed clean mobility programs. |

|

India |

4.7% |

Driven by increasing EV adoption, expanding public charging infrastructure, and supportive electrification policies. |

|

Australia |

3.1% |

Supported by rising EV sales, highway charging corridor development, and investments in renewable energy-based charging infrastructure. |

|

Indonesia |

2.4% |

Supported by EV ecosystem development, battery industry investments, and government electrification strategies. |

|

Others |

2.4% |

The others segment includes developing Asia Pacific markets that are gradually expanding charging infrastructure alongside increasing EV adoption. |

China, at 73.8%, represents the defining market force in APAC EV charging; any analysis of the regional market is largely a study of China's infrastructure policy and commercial deployment dynamics. Japan, at 8.2%, and South Korea, at 5.4%, are the two most commercially sophisticated non-China APAC markets.

India, at 4.7%, is the region's fastest-growing major market from a small base. Australia, at 3.1%, represents the developed APAC market with the fastest transition pace outside East Asia. Indonesia, at 2.4%, and others, at 2.4%, collectively represent the emerging Southeast Asian APAC EV charging growth frontier where large populations and growing middle-class EV adoption create the next wave of APAC charging market growth.

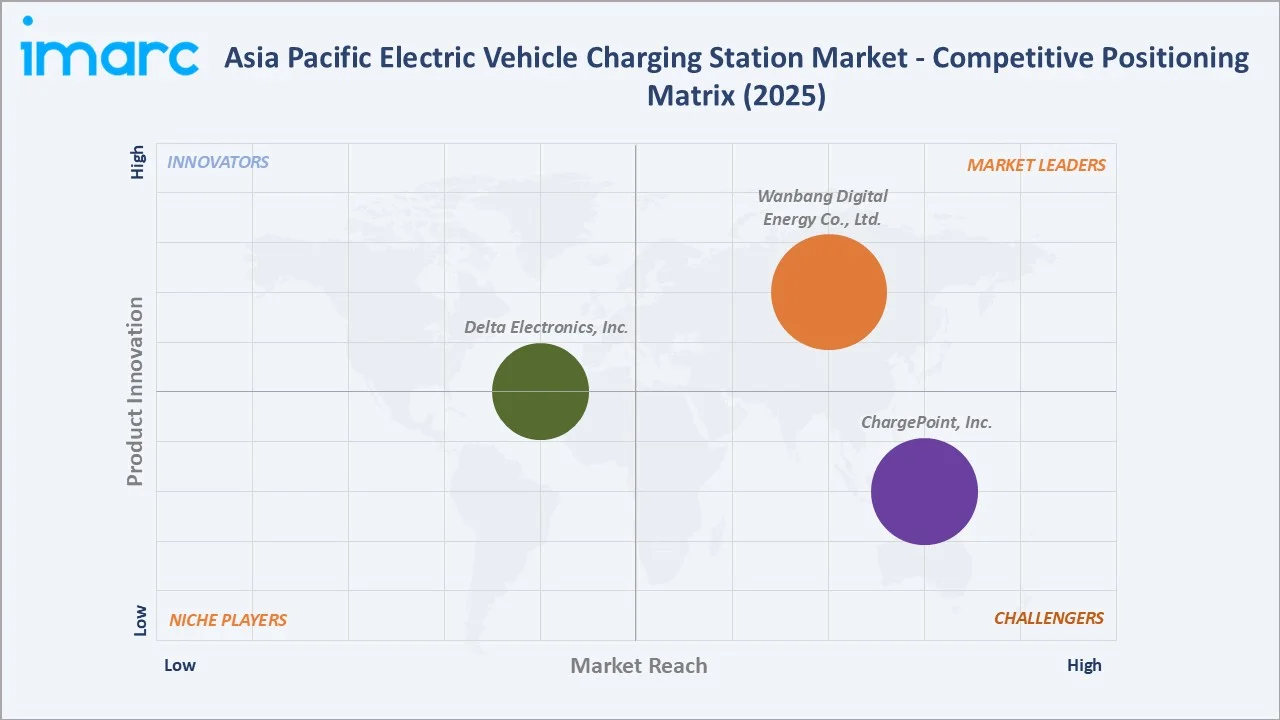

Competitive Landscape

The Asia Pacific EV charging station market competitive landscape is structured in three tiers: China dominant operators, international hardware and technology companies with APAC presence, and emerging market specialists.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Wanbang Digital Energy Co., Ltd. |

Artemis |

Market Leader |

Wanbang Digital Energy Co., Ltd. (operating under the brand StarCharge), a prominent player in China, provides comprehensive hardware (AC, DC, and V2G chargers). |

|

ChargePoint, Inc. |

Express Plus, Express 280, Express 250, CP6000, CT4000, CPF50 |

Strong Challenger |

ChargePoint, Inc. operates a robust network in the APAC region, offering smart Level 2 AC and DC fast charging solutions for homes, workplaces, and commercial fleets. |

|

Delta Electronics, Inc. |

AC Mini Plus, AC MAX, 15KW Bharat DC Charger, 30KW DC Charger, 120KW DC City Charger, 180KW DC Ultra Fast Charger |

Established Player |

Delta Electronics, Inc. provides a comprehensive AC and DC fast-charging infrastructure. |

The competitive boundary between EV OEMs and charging network operators is uniquely blurred in the Asia Pacific. This OEM charging network strategy is most developed in China but is progressively extending to APAC export markets, creating an OEM-led charging network competitive layer in APAC markets that independent CPOs must address through interoperability and pricing competitive strategy.

Key Company Profiles

Wanbang Digital Energy Co., Ltd.

Wanbang Digital Energy Co., Ltd. (operating under the StarCharge brand) is a leading EV charging infrastructure company and a prominent participant in the Asia Pacific EV charging station market. Headquartered in China, the company specializes in EV charging equipment manufacturing and charging network solutions.

- Key Products: Artemis, StarLeap, StarStride, Interstellar, Morning Star.

- Strategic Focus: Focuses on expanding smart, fast, and grid-integrated EV charging solutions through AC/DC chargers, V2G, energy storage, and digital energy management platforms.

ChargePoint, Inc.

ChargePoint, Inc. is a leading EV charging infrastructure company and an active participant in the Asia Pacific EV charging station market through its charging hardware, software, and network management solutions. The company provides a broad portfolio of AC chargers, DC fast chargers, and fleet charging solutions for residential, commercial, workplace, and public charging applications.

- Key Products: Express Plus, Express 280, Express 250, CP6000, CT4000, CPF50.

- Recent Developments: In February 2025, HCLTech announced a partnership with ChargePoint to accelerate innovation in EV charging software solutions. As part of the collaboration, HCLTech established an advanced research and development center for ChargePoint in Bengaluru, India, which will function as a key hub for the company’s software development activities in the country.

- Strategic Focus: Focuses on software-led, networked EV charging solutions, and R&D-driven innovation to support scalable charging infrastructure in the Asia Pacific.

Market Concentration Analysis

The Asia Pacific EV charging station market is highly concentrated at the China market level, with Chinese domestic operators collectively representing approximately 60-65% of total APAC market revenue. At the non-China APAC level, market concentration is more distributed among international operators and local national CPOs. Market concentration is declining as non-China APAC markets grow faster than the China market, progressively increasing the non-China APAC share.

Investment & Growth Opportunities

Highest Growth Segments

Inductive charging (~15.5% CAGR), DC charging (~13.2% CAGR), BEV demand (~12.4% CAGR), India country market (~28-32% CAGR), Southeast Asia (Thailand, Malaysia, Vietnam, Indonesia collectively ~20-25% CAGR), V2G services (USD 500 Million-2 Billion new revenue stream by 2030), solar-integrated charging (~20% CAGR), and electric bus depot charging (~18% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

India's public EV charging infrastructure represents APAC's highest-potential emerging market investment opportunity, with India's combination of a large and fast-growing EV market, extremely low current charging infrastructure density, and growing domestic EV charging hardware manufacturing capability creating a market where early infrastructure investment positions CPOs for dominant network position through the market's formative development period.

Investment Themes

- Highway DC ultra-fast charging corridor investment in India, Southeast Asia, and Australia, creating first-mover network position: The construction of highway DC fast charging corridors in India, Thailand, Indonesia, Vietnam, and Australia represents the infrastructure that enables intercity EV travel in each market, the critical moment where EV becomes a viable choice for buyers who regularly drive 300+ km intercity trips.

- V2G grid services platform development capturing the highest-margin EVCS service revenue tier: V2G commercial service development, building the software, hardware, and grid authority agreements enabling aggregated EV batteries to provide frequency regulation, peak shaving, and renewable energy integration services, creates charging network revenues of USD 50-300 per EV per year in grid services that substantially improve CPO commercial economics beyond energy retail margin alone.

Future Market Outlook (2026-2034)

The Asia Pacific EV charging station market is projected to grow from USD 12.48 Billion in 2025 to USD 39.84 Billion by 2034, delivering an 11.90% CAGR over the forecast period. The market's anchor value of USD 21.89 Billion in 2030 represents an APAC EV charging industry at its critical mass inflection point. China's charging network is achieving universal urban coverage and expanding toward secondary cities and rural completeness. India's public charging infrastructure is reaching adequate density for confident BEV adoption across top-50 cities, and Southeast Asian EV charging networks are achieving the highway corridor coverage that enables intercity BEV travel in Thailand, Malaysia, and Vietnam as first movers among ASEAN markets.

Three structural forces define the APAC EV charging station market growth through 2034 with confidence. The EV fleet growth compounding effect creates a self-reinforcing demand cycle where infrastructure investment begets EV adoption, which begets further infrastructure investment. The APAC region's annual new EV fleet addition. The DC ultra-fast technology transition enables the commercial economics of DC charging to progressively improve, accelerating the AC-to-DC mix shift that drives above-average revenue per station as charging stations serve more vehicles per day with shorter dwell times at premium pricing.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including EV Charging Network Directors; CPO commercial development leads; Government EV infrastructure programme leads; EV OEM charging service directors; and grid utility EV integration leads.

Secondary Research

Secondary research encompassed the China Ministry of Industry and Information Technology EV charging infrastructure report 2024; EV Outlook 2024; China Passenger Car Association data; India Ministry of Power dashboard; Australian EV Council market data; South Korea Ministry of Environment EV charging statistics 2024; Japan EV infrastructure whitepaper; company annual reports; EV charging APAC market report; Electric Vehicle Outlook 2025. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a country-level bottom-up model: (i) country-level EV fleet projections from government policy targets and historical adoption rates calibrated against IEA EV adoption scenarios; (ii) infrastructure investment per EV (AC per-station cost times station-to-EV ratio target plus DC fast charger station count times installation cost) by country and charging type; (iii) network operations and services revenue (CPO energy retail margin, network subscription, V2G services where applicable) added to hardware revenue.

Asia Pacific Electric Vehicle Charging Station Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging, Inductive Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combined Charging System (CCS), CHAdeMO, Normal Charging, Tesla Supercharger, Type-2 (IEC 62196), Others |

| Applications Covered | Residential, Commercial |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Companies Covered | Wanbang Digital Energy Co., Ltd., ChargePoint, Inc., Delta Electronics, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Asia Pacific electric vehicle charging station market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Asia Pacific electric vehicle charging station market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the electric vehicle charging station industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Asia Pacific Electric Vehicle Charging Station Market Report

The Asia Pacific EV charging station market reached USD 12.48 Billion in 2025, driven by China's dominant 73.8% market share from NEV mandate-driven infrastructure deployment, South Korea's high-density charging network, Japan's DC fast charging upgrade programme, and Australia's accelerating EV adoption under the national charging infrastructure programme.

The market grows at 11.90% CAGR during 2026-2034, reaching USD 39.84 Billion by 2034. Growth is driven by BEV fleet compounding demand, DC ultra-fast charging technology deployment accelerating from pilot to mainstream, V2G commercial service revenue creating new CPO revenue streams, India and Southeast Asia transitioning from nascent to growth phase charging markets, and solar-integrated charging park economics enabling infrastructure deployment without grid upgrade cost constraints.

AC charging leads at 68.7% through the installed base dominance of residential, workplace, and destination Level 2 AC charging infrastructure.

Battery electric vehicles (BEV) lead at 65.1% as BEVs create full dependency on charging infrastructure for all propulsion energy and are growing fastest at ~12.4% CAGR through NEV mandate compliance, and India BEV expansion.

China leads at 73.8% through the largest EV fleet, the largest public charging network, NEV mandate for new vehicle sales, and infrastructure investments.

Leading companies include Wanbang Digital Energy Co., Ltd., ChargePoint, Inc., and Delta Electronics, Inc., among others.

The market is projected to reach approximately USD 21.89 Billion by 2030, with China's ultra-fast charging hub programme, V2G commercial services launching nationally in China, generating high annual V2G revenue contribution, and India's public DC fast charging stations growth.

AC (alternating current) charging uses the EV's built-in on-board charger (OBC) to convert grid AC to battery DC, providing 7-22 kW (Level 2) charging for overnight and destination use at a USD 500-5,000 installation cost. DC (direct current) fast charging converts grid AC to high-voltage DC directly in the charging station and delivers ready-to-use DC to the battery, bypassing the OBC, providing 20-480 kW for rapid public charging at a USD 20,000-200,000 installation cost. Inductive (wireless) charging uses magnetic resonance coupling to transfer power from a ground pad to a vehicle receiver coil without physical connection, providing 7.4-22 kW for premium destination charging at USD 3,000-10,000 installation cost, enabling seamless charging at compatible vehicles without plugging in.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)