Asia Pacific Logistics Market Size, Share, Trends and Forecast by Model Type, Transportation Mode, End Use, and Region, 2026-2034

Asia Pacific Logistics Market Size, Share, Trends & Forecast (2026-2034)

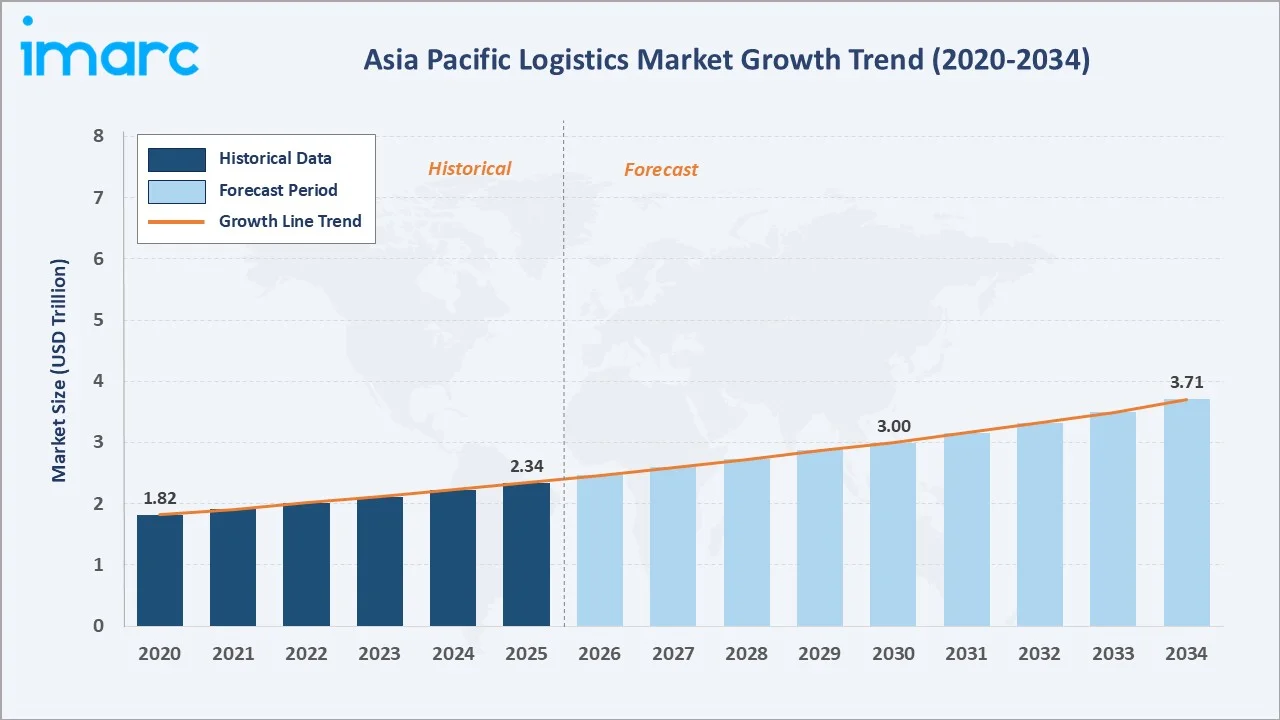

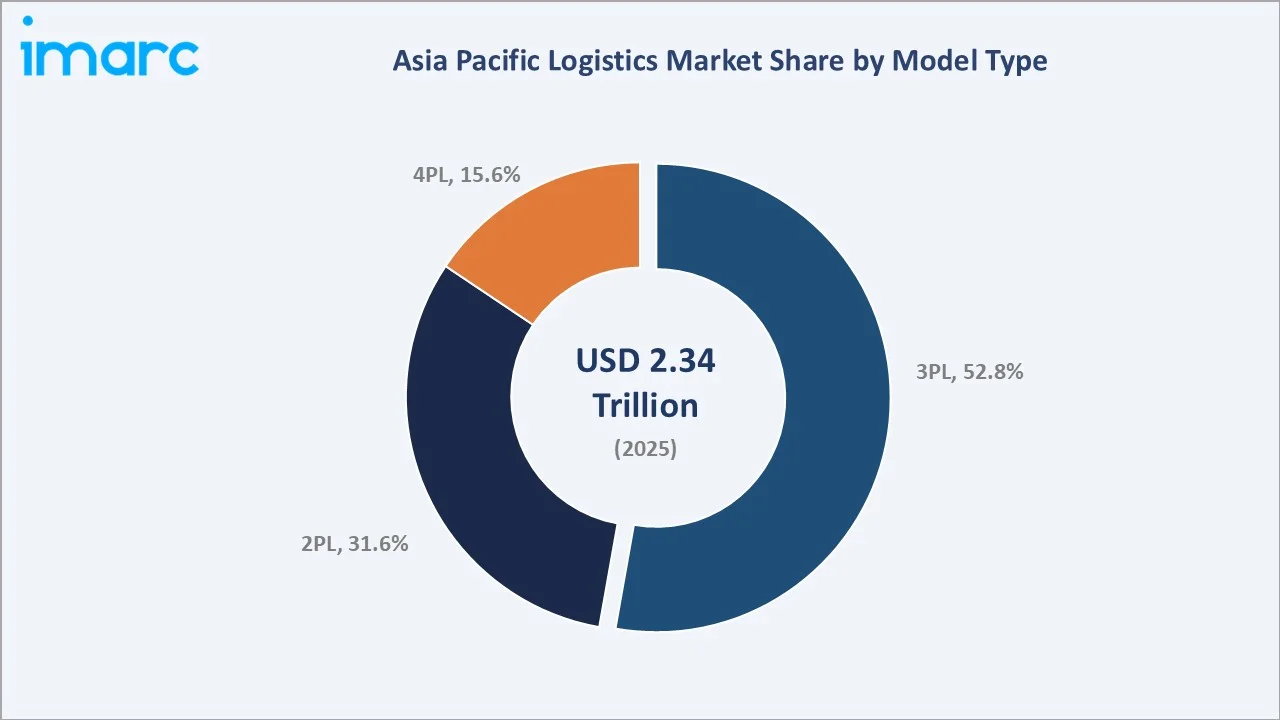

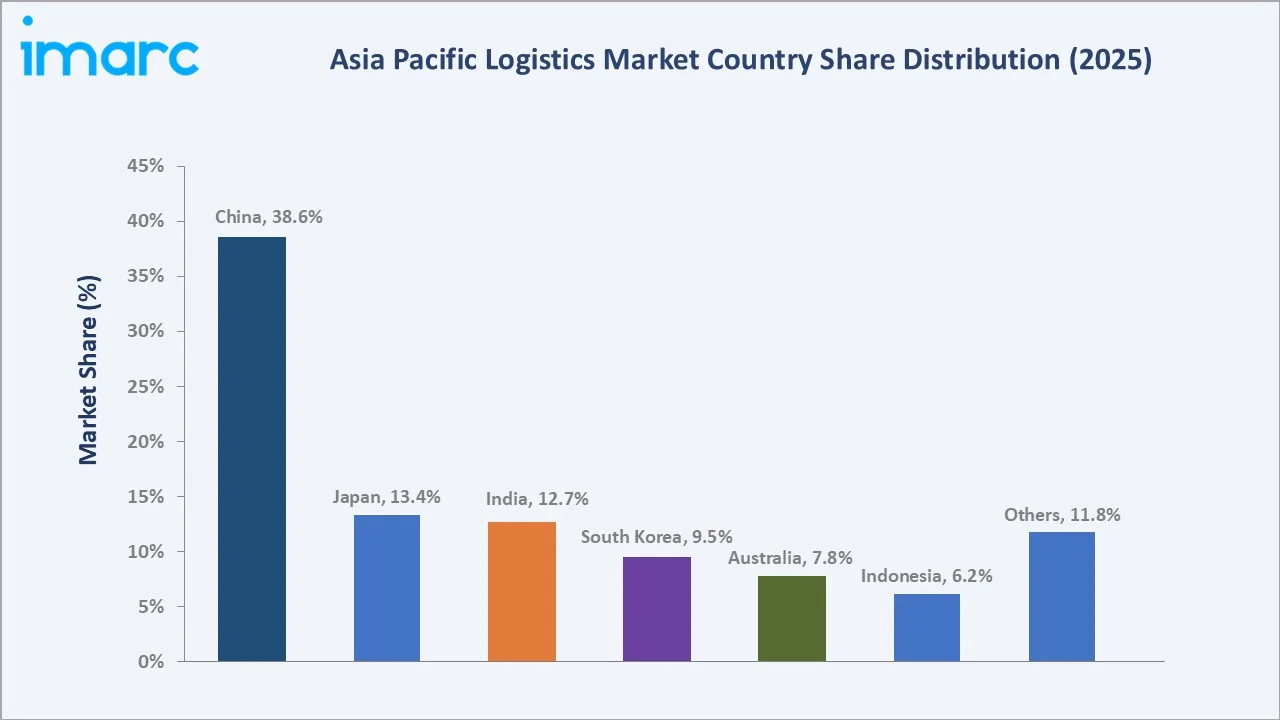

The Asia Pacific logistics market reached USD 2.34 Trillion in 2025 and is projected to reach USD 3.71 Trillion by 2034, growing at a CAGR of 5.11% during 2026-2034. The market is driven by rapid e-commerce growth, expanding manufacturing hubs, and increasing demand for efficient supply chain solutions across the region. Government initiatives like the National Logistics Policy, GatiShakti, GST, and Logistics Parks are driving the market by modernizing infrastructure, improving efficiency, and reducing operational costs. 3PL dominates the model type at 52.8%. Roadways lead the transport mode at 43.7%. China commands 38.6% of regional revenues.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 2.34 Trillion |

|

Forecast Market Size (2034) |

USD 3.71 Trillion |

|

CAGR (2026-2034) |

5.11% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Model Type |

3PL (52.8%, 2025) |

|

Dominant Transport Mode |

Roadways (43.7%, 2025) |

|

Leading Region |

China (38.6%, 2025) |

The market expanded from USD 1.82 Trillion in 2020 to USD 2.34 Trillion in 2025, anchored at USD 3.00 Trillion in 2030, and forecast to reach USD 3.71 Trillion by 2034. COVID-19's disruption of global supply chains created structural awareness of APAC logistics vulnerability and permanently elevated investment in supply chain resilience, redundancy, and digitalization, catalyzing 3PL and 4PL adoption as shippers recognized that specialized logistics providers could navigate supply chain complexity more effectively than in-house logistics functions.

To get more information on this market, Request Sample

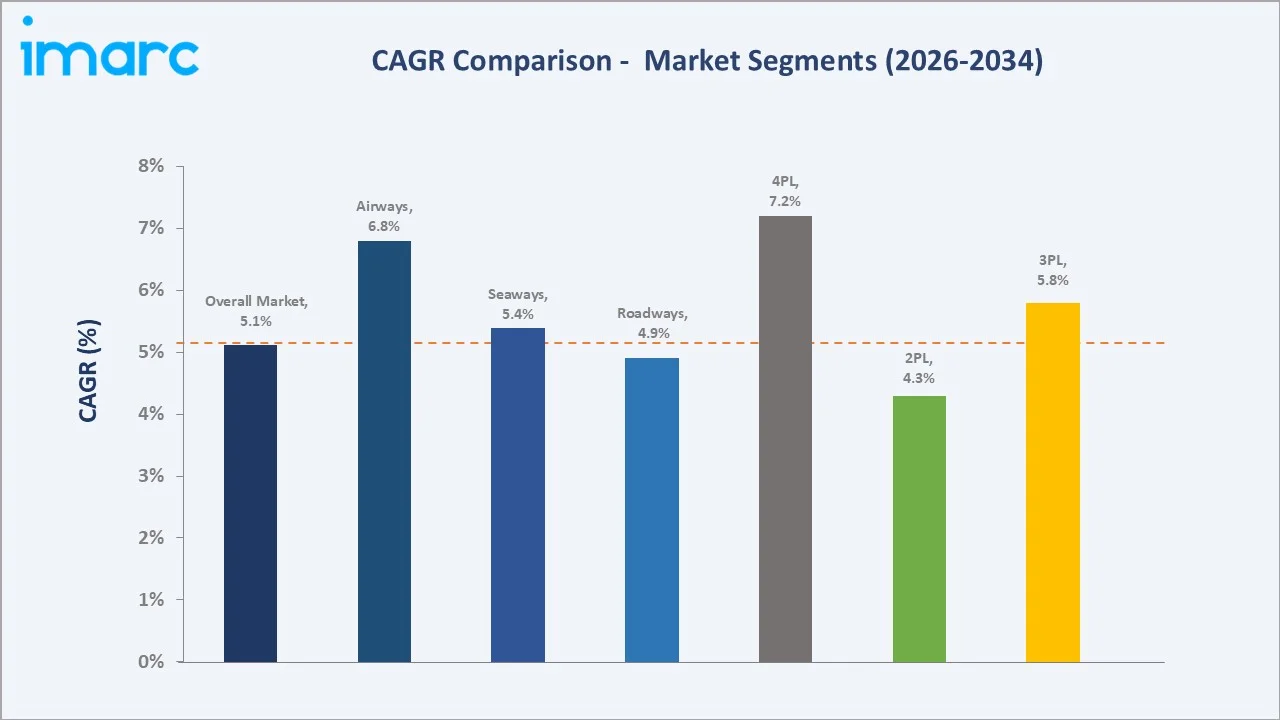

4PL model type grows fastest at ~7.2% CAGR (2026-2034), driven by AI-powered supply chain orchestration platforms that manage multiple 3PL providers, carriers, and warehouses as an integrated network on behalf of shippers who lack internal supply chain expertise. Airways grows at ~6.8% CAGR through APAC e-commerce's time-sensitive parcel demand and the premium pharmaceutical and semiconductor air freight market, driven by post-COVID supply chain security requirements.

Executive Summary

The Asia Pacific logistics market reached USD 2.34 Trillion in 2025, representing one of the world's largest regional logistics markets and one of the most complex, covering the world's most populous region, greatest geographic diversity, and most dynamic manufacturing and trade ecosystem. APAC handles most of the global container trade, global air freight, and generates 50%+ of global e-commerce transactions, making its logistics infrastructure the operational backbone of the global economy. The market is projected to reach USD 3.71 Trillion by 2034 at 5.11% CAGR.

3PL model type commands 52.8% market share (2025), reflecting the dominant role of third-party logistics providers in managing Asia Pacific's fragmented, multi-country supply chains across manufacturing, ocean freight, and distribution. Roadways at 43.7% reflects domestic distribution's dependence on trucking networks across all APAC markets, complemented by Seaways at 29.4% for the region's intra-Asian and global container shipping dominance. China, at 38.6%, is the market's structural anchor, reflecting the world's largest manufacturing economy's logistics intensity.

Key Market Insights

|

Insight |

Data |

|

Dominant Model Type |

3PL - 52.8% share (2025) |

|

Dominant Transport Mode |

Roadways - 43.7% market share (2025) |

|

Leading Region |

China - 38.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- 3PL at 52.8% anchored by APAC's multi-country manufacturing and distribution complexity requiring specialist orchestration: Asia Pacific's logistics complexity creates structural demand for specialized 3PL expertise that in-house logistics teams cannot maintain cost-effectively.

- Roadways at 43.7% reflecting domestic distribution's trucking dominance across APAC's diverse markets: Despite APAC's iconic ocean freight prominence, the majority of APAC logistics market value is generated in domestic distribution, the 'last thousand miles' from port or distribution center to retail store, factory, or consumer delivery address.

- China at 38.6% as APAC logistics anchor through manufacturing scale and digital logistics innovation: China's high logistics market is simultaneously the world's largest manufacturing source, largest e-commerce market, and most advanced domestic logistics ecosystem.

Asia Pacific Logistics Market Overview

The Asia Pacific logistics market encompasses all services involved in the planning, implementation, and control of the efficient flow and storage of goods, services, and information within the region, including freight forwarding (ocean, air, road, rail), contract logistics and warehousing (3PL/4PL), express and parcel delivery, cold chain and temperature-controlled logistics, customs brokerage, port and terminal handling, supply chain consulting, and digital logistics platform services. The market serves every industry vertical from electronics and automotive manufacturing through pharmaceutical cold chain, e-commerce fulfillment, and agricultural commodity bulk logistics.

The ecosystem integrates shippers (manufacturers, retailers, importers, exporters), freight forwarders and brokers, ocean carriers, air cargo carriers, road and rail operators, port and airport authorities, warehouse and distribution center operators, digital logistics platforms, customs and regulatory authorities across APAC jurisdictions, and end customers across residential, commercial, and industrial consumption points. Macroeconomic factors include robust economic growth, increasing trade activities, and the expansion of e-commerce, which demand more efficient, scalable, and cost-effective logistics solutions.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

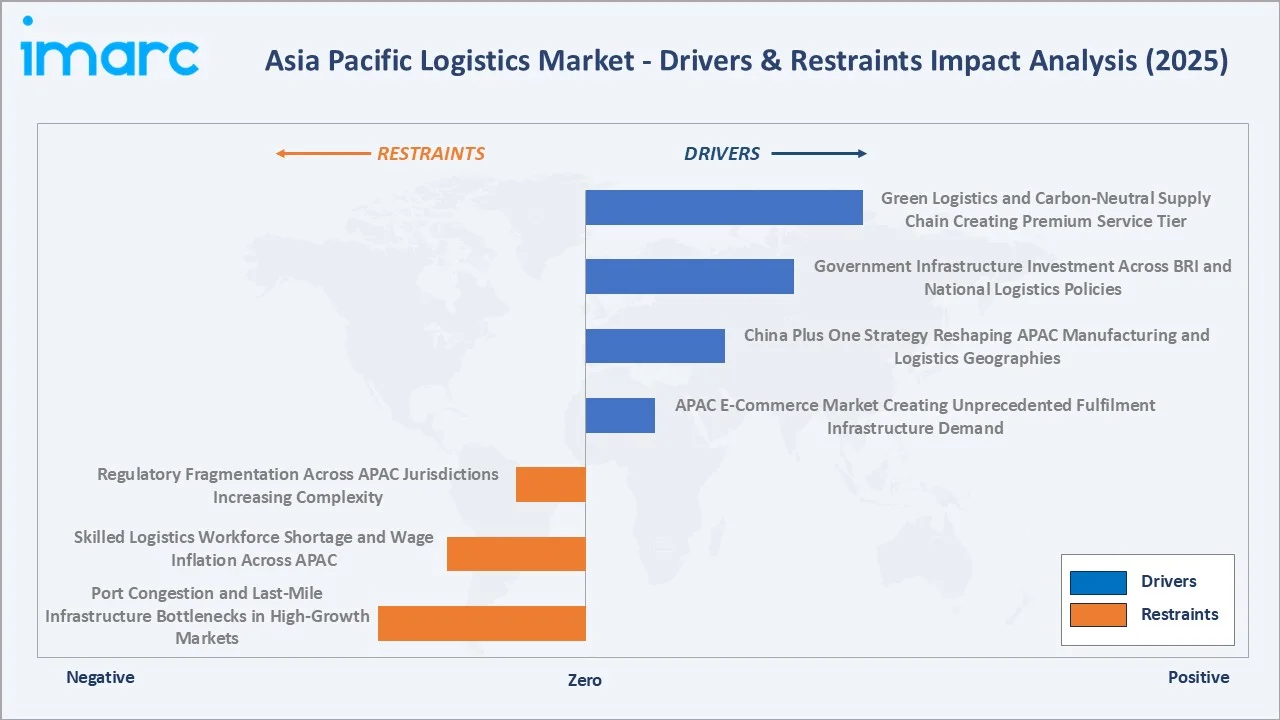

- APAC E-Commerce Market Creating Unprecedented Fulfilment Infrastructure Demand: Asia Pacific's e-commerce market growth is generating fulfillment, last-mile delivery, and returns logistics demand that is structurally the largest single driver of APAC logistics market growth.

- China Plus One Strategy (C+1) Reshaping APAC Manufacturing and Logistics Geographies: The China Plus One Strategy (C+1) is a supply chain approach that encourages businesses to diversify their supply chains beyond China to reduce risks. Introduced in 2013 in response to concerns over global reliance on China, it has gained traction amid trade tensions, COVID-19 disruptions, and increasing labor costs. The China Plus One Strategy is driving the market by increasing demand for alternative supply chain routes and logistics infrastructure across Southeast Asia and other regions to reduce dependence on China.

- Government Infrastructure Investment Across Belt and Road Initiative and National Logistics Policies: In 2025, the Belt and Road Initiative (BRI) reached its highest level of engagement, securing USD 128.4 billion in construction contracts and approximately USD 85.2 billion in investments, creating new port, railway, and road infrastructure that opens logistics corridors previously constrained by infrastructure capacity.

Market Restraints

- Port Congestion and Last-Mile Infrastructure Bottlenecks in High-Growth Markets: APAC's logistics infrastructure investment has consistently lagged demand growth, limited road network in rural areas, inadequate cold chain infrastructure in India beyond metro cities, irregular electricity supply affecting automated warehouse operations in Southeast Asia, constraining logistics efficiency improvement and increasing operating costs for 3PL providers expanding beyond primary markets.

- Skilled Logistics Workforce Shortage and Wage Inflation Across APAC: The shortage of skilled logistics workers and rising wage inflation across APAC are increasing operational costs and limiting the ability to meet the growing demand for efficient supply chain services. This talent gap and higher labor expenses are creating challenges for companies in maintaining productivity and scaling logistics operations effectively.

Market Opportunities

- Green Logistics and Carbon-Neutral Supply Chain Creating Premium Service Tier: APAC's largest shippers have committed to scope 3 supply chain emissions reduction targets, requiring logistics providers to offer verified carbon-neutral transport options. Asia Pacific's shipping decarbonization regulations will create structural demand for green logistics services that today represent a premium niche but will become mandatory requirements by 2030-2035.

- Southeast Asia's Digital Logistics Platform Ecosystem Enabling New Business Models: Southeast Asia's digital logistics platforms are creating digitally-integrated last-mile logistics networks that connect Southeast Asian consumers to e-commerce and quick commerce platforms with varying regulatory frameworks, payment systems, and infrastructure standards. These platforms are creating the Southeast Asia equivalent of what JD Logistics has done for China, enabling logistics revenue growth at GDP+ rates.

Market Challenges

- Regulatory Fragmentation Across APAC Jurisdictions Increasing Cross-Border Logistics Complexity: Asia Pacific's national regulatory frameworks create significant cross-border logistics complexity and cost that constrains the APAC single market integration that would unlock substantially higher logistics efficiency.

- Infrastructure Quality Disparity Between APAC's Advanced and Emerging Markets Creating Service Tier Imbalance: Logistics infrastructure quality varies enormously across APAC, while limited port infrastructure and port congestion represent constraining bottlenecks for multinational logistics providers seeking to offer pan-APAC standardized service quality.

Emerging Market Trends

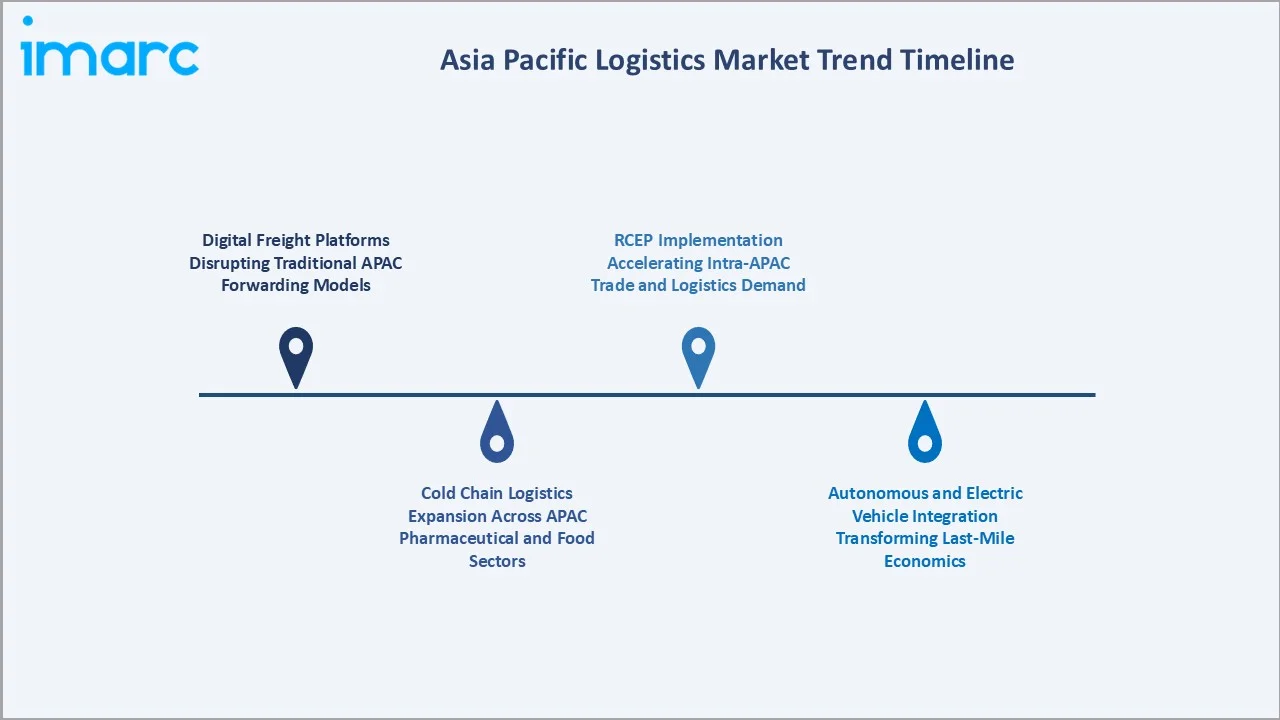

1. Digital Freight Platforms Disrupting Traditional APAC Forwarding Models

Digital freight platforms are disrupting traditional forwarding models in the logistics market by offering real-time tracking, streamlined booking processes, and increased transparency. These platforms enhance efficiency, reduce costs, and provide greater flexibility, enabling businesses to optimize their supply chains and meet the growing demand for faster, more reliable logistics solutions.

2. Cold Chain Logistics Expansion Across APAC Pharmaceutical and Food Sectors

The expansion of cold chain logistics across the APAC pharmaceutical and food sectors is driving growth in the region’s logistics market by ensuring the safe and efficient transportation of temperature-sensitive products. With rising demand for vaccines, perishable goods, and quality food products, the need for advanced cold storage and transportation infrastructure is increasing, creating new opportunities for logistics providers to innovate and scale their operations.

3. Autonomous and Electric Vehicle Integration Transforming Last-Mile Economics

The integration of autonomous and electric vehicles is transforming last-mile logistics by reducing operational costs, enhancing delivery speed, and improving sustainability. These innovations are streamlining urban deliveries, reducing carbon emissions, and addressing labor shortages, making last-mile delivery more efficient and eco-friendly in rapidly growing cities across the region.

4. RCEP Implementation Accelerating Intra-APAC Trade and Logistics Demand

The implementation of the Regional Comprehensive Economic Partnership (RCEP) is accelerating intra-APAC trade by reducing tariffs and trade barriers, driving increased logistics demand across the region. This trade agreement enhances supply chain efficiency and connectivity, fostering greater movement of goods, particularly in manufacturing and e-commerce sectors, while boosting demand for more advanced and streamlined logistics services.

Industry Value Chain Analysis

The Asia Pacific logistics value chain integrates shipper demand origination through freight forwarding, origin port/airport handling, carrier transit, destination warehousing and distribution, and final-mile delivery to consumers or commercial end users. 3PL providers capture 12-25% net margins on bundled services; freight forwarders earn 8-15% on forwarding fees; ocean and air carriers earn 15-30% depending on market conditions; and last-mile platforms earn 3-8% net margins on delivery revenues. Digital platforms increasingly extract value through data and platform fees independent of physical service margins.

|

Stage |

Key Participants |

|

Shipper Order & Booking |

FMCG, automotive, electronics, pharmaceutical, and retail shippers, TMS (Transportation Management System) platforms, and digital freight booking portals |

|

Freight Forwarding & Customs |

Global freight forwarding services, customs brokerage services, import/export documentation, and tariff optimization and duty management |

|

Origin Port/Airport Handling |

Major international ports and airports handling container and air cargo operations |

|

Carrier Transit (Ocean/Air/Road/Rail) |

Ocean carriers, rail services, air cargo providers; international and regional carriers offering full-load and less-than-container load (LCL) services, and specialized trucking networks |

|

Destination Warehouse & DC |

Supply chain and distribution centers, major APAC logistics parks, and automated sorting facilities |

|

Last-Mile Delivery to End Customer |

E-commerce logistics providers, urban micro-fulfillment centers, third-party logistics (3PL) integrated last-mile delivery platforms |

The destination warehouse and DC tier is the APAC logistics value chain's fastest-growing investment segment, driven by APAC e-commerce demanding automated sortation, climate-controlled pharmaceutical storage, and AI-driven inventory management that conventional trucking and port operators cannot provide.

Technology Landscape in the Asia Pacific Logistics Industry

AI-Powered Route Optimization and Demand Forecasting

AI-powered route optimization and demand forecasting are transforming logistics by enhancing efficiency and reducing costs. These technologies enable real-time decision-making, improving delivery accuracy, reducing fuel consumption, and optimizing resource allocation, while helping companies predict demand fluctuations and adjust logistics operations accordingly.

Blockchain and IoT Supply Chain Visibility

Blockchain and IoT are reshaping the logistics industry by enhancing supply chain visibility and transparency. Blockchain ensures secure, immutable records for real-time tracking of goods, while IoT devices provide real-time data on the condition and location of shipments, improving efficiency, reducing fraud, and enabling better decision-making across the supply chain.

Automation and Robotics in APAC Warehousing

Automation and robotics in APAC warehousing are transforming logistics by streamlining operations, reducing labor costs, and increasing throughput. These technologies enable faster, more accurate inventory management, order picking, and sorting, improving efficiency and scalability in response to growing demand for e-commerce and rapid deliveries.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Model Type | 3 PL | 52.8% | 2025 |

| Transportation Mode | Roadways | 43.7% | 2025 |

| End Use | 🔒 | 🔒 | 2025 |

| Region | China | 38.6% | 2025 |

By Model Type

3PL leads at 52.8% market share (2025). Third-party logistics providers manage contracted warehousing, transportation, customs brokerage, and value-added services (labeling, kitting, quality inspection) for shipper clients under multi-year contracts that generate predictable recurring revenues. APAC's 3PL market is highly fragmented.

To access detailed market analysis, Request Sample

2PL at 31.6% covers carrier-direct transportation services, shipping lines, air cargo carriers, trucking companies, and rail freight operators who provide basic transport without value-added supply chain management. 4PL at 15.6% grows fastest at ~7.2% CAGR, representing supply chain management orchestration services where the 4PL provider manages multiple 3PLs, carriers, and technology platforms as an integrated network.

By Transportation Mode

Roadways lead at 43.7% market share (2025). APAC's trucking market encompasses China's commercial trucks, India's commercial vehicles, Japan's trucks, and ASEAN's combined trucking fleet serving domestic distribution from production points and ports to retail and consumer endpoints. Cross-border road freight is growing as RCEP tariff reductions improve cross-border trucking economics.

Seaways at 29.4% generate APAC's highest-volume freight flows. Railways at 16.2% are growing through China's massive rail infrastructure investment and China Railway Express (CRE) expansion, and ASEAN's improving rail connectivity. Airways at 10.7% grow fastest at ~6.8% CAGR, driven by e-commerce time-sensitive parcel air freight, pharmaceutical cold chain air shipments, and semiconductor high-value component express logistics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

China |

38.6% |

Largest logistics market driven by e-commerce growth, advanced logistics platforms, and government-led infrastructure development connecting multiple regions. |

|

Japan |

13.4% |

Strong growth in logistics due to automation, parcel logistics expansion, and the need for efficient pharmaceutical supply chains. |

|

India |

12.7% |

Rapid growth driven by e-commerce, government initiatives to improve logistics infrastructure, and a focus on enhancing supply chain efficiency. |

|

South Korea |

9.5% |

Growth fueled by electronics supply chains, the expansion of autonomous logistics solutions, and cross-border logistics services across the region. |

|

Australia |

7.8% |

The expanding logistics market is due to vast geographic needs, growth in cold chain logistics for agricultural exports, and increasing demand for e-commerce solutions. |

|

Indonesia |

6.2% |

The growing logistics market is driven by its unique geographic challenges, multi-modal transport expansion, and rising e-commerce activities. |

|

Others |

11.8% |

The logistics market growth across Southeast Asia is driven by cross-border trade, e-commerce growth, and strategic infrastructure investments. |

China's 38.6% dominance reflects the structurally irreplaceable role of the world's factory and its domestic logistics infrastructure in APAC's total market. Japan's 13.4% reflects a mature, high-value logistics market undergoing structural automation-driven efficiency transformation as the logistics crisis driver shortages force industry-wide technology adoption.

India's 12.7% and fastest-growing major market position reflects the world's most compelling near-term logistics investment opportunity. South Korea (9.5%), Australia (7.8%), and Indonesia (6.2%) represent distinct market archetypes. South Korea's tech-manufacturing logistics specialization, Australia's commodity export and urbanized e-commerce logistics, and Indonesia's archipelago geography challenge and massive ASEAN opportunity positioning.

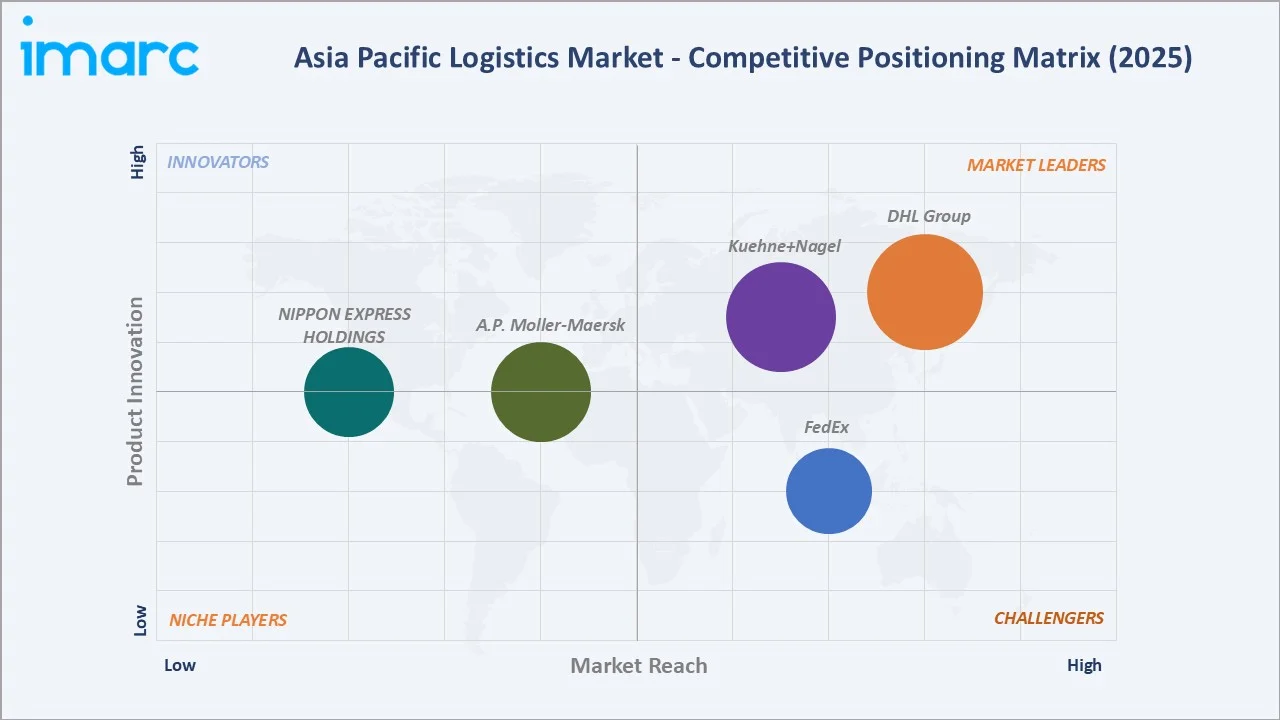

Competitive Landscape

The Asia Pacific logistics market is moderately fragmented at the premium 3PL and international freight forwarding level, and highly fragmented at the domestic road freight, last-mile, and regional logistics level. Global logistics conglomerates control approximately 15-20% of total APAC logistics revenues, while national champions and regional specialists collectively serve 40-50% of the market. The remaining 35-40% is served by thousands of small and mid-size trucking companies, freight brokers, customs agents, and local warehousing operators across APAC.

|

Company Name |

Brands |

Market Position |

Core Strength |

|

DHL Group |

DHL Supply Chain |

Market Leader |

One of the largest logistics companies in APAC |

|

Kuehne+Nagel |

Kuehne+Nagel |

Market Leader |

With close to 85,000 employees at almost 1,300 sites in close to 100 countries, the Kuehne+Nagel Group is one of the world's leading logistics providers. |

|

FedEx |

FedEx Express |

Strong Challenger |

Its extensive global network, advanced technology integration, and the ability to provide reliable, fast, and efficient shipping solutions. |

|

A.P. Moller - Maersk |

Maersk |

Established Player |

Maersk offers global and local logistics solutions that enable small and large businesses to grow. |

|

NIPPON EXPRESS HOLDINGS |

Nippon Express |

Established Player |

Using Nippon Express's warehouse and delivery network, which covers more than 50 countries, they provide comprehensive logistics services that extend beyond storage and delivery. |

The competitive landscape is being reshaped by Maersk's strategic pivot from pure ocean carrier to integrated logistics provider and by the emergence of APAC-born logistics unicorns that are building digitally-native last-mile networks across Southeast Asia, competing with established global 3PLs in the fastest-growing APAC logistics sub-market.

Key Company Profiles

DHL Group

DHL Group, known for its DHL Supply Chain, Asia Pacific’s one of the largest logistics providers by revenue and geographic footprint, operating facilities across APAC countries as part of Deutsche Post DHL Group's global revenue organization.

- Brand: DHL Supply Chain

- Recent Developments: DHL Group will invest EUR 1 billion across all its business units in India by 2030. This investment reflects DHL's confidence in India's dynamic market and aligns with its Strategy 2030 to accelerate sustainable growth.

- Strategic Focus: Expanding its regional infrastructure, enhancing e-commerce logistics capabilities, and leveraging digitalization and automation.

Kuehne+Nagel

Kuehne+Nagel, with close to 85,000 employees at almost 1,300 sites in close to 100 countries, is one of the world's leading logistics providers.

- Brand: Kuehne+Nagel

- Recent Developments: In February 2026, Kuehne+Nagel opened a new, built-to-suit 3,500 sqm Container Freight Station (CFS) in Mumbai. This facility reinforces its Sea Logistics capabilities in India and supports the country’s expanding trade ecosystem.

- Strategic Focus: Expanding its presence in key regional hubs, enhancing its air, sea, and road transport networks, and focusing on e-commerce and digital logistics solutions.

Market Concentration Analysis

The Asia Pacific logistics market is moderately fragmented, and global 3PLs and freight forwarders collectively account for 15-18% of total APAC logistics revenues. National champions account for an additional 10-15%. The remaining 67-75% is served by regional and local logistics providers ranging from mid-size ASEAN logistics conglomerates to millions of small trucking and last-mile delivery operators across APAC's diverse markets.

Market concentration is higher in specific segments. The premium APAC international freight forwarding market is served by the top 10 forwarders, handling 60%+ of volume. The APAC automotive sector 3PL is heavily concentrated among Japanese and Korean 3PLs serving Japanese and Korean OEM supply chains. APAC pharmaceutical cold chain logistics is dominated by DHL Life Sciences, Kuehne+Nagel Pharma, and Nippon Express, with specialised GDP-compliant infrastructure that creates high barriers to entry.

Investment & Growth Opportunities

Fastest Growing Segments

4PL model type (~7.2% CAGR), airways (~6.8% CAGR), pharmaceutical cold chain (~9-12% CAGR), Southeast Asia digital last-mile (~15%+ CAGR), and India logistics (~8-10% CAGR) represent the Asia Pacific logistics market's highest-growth investment vectors through 2034. India's logistics market represents the single most attractive large-market growth opportunity in APAC.

Emerging Market Opportunities

Southeast Asia's logistics infrastructure investment gap is the region's most underserved market opportunity. Vietnam, Indonesia, Philippines, Thailand, Malaysia, and Cambodia collectively are receiving high manufacturing FDI through 2030, but Grade A logistics warehouse capacity in these markets is 30-50% below demand, creating significant development opportunity for logistics real estate developers and 3PL operators willing to invest in non-primary market facilities.

Investment Themes

- India logistics infrastructure and 3PL development: India's National Logistics Policy-aligned investments represent a high logistics infrastructure capital opportunity through 2030. Foreign 3PL operators are competing for anchor tenant status in MMLPs, creating facility development opportunities for logistics park developers with government partnerships.

- Southeast Asia digital logistics platform development: Southeast Asia's consumers represent the world's largest underserved digital logistics platform market.

Future Market Outlook (2026-2034)

The Asia Pacific logistics market is projected to grow from USD 2.34 Trillion in 2025 to USD 3.71 Trillion by 2034, delivering a 5.11% CAGR and USD 1.37 Trillion in absolute market value addition over the forecast period. The market's anchor value of USD 3.00 Trillion in 2030 represents an APAC logistics industry that has absorbed the structural changes initiated by COVID-19 supply chain disruption, China+1 manufacturing diversification, and e-commerce fulfillment normalization, emerging as a more distributed, digitally integrated, and sustainability-aware industry.

Three structural forces define the Asia Pacific logistics market's trajectory with high certainty through 2034: APAC's e-commerce market growth; the China+1 manufacturing diversification megatrend creating high cumulative manufacturing investment, each investment generating proportional logistics infrastructure demand in markets where Grade A warehousing, cold chain, and multimodal logistics are severely undersupplied; and the APAC logistics industry's own digital transformation, through AI-powered 4PL platforms, autonomous warehouse technology, and digital freight marketplaces, improving operating leverage and enabling market participants to serve growing volumes with proportionally lower cost increases.

Research Methodology

Primary Research

Primary research comprised structured interviews with 80+ industry stakeholders (2025), including Regional Vice Presidents from market players; country logistics directors from major shippers; port authority commercial directors at PSA Singapore, Shanghai International Port Group (SIPG), and Busan Port Authority; government logistics policy officials from Singapore EDB, India DPIIT, and Japan Ministry of Land, Infrastructure, Transport and Tourism; and APAC logistics real estate executives from GLP, ESR, and Goodman Group.

Secondary Research

Secondary research encompassed World Bank Logistics Performance Index (LPI) 2025, APEC Supply Chain Connectivity Framework assessments, CFLP (China Federation of Logistics & Purchasing) annual survey 2024, India Ministry of Commerce NLP implementation reports, Japan Ministry of Land Logistics Census 2025, Agility Emerging Markets Logistics Index 2025, Armstrong & Associates Global 3PL Market Size report, Drewry Freight Forwarder Benchmarking Study 2025, company investor relations and annual reports. Over 140 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using bottom-up country-level GDP-logistics intensity models calibrated against World Bank LPI scores, IMF GDP projections by APAC country, APAC e-commerce growth projections (eMarketer, Euromonitor), China+1 manufacturing FDI trajectory models (UNCTAD FDI data), BRI infrastructure investment-to-trade-flow conversion ratios, and 3PL/4PL market share trajectory models based on Armstrong & Associates historical 3PL penetration growth data. Key inputs include RCEP tariff reduction schedule impacts on intra-APAC trade volumes, India NLP implementation milestone timelines, APAC port capacity development plans, and aviation cargo capacity.

Asia Pacific Logistics Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Trillion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Model Types Covered | 2 PL, 3 PL, 4 PL |

| Transportation Modes Covered | Roadways, Seaways, Railways, Airways |

| End Uses Covered | Manufacturing, Consumer Goods, Retail, Food and Beverages, IT Hardware, Healthcare, Chemicals, Construction, Automotive, Telecom, Oil and Gas, Others |

| Regions Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Companies Covered | DHL Group, Kuehne+Nagel, FedEx, A.P. Moller - Maersk, NIPPON EXPRESS HOLDINGS, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Asia Pacific logistics market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Asia Pacific logistics market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Asia Pacific logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Asia Pacific Logistics Market Report

The Asia Pacific logistics market reached USD 2.34 Trillion in 2025, representing the world's largest regional logistics market, driven by APAC's e-commerce market, China's manufacturing dominance, China+1 supply chain diversification to ASEAN, and government infrastructure investments across the Belt and Road Initiative and national logistics policies.

The market grows at 5.11% CAGR during 2026-2034, reaching USD 3.71 Trillion by 2034, driven by India's fastest-growing major APAC logistics market, Southeast Asia's manufacturing FDI logistics demand, APAC e-commerce fulfillment growth, and supply chain orchestration adoption.

3PL leads at 52.8% through DHL, Kuehne+Nagel, Nippon Express, and other players managing complex multi-country APAC supply chains.

Roadways lead at 43.7% through APAC's combined trucking market, serving domestic distribution across all APAC markets.

China leads at 38.6%, anchored by the world's largest manufacturing economy and Belt and Road Initiative cross-border freight development.

Leading companies include DHL Group, Kuehne+Nagel, FedEx, A.P. Moller – Maersk, and NIPPON EXPRESS HOLDINGS, among others.

The market is projected to reach approximately USD 3.00 Trillion by 2030, with India emerging as APAC's second-largest absolute-growth market, Vietnam's logistics market growth, 4PL market exceeding through AI orchestration adoption, and China's logistics completing its transition from manufacturing-led to e-commerce-led demand structure.

China+1 strategy has driven multinationals to establish or expand in Vietnam, India, Thailand, Indonesia, and Malaysia, creating new freight corridors, warehouse demand, and 3PL contract opportunities in markets previously peripheral to APAC logistics investment.

4PL (Fourth-Party Logistics) at 15.6% growing at ~7.2% CAGR represents AI-powered supply chain orchestration managing multiple 3PLs, carriers, and warehouses for complex multinational clients.

NLP targets reducing India's logistics cost by 2030. This creates 50+ million sq.ft. of Grade A warehouse development and makes India the world's most attractive greenfield 3PL investment market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)