Asia Pacific Welding Consumables Market Size, Share, Trends and Forecast by Product, Welding Technique, End Use Industries, and Country, 2026-2034

Asia Pacific Welding Consumables Market Summary:

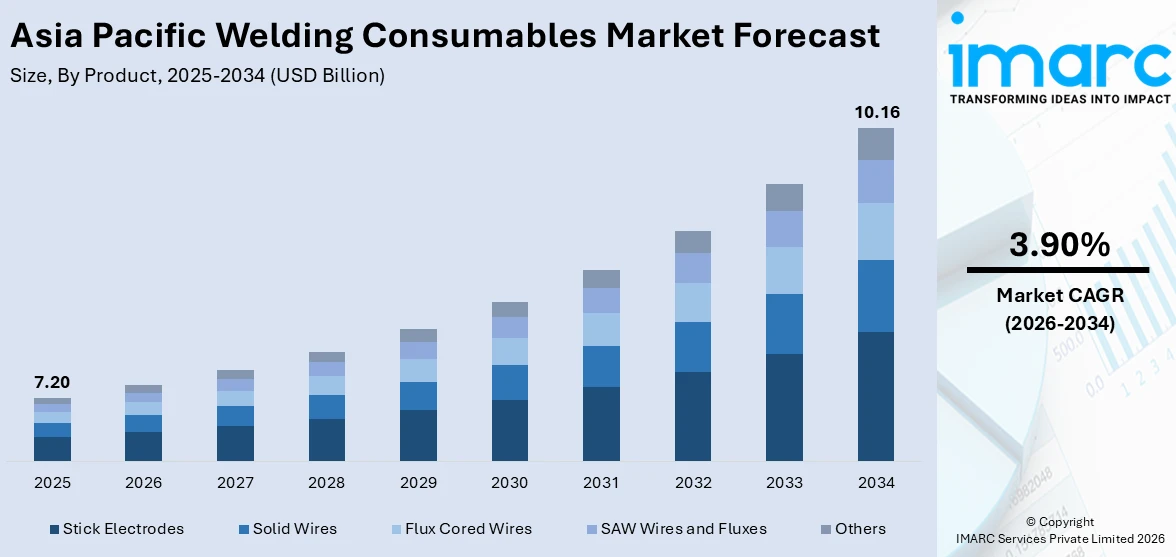

The Asia Pacific welding consumables market size was valued at USD 7.20 Billion in 2025 and is projected to reach USD 10.16 Billion by 2034, growing at a compound annual growth rate of 3.90% from 2026-2034.

The Asia Pacific welding consumables market is expanding steadily, driven by rapid industrialization and urbanization across major economies. Growing infrastructure investments, rising automotive production, and expanding shipbuilding activities are fueling demand for diverse welding materials. Technological advancements in precision welding, increasing adoption of automated welding systems, and heightened focus on sustainable manufacturing practices are further accelerating the Asia Pacific welding consumables market share.

Key Takeaways and Insights:

- By Product: Stick electrodes dominate the market with a share of 30% in 2025, owing to their cost-effectiveness, portability, and versatility across outdoor and remote welding applications. Widespread use in construction, shipbuilding, and pipeline projects is fueling the segment expansion.

- By Welding Technique: Arc welding leads the market with a share of 45% in 2025, driven by its extensive adoption across heavy industries, including infrastructure development, shipbuilding, and pipeline fabrication. Minimal equipment requirements and adaptability in varied conditions strengthen its dominance.

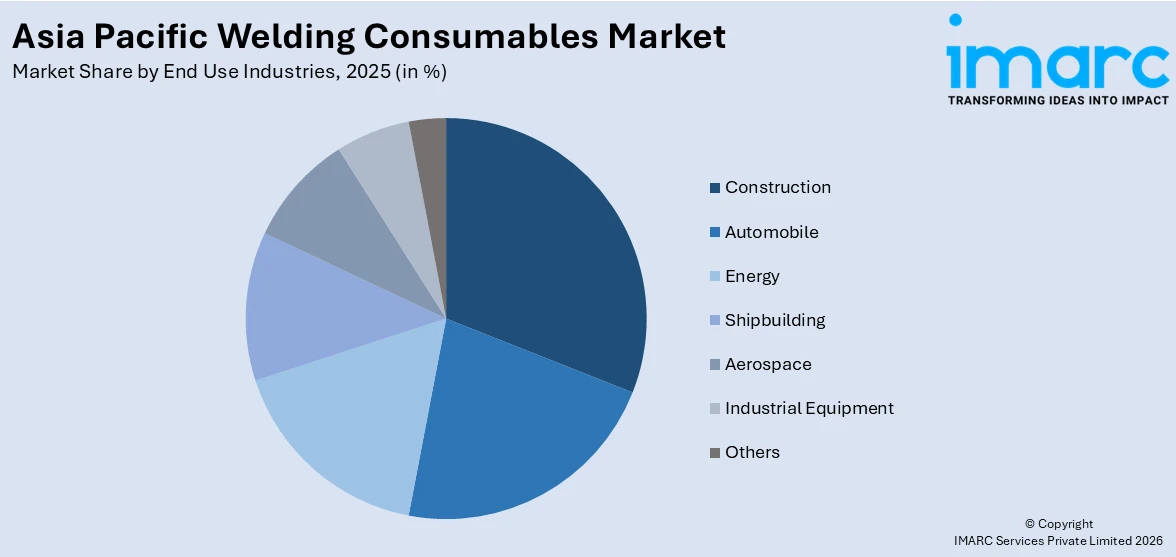

- By End Use Industries: Construction represents the largest segment with a market share of 26% in 2025, reflecting the massive infrastructure investments across Asia Pacific economies. Rising urbanization, expanding commercial real estate development, and government-funded public works programs sustain robust demand.

- Key Players: Key players drive the Asia Pacific welding consumables market by expanding product portfolios, advancing automation-compatible consumables, strengthening regional manufacturing capabilities, and investing in research and development. Their strategic partnerships and distribution network expansion ensure consistent product availability across diverse industrial segments.

To get more information on this market Request Sample

The Asia Pacific welding consumables market is experiencing robust growth as economies across the region invest heavily in infrastructure modernization, industrial expansion, and advanced manufacturing capabilities. China remains the dominant consumer, driven by its massive construction sector, shipbuilding industry, and government-backed manufacturing upgrades under strategic industrial policies. Japan and South Korea contribute through demand for precision welding solutions in aerospace, automotive, and electronics manufacturing. The rising adoption of robotic and automated welding systems is accelerating demand for premium consumables with tighter chemical tolerances and enhanced arc stability. Additionally, the growing emphasis on eco-friendly welding practices, including low-fume electrodes and copper-free welding wires, is reshaping product development priorities across the region. Expanding renewable energy infrastructure, particularly wind and solar installations, is creating sustained demand for specialized welding materials suitable for high-performance and corrosion-resistant applications.

Asia Pacific Welding Consumables Market Trends:

Rising Adoption of Automation and Robotic Welding Systems

The Asia Pacific welding consumables market is witnessing a significant shift toward automated and robotic welding processes, particularly in automotive, electronics, and heavy fabrication sectors. Manufacturers are increasingly deploying collaborative robots and multi-axis robotic welding cells to improve precision, reduce rework, and address skilled labor shortages. In April 2024, Daihen Corporation acquired Rolan Robotics, a global leader in robotic systems, to expand its portfolio of robotic welders for the metal and broader industrial sectors. This automation trend is driving demand for premium, automation-ready consumables with consistent chemical compositions and superior arc stability.

Growing Shift Toward Eco-Friendly and Low-Fume Consumables

Environmental regulations across the region are accelerating demand for low-emission welding consumables, including low-spatter electrodes, copper-free welding wires, and reduced-fume flux-cored wires. Industrially advanced economies such as China, Japan, and South Korea are enforcing stricter workplace air quality standards, compelling fabricators to adopt cleaner welding solutions. Manufacturers are increasingly developing environmentally responsible formulations that minimize harmful fume generation while maintaining weld integrity and performance. The growing emphasis on occupational health and sustainable manufacturing practices is influencing product development strategies and reshaping the Asia Pacific welding consumables market growth.

Integration of Advanced Precision Welding Technologies

Precision welding technologies, including laser welding, electron beam welding, and hybrid laser-arc processes, are gaining traction across aerospace, defense, and electric vehicle manufacturing sectors. These advanced techniques require specialized consumables and protective materials, opening new market avenues. In March 2024, researchers at the Korea Electrotechnology Research Institute achieved a breakthrough in electron beam welding, developing a high-performance electron gun with world-class power of 60 kW and acceleration voltage of 120 kV, enabling defect-free welding of thick materials for nuclear power and aerospace applications.

Market Outlook 2026-2034:

The Asia Pacific welding consumables market is positioned for sustained growth over the forecast period, underpinned by large-scale infrastructure development programs, expanding automotive and shipbuilding industries, and increasing investments in renewable energy projects. The continued modernization of manufacturing capabilities across China, India, Japan, South Korea, and Southeast Asian economies is driving demand for high-performance welding materials. Technological advancements in automated welding processes, precision joining techniques, and eco-friendly consumable formulations are reshaping industry dynamics. Rising government expenditure on transportation corridors, energy pipelines, smart city initiatives, and defense modernization is expected to generate substantial demand for specialized welding consumables, positioning the region as a leading global hub for welding material consumption. The market generated a revenue of USD 7.20 Billion in 2025 and is projected to reach a revenue of USD 10.16 Billion by 2034, growing at a compound annual growth rate of 3.90% from 2026-2034.

Asia Pacific Welding Consumables Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Stick Electrodes |

30% |

|

Welding Technique |

Arc Welding |

45% |

|

End Use Industries |

Construction |

26% |

Product Insights:

- Stick Electrodes

- Solid Wires

- Flux Cored Wires

- SAW Wires and Fluxes

- Others

Stick electrodes dominate with a market share of 30% of the total Asia Pacific welding consumables market in 2025.

Stick electrodes maintain their leading position in the Asia Pacific welding consumables market due to their affordability, ease of use, and exceptional adaptability in challenging environments. These consumables do not require external shielding gas, making them ideal for outdoor construction sites, remote infrastructure projects, and shipyard operations. Their portability and minimal equipment requirements make them a preferred choice for small and medium enterprises across developing economies such as India, Indonesia, and Vietnam, where manual welding remains widely prevalent in building and repair applications.

The sustained demand for stick electrodes is further reinforced by massive infrastructure development and pipeline construction activities across the region. Chinese engineering, procurement, and construction contractors working on Belt and Road Initiative projects favor electrodes certified to international standards for seismic-grade structures, stimulating premium electrode sales. In Japan, ongoing renovation of aging infrastructure, including railways and bridges, supports steady consumption. The growing emphasis on low-hydrogen electrode formulations for critical welding applications in energy and defense sectors is also contributing to segment resilience.

Welding Technique Insights:

- Arc Welding

- Resistance Welding

- Oxyfuel Welding

- Ultrasonic Welding

- Others

Arc welding leads with a share of 45% of the total Asia Pacific welding consumables market in 2025.

Arc welding maintains its commanding position across the Asia Pacific region due to its extensive adoption in heavy industries such as shipbuilding, pipeline construction, structural fabrication, and infrastructure development. The technique offers versatility across various material types and thicknesses, making it indispensable for large-scale industrial operations. In Southeast Asian countries like Indonesia and Vietnam, shielded metal arc welding remains the preferred method among small and medium enterprises due to its minimal equipment requirements and operational simplicity, supporting consistent consumable demand throughout diverse manufacturing environments.

The dominance of arc welding is further strengthened by the integration of automation and Industry 4.0 principles into fabrication workflows. Japanese shipyards extensively rely on arc welding techniques, with industry assessments indicating that welding operations in these facilities employ arc-based processes due to their adaptability in both indoor and outdoor conditions. The growing adoption of gas metal arc welding and gas tungsten arc welding in precision-dependent sectors such as electronics, aerospace, and electric vehicle manufacturing is expanding the technique's application scope.

End Use Industries Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Automobile

- Energy

- Shipbuilding

- Aerospace

- Industrial Equipment

- Others

The construction exhibits a clear dominance with a 26% share of the total Asia Pacific welding consumables market in 2025.

The construction sector's leadership in welding consumable consumption is driven by unprecedented infrastructure development across Asia Pacific economies. Massive investments in residential buildings, commercial complexes, bridges, highways, and railway networks generate sustained demand for structural steel fabrication and associated welding operations. China's extensive urban development programs, encompassing large-scale residential construction, commercial infrastructure expansion, and transportation network upgrades, exemplify the scale of construction activity sustaining welding consumable demand throughout the region.

Government-funded infrastructure initiatives further reinforce the construction sector's dominant position. India's Smart Cities Mission and Bharatmala Pariyojana highway development program are generating substantial demand for durable welding solutions across road, bridge, and urban infrastructure projects. Smart city developments across multiple Asia Pacific nations are increasing the need for high-quality welding consumables for structural steel applications. The ongoing emphasis on earthquake-resistant construction standards in seismically active regions such as Japan and Indonesia necessitates specialized welding techniques and premium consumable materials.

Country Insights:

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

China currently has the largest market share in the Asia Pacific market for welding consumables due to its huge manufacturing base, infrastructure development, and overall steel production and shipbuilding capacity. The Dual Circulation approach adopted by the Chinese government emphasizes the need for modernization of its manufacturing base, thereby increasing investments in automation and advanced welding technology. The availability of local raw materials and lower production costs for electrodes further accentuate China's leadership position in the consumption and export of welding consumables in the Asia Pacific market.

The market for welding consumables in Japan is marked by stable demand for high-quality, high-precision welding consumables due to the presence of advanced automotive manufacturing, aerospace engineering, and shipbuilding industries. The country's emphasis on innovation in technology, such as laser welding and hydrogen fuel cell assembly, further helps to create demand for specialty welding consumables.

The Indian market is poised to be one of the fastest-growing in the welding consumables industry, driven by the country's rapid urbanization, growing construction activities, and the government's support for infrastructure development. Initiatives like the National Infrastructure Pipeline and Make in India are fueling major investments in infrastructure development, including road development, railway development, energy, and housing. The country's growing automobile manufacturing industry and adoption of advanced welding technology are also driving the demand for various welding consumable products.

The demand for welding consumables in South Korea is driven by the country's world-leading shipbuilding industry and its advanced automobile and electronics manufacturing industries. The country has won a major share of the world's shipbuilding orders in the past few years, ensuring strong demand for flux cored wires and solid wires used in shipbuilding. The country's government support for the adoption of robotic welding is also fueling the demand for automation-compatible welding consumables.

The welding consumables market in Australia is fueled by the mining, oil & gas, and infrastructure development industries. Large-scale investments in mining activities, gas pipeline development, and infrastructure development create a steady demand for robust welding consumables. Australia's emphasis on developing renewable energy projects, such as wind and solar farms, is opening up new opportunities for high-performance welding consumables designed to withstand harsh climatic conditions.

The growing manufacturing base and infrastructure development activities in Indonesia are fueling the demand for welding consumables. Indonesia's shipbuilding industry, growing automotive industry, and government investments in infrastructure development, including transportation networks and industrial estates, are increasing demand. The prevalence of manual and semi-automated welding practices in small and medium-scale enterprises maintains strong demand for economical stick electrodes and solid wires.

Market Dynamics:

Growth Drivers:

Why is the Asia Pacific Welding Consumables Market Growing?

Rapid Infrastructure Development and Urbanization Across Key Economies

The Asia Pacific welding consumables market is experiencing significant growth driven by unprecedented infrastructure development and urbanization across major economies. Countries throughout the region are investing heavily in transportation corridors, energy pipelines, commercial buildings, housing complexes, and smart city initiatives that require extensive structural steel fabrication and welding operations. India's National Infrastructure Pipeline targets investments of nearly USD 1.4 Trillion across various infrastructure categories, directly generating massive demand for welding consumables. China continues to pursue large-scale urban renewal programs and Belt and Road Initiative projects that intensify steel consumption and associated welding requirements. Southeast Asian nations, including Indonesia, Vietnam, and the Philippines, are accelerating infrastructure modernization through government-funded public works programs. The expanding construction of bridges, railways, airports, and industrial facilities across these economies creates sustained demand for diverse welding materials, positioning infrastructure development as the primary growth engine for the regional welding consumables market.

Expanding Automotive and Electric Vehicle Manufacturing

The automotive sector's rapid expansion across Asia Pacific is generating substantial demand for welding consumables used in vehicle body assembly, chassis fabrication, and component manufacturing. The transition toward electric vehicle production is introducing new welding requirements, particularly for battery pack assembly, motor housing fabrication, and lightweight material joining. China's electric vehicle industry has significantly driven adoption of advanced welding techniques, with industry assessments indicating that the majority of new electric vehicle models launched in recent years incorporate laser-welded components for superior weld quality and thermal efficiency. Japan and South Korea's automotive manufacturers continue to invest in robotic welding systems that require premium consumables with tight chemical tolerances. India's growing automotive manufacturing base is further contributing to market expansion. The rising production volumes across passenger vehicles, commercial vehicles, and electric mobility platforms collectively sustain robust demand for specialized welding consumables throughout the region.

Growth in Renewable Energy and Power Generation Infrastructure

The expanding renewable energy sector across Asia Pacific is creating significant demand for specialized welding consumables used in wind turbine manufacturing, solar panel mounting structures, and power transmission infrastructure. Countries throughout the region are pursuing ambitious clean energy targets that require extensive fabrication and installation work. India added 24.5 GW of solar capacity and 3.4 GW of wind capacity in 2024, supported by initiatives such as the PM Surya Ghar Muft Bijli Yojana and green hydrogen policies, generating substantial demand for corrosion-resistant and high-strength welding materials. Japan's hydrogen economy initiatives, including plans to deploy fuel cell vehicles and expand hydrogen infrastructure, are spurring demand for high-purity welding consumables for fuel cell stack assembly. The construction of offshore wind farms, hydroelectric facilities, and nuclear power plants across the region further drives consumption of premium welding materials suitable for demanding operational environments and stringent safety standards.

Market Restraints:

What Challenges the Asia Pacific Welding Consumables Market is Facing?

Raw Material Price Volatility and Supply Chain Disruptions

Fluctuating prices of essential raw materials such as steel, nickel, aluminum, rutile, and manganese significantly impact the welding consumables market. These price variations create cost pressures for manufacturers, disrupt production planning, and affect overall profitability. The dependence on imported specialized materials for high-performance consumables, particularly in the aviation and nuclear power sectors, further compounds supply chain vulnerabilities and pricing instability across the region.

Shortage of Skilled Welders and Technical Workforce

The growing gap between demand for qualified welders and the available skilled workforce presents a significant challenge for the welding consumables market. Many developing economies face insufficient training infrastructure and declining interest among younger workers in manual welding occupations. This shortage constrains manufacturing capacity, delays project timelines, and creates inconsistencies in weld quality, ultimately impacting consumable demand patterns and market growth potential.

Competition from Alternative Joining Technologies

Emerging joining technologies such as friction stir welding, adhesive bonding, and mechanical fastening are gradually reducing reliance on traditional welding consumables in certain applications. Friction stir welding eliminates the need for filler metals in aluminum and mixed-material joints, posing a structural challenge to conventional consumable demand. The automotive and aerospace sectors are increasingly adopting these alternative techniques for lightweight material assembly, which may constrain long-term growth prospects for traditional welding consumable categories.

Competitive Landscape:

The Asia Pacific market for welding consumables is observed to have a moderately competitive environment, with global giants competing alongside regional and local players. The key strategies adopted by players in this market include innovation, geographical expansion, and acquisitions to enhance their market position. The development of automation-compatible welding consumables, low-emission welding consumables, and specialty materials for new applications such as electric vehicle production and renewable energy is expected to increase the level of competitiveness. Collaborations between welding consumable suppliers and end-use industries are expected to promote the development of customized products, while the expansion of manufacturing and distribution infrastructure is expected to enable market penetration in developing countries.

Recent Developments:

- In January 2025, voestalpine Bohler Welding announced the expansion of its local business activities in India, having invested over EUR 3 Million across its three locations in Bhiwadi, Thane/Mumbai, and Delhi over the past five years. The expansion strengthens production of welding consumables and application technology to serve customers in energy, construction, chemical processing, and transportation sectors, with future plans to add solid wire production to boost local manufacturing.

- In October 2024, Larsen & Toubro secured a significant order from the ITER Organization to deploy advanced welding technologies for assembling the ITER Tokamak vacuum vessel at the world's largest nuclear fusion project in Cadarache, Southern France. The company also signed an MoU for technical collaboration, showcasing India's expertise in high-tech welding and manufacturing for sustainable energy development.

Asia Pacific Welding Consumables Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Stick Electrodes, Solid Wires, Flux Cored Wires, SAW Wires and Fluxes, Others |

| Welding Techniques Covered | Arc Welding, Resistance Welding, Oxyfuel Welding, Ultrasonic Welding, Others |

| End Use Industries Covered | Construction, Automobile, Energy, Shipbuilding, Aerospace, Industrial Equipment, Others |

| Countries Covered | China, Japan, India, South Korea, Australia, Indonesia, Others |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report

The Asia Pacific welding consumables market size was valued at USD 7.20 Billion in 2025.

The Asia Pacific welding consumables market is expected to grow at a compound annual growth rate of 3.90% from 2026-2034 to reach USD 10.16 Billion by 2034.

Stick electrodes dominated the market with a share of 30%, driven by their cost-effectiveness, portability, versatility across outdoor and remote applications, and widespread adoption in construction, shipbuilding, and pipeline projects throughout the region.

Key factors driving the Asia Pacific welding consumables market include rapid infrastructure development, expanding automotive and electric vehicle manufacturing, growing renewable energy investments, increasing adoption of automated welding systems, and rising demand for eco-friendly consumable formulations.

Major challenges include raw material price volatility, shortage of skilled welders, competition from alternative joining technologies, stringent environmental compliance requirements, supply chain disruptions, and high initial investment costs for advanced automated welding systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)