Asphalt Market Size, Share, Trends and Forecast by Product, Asphalt Type, Application, End-Use Sector, and Region 2026-2034

Global Asphalt Market Size, Share, Trends & Forecast (2026-2034)

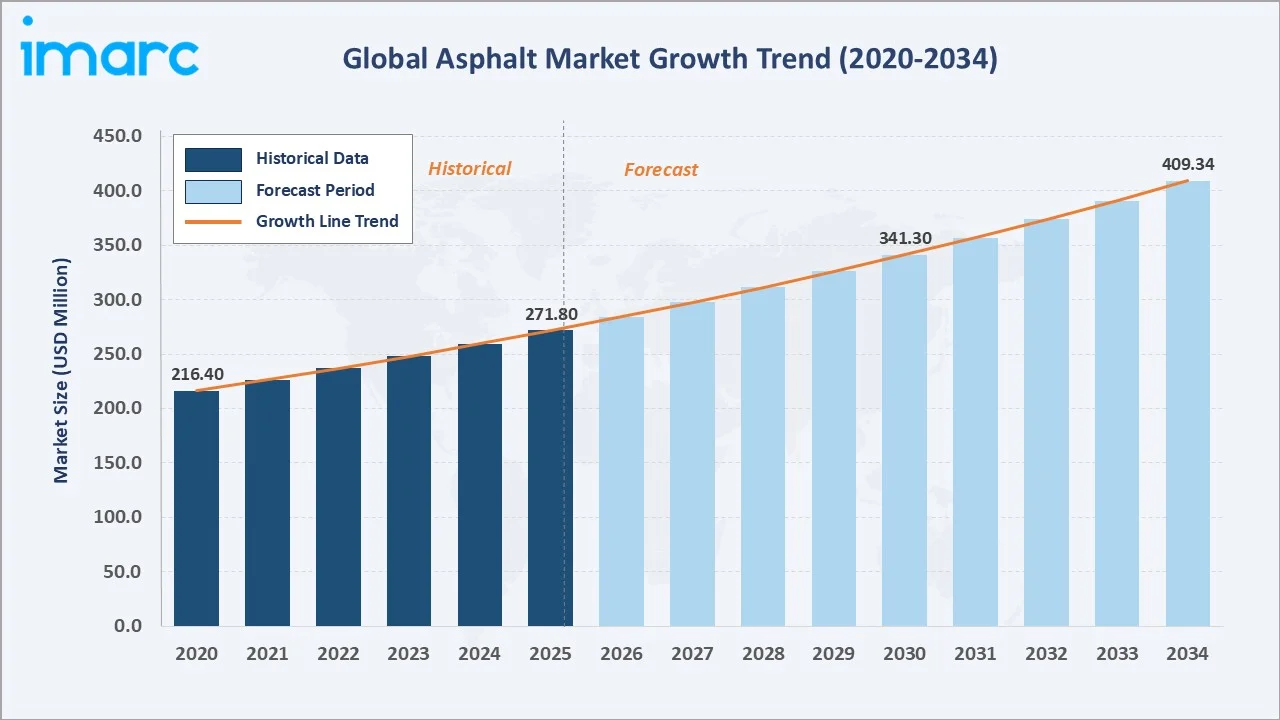

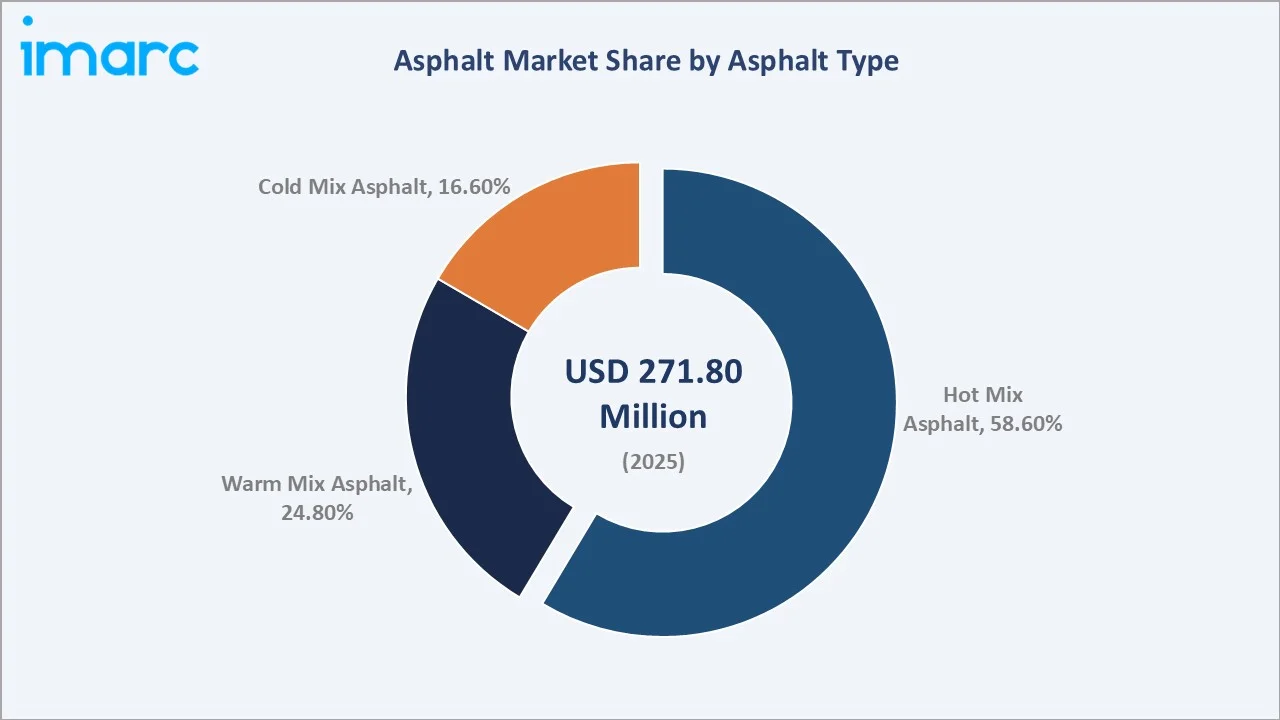

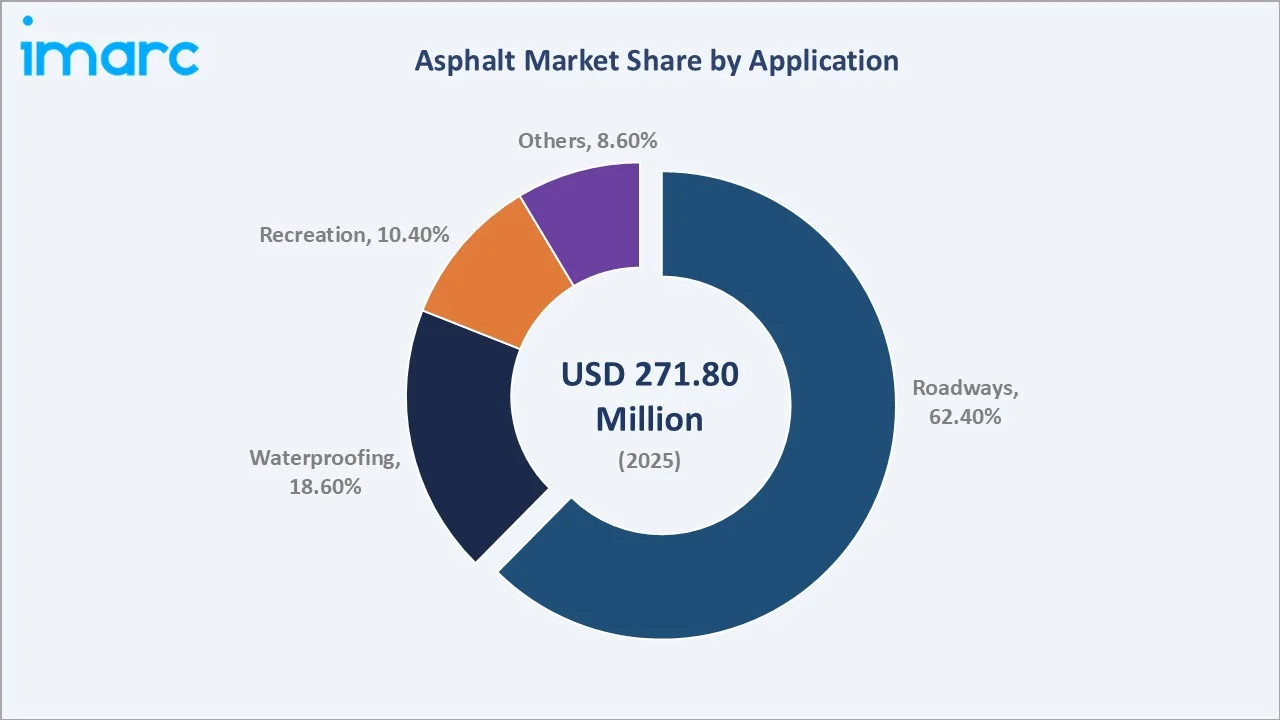

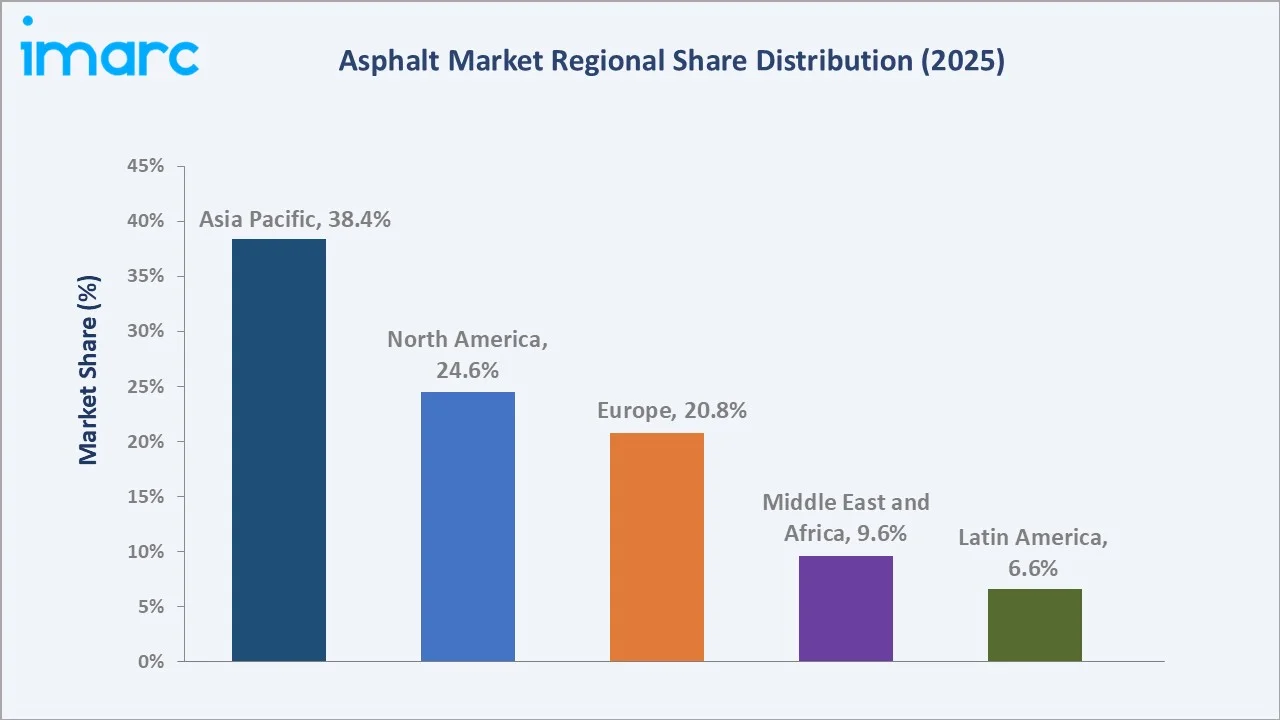

The global asphalt market was valued at USD 271.80 Million in 2025 and is projected to reach USD 409.34 Million by 2034, expanding at a CAGR of 4.66% during the forecast period (2026-2034). The market is driven by escalating road infrastructure investment with Bharatmala Pariyojana targeting 34,800 km of highways with INR 5.35 lakh crore investment, rapid urbanization in Asia Pacific, and government-mandated highway expansion programs globally. Hot mix asphalt dominates with a 58.6% share (2025), while roadway applications account for 62.4% of total demand. Asia Pacific leads all regions with a 38.4% revenue share (2025).

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 271.80 Million |

|

Forecast Market Size (2034) |

USD 409.34 Million |

|

CAGR (2026-2034) |

4.66% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (38.4%, 2025) |

|

Fastest Growing Region |

Middle East & Africa (CAGR ~5.8%, 2026-2034) |

The asphalt market from 2020 through 2034 expanded from USD 216.4 Million in 2020 to USD 271.80 Million in 2025, anchored at USD 341.3 Million in 2030 before reaching USD 409.34 Million by 2034.

To get more information on this market, Request Sample

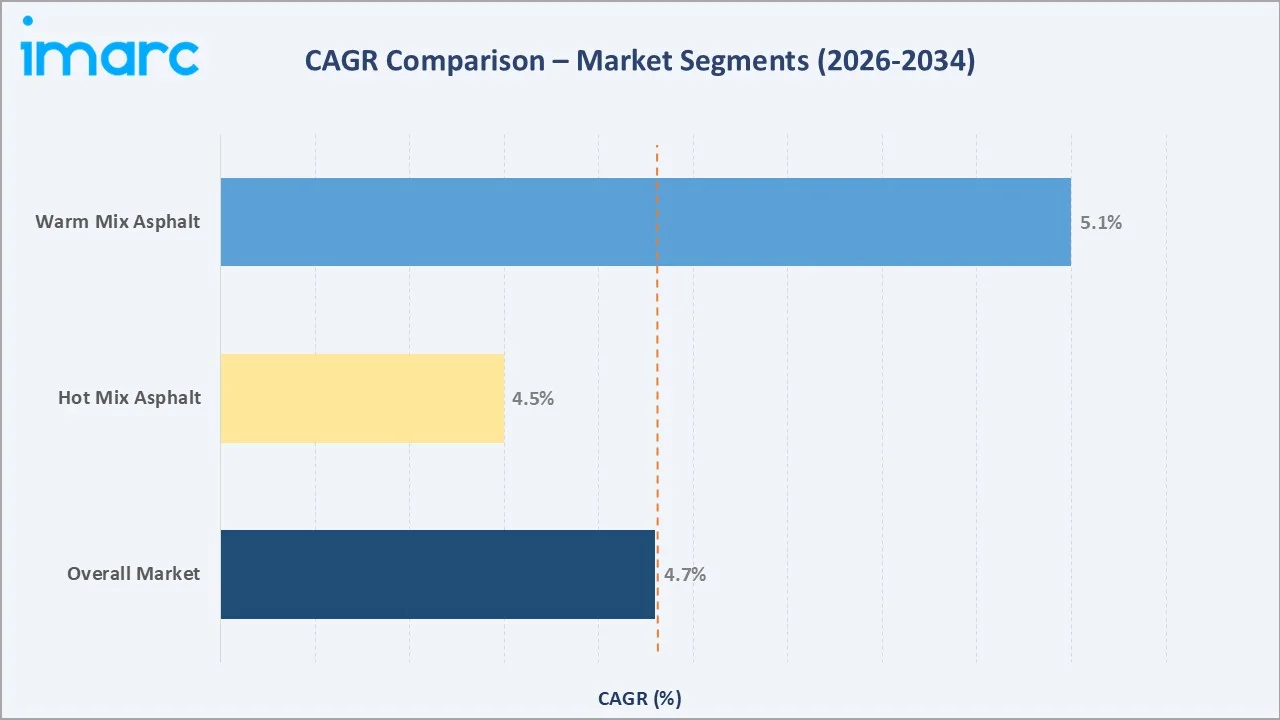

The overall asphalt market CAGR is 4.66%, the warm mix asphalt segment is growing at a CAGR of 5.1%, and the hot mix asphalt segment is growing at a CAGR of 4.5%.

Executive Summary

The global asphalt market continues its steady growth trajectory, underpinned by robust public infrastructure spending and sustained construction activity worldwide. Valued at USD 271.80 million in 2025, the market is forecast to reach USD 409.34 Million by 2034, registering a CAGR of 4.66%. Government road development programs, including the U.S. Infrastructure Investment and Jobs Act (USD 110 billion for highways), India's Pradhan Mantri Gram Sadak Yojana, and China's Belt and Road Initiative, are generating sustained baseline demand for asphalt across all product categories.

Hot mix asphalt commands the largest market share at 58.6% (2025), driven by its superior performance characteristics in high-traffic road applications. Warm mix asphalt (WMA) is the fastest growing type, benefiting from lower production temperatures that deliver energy savings of 20–30% and meaningful VOC emission reductions. The roadways application segment holds 62.4% of total asphalt demand (2025), with airport runway resurfacing and highway expansion programs generating additional demand uplift beyond routine maintenance needs.

Asia Pacific anchors market leadership with a 38.4% revenue share (2025), fueled by China's Belt and Road Initiative (BRI), USD 128.4 billion in construction contracts and USD 85.2 billion in investments and India's National Highways Authority road expansion targets. North America follows with 24.6%, with U.S. federal highway spending at multi-decade highs. Europe maintains a 20.8% share, driven by EU Trans-European Transport Network (TEN-T) upgrade requirements and growing warm mix asphalt adoption mandated by regional emissions standards.

Key Market Insights

|

Insight |

Data |

|

Leading Asphalt Type |

Hot Mix Asphalt – 58.6% share (2025) |

|

Largest Application |

Roadways – 62.4% share (2025) |

|

Leading Region |

Asia Pacific – 38.4% revenue share (2025) |

|

Fastest Growing Region |

Middle East & Africa (CAGR ~5.8%, 2026-2034) |

Key Analytical Observations Supporting The Above Data:

- Hot mix asphalt dominates with a 58.6% share (2025), reflecting its unmatched performance in heavy-duty roadway applications.

- Roadways application commands 62.4% of total demand (2025). There are over 2.2 million miles of paved roads in the United States, over 94% of which are surfaced with asphalt.

- Asia Pacific holds 38.4% market share (2025) with China alone contributing an estimated more in global asphalt consumption. India's road construction target of 50 km per day under the Bharatmala Pariyojana program is generating incremental asphalt demand.

Global Asphalt Market Overview

Asphalt is a semi-solid petroleum-derived material used primarily as a binder in pavement construction and as a waterproofing agent across roofing, hydraulic engineering, and industrial applications. Produced as a residue from crude oil distillation, asphalt's properties can be modified using polymers, rubber crumbs, and chemical additives to deliver specific performance grades for varied end-use requirements. The global asphalt ecosystem spans crude oil refiners, specialty additive producers, asphalt plant operators, road construction contractors, and infrastructure asset managers.

Applications range from high-traffic highway paving and airport runway surfacing to residential roofing, dam waterproofing, and sports court construction. Macroeconomic drivers are compelling the global infrastructure investment, with roads representing the single largest component. Urbanization rates reaching 68% globally by 2050 will generate sustained structural demand for road construction and maintenance materials, with asphalt serving as the dominant flexible pavement solution.

Market Dynamics

To evaluate market opportunities, Request Sample

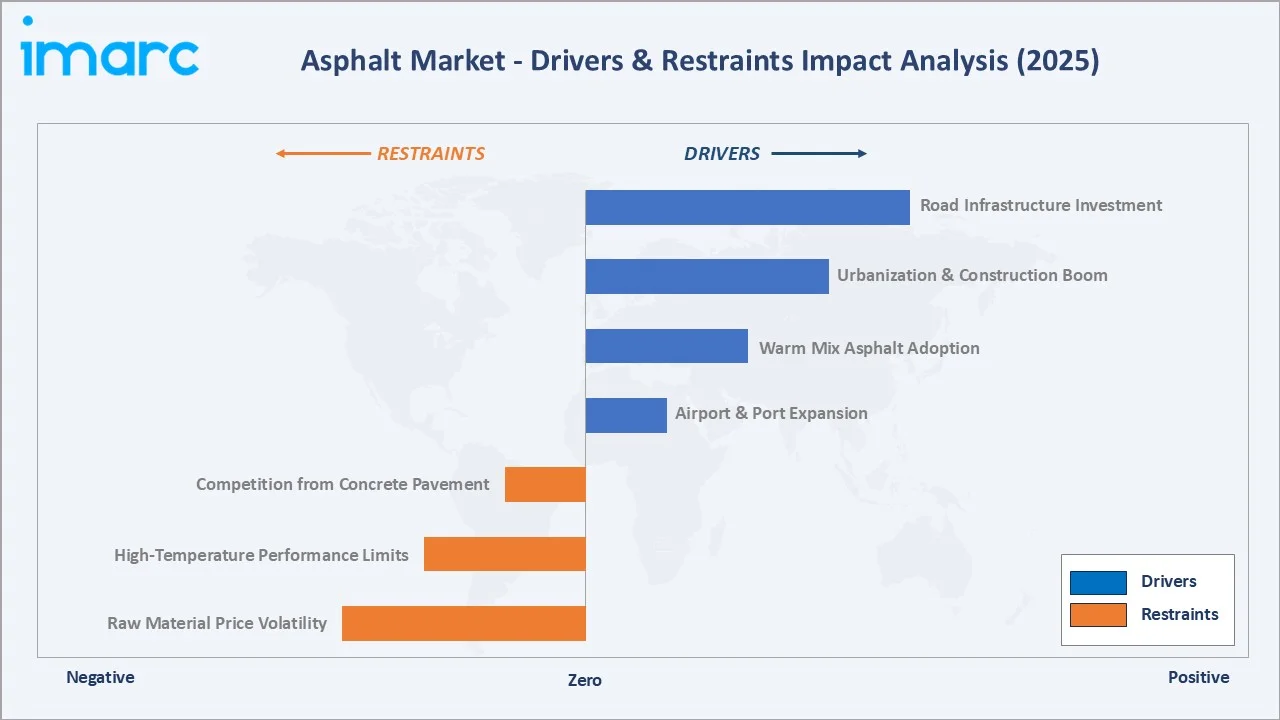

Market Drivers

- Global Road Infrastructure Investment Surge: Total investment in road transport infrastructure increased 20% to reach USD 757 billion in 2024, accelerating highway expansion. This directly underpins asphalt demand across all product types and grades.

- Urbanization and Construction Activity: Over 2.5 billion people will be added to urban areas globally by 2050. Urban road network expansion in emerging markets requires new road construction, generating multi-decade asphalt demand visibility for producers and contractors alike.

- Warm Mix Asphalt Adoption Growth: WMA's energy reduction translates to meaningful contractor cost savings, while regulatory pressure to reduce plant stack emissions is making WMA mandatory.

- Airport and Port Infrastructure Expansion: Global airport capital spending, with runway resurfacing representing a high-specification asphalt demand driver.

Market Restraints

- Stringent Environmental Regulations: HMA plant VOC and particulate emissions face tightening limits under the EU Industrial Emissions Directive and U.S. EPA regulations.

- Competition from Concrete Pavement: Portland cement concrete is capturing share in high-axle-load applications (port yards, heavy industrial roads) where asphalt's rutting resistance is a limitation.

Market Opportunities

- Recycled Asphalt Pavement (RAP) Expansion: RAP usage reduces virgin asphalt requirements, cutting material costs and landfill burden simultaneously.

- Sustainable and Bio-Based Asphalt: Bio-asphalt derived from vegetable oils, lignin, and sugar cane processing waste is commercially available from producers including TotalEnergies and Shell.

- Middle East and Africa Infrastructure Gap: Sub-Saharan Africa has only 34% paved road coverage, representing a structurally underserved market.

Market Challenges

- Supply Chain Concentration Risk: Refinery rationalization, accelerated by the energy transition, is reducing asphalt supply availability in some markets, particularly Europe, where 6 refineries have closed since 2020.

- Long-Term Competition from Porous and Smart Pavements: Next-generation pavement technologies, including solar road panels, self-healing asphalt, and porous drainage asphalt, command higher unit values but require reformulation of conventional HMA, necessitating significant R&D investment from established producers.

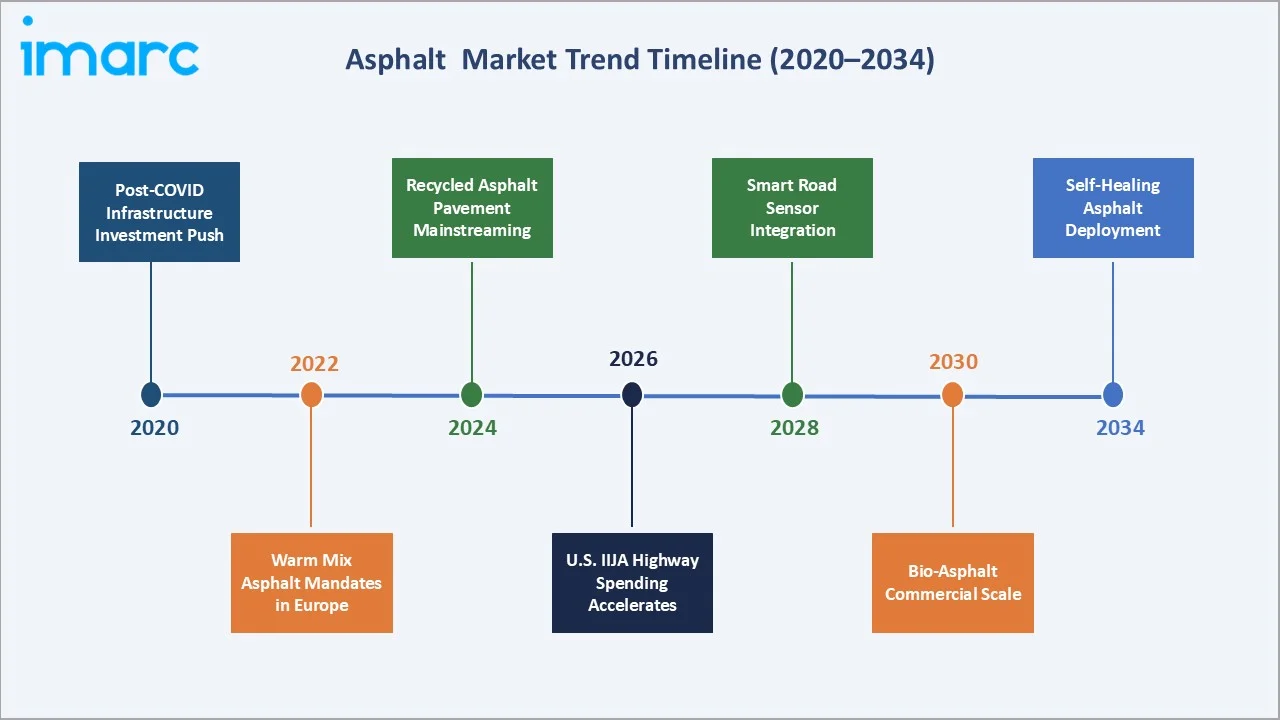

Emerging Market Trends

1. Warm Mix Asphalt Becomes the New Standard

WMA adoption is accelerating beyond early adopter markets, driven by federal Buy America requirements and state-level contractor incentive programs. Germany, France, and the UK have all updated national road specifications to mandate WMA for urban road projects with speed limits below 50 mph speed limits.

2. Recycled Asphalt Pavement Mainstream Adoption

RAP content in new asphalt mixes is rising globally, reshaping procurement models and bitumen demand patterns. 94.6 Million tons of reclaimed asphalt pavement (RAP) were recycled into new mixes in 2021 and 630,000 tons of recycled asphalt shingles (RAS) were put to use in asphalt mixes in 2021. This trend is structurally reducing demand for virgin bitumen per lane-kilometer paved while creating premium opportunities for high-performance polymer-modified rejuvenators.

3. Bio-Based and Sustainable Asphalt Innovation

TotalEnergies, Shell, and start-up producers are commercializing bio-asphalt binders that reduce fossil resource dependency.

4. Smart Road Technology Integration

Asphalt embedded with IoT sensors represents an emerging high-value market. Sensor-embedded asphalt commands a unit price premium over standard product, creating a technology-driven value uplift pathway for innovative producers and road construction specialists.

5. Self-Healing Asphalt Technology

Self-healing asphalt, which contains steel wool or bitumen capsules that repair micro-cracks when heated by induction coils or solar radiation, is transitioning from laboratory to field-scale deployment.

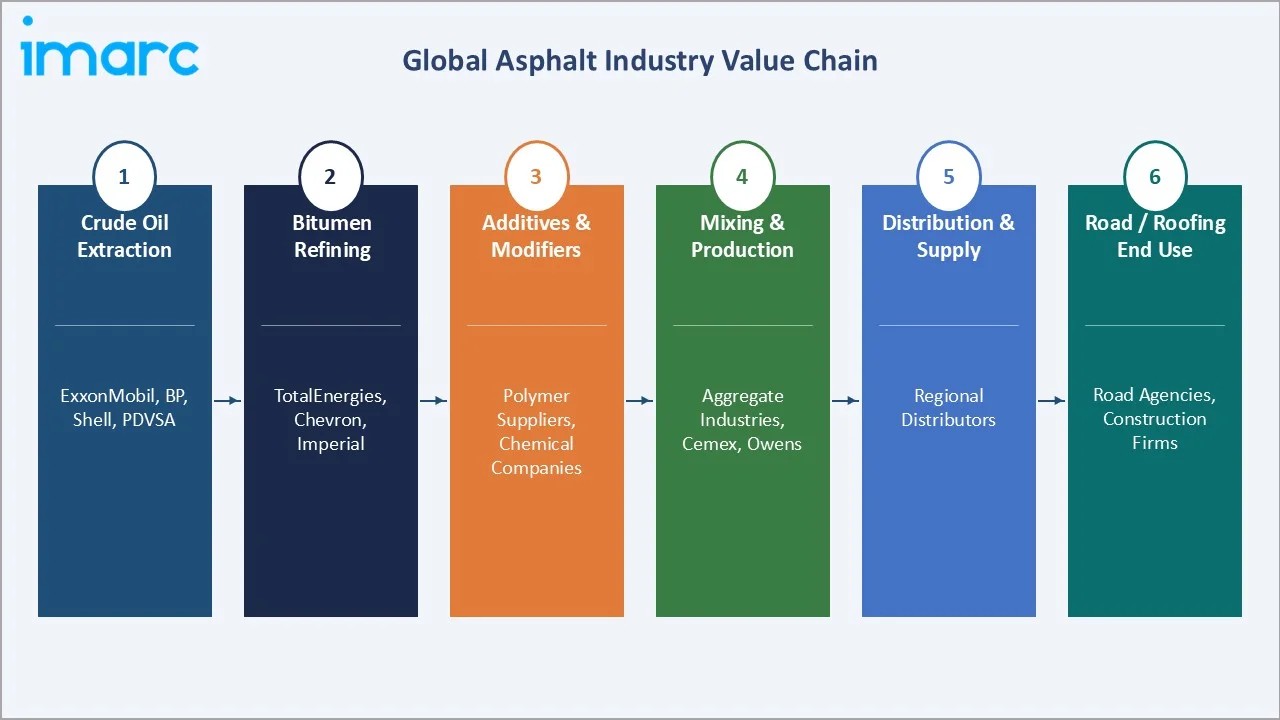

Industry Value Chain Analysis

The asphalt industry value chain begins with crude oil extraction and terminates at finished pavement and roofing installations. Each stage involves specialized capital assets, technical expertise, and regulatory compliance requirements that create distinct competitive dynamics and margin structures across the chain.

|

Stage |

Key Players / Examples |

|

Crude Oil Extraction |

ExxonMobil, BP Plc, Chevron, TotalEnergies, Shell, PDVSA |

|

Refining & Processing |

Imperial Oil, United Refining, Shell International |

|

Additives & Modifiers |

Polymer additive suppliers, rubber modifier producers, chemical companies |

|

Mixing & Production |

Aggregate Industries, Cemex, Owens Corning, Atlas Roofing Corporation |

|

Distribution & Supply |

Regional distributors, construction material logistics providers |

|

End-Use Sectors |

Road agencies, airports, waterproofing firms, sports facility constructors |

The refining and production stage captures the highest margin within the asphalt value chain, with major integrated oil companies focusing on value-added performance grade products. The mixing and production stage is more commoditized, with typical EBIT margins of 6-12% among regional asphalt plant operators in competitive markets such as the U.S., Germany, and Japan.

Technology Landscape in the Asphalt Industry

Advanced Bitumen Modification

Polymer-modified bitumen (PMB) is the fastest-growing asphalt technology segment, commanding a price premium over unmodified penetration grade bitumen. Styrene-butadiene-styrene (SBS) and ethylene-vinyl-acetate (EVA) polymers improve rutting resistance, fatigue life, and low-temperature cracking performance.

Warm Mix Additive Technology

WMA additives, including zeolite-based water foaming agents, chemical surfactants, and wax-based viscosity reducers, enable asphalt mixing temperatures to be reduced by 20-40°C without compromising workability or compaction performance.

Recycling and Rejuvenation Technology

High-RAP asphalt requires bitumen rejuvenators to restore aged binder properties. 26 Million Barrels of virgin asphalt binder that was replaced by recycled binder from reclaimed asphalt pavement (RAP) and recycled asphalt shingles (RAS) in 2021.

Digital Plant Management

Asphalt plant automation systems from suppliers offer real-time mix recipe optimization, energy monitoring, and predictive maintenance. Smart plants with automated aggregate moisture compensation and bitumen temperature management deliver mix quality improvements versus manually operated plants.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Asphalt Paving Mixtures and Blocks | 🔒 | 2025 |

| Asphalt Type | Hot Mix Asphalt | 58.6% | 2025 |

| Application | Roadways | 62.4% | 2025 |

| End Use Sector | 🔒 | 🔒 | 2025 |

| Region | Asia Pacific | 38.4% | 2025 |

By Asphalt Type

Hot mix asphalt is the dominant segment with a 58.6% market share in 2025. HMA is produced at temperatures of 150–190°C and provides superior mechanical performance for high-traffic road surfaces, airport runways, and major highway projects. Its dominance is structural; HMA's performance characteristics in extreme climate conditions are unmatched by current WMA or CMA alternatives for heavy-duty applications.

To access detailed market analysis, Request Sample

Warm mix asphalt holds a 24.8% share (2025) and is the fastest growing type, forecast to grow at ~5.1% CAGR through 2034. WMA adoption has been accelerating since 2020 as energy prices rose and carbon reduction mandates tightened. Cold Mix Asphalt accounts for 16.6% of the market (2025), primarily used in remote-area road maintenance, temporary repairs, and developing country rural road programs where hot-mix plant access is limited.

By Application

Roadways is the dominant application, capturing 62.4% of total asphalt demand in 2025. Asphalt accounts for approximately 83.5% of all paved road surfaces. India's Bharatmala Pariyojana targets 26,425 km length is expected to be completed by 2027-28. In the U.S., IIJA-funded highway resurfacing programs are increasing asphalt consumption.

Waterproofing accounts for 18.6% of demand (2025), encompassing roofing asphalt, hydraulic engineering waterproofing membranes, and underground structure protection systems. Recreation (10.4%) covers sports courts, running tracks, and cycling infrastructure where smooth, durable asphalt surfaces are essential. Others (8.6%) include industrial flooring and noise-reduction pavement applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

38.4% |

China BRI road network, India PMGSY, rapid urbanization |

|

North America |

24.6% |

U.S. IIJA highway funding, airport resurfacing |

|

Europe |

20.8% |

EU TEN-T network upgrades, warm mix adoption for emissions |

|

Middle East & Africa |

9.6% |

Saudi Vision 2030 roads, NEOM city, Africa road deficiency |

|

Latin America |

6.6% |

Brazil road privatization, Mexico highway expansion plan |

Asia Pacific's 38.4% market dominance (2025) reflects the region's extraordinary road infrastructure expansion pace. China’s new plan involves national roads with a total length of about 461,000 km, consisting of 162,000 km of national expressways and 299,000 km of highways. India constructed 12,349 km of national highways in FY2024, which are among the region's most significant ongoing asphalt demand generators.

North America's 24.6% share (2025) is underpinned by the U.S. IIJA's USD 110 billion highway allocation, the largest federal surface transportation investment in U.S. history. The U.S. consumed approximately 350 million tons of asphalt annually. Canada's federal Investing in Canada Infrastructure Program. Mexico's road concession expansion program is adding incremental asphalt demand across its highway network upgrades under the AMLO-era infrastructure legacy pipeline.

Competitive Landscape

The global asphalt market is moderately concentrated at the production tier, with integrated oil major bitumen divisions collectively accounting for approximately 45-50% of global bitumen production capacity.

|

Company Name |

Brand / Product |

Market Position |

Core Strength |

|

Exxon Mobil Corporation |

ExxonMobil Asphalt |

Market Leader |

Vertically integrated crude-to-asphalt supply chain |

|

BP Plc |

BP Bitumen |

Strong Challenger |

Advanced polymer-modified bitumen products, strong European and Middle East distribution infrastructure |

|

Owens Corning |

Oakridge |

Specialist Leader |

Roofing asphalt dominance, glass fiber reinforced asphalt products, U.S. residential reroofing leader |

|

Cemex |

VIA series |

Established |

Integrated construction materials ecosystem, ready-mix asphalt for road maintenance markets |

|

Atlas Roofing Corporation |

StormMaster, Pinnacle, ProLam |

Niche Specialist |

U.S. residential and commercial roofing asphalt systems, energy-efficient roof design integration |

|

Shell Plc |

Shell Bitumen |

Integrator |

Global bitumen trading and supply logistics, technical bitumen specifications advisory |

The downstream asphalt mixing and road construction segment is highly fragmented, with thousands of regional operators. Specialty roofing asphalt is more concentrated, with Owens Corning and Atlas Roofing dominating the U.S. market.

Key Company Profiles

Exxon Mobil Corporation

ExxonMobil is one of the world's largest publicly traded bitumen and asphalt producers, with refinery bitumen production capacity across refineries in North America, Europe, and the Asia Pacific.

- Product Portfolio: Paving Asphalt PG 58-28, Paving Asphalt PG 64-22, Asphalt Blendstock, Asphalt Blendstock VTB, Paving Asphalt PG 46-34, Roofing Asphalt Flux (RAF).

- Recent Developments: Expanded Baytown refinery bitumen capacity to meet U.S. IIJA-driven demand acceleration.

- Strategic Focus: Performance grade bitumen leadership; bio-circular feedstock integration for sustainable asphalt; strengthening North America distribution infrastructure ahead of IIJA spending cycle peak.

BP Plc

BP is a major global bitumen producer and supplier. Whiting, IN refinery is one of the largest asphalt producing refineries in the world.

- Product Portfolio: bp unmodified performance graded asphalt binders.

- Recent Developments: In March 2026, bp reached an agreement to sell its Gelsenkirchen refinery and related businesses to Klesch Group.

- Strategic Focus: Premium polymer-modified bitumen differentiation; Middle East and Africa market expansion through BP Bitumen's regional technical center network; sustainable bitumen product development aligned with BP's net-zero 2050 roadmap.

Owens Corning

Owens Corning is one of the leading U.S. roofing asphalt companies and a major manufacturer of asphalt shingles, roofing membranes, and glass fiber reinforced asphalt composite products.

- Product Portfolio: Duration Series and TruDefinition asphalt shingles, WeatherLock self-adhering bituminous underlayments, and Fiberglas-reinforced asphalt composite shingles for residential and commercial applications.

- Recent Developments: Announced to acquire Masonite International in February 2024 for USD 3.9 billion, expanding building envelope solutions.

- Strategic Focus: U.S. residential reroofing market share defense; premium asphalt shingle innovation (impact-resistant, algae-resistant, solar-integrated); geographic expansion in European and Latin American roofing asphalt markets.

Market Concentration Analysis

The global asphalt market exhibits moderate concentration at the bitumen production tier. The top five integrated oil company bitumen producers collectively control approximately 45–50% of global refinery bitumen production capacity. This concentration is driven by the capital-intensive nature of oil refinery operations and the vertical integration advantages that major oil companies possess from crude oil sourcing through to finished bitumen supply.

The roofing and specialty asphalt segment is more concentrated still, collectively holding approximately 55–60% of the U.S. residential asphalt shingle market. In contrast, the asphalt mixing and road paving segment is highly fragmented globally. Leading regional paving contractors are consolidating the North American market through acquisitions.

Consolidation is accelerating across the value chain. Refinery rationalization driven by the energy transition is reducing independent bitumen production capacity in Western Europe, effectively increasing concentration among major producers. This trend is expected to continue through 2034 as smaller refinery operators exit the market.

Investment & Growth Opportunities

Fastest Growing Segments

Warm mix asphalt is growing at a CAGR of ~5.1%, sustainable and bio-based asphalt formulations at a CAGR of ~12%, and polymer-modified bitumen for high-performance infrastructure at a CAGR of ~5.8% represent the three highest-growth investment vectors through 2034.

Emerging Market Expansion

Sub-Saharan Africa represents the most structurally underserved asphalt market globally. The continent's incremental asphalt demand represents a compelling investment destination. India's asphalt market growth is driven by Bharatmala and PMGSY targets. Saudi Arabia's Vision 2030 road program and NEOM megacity infrastructure require specialized performance-grade asphalt products suited to extreme heat conditions.

Venture Investment Trends

Smart road infrastructure embedding is attracting IoT and materials science convergence capital from both the construction and technology sector investors.

- Key growth bets: Bio-asphalt binder platforms, warm mix additive formulations for high-RAP mixes, and smart asphalt sensor integration systems.

- ESG-aligned investors are targeting bitumen producers with verified carbon reduction roadmaps, particularly those integrating bio-circular feedstocks and renewable energy into HMA/WMA plant operations.

- Infrastructure PE and sovereign wealth funds are acquiring asphalt plant networks as regulated infrastructure assets, particularly in North America, where IIJA spending provides multi-year revenue visibility for HMA producers adjacent to federally funded highway corridors.

Future Market Outlook (2026-2034)

The global asphalt market is positioned for steady, government-spending-anchored growth through 2034. From a base of USD 271.80 Million in 2025, the market is forecast to reach USD 409.34 Million by 2034, representing an absolute value addition of USD 137.54 Million over the nine-year forecast horizon. Unlike cyclical construction materials, asphalt benefits from multi-year infrastructure program commitments, particularly the U.S. IIJA, EU TEN-T, India's Bharatmala, and China's BRI, which provide structural demand visibility well beyond typical economic cycles.

Between 2026 and 2030, the product mix will shift meaningfully toward warm mix and sustainable asphalt formulations as environmental regulations tighten. Bio-asphalt and recycled asphalt pavement technologies will transition from regulatory compliance tools to genuine competitive differentiators, with producers that commercialize them earliest capturing premium pricing and preferred supplier status with ESG-mandated public road agencies across Europe and North America.

Research Methodology

Primary Research

Primary research for this report included structured interviews with over 140 industry stakeholders in 2025, comprising bitumen refinery executives, asphalt plant operators, road construction contractors, national road agency procurement officers, and building materials distributors across North America, Europe, Asia Pacific, and the Middle East. Primary research validated market size estimates, identified emerging product category trends, and assessed competitive positioning.

Secondary Research

Secondary research encompassed company annual reports, refinery capacity databases, government infrastructure budget documents, trade publications, and regulatory filings across 35 countries. Over 260 secondary sources were reviewed and triangulated to construct a comprehensive global asphalt market model.

Forecasting Models

Market size estimations were developed using a hybrid approach combining bottom-up and top-down methodologies. Key input variables include crude oil price forecasts, government infrastructure budget commitments, urbanization trajectories, and RAP adoption rates by region.

Asphalt Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Asphalt Paving Mixtures and Blocks, Prepared Asphalt and Tar Roofing and Siding Products, Roofing Asphalts and Pitches, Coatings and Cement |

| Asphalt Types Covered | Hot Mix Asphalt, Warm Mix Asphalt, Cold Mix Asphalt |

| Applications Covered | Roadways, Waterproofing, Recreation, Others |

| End-Use Sectors Covered | Non-Residential, Residential, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Exxon Mobil Corporation, BP Plc, Owens Corning, Cemex, Atlas Roofing Corporation, Shell Plc, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the asphalt market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global asphalt market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the asphalt industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Asphalt Market Report

The global asphalt market was valued at USD 271.80 Million in 2025 and is projected to reach USD 409.34 Million by 2034, growing at a CAGR of 4.66% during the forecast period.

Asia Pacific dominates with a 38.4% revenue share (2025), anchored by China's expressway network expansion, India's national highway program, and Indonesia's major road infrastructure projects.

Middle East and Africa are the fastest growing regions, driven by Saudi Vision 2030 road programs, NEOM megacity infrastructure, and Sub-Saharan Africa's significant paved road coverage deficit.

Key drivers include global road infrastructure investment at USD 2.1 trillion annually, urbanization-driven road construction, U.S. IIJA highway funding, and India's Bharatmala highway program.

Hot Mix Asphalt is the largest segment with a 58.6% market share (2025), driven by its superior performance in high-traffic roads, highways, and airport runways globally.

Roadways are the dominant application, accounting for 62.4% of total asphalt demand (2025), driven by global highway construction and maintenance activity.

The leading companies include Exxon Mobil Corporation, BP Plc, Owens Corning, Cemex, Atlas Roofing Corporation, and Shell Plc.

Key trends include warm mix asphalt adoption, recycled asphalt pavement mainstreaming, bio-based bitumen innovation, smart road pavement integration, and self-healing asphalt technology commercialization.

High-growth opportunities include warm mix asphalt additives, bio-asphalt binders, Sub-Saharan Africa road infrastructure, India highway expansion, and smart pavement sensor integration systems.

Key challenges include crude oil price volatility affecting production costs, tightening environmental regulations on HMA plant emissions, competition from concrete pavement, and skilled labor shortages in road construction.

Bio-based bitumen, recycled asphalt pavement mandates, warm mix energy savings, and self-healing asphalt technologies are collectively transforming the industry's environmental profile through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)