Australia Adeno-associated Virus Gene Therapy Market Size, Share, Trends and Forecast by Therapeutic Area, Vector Serotype, Route of Administration, Application, Manufacturing Type, End User, and Region, 2026-2034

Australia Adeno-associated Virus Gene Therapy Market Summary:

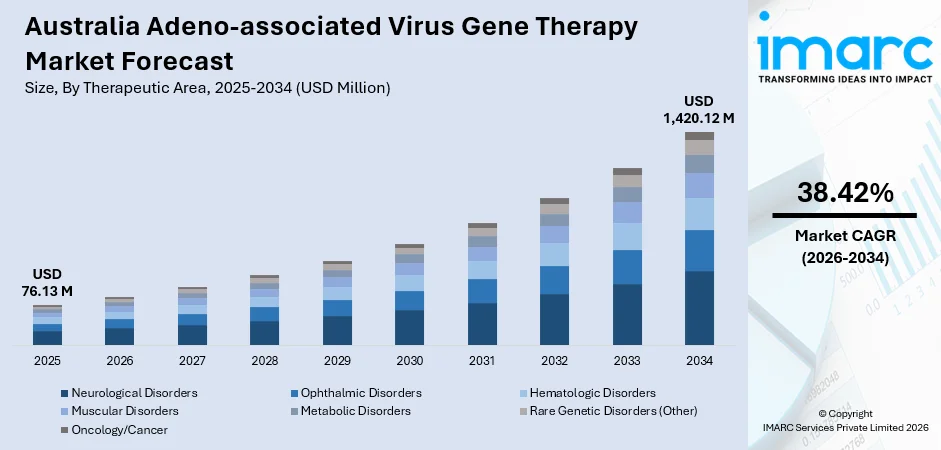

The Australia adeno-associated virus gene therapy market size was valued at USD 76.13 Million in 2025 and is projected to reach USD 1,420.12 Million by 2034, growing at a compound annual growth rate of 38.42% from 2026-2034.

The Australia adeno-associated virus gene therapy market is experiencing transformative growth driven by expanding clinical pipelines, increasing regulatory approvals for neurological disorders, and strengthening biotechnology research infrastructure. Rising investments in advanced therapeutic manufacturing, government initiatives supporting regenerative medicine development, and growing collaborations between pharmaceutical companies and academic institutions are fostering innovation and accelerating product commercialization. Technological advancements in AAV vector engineering, favorable regulatory pathways established by the Therapeutic Goods Administration, and robust clinical trial ecosystems are strengthening Australia adeno-associated virus gene therapy market share.

Key Takeaways and Insights:

- By Therapeutic Area: Neurological disorders reign the market with a share of 36.8% in 2025, driven by the rising prevalence of neurodegenerative diseases and limited treatment alternatives for conditions such as spinal muscular atrophy and Parkinson's disease.

- By Vector Serotype: AAV9 dominates the market with a share of 28.5% in 2025, supported by its superior ability to cross the blood-brain barrier and efficiently transduce central nervous system tissues.

- By Route of Administration: Intravenous (I.V.) leads the market with a share of 42.7% in 2025, enabled by its systemic delivery capabilities and widespread applicability across multiple therapeutic indications.

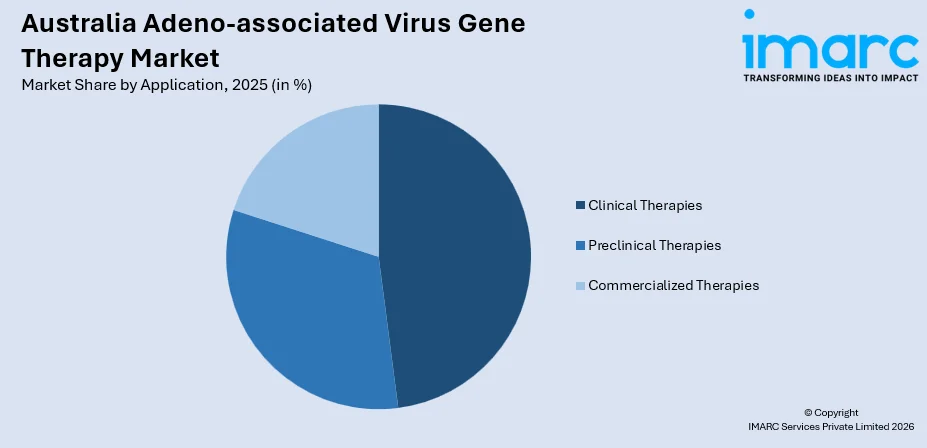

- By Application: Clinical therapies exhibit prominence in the market with a share of 47.9% in 2025, reflecting robust clinical trial pipelines and substantial investment in late-stage gene therapy development programs.

- By Manufacturing Type: CDMOs/vector production facilities represent the leading category with a share of 58.6% in 2025, driven by the specialized infrastructure requirements and increasing outsourcing preferences among biotechnology companies.

- By End User: Pharmaceutical and biotechnology companies hold the largest share at 51.3% in 2025, propelled by intensive research investments and expanding therapeutic portfolios in genetic medicine.

- By Region: Australian Capital Territory & New South Wales are the biggest segment, commanding 39.4% share in 2025, supported by premier research institutions and advanced healthcare infrastructure.

- Key Players: The competitive landscape of the market features a mix of global pharmaceutical giants and specialized biotechnology firms focusing on innovative vector engineering, strategic partnerships, manufacturing scale-up, and regulatory expertise to advance gene therapy commercialization.

To get more information on this market Request Sample

The Australia adeno-associated virus gene therapy market is positioned at the forefront of regenerative medicine advancement, underpinned by a robust regulatory framework administered by the Therapeutic Goods Administration and a thriving biotechnology research ecosystem. The country has established itself as a strategic hub for clinical gene technology, with multiple TGA-approved gene therapies including Zolgensma and Luxturna already accessible to patients. Australia's gene therapy clinical trial landscape continues to expand significantly. As such, in October 2025, Australia opened its first clinical and commercial-scale Viral Vector Manufacturing Facility (VVMF) in Sydney, backed by USD 134.5 Million NSW funding. The CDMO will supply GMP-grade vectors, supporting gene therapies, streamlined clinical trials, job creation, and exports. Moreover, the increasing confidence of international biotechnology companies in Australia's clinical trial infrastructure, regulatory expertise, and patient access capabilities is positioning the market for sustained long-term expansion.

Australia Adeno-associated Virus Gene Therapy Market Trends:

AI-Powered AAV Capsid Engineering Accelerating Vector Development

The Australia adeno-associated virus gene therapy market is witnessing transformative advancements through artificial intelligence integration in capsid engineering, enabling faster identification of optimal viral vectors with enhanced tissue specificity and reduced immunogenicity. For example, in October 2024, Roche and Dyno Therapeutics launched a strategic collaboration valued at over USD 1 Billion to develop next-generation AAV vectors using AI-based capsid engineering for neurological gene therapies. This partnership exemplifies the industry's commitment to leveraging computational biology for accelerating vector design and improving therapeutic outcomes across diverse genetic disorders.

Expansion of CNS-Targeted AAV Therapies Driving Clinical Development

Central nervous system-targeted AAV gene therapies are seeing rapid pipeline growth as researchers pursue new solutions for neurological conditions that have limited treatment options. The neurological disorders segment remains a major focus within gene therapy development, supported by progress in capsid engineering designed to improve blood–brain barrier penetration and more effective intrathecal delivery approaches. Companies and academic groups are actively advancing therapies for disorders such as spinal muscular atrophy, Parkinson’s disease, and rare inherited neuropathies. These innovations are strengthening clinical momentum and expanding the future potential of CNS-focused gene therapy applications.

Regulatory Acceleration and Label Expansions Broadening Patient Access

Regulatory agencies worldwide are demonstrating increased receptivity to accelerated approval pathways for AAV gene therapies, enabling faster patient access to transformative treatments for rare genetic diseases. This regulatory momentum is supporting Australia adeno-associated virus gene therapy market growth by creating favorable conditions for clinical development and product registration. In June 2024, Sarepta Therapeutics' Elevidys received full FDA approval for ambulatory Duchenne muscular dystrophy patients, following its initial accelerated approval in 2023, signaling growing regulatory confidence in AAV-based therapeutic platforms.

Market Outlook 2026-2034:

The Australia adeno-associated virus gene therapy market is projected to experience robust expansion throughout the forecast period, driven by continuous clinical pipeline advancement, regulatory framework maturation, and expanding manufacturing capabilities across the region. In accordance with this, government investment in advanced therapeutic infrastructure remains a key catalyst for market growth. For example, in January 2025, the Medical Research Future Fund allocated AUD 35.7 Million to enhance clinical trial and manufacturing infrastructure, bolstering early-stage development capacity and attracting global pharmaceutical interest. The progressive commercialization of approved gene therapies, increasing adoption of AI-driven vector engineering technologies, and deepening collaborations between international biotechnology companies and Australian research institutions are expected to sustain strong momentum. Furthermore, expanding therapeutic applications beyond rare diseases into more prevalent neurological and muscular disorders, coupled with improving reimbursement pathways, will drive broader patient access and market penetration. The market generated a revenue of USD 76.13 Million in 2025 and is projected to reach a revenue of USD 1,420.12 Million by 2034, growing at a compound annual growth rate of 38.42% from 2026-2034.

Australia Adeno-associated Virus Gene Therapy Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Therapeutic Area |

Neurological Disorders |

36.8% |

|

Vector Serotype |

AAV9 |

28.5% |

|

Route of Administration |

Intravenous (I.V.) |

42.7% |

|

Application |

Clinical Therapies |

47.9% |

|

Manufacturing Type |

CDMOs/Vector Production Facilities |

58.6% |

|

End User |

Pharmaceutical and Biotechnology Companies |

51.3% |

|

Region |

Australian Capital Territory & New South Wales |

39.4% |

Therapeutic Area Insights:

- Neurological Disorders

- Spinal Muscular Atrophy (SMA)

- Parkinson’s Disease

- Alzheimer’s Disease

- Rett Syndrome

- Amyotrophic Lateral Sclerosis (ALS)

- Canavan Disease

- AADC Deficiency

- Huntington’s Disease

- Friedreich’s Ataxia

- Ophthalmic Disorders

- Leber Congenital Amaurosis (LCA)

- Retinitis Pigmentosa

- Wet Age-related Macular Degeneration (AMD)

- Stargardt Disease

- Choroideremia

- Hematologic Disorders

- Hemophilia A (e.g., Roctavian)

- Hemophilia B (e.g., Hemgenix)

- Thalassemia

- Sickle Cell Disease

- Muscular Disorders

- Duchenne Muscular Dystrophy (DMD) (e.g., Elevidys)

- Limb-Girdle Muscular Dystrophy (LGMD)

- Metabolic Disorders

- Alpha-1 Antitrypsin Deficiency

- Phenylketonuria (PKU)

- Glycogen Storage Diseases

- Hereditary Lipoprotein Lipase Deficiency (LPLD) (e.g., Glybera - though withdrawn)

- Rare Genetic Disorders (Other)

- Mucopolysaccharidosis (MPS)

- Batten Disease

- Cystic Fibrosis

- Sanfilippo Syndrome

- Oncology/Cancer

- Various cancer types where AAVs are used for targeted delivery of anti-cancer genes

- Cardiovascular Diseases

Neurological disorders lead the market, accounting for 36.8% share of the total Australia adeno-associated virus gene therapy market, in 2025.

The neurological disorders segment dominates the Australia adeno-associated virus gene therapy market, driven by the substantial unmet medical need for treating complex neurodegenerative and genetic conditions affecting the central nervous system. AAV vectors, particularly AAV9, have demonstrated exceptional therapeutic potential due to their unique ability to cross the blood-brain barrier and efficiently transduce neural tissues. The segment's leadership position reflects strong clinical development activity targeting conditions such as spinal muscular atrophy, Parkinson's disease, Huntington's disease, and various inherited neuropathies where conventional treatments offer limited efficacy or disease modification.

The rising prevalence of neurological disorders, affecting approximately 8.7% of Australians, or around 2.2 million people living with long-term neurological conditions, continues to drive increased research investment and the expansion of clinical trials within this therapeutic area. Advances in genome delivery methods, combined with increasing regulatory support for orphan drug development and accelerated approval pathways, are strengthening the segment's growth trajectory. The establishment of specialized treatment centers and improvements in patient identification through genetic screening programs are further enabling broader therapeutic access across Australia's healthcare system.

Vector Serotype Insights:

- AAV1

- AAV2

- AAV3

- AAV4

- AAV5

- AAV6

- AAV7

- AAV8

- AAV9

- AAV10

- AAV11

- AAV12

- Engineered/Synthetic/Hybrid Capsids

AAV9 dominates the market with a 28.5% share of the total Australia adeno-associated virus gene therapy market in 2025.

The AAV9 serotype holds the leading position in the market, attributed to its superior ability to efficiently target both systemic tissues and the central nervous system, making it ideal for treating a broad range of genetic diseases. AAV9's extensive utilization in approved therapies such as Zolgensma for spinal muscular atrophy has established strong clinical validation and commercial precedent. The serotype's favorable safety profile, combined with its capacity for widespread biodistribution following intravenous administration, has positioned AAV9 as the preferred vector choice for multiple late-stage clinical programs.

Continued advancements in AAV9 manufacturing processes and growing adoption across pipeline programs spanning neurology, cardiology, and metabolic disorder treatments are reinforcing the serotype's market leadership position. Furthermore, ongoing research into AAV9 capsid modifications to reduce immunogenicity and enhance tissue specificity is expected to sustain strong demand as companies seek optimized vector platforms for next-generation gene therapy applications targeting diverse patient populations.

Route of Administration Insights:

- Intravenous (I.V.)

- Intrathecal (I.T.) (for CNS delivery)

- Intraocular (I.O.) (e.g., intravitreal, subretinal)

- Intramuscular (I.M.)

- Intracerebral

- Subcutaneous

- Local/Direct Injection (e.g., into specific organs)

Intravenous holds the largest share, accounting for 42.7% of the total Australia adeno-associated virus gene therapy market in 2025.

The intravenous route of administration dominates the Australia adeno-associated virus gene therapy market, enabled by its capacity for systemic delivery allowing AAV vectors to circulate throughout the body and reach multiple target tissues through a single infusion. This administration route is particularly advantageous for treating systemic genetic disorders requiring widespread transgene expression, such as muscular dystrophies and metabolic conditions. The demand for minimally invasive gene delivery methods and the need to avoid complexities associated with direct tissue injections make intravenous administration the preferred choice for many clinical development programs.

The intravenous segment accounted for approximately 40% of global gene therapy clinical trials by route of administration in 2024, underscoring its widespread adoption across therapeutic applications. The route's established safety profile and well-characterized pharmacokinetic properties facilitate regulatory approval processes and clinical protocol standardization. Additionally, the growing pipeline of intravenously administered AAV therapies for neurological, hematological, and muscular disorders is expected to sustain strong segment growth as more products progress toward commercialization and become accessible to Australian patients.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Preclinical Therapies

- Clinical Therapies

- Commercialized Therapies

Clinical therapies are the largest segment, commanding 47.9% share of the total Australia adeno-associated virus gene therapy market in 2025.

The clinical therapies segment holds the dominant position in the Australia adeno-associated virus gene therapy market, reflecting the substantial investment in late-stage clinical development programs and the robust pipeline of AAV-based therapies undergoing regulatory evaluation. Many AAV gene therapies are currently progressing through Phase II and Phase III clinical trials targeting neurological, muscular, and ocular conditions, demonstrating healthy investment from pharmaceutical companies and continued regulatory momentum in advancing innovative treatments.

The segment's leadership position is reinforced by expanding therapeutic applications beyond rare diseases into broader patient populations and the increasing number of clinical trials receiving regulatory clearance in Australia. Strong support from venture capital, institutional investors, and strategic partnerships between biotechnology companies and academic medical centers is accelerating clinical development timelines. As the pipeline matures and more therapies transition toward commercialization, the clinical therapies segment is expected to maintain its dominant market position while driving continued innovation in trial design and patient selection strategies.

Manufacturing Type Insights:

- In-House Manufacturing

- CDMOs/Vector Production Facilities

CDMOs and vector production facilities represents the largest category with 58.6% share of the total Australia adeno-associated virus gene therapy market in 2025.

The CDMOs and vector production facilities segment dominates the Australia adeno-associated virus gene therapy market, driven by the highly specialized nature of AAV manufacturing that requires substantial capital investment, advanced infrastructure, and deep regulatory expertise. Many biotechnology and pharmaceutical companies, despite their scale, often lack the ready-to-go infrastructure and technical setups required to manage AAV vector production internally, leading to increased reliance on contract manufacturing partners.

Australia's CDMO landscape is strengthening through strategic partnerships and facility expansions to meet rising regional demand. In April 2025, Cell Therapies Pty Ltd and Xellera Therapeutics entered a strategic partnership to accelerate cell and gene therapy development across the Asia-Pacific region, focusing on expanding CGT access through enhanced GMP manufacturing capabilities. The increasing preference for full-service CDMOs offering end-to-end capabilities from process development through commercial manufacturing is driving market consolidation and capability investment, positioning Australia as an emerging hub for advanced therapeutic production.

End User Insights:

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutions

- Contract Research Organizations (CROs)

Pharmaceutical and biotechnology companies hold the largest share at 51.3% of the total Australia adeno-associated virus gene therapy market in 2025.

The pharmaceutical and biotechnology companies segment dominates the Australia adeno-associated virus gene therapy market, driven by intensive research investments, expanding therapeutic portfolios in genetic medicine, and strategic positioning to capitalize on the curative potential of gene-based treatments. Large pharmaceutical companies are increasingly acquiring specialized gene therapy developers and establishing internal capabilities to access advanced AAV technologies.

The growing pipeline of AAV-based therapies approaching regulatory milestones is driving pharmaceutical companies to invest heavily in clinical development, manufacturing scale-up, and commercialization infrastructure. Strategic collaborations between global pharmaceutical giants and Australian biotechnology firms are facilitating technology transfer, expertise sharing, and accelerated market access. Furthermore, the competitive dynamics of the gene therapy landscape, combined with patent exclusivity considerations and first-mover advantages in key therapeutic areas, are intensifying pharmaceutical company engagement and investment across all stages of the AAV product development lifecycle.

Regional Insights:

- Australian Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australian Capital Territory & New South Wales holds the largest share, accounting for 39.4% of the total Australia adeno-associated virus gene therapy market in 2025.

The region dominates the market, supported by premier research institutions, leading teaching hospitals, and advanced biotechnology infrastructure concentrated in Sydney and surrounding areas. The region hosts major academic medical centers conducting cutting-edge gene therapy research and clinical trials, creating a robust ecosystem for therapeutic innovation and translation. The presence of established pharmaceutical company headquarters and specialized biotechnology clusters strengthens the region's competitive position in attracting investment and advancing clinical development programs.

New South Wales benefits from strong government support for biotechnology development and healthcare innovation, including dedicated funding programs and industry collaboration initiatives. Accordingly, NSW contributed USD 35.1 Billion economically and hosting 35% of Australia’s MedTech ecosystem. Strong clinical trial networks, GMP viral vector manufacturing investment, and advanced therapeutics research position NSW as a global biotech innovation leader. Additionally, the Royal Children's Hospital, Westmead Hospital, and university-affiliated research centers provide critical infrastructure for patient recruitment and clinical trial execution. Additionally, the region's proximity to regulatory authorities and access to specialized manufacturing capabilities through local CDMOs enhance its attractiveness for gene therapy sponsors seeking efficient pathways to market authorization and commercial launch across the Australian healthcare system.

Market Dynamics:

Growth Drivers:

Why is the Australia Adeno-associated Virus Gene Therapy Market Growing?

Rising Prevalence of Genetic and Neurological Disorders

The increasing incidence of genetic and neurological disorders across Australia represents a fundamental driver for the adeno-associated virus gene therapy market, as these conditions often lack effective conventional treatment options and present significant unmet medical needs. For instance, the Australian Institute of Health and Welfare reported that in 2022, about 8.7% of Australians (around 2.2 million people) were living with long-term neurological conditions, with females nearly twice as likely as males to be affected (11% compared with 6.1%). Furthermore, the growing awareness of genetic testing and improved diagnostic capabilities are enabling earlier identification of patients who could benefit from AAV gene therapies. Australia's aging population and expanding newborn screening programs are further amplifying the identification of treatable genetic conditions, creating sustained demand for curative gene therapy approaches that can address the underlying molecular causes of disease rather than merely managing symptoms.

Expanding Regulatory Approvals and Favorable TGA Pathways

The progressive expansion of regulatory approvals for AAV gene therapies is catalyzing market growth by validating therapeutic efficacy and establishing reimbursement precedents that improve patient access. Australia's Therapeutic Goods Administration approved multiple gene therapies including Zolgensma for spinal muscular atrophy and Luxturna for inherited retinal dystrophy, creating established regulatory pathways for subsequent product approvals. The TGA's alignment with international regulatory standards and participation in collaborative review mechanisms facilitate efficient evaluation of innovative therapies. For example, in November 2025, the FDA approved Novartis' intrathecally-delivered version of Zolgensma for treating spinal muscular atrophy in patients aged two years and older, demonstrating continued regulatory momentum that will influence Australian therapeutic access and market expansion.

Government Investment in Advanced Therapeutic Manufacturing Infrastructure

Substantial government investment in clinical trial infrastructure and advanced therapeutic manufacturing capabilities is strengthening Australia's position as an attractive destination for gene therapy development and commercialization. Public funding programs are supporting the expansion of GMP manufacturing capacity, clinical trial site capabilities, and specialized workforce development essential for the cell and gene therapy sector. These investments are creating the foundational capabilities necessary to support local production, reduce supply chain dependencies, and accelerate patient access to transformative AAV gene therapies across the Australian healthcare system.

Market Restraints:

What Challenges the Australia Adeno-associated Virus Gene Therapy Market is Facing?

High Manufacturing Costs and Production Complexity

AAV gene therapy manufacturing remains exceptionally complex and capital-intensive, requiring specialized facilities, highly trained personnel, and stringent quality control processes that significantly elevate production costs. The limited number of manufacturers with validated AAV production capabilities creates capacity constraints and extends development timelines for clinical programs. Scaling production from clinical to commercial volumes while maintaining product consistency and meeting regulatory standards presents substantial technical challenges that can impact market growth and therapeutic accessibility across Australia's healthcare system.

Pre-existing Anti-AAV Antibodies Limiting Patient Eligibility

A major challenge for AAV gene therapies is the presence of pre-existing antibodies in many individuals, developed through natural exposure to wild-type viruses. These antibodies can neutralize therapeutic vectors before they reach target tissues, reducing treatment effectiveness and limiting patient eligibility for clinical use. As a result, patients often require antibody screening prior to therapy, which narrows the addressable population for many programs. This immunological barrier is driving research into engineered capsids with lower immunogenicity, alternative serotypes, and re-dosing strategies that could expand access and improve outcomes.

Safety Concerns Requiring Enhanced Monitoring Protocols

Safety remains a critical consideration in the development and commercialization of AAV-based gene therapies, requiring strict monitoring and risk management. Clinical experience has highlighted potential adverse effects, including immune-mediated responses, liver toxicity, and inflammatory complications, which can influence patient selection and treatment protocols. These concerns have led regulators and developers to adopt more intensive follow-up requirements, optimized dosing regimens, and supportive immunosuppressive strategies. Ongoing pharmacovigilance and long-term safety studies are essential to better characterize risks, build clinical confidence, and support broader adoption of AAV gene therapies across diverse patient populations.

Competitive Landscape:

The Australia adeno-associated virus gene therapy market features a competitive landscape characterized by global pharmaceutical leaders, specialized biotechnology firms, and emerging regional players focused on advancing therapeutic innovation. Competition is intensifying through investments in proprietary vector engineering platforms, strategic acquisitions of gene therapy developers, and expansion of manufacturing capabilities. Companies are differentiating through deep regulatory expertise, efficient clinical development pathways, and comprehensive commercialization strategies. Strategic partnerships between international sponsors and Australian research institutions are fostering technology transfer and accelerating product development timelines. The market is witnessing consolidation as larger players seek to strengthen their gene therapy portfolios while smaller innovators pursue partnerships for manufacturing access and regulatory support.

Recent Developments:

- In January 2026, the Centenary Institute researchers obtained NHMRC Ideas Grants to fund their research on gene therapy and liver disease. Dr Chuck Bailey received USD 1.94 Million to develop safer AAV gene therapy methods which include his work on Pompe disease. Associate Professor Patrick Bertolino received USD 1.36 Million to investigate immune-liver interactions which will help him develop new treatment methods and vaccines.

- In October 2025, Australia established its initial clinical and commercial viral vector CDMO facility VVMF at Westmead Health and Innovation Precinct in Sydney Australia. The facility will manufacture GMP-grade lentiviral and AAV vectors which will support gene and cell therapy development as well as clinical production and technology transfer and advanced biomanufacturing development through its USD 134.5 Million funding from New South Wales.

Australia Adeno-associated Virus Gene Therapy Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Therapeutic Areas Covered |

|

|

Vector Serotypes Covered |

AAV1, AAV2, AAV3, AAV4, AAV5, AAV6, AAV7, AAV8, AAV9, AAV10, AAV11, AAV12, Engineered/Synthetic/Hybrid Capsids |

|

Routes of Administration Covered |

Intravenous (I.V.), Intrathecal (I.T.) (for CNS delivery), Intraocular (I.O.) (e.g., intravitreal, subretinal), Intramuscular (I.M.), Intracerebral, Subcutaneous, Local/Direct Injection (e.g., into specific organs) |

|

Applications Covered |

Preclinical Therapies, Clinical Therapies, Commercialized Therapies |

|

Manufacturing Types Covered |

In-House Manufacturing, CDMOs and Vector Production Facilities |

|

End Users Covered |

Pharmaceutical and Biotechnology Companies, Academic and Research Institutions, Contract Research Organizations (CROs) |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Adeno-associated Virus Gene Therapy Market Report

The Australia adeno-associated virus gene therapy market reached a value of USD 76.13 Million in 2025.

The market is expected to grow at a compound annual growth rate of 38.42% from 2026-2034 to reach USD 1,420.12 Million by 2034.

Neurological disorders held the largest market share at 36.8%, driven by the rising prevalence of neurodegenerative diseases, limited conventional treatment alternatives, and the superior ability of AAV vectors to cross the blood-brain barrier for central nervous system targeting.

Key factors driving growth in the Australia adeno-associated virus gene therapy market include the rising prevalence of genetic and neurological disorders, expanding regulatory approvals through favorable TGA pathways, government investment in manufacturing infrastructure, AI advancements in vector engineering, and increasing pharmaceutical company investment in gene therapy portfolios.

Major challenges include high manufacturing costs and production complexity, pre-existing anti-AAV antibodies limiting patient eligibility, safety concerns requiring enhanced monitoring protocols, limited specialized manufacturing capacity, and reimbursement complexities for high-cost curative therapies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)