Australia Aerospace Insurance Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Australia Aerospace Insurance Market Summary:

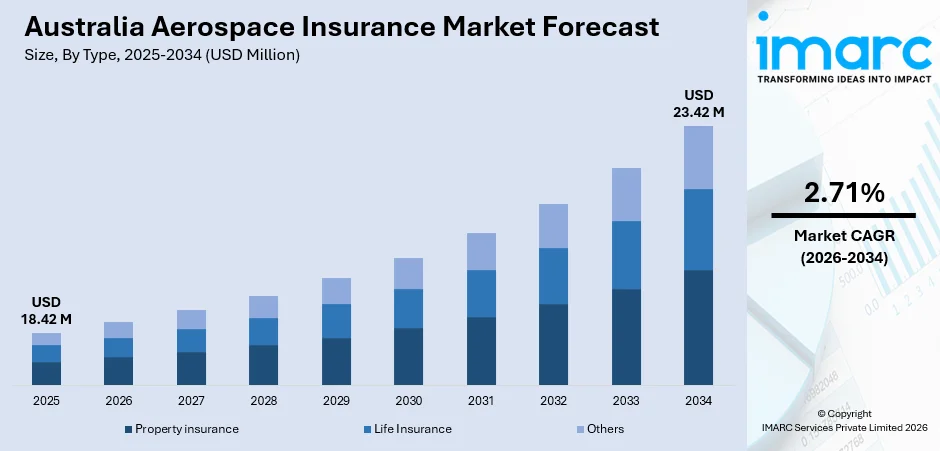

The Australia aerospace insurance market size was valued at USD 18.42 Million in 2025 and is projected to reach USD 23.42 Million by 2034, growing at a compound annual growth rate of 2.71% during 2026-2034.

The Australia aerospace insurance market is gaining momentum as the country’s aviation sector experiences significant expansion in airport infrastructure, fleet modernization, and rising air passenger traffic. Increasing commercial operations, growing UAV adoption, and evolving regulatory requirements are driving demand for comprehensive coverage solutions. Advancements in underwriting technologies, expanding risk management frameworks, and rising defense aviation investments are contributing to sustained growth in the Australia aerospace insurance market share.

Key Takeaways and Insights:

- By Type: Property insurance holds the largest market share at 58.4% in 2025, establishing itself as the leading coverage category in Australia’s aerospace insurance landscape.

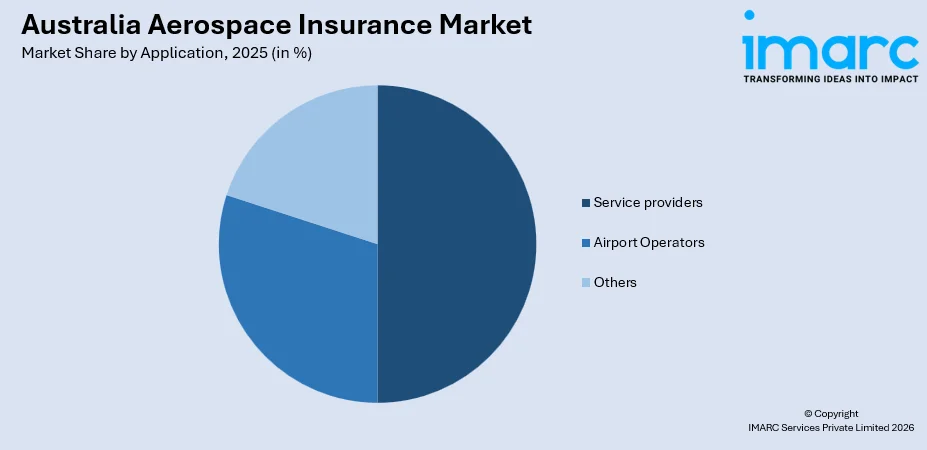

- By Application: Service providers dominate the market with a 46.7% share in 2025, reflecting their critical role in supporting aviation operations and maintenance activities across the country.

- By Region: Australia Capital Territory and New South Wales accounts for the highest revenue share at 38.6% in 2025, driven by concentrated aviation infrastructure and major airport operations in the region.

- Key Players: The Australia aerospace insurance market is competitive, with major insurers expanding coverage portfolios, leveraging advanced risk modeling, forming strategic partnerships, and enhancing underwriting capabilities to strengthen their position across the growing aerospace sector.

To get more information on this market Request Sample

The Australia aerospace insurance market is advancing as the country continues to strengthen its aviation ecosystem through major infrastructure investments and fleet expansion programs. In line with this, rising air passenger traffic, growing drone operations, and strengthened regulatory oversight are creating a favorable environment for insurance adoption. For instance, domestic air traffic in Australia surpassed pre-pandemic benchmarks, reaching approximately 3.7 million aircraft movements in FY2024. Additionally, expanding risk assessment technologies and the rising value of aerospace assets are further supporting robust market development across the country. The increasing defense aviation spending and modernization of military fleets are expanding demand for specialized coverage in the market. At the same time, greater use of advanced aircraft and maintenance technologies is elevating asset values and liability exposure, further supporting sustained market growth across Australia.

Australia Aerospace Insurance Market Trends:

Integration of advanced data analytics in aerospace underwriting

Australia’s aerospace insurance sector is increasingly leveraging data analytics and real-time flight data to refine underwriting models and improve risk assessment accuracy. For instance, in March 2025, Brisbane Airport partnered with Cirium to integrate Cirium Sky Warehouse, a cloud-based platform, to enhance operational efficiency. This integration supports advanced flight scheduling, resource allocation, and passenger experience, leveraging data analytics for 25 million passengers, with a projected 10 million more by 2032.

Rising demand for unmanned aerial vehicle insurance coverage

The rapid proliferation of commercial drones across industries such as agriculture, mining, logistics, and emergency services is generating strong demand for specialized UAV insurance coverage in Australia. For example, in March 2024, remote-pilot license holders in Australia rose to 33,388, surpassing the 30,843 conventional pilots registered in the country. This shift is expanding the scope of aerospace insurance products and encouraging insurers to develop tailored coverage solutions for commercial and recreational drone operators.

Expansion of cyber-aviation risk coverage

As Australia’s aviation industry increasingly relies on digital technologies and interconnected systems, the need for cyber-risk coverage within aerospace insurance portfolios is intensifying. For instance, in 2024, cyber-aviation risk coverage had expanded to 41% of aerospace insurance portfolios globally, reflecting a 17% rise in aviation-related cyber incidents. Hence, insurers are developing targeted cyber policies to protect airlines, airports, and service providers from data breaches, system failures, and emerging digital threats.

Market Outlook 2026-2034:

Australia’s aerospace insurance market is poised for steady expansion, driven by ongoing airport infrastructure development, fleet modernization programs, and a strengthening regulatory environment. In tandem, continued growth in domestic and international air traffic, is expected to create substantial new insurance demand. Likewise, increasing adoption of advanced underwriting technologies, expanding drone operations, and rising defense aviation spending under Australia’s National Defence Strategy are anticipated to further fuel market growth. A such, the Albanese Government is strengthening Australia’s Defence by investing USD 57.6 Billion over a decade, accelerating capability acquisition, expanding the ADF, implementing the Defence Strategic Review, and enhancing operational readiness amid global strategic uncertainty. Additionally, the entry of new insurance capacity providers and the development of specialized coverage products for emerging aerospace risks such as UAVs and cyber vulnerabilities will strengthen the market’s long-term trajectory and foster a more competitive insurance landscape across the country. The market generated a revenue of USD 18.42 Million in 2025 and is projected to reach a revenue of USD 23.42 Million by 2034, growing at a compound annual growth rate of 2.71% during 2026-2034.

Australia Aerospace Insurance Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Property Insurance |

58.4% |

|

Application |

Service Providers |

46.7% |

|

Region |

Australia Capital Territory and New South Wales |

38.6% |

Type Insights:

- Life Insurance

- Property Insurance

- Others

Property insurance leads the market with a revenue share of 58.4% of the total Australia aerospace insurance market in 2025.

Property insurance plays a vital role in Australia’s aerospace sector by safeguarding physical assets including aircraft, airport infrastructure, hangars, and ground equipment against damage from accidents, natural disasters, and operational risks. Australia’s growing aviation infrastructure is driving stronger demand for comprehensive property coverage. For instance, Western Sydney International Airport, a major infrastructure project with an initial capacity to handle up to 10 million annual passengers, is set to open in 2026. The expansion of airport facilities and increasing fleet values are generating greater need for property insurance products across the country.

The property insurance segment’s dominance is further reinforced by ongoing fleet modernization and maintenance facility investments across Australia. As such, in February 2025, Textron Aviation announced the construction of a new 3,343-square-metre service facility at Essendon Fields Airport in Melbourne to support more than 1,400 aircraft operating across the Asia-Pacific region. The rising value of aviation assets, coupled with heightened exposure to environmental and operational risks, is driving airport operators and airlines to invest more in property insurance solutions to protect their expanding infrastructure and fleet portfolios.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Service Providers

- Airport Operators

- Others

Service providers dominate the market with a share of 46.7% in the total Australia aerospace insurance market in 2025.

Service providers constitute the largest application segment in Australia’s aerospace insurance market, encompassing maintenance, repair, and overhaul (MRO) operators, ground handling companies, fueling services, and aviation support businesses. These entities require extensive insurance coverage to protect against liabilities arising from third-party property damage, bodily injury, and product defects. Australia’s growing fleet operations are fueling demand for insured service activities.

The continued expansion of service infrastructure is further driving demand within this segment. For example, in August 2025, BESIX Watpac won the contract for Adelaide Airport’s Project Flight, expanding terminals, check-in areas, and integrating advanced technology. Building on a 15-year partnership, the company ensures safe, efficient, and future-ready airport infrastructure. As more specialized service providers enter the market and existing operators expand their offerings, the need for tailored insurance products covering professional liability, equipment protection, and operational risks continues to grow substantially across the country.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria and Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales accounts for the highest revenue share of 38.6% in the total Australia aerospace insurance market in 2025.

Australia Capital Territory & New South Wales represent the dominant regional market for aerospace insurance, anchored by the presence of Sydney Kingsford Smith Airport, the nation’s busiest aviation hub, along with a dense concentration of airline headquarters, MRO facilities, and aviation service providers. The region is further strengthened by the infrastructure expansion generating significant new demand for property, liability, and operational insurance coverage across the aerospace sector.

The region also benefits from a strong defense and general aviation presence, with key aerospace assets located across the ACT and Greater Sydney areas. Airlines such as Qantas have committed to operating up to 15 aircraft and approximately 25,000 domestic flights annually from Western Sydney International in its first year of operation. The combination of commercial aviation growth, defense procurement activities, expanding MRO operations, and a favorable regulatory environment is reinforcing ACT and New South Wales’s position as the primary hub for aerospace insurance demand in Australia.

Market Dynamics:

Growth Drivers:

Why is the Australia Aerospace Insurance Market Growing?

Expanding airport infrastructure and modernization programs

Australia is witnessing significant investments in airport development and modernization, which are directly contributing to rising aerospace insurance demand. The construction of new terminals, runways, and associated facilities increases the value of insured assets and expands the scope of required coverage. For instance, in February 2025, Bechtel selected Perth Airport’s multi-billion-dollar expansion, adding a new runway, terminal, hotel, and two multi-story car parks. Passenger numbers are expected to grow from 16 million to 20 million annually by 2030, boosting jobs and regional economy. Such large-scale infrastructure projects increase insurance requirements for property, liability, and construction-related risks, supporting the overall growth of the aerospace insurance market across Australia.

Rising air passenger traffic and fleet expansion

The steady growth in domestic and international air passenger traffic across Australia is driving airlines and operators to expand and modernize their fleets, creating additional demand for aerospace insurance coverage. As airlines introduce newer aircraft models and expand their route networks, the value of insured assets rises accordingly. Fleet modernization programs, including the adoption of fuel-efficient next-generation aircraft such as the Airbus A321neo and Boeing 737 MAX, are increasing per-unit asset values and driving demand for comprehensive hull and liability insurance solutions across both commercial and regional aviation operators in Australia.

Growing defense spending and aviation procurement

Australia’s increased defense spending is generating demand for specialized aerospace insurance products covering military aircraft, training operations, and support services. For instance, Australia’s 2024 National Defence Strategy earmarks USD 330 Billion for air capabilities over the decade, including program expansions for F-35A fighters and P-8A maritime patrol aircraft. These investments are expanding the range of insured defense aviation assets and creating new insurance requirements for advanced aircraft, drone operations, and defense contractor activities. The growing scale of military aviation procurement, combined with increasingly complex operational environments, is driving insurers to develop specialized coverage products and risk management solutions tailored to Australia’s evolving defense aerospace sector.

Market Restraints:

What Challenges the Australia Aerospace Insurance Market is Facing?

Limited specialized underwriting expertise

The Australia aerospace insurance market faces challenges due to a shortage of specialized underwriting talent capable of accurately assessing complex aviation and space-related risks. Aerospace insurance requires deep technical knowledge of aircraft operations, regulatory environments, and emerging technologies such as drones and satellite systems. The limited pool of experienced aerospace underwriters constrains insurers’ ability to price risks effectively and develop innovative coverage products tailored to Australia’s evolving aviation landscape.

Geopolitical instability and claims uncertainty

Ongoing geopolitical tensions and international conflicts create uncertainty within the aerospace insurance market, particularly regarding war risk coverage and excess liability claims. The resolution of large-scale claims, including those related to aircraft trapped or lost in conflict zones, introduces pricing volatility and complicates risk assessment. Insurers must navigate unpredictable geopolitical developments while maintaining adequate reserves and pricing discipline, which can constrain market capacity and increase premium costs for Australian aerospace operators.

Rising claims severity amid declining incident rates

Although aviation safety has improved and incident rates have declined, the severity of individual claims continues to rise due to increasing aircraft values, higher repair costs, and growing liability awards. The escalating cost of aircraft parts, advanced avionics, and specialized materials means that even minor incidents can result in substantial insurance payouts. Additionally, evolving legal frameworks and higher compensation standards are amplifying claim values, placing pressure on insurers to maintain profitability while keeping premiums competitive in the Australian market.

Competitive Landscape:

The Australia aerospace insurance market is moderately competitive, with global insurers and specialized underwriting agencies expanding their presence in the region. Leading players are focusing on portfolio diversification, advanced risk modeling, and digital underwriting platforms to enhance operational efficiency and customer service. Competition is driven by capacity availability, pricing strategies, and the ability to offer customized coverage solutions across diverse aerospace segments including airlines, general aviation, airports, and UAV operators. Strategic collaborations and capacity partnerships are enabling insurers to broaden their market reach and strengthen their position within Australia’s growing aerospace sector.

Recent Developments:

- In November 2025, Sydney Airport launched a global tender for consulting partners to support its AUD 6 Billion (USD 3.2 Billion) five-year infrastructure programme. Key projects include connecting T2 and T3 terminals, adding 12 swing gates, boosting efficiency, and accommodating 72 million passengers annually by 2045, emphasizing integrated delivery and long-term design excellence.

- In November 2025, NRMA Insurance launched a large-scale out-of-home campaign across Sydney and Adelaide airports, featuring prime locations like aerobridges, a 2,000 m² T1 display, and digital large-format sites. The campaign targets over 50 million annual passengers, reinforcing brand visibility during its centenary year.

Australia Aerospace Insurance Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Life Insurance, Property Insurance, Others |

|

Applications Covered |

Service Providers, Airport Operators, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria and Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Aerospace Insurance Market Report

The Australia aerospace insurance market size was valued at USD 18.42 Million in 2025.

The market is expected to grow at a compound annual growth rate of 2.71% during 2026-2034 to reach USD 23.42 Million by 2034.

Property insurance, holding the largest revenue share of 58.4%, remains pivotal for Australia’s aerospace insurance market, providing comprehensive coverage for aircraft, airport infrastructure, and ground equipment against physical damage and operational risks.

Key factors driving the Australia aerospace insurance market include expanding airport infrastructure, rising air passenger traffic, fleet modernization programs, growing defense aviation spending, increasing UAV adoption, and evolving regulatory requirements.

Major challenges include limited specialized underwriting expertise, geopolitical instability affecting war risk coverage, rising claims severity, and the need to develop innovative products for emerging risks such as cyber threats and unmanned aerial vehicles.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)