Australia Agricultural Chelates Market Size, Share, Trends and Forecast by Type, Crop Type, Application, and Region, 2026-2034

Australia Agricultural Chelates Market Summary:

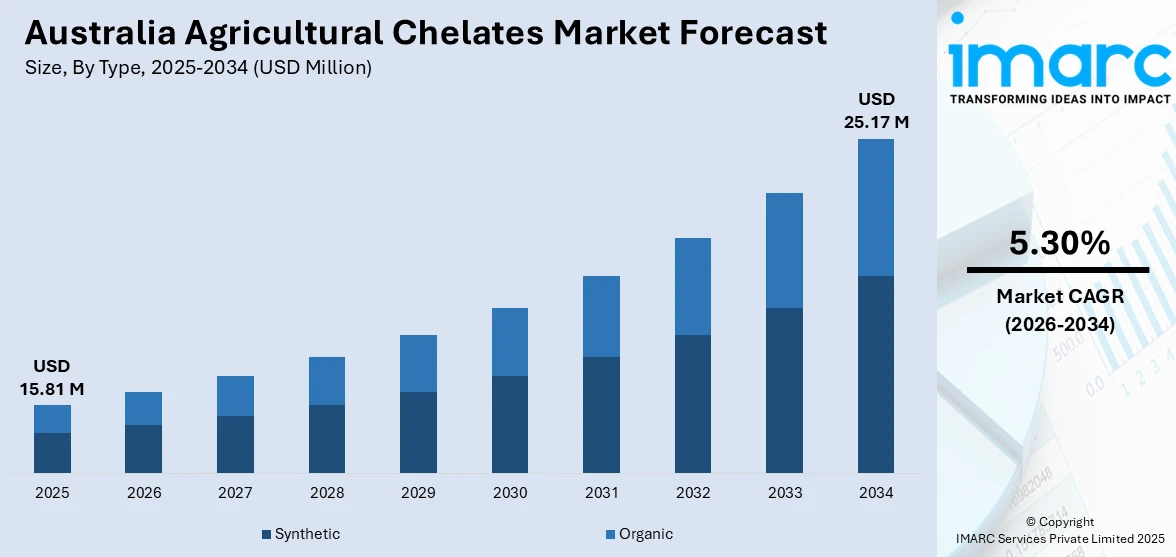

The Australia agricultural chelates market size was valued at USD 15.81 Million in 2025 and is projected to reach USD 25.17 Million by 2034, growing at a compound annual growth rate of 5.30% from 2026-2034.

The market's growth is underpinned by increasing awareness of micronutrient management in addressing Australia's widespread soil deficiencies, particularly across alkaline soils that comprise nearly one-quarter of the nation's agricultural land. The rising adoption of precision agriculture technologies, coupled with government initiatives promoting sustainable farming practices, is driving demand for chelated fertilizers that enhance nutrient bioavailability and crop productivity. The shift toward intensive farming systems in grain production and high-value horticulture, combined with the need to optimize yield on limited arable land, is expanding the Australia agricultural chelates market share.

Key Takeaways and Insights:

- By Type: Synthetic dominates the market with a share of 68.9% in 2025, driven by their superior nutrient stability and effectiveness in alkaline soil conditions prevalent across Australian farmlands.

- By Crop Type: Grains and cereals lead the market with a share of 39.7% in 2025, reflecting the sector's critical role in Australia's agricultural exports and the extensive micronutrient requirements of wheat and barley cultivation.

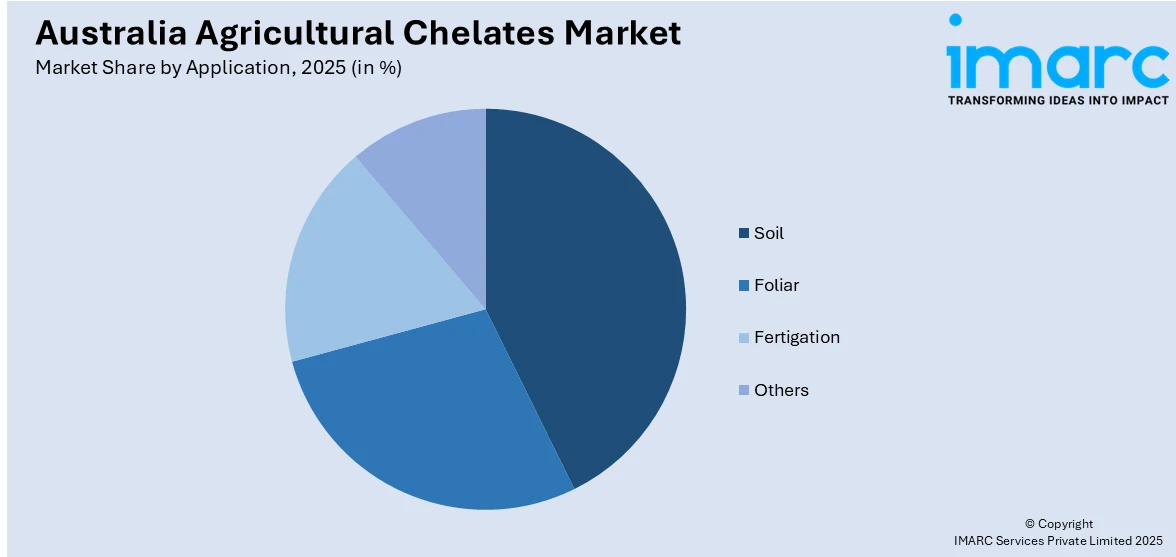

- By Application: Soil represents the largest segment with a market share of 47.7% in 2025, preferred for its direct nutrient delivery to root zones and compatibility with mechanical spreading equipment used in broadacre farming systems.

- By Region: Australian Capital Territory & New South Wales account for 35.4% market share in 2025, underpinned by diverse agricultural landscapes spanning extensive wheat production, intensive irrigation horticulture, and well-established distribution network.

- Key Players: The Australia agricultural chelates market features both multinational specialty chemical corporations and regional agricultural input suppliers, competing across product quality, technical support, and distribution networks tailored to diverse farming regions.

To get more information on this market Request Sample

The Australia agricultural chelates market is experiencing transformation driven by the convergence of sustainable agriculture imperatives and technological advancement. Over eight million hectares of agricultural land, particularly in southwest Western Australia, require strategic micronutrient applications to address widespread zinc, copper, and molybdenum deficiencies resulting from the nation's ancient, nutrient-poor soils. The integration of precision agriculture technologies with chelated fertilizer applications is enabling farmers to achieve targeted nutrient delivery, reducing wastage while improving crop health across variable soil conditions. Owing to these benefits, various companies in the country are focussing on the launch of precision tools for farming which make the use of fertilizers effortless. For example, in 2025, Yamaha Motor Corporation, Limited. (“Yamaha”) unveiled Yamaha Agriculture, Inc., a new venture dedicated to providing autonomous machinery and AI-driven digital solutions that assist specialty crop producers in becoming more sustainable, profitable, and adaptive to the challenges posed by diminishing resources and climate change. Yamaha Agriculture will offer robotics solutions for spraying, weeding, and other field tasks by strategically acquiring Robotics Plus1 and The Yield, while utilizing advanced data analytics and AI to facilitate precision farming and informed decision-making for growers of wine grapes, apples, and other specialty crops in North America, Australia, and New Zealand.

Australia Agricultural Chelates Market Trends:

Accelerating Integration of Precision Agriculture Technologies

The Australian agricultural sector is witnessing rapid adoption of precision agriculture tools, fundamentally transforming how farmers manage micronutrient applications. The Australian government allocated AUD 1.5 billion in 2024 to enhance sustainable agriculture and environmental resilience across the country. This evolution is particularly evident in the grains sector, where variable-rate application systems deliver chelated micronutrients based on precise soil mapping data. The Australia precision agriculture market reached USD 261 Million in 2024, reflecting a nine percent annual growth trajectory as farmers leverage GPS-guided equipment, drone-based crop monitoring, and data analytics platforms to optimize chelate applications, ensuring nutrients reach deficient zones while avoiding over-application in areas with adequate micronutrient levels.

Heightened Focus on Soil Health and Regenerative Farming Practices

Australian farmers are increasingly prioritizing soil health management as the foundation for sustainable productivity, with 85 percent of broadacre cropping farms retaining stubble and 68 percent minimizing tillage operations. This shift toward regenerative agriculture is driving demand for chelated micronutrients that support long-term soil fertility rather than providing merely short-term yield boosts. Recently, the Australian Government is collaborating with states and territories to implement 17 projects aimed at tackling one or more priority actions of the National Soil Action Plan (2023-2028) via explicit, quantifiable commitments to localized initiatives.

Growing Development of Bio-Based and Biodegradable Chelate Formulations

The Australia agricultural chelates market is experiencing innovation in environmentally sustainable chelate formulations, responding to increasing regulatory scrutiny and consumer demand for eco-friendly agricultural inputs. In 2024, The Australian Government allocated $40.7 million to establish a national network of Sustainable Agriculture Facilitators as part of the Climate-Smart Agriculture Program, financed by the Natural Heritage Trust (NHT). Manufacturers are developing bio-based chelates derived from amino acids and organic acids that offer improved biodegradability compared to traditional EDTA formulations, aligning with Australia's sustainable agriculture frameworks. This trend reflects broader industry movement toward controlled-release fertilizers and precision nutrient delivery systems that minimize environmental impact while maintaining agronomic effectiveness. Research institutions across Australia are collaborating with agrochemical companies to evaluate novel chelating agents that maintain micronutrient availability in alkaline soils while reducing persistence in soil environments, addressing farmer concerns about long-term soil health and regulatory compliance under tightening environmental standards.

Market Outlook 2026-2034:

The Australia agricultural chelates market is positioned for sustained expansion through 2032, driven by intensifying pressure to enhance agricultural productivity on limited arable land amid climate variability and resource constraints. The market generated a revenue of USD 15.81 Million in 2025 and is projected to reach a revenue of USD 25.17 Million by 2034, growing at a compound annual growth rate of 5.30% from 2026-2034. The integration of artificial intelligence (AI) and remote sensing technologies with variable-rate fertilizer systems will transform chelate application efficiency, thereby strengthening domestic fertilizer supply chains, potentially creating downstream opportunities for chelate manufacturers. Growing consumer preference for sustainably produced agricultural commodities will accelerate adoption of precision nutrient management systems, supporting steady market expansion across Australia's diverse agricultural regions.

Australia Agricultural Chelates Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Synthetic |

68.9% |

|

Crop Type |

Grains and Cereals |

39.7% |

|

Application |

Soil |

47.7% |

|

Region |

Australia Capital Territory & New South Wales |

35.4% |

Type Insights:

- Synthetic

- EDTA

- EDDHA

- DTPA

- IDHA

- Others

- Organic

- Lignosulfonates

- Aminoacids

- Heptagluconates

- Others

Synthetic dominates with a market share of 68.9% of the total Australia agricultural chelates market in 2025.

Synthetic chelates maintain market dominance through their superior performance characteristics in addressing Australia's unique soil challenges, particularly the widespread occurrence of alkaline soils with pH ranges between 4 and 8.5 across western regions. EDTA chelates demonstrate exceptional stability across broad pH ranges and effectively deliver micronutrients such as zinc, iron, manganese, and copper in calcareous soils that dominate much of Australia's prime agricultural land. The segment's strength reflects farmers' preference for proven nutrient delivery systems that ensure consistent crop response across variable environmental conditions.

Synthetic chelates offer agronomic advantages that resonate strongly with Australia's large-scale broadacre farming operations, where reliability and mechanical application compatibility determine input selection. These compounds integrate seamlessly with precision agriculture technologies, enabling variable-rate application systems to deliver targeted micronutrient doses based on soil testing and yield mapping data. The segment benefits from extensive research validating long-term residual effectiveness, exemplified by South Australian studies showing copper chelate applications maintaining crop response for over 30 years after initial treatment. Farmers appreciate synthetic chelates' predictable performance characteristics and compatibility with existing fertigation infrastructure, particularly in protected cropping systems and high-value horticulture where precise nutrient management directly impacts crop quality and market value, justifying the premium pricing associated with chelated formulations over conventional inorganic micronutrient sources.

Crop Type Insights:

- Grains and Cereals

- Pulses and Oilseeds

- Commercial Crops

- Fruits and Vegetables

- Turf and Ornamentals

Grains and cereals lead with a share of 39.7% of the total Australia agricultural chelates market in 2025.

The segment's dominance reflects Australia's position as a major wheat and barley exporter, with grain crops occupying the majority of the nation's agricultural land, particularly across New South Wales, Victoria, and Western Australia's extensive wheatbelt regions. Grain crops demonstrate high responsiveness to chelated micronutrient applications, particularly zinc and manganese, which are frequently deficient in Australia's ancient, weathered soils. The shift from superphosphate to ammonium phosphate fertilizers during the late 1980s precipitated widespread zinc deficiency symptoms across South Australian pastures and cereal crops, establishing regular zinc chelate applications as standard practice in modern grain production systems. The segment's growth is reinforced by Australia's export-oriented grain sector, where wheat production enters international markets, driving farmers to maximize yield potential and grain quality through comprehensive nutrient management programs.

Grain producers are increasingly adopting chelated micronutrients as part of integrated precision agriculture strategies that optimize input efficiency while managing production costs in globally competitive markets. Research conducted across various field trials demonstrated yield responses to chelated micronutrient applications in several trial sites, validating the agronomic effectiveness of targeted chelate use in deficient soils. The emergence of conservation tillage practices, adopted by broadacre farms, has altered nutrient cycling dynamics and increased the importance of readily available micronutrient sources like chelates that remain accessible in no-till systems. Additionally, plant tissue surveys reveal wheat grain consistently showing zinc concentrations below recommendations for human health, prompting consideration of biofortification strategies through enhanced zinc chelate applications, creating additional demand drivers beyond traditional agronomic yield optimization objectives.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Soil

- Foliar

- Fertigation

- Others

Soil exhibits a clear dominance with a 47.7% share of the total Australia agricultural chelates market in 2025.

Soil-applied chelates align perfectly with Australia's mechanized broadacre farming operations, where granular and liquid fertilizer application equipment enables efficient coverage of extensive paddocks during planting or as broadcast top-dressing operations. This application method delivers micronutrients directly to the root zone, where chelates protect metal ions from precipitation and sorption reactions in alkaline soils, ensuring sustained nutrient availability throughout critical crop growth stages. The method's popularity stems from operational simplicity and compatibility with existing farm equipment, allowing integration into established fertilizer application routines without requiring specialized spraying infrastructure or additional field passes. Australian grain farmers particularly favor soil applications for their ability to address long-term micronutrient deficiencies through single applications that provide multi-season residual benefits, exemplified by research demonstrating copper applications maintaining effectiveness for decades in Western Australian soils.

The soil application segment benefits from advances in controlled-release fertilizer technologies that enhance chelate efficiency while reducing environmental impacts, aligning with sustainability objectives embedded in Australian agricultural policy frameworks. Recent developments in multi-nutrient fluid fertilizers have demonstrated superior response efficiency compared to granular formulations on calcareous soils prevalent across southern growing regions, driving innovation in soil-applied chelate products. Farmers appreciate the flexibility of soil applications for addressing diagnosed deficiencies revealed through routine soil testing programs, with plant analysis providing reliable prediction and confirmation of micronutrient status in crops and pastures. The integration of precision soil sampling techniques with GPS-guided variable-rate spreaders enables targeted chelate placement in deficient zones within individual paddocks, optimizing nutrient distribution while minimizing input costs across Australia's diverse soil landscapes.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales leads with a share of 35.4% of the total Australia agricultural chelates market in 2025.

The region's leadership reflects its diverse agricultural landscape encompassing extensive wheat and barley production across the inland slopes and plains, intensive horticulture in Murray-Darling Basin irrigation districts, and high-value specialty crop cultivation in coastal regions. New South Wales farmers confront varied soil challenges ranging from acidic soils in high-rainfall zones to alkaline conditions in western districts, creating sustained demand for chelated micronutrients that ensure nutrient availability across pH spectrums. The state's agricultural productivity benefits from well-established distribution networks connecting major port facilities at Newcastle and Port Kembla with inland farming communities, enabling efficient chelate product supply chains. The region hosts concentrated agricultural research infrastructure, including university experimental farms and government research stations that validate chelate efficacy and develop application recommendations tailored to local soil conditions and cropping systems.

The Australia Capital Territory and New South Wales agricultural sector embraces technology adoption at rates exceeding national averages, with precision farming tools enabling optimized chelate applications guided by detailed soil mapping and yield monitoring data. The region's farmers demonstrate sophisticated understanding of micronutrient management, supported by extensive agronomic advisory services and soil testing laboratories that provide diagnostic capabilities for identifying specific deficiencies requiring chelate intervention. Northern inland regions face increasing production challenges from climate variability, driving interest in chelated formulations that improve stress tolerance and maintain crop productivity under water-limited conditions. The expansion of cotton cultivation into northern New South Wales districts creates additional chelate demand for this micronutrient-responsive crop, while the region's viticulture sector in Hunter Valley and riverine areas utilizes chelated iron and zinc to address chlorosis issues in alkaline vineyard soils, supporting premium wine grape production.

Market Dynamics:

Growth Drivers:

Why is the Australia Agricultural Chelates Market Growing?

Widespread Micronutrient Deficiencies in Australian Agricultural Soils

Australia's ancient geological landscape has produced soils of exceptionally low natural fertility, with documented deficiencies spanning all known plant nutrients across diverse agricultural regions. Zinc and molybdenum deficiencies prove most prevalent, occurring commonly on alkaline and acid soils respectively, while zinc deficiency specifically affects all soil classes including sandy and clayey types across both humid and arid growing environments. The presence of fine, free lime derived from shellgrit deposits blown across the continent during historical low sea-level periods has created calcareous soils particularly prone to micronutrient cation deficiencies including iron, zinc, manganese, copper, and cobalt. Multiple nutrient deficiencies frequently occur simultaneously, generating complex nutrient interaction effects that amplify the agronomic and economic importance of effective micronutrient delivery systems like chelates. In 2025, Australian farmers aiming to enhance soil health are experiencing encouraging outcomes after testing the biologically enhanced efficiency fertiliser (EEF) Fertica H+ prior to its market introduction. ProdOz International has officially introduced Seawin Biotech’s Fertica H+ after thoroughly testing the granular compound NPK fertiliser in commercial trials across Australia. ProdOz crop science technologist Zenon Kynigos stated that Fertica H+ was created specifically to enhance soil health in Australia and promote sustainable agricultural methods.

Government Policy Support and Precision Agriculture Investment Programs

Australian federal and state governments actively promote agricultural modernization through substantial funding programs that facilitate precision farming technology adoption and sustainable intensification strategies. The Australian Government has committed $53 million from 2023-24 to 2025-26 for the On Farm Connectivity Program (the Program) to help primary producers in agriculture, forestry, and fisheries enhance connectivity in their operations and utilize connected machinery and sensor technology. State-level programs provide technical assistance and cost-sharing arrangements for soil testing and nutrient management planning, reducing barriers to chelate adoption among farmers requiring evidence-based recommendations for micronutrient supplementation. The establishment of grower groups and research consortia receives government backing to demonstrate chelate effectiveness under commercial farming conditions, building farmer confidence in product performance while generating localized application guidelines that account for regional soil variations and cropping system differences across Australia's diverse agricultural zones.

Intensification of High-Value Crop Production and Export-Oriented Agriculture

Australia's agricultural sector is experiencing strategic shifts toward higher-value crop production systems that demand intensive nutrient management to achieve quality specifications for export markets. Tasmania's ambitious farm-gate value target of USD 10 Billion by 2050 relies heavily on intensive horticulture expansion supported by smart irrigation and variable-rate fertigation systems that integrate chelated micronutrient delivery. The fruits and vegetables segment demonstrates the highest growth trajectory, driven by consumer preference shifts toward fresh and organic produce that command premium pricing when produced using advanced nutrient management protocols including chelated micronutrient programs that enhance nutritional quality and post-harvest characteristics.

Market Restraints:

What Challenges the Australia Agricultural Chelates Market is Facing?

Environmental Persistence and Contamination Concerns from Synthetic Chelates

Synthetic chelating agents, particularly EDTA formulations that dominate current market applications, demonstrate limited biodegradability and extended persistence in soil environments, raising concerns about potential environmental accumulation and downstream contamination risks. These compounds can leach into groundwater systems and surface water bodies, carrying mobilized heavy metals that pose ecological hazards to aquatic organisms and soil microbial communities essential for nutrient cycling functions. Non-biodegradable chelates accumulating in agricultural soils may alter microbial community structures over extended timeframes, potentially compromising soil ecosystem services that underpin long-term agricultural sustainability. Regulatory authorities and environmental advocacy organizations increasingly scrutinize synthetic chelate usage, particularly in organic farming systems where product eligibility faces strict limitations based on environmental impact assessments and biodegradability criteria that exclude many conventional chelate formulations from approved input lists.

Premium Pricing Relative to Conventional Micronutrient Fertilizer Alternatives

Chelated micronutrient products command substantial price premiums compared to inorganic sulfate or oxide formulations, creating adoption barriers for cost-conscious farmers operating under tight profit margins in competitive global commodity markets. The manufacturing complexity and specialized raw material requirements for chelate production translate into elevated per-unit costs that farmers must justify through demonstrated yield responses or quality improvements that offset higher input expenditures. Economic viability challenges prove particularly acute in extensive broadacre grain production systems where micronutrient response magnitudes may not consistently justify chelate premiums over conventional products across all paddocks and seasons. Many Australian farmers prioritize immediate return-on-investment considerations when evaluating fertilizer purchases, potentially deferring chelate adoption until deficiency symptoms become visually apparent or yield data definitively confirms productivity limitations from micronutrient constraints rather than adopting proactive nutrient management approaches.

Limited Farmer Awareness and Technical Knowledge Regarding Optimal Chelate Application

Effective chelate utilization requires sophisticated understanding of soil chemistry, crop nutrient requirements, and product selection criteria that many farmers lack without access to specialized agronomic advisory services. The complexity of choosing appropriate chelate types for specific soil pH conditions, selecting optimal application methods, and determining proper rates creates decision-making uncertainties that discourage product trial and adoption among farmers unfamiliar with chelate technologies. Regional variation in soil micronutrient status and crop responsiveness necessitates localized research and demonstration trials to develop evidence-based application recommendations, yet such information gaps persist across many Australian agricultural districts where chelate research receives limited public investment. Educational programs and extension services providing farmers with practical chelate application guidance remain unevenly distributed across states and regions, leaving many producers reliant on fertilizer retailer recommendations that may not reflect independent agronomic optimization of nutrient management strategies.

Competitive Landscape:

The Australia agricultural chelates market exhibits moderate competitive intensity with multinational specialty chemical corporations competing alongside regional agricultural input suppliers across diverse geographic and crop market segments. Global players leverage extensive product portfolios spanning multiple chelate chemistries and application forms, supported by technical service capabilities that provide agronomic advice and soil testing services to major farming operations. These established companies benefit from long-standing relationships with fertilizer distributors and agricultural retailers who serve as primary channels connecting chelate products with end-user farmers across broadacre and intensive production systems. Regional suppliers differentiate through specialized formulations tailored to specific crop requirements and localized distribution networks that enable responsive service to farmers in remote agricultural districts. Competition extends beyond product pricing to encompass technical support quality, delivery reliability, and integration with precision agriculture platforms that enable variable-rate application capabilities increasingly demanded by technology-adopting farmers. Market participants pursue innovation in biodegradable chelate formulations and controlled-release technologies that address environmental concerns while maintaining agronomic effectiveness, positioning their portfolios to align with sustainability trends shaping farmer purchasing preferences and regulatory requirements governing fertilizer product registrations across Australian jurisdictions.

Australia Agricultural Chelates Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

|

|

Crop Types Covered |

Grains and Cereals, Pulses and Oilseeds, Commercial Crops, Fruits and Vegetables, Turf and Ornamentals |

|

Applications Covered |

Soil, Foliar, Fertigation, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Agricultural Chelates Market Report

The Australia agricultural chelates market size was valued at USD 15.81 Million in 2025.

The Australia agricultural chelates market is expected to grow at a compound annual growth rate of 5.30% from 2026-2034 to reach USD 25.17 Million by 2034.

Synthetic chelates dominated the market with 68.9% revenue share in 2025, driven by their superior performance characteristics in addressing micronutrient deficiencies prevalent in Australia's alkaline and calcareous soils that comprise nearly one-quarter of the nation's agricultural land.

Key factors driving the Australia agricultural chelates market include widespread micronutrient deficiencies in Australian agricultural soils particularly affecting zinc and molybdenum availability, government policy support through precision agriculture investment programs providing rebates for digital farming technologies, and intensification of high-value crop production for export markets where Asian buyers prioritize verified sustainable farming practices that utilize precision nutrient management solutions.

Major challenges include environmental persistence and potential contamination concerns from synthetic chelates that demonstrate limited biodegradability in soil systems, premium pricing relative to conventional micronutrient fertilizer alternatives that creates adoption barriers for cost-conscious broadacre farmers, limited farmer awareness regarding optimal chelate selection and application methodologies, and regulatory scrutiny over long-term soil accumulation risks particularly affecting organic farming system approvals where synthetic chelates face strict eligibility restrictions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)