Australia Agrochemical Market Size, Share, Trends and Forecast by Fertilizer Type, Pesticide Type, Crop Type, and Region, 2026-2034

Australia Agrochemical Market Overview:

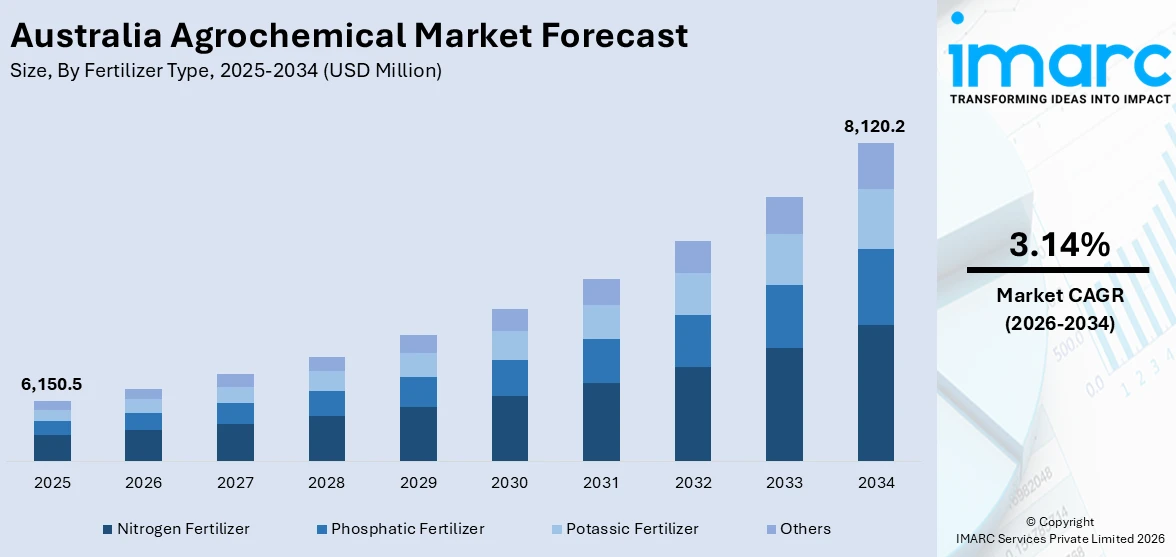

The Australia agrochemical market size reached USD 6,150.5 Million in 2025. Looking forward, the market is expected to reach USD 8,120.2 Million by 2034, exhibiting a growth rate (CAGR) of 3.14% during2026-2034. The increasing agrochemicals demand for crop protection solutions, growing need for higher agricultural productivity and sustainability, advanced formulation technologies, government support for agricultural innovations, and rising export opportunities for Australian produce are some of the factors positively impacting the Australia agrochemical market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 6,150.5 Million |

| Market Forecast in 2034 | USD 8,120.2 Million |

| Market Growth Rate (2026-2034) | 3.14% |

Australia Agrochemical Market Trends:

Shift Toward Biopesticides and Sustainable Agrochemicals

As global awareness of environmental sustainability rises, there is a noticeable shift toward biopesticides and eco-friendly agrochemicals, which is positively influencing the Australia agrochemicals market outlook. Biopesticides, derived from natural materials like plants, microorganisms, and minerals, offer a safer alternative to traditional chemical pesticides. The implementation of government policies and initiatives are making the landscapes and ecosystems less harmful and helps to maintain the health of soils. For example, on February 7, 2025, Australia was allocated USD 13 Million to enhance access to agricultural chemicals and veterinary chemicals. Such an effort aims to increase the availability of critical chemicals for enhancing productivity and sustainable agriculture. The developing regulatory frameworks and innovation in chemicals for agricultural sectors contributes to market expansion. Growing consumer demand and preference for chemical-free food also drive this trend. The rise of biological crop protection agents is supported by advances in biotechnology, which is making these products more effective and cost competitive. The agriculture sector seeks to meet both local and export market demands with stringent environmental regulations, thereby biopesticides are seen as key to achieving sustainable farming practices while maintaining productivity levels.

To get more information on this market Request Sample

Circular Economy Adoption in Agrochemical Production

The growing emphasis on circular economy principles accelerate changes in the way chemicals are produced, used, and disposed of. In agrochemicals, this translates into efforts to reduce the environmental footprint of production processes, as well as to enhance the lifecycle of products used in farming. According to industry reports, the Australian government launched the National Circular Economy Framework (NCEF) to double the nation's circularity by 2035. The framework sets objectives toward reducing material consumption by 10% alongside increasing material productivity by 30% and recovering resources by 80%. It focuses on key sectors like industry, built environment, food, and agriculture, with economic projections showing an annual GDP boost of USD 26 Billion and a 14% reduction in greenhouse gas emissions. Therefore, Australian agrochemical companies are increasingly adopting practices such as using renewable raw materials for pesticide and fertilizer formulations, as well as developing bio-based alternatives to synthetic chemicals. Also, manufacturers are exploring ways to recycle and repurpose agricultural waste products, like crop residues, into inputs for agrochemical production. These initiatives support both the increasing consumer demand for sustainable agriculture methods and regulatory obligations, which is contributing to Australia agrochemical market growth.

Growth Drivers of Australia Agrochemical Market:

Technological Adoption and Precision Farming

A key driver of growth in this market has been the rapid adoption of precision agriculture technologies. Greater precision in applying chemicals is attained through advanced tools such as drones, GPS-guided sprayers, and data-analytics platforms. This sophistication enables targeted use of fertilizers and pesticides, reducing wastage and thereby lessening environmental impact-a key concern in a country known for fragile ecosystems and strict chemical-use regulations. In addition, government-backed programs have encouraged connectivity on farms, enabling digital farming practices and making farming more cost-efficient. Optimization of inputs will result in lower total chemical use and overlaps in application, hence making the use of agrochemicals more economical per hectare. This shift toward smart application increases the value of agrochemicals and contributes toward meeting sustainability goals, reinforcing market growth through efficient and environmentally conscious use.

Resistance Management and Pest Pressure

Other key factors contributing to growth in the Australian agrochemical market include increasing pest, weed, and disease pressure, which is further exacerbated by climatic variability and the development of resistance. The broadacre cropping areas of Western Australia, New South Wales, and Victoria have faced unabated challenges from weed species that are resistant to some herbicides and insect pests over the years. The “resistance” phenomenon persists and thus forces farmers to shift to new, more potent chemical formulations and diversify modes of action against the increasingly stubborn weeds. In addition to this, unpredictable weather with droughts, heatwaves, and sudden storms predispose or accelerate outbreaks of pest organisms, which makes it very difficult for growers not to be highly dependent on crop protection inputs. Together, these factors create strong and continued demand for advanced agrochemicals. Production companies offering resistance-breaking herbicides, more efficient fungicides, and integrated pest-management-compatible products find favor, fostering innovation and reinforcing the Australia agrochemical market growth.

Regulatory and Institutional Support for Sustainable Chemistry

The regulatory framework and institutional support in Australia are also contributing to the growth of the agrochemical market through the promotion of innovation and safer chemistry. The national regulatory authority, tasked with regulating the registration of agricultural and veterinary (agvet) chemicals, has introduced streamlined approval pathways for lower-risk products, allowing biopesticides, controlled-release formulations, and environmentally benign options to reach the market more quickly. Reforms like this reduce barriers for manufacturers to develop and market new chemistries. At the same time, government grants and incentive schemes covering the adoption of precision-spraying tools and efficient nutrient management promote farmer access to more advanced and sophisticated agrochemical solutions. Serving to propel this market, such a policy thrust also orients the industry toward sustainability in the light of reduced residues, reduced environmental footprints, and global trade standards for zero residues in foodstuffs. These regulatory and institutional levers will, therefore, increase demand for next-generation agrochemicals that meet specific agronomic and ecological needs of the Australia agrochemical market share.

Government Support of Australia Agrochemical Market:

Strategic Grant Programs for Agvet Chemical Access

The Australian government has set up special grant programs to enhance the access of farmers to essential agricultural and veterinary (agvet) chemicals, particularly for uses which otherwise might be neglected. In its program "Improved Access to Agvet Chemicals," the government, in consultation with the Australian Pesticides and Veterinary Medicines Authority, the grower groups, and research bodies, identifies unmet chemical-use priorities. Grants are provided for generating the scientific data required for regulatory approval, thereby helping to convert authorized "permits" into uses that are registered on labels. The net result is that Australian farmers have longer-term and more stable access to protective products that are better aligned with their specific crop and pest requirements-a situation that is of value for smaller or niche crop sectors that may otherwise fail to attract investment on commercial grounds. This structure reduces the financial barrier to bringing key but less commercially attractive chemical uses into the formal regulatory system and accordingly demonstrates how government support can steer agrochemical innovation toward true agricultural need.

Regulatory Backbone and Resourcing of the APVMA

Another form of government support lies in the resourcing and strengthening of the APVMA, Australia's statutory authority for assessing and registering agvet chemicals under the National Registration Scheme. The government ensures the regulator remains adequately funded and operationally robust so that chemical approvals, compliance, and reviews are thoroughly conducted. Recent funding boosts have aimed to achieve a balance between cost-recovered fees from industry and public good responsibilities, in particular ensuring safety standards and environmental risk management. For a country with large-scale agriculture across remote regions, a well-resourced regulatory agency is crucial to safeguarding both human and ecological health, while also enabling trade by assuring that locally used agrochemicals meet international quality benchmarks. This kind of support underlines how Australia treats agrochemical regulation as both a market enabler and a public-interest mandate.

Policy Supported Biosecurity and Integrated Pest Management

Beyond pure chemical access, the government actively supports programs that link pest-management with biosecurity and sustainability goals, thus reinforcing the Australia agrochemical market demand in a more holistic way. One prominent example is the program entitled “Supporting Communities Manage Pest Animals and Weeds”, which funnels government funds into on-ground control of invasive species through chemical and non-chemical methods alike. This involves working with Indigenous ranger groups in northern Australia to implement pest-weed management in areas of cultural significance. Here, traditional ecological knowledge of the Indigenous people fuses with modern chemical control. The government is subsidizing pesticide use and nurturing an ecosystem-based approach which makes chemical tools part of a broader pest-resilience strategy. This coordinated backing assists in ensuring that the deployment of agrochemicals is efficient while also being socially and environmentally responsible, thereby underlining how public policy shapes sustainable demand and innovation in Australia’s peculiar agrarian contexts.

Opportunities in Australia Agrochemical Market Trends:

Opportunity in Climate-Driven Pest and Pest-Resistance Challenges

One of the most exciting opportunities as per the Australia agrochemical market analysis, pertain to addressing unique, climate-driven pest challenges and growing resistance issues. From the arid interior to the coastal cropping zones, the vast and variable landscapes of the country create conditions that foster periodic outbreaks of pests such as the Australian plague locust. This calls for effective, region-tailored chemistries to take up the challenge against native pest species. Moreover, herbicide resistance among weeds remains a serious concern across many of Australia's largest grain-growing areas. This is driving demand for novel modes of action for which agrochemical firms have an open window of opportunity to develop and supply next-generation herbicides, insecticides, and biopesticides that target resistant populations. Because resistance is particularly problematic in Australia, innovations that break through that resistance-or delay its onset-have strong commercial potential, making Australia a testing ground for global-scale resistance-management chemistries. Agrochemical firms that invest in research and development to meet these local ecological pressures head-on can seize a growing market while helping to remove a critical pain point for growers across Australia.

Agritech synergy: precision delivery and digital platforms

Other significant opportunities in the Australian agrochemical market are with agritech synergies, particularly in precision delivery systems and digital decision-support platforms. Australia is renowned for its early-adopting farming culture, supported by sound agritech infrastructure comprising various startups, research organizations, and technology hubs centered on drones, AI, and robotics. These can transform the way agrochemicals are applied-smarter and more targeted, applying the crop protection product exactly where it is required at the right rate, hence reducing waste and enhancing environmental outcomes. Agrochemical companies can create partnerships with these agritech providers and offer bundling of chemical solutions with data-driven sprayer platforms or predictive models, which provides value and cost-effectiveness to the farmers. Since Australian farmers increasingly value sustainability and input-use efficiency, combination of crop protection formulations with digital platforms results in a differentiated offer. This chemistry and electronics convergence is one of the key opportunities for players to expand market share while creating more value for growers.

Biocontrols, Biologicals, and Low-Risk Chemistry Demand

Another key opportunity arising in the Australian agrochemical marketplace is growing demand for biocontrols, biologicals, and low-risk chemistries influenced by sustainability goals, export standards, and regulatory trends. Australian agriculture exports to high-value, discerning markets where residue-minimized produce may attract premium prices. There is increasing interest among farmers in biological insecticides, bio-fungicides, and microbial-based crop protectants for use as part of integrated pest-management strategies. Companies that develop natural-active compounds or novel biological agents can localize or tailor their products for Australian broadacre grains, horticulture, and specialty crops. Some pests in Australia, especially those being managed through government-industry biosecurity initiatives, are unique targets for biopesticides. By focusing on environmentally benign chemistries and biocontrol agents, agrochemical firms can tap into both domestic sustainability trends and the export-driven ambition of Australian agriculture in a clear opportunity for low-risk, high-value protection products in this market, which places increasing priority on green credentials.

Australia Agrochemical Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the regional level for 2026-2034. Our report has categorized the market based on fertilizer type, pesticide type, and crop type.

Fertilizer Type Insights:

- Nitrogen Fertilizer

- Phosphatic Fertilizer

- Potassic Fertilizer

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes nitrogen fertilizer, phosphatic fertilizer, potassic fertilizer, and others.

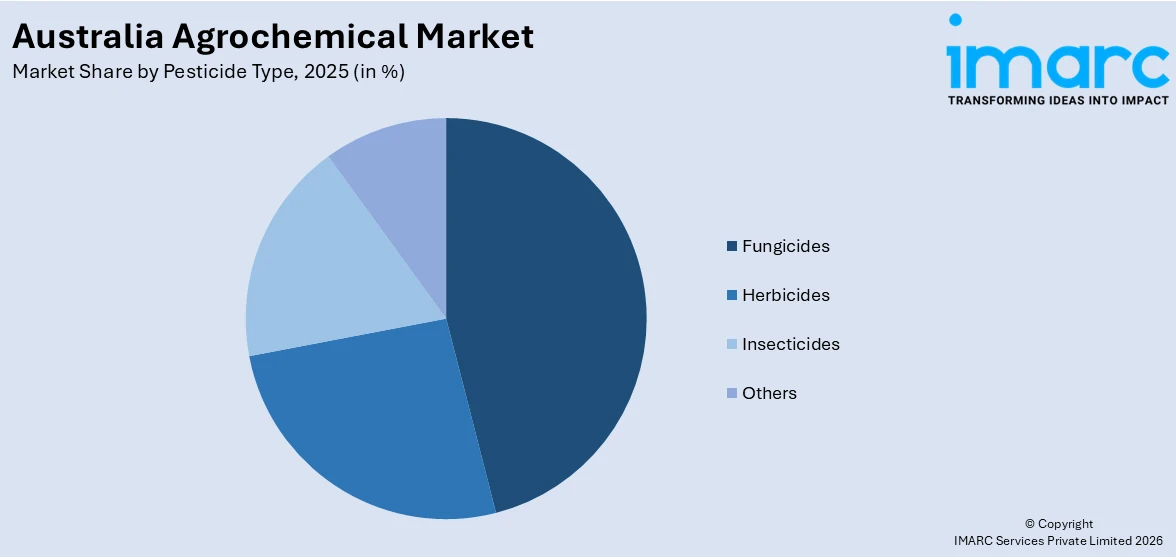

Pesticide Type Insights:

Access the comprehensive market breakdown Request Sample

- Fungicides

- Herbicides

- Insecticides

- Others

A detailed breakup and analysis of the market based on the pesticide type have also been provided in the report. This includes fungicides, herbicides, insecticides, and others.

Crop Type Insights:

- Cereals and Grains

- Oilseeds and Pulses

- Fruits and Vegetables

- Others

The report has provided a detailed breakup and analysis of the market based on the crop type. This includes cereals and grains, oilseeds and pulses, fruits and vegetables, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & News South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Agrochemical Market News:

- May 28, 2024: BASF introduced the Cimegra® insecticide in Australia. It is intended to provide crops, especially Brassica vegetables, with efficient protection. With a unique mode of action and no known resistance problems, the product, which is powered by a new active component, offers quick and durable control of pests like the Diamondback moth. With this introduction, BASF strengthens its position in the market and helps farmers in Australia manage insect resistance by using integrated pest management.

- September 23, 2024: Albaugh launched its new fungicide, Spiromax, in the Australian market. By shielding crops from a variety of fungal infections, the product is intended to increase crop quality and yield. Spiromax is a component of Albaugh's plan to diversify its business and provide Australian farmers with cutting-edge solutions.

Australia Agrochemical Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Nitrogen Fertilizer, Phosphatic Fertilizer, Potassic Fertilizer, Others |

| Pesticide Types Covered | Fungicides, Herbicides, Insecticides, Others |

| Crop Types Covered | Cereals and Grains, Oilseeds and Pulses, Fruits and Vegetables, Others |

| Regions Covered | Australia Capital Territory & News South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia agrochemical market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia agrochemical market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia agrochemical industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Agrochemical Market Report

The Australia agrochemical market was valued at USD 6,150.5 Million in 2025.

The Australia agrochemical market is projected to exhibit a CAGR of 3.14% during 2026-2034.

The Australia agrochemical market is expected to reach a value of USD 8,120.2 Million by 2034.

Key trends in Australia agrochemical market include rising adoption of biologicals, increased integration of digital farming tools, and a shift toward low-environmental-impact formulations. Farmers are embracing precision-spraying technologies, resistance-management strategies, and sustainable crop protection solutions that align with changing climate conditions and stricter stewardship expectations.

Australia agrochemical market is driven by expanding precision-farming adoption, increasing pest and weed pressure across diverse climates, and the need for resistance-management solutions. Farmers’ focus on sustainability, efficient input use, and region-specific crop protection also boosts demand, encouraging continual innovation tailored to Australia’s unique agricultural and environmental conditions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)