Australia Aviation Fuel Market Size, Share, Trends and Forecast by Fuel, Aircraft, End Use, and Region, 2026-2034

Australia Aviation Fuel Market Overview:

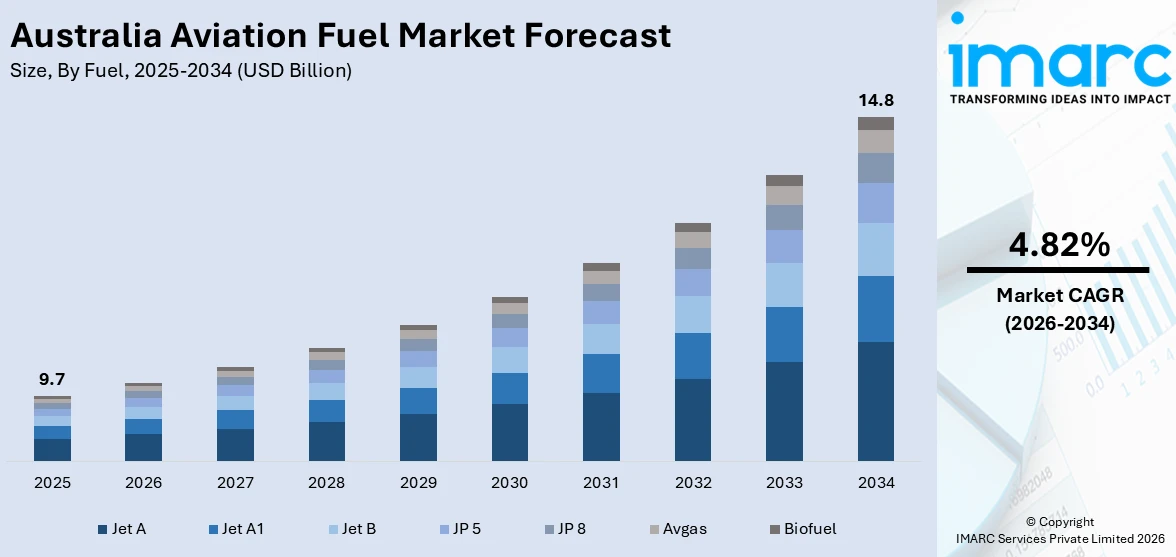

The Australia aviation fuel market size reached USD 9.7 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 14.8 Billion by 2034, exhibiting a growth rate (CAGR) of 4.82% during 2026-2034. The increasing number of international and domestic air travelers is propelling the growth of the market. This trend, along with the heightened spending on fleet renewal to achieve better fuel efficiency and comply with changing emission regulations, is bolstering the market growth. Besides this, the implementation of policies and funding mechanisms aimed at integrating sustainable aviation fuel (SAF) into the broader energy mix of the aviation sector is expanding the Australia aviation fuel market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 9.7 Billion |

| Market Forecast in 2034 | USD 14.8 Billion |

| Market Growth Rate 2026-2034 | 4.82% |

Australia Aviation Fuel Market Trends:

Increasing Air Passenger Traffic and Tourism Activity

The Australian aviation fuel sector is experiencing strong growth driven by the increasing number of international and domestic air travelers. As of January 2025, the Australian aviation network experienced an increment of 0.8% in daily flights compared to the earlier month. Passenger traffic is consistently rising as Australians return to travel after the pandemic and inbound tourism recover, especially from major markets. The geographical width of the nation and dependence upon air connectivity for commerce and travel are increasing the intensity and rate of flights, particularly by regional carriers and budget airlines. The heightened need is also improving commercial flight operations on aviation turbine fuel (ATF), the cornerstone of domestic aviation. Tourism promotions by the Australian government, which include Tourism Australia's promotional efforts, are drawing international tourists. Furthermore, the development of low-cost carriers and increased air routes to hitherto underserved regional regions are also driving consumption.

To get more information on this market Request Sample

Expanding Fleet Modernization and Airline Network

Airlines operating within and to Australia are continually spending on fleet renewal to achieve better fuel efficiency and comply with changing emission regulations. This development is adding to the need for newer aircraft models that are more fuel-efficient using aviation fuel, as opposed to being replaced with alternatives. As new aircraft like the Boeing 787 and Airbus A350 are becoming part of fleets, operating efficiency is getting better, but growth in overall aircraft movements is continuing to maintain fuel demand high. In addition to this, airlines are going out of their way to add to their route systems and transcontinental points, involving more fuel quantities. This increase is driven by bilateral air service agreements and open aviation policies. Even domestic carriers are enhancing flight frequencies, thus rising consumption. The improvement in cargo movement through airfreight, together with a pickup in passenger flights, is impelling the Australia aviation fuel market growth. Qantas the largest airline in Australia, is expected to invest in 20 new passenger aircraft in 2025, according to Travel Weekly.

Government Policies Supporting Sustainable Aviation Fuel (SAF) Integration

The Australian government is actively implementing policies and funding mechanisms aimed at integrating sustainable aviation fuel (SAF) into the broader energy mix of the aviation sector. Although SAF adoption is still in early stages, initiatives such as the Jet Zero Council and the National Jet Fuel Supply Chain Strategy are accelerating investment and infrastructure development. These efforts are driving the demand for conventional aviation fuel in the interim, as SAF requires blending with traditional ATF to meet current operational standards. The support for SAF is encouraging fuel producers, airports, and airlines to enhance fuel logistics and blending infrastructure, indirectly increasing the throughput and distribution of aviation fuel. In 2025, Technip Energies is given a contract by Jet Zero Australia Pty Ltd (Jet Zero) to undertake a Front-End Engineering Design (FEED) contract for Project Ulysses, a bioethanol to sustainable aviation fuel (SAF) project in Townsville, Australia.

Australia Aviation Fuel Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on fuel, aircraft, and end use.

Fuel Insights:

- Jet A

- Jet A1

- Jet B

- JP 5

- JP 8

- Avgas

- Biofuel

The report has provided a detailed breakup and analysis of the market based on the fuel. This includes Jet A, Jet A1, Jet B, JP 5, JP 8, Avgas, and biofuel.

Aircraft Insights:

- Fixed Wings

- Rotorcraft

- Others

The report has provided a detailed breakup and analysis of the market based on the aircraft. This includes fixed wings, rotorcraft, and others.

End Use Insights:

Access the comprehensive market breakdown Request Sample

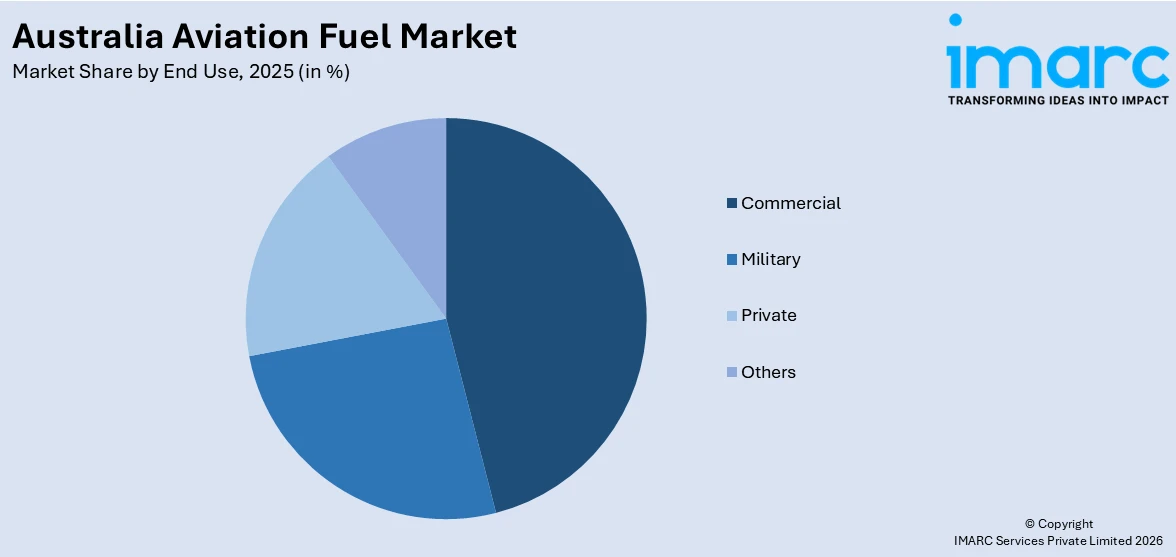

- Commercial

- Military

- Private

- Others

A detailed breakup and analysis of the market based on the end use have also been provided in the report. This includes commercial, military, private, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Aviation Fuel Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fuels Covered | Jet A, Jet A1, Jet B, JP 5, JP 8, Avgas, Biofuel |

| Aircrafts Covered | Fixed Wings, Rotorcraft, Others |

| End Uses Covered | Commercial, Military, Private, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia aviation fuel market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia aviation fuel market on the basis of fuel?

- What is the breakup of the Australia aviation fuel market on the basis of aircraft?

- What is the breakup of the Australia aviation fuel market on the basis of end use?

- What is the breakup of the Australia aviation fuel market on the basis of region?

- What are the various stages in the value chain of the Australia aviation fuel market?

- What are the key driving factors and challenges in the Australia aviation fuel market?

- What is the structure of the Australia aviation fuel market and who are the key players?

- What is the degree of competition in the Australia aviation fuel market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia aviation fuel market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia aviation fuel market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia aviation fuel industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)