Australia Beauty Products Market Size, Share, Trends and Forecast by Type, Distribution Channel, and Region, 2026-2034

Australia Beauty Products Market Size, Share, Trends & Forecast (2026-2034)

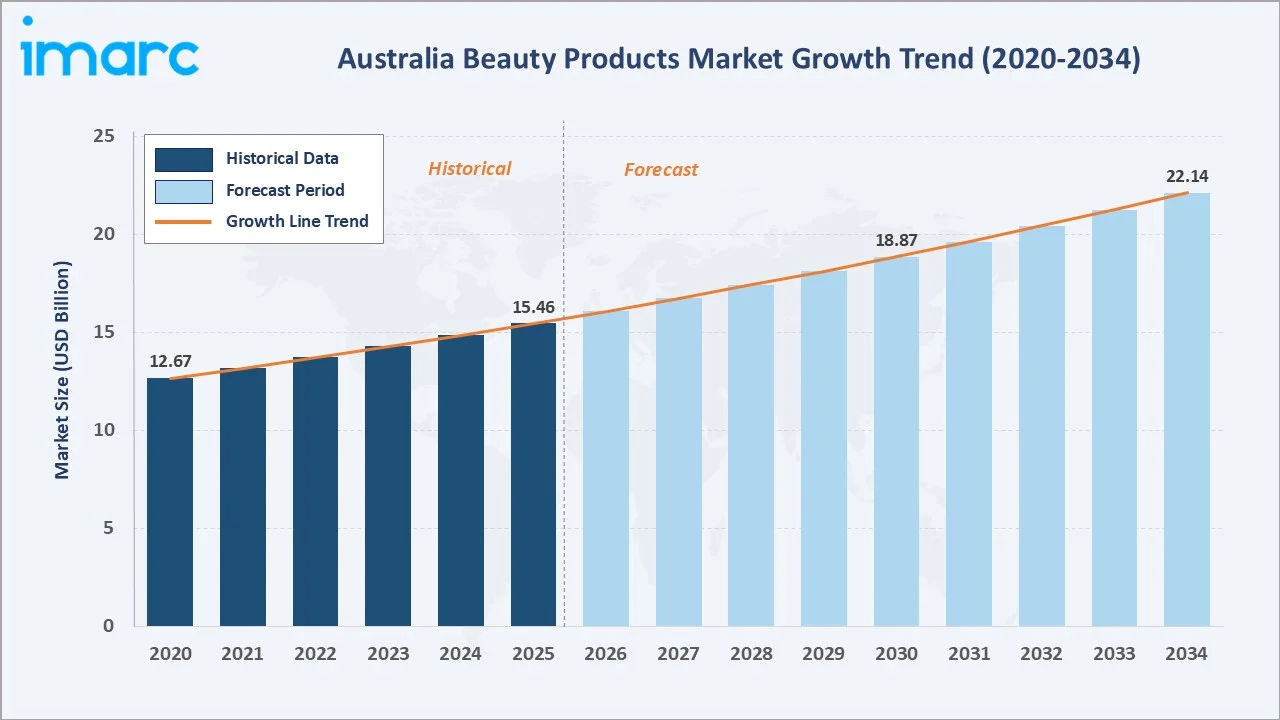

The Australia beauty products market was valued at USD 15.46 Billion in 2025 and is projected to reach USD 22.14 Billion by 2034, exhibiting a CAGR of 4.07% during 2026-2034. Rising consumer awareness of personal grooming, premiumization trends, and the expanding availability of specialty and e-commerce retail channels are the primary forces shaping market growth. Australia Post's Inside Australian Online Shopping 2023 report identified health and beauty as among the fastest-growing online retail categories in the country, reflecting the accelerating digital shift in consumer purchasing behavior.

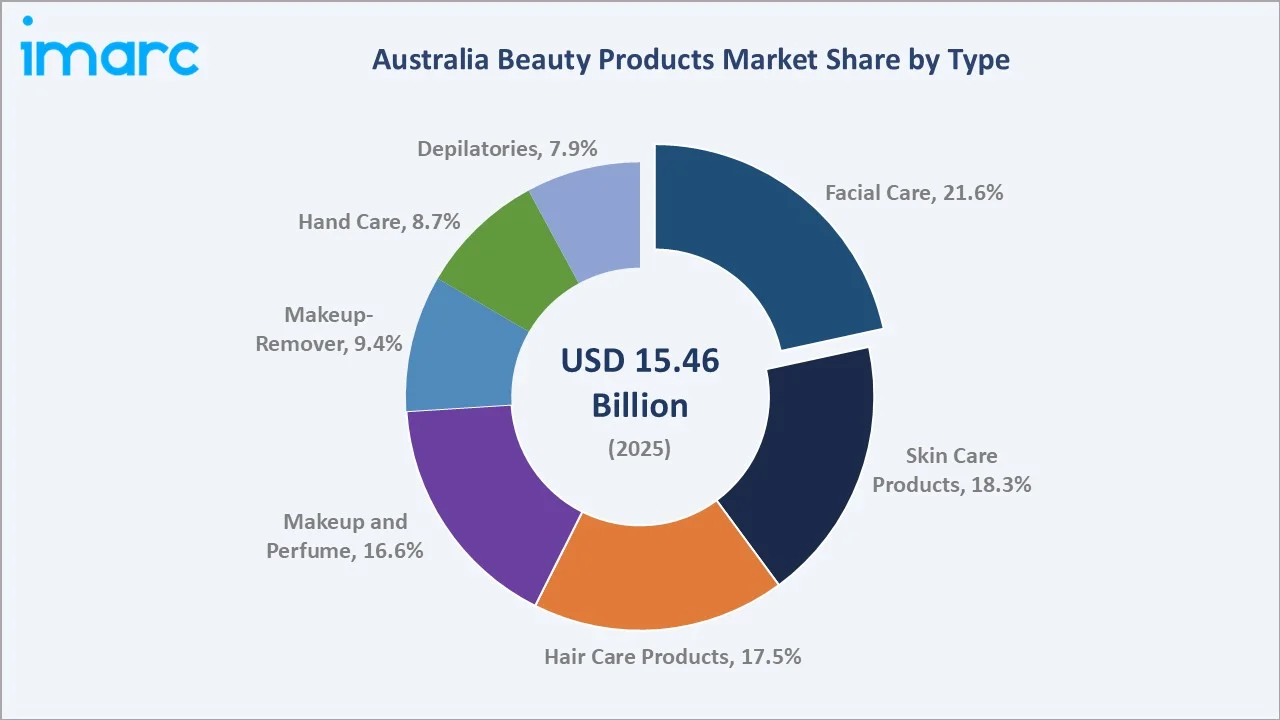

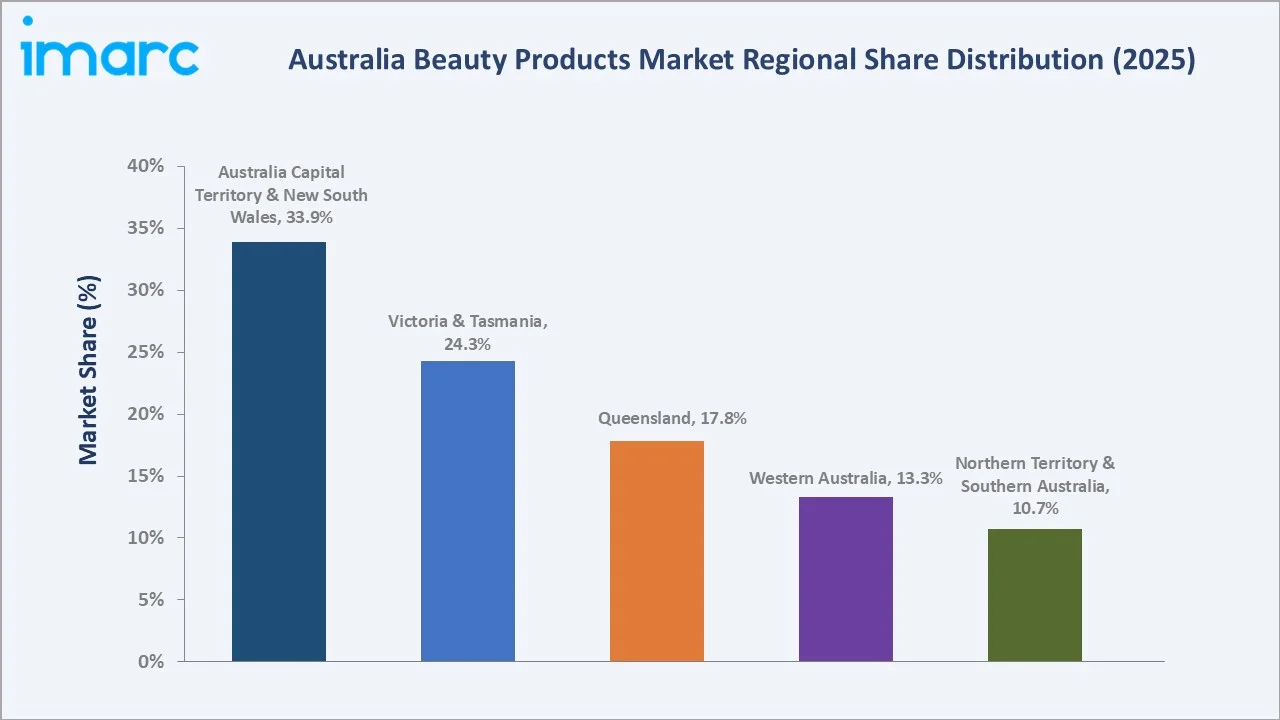

Facial care leads the type segment at 21.6% in 2025, offline commands distribution channel at 57.2%, and Australia Capital Territory & New South Wales holds the dominant 33.9% regional share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 15.46 Billion |

|

Forecast Market Size (2034) |

USD 22.14 Billion |

|

CAGR (2026-2034) |

4.07% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Australia Capital Territory & New South Wales (33.9%, 2025) |

|

Fastest Growing Region |

Victoria & Tasmania (24.3%, 2025) |

|

Leading Type |

Facial Care (21.6%, 2025) |

|

Leading Distribution Channel |

Offline (57.2%, 2025) |

The Australia beauty products market expanded from USD 12.67 Billion in 2020 to USD 15.46 Billion in 2025, driven by strong consumer spending, premiumization, and growing digital adoption across retail channels. Anchored at USD 18.87 Billion in 2030, the forecast to USD 22.14 Billion by 2034 is supported by sustained demand for science-backed skin care, clean beauty formulations, and expanding e-commerce penetration.

To get more information on this market, Request Sample

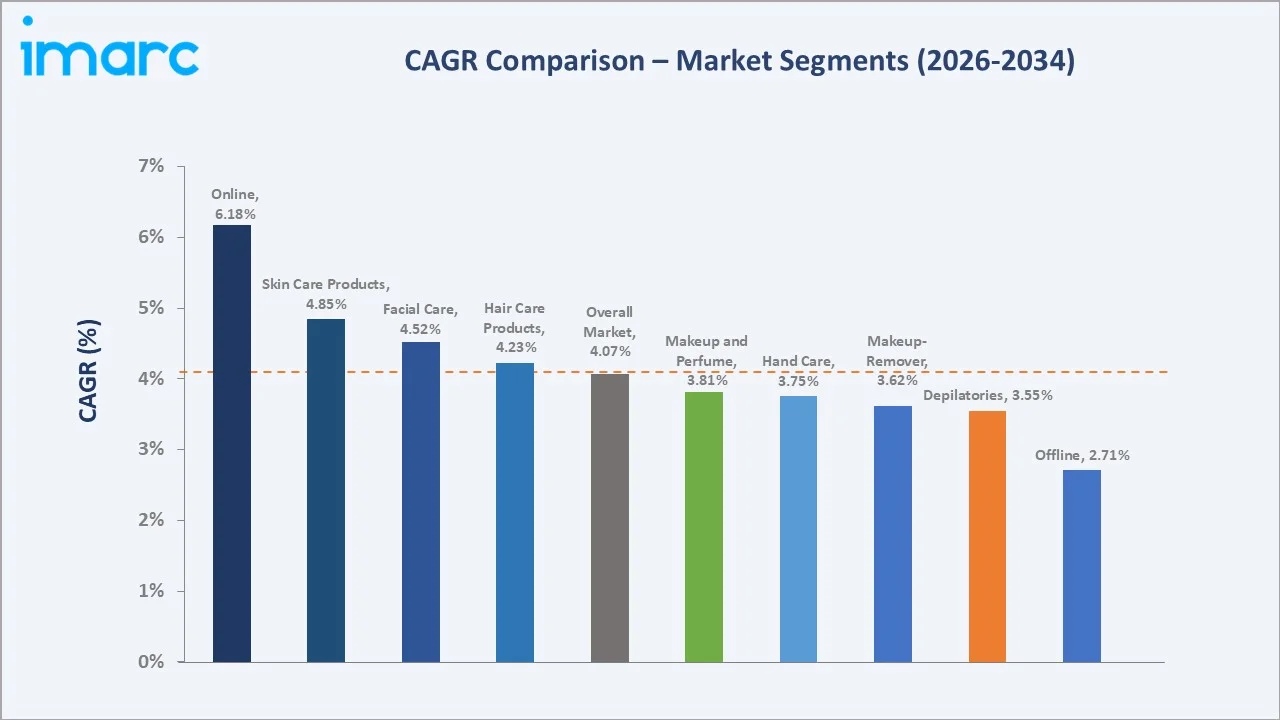

CAGR trajectories across the type and distribution channel sub-segments show online and skin care products expanding faster than the overall 4.07% market CAGR, driven by digital retail penetration and heightened consumer focus on efficacy-led skincare routines.

Executive Summary

The Australia beauty products market is on a consistent upward trajectory from USD 12.67 Billion in 2020 to USD 22.14 Billion by 2034. Consumer spending on personal grooming has evolved from discretionary to habitual across multiple demographic groups. Premiumization, growing influence of social media on purchase decisions, and the expansion of the specialty beauty retail segment are key forces sustaining demand across the facial care, skin care products, and hair care products categories.

Facial care leads the type segment at 21.6% in 2025, underpinned by Australia's high ultraviolet (UV) exposure environment and strong consumer awareness of photoaging and sun damage. As per the Australian Institute of Health and Welfare, age-standardized incidence rates for skin melanoma rose from 54 cases per 100,000 individuals in 2000 to a projected 63 cases per 100,000 individuals in 2025, driving sustained demand for SPF-incorporated and sun-protective beauty formulations across facial care and skin care categories. Based on distribution channel, offline holds 57.2% share in 2025, anchored by broadening of pharmacy chains, department stores, and specialty beauty retailers. Australia Capital Territory & New South Wales commands 33.9% of the market by region, fueled by high population concentration and a mature beauty retail ecosystem.

Key Market Insights

|

Insight |

Data |

|

Leading Type |

Facial Care - 21.6% share (2025) |

|

Second Type |

Skin Care Products - 18.3% share (2025) |

|

Leading Distribution Channel |

Offline - 57.2% share (2025) |

|

Second Distribution Channel |

Online - 42.8% share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 33.9% share (2025) |

|

Fastest Growing Region |

Victoria & Tasmania - 24.3% share (2025) |

|

Top Companies |

Procter & Gamble, Unilever, Shiseido Company, Limited, Revlon |

Key Analytical Observations Expanding on the Data Above:

- Facial care leads at 21.6% in 2025, driven by Australia's high UV radiation environment which accelerates consumer adoption of SPF-formulated facial care products. Growing consumer preference for multifunctional products combining hydration, anti-aging, and sun protection is further strengthening demand across premium and mass-market segments.

- Skin care products at 18.3% reflect growing consumer awareness of skincare routines influenced by dermatological advice, social media engagement, and the penetration of science-backed, ingredient-led formulations into mainstream retail channels.

- Offline at 57.2% maintains leadership through pharmacy chains and specialty beauty retailers, which provide expert consultation and curated product assortments that sustain strong in-store consumer engagement.

- Online at 42.8% reflects Australia's high internet penetration and the rapid growth of direct-to-consumer (D2C) beauty brands, subscription beauty services, and international brand websites targeting Australian consumers. DataReportal’s Global Digital Report 2024 revealed that about 97% of Australians possessed at least one smartphone, while 96.4% utilized it to go online.

- Australia Capital Territory & New South Wales dominance at 33.9% is supported by high urban population density, premium retail concentration, stronger disposable incomes, and elevated beauty product consumption trends.

Australia Beauty Products Market Overview

The Australia beauty products market encompasses a broad range of personal care categories, including facial care, skin care products, hair care products, makeup and perfume, makeup-remover, hand care, and depilatories. These products are distributed through an integrated ecosystem of manufacturers, importers, specialty retailers, pharmacies, department stores, and e-commerce platforms.

Australia's beauty ecosystem is shaped by a combination of global multinational brands, regional Asia-Pacific players, and a growing segment of domestically founded indie brands. Macroeconomic tailwinds, including a high household disposable income base, strong urbanization, and a culturally diverse population with affinity for both Western and Asia-Pacific beauty innovations, support structural market growth.

Market Dynamics

To evaluate market opportunities, Request Sample

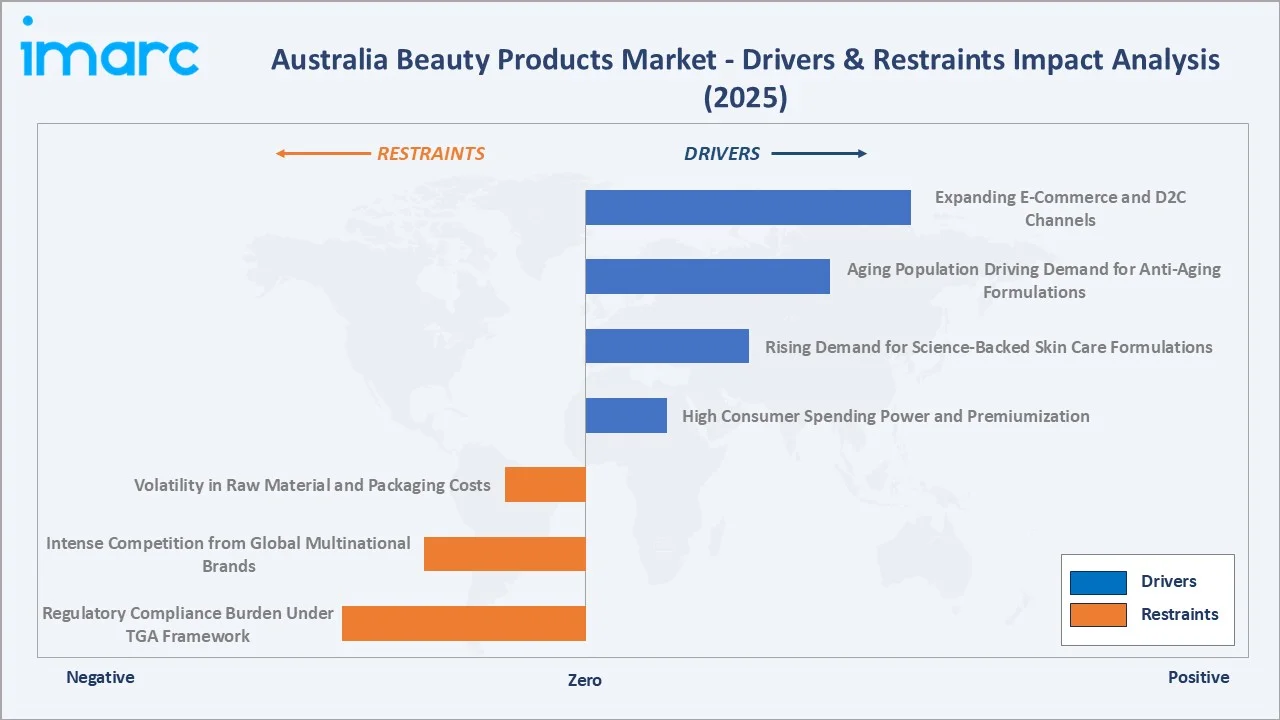

Market Drivers

- High Consumer Spending Power and Premiumization: Australia's high per capita income supports significant discretionary spending on personal care. Consumers are increasingly trading up from mass-market to premium and prestige beauty products, driving higher average selling prices and favorable revenue mix across facial care, skin care products, and fragrance sub-categories.

- Rising Demand for Science-Backed Skin Care Formulations: Growing consumer interest in active ingredients, such as retinol, niacinamide, hyaluronic acid, and peptides, is driving development and retail availability of efficacy-focused skin care products, supported by dermatological endorsements and strong influencer-led education on ingredient benefits.

- Aging Population Driving Demand for Anti-Aging Formulations: As per the Centre for Population’s 2024 Population Statement, over 2.1 Million individuals aged 75 and older resided in Australia, a figure expected to exceed 3.2 Million by 2034, creating sustained structural demand for anti-aging skin care products, scalp care formulations, and dermatologically targeted hair care products.

- Expanding E-Commerce and D2C Channels: The rapid growth of beauty-specific e-commerce platforms, subscription beauty services, and brand-owned D2C websites is broadening the addressable market, enabling brands to reach consumers in regional areas with limited physical retail access and broadening market penetration beyond major metropolitan centers.

Market Restraints

- Regulatory Compliance Burden Under TGA Framework: The Therapeutic Goods Administration (TGA) in Australia classifies certain cosmeceutical products, such as medicated skin treatments and SPF-rated formulations above specified thresholds, as therapeutic goods subject to additional safety, registration, and labelling requirements. This regulatory complexity increases compliance costs and extends time-to-market for new product launches, particularly for smaller domestic brands and international entrants.

- Intense Competition from Global Multinational Brands: The market is heavily influenced by globally recognized brands with established retail partnerships, strong marketing budgets, and extensive product portfolios. This creates high barriers to shelf space and consumer mindshare for emerging domestic brands and smaller category players attempting to scale.

- Volatility in Raw Material and Packaging Costs: Fluctuations in the prices of key cosmetic ingredients, such as natural botanical extracts, specialty actives, and sustainable packaging materials, are compressing manufacturer margins and creating product pricing challenges, particularly for brands committed to natural and clean formulation positioning.

Market Opportunities

- Clean and Sustainable Beauty Growth: Growing consumer preference for natural, organic, and sustainably packaged beauty products is opening significant new product development and brand positioning opportunities. Retailers are dedicating expanded shelf space to clean beauty ranges, and brands that credibly communicate ingredient transparency and environmental responsibility are gaining strong consumer preference across key retail channels.

- Men's Grooming and Gender-Inclusive Beauty Expansion: The Australian men's grooming industry remains underpenetrated relative to facial care and skin care for women. Shifting cultural attitudes toward male personal care, combined with targeted marketing campaigns and dedicated product lines, are creating a material growth opportunity across facial moisturizers, hair care, and depilatories sub-categories.

Market Challenges

- Greenwashing Scrutiny and Claims Compliance: Growing regulatory and consumer scrutiny of environmental and natural claims in the beauty sector is creating compliance risk for brands making unsubstantiated sustainability assertions. The Australian Competition and Consumer Commission has increased enforcement activity around greenwashing claims, requiring brands to ensure all environmental marketing is evidence-based and clearly substantiated.

- Consumer Trust and Ingredient Misinformation Risk: The proliferation of social media-driven beauty advice creates risks of ingredient misinformation and unverified product claims reaching consumers rapidly. Brands must invest in proactive consumer education and dermatological endorsement strategies to build credibility in an increasingly ingredient-aware market.

Emerging Market Trends

1. Accelerated Rise of Clean and Sustainable Beauty

Australian consumers are increasingly demanding transparency in ingredient sourcing, formulation ethics, and packaging sustainability. Brands committed to cruelty-free, vegan, and reduced-impact packaging are gaining accelerated retail traction. The Australian Competition and Consumer Commission issuing dedicated guidance on greenwashing in the cosmetics sector underscores the growing regulatory expectation for substantiated environmental claims in the Australian beauty market. This trend is prompting both multinational and indie brands to reformulate product lines and redesign packaging in alignment with circular economy principles.

2. K-Beauty and J-Beauty Mainstream Adoption

Korean and Japanese beauty philosophies are achieving mainstream adoption in Australia, driven by the country's culturally diverse population and strong consumer interest in innovative formulation formats, such as essences, ampoules, sheet masks, and multi-step skincare routines. Korean cosmetics imports into Australia have grown significantly, with major specialty retailers dedicating expanded floor space and curated collections to K-beauty and J-beauty brands, expanding the facial care and skin care products segments. In 2025, Australia imported beauty or make-up preparations and skin care products from South Korea totaling USD 180.07 Million, as per the United Nations COMTRADE database on international trade.

3. AI-Driven Personalization and Virtual Try-On Technology

Beauty brands and retailers are deploying artificial intelligence (AI) tools that enable skin analysis, personalized product recommendations, and virtual makeup try-on experiences through mobile applications and retail installations. These digital tools are reducing consumer hesitation around online purchases of makeup and perfume and enabling more targeted cross-selling of facial care and skin care products, with personalization emerging as a key competitive differentiator for both distribution channels.

4. Rise of Skinimalism and Ingredient-Focused Routines

Consumers are simplifying their beauty routines, focusing on fewer, high-efficacy products with clinically validated active ingredients rather than extensive multi-step regimens. This skinimalism trend is driving innovation in multi-functional skin care products that combine hydration, sun protection, anti-aging, and brightening benefits in single formulations, benefiting the facial care and skin care products segments and reshaping product development priorities for leading brands.

Industry Value Chain Analysis

The Australia beauty products value chain spans six stages from raw material sourcing through retail and end use. Formulation R&D and manufacturing capture the highest value-add, while retail channel relationships and consumer engagement capabilities generate the most durable competitive advantages in this branded consumer market.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of natural oils, botanical extracts, synthetic actives, emulsifiers, and cosmetic-grade packaging materials supporting beauty product manufacturing |

|

Ingredient & Formula R&D |

Cosmetic chemists, contract research organizations, and in-house innovation teams developing efficacious and TGA-compliant formulations |

|

Manufacturing & Production |

Contract manufacturers, OEM producers, and vertically integrated brand-owned production facilities producing finished beauty goods at scale |

|

Quality Control & Compliance |

Regulatory frameworks, TGA guidelines, ACCC compliance requirements, safety testing protocols, and labelling standards governing beauty product claims |

|

Distribution & Logistics |

National wholesalers, specialty beauty distributors, third-party logistics providers, and e-commerce fulfilment networks servicing retail channels |

|

Retail & End Use |

Pharmacies, department stores, specialty beauty retailers, supermarkets, D2C platforms, and online marketplaces |

Vertically integrated global players achieve superior cost control and supply chain resilience through ownership of formulation R&D and manufacturing capabilities. Mid-tier and indie brands typically rely on contract manufacturing relationships while focusing investment on formulation innovation, brand building, and channel development to achieve differentiation in the competitive Australian marketplace.

Technology Landscape in the Australia Beauty Products Industry

Advanced Formulation Science

Biotechnology-derived ingredients, including fermentation-based actives, biomimetic peptides, and microbiome-supportive formulations, are redefining efficacy expectations in the skin care products segment. These innovations are enabling brands to deliver clinically validated results with reduced synthetic chemical loads, supporting both the clean beauty trend and the ingredient-conscious consumer segment in Australia.

Smart Packaging and Connected Beauty

Digital and smart packaging technologies, including QR code-integrated product labelling, dose-tracking dispensers, and NFC-enabled authentication tools, are being introduced across the premium and prestige beauty segments. These technologies enhance consumer trust, reduce counterfeiting risk, and provide brands with real-time retail performance data to optimize inventory and repurchase messaging strategies.

E-Commerce Personalization and AI Tools

Beauty-specific AI platforms enabling skin tone matching, concern-based product recommendation engines, and augmented reality makeup try-on are becoming standard capabilities for leading e-commerce retailers and brand-owned D2C platforms. These tools are driving higher conversion rates, lower product return rates, and stronger customer lifetime value across the online distribution channel.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Facial Care |

21.6% |

2025 |

|

Distribution Channel |

Offline |

57.2% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

33.9% |

2025 |

By Type

Facial care commands the leading share at 21.6% in 2025, driven by Australia's high UV radiation environment, strong consumer awareness of photoaging and sun damage, and the expanding availability of SPF-fortified and cosmeceutical facial care formulations across pharmacy and specialty retail channels. Facial moisturizers, sunscreens, serums, and eye creams represent the most commercially active sub-categories within this segment.

To access detailed market analysis, Request Sample

Skin care products hold 18.3% share in 2025, supported by strong consumer adoption of science-backed active ingredient routines and the influence of dermatological recommendations on purchasing decisions. Rising demand for hydration-focused, anti-aging, and barrier-repair formulations is further supporting category expansion across both premium and mass-market brands.

By Distribution Channel

Offline leads at 57.2% in 2025, reflecting the important role of physical retail in the beauty purchase decision. Pharmacy chains, specialty beauty retailers, department stores, and supermarkets provide consumers with hands-on product experience, expert consultation, and immediate purchase gratification that remain important to the beauty buying process.

Online commands a significant 42.8% share in 2025, anchored by purpose-built beauty e-commerce platforms and the strong adoption of D2C purchasing. Australia's high internet penetration, the proliferation of influencer-driven beauty content, and the convenience of product comparison and review-led discovery are sustaining robust online channel growth.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Australia Capital Territory & New South Wales |

33.9% |

High population density, strong disposable incomes, presence of major retail chains, and well-developed e-commerce infrastructure supporting premium beauty consumption |

|

Victoria & Tasmania |

24.3% |

Robust urban retail ecosystem, strong fashion and beauty culture, growing adoption of luxury and premium beauty brands across major metropolitan centers |

|

Queensland |

17.8% |

High sun exposure driving demand for SPF and skin protection products, growing tourism sector, expanding suburban retail network, and rising health consciousness |

|

Western Australia |

13.3% |

Resource-sector driven household incomes, expanding urban population in Perth, growing demand for premium personal care and wellness-oriented beauty products |

|

Northern Territory & Southern Australia |

10.7% |

Niche market dynamics, growing interest in locally sourced botanical ingredients, and increasing focus on natural and organic beauty formulations |

Australia Capital Territory & New South Wales commands 33.9% of the market in 2025, driven by high population concentration in Sydney and Canberra, elevated household incomes, and the presence of flagship specialty beauty retail destinations. The region benefits from a mature and well-developed retail ecosystem, including high-density pharmacy networks, department store beauty halls, and a growing portfolio of standalone specialty beauty boutiques that collectively support premium beauty consumption.

Victoria & Tasmania at 24.3% reflects Melbourne's role as a fashion and beauty culture hub, with strong consumer interest in premium and prestige beauty categories and a well-developed specialty retail network.

Competitive Landscape

The Australia beauty products market is moderately concentrated, with global multinational brands dominating brand awareness, retail shelf presence, and marketing investment while specialty domestic players and emerging indie brands compete on formulation innovation, ingredient transparency, and community-led marketing strategies. Retail channel depth, brand recognition, and product portfolio breadth form the primary competitive moats for leading players in this market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Procter & Gamble |

Olay, Pantene, Head & Shoulders, Gillette Venus |

Leader |

Mass-market consumer brand leadership; broad distribution across supermarkets and pharmacies |

|

Unilever |

Dove, TRESemmé, Vaseline |

Leader |

Broad consumer reach across skin care and hair care; strong sustainability brand positioning |

|

Shiseido Company, Limited |

NARS, Clé de Peau Beauté |

Challenger |

Premium Japanese beauty heritage; growing presence in specialty retail and DTC channels |

|

Revlon |

Revlon, Elizabeth Arden, Almay |

Emerging |

Value-positioned color cosmetics; rebuilding digital and specialty retail presence |

Key players include Procter & Gamble, Unilever, Shiseido Company, Limited, and Revlon, among others.

Key Company Profiles

Procter & Gamble

Procter & Gamble is a global consumer goods leader with a large-scale presence in the Australian beauty and personal care market through its portfolio of mass-market and mid-tier brands. The company's products are among the most widely distributed in Australian supermarkets, pharmacies, and general merchandise retailers, with category leadership in hair care and skin care.

- Product Portfolio: Olay (skin care products and facial care), Pantene (hair care products), Head & Shoulders (scalp care), and Gillette Venus (depilatories and personal care).

- Recent Developments: Procter & Gamble has invested in expanding its sustainable packaging commitments across the Australian portfolio, introducing recyclable and refillable product formats for Olay and Pantene to align with growing consumer demand for environmentally responsible beauty packaging.

- Strategic Focus: Mass and mid-tier market leadership; broad retail distribution; product innovation in skin care and hair care formulations; advancing sustainable packaging and ingredient transparency across the Australian portfolio.

Unilever

Unilever is one of the largest consumer goods companies globally and a significant player in the Australian beauty and personal care market. The company's portfolio spans skin care, hair care, and body care segments, with strong brand recognition across mass and mid-tier consumer segments.

- Product Portfolio: Dove (skin care and hair care), TRESemmé (hair care products), and Vaseline (skin care).

- Recent Developments: Unilever has accelerated its beauty and personal care sustainability agenda in Australia, including increasing the use of recycled plastics in packaging for Dove and TRESemmé, and expanding its refill and concentrated product formats to reduce packaging waste across the Australian market.

- Strategic Focus: Purpose-led brand positioning; strong sustainability credentials; broad mass-market distribution; emphasis on diverse and inclusive beauty representation across brand marketing strategies.

Revlon

Revlon is a global beauty company with a long-standing presence in the Australian market across color cosmetics, hair care, and fragrances. The company continues to strengthen brand visibility through mass retail distribution and product portfolio expansion.

- Product Portfolio: Revlon, Elizabeth Arden (premium facial care and fragrance) and Almay (hypoallergenic color cosmetics).

- Recent Developments: Revlon has been focused on revitalizing its core Revlon and Elizabeth Arden brands in Australia through digital marketing investments, renewed influencer partnerships, and selective product innovation in high-demand color cosmetic categories.

- Strategic Focus: Brand revitalization and accessible prestige positioning; selective retail distribution; digital marketing-led consumer re-engagement; leveraging Elizabeth Arden for premium skin care and fragrance growth.

Market Concentration Analysis

The Australia beauty products market is moderately concentrated, with the top companies - Procter & Gamble, Unilever, Shiseido Company, Limited, and Revlon, estimated to collectively account for approximately 50-60% of market revenue in 2025 across their combined product category and retail channel footprints.

Barriers to market leadership include the cost of establishing broad retail distribution across Australia's geographically dispersed market, the investment required to build brand recognition across culturally diverse consumer segments, and the regulatory compliance capabilities needed to navigate TGA classification requirements for certain product categories. These factors favor well-resourced multinational players with established market infrastructure.

Consolidation dynamics are visible through selective brand acquisitions and portfolio rationalization strategies, as larger groups evaluate the performance of their sub-brands against evolving consumer preferences. The clean beauty, dermatological skin care, and personalized beauty segments are attracting investment interest from both strategic buyers and private equity as high-growth pockets within the broader market.

Investment & Growth Opportunities

Fastest-Growing Segments

Online at 42.8% in 2025 is the fastest-growing distribution channel, projected to expand at 6.18% CAGR through 2034 - materially above the overall market CAGR of 4.07%. Skin care products at 18.3% and facial care at 21.6% are the fastest-growing type segments, driven by the Australian consumer's growing investment in efficacy-led skincare routines and sun-protective formulations.

Emerging Markets

Within Australia, Queensland at 17.8% and Western Australia at 13.3% represent emerging growth regions driven by urbanization, increasing household income, and growing consumer engagement with premium beauty retail. The men's grooming sub-segment across facial care, depilatories, and hair care products represents one of the most materially underpenetrated opportunity spaces in the Australian market.

Venture & Investment Trends

Investment activity in the Australian beauty sector is concentrated in three areas: D2C indie beauty brands with strong social media communities; clean and sustainable beauty formulation platforms with demonstrated ingredient transparency; and beauty technology start-ups deploying AI-driven personalization, skin diagnostics, and virtual try-on tools to enhance online conversion and customer lifetime value.

Future Market Outlook (2026-2034)

The Australia beauty products market is forecast to expand from USD 15.46 Billion in 2025 to USD 22.14 Billion by 2034, growing at a CAGR of 4.07% and adding approximately USD 6.68 Billion in incremental annual market value over the forecast period.

Four structural forces will shape the market through 2034: sustained premiumization across facial care and skin care products; accelerated online distribution channel penetration driven by digital-native consumer cohorts; the mainstreaming of clean and sustainable beauty formulations; and the growing influence of Asia-Pacific beauty innovation on Australian consumer preferences and product development pipelines.

By 2034, the online distribution channel is expected to approach parity with the offline channel, reshaping retailer investment priorities and brand channel strategies. Facial care and skin care products will consolidate their position as the largest type segments as Australia's aging population and UV-aware consumer base drive sustained demand for skin health-oriented formulations.

Research Methodology

Primary Research

Primary research included consultations with senior brand managers at leading beauty manufacturers and distributors operating in Australia, category buyers at major specialty beauty and pharmacy retailers, dermatologists and beauty professionals advising on consumer product adoption, and regulatory compliance specialists with expertise in TGA requirements for cosmetic and cosmeceutical products.

Secondary Research

Secondary research drew upon Australian Bureau of Statistics household expenditure surveys, Australian Competition and Consumer Commission guidance documents, Therapeutic Goods Administration regulatory publications, and publicly available annual reports, investor presentations, and press releases from listed multinational beauty companies. Industry association publications and specialty retail channel reports were also reviewed.

Forecasting Models

Market forecasts were developed using top-down and bottom-up methodologies, integrating macroeconomic household spending data, per capita beauty expenditure trends, category penetration rates, distribution channel growth assumptions, and demographic projections from the Australian Institute of Health and Welfare. Scenario analysis addressed potential variation in consumer spending, regulatory changes, and competitive entry dynamics.

Australia Beauty Products Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Facial Care, Makeup-Remover, Hand Care, Depilatories, Skin Care Products, Hair Care Products, Makeup and Perfume |

| Distribution Channels Covered |

|

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Procter & Gamble, Unilever, Shiseido Company, Limited, Revlon, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia beauty products market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia beauty products market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia beauty products industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Beauty Products Market Report

The Australia beauty products market was valued at USD 15.46 Billion in 2025, driven by strong consumer spending on facial care, skin care products, and hair care products.

The market is projected to grow at a CAGR of 4.07% from 2026 to 2034, reaching USD 22.14 Billion by 2034.

Facial care leads with 21.6% share in 2025, driven by high UV awareness and strong demand for SPF-incorporated formulations.

Offline leads with 57.2% share in 2025, supported by pharmacy chains, department stores, and specialty beauty retailers.

Australia Capital Territory & New South Wales holds 33.9% in 2025, driven by high population density and a mature retail infrastructure.

Key drivers include high consumer spending power, premiumization, aging population demand for anti-aging products, and rapid growth of e-commerce retail channels.

Key challenges include TGA regulatory compliance for cosmeceutical products, intense competition from global brands, and greenwashing scrutiny from the ACCC.

Leading companies include Procter & Gamble, Unilever, Shiseido Company, Limited, and Revlon.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)