Australia Bicycle Market Size, Share, Trends and Forecast by Type, Technology, Price, Distribution Channel, End User, and Region, 2026-2034

Australia Bicycle Market Summary:

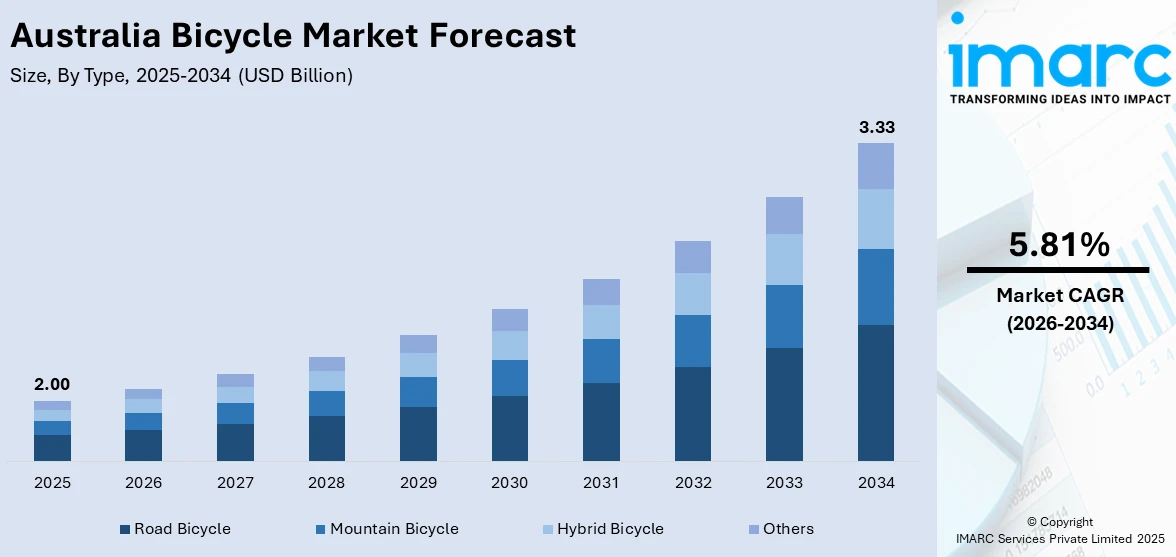

The Australia bicycle market size was valued at USD 2.00 Billion in 2025 and is projected to reach USD 3.33 Billion by 2034, growing at a compound annual growth rate of 5.81% from 2026-2034.

The market is propelled by increasing health consciousness driving cycling adoption as an effective cardiovascular exercise, rising urban congestion pushing commuters toward efficient alternatives, and growing environmental awareness favoring sustainable transport. Apart from this, government investments in dedicated cycling infrastructure, expanding recreational cycling culture, and technological innovations in bicycle design further strengthen market growth across diverse consumer segments, thereby expanding the Australia bicycle market share.

Key Takeaways and Insights:

- By Type: Road bicycle dominates the market with a share of 36% in 2025, driven by performance-focused designs, aerodynamic innovations, and strong demand from fitness enthusiasts and competitive cyclists.

- By Technology: Conventional leads the market with a share of 60% in 2025, owing to affordability advantages, lower maintenance requirements, and established consumer preference for traditional cycling experiences.

- By Price: Mid-range represents the largest segment with a market share of 45% in 2025, reflecting consumer demand for quality bicycles offering reliable performance without premium pricing across commuting and recreational applications.

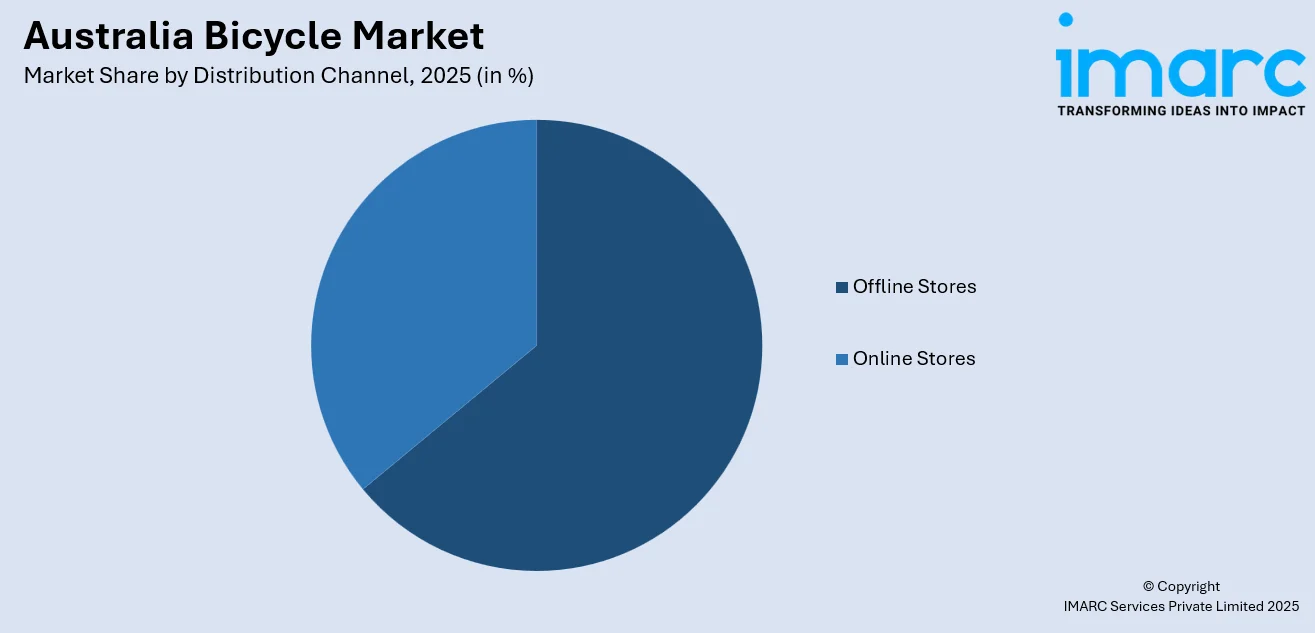

- By Distribution Channel: Offline stores lead the market with a share of 64% in 2025, supported by the value consumers place on test rides, expert consultations, and after-sales service availability at physical retail locations.

- By End User: Men represent the largest segment with a market share of 51% in 2025, reflecting higher participation rates in cycling activities, longer average riding distances, and stronger engagement across competitive and recreational cycling.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 30% in 2025, driven by Sydney's population concentration, extensive urban cycling infrastructure investments, and high commuting demand in metropolitan areas.

- Key Players: The Australian market exhibits moderate competitive intensity, with multinational manufacturers Giant, Trek, and Specialized leveraging established dealer networks alongside regional brands and emerging direct-to-consumer e-bike specialists competing across price segments and technology categories. Some of the market players include Avanti Bikes, Bastion Cycles, Bossi Bicycles, Curve Cycling, Down Under Cycles Pty Ltd, EARTH Electric Bikes, Giant Bicycles, GPI Apollo Bicycle Co. Pty. Ltd, Malvern Star, Merida Bikes, Reid Cycles, and Trek Bicycle Corporation.

To get more information on this market Request Sample

Australia's cycling environment is being rapidly changed by the growth of inner city communities and urban mobility, increased awareness of health and wellbeing among Australians, and large scale upgrading of infrastructure. The Australian bicycle market is being positively influenced by government policy acknowledging that bicycles are one solution to reducing congestion caused by cars on the road and promoting environmental sustainability. Major cities throughout Australia have invested heavily in constructing dedicated cycle lane networks and implementing active transport initiatives. The fastest growing segment of the bicyclist population are commuters, as well as those aged 40+. The growth in e-bike usage follows the introduction of government-funded rebate/discount schemes, and improvements in battery technology that enable e-bikes to travel over 120km on a single charge. Many of these e-bikes come equipped with smart technology capabilities such as GPS tracking, fitness monitoring, and wired or wireless connectivity which appeals to technology inclined consumers. Mountain biking infrastructure development in Queensland and regional areas is supporting the growth in recreation demand and similarly the increasing use of cargo bikes for last mile delivery applications represents the increasing use of bicycles for commercial purposes. In 2025, MATE.BIKE announced a major collaboration with Directed, Australia's leading supplier of high-end mobility, automotive & lifestyle technology. This alliance will enable the complete range of MATE.BIKE to be offered to Australians on December 2025 via Directed's network of retailers and dealers throughout Australia.

Australia Bicycle Market Trends:

E-Bike Adoption Surge Transforms Urban Commuting

Electric bicycle adoption is accelerating rapidly across Australian cities, driven by falling battery costs, extended range capabilities, and government incentive programs. Queensland introduced a one million dollar rebate scheme in September 2024 providing 500 dollar subsidies for e-bike purchases to encourage sustainable transport adoption. Tasmania has emerged as the national leader in e-bike usage, with electric assistance featured in the majority of bike trips and women accounting for over one-third of users, demonstrating broadening demographic appeal. Pedal-assist models dominate the market, while speed-pedelec adoption grows among long-distance commuters covering 20-plus kilometer journeys in Sydney and Melbourne seeking viable car substitutes. Battery technology improvements now deliver 120 kilometer real-world range, reducing charging frequency concerns and strengthening consumer confidence for daily commuting applications.

Cycling Infrastructure Expansion Reshapes Urban Mobility

Major infrastructure investments are transforming Australia's cycling networks, with state and local governments committing substantial funding to build protected bike lanes and strategic corridors. Infrastructure Victoria launched its comprehensive 2025-2055 strategy in November 2025, recommending 500 to 620 million dollars investment over ten years to construct 250 continuous kilometers of high-standard bike routes across Melbourne and regional cities including Geelong, Ballarat, Bendigo, and Wangaratta. Work commenced on the 38.9 million dollar Sydney Harbour Bridge ramp upgrade project connecting the iconic bridge to the Milsons Point bike network, enhancing commuter accessibility. Queensland allocated 315 million dollars over four years to expand cycling and walking paths. The funding is a component of the $37.4 billion Queensland Transport and Roads Investment Program 2024-25 to 2027-28 (QTRIP), encompassing significant initiatives such as a velobridge in Greenslopes and the Riverwalk extension at Kangaroo Point.

Smart and Connected Bicycles Drive Digital Integration

Technological integration is advancing rapidly as manufacturers incorporate smartphone connectivity, GPS navigation, fitness tracking, and advanced safety features into modern bicycles. Bike-sharing programs are deploying IoT-enabled bicycles with GPS tracking and wireless charging systems, creating networked urban mobility solutions. The integration of telematics in commercial cargo bikes provides fleet managers with real-time data on cornering speeds, braking patterns, and average speeds, enhancing safety protocols and operational efficiency for delivery applications. TAV Systems announced its plans to launch its Scrambike in Australia during the second quarter of 2025, showcasing its innovative design and performance to the domestic market.

Market Outlook 2026-2034:

Australia's bicycle market is poised for sustained expansion as urban planning prioritizes active transport solutions, environmental consciousness drives sustainable mobility choices, and technological innovations enhance cycling accessibility across diverse demographics. The market generated a revenue of USD 2.00 Billion in 2025 and is projected to reach a revenue of USD 3.33 Billion by 2034, growing at a compound annual growth rate of 5.81% from 2026-2034. Infrastructure improvements including dedicated bike lane networks and safe corridor development will reduce safety concerns that currently deter potential cyclists, particularly in outer suburban areas where infrastructure gaps persist. E-bike adoption will accelerate among older adults, commuters, and delivery fleets as battery costs continue declining and charging infrastructure expands, while government rebate programs in Victoria, Queensland, and ACT maintain purchase incentives.

Australia Bicycle Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Road Bicycle |

36% |

|

Technology |

Conventional |

60% |

|

Price |

Mid-Range |

45% |

|

Distribution Channel |

Offline Stores |

64% |

|

End User |

Men |

51% |

|

Region |

Australia Capital Territory & New South Wales |

30% |

Type Insights:

- Road Bicycle

- Mountain Bicycle

- Hybrid Bicycle

- Others

Road bicycle dominates with a market share of 36% of the total Australia bicycle market in 2025.

Road bicycles lead the market through their specialized design optimizing speed, efficiency, and performance on paved surfaces, attracting serious cyclists, fitness enthusiasts, and competitive riders seeking superior aerodynamic capabilities. Manufacturers continuously innovate with carbon fiber frame technology, aerodynamic tube profiles, and lightweight component integration, with companies like Trek introducing IsoFlow seat tube designs that reduce frame weight while improving rider comfort. The segment benefits from Australia's established road cycling culture including organized events, racing competitions, and group riding communities that sustain consistent demand. Pricing spans from entry-level models around 1,000 dollars to premium offerings exceeding 10,000 dollars featuring advanced materials and electronic shifting systems.

Professional cycling's influence drives consumer interest in road bike technology, with enthusiasts seeking equipment similar to WorldTour teams, while Gran Fondo events and charity rides create participation opportunities encouraging road bike purchases. Urban commuters increasingly adopt road-style bikes for efficient city travel, appreciating their speed advantages on longer commutes compared to hybrid alternatives. The segment faces competition from gravel bikes offering similar performance with increased versatility, though pure road bikes maintain popularity among performance-focused riders prioritizing maximum speed and efficiency on smooth surfaces.

Technology Insights:

- Electric

- Conventional

Conventional leads with a share of 60% of the total Australia bicycle market in 2025.

Conventional bicycles maintain market dominance through their affordability advantages, with per-unit costs running 40 to 50 percent lower than electric alternatives, making them accessible to budget-conscious consumers, students, and recreational riders. The segment benefits from established distribution networks, extensive service provider availability, and consumer familiarity with traditional bicycle mechanics requiring no specialized electrical system knowledge or battery management. Maintenance simplicity appeals to riders preferring straightforward mechanical repairs, avoiding concerns about battery replacement costs, charging infrastructure access, and electronic component longevity that characterize e-bike ownership. Fitness-oriented cyclists actively choose conventional bicycles for workout intensity control and calorie-burning benefits that electric assistance would diminish.

Conventional bicycles serve diverse applications from children's bikes and BMX riding to mountain biking and road racing where mechanical simplicity, weight reduction, and rider-powered performance remain priorities. The segment maintains strong presence in regional areas where charging infrastructure limitations make e-bikes less practical for extended rides. Manufacturers continue innovation through improved gear systems, hydraulic disc brakes, and lightweight materials that enhance performance without electric propulsion. Market sustainability depends on maintaining value propositions of affordability, simplicity, and pure cycling experience as e-bike technology advances and costs gradually decline.

Price Insights:

- Premium

- Mid-Range

- Low-Range

Mid-range exhibits a clear dominance with a 45% share of the total Australia bicycle market in 2025.

Mid-range bicycles occupy the market sweet spot by delivering reliable quality, modern features, and satisfactory performance at price points between 1,500 and 2,500 dollars that balance value and capability for mainstream consumers. This segment attracts urban commuters seeking dependable transportation with decent components, recreational riders wanting weekend enjoyment without premium investment, and fitness enthusiasts requiring adequate performance for regular exercise routines. Manufacturers position mid-range offerings with aluminum frames, quality gear systems, mechanical or hydraulic disc brakes, and contemporary geometries providing comfortable riding experiences suitable for varied applications.

The segment benefits from perceived value optimization, where consumers believe they receive substantial quality improvements over budget options without paying premium brand markups or marginal performance gains characteristic of high-end models. E-bike penetration is particularly strong in mid-range pricing as technology costs decline, making electric assistance accessible at 2,000 to 3,500 dollar price points. Distribution through both specialty retailers and larger sporting goods chains provides broad market access, while financing options make mid-range purchases manageable for average households facing cost-of-living pressures.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Online Stores

- Offline Stores

Offline stores lead with a share of 64% of the total Australia bicycle market in 2025.

Physical bicycle retailers maintain distribution dominance through providing essential services including test rides enabling customers to assess fit and handling, expert consultations matching riders with appropriate models, and professional assembly ensuring safety and optimal performance. Specialty bike shops offer ongoing relationship value through maintenance services, component upgrades, warranty support, and technical advice that online channels cannot replicate, building customer loyalty particularly for premium purchases where investment protection matters. The tactile experience of comparing multiple models, evaluating build quality, and receiving personalized recommendations from knowledgeable staff significantly influences purchase decisions for considered purchases often exceeding 1,000 dollars.

Giant operates over 12,000 retail stores across 50 countries demonstrating the enduring importance of physical presence, while Trek and Specialized maintain extensive authorized dealer networks ensuring consistent brand experience and service quality. Post-pandemic, traditional retailers successfully implemented hybrid models combining showroom experiences with online ordering and home delivery, capturing e-commerce growth while preserving service advantages. The channel faces pressure from direct-to-consumer brands bypassing traditional distribution and Chinese imports utilizing warehouse models with compressed pricing, though service quality concerns limit their premium segment penetration.

End User Insights:

- Men

- Women

- Kids

Men exhibit a clear dominance with a 51% share of the total Australia bicycle market in 2025.

Male cyclists dominate market participation through higher riding frequency, longer average distances, and stronger engagement across competitive, recreational, and commuting categories. Demographic data shows men participate in cycling at significantly higher rates than women, with male riders demonstrating aerobic insufficiency compared to female riders, indicating more active lifestyle integration. The segment spans diverse cycling disciplines from road racing and mountain biking to bike-packing and triathlon, with male consumers showing particular interest in performance-oriented road bikes, technical mountain bikes, and e-bikes for longer commutes.

Moreover, men aged 25 to 34 represent the most active gym and fitness participants, with significant crossover into cycling activities for cardiovascular fitness and outdoor recreation. Male consumers demonstrate stronger willingness to invest in premium bicycles, components, and accessories, driving higher average transaction values particularly in road cycling and mountain biking categories. Marketing strategies effectively target male demographics through competitive cycling events, professional team sponsorships, and performance-focused product positioning emphasizing speed, technical specifications, and achievement metrics.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales lead with a share of 30% of the total Australia bicycle market in 2025.

Australia Capital Territory and New South Wales lead the market through Sydney's position as the nation's largest city with over five million residents generating substantial commuting demand, recreational cycling participation, and urban mobility challenges that bicycles help address. The region benefits from major infrastructure investments, alongside extensive cycling corridor development throughout metropolitan Sydney and regional centers. High population density in Sydney, Newcastle, and Wollongong creates concentrated consumer bases supporting specialty bicycle retailers, service providers, and cycling communities that sustain market activity.

Canberra's planning as a purpose-built capital city incorporated cycling infrastructure from inception, with extensive path networks enabling high cycling participation rates supported by public service employment patterns favoring active commuting. The Garden City cycleway project commenced in 2025, enhancing northern suburbs connectivity and demonstrating ongoing infrastructure commitment. New South Wales government allocated significant Road Safety Program funding directed toward cycling and pedestrian upgrades, reinforcing policy support for active transport development. The region hosts major cycling events including the Great Victorian Bike Ride crossing into southern NSW, Tour de Cure charity rides, and numerous Gran Fondo events that strengthen cycling culture and drive bicycle purchases.

Market Dynamics:

Growth Drivers:

Why is the Australia Bicycle Market Growing?

Health & Wellness Consciousness Drives Cycling Adoption

The increasing focus on preventive healthcare and active lifestyles is fundamentally reshaping transportation and recreation choices across Australian demographics, with cycling recognized as an accessible, low-impact exercise delivering cardiovascular benefits, weight management support, and mental wellness improvements. 1,427,691 bicycle trips per day by Australians aged 9+ in 2025 was 13.3%. Fitness enthusiasts and health-conscious individuals significantly contribute to market growth, incorporating cycling into daily routines as an effective alternative to sedentary lifestyles linked to chronic disease risks including obesity, diabetes, and cardiovascular conditions.

Urban Mobility and Sustainability Requirements Transform Transportation Patterns

Rising urban congestion and escalating fuel costs are making traditional car commuting increasingly expensive and time-consuming, positioning bicycles as efficient alternatives enabling quicker travel through congested metropolitan areas while eliminating fuel expenses and vehicle maintenance costs. Prices of petrol in the five biggest cities (Sydney, Melbourne, Brisbane, Adelaide, and Perth) stood at 178.8 cents per litre (cpl), rising by 3.1 cpl compared to the last quarter. Moreover, traffic delays across Sydney, Melbourne, Brisbane, and Perth motivate office workers, students, and delivery riders to adopt cycling for superior mobility, with bicycles navigating congested routes, utilizing dedicated lanes, and avoiding parking challenges that plague motor vehicle commuters. The economic benefits of cycling extend beyond fuel savings to include reduced vehicle depreciation, lower insurance costs, and minimal maintenance requirements, enhancing appeal among cost-conscious consumers facing elevated living expenses.

Government Support and Infrastructure Investment Creates Enabling Environment

Substantial government investments in cycling infrastructure are fundamentally improving safety, convenience, and accessibility, directly addressing primary barriers that historically limited bicycle adoption across Australian communities. In 2026, the cycle path on the Sydney Harbour Bridge now features a new, smooth ramp that replaces a well-known 55-step staircase, providing cyclists with an uninterrupted route from North Sydney to the CBD after years of advocacy, discarded plans, and community resistance. The unique enhancement to the city's renowned bridge, which became accessible to the public, will facilitate the bike path for heavy e-bikes, bicycles with trailers, and senior riders.

Market Restraints:

What Challenges the Australia Bicycle Market is Facing?

High Initial Cost Barriers Limit Market Accessibility

Premium bicycle pricing creates significant entry barriers particularly for e-bikes where costs frequently exceed 3,000 dollars for quality models featuring reliable battery systems, capable motors, and durable components. E-bikes continue selling at substantially higher prices compared to traditional bicycles, with the technology premium representing 40 to 50 percent cost increases that challenge budget-conscious consumers in regions where wages remain modest and discretionary spending capacity faces pressure from elevated housing costs and living expenses. Financial access challenges emerge in areas lacking retailer financing options or buy-now-pay-later arrangements, while resale market uncertainty regarding battery lifespan and technological obsolescence creates hesitation around substantial e-bike purchases.

Infrastructure Gaps & Safety Concerns Constrain Adoption Growth

Significant infrastructure deficiencies persist across Australian cities despite recent investment commitments, revealing that trips under five kilometers still spend half their journey on roads without bike lanes or protective safety features even after planned strategic cycling corridor completion. Accident statistics and media coverage of cyclist injuries or fatalities reinforce perceptions of cycling danger, deterring potential riders despite data showing per-kilometer injury rates comparable to other transport modes. Infrastructure coordination challenges between state governments managing major arterial roads and local councils controlling residential streets create gaps where protected bike lanes terminate abruptly, forcing cyclists onto dangerous shared roadways for critical connection segments. Parking infrastructure limitations at transport hubs, commercial centers, and public venues constrain multi-modal journey planning, with inadequate secure bike storage deterring theft-concerned commuters who require confidence their bicycles will remain safe during work hours or shopping activities.

Supply Chain Dependencies Create Vulnerability & Cost Pressures

Australia's minimal domestic bicycle manufacturing creates near-total reliance on overseas production, with all major brands and emerging direct-to-consumer companies manufacturing bicycles in Taiwan, China, Cambodia, and other Asian production centers before importing finished products. China's dominance over four-fifths of global lithium-ion battery cell manufacturing for e-bikes introduces supply chain vulnerabilities where geopolitical tensions, trade disputes, or pandemic-style disruptions could severely constrain component availability and drive price increases beyond consumer affordability thresholds. Import tariffs including the five percent duty on e-bikes from countries without free trade agreements with Australia directly increase retail pricing for products manufactured in Taiwan, Europe, and India, disadvantaging these suppliers relative to Chinese and ASEAN competitors covered by preferential trade arrangements. Shipping cost volatility experienced during pandemic periods demonstrated exposure to freight rate fluctuations, with container shortages and port congestion creating months-long delivery delays that frustrated consumers expecting prompt product availability and forced retailers to maintain elevated inventory levels tying up working capital.

Competitive Landscape:

Key market players in Australia’s bicycle market are focusing on several practical moves to strengthen business growth. Major brands and retailers are expanding their e-bike portfolios, responding to rising demand for commuter-friendly and sustainable transport options. Companies are also investing in local assembly and better supply chain partnerships to reduce delivery delays and manage cost pressures. Many players are improving customer experience through omni-channel retail models, combining online sales with in-store servicing and test-ride facilities. Subscription-based bike leasing and finance options are being introduced to make premium bicycles more accessible. At the same time, businesses are building stronger community engagement through cycling events, club partnerships, and advocacy for better cycling infrastructure. Sustainability is another focus area, with brands adopting recycled materials and longer-life product designs. Overall, these strategies help companies attract urban commuters, recreational cyclists, and performance-focused consumers while keeping pace with shifting lifestyle trends. Some of the market players include:

- Avanti Bikes

- Bastion Cycles

- Bossi Bicycles

- Curve Cycling

- Down Under Cycles Pty Ltd

- EARTH Electric Bikes

- Giant Bicycles

- GPI Apollo Bicycle Co. Pty. Ltd

- Malvern Star

- Merida Bikes

- Reid Cycles

- Trek Bicycle Corporation

Recent Developments:

- In December 2025, Mountain Biking in Oceania is poised for growth in 2025 with the debut of the Oceania Mountain Bike Continental Series. The Continental Series was created through strong cooperation between the Union Cycliste Internationale (UCI) and the Continental Confederations. The Oceania Mountain Bike Continental Series will offer Oceania riders a new chance to qualify for the UCI Mountain Bike World Cups, which are part of the WHOOP UCI Mountain Bike World Series. The first Oceania Mountain Bike Continental Series will feature three Cross-country rounds and five Downhill rounds in Australia and New Zealand, from January to May 2025.

Australia Bicycle Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Road Bicycle, Mountain Bicycle, Hybrid Bicycle, Others |

| Technologies Covered | Electric, Conventional |

| Prices Covered | Premium, Mid-Range, Low-Range |

| Distribution Channel Covered | Online Stores, Offline Stores |

| End Users Covered | Men, Women, Kids |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Avanti Bikes, Bastion Cycles, Bossi Bicycles, Curve Cycling, Down Under Cycles Pty Ltd, EARTH Electric Bikes, Giant Bicycles, GPI Apollo Bicycle Co. Pty. Ltd, Malvern Star, Merida Bikes, Reid Cycles, Trek Bicycle Corporation, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Bicycle Market Report

The Australia bicycle market size was valued at USD 2.00 Billion in 2025.

The Australia bicycle market is expected to grow at a compound annual growth rate of 5.81% from 2026-2034 to reach USD 3.33 Billion by 2034.

Road bicycle dominated the market with 36% share in 2025, driven by performance-focused designs, aerodynamic innovations, strong demand from fitness enthusiasts, and Australia's established road cycling culture including organized events, racing competitions, and group riding communities that sustain consistent premium segment demand.

Key factors driving the Australia bicycle market include increasing health consciousness, rising urban congestion making bicycles efficient commuting alternatives avoiding fuel costs and parking challenges, growing environmental awareness favoring zero-emission transport, government infrastructure investments committed across states for bike lanes and strategic corridors, e-bike adoption accelerating among commuters and older demographics supported by rebate programs, and expanding recreational cycling culture strengthened by organized events and community groups.

Major challenges include high upfront e-bike costs exceeding creating affordability barriers despite limited rebate program reach, infrastructure gaps with two-thirds of inner Melbourne roads lacking cycling facilities and outer suburbs creating safety concerns particularly for women and older adults, supply chain dependencies with minimal domestic manufacturing creating vulnerability to overseas disruption, component shortages affecting drivetrain and brake system availability, and coordination difficulties between state governments managing arterial roads and local councils controlling residential streets producing disconnected bike lane networks that terminate abruptly forcing cyclists onto dangerous shared roadways.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)