Australia Biomethane Market Size, Share, Trends and Forecast by Feedstock, Application, Production Method, and Region, 2026-2034

Australia Biomethane Market Summary:

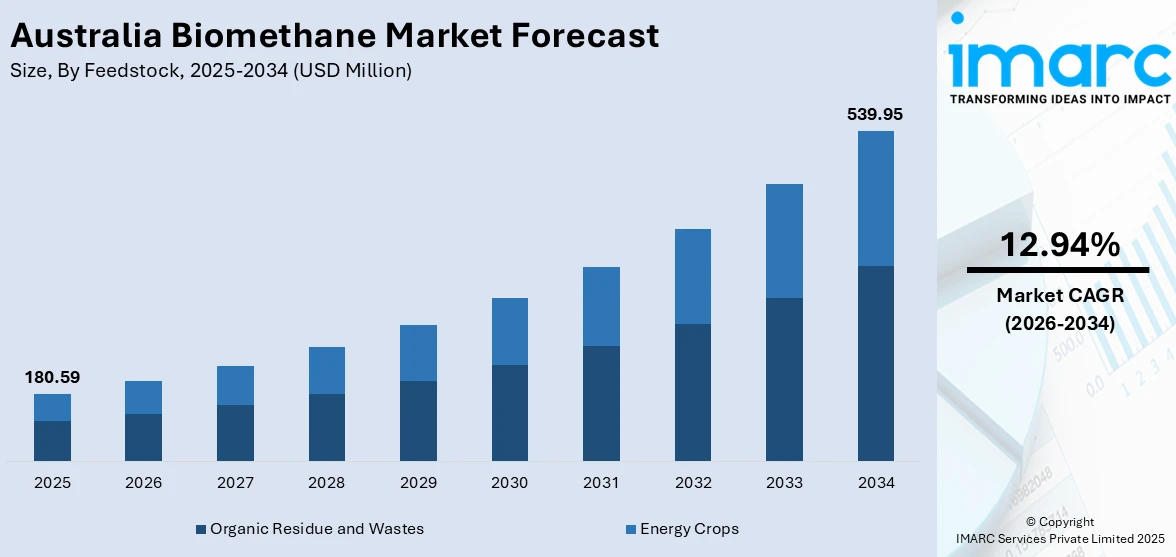

The Australia biomethane market size was valued at USD 180.59 Million in 2025 and is projected to reach USD 539.95 Million by 2034, growing at a compound annual growth rate of 12.94% from 2026-2034.

The Australia biomethane market is gaining significant momentum as the nation accelerates its transition toward renewable gas solutions and sustainable energy pathways. Increasing government commitment to decarbonizing hard-to-abate industrial sectors, expanding waste-to-energy infrastructure, and growing circular economy practices are strengthening adoption. Advancements in anaerobic digestion technologies, rising demand for carbon-neutral gas alternatives, and strategic investments in biogas upgrading systems are reshaping the energy landscape, positioning Australia as an emerging hub for renewable gas production and Australia biomethane market share.

Key Takeaways and Insights:

- By Feedstock: Organic residue and wastes dominates the market with a share of 72.4% in 2025, owing to the widespread availability of municipal solid waste, sewage sludge, and agricultural residues combined with established collection mechanisms and proximity to major population centers across the country.

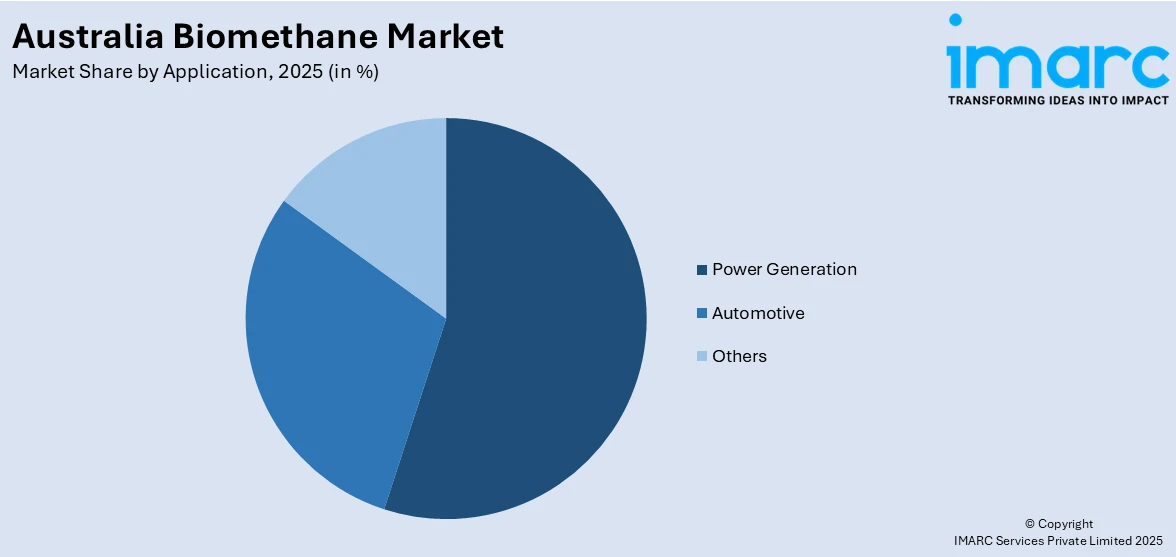

- By Application: Power generation leads the market with a share of 54.6% in 2025, driven by growing integration of biogas-derived electricity into the national grid and increasing demand for dispatchable renewable energy sources to complement intermittent solar and wind generation.

- By Production Method: Anaerobic digestion exhibits a clear dominance in the market with 81.9% share in 2025, reflecting its proven reliability, technological maturity, and suitability for processing diverse organic waste feedstocks including municipal waste, sewage sludge, and agricultural residues.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 34.7% share in 2025, driven by the existence of historic biomethane infrastructure projects, the production of a lot of trash in cities, and the government's strong support for renewable gas projects throughout the Sydney metropolitan area.

- Key Players: Key players drive the Australia biomethane market by expanding production capacities, investing in advanced biogas upgrading technologies, and forging strategic partnerships with gas network operators. Their investments in circular economy infrastructure, waste processing capabilities, and renewable gas certification are boosting awareness, accelerating commercial deployment, and ensuring consistent biomethane availability across diverse industrial and residential segments.

To get more information on this market Request Sample

The Australia biomethane market is advancing as government, industry, and energy infrastructure operators embrace renewable gas as a practical pathway to decarbonize sectors that cannot be easily electrified. A major driver shaping this progress is the growing recognition of biomethane as a direct, carbon-neutral substitute for fossil natural gas, enabling seamless integration into existing pipeline networks without requiring appliance modifications. For instance, the Australian Government’s 2024 Future Made in Australia initiative allocated $22.7 Billion over the next decade to the Australian Renewable Energy Agency to support the commercialization of low-carbon fuels including biomethane, reinforcing the nation’s commitment to renewable gas development. Policy encouragement through emission reduction frameworks such as the Safeguard Mechanism, expanding waste diversion mandates, and rising demand from hard-to-abate manufacturing sectors reliant on high-temperature gas applications are contributing to a more favorable investment environment. These structural tailwinds are expected to sustain strong growth in biomethane production and consumption across Australia.

Australia Biomethane Market Trends:

Growing Integration of Renewable Gas into National Energy Policy

Australia is witnessing a strategic shift as biomethane gains recognition within national energy planning frameworks. The release of the 2024 Future Gas Strategy explicitly acknowledged biomethane’s role in decarbonizing the gas sector, while calls for a Renewable Gas Target and amendments to the National Greenhouse and Energy Reporting Scheme are building policy momentum. Energy Networks Australia has recommended Hydrogen Headstart Program to include biomethane funding, reflecting the growing institutional support for renewable gas across federal and state jurisdictions, contributing to Australia biomethane market growth.

Expansion of Waste-to-Energy Circular Economy Infrastructure

Australia is rapidly developing circular economy systems that convert organic waste into renewable energy and useful byproducts. These projects divert municipal, commercial, and agricultural waste from landfills while producing biomethane, biogenic carbon dioxide, and organic fertilizers. For example, Optimal Renewable Gas announced the Westbury BioHub in Tasmania in partnership with Solstice Energy, designed to process between 86,000 and 150,000 tons of organic waste annually and produce approximately 320 terajoules of biomethane, making it the first facility of its kind in the country.

Advancement of Biomethane Grid Injection Technologies

Biomethane grid injection is emerging as a commercially viable pathway in Australia, supported by pioneering demonstration projects and evolving technical standards. The Malabar Biomethane Injection Plant, developed by Jemena in partnership with Sydney Water, became Australia’s first facility to inject biomethane into a gas distribution network in 2023, initially producing around 95 terajoules of renewable gas annually for approximately 6,300 homes. This milestone has catalyzed broader industry interest in scaling biogas-to-grid infrastructure across multiple states.

Market Outlook 2026-2034:

Australia’s biomethane market is positioned for robust expansion, underpinned by strengthening policy frameworks, rising industrial demand for carbon-neutral gas alternatives, and ongoing infrastructure development across key states. Increasing feedstock availability from agricultural, municipal, and industrial organic waste streams, coupled with advancements in anaerobic digestion and biogas upgrading technologies, are expected to drive higher production capacities. Expanding renewable gas certification schemes, strategic partnerships between energy infrastructure companies and waste processors, and growing state-level support for biogas-to-grid projects are anticipated to strengthen the commercial viability and long-term growth trajectory of the market. The market generated a revenue of USD 180.59 Million in 2025 and is projected to reach a revenue of USD 539.95 Million by 2034, growing at a compound annual growth rate of 12.94% from 2026-2034.

Australia Biomethane Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Feedstock |

Organic Residue and Wastes |

72.4% |

|

Application |

Power Generation |

54.6% |

|

Production Method |

Anaerobic Digestion |

81.9% |

|

Region |

Australia Capital Territory & New South Wales |

34.7% |

Feedstock Insights:

- Organic Residue and Wastes

- Biowaste

- Municipal Waste

- Sewage Waste

- Agricultural Waste

- Others

- Energy Crops

Organic residue and wastes dominates with a market share of 72.4% of the total Australia biomethane market in 2025.

Organic residue and waste-based feedstocks form the backbone of Australia’s biomethane production ecosystem, driven by the consistent year-round availability of municipal solid waste, sewage sludge, and food processing residues. Urban areas generate substantial volumes of organic waste through established collection systems, creating a reliable and cost-effective feedstock supply for anaerobic digestion facilities. Australia’s Bioenergy Roadmap identifies municipal solid waste and wastewater processing as the largest feedstock opportunity for at-scale biogas production, owing to their proximity to population centres and existing waste management infrastructure.

Agricultural waste, including crop residues and livestock manure, further supplements the organic feedstock base, particularly in regional areas with intensive farming operations. These diverse waste streams enable biomethane producers to optimize plant utilization rates and diversify revenue through waste gate fees, renewable gas production, and digestate sales. For instance, Delorean Corporation’s SA1 bioenergy facility in Edinburgh Parks, South Australia, is designed to process approximately 70,000 tonnes per annum of commercial and industrial food waste, demonstrating the viability of large-scale organic waste-to-biomethane conversion in Australia.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Automotive

- Power Generation

- Others

Power generation leads with a share of 54.6% of the total Australia biomethane market in 2025.

Power generation represents the primary application for biomethane in Australia, driven by the growing need for dispatchable renewable energy sources that can complement intermittent solar and wind generation. Biomethane-fueled power plants provide baseload and peaking capacity, enhancing grid stability while reducing the carbon intensity of electricity production. The national electricity market has seen renewables account for over 27.7% of electricity generation by 2024, and bioelectricity continues to expand through federal support via the Australian Renewable Energy Agency and state-level biogas-to-grid injection initiatives.

The expansion of power generation from biomethane is further supported by Australia's updated Safeguard Mechanism, which requires the nation's largest industrial emitters to progressively reduce scope one emissions. This regulatory pressure is encouraging power producers and industrial users to adopt renewable gas as a compliance pathway. The Malabar Biomethane Injection Plant, jointly funded by Jemena and ARENA, became the first project in Australia to inject biomethane into a gas distribution network, producing renewable gas capable of supplying thousands of residential customers across New South Wales and establishing a benchmark for future biogas-to-grid initiatives nationwide.

Production Method Insights:

- Anaerobic Digestion

- Gasification

Anaerobic digestion exhibits a clear dominance with a 81.9% share of the total Australia biomethane market in 2025.

Anaerobic digestion is the predominant production method in Australia’s biomethane sector, leveraging its technological maturity and proven effectiveness in processing diverse organic waste streams. The method involves bacterial decomposition of organic matter in oxygen-free environments to produce biogas, which is subsequently upgraded to pipeline-quality biomethane through membrane separation or pressure swing adsorption technologies. Australia’s existing wastewater treatment plants, many of which already operate anaerobic digesters, provide a natural foundation for scaling biomethane production with relatively modest capital additions for biogas upgrading equipment.

The dominance of anaerobic digestion is reinforced by its versatility in handling varied feedstock types, including sewage sludge, food waste, and agricultural residues, enabling operators to diversify input sources and stabilize production volumes. Furthermore, the technology supports circular economy outcomes by generating digestate that can be processed into organic fertilizers. For instance, Delorean Corporation’s SA1 facility in South Australia utilizes anaerobic digestion technology to process commercial and industrial food waste into biomethane, with the project also producing biogenic food-grade liquid carbon dioxide and liquid fertilizer products, demonstrating multiple revenue stream potential.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the leading segment with a 34.7% share of the total Australia biomethane market in 2025.

Australia Capital Territory and New South Wales lead the national biomethane market, driven by the concentration of waste processing infrastructure, dense urban populations generating substantial organic waste volumes, and pioneering renewable gas initiatives. The region benefits from the landmark Malabar Biomethane Injection Plant in Sydney's south-eastern suburbs, which established the country's first biomethane-to-gas-network injection. Strong government backing for renewable energy frameworks and growing industrial demand for carbon-neutral gas alternatives continue to reinforce the region's dominance.

Strategic partnerships are further accelerating biomethane development across the region. In October 2024, Jemena signed a memorandum of understanding with Japanese trading company Sojitz to assess the feasibility of developing several new biomethane plants across regional New South Wales. This collaboration follows earlier agreements with Optimal Renewable Gas and Valorify, collectively aiming to build a robust biomethane supply chain capable of serving residential and industrial customers throughout the state's extensive gas distribution network.

Market Dynamics:

Growth Drivers:

Why is the Australia Biomethane Market Growing?

Strengthening Government Policy and Regulatory Support for Renewable Gas

The Australian Government’s escalating commitment to decarbonization through comprehensive policy frameworks is creating a robust foundation for biomethane market expansion. The 2024 Future Gas Strategy explicitly recognized biomethane’s critical role in decarbonizing the gas sector, while the updated Safeguard Mechanism mandates Australia’s largest industrial emitters to progressively reduce their emissions. These regulatory drivers are compelling energy-intensive industries to seek renewable gas alternatives for their operations.. State governments are also advancing supportive policy environments. New South Wales has actively consulted on the development of a renewable gas sector, while Energy Networks Australia has recommended implementing a Renewable Gas Target for Australian industry by 2030. The development of new Emissions Reduction Fund methods for biomethane by the Clean Energy Regulator and the launch of GreenPower’s Renewable Gas Certification scheme are establishing the market infrastructure necessary to incentivize production and enable commercial uptake of biomethane across the economy.

Rising Industrial Demand for Carbon-Neutral Gas in Hard-to-Abate Sectors

Australia’s manufacturing and industrial sectors are increasingly recognizing biomethane as the most practical decarbonization option for processes that require high-temperature heat and cannot be easily electrified. Industries producing essential goods such as glass, bricks, cement, fertilizers, and processed foods rely heavily on natural gas for their operations, and biomethane offers a chemically identical, carbon-neutral substitute that requires no modifications to existing equipment or appliances. This compatibility with current gas infrastructure makes biomethane uniquely positioned to address industrial emissions without disrupting production processes. A July 2025 report commissioned by Bioenergy Australia found that Renewable Natural Gas is emerging as the most affordable and practical solution to looming gas shortages on Australia’s east coast, while simultaneously providing a critical decarbonization pathway for hard-to-abate sectors. With approximately seventy percent of Australia’s gas consumption attributed to industrial activities, the demand for renewable gas alternatives is expected to grow substantially as emission reduction obligations tighten and industries seek compliant fuel options.

Expanding Waste Diversion Mandates and Circular Economy Adoption

Australia’s evolving waste management regulations and growing emphasis on circular economy principles are creating favorable conditions for biomethane production by ensuring a steady supply of organic feedstocks. Rising landfill levies, organic waste bans in several states, and waste separation requirements are redirecting substantial volumes of biodegradable material toward energy recovery pathways. These regulatory changes are encouraging investment in anaerobic digestion infrastructure that converts waste into renewable gas, organic fertilizers, and other valuable byproducts. The circular economy model underpinning biomethane projects delivers multiple environmental and economic benefits simultaneously. For instance, in April 2025, the Australian Gas Infrastructure Group signed a formal connection agreement with Delorean Corporation to inject up to 210 terajoules of biomethane annually from commercial and industrial organic waste into the South Australian gas network, marking the first such agreement in the country. These developments demonstrate how waste diversion objectives and renewable energy targets are converging to create commercially viable biomethane production opportunities across Australia.

Market Restraints:

What Challenges the Australia Biomethane Market is Facing?

High Production Costs and Limited Financial Incentives

The cost of producing biomethane in Australia remains significantly higher than conventional natural gas, posing a substantial barrier to widespread commercial adoption. Capital expenditure for anaerobic digestion plants, biogas upgrading equipment, and grid injection infrastructure is considerable, and the absence of dedicated federal incentive programs equivalent to those available in European markets limits investor confidence. Without targeted production subsidies, renewable gas mandates, or biomethane-specific funding mechanisms, project developers face challenges in achieving competitive pricing against fossil gas alternatives, slowing the pace of new facility commissioning.

Dispersed Feedstock Supply and Seasonal Availability Constraints

Although Australia possesses abundant organic waste and agricultural biomass resources, feedstock supply chains for biomethane production remain underdeveloped and geographically dispersed. Agricultural residues and crop wastes are distributed across vast rural areas far from gas network connection points, increasing collection and transportation costs. Furthermore, the inherent seasonality of many agricultural feedstock sources creates variability in biomethane plant utilization rates, directly impacting project economics and making it challenging to maintain consistent year-round production volumes necessary for viable commercial operations.

Immature Byproduct Markets and Regulatory Uncertainty

The market for anaerobic digestion byproducts, particularly digestate used as biofertilizer, remains limited in Australia due to low farmer awareness and a lack of standardized regulatory guidelines ensuring digestate quality and safety. Underdeveloped byproduct revenue streams reduce the overall economic viability of biomethane projects that depend on value-stacking across multiple outputs. Additionally, regulatory uncertainty surrounding renewable gas certification frameworks, gas quality standards for grid injection, and long-term emission reduction credit eligibility continues to create investment hesitancy among project proponents and financial institutions.

Competitive Landscape:

The Australia biomethane market is evolving rapidly as energy infrastructure operators, bioenergy developers, and waste management companies expand their presence in the renewable gas sector. Companies are focusing on securing feedstock supply agreements, developing advanced biogas upgrading capabilities, and establishing long-term offtake arrangements with industrial gas users. Competition is driven by investments in grid injection infrastructure, anaerobic digestion technologies, and strategic partnerships between gas network operators and biogas producers. GreenPower’s Renewable Gas Certification scheme is further shaping competitive dynamics by enabling certified producers to access premium market segments. As a result, market participants are continually refining their strategies to strengthen operational capabilities and capture emerging commercial opportunities in Australia’s growing biomethane sector.

Australia Biomethane Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Feedstocks Covered |

|

|

Applications Covered |

Automotive, Power Generation, Others |

|

Production Methods Covered |

Anaerobic Digestion, Gasification |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Biomethane Market Report

The Australia biomethane market size was valued at USD 180.59 Million in 2025.

The Australia biomethane market is expected to grow at a compound annual growth rate of 12.94% from 2026-2034 to reach USD 539.95 Million by 2034.

Organic residue and wastes dominated the market with a share of 72.4%, driven by the widespread availability of municipal solid waste, sewage sludge, and agricultural residues along with established collection infrastructure and proximity to major urban centers.

Key factors driving the Australia biomethane market include strengthening government policy support, rising industrial demand for carbon-neutral gas in hard-to-abate sectors, expanding waste diversion mandates, and growing investments in anaerobic digestion and grid injection infrastructure.

Major challenges include high production costs relative to conventional natural gas, dispersed feedstock supply chains with seasonal availability constraints, immature byproduct markets for digestate, limited dedicated financial incentive mechanisms, and regulatory uncertainty around renewable gas certification and grid injection standards.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)