Australia Black Pepper Market Size, Share, Trends and Forecast by Product, Source, Form, Distribution Channel, Application, and Region, 2026-2034

Australia Black Pepper Market Summary:

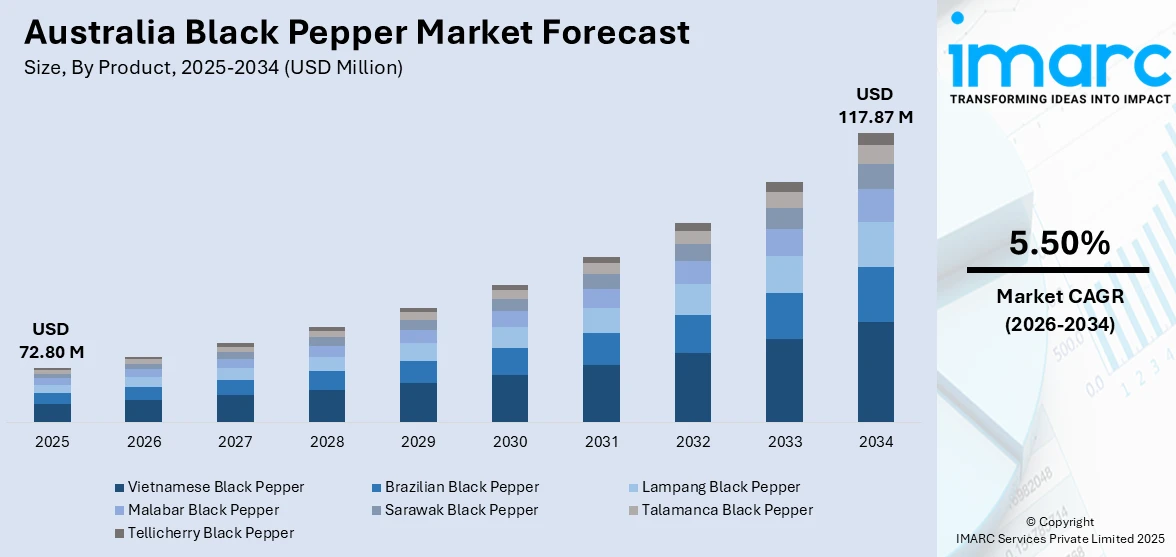

The Australia black pepper market size was valued at USD 72.80 Million in 2025 and is projected to reach USD 117.87 Million by 2034, growing at a compound annual growth rate of 5.50% from 2026-2034.

The Australia black pepper market is experiencing sustained expansion driven by rising consumer preference for natural seasonings and clean-label ingredients. Increasing adoption of diverse international cuisines, growing awareness about the health benefits of piperine, and steady demand from the food processing sector are contributing to market momentum. The expanding e-commerce landscape and premiumization of spice products are further strengthening the Australia black pepper market share.

Key Takeaways and Insights:

- By Product: Vietnamese black pepper dominates the market with a share of 34.8% in 2025, owing to its competitive pricing, consistent supply volume, and well-established trade networks that ensure reliable access across Australian import channels.

- By Source: Inorganic leads the market with a share of 71.2% in 2025. This dominance is driven by cost-effectiveness, wider commercial availability, and strong demand from food processing and foodservice industries requiring large-volume conventional pepper supplies.

- By Form: Ground black pepper holds the majority of the market with a share of 46.5% in 2025, owing to its convenience for immediate culinary application, widespread use in commercial food preparation, and consistent consumer preference for ready-to-use spice formats.

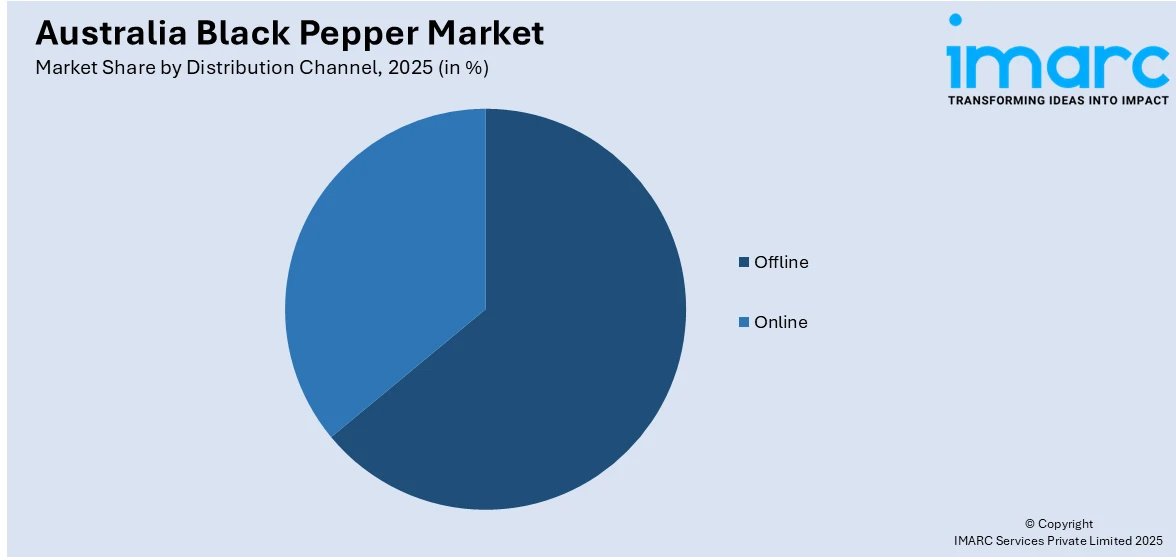

- By Distribution Channel: Offline exhibits a clear dominance in the market with 63.9% share in 2025, reflecting strong consumer reliance on supermarkets, specialty stores, and wholesale channels for purchasing everyday seasoning products with tactile quality assessment.

- By Application: Food and beverages represent the biggest segment with a market share of 68.7% in 2025, reflecting the core role of black pepper as an essential seasoning ingredient across meat processing, ready-to-eat meal production, and household cooking applications throughout Australia.

- By Region: Australia Capital Territory & New South Wales are the largest region with 36.4% share in 2025, driven by the concentration of population centers in Sydney and Canberra, higher density of food processing facilities, and a diverse multicultural demographic fueling spice consumption.

- Key Players: Key players drive the Australia black pepper market by expanding product portfolios, improving sourcing transparency, and strengthening retail distribution. Their investments in premiumization, sustainable procurement, and partnerships with foodservice providers boost awareness, accelerate adoption, and ensure consistent product availability.

To get more information on this market Request Sample

The Australia black pepper market is advancing steadily as consumers, food manufacturers, and foodservice operators increasingly prioritize natural flavor enhancement and health-conscious ingredient sourcing. A key factor driving this progress is the growing integration of black pepper across diverse culinary applications, supported by Australia’s expanding multicultural dining culture and rising preference for ethnic cuisines. For instance, Australia’s overall spices and seasonings market reached approximately USD 570.6 Million in 2024, reflecting broad-based growth in consumer demand for diverse flavoring ingredients. The country’s strict food safety standards administered by the Department of Agriculture, Fisheries and Forestry ensure that imported black pepper meets rigorous quality benchmarks, reinforcing consumer confidence. Additionally, the health benefits associated with piperine, the active compound in black pepper, are gaining recognition among wellness-oriented consumers, further strengthening demand. The premiumization of spice offerings, including single-origin and organic variants, along with expanding online retail channels, is creating new revenue opportunities and broadening market access for both established brands and emerging specialty producers across Australia.

Australia Black Pepper Market Trends:

Growing Preference for Organic and Clean-Label Spices

Australian consumers are increasingly seeking organic and clean-label spice products, driven by heightened awareness of food quality and sustainable sourcing practices. This shift is prompting retailers and brands to expand their organic black pepper offerings. For instance, Australia’s organic spices market was valued at approximately USD 584 Million in 2025 and is projected to reach USD 995 Million by 2034. The preference for transparency in ingredient sourcing and pesticide-free cultivation is reshaping purchasing patterns and supporting Australia black pepper market growth.

Rising Demand Driven by Multicultural Cuisine Adoption

The expanding multicultural population in Australia is currently fueling the demand for diverse spice profiles, including black pepper varieties used in Asian, Middle Eastern, and Mediterranean cuisines. Restaurants, home cooks, and food manufacturers are incorporating broader seasoning blends into their offerings. For instance, in May 2025, Melbourne-based Mingle Seasoning expanded into Coles and Woolworths with eight new flavour blends across Australia. This cultural diversification is broadening black pepper consumption patterns significantly.

Expansion of E-Commerce and Direct-to-Consumer Spice Sales

Digital retail channels are transforming spice purchasing in Australia, enabling consumers to access premium, single-origin, and specialty black pepper varieties previously limited to niche stores. E-commerce platforms and subscription-based spice services are gaining traction among urban consumers seeking convenience and product diversity. For instance, in December 2025, ofi launched a solar-powered facility at Kerabury Orchards in New South Wales, generating 83% of the site’s energy needs, supporting sustainable spice processing operations in Australia.

Market Outlook 2026-2034:

The Australia black pepper market is positioned for steady growth over the forecast period, supported by sustained consumer demand for natural seasonings, expanding foodservice operations, and increasing integration of black pepper in processed food manufacturing. Rising health consciousness, premiumization trends, and growing multicultural culinary influences are expected to drive consistent demand across retail, wholesale, and online distribution channels. The market generated a revenue of USD 72.80 Million in 2025 and is projected to reach a revenue of USD 117.87 Million by 2034, growing at a compound annual growth rate of 5.50% from 2026-2034. Investments in sustainable sourcing, traceability frameworks, and digital supply chain optimization are expected to enhance product quality assurance and strengthen consumer confidence. Additionally, the expansion of organic and specialty pepper offerings, coupled with the growth of food delivery platforms and home cooking culture, is anticipated to create new consumption avenues and broaden market accessibility across urban and regional areas throughout Australia.

Australia Black Pepper Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Vietnamese Black Pepper |

34.8% |

|

Source |

Inorganic |

71.2% |

|

Form |

Ground Black Pepper |

46.5% |

|

Distribution Channel |

Offline |

63.9% |

|

Application |

Food and Beverages |

68.7% |

|

Region |

Australia Capital Territory and New South Wales |

36.4% |

Product Insights:

- Brazilian Black Pepper

- Lampang Black Pepper

- Malabar Black Pepper

- Sarawak Black Pepper

- Talamanca Black Pepper

- Tellicherry Black Pepper

- Vietnamese Black Pepper

Vietnamese black pepper dominates with a market share of 34.8% of the total Australia black pepper market in 2025.

Vietnam's established position as the world's foremost black pepper exporting nation underpins the strong preference for Vietnamese varieties within the Australian market. Vietnamese black pepper is widely recognized for delivering a consistently bold flavor profile with reliable piperine concentration, making it a preferred choice among food manufacturers, retailers, and foodservice operators seeking dependable quality at competitive price points. Australia's well-developed trade relationships and import channels with Vietnamese suppliers ensure a stable and continuous supply pipeline that effectively meets the procurement requirements of both large-scale commercial processors and everyday retail consumers throughout the country.

The versatility of Vietnamese black pepper across a broad spectrum of culinary applications, ranging from finely ground seasoning blends to whole peppercorn mixes, significantly enhances its appeal within Australia's increasingly diverse food landscape. Food processors particularly value Vietnamese varieties for their uniform quality when incorporated into marinades, ready-to-eat meal formulations, and pre-mixed seasoning products that demand consistent flavor delivery. The growing consumer preference for affordable yet high-quality spice options further reinforces sustained demand for Vietnamese-origin black pepper across both household and commercial consumption channels throughout Australia.

Source Insights:

- Organic

- Inorganic

Inorganic leads with a share of 71.2% of the total Australia black pepper market in 2025.

Conventionally sourced black pepper maintains its commanding position within the Australian market, driven by its cost-effectiveness, widespread commercial availability, and strong compatibility with large-volume food manufacturing operations. Food processors, restaurant chains, institutional caterers, and wholesale buyers consistently rely on conventional pepper for its predictable quality characteristics and significantly lower procurement costs compared to certified organic alternatives. Well-established global supply networks connecting major pepper-producing nations with Australian importers ensure uninterrupted year-round access to conventional black pepper, supporting stable pricing and efficient inventory management for businesses across the supply chain.

The extensive distribution of conventionally sourced pepper across supermarket chains, wholesale outlets, specialty food stores, and foodservice supply channels reinforces its accessibility across all consumer and commercial segments. Although demand for organic spice alternatives continues to grow, the considerable price premium associated with organic certification limits its penetration within price-sensitive commercial and mass-market retail environments. Conventional pepper's seamless integration into high-throughput automated food processing systems, standardized seasoning formulations, and bulk blending operations further consolidates its dominance, as established procurement networks continue to sustain preference for inorganic black pepper across Australia's food industry.

Form Insights:

- Ground Black Pepper

- Rough Cracked Black Pepper

- Whole Black Pepper

Ground black pepper is the largest segment, accounting for 46.5% of the total Australia black pepper market in 2025.

Ground black pepper's market leadership is firmly rooted in its ready-to-use convenience and widespread integration across household kitchens, commercial food preparation environments, and industrial manufacturing operations throughout Australia. Consumers and food processors alike prefer the ground format for its consistent granularity, effortless incorporation into diverse recipes, and immediate flavor release upon application, eliminating the need for additional grinding equipment or preparation steps. The format is especially well-suited for processed food applications, including marinades, sauces, snack seasonings, soup bases, and ready-to-eat meal formulations that require uniform seasoning distribution across large production volumes.

The extensive retail availability of ground black pepper across major Australian supermarket networks, independent grocery stores, and specialty food outlets ensures consistent consumer access at accessible price points, supporting habitual repurchase patterns among households. Food manufacturers particularly favor ground pepper for its compatibility with automated production lines and standardized seasoning blend specifications that demand precise flavor consistency across large batches. The strengthening home cooking culture in Australia, fueled by growing interest in culinary experimentation, international recipe exploration, and meal preparation from scratch, continues to sustain robust household demand for ground black pepper products across diverse demographic segments.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Offline

- Online

Offline holds the largest share at 63.9% of the total Australia black pepper market in 2025.

Offline distribution channels retain their dominant position within the Australian black pepper market, underpinned by the extensive retail footprint of major supermarket networks, specialty food stores, independent grocers, and wholesale distributors operating across metropolitan and regional areas. Australian consumers continue to demonstrate a strong preference for in-store spice purchasing, driven by the ability to physically assess packaging integrity, compare competing brands, evaluate product freshness, and take advantage of promotional pricing and loyalty program benefits. The integration of black pepper into routine grocery shopping baskets as a staple pantry item ensures high-frequency repeat purchases through brick-and-mortar retail outlets nationwide.

The well-established presence of leading retailers and independent specialty stores across diverse geographic locations ensures broad and equitable accessibility for black pepper products throughout the country. Foodservice distributors, wholesale supply companies, and cash-and-carry outlets further reinforce offline channel dominance by catering to restaurants, hotels, catering companies, and institutional buyers requiring bulk pepper procurement at competitive wholesale pricing. Strategic in-store merchandising of black pepper alongside complementary cooking ingredients and meal preparation essentials maximizes consumer visibility, encourages impulse purchasing, and strengthens overall brand engagement within physical retail environments.

Application Insights:

- Food and Beverages

- Pharmaceuticals

- Personal Care

- Others

Food and beverages represent the leading category with 68.7% share of the total Australia black pepper market in 2025.

The market for black pepper in Australia is dominated by the food and beverage sector, which is indicative of the spice's essential and indispensable function as a flavoring in almost every culinary application. Black pepper creates steady and recurrent commercial demand all year long because it is a necessary ingredient in the manufacture of meat, sauces, snacks, soups, and broths, as well as ready-to-eat meals. Black pepper continues to be one of the most widely used seasonings in domestic kitchens across Australia, where households also use large amounts of the spice for regular cooking. Household consumption patterns are being amplified by the increasing popularity of preparing meals at home and experimenting with gourmet cooking.

High-volume black pepper procurement for commercial kitchen operations nationwide is fueled by the ongoing growth of Australia's foodservice sector, which includes eateries, cafes, fast-food chains, catering businesses, and meal delivery services. Black pepper's extraordinary adaptability to a wide range of culinary styles, including traditional Australian cuisines as well as Asian, European, Middle Eastern, and Latin American preparations, guarantees incredibly wide application coverage. In the Australian market, the growing trend of functional food production that incorporates piperine due to its known bioavailability-enhancing qualities is opening up new demand channels in the categories of nutritional food products and health-oriented beverages.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory and New South Wales accounts for the highest revenue share of 36.4% of the total Australia black pepper market in 2025.

Due mainly to the concentration of the country's most populated metropolitan centers and their vast surrounding urban corridors along with the national capital, the Australia Capital Territory and New South Wales area hold the highest share of the Australian black pepper market. A significant amount of Australia's import distribution centers, cold chain logistics infrastructure, and food processing facilities are located in this region, which makes it easier to buy peppers, store them, and run a supply chain that efficiently serves both domestic and international markets. There is a strong need for a variety of spice profiles throughout retail supermarkets, specialty food stores, and a vast foodservice network due to the region's extremely diverse and expanding multicultural population.

The region's major cities have a significant concentration of restaurants, cafes, catering services, and institutional food suppliers, which results in year-round high commercial black pepper consumption volumes. The region's access to reasonably cost international pepper supply is strengthened by the existence of significant port facilities and well-established trade corridors that promote agricultural commodity imports, solidifying its dominant market position. Furthermore, the region's urban centers are home to a concentration of health-conscious and culinarily inclined consumer demographics, which sustains demand for both high-end and regular black pepper products across a range of retail and foodservice channels.

Market Dynamics:

Growth Drivers:

Why is the Australia Black Pepper Market Growing?

Rising Health and Wellness Consciousness Among Consumers

Australian consumers are increasingly incorporating black pepper into their diets due to growing awareness of its health-promoting properties. Piperine, the bioactive compound in black pepper, is widely recognized for its antioxidant, anti-inflammatory, and digestive benefits, making it a preferred natural ingredient in functional food preparations and wellness-oriented dietary routines. The broader health and wellness movement sweeping across Australia is encouraging consumers to replace artificial seasonings, synthetic flavor enhancers, and processed condiments with natural spice alternatives, directly benefiting the black pepper market. Health-focused food manufacturers are actively integrating piperine into dietary supplements, functional beverages, and nutraceutical formulations to enhance nutrient bioavailability and support holistic wellness objectives. This trend aligns with the Australian government's growing emphasis on preventive healthcare, nutritional awareness campaigns, and clean-label food transparency. Retailers are responding by expanding their natural spice aisles, promoting health-benefit claims on product packaging, and curating dedicated wellness-oriented seasoning sections. The rising consumer willingness to invest in premium, health-oriented natural food ingredients continues to strengthen demand for black pepper products across retail, foodservice, and health food distribution channels throughout Australia.

Expanding Food Processing and Foodservice Industry

The sustained growth of Australia's food processing sector is generating consistent and expanding demand for black pepper as a primary seasoning ingredient across diverse manufacturing applications. Food manufacturers utilize black pepper extensively in meat processing, sauce production, snack seasoning, soup and broth formulations, and ready-to-eat meal preparations, ensuring year-round commercial procurement. The rising consumption of convenience foods, frozen meal products, and pre-packaged seasoning kits, combined with the proliferation of quick-service restaurants and fast-casual dining establishments across Australian cities, is amplifying commercial pepper procurement volumes significantly. The foodservice industry's continued expansion has further strengthened demand, with restaurants, hotels, catering companies, and institutional food providers steadily increasing their spice purchasing to accommodate growing customer volumes and diversifying menu offerings. The rapid expansion of food delivery platforms and cloud kitchen operations is creating additional demand from commercial kitchens that rely on consistent, high-quality seasoning supplies to maintain flavor standardization across distributed preparation environments. Black pepper's essential role as a foundational flavoring component in commercial food preparation, spanning cuisines from traditional Australian fare to international culinary traditions, ensures its position as an indispensable procurement item across the entire foodservice and food manufacturing value chain.

Strengthening Sustainable Sourcing and Supply Chain Transparency

The growing emphasis on sustainability and ethical sourcing within Australia's food industry is driving significant investment in transparent and traceable black pepper supply chains that meet evolving consumer and regulatory expectations. Australian importers, retailers, and food manufacturers are increasingly demanding sustainability certifications, origin traceability documentation, and fair-trade assurances from their pepper suppliers, reflecting a broader industry shift toward responsible procurement practices. This transformation is encouraging upstream suppliers in major pepper-producing nations to adopt environmentally responsible farming methods, reduce chemical inputs, implement water conservation measures, and deploy digital traceability tools that provide end-to-end visibility across the supply chain. Corporate sustainability commitments among leading food companies are reshaping procurement strategies across the spice industry, with organizations investing in farm-level programs that improve crop yield quality, strengthen farmer livelihoods, and promote regenerative agricultural practices. The integration of mobile-based traceability applications, blockchain-enabled supply chain platforms, and sustainability reporting frameworks is enhancing transparency and accountability from farm to shelf. As Australian consumers increasingly prioritize ethically sourced and environmentally responsible food products, the demand for sustainably procured black pepper with verified provenance credentials continues to strengthen across premium retail and institutional purchasing channels.

Market Restraints:

What Challenges the Australia Black Pepper Market is Facing?

Price Volatility and Global Supply Chain Disruptions

The Australia black pepper market faces significant challenges from fluctuating global pepper prices driven by weather-related crop disruptions, shifting export volumes from major producing nations, and logistical bottlenecks. Australia’s reliance on imports from Vietnam, India, and Malaysia exposes the market to international price volatility that directly affects procurement costs for food manufacturers and retailers, potentially limiting margin stability and consumer affordability.

Intense Competition from Lower-Cost Imported Alternatives

The Australian black pepper market confronts competitive pressure from lower-cost imported spice blends and substitute seasonings that compete for consumer spending. Price-sensitive consumers and commercial buyers may opt for cheaper seasoning alternatives or blended spice products, limiting premium black pepper uptake. The absence of significant domestic black pepper cultivation further intensifies import dependency, making local pricing susceptible to competitive dynamics in global sourcing markets.

Stringent Regulatory and Biosecurity Compliance Requirements

Australia’s rigorous food safety and biosecurity regulations, administered by the Department of Agriculture, Fisheries and Forestry under the Imported Food Control Order 2019, impose significant compliance burdens on black pepper importers. Products must undergo analytical testing, visual inspection, and label assessment prior to market entry. Non-compliant shipments face treatment, re-export, or destruction at the importer’s expense, increasing procurement risk and operational costs for supply chain participants.

Competitive Landscape:

The Australia black pepper market features a competitive landscape characterized by the presence of established multinational spice companies alongside growing domestic specialty brands. Market participants are focusing on product differentiation through premium offerings, organic certifications, single-origin sourcing, and innovative packaging formats. Competition is intensified by the expansion of private-label spice lines by major retailers and the entry of direct-to-consumer brands leveraging e-commerce platforms. Strategic investments in sustainable supply chains, digital distribution, and brand-building through health and wellness positioning are enabling companies to strengthen their market presence and capture evolving consumer preferences.

Australia Black Pepper Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Brazilian Black Pepper, Lampang Black Pepper, Malabar Black Pepper, Sarawak Black Pepper, Talamanca Black Pepper, Tellicherry Black Pepper, Vietnamese Black Pepper |

|

Sources Covered |

Organic, Inorganic |

|

Forms Covered |

Ground Black Pepper, Rough Cracked Black Pepper, Whole Black Pepper |

|

Distribution Channels Covered |

Offline, Online |

|

Applications Covered |

Food and Beverages, Pharmaceuticals, Personal Care, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Black Pepper Market Report

The Australia black pepper market size was valued at USD 72.80 Million in 2025.

The Australia black pepper market is expected to grow at a compound annual growth rate of 5.50% from 2026-2034 to reach USD 117.87 Million by 2034.

Vietnamese black pepper, holding the largest revenue share of 34.8%, leads the market owing to competitive pricing, reliable supply from Vietnam’s established export networks, and consistent quality preferred by Australian food processors and retailers.

Key factors driving the Australia black pepper market include rising health consciousness, expanding food processing and foodservice industries, growing multicultural cuisine adoption, increasing demand for clean-label ingredients, and strengthening sustainable sourcing practices across supply chains.

Major challenges include global price volatility affecting import costs, intense competition from lower-cost seasoning alternatives, stringent biosecurity and food safety compliance requirements, limited domestic cultivation capacity, and supply chain disruptions linked to weather-related crop yield fluctuations in key producing nations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)