Australia Building Materials Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Australia Building Materials Market Overview:

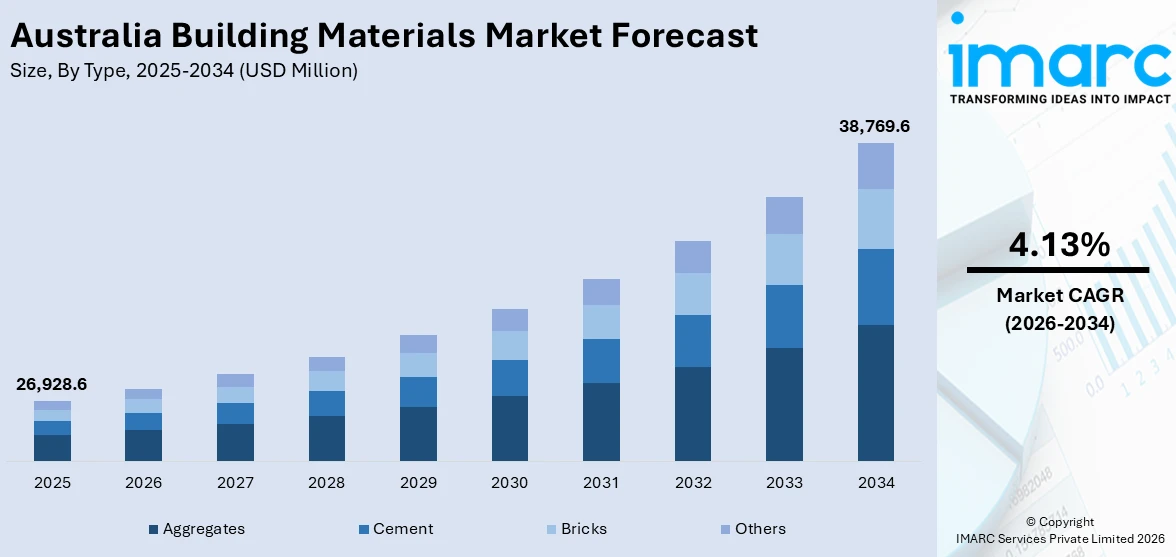

The Australia building materials market size reached USD 26,928.6 Million in 2025. Looking forward, the market is expected to reach USD 38,769.6 Million by 2034, exhibiting a growth rate (CAGR) of 4.13% during 2026-2034. The market is fueled by heightening residential and commercial construction activity, eco-friendly urban planning, and technologies in prefabrication. Amplifying energy-efficient material demand, backed by regulatory policies and digitalization, is revolutionizing material selection throughout the industry. Modular and green construction innovations continue to shape supply chain operations and project schedules. These changing trends as a whole assist in accelerating the growing Australia building materials market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 26,928.6 Million |

| Market Forecast in 2034 | USD 38,769.6 Million |

| Market Growth Rate 2026-2034 | 4.13% |

Key Trends of Australia Building Materials Market:

Adoption of Sustainable Materials in Construction

There is a noted shift towards sustainability in Australia's building materials industry, spurred on by growing awareness of the environment and supportive legislation. Developers and builders are progressively incorporating low-impact materials like recycled timber, eco-concrete, and insulation from renewable materials into mainstream development. This is also spurred by national standards calling for energy-efficient buildings and reducing carbon emissions. The focus on sustainability is generating innovation in the field of material science, encouraging manufacturers to come up with products that are more durable along with a reduced environment impact. As per the reports, in August 2024, ClearVue Technologies gained its first commercial order of more than 200 solar building envelope modules for Perth's Enex100, which was a landmark in solar façade uptake and net-zero building. Moreover, urban planners and architects are also highlighting lifecycle influence at the time of material choice, further endorsing preference for sustainable solutions in residential and commercial projects alike. This emerging demand is changing supply chains steadily, promoting transparency and traceability. Australia building materials growth is also driven by this green momentum, moving the industry toward longer-term development in support of global climate targets and sustainable urbanization initiatives.

To get more information on this market Request Sample

Demand for Prefabricated and Modular Materials

The increasing trend for prefabricated and modular construction is exercising substantial impact on material choice in Australia's building industry. For instance, in May 2024, Luyten 3D finished the first 3D-printed two-storey home in the Southern Hemisphere. The project utilized the Platypus X12 printer, which took only 32 hours, improving construction efficiency and sustainability. Furthermore, these new age construction techniques require precision-engineered building materials with precise specifications to ensure easy transportation and assembly on site. The move towards off-site production has seen more application of lightweight steel framing, modular concrete panels, and pre-assembled insulation systems. Not only do these materials improve construction speed, but they also reduce waste and decrease overall project costs. The cost savings and efficiency that come with prefabricated techniques are particularly applicable in high-rise residential and institutional projects in Australia's urban and regional zones. This shift is part of the larger movement towards industrialized construction, with consistency and quality control being of utmost importance. Australia building materials growth is seeing the advantage of this change as demand for material appropriate to modular use continues to grow and redefine traditional supply chains.

Digital Integration in Material Selection

Digital transformation is transforming the way construction materials are procured, assessed, and applied in Australia. Employment of digital solutions like Building Information Modelling (BIM), material libraries, and artificial intelligence-based design platforms enables stakeholders to make better-informed decisions concerning performance, cost-effectiveness, and sustainability. These technologies support real-time interaction among architects, engineers, and suppliers, optimizing the whole process of material selection and specification. This convergence is also fueling demand for intelligent materials that will interface with digital systems—such as self-monitoring concrete or thermochromic glass that can react to heat. The shift to digital is improving construction productivity and minimizing lifecycle costs, as it is consonant with national infrastructure aspirations. Australia building materials growth is being supported by uptake of these technologies, putting the industry in place to address future construction requirements with flexibility, openness, and creativity.

Growth Drivers of Australia Building Materials Market:

Government Infrastructure Investment and Urban Development Programs

The Australian government's heavy investment in infrastructure development is a key driver of the market demand. Federal and state governments have invested sizeable budgets in transport networks, such as rail networks, freeways, and inner-city transit corridors, generating consistent demand for cement, aggregates, and concrete. Large-scale projects like the Western Sydney Airport development, Melbourne Metro Tunnel, and Queensland's Olympic infrastructure buildup call for gigantic volumes of building materials over lengthy periods. These massive public works projects have ascertainable demand patterns, thus allowing producers to efficiently increase their capacity levels. Besides, there are such massive urban renewal programs going on in the major cities that are driving residential and commercial development, amplifying material consumption. Residential development toward government housing initiatives is driving heightened demand across the board of construction material categories. These policy measures are fostering steady market growth while stimulating private sector investment in manufacturing capacity and supply chain infrastructure.

Population Growth and Urbanization Trends

Australia's rapid population expansion, driven by immigration and natural growth, is fundamentally reshaping housing and infrastructure requirements. The country has witnessed a sharp rise in overseas migration in recent years, leading to severe housing shortages across major cities. This growing population pressure is driving strong demand for residential construction materials such as bricks, timber framing, plasterboard, and roofing products. Urban densification policies in Sydney, Melbourne, and Brisbane are encouraging high-rise apartment development, which requires specialized materials such as structural steel, high-performance concrete, and curtain wall systems. Beyond residential needs, population growth is driving expansion of commercial infrastructure including retail centers, office buildings, healthcare facilities, and educational institutions. Each of these sectors demands distinct material specifications and volumes. The sustained nature of demographic growth ensures that Australia building materials market analysis projects continued expansion well into the next decade, making it an attractive sector for long-term investment and strategic planning.

Energy Efficiency Mandates and Green Building Regulations

Increasingly stringent energy efficiency standards and environmental regulations are compelling the construction industry to adopt advanced building materials, thereby driving market growth. These regulatory frameworks mandate the use of high-performance insulation materials, energy-efficient glazing systems, and low-embodied-carbon alternatives to traditional products. Compliance requirements are pushing developers toward premium materials that meet certification standards from the Green Building Council of Australia and other rating systems. Furthermore, federal incentives for energy-efficient construction are making advanced materials more economically viable for mainstream projects. The transition toward net-zero buildings is creating new market segments for innovative products such as phase-change materials, reflective roofing systems, and thermally efficient concrete mixtures. This regulatory push is not merely constraining material choices but actively expanding the market by creating demand for higher-value, technically sophisticated products that command premium pricing.

Opportunities of Australia Building Materials Market:

Expansion into Circular Economy and Recycled Materials

The emerging circular economy presents substantial opportunities for innovation and market expansion within Australia's building materials sector. Increasing environmental consciousness and regulatory pressure to reduce construction waste are driving demand for recycled aggregates, reclaimed timber, and reprocessed concrete. Companies that develop efficient collection, processing, and certification systems for recycled materials can capture growing market share while contributing to sustainability goals. Advanced recycling technologies are enabling the production of high-quality materials from demolition waste, reducing dependence on virgin resource extraction. Organizations investing in closed-loop systems that transform construction debris into specification-grade products are positioning themselves advantageously for future growth. Additionally, government procurement policies increasingly favor suppliers demonstrating circular economy principles, creating preferential access to lucrative public sector contracts. The development of standardized testing and quality assurance protocols for recycled materials will further legitimize this market segment. Companies pioneering these innovations can establish competitive advantages through intellectual property, specialized processing capabilities, and strong sustainability credentials that resonate with environmentally conscious clients.

Smart Materials and Technology-Integrated Products

The convergence of construction and technology is creating unprecedented opportunities for manufacturers of intelligent building materials, which is further driving the Australia building materials market demand. Products incorporating sensors, data analytics, and responsive properties represent a high-growth market segment with significant profit potential. Self-healing concrete that autonomously repairs micro-cracks, thermochromic glass that adjusts transparency based on temperature, and materials embedded with IoT sensors for structural health monitoring are transitioning from experimental applications to commercial viability. These advanced materials command premium pricing while offering clients measurable value through reduced maintenance costs and enhanced building performance. The integration of materials with Building Information Modeling (BIM) systems enables real-time tracking of material specifications, installation quality, and lifecycle performance. Manufacturers developing digital twins of their products and providing data-rich specifications compatible with digital design platforms will gain preferential specification by architects and engineers. As smart city initiatives expand across Australian metropolitan areas, demand for technology-integrated construction materials will accelerate, offering early movers substantial market opportunities and the potential to establish industry standards.

Export Potential to Asia-Pacific Construction Markets

Australia's geographic proximity to rapidly developing Asia-Pacific economies presents significant export opportunities for building materials manufacturers. Countries throughout Southeast Asia and the Pacific Islands are experiencing construction booms driven by urbanization, infrastructure investment, and economic development. Australian companies can leverage their reputation for quality, regulatory compliance, and technical expertise to capture market share in these growing economies. Premium products such as engineered timber systems, high-performance concrete additives, and sustainable building materials are particularly well-positioned for export. Establishing partnerships with regional developers and participating in major infrastructure projects across the Asia-Pacific can create substantial revenue streams beyond domestic markets. Trade agreements and diplomatic relationships facilitate market access while Australia's stable business environment and advanced manufacturing capabilities provide competitive advantages. Companies investing in regional distribution networks, localized technical support, and adaptation of products to tropical climates and seismic requirements can establish strong positions in these emerging markets. The export opportunity not only diversifies revenue sources but also provides scale economies that enhance competitiveness in the domestic Australian market.

Challenges of Australia Building Materials Market:

Skilled Labor Shortages and Workforce Constraints

The Australian building materials industry faces persistent challenges related to skilled labor shortages that constrain production capacity and operational efficiency. Manufacturing facilities require specialized technicians, quality control experts, and equipment operators with specific expertise in materials processing. An aging workforce combined with insufficient vocational training pipelines has created critical skill gaps across the sector. This scarcity drives wage inflation, increasing production costs and compressing margins for materials manufacturers. Extended project timelines resulting from labor constraints reduce throughput and delay revenue recognition. Companies struggle to maintain consistent quality standards when forced to utilize less experienced personnel or operate facilities below optimal capacity. The challenge is particularly acute in regional areas where attracting and retaining skilled workers proves difficult. Immigration restrictions and competition from other industries for technical talent further exacerbate the problem. Addressing this challenge requires substantial investment in training programs, automation technologies, and competitive compensation packages that strain financial resources.

Supply Chain Volatility and Input Cost Fluctuations

Building materials manufacturers contend with significant supply chain disruptions and volatile input costs that complicate planning and margin management. Energy costs, particularly for energy-intensive products like cement, bricks, and glass, fluctuate substantially based on natural gas prices and electricity rates. Transportation expenses for bulky, heavy materials represent a major cost component vulnerable to fuel price variations and logistics constraints. International supply chain disruptions affect the availability and pricing of specialized components, additives, and equipment essential for production. Currency fluctuations impact the cost of imported inputs and machinery, creating unpredictability in financial planning. The concentration of certain raw material sources creates supply vulnerabilities, as disruptions in key quarries or mines can constrain availability of essential aggregates and minerals. Extended lead times for equipment maintenance parts and specialized consumables can force production stoppages with significant financial consequences. Manufacturers operating on fixed-price contracts face pressure when input costs rise unexpectedly, potentially leading to project losses. The challenge of supply chain management is compounded by the need for substantial inventory buffers that tie up working capital while protecting against disruptions.

Environmental Compliance and Decarbonization Pressures

Escalating environmental regulations and decarbonization mandates present substantial challenges for traditional building materials manufacturers. The production of cement, the most carbon-intensive construction material, faces intense scrutiny and regulatory pressure to reduce emissions. Achieving meaningful carbon reduction requires substantial capital investment in alternative fuel systems, carbon capture technologies, and process modifications. Transitioning to low-carbon production methods often increases operating costs and reduces competitiveness against imports from jurisdictions with less stringent environmental standards. Quarrying operations face increasingly stringent approvals processes, community opposition, and restrictions on operating hours and blast schedules that limit production flexibility. Water usage regulations in drought-prone regions constrain operations for concrete and other materials requiring significant water inputs. The complexity of environmental compliance across multiple jurisdictions creates administrative burdens and requires specialized expertise. Companies must balance investment in sustainability initiatives against immediate profitability pressures and shareholder return expectations. The risk of stranded assets as regulations tighten creates uncertainty around long-term capital investments in conventional production facilities. Small and medium-sized manufacturers particularly struggle with the technical and financial resources required to meet evolving environmental standards while remaining commercially viable in competitive markets.

Australia Building Materials Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type and application.

Type Insights:

- Aggregates

- Cement

- Bricks

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes aggregates, cement, bricks, and others.

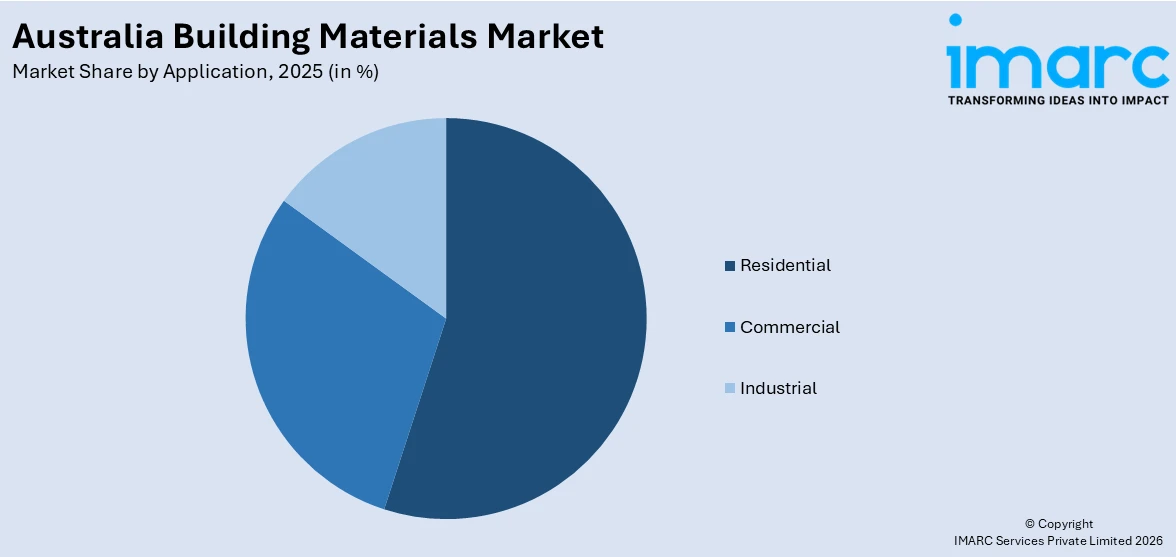

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Industrial

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes residential, commercial, and industrial.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Building Materials Market News:

- In October 2024, RMIT University's coffee concrete, the world's first such innovation in building materials, was first unveiled in a significant infrastructure development on McGregor Road, Pakenham, Victoria. The green concrete, blended with spent coffee grounds' biochar, substitutes river sand traditionally used, providing both environmental advantages and increasing sustainability in Australia's building materials industry.

- In August 2024, the University of Technology Sydney (UTS), together with Boral, the SmartCrete Cooperative Research Centre (CRC), Calix, and Transport for NSW, started a two-year study to create low-carbon concrete with the use of Australian calcined clay. The project aims to lower CO2 emissions and provide a sustainable substitute for conventional cement in Australia's building materials industry. The project caters to an increasing industry need for green construction solutions.

Australia Building Materials Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Aggregates, Cement, Bricks, Others |

| Applications Covered | Residential, Commercial, Industrial |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia building materials market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia building materials market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia building materials industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Building Materials Market Report

The building materials market in Australia was valued at USD 26,928.6 Million in 2025.

The Australia building materials market is projected to exhibit a CAGR of 4.13% during 2026-2034.

The Australia building materials market is projected to reach a value of USD 38,769.6 Million by 2034.

The Australia building materials market is witnessing trends such as rising adoption of sustainable and energy-efficient materials, increased use of prefabrication, digital construction technologies, circular economy practices, and growing demand driven by urban development and housing projects.

The Australia building materials market is driven by rapid infrastructure expansion, government investments in transport and housing, reconstruction activities following natural disasters, rising renovation projects, favorable lending policies, and increasing demand from commercial real estate and industrial construction sectors across urban and regional areas.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)