Australia Catalyst Market Size, Share, Trends and Forecast by Type, Process, Raw Material, Application, and Region, 2026-2034

Australia Catalyst Market Summary:

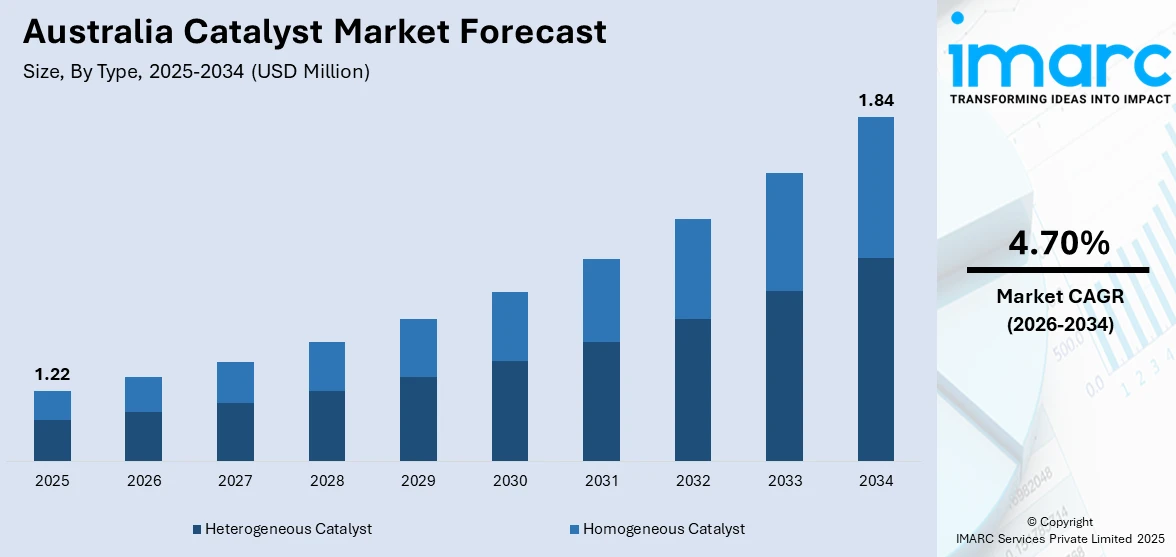

The Australia catalyst market size was valued at USD 1.22 Million in 2025 and is projected to reach USD 1.84 Million by 2034, growing at a compound annual growth rate of 4.70% from 2026-2034. The Australian catalyst market is experiencing robust growth driven by increasing demand for sustainable emission reduction technologies across key industrial sectors including manufacturing, mining, and petroleum refining. The nation's commitment to achieving net-zero emissions by 2050, coupled with stringent environmental regulations such as the New Vehicle Efficiency Standard and Euro 6d emissions standards, is accelerating the adoption of advanced catalyst solutions. The expanding petroleum refining sector and the emergence of sustainable aviation fuel production initiatives are further contributing to the growing Australia catalyst market share.

To get more information on this market Request Sample

Key Takeaways and Insights:

- By Type: Heterogeneous catalyst dominated the market with a share of 56% in 2025, owing to its widespread application in petroleum refining, chemical synthesis, and environmental catalysis, where its ease of separation and recovery from reaction mixtures provides significant operational advantages.

- By Process: Regeneration leads the market with a share of 40% in 2025, driven by the cost-effectiveness of restoring catalyst activity through thermal, chemical, and oxidative treatments, enabling extended operational lifecycles and reduced procurement expenses for industrial operators.

- By Raw Material: Chemical compounds represent the largest segment with a market share of 35% in 2025, attributable to their versatility and adaptability in catalyzing diverse chemical reactions across petrochemical, pharmaceutical, and environmental protection applications.

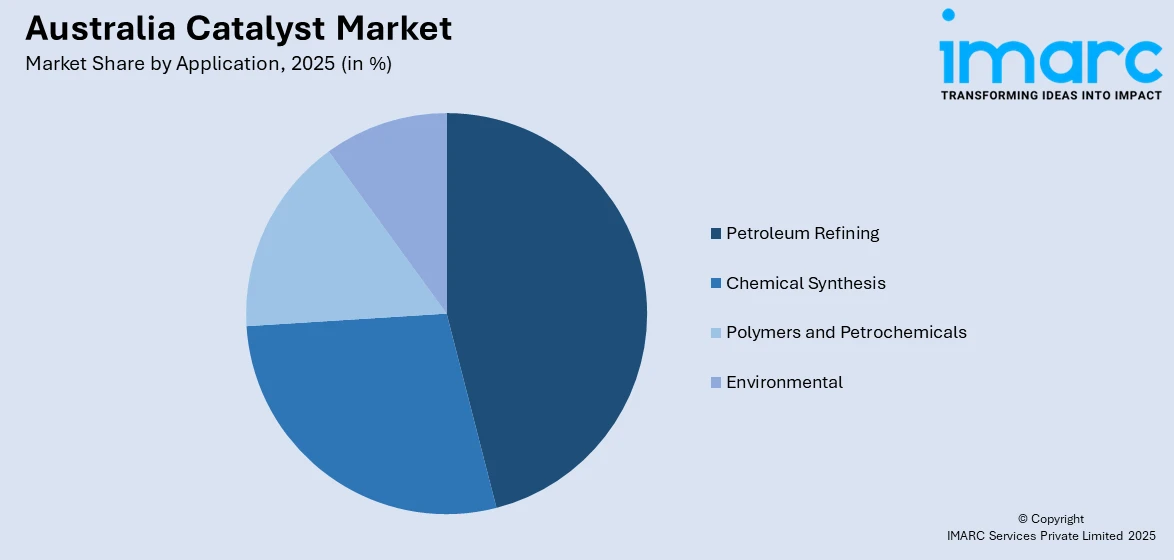

- By Application: Petroleum refining leads the market with a share of 29% in 2025, supported by the essential role of catalysts in fluid catalytic cracking, hydrocracking, and hydrotreating processes that convert crude oil into high-value transportation fuels.

- By Region: Australia Capital Territory & New South Wales dominate with 31% market share in 2025, attributed to the concentration of industrial manufacturing facilities, research institutions, and major refineries in the metropolitan Sydney region and surrounding industrial corridors.

- Key Players: The Australian catalyst market exhibits a moderately competitive landscape characterized by the presence of global multinational corporations alongside specialized regional suppliers. Major international players maintain significant market positions through established distribution networks, advanced research capabilities, and comprehensive product portfolios catering to diverse industrial applications.

Australia's catalyst market is undergoing significant transformation as industries align with the nation's ambitious sustainability targets and environmental compliance requirements. The market is witnessing substantial investments in emission control technologies, particularly in the mining and chemical manufacturing sectors where catalytic solutions play a critical role in reducing greenhouse gas emissions. The petroleum refining segment continues to be a major consumer of catalysts, utilizing advanced formulations for fluid catalytic cracking and hydrotreating processes to meet stringent fuel quality standards. For instance, in April 2024, thyssenkrupp Uhde completed a USD 20 million EnviNOx project at Dyno Nobel's nitric acid plant in Moranbah, Australia, deploying BASF-manufactured catalysts that reduced N₂O emissions to below 5 ppm, demonstrating the effectiveness of advanced catalyst technologies in industrial emission abatement. The growing focus on sustainable aviation fuel production and hydrogen economy development is creating new avenues for catalyst applications, positioning Australia as an emerging hub for clean energy catalyst innovation.

Australia Catalyst Market Trends:

Catalyst Innovation Drives Industrial Emission Control

Australia's industrial sector is increasingly adopting advanced catalyst technologies to meet stringent emission reduction targets and align with national decarbonization objectives. The deployment of specialized catalytic systems in nitric acid production, ammonia manufacturing, and chemical processing facilities is accelerating as companies seek to minimize their environmental footprint. The successful implementation of EnviNOx technology at the Moranbah facility, which achieved N₂O emission reductions exceeding 99%, exemplifies the transformative potential of catalyst innovation in industrial emission control. This trend is expected to intensify as regulatory frameworks become more stringent and industries face increasing pressure to demonstrate environmental responsibility.

Catalysts for Sustainable Mining Practices

The Australian mining industry is emerging as a significant driver of catalyst market growth through its adoption of catalytic oxidation technologies for methane abatement. With methane possessing a global warming potential 28 times greater than carbon dioxide, mining companies are increasingly investing in catalyst-based solutions to address ventilation air methane emissions from underground coal operations. For instance, in January 2026, Mining3 and Low Emission Technology Australia (LETA) announced the successful conclusion of Phase 1 of the CATCH4 program and the commencement of Phase 2, marking a significant advancement in the initiative’s ongoing development and implementation efforts. This initiative represents a critical step toward commercializing catalytic solutions that can operate at lower temperatures and methane concentrations than traditional thermal oxidation methods.

Growth of Sustainable Aviation Fuel Catalyst Applications

Australia’s growing sustainable aviation fuel sector is driving demand for advanced catalyst technologies that convert biomass and agricultural residues into low-carbon liquid fuels. Hydrothermal liquefaction, using specialized catalyst systems, is increasingly adopted to transform organic feedstocks into biocrude as aviation stakeholders seek alternatives to conventional jet fuel. Ongoing investments in catalyst-based biorefinery projects are supporting the development of scalable production processes, enabling more efficient, environmentally friendly fuel solutions and promoting the broader adoption of sustainable aviation technologies across the country.

Market Outlook 2026-2034:

The Australia catalyst market is set for steady growth, supported by a combination of regulatory requirements, sustainability efforts, and technological innovation. Increasing emphasis on reducing vehicle emissions is boosting demand for automotive catalysts in emission control systems. Simultaneously, the push toward renewable energy and clean fuel technologies is driving investment in catalysts for hydrogen production and related applications. These factors, alongside ongoing advancements in catalyst efficiency and performance, are creating a favorable environment for the adoption and development of catalytic solutions across both industrial and automotive sectors. The market generated a revenue of USD 1.22 Million in 2025 and is projected to reach a revenue of USD 1.84 Million by 2034, growing at a compound annual growth rate of 4.70% from 2026-2034.

Australia Catalyst Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Heterogeneous Catalyst |

56% |

|

Process |

Regeneration |

40% |

|

Raw Material |

Chemical Compounds |

35% |

|

Application |

Petroleum Refining |

29% |

|

Region |

Australia Capital Territory & New South Wales |

31% |

Type Insights:

- Heterogeneous Catalyst

- Homogeneous Catalyst

Heterogeneous catalyst dominates with a market share of 56% of the total Australia catalyst market in 2025.

Heterogeneous catalysts represent the cornerstone of Australia's industrial catalysis landscape, characterized by their presence in a different phase than the reactants, typically as solid materials interacting with gaseous or liquid substrates. These catalysts are extensively deployed across petroleum refining operations, chemical manufacturing processes, and environmental applications due to their superior operational characteristics including ease of separation, straightforward recovery, and minimal purification requirements. The segment's dominance is reinforced by the growing demand for zeolite-based catalysts in fluid catalytic cracking processes, which convert heavy petroleum fractions into valuable transportation fuels while meeting increasingly stringent sulfur content regulations.

The heterogeneous catalyst segment is witnessing significant innovation through the development of hierarchically porous materials that combine the shape selectivity of microporous zeolites with enhanced mass transfer characteristics of mesoporous structures. Research institutions, including the University of Sydney's Laboratory for Catalysis Engineering, are advancing metal-zeolite hybrid materials that offer unprecedented selectivity and stability for challenging chemical transformations. The industrial adoption of these advanced heterogeneous catalysts is being driven by the need for more efficient processes that minimize energy consumption, reduce waste generation, and improve overall process economics across Australia's chemical and refining sectors.

Process Insights:

- Recycling

- Regeneration

- Rejuvenation

Regeneration leads the market with a 40% share of the total Australia catalyst market in 2025.

Catalyst regeneration has emerged as the dominant process segment within Australia's catalyst market, driven by the compelling economic advantages of restoring spent catalysts to near-original activity levels rather than procuring new materials. The regeneration process encompasses various techniques including thermal treatment, chemical washing, oxidative regeneration, and controlled combustion of coke deposits that accumulate during catalyst operation. Petroleum refineries represent the largest consumers of regeneration services, as fluid catalytic cracking units continuously circulate catalyst between reaction and regeneration zones to maintain optimal cracking performance and accommodate the high throughput demands of modern refining operations.

The regeneration segment's growth trajectory is further supported by the sustainability imperative driving Australian industries toward circular economy principles. Extended catalyst lifecycles achieved through effective regeneration protocols significantly reduce the environmental footprint associated with catalyst production and disposal while generating substantial cost savings for industrial operators. The development of advanced regeneration technologies capable of addressing multiple deactivation mechanisms, including metal poisoning, structural damage, and pore blockage, is expanding the scope of catalysts that can be successfully regenerated and returned to productive service.

Raw Material Insights:

- Chemical Compounds

- Peroxides

- Acids

- Amines

- Others

- Metals

- Precious Metals

- Base Metals

- Zeolites

- Others

Chemical compounds dominates with a market share of 35% of the total Australia catalyst market in 2025.

Chemical compound-based catalysts command the largest share of Australia's catalyst raw material market, attributed to their exceptional versatility in facilitating diverse chemical transformations across multiple industrial sectors. These catalysts, which include peroxides for oxidation reactions, acids for isomerization and alkylation processes, and amines for various organic synthesis applications, offer the flexibility to be tailored for specific reaction requirements through controlled synthesis and formulation procedures. The segment benefits from the established supply chains for chemical compound precursors and the relatively lower costs compared to precious metal-based alternatives.

The demand for chemical compound catalysts is being augmented by their expanding applications in environmental protection, including volatile organic compound oxidation, selective catalytic reduction of nitrogen oxides, and industrial wastewater treatment. The development of iron-loaded zeolite catalysts, which combine the structural advantages of zeolitic materials with the catalytic activity of transition metal compounds, represents a significant advancement in this segment. These hybrid materials are finding application in the abatement of nitrous oxide emissions from nitric acid production facilities, where they achieve removal efficiencies exceeding 99% while maintaining long operational lifetimes.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Chemical Synthesis

- Chemical Catalysts

- Adsorbents

- Syngas Production

- Others

- Petroleum Refining

- Fluid Catalytic Cracking (FCC)

- Alkylation

- Hydrotreating

- Catalytic Reforming

- Purification

- Bed Grading

- Others

- Polymers and Petrochemicals

- Ziegler Natta

- Reaction Initiator

- Chromium

- Urethane

- Solid Phosphorous Acid Catalyst

- Others

- Environmental

- Light-duty Vehicles

- Motorcycles

- Heavy-duty Vehicles

- Others

Petroleum refining represents the highest revenue with a 29% share of the total Australia catalyst market in 2025.

Petroleum refining represents the largest application segment for catalysts in Australia, driven by the critical role of catalytic processes in converting crude oil into high-value transportation fuels and petrochemical feedstocks. Fluid catalytic cracking remains the predominant catalyst-consuming process, utilizing zeolite-based formulations to convert heavy gas oil fractions into gasoline and lighter products while maximizing yields of valuable olefinic gases. Australian refineries are increasingly adopting advanced catalyst technologies that enhance selectivity toward premium products while minimizing coke formation and environmental emissions.

The petroleum refining segment is experiencing significant evolution as refineries adapt to changing fuel specifications and market demands. The introduction of Euro 6d emission standards in Australia from December 2024 is driving increased adoption of hydrotreating catalysts capable of producing ultra-low sulfur fuels. For instance, in August 2024, BASF launched Fourtiva, an advanced fluidized catalytic cracking catalyst incorporating Multiple Frameworks Topology and Advanced Innovative Matrix technologies to maximize butylene yields while improving naphtha octane, demonstrating the ongoing innovation in refining catalyst formulations. These developments are enabling Australian refineries to maintain competitiveness while meeting increasingly stringent environmental performance requirements.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales dominate the market with a 31% share of the total Australia catalyst market in 2025.

The catalyst market in the Australian Capital Territory is driven primarily by environmental regulations and government-led initiatives aimed at reducing industrial emissions and promoting sustainable technologies. Demand is increasing for catalysts used in research institutions, pilot projects, and small-scale industrial applications focused on air quality improvement and energy efficiency. Investments in innovation, public-sector projects, and collaborations with technology providers are supporting the development and deployment of advanced catalytic solutions, positioning the ACT as a hub for environmentally focused catalyst applications and research-driven market growth.

In New South Wales, the catalyst market is fueled by the state’s large industrial base, including mining, chemical production, and renewable energy sectors. Adoption of catalytic technologies for methane abatement in mining and emission reduction in chemical plants is a key driver. Additionally, initiatives supporting bio-refinery projects, sustainable fuel production, and industrial decarbonization are increasing demand for advanced catalysts. Strong R&D infrastructure, government incentives, and growing environmental awareness among industries further accelerate the market, fostering innovation and large-scale deployment of catalytic solutions across NSW.

Market Dynamics:

Growth Drivers:

Why is the Australia Catalyst Market Growing?

Stringent Environmental Regulations Driving Catalyst Adoption

Australia's increasingly stringent environmental regulatory framework is serving as a primary catalyst for market growth, compelling industrial operators to invest in advanced catalytic technologies for emission control and pollution abatement. The implementation of the New Vehicle Efficiency Standard from January 2025, which mandates progressively lower CO₂ emissions from new light vehicles, is driving substantial demand for automotive catalytic converters and emission control systems. The Euro 6d emissions standards, effective from December 2024, require vehicles to meet real-world driving emissions criteria that necessitate sophisticated three-way catalytic converters and selective catalytic reduction systems. These regulatory developments are creating sustained demand for platinum group metals, zeolite-based catalysts, and specialized formulations capable of meeting increasingly challenging performance specifications while maintaining durability under demanding operational conditions.

Expansion of Petroleum Refining and Petrochemical Industries

The continued operation and modernization of Australia's petroleum refining infrastructure represents a significant driver of catalyst market growth, as refineries seek to maximize operational efficiency, product quality, and environmental performance. Fluid catalytic cracking units require continuous catalyst addition and sophisticated regeneration systems to maintain optimal conversion rates and product selectivity, generating sustained demand for zeolite-based cracking catalysts and associated additives. The hydrotreating segment is experiencing particular growth as refiners upgrade their desulfurization capabilities to produce ultra-low sulfur diesel and gasoline that comply with evolving fuel quality standards. Additionally, the petrochemical sector's demand for catalysts in polymer production, particularly Ziegler-Natta catalysts for polyethylene and polypropylene manufacturing, contributes to the overall market expansion as Australia's plastics and packaging industries continue to grow.

Emerging Clean Energy and Sustainability Initiatives

Australia's ambitious clean energy transition is creating transformative growth opportunities for the catalyst market across multiple emerging applications. The National Hydrogen Strategy 2024, targeting 15 million metric tons of renewable hydrogen production by 2050, is driving substantial investments in electrolyzer catalyst technologies and ammonia synthesis catalysts that will underpin the nation's hydrogen export ambitions. The Future Made in Australia Innovation Fund, with AUD 1.7 billion allocated to priority industries, specifically supports hydrogen electrolyzer manufacturing and low-carbon liquid fuel production, where catalysts play an essential enabling role. The sustainable aviation fuel sector represents another high-growth opportunity, with projects such as Licella's Queensland biorefinery utilizing proprietary catalyst technology to convert agricultural residues into renewable jet fuel. These emerging applications are diversifying the catalyst market beyond traditional industrial uses and positioning Australia as a leader in clean energy catalyst innovation.

Market Restraints:

What Challenges the Australia Catalyst Market is Facing?

High Costs of Advanced Catalyst Materials

The elevated costs associated with advanced catalyst formulations, particularly those incorporating precious metals such as platinum, palladium, and rhodium, present a significant barrier to market expansion. Price volatility in precious metal markets introduces uncertainty into catalyst procurement budgets and can delay investment decisions for new installations or upgrades. Smaller industrial operators may defer catalyst replacement or accept suboptimal performance rather than incur the capital expenditure required for state-of-the-art catalytic systems.

Technical Challenges in Large-Scale Catalyst Deployment

The transition of promising catalyst technologies from laboratory and pilot scales to full commercial deployment presents persistent technical and operational challenges. Many emerging catalyst applications, including methane abatement in mining operations and biomass conversion for sustainable fuels, require extensive validation under real-world conditions before industrial adoption can proceed. Safety considerations, particularly for catalytic systems operating in potentially hazardous environments, necessitate rigorous risk assessment and regulatory approval processes that extend project timelines.

Supply Chain Vulnerabilities and Geopolitical Dependencies

Australia's catalyst market remains vulnerable to supply chain disruptions and geopolitical factors affecting the availability and pricing of critical raw materials. The concentration of precious metal mining and processing in a limited number of countries creates dependency risks that can impact catalyst availability and costs. Additionally, the reliance on imported catalyst formulations and manufacturing expertise for specialized applications limits domestic industry autonomy and exposes the market to international supply chain fluctuations.

Competitive Landscape:

The Australian catalyst market exhibits a competitive landscape characterized by the dominance of multinational corporations with established global research and manufacturing capabilities, complemented by specialized regional suppliers and emerging clean technology enterprises. Major international players maintain significant market positions through comprehensive product portfolios spanning petroleum refining, chemical synthesis, environmental, and automotive applications. These companies leverage their technological leadership and established distribution networks to serve Australia's industrial customers while continuously investing in research and development to address evolving performance and sustainability requirements. The market is witnessing increasing collaboration between industrial end-users and technology providers to develop customized catalyst solutions that address specific operational challenges and regulatory compliance needs. Strategic partnerships between global catalyst manufacturers and Australian research institutions are accelerating the commercialization of innovative materials and processes, particularly in emerging applications such as hydrogen production, carbon capture, and sustainable fuel synthesis.

Recent Developments:

- March 2025: Mining3 and Low Emission Technology Australia partnered with hte GmbH to advance catalyst-based methane abatement through the CATCH4 project. Through the evaluation of advanced catalysts for mining emissions, this initiative has reinforced Australia’s catalyst sector and demonstrated significant progress in implementing catalytic technologies for sustainable mining practices and effective emission mitigation.

- March 2025: Australia advanced its catalyst market with Licella's AUD 8 million-funded Project Swift, utilizing patented Cat-HTR catalyst technology to convert sugarcane waste into sustainable aviation fuel. This development boosted domestic catalyst innovation, enhancing Australia's bio-refinery capabilities and strengthening its position in sustainable fuel production.

Australia Catalyst Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Heterogeneous Catalyst, Homogeneous Catalyst |

| Processes Covered | Recycling, Regeneration, Rejuvenation |

| Raw Materials Covered |

|

| Applications Covered |

|

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Catalyst Market Report

The Australia catalyst market size was valued at USD 1.22 Million in 2025.

The Australia catalyst market is expected to grow at a compound annual growth rate of 4.70% from 2026-2034 to reach USD 1.84 Million by 2034.

Heterogeneous catalyst dominated the Australia catalyst market with a 56% share in 2025, driven by its extensive application in petroleum refining, chemical synthesis, and environmental catalysis where its ease of separation and recovery provides significant operational advantages.

Key factors driving the Australia catalyst market include stringent environmental regulations mandating emission reductions, expansion of petroleum refining operations requiring advanced catalytic processes, and emerging clean energy initiatives driving demand for catalysts in hydrogen production and sustainable aviation fuel development.

Major challenges include high costs of advanced catalyst materials incorporating precious metals, technical difficulties in scaling emerging catalyst technologies for commercial deployment, supply chain vulnerabilities affecting the availability of critical raw materials, and geopolitical dependencies on international suppliers for specialized catalyst formulations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)