Australia Commercial Real Estate Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

Australia Commercial Real Estate Market Size, Share, Trends & Forecast (2026-2034)

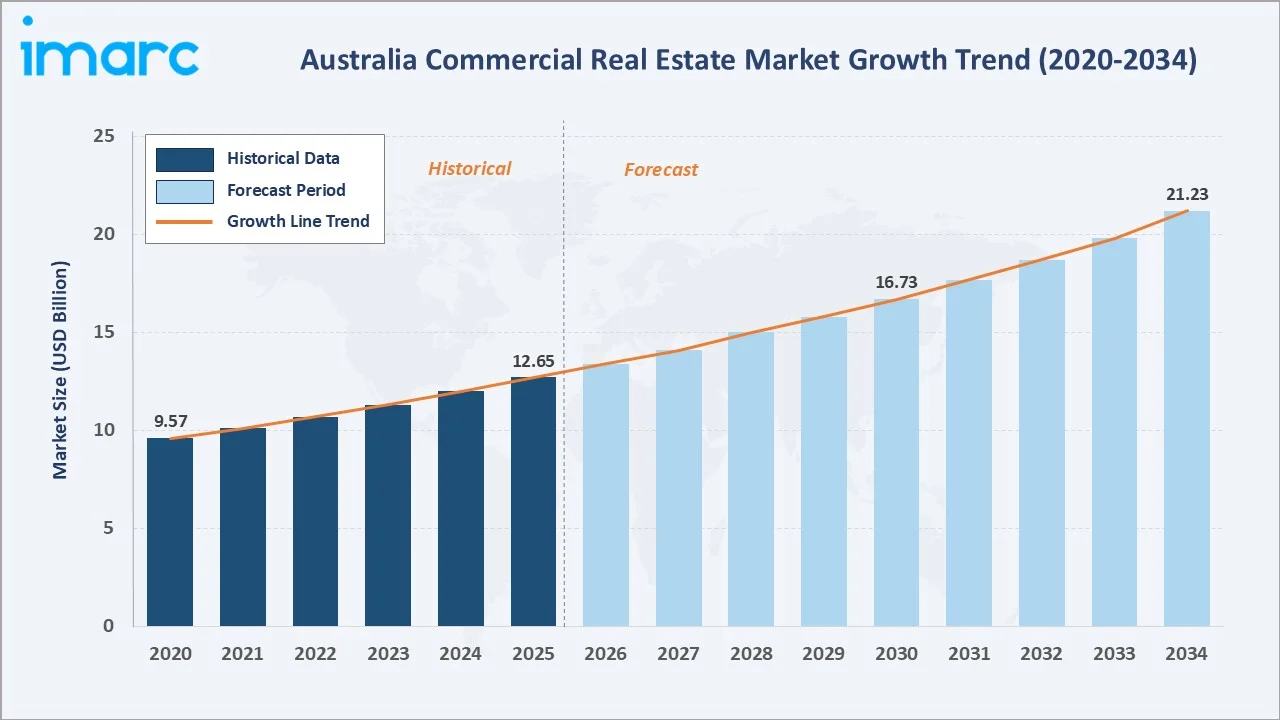

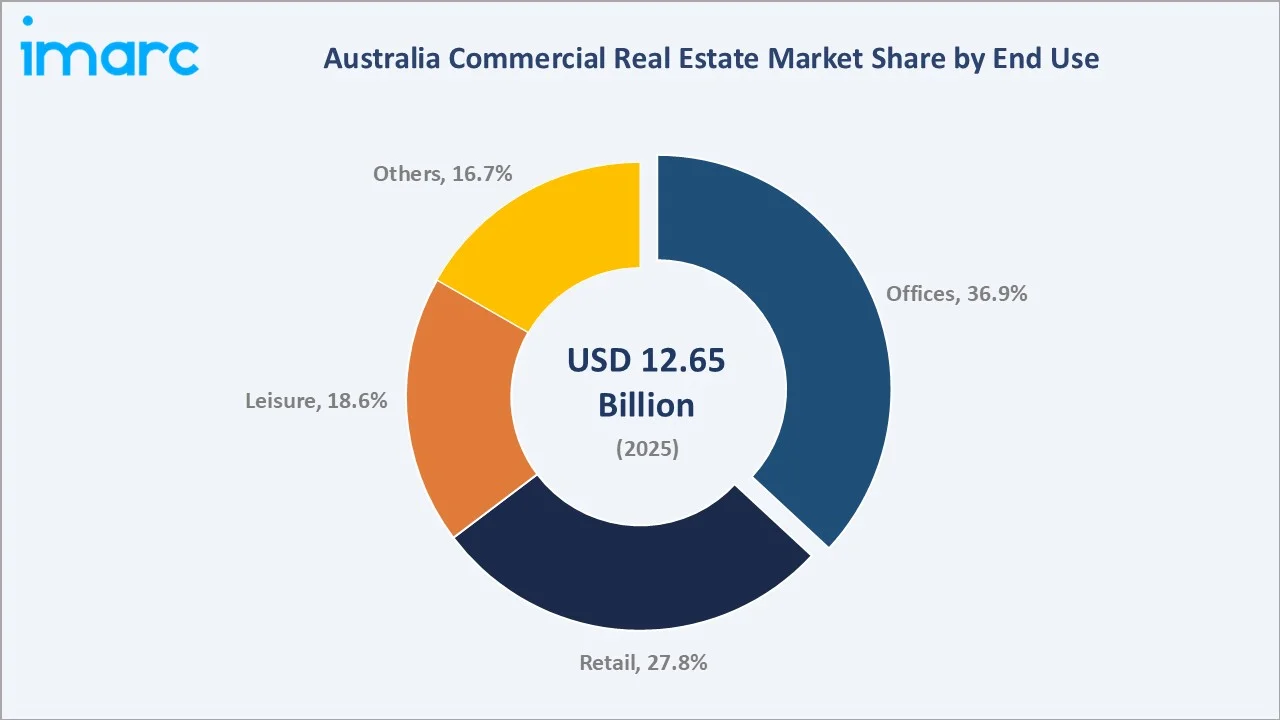

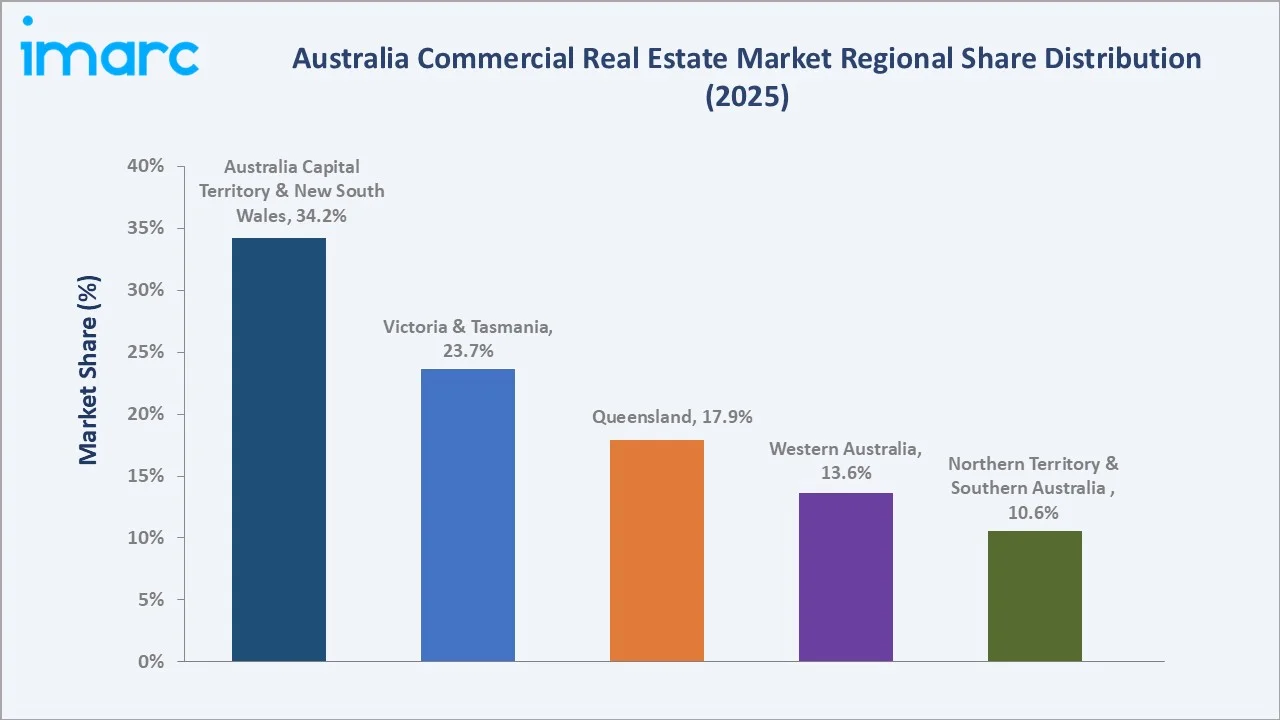

The Australia commercial real estate market reached USD 12.65 Billion in 2025 and is projected to reach USD 21.23 Billion by 2034, growing at a CAGR of 5.74% during 2026-2034. The market is driven by strong demand for modern office spaces, with 62% of businesses in Australia redesigning their offices, industrial and logistics assets, retail redevelopment, and mixed-use developments. Rental type dominates at 58.6%. Offices lead end use at 36.9%. Australia Capital Territory & New South Wales command 34.2% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 12.65 Billion |

|

Forecast Market Size (2034) |

USD 21.23 Billion |

|

CAGR (2026-2034) |

5.74% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Type |

Rental (58.6%, 2025) |

|

Dominant End Use |

Offices (36.9%, 2025) |

|

Leading Region |

Australia Capital Territory & New South Wales (34.2%, 2025) |

The market expanded from USD 9.57 Billion in 2020 to USD 12.65 Billion in 2025, anchored at USD 16.73 Billion in 2030, and forecast to reach USD 21.23 Billion by 2034. COVID-19 created Australia's most significant commercial real estate market disruption since the early 1990s recession. The market's recovery from 2021-2025 has been structurally differentiated. Prime-grade office space in greener buildings recovered faster and stronger than secondary stock, experiential and convenience retail recovered while fashion-only retail continued struggling, and leisure commercial real estate rebounded strongly on pent-up travel and experience demand.

To get more information on this market, Request Sample

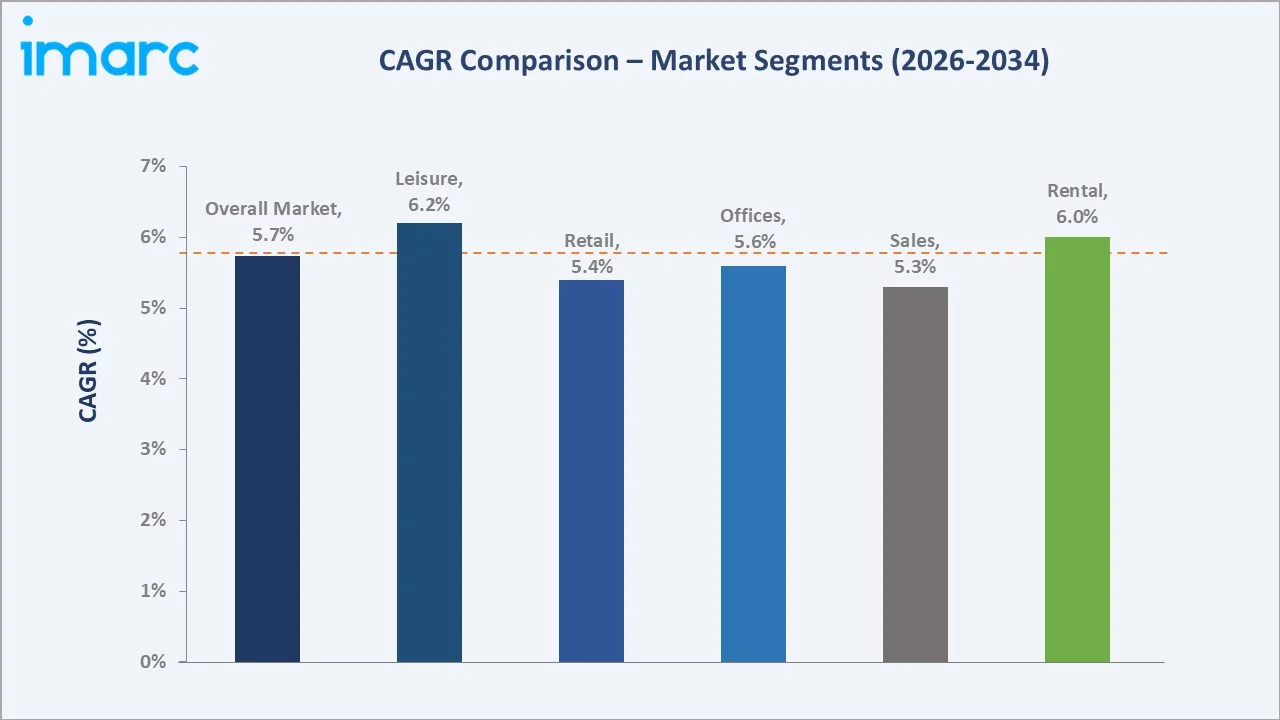

Rental grows fastest at ~6.0% CAGR as premium, green-rated office face rents sustain 3-8% annual rental growth driven by flight-to-quality tenant demand. Leisure commercial grows at ~6.2% CAGR through Australia's post-COVID hotel and tourism investment recovery, Brisbane Olympics hospitality infrastructure, and the acceleration of entertainment-anchored mixed-use commercial precinct development.

Executive Summary

The Australia commercial real estate market reached USD 12.65 Billion in 2025, making Australia one of the Asia-Pacific region's largest commercial real estate markets by transaction value and the most institutionally sophisticated commercial property market in the Southern Hemisphere. The Australian commercial real estate market is distinctive globally for the dominance of listed Australian real estate investment trusts. The market is projected to reach USD 21.23 Billion by 2034.

Rental at 58.6% leads through the ongoing income yield from Australia's commercial real estate stock, office, retail, leisure, and other commercial buildings, generating rental income for their owners at capitalization rates of 4-7% across the quality spectrum. Offices at 36.9% lead end use through the prime importance of CBD office accommodation in Australia's knowledge-economy business model. Australia Capital Territory & New South Wales dominate regionally at 34.2%.

Key Market Insights

|

Insight |

Data |

|

Dominant Type |

Rental - 58.6% share (2025) |

|

Dominant End Use |

Offices - 36.9% market share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 34.2% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Rental at 58.6%: The rental segment dominates the market as most businesses prefer leasing office, retail, warehouse, and industrial spaces to reduce upfront capital investment and maintain flexibility. Strong demand from corporates, retailers, logistics firms, SMEs, and service providers continues to support long-term rental activity across major Australian cities.

- Offices at 36.9%: The offices segment dominates the market due to strong demand from corporate headquarters, financial institutions, technology firms, and professional service companies across major cities. Hybrid work has increased demand for flexible, premium, and well-connected office spaces with modern amenities, sustainability features, and collaborative workplace designs.

- Australia Capital Territory & New South Wales at 34.2%: The Australia Capital Territory & New South Wales region dominates the market due to the strong concentration of government institutions, corporate headquarters, financial services, technology firms, and major office occupiers. Sydney’s role as a leading business and investment hub, along with Canberra’s stable public-sector demand, supports strong leasing activity and commercial property development.

Australia Commercial Real Estate Market Overview

The Australia commercial real estate market encompasses the development, ownership, leasing, management, and sale of income-producing property for commercial purposes across office, retail, leisure, healthcare, education, and other non-residential use categories. The market is structured around five primary asset classes: CBD and metropolitan office, major regional and sub-regional retail, hotel and leisure commercial, healthcare commercial, and specialty commercial.

The ecosystem integrates commercial property developers, listed REITs, unlisted wholesale property funds, institutional direct investors, commercial property services firms, and occupiers across all industries. Macroeconomic factors include economic growth, urbanization, infrastructure development, business expansion, and sustained demand from office, retail, logistics, and industrial occupiers.

Market Dynamics

To evaluate market opportunities, Request Sample

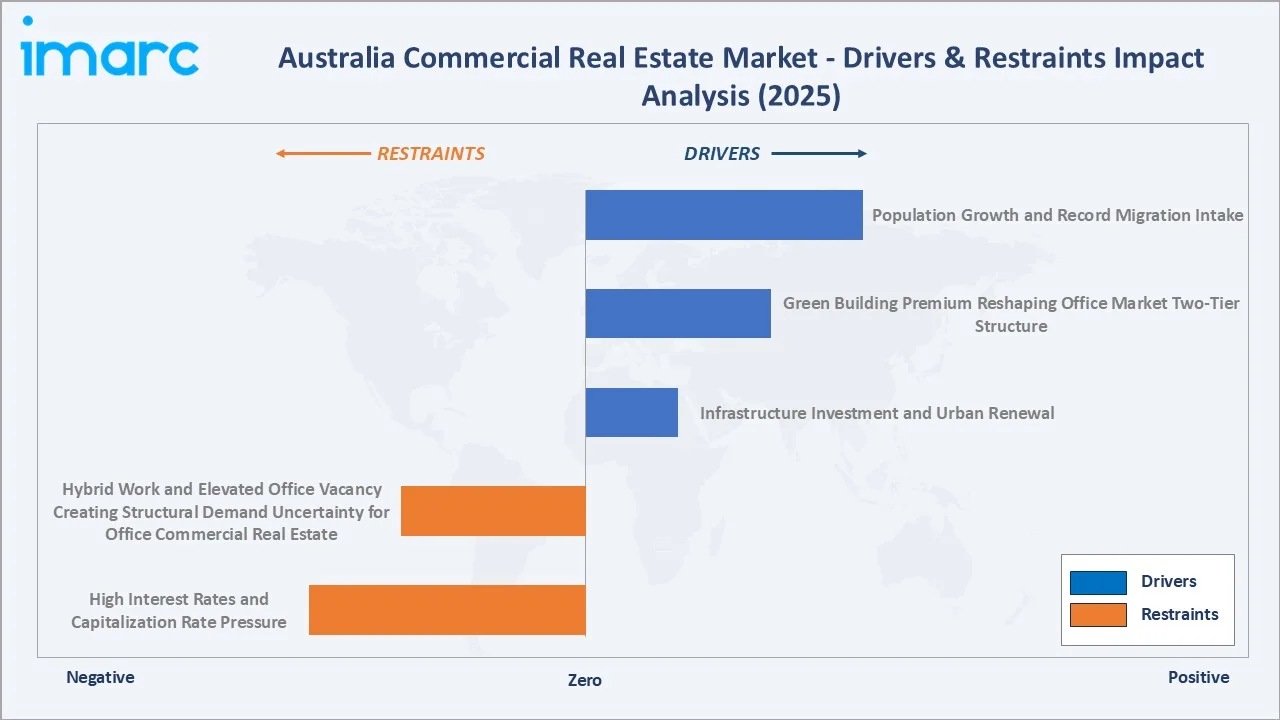

Market Drivers

- Population Growth and Record Migration Intake: Australia's population was 27.72 million people as of September 2025 is the foundational driver of all commercial real estate demand. Each new Australian resident creates demand for new commercial floor space. Net overseas migration was 306,000 in 2024-25. As more people move into major cities, businesses expand their physical presence to serve a larger consumer and workforce base. This supports stronger leasing activity, urban redevelopment, and investment in commercial assets across high-growth metropolitan regions.

- Green Building Premium Reshaping Office Market Two-Tier Structure: Green building premiums are driving as tenants increasingly prefer energy-efficient, low-carbon, and sustainability-certified office spaces. This is creating a two-tier office market, where premium green buildings attract stronger leasing demand, higher rents, and better occupancy, while older non-compliant assets face weaker demand. As a result, developers and landlords are investing in retrofits, ESG upgrades, and net-zero-ready commercial properties.

- Infrastructure Investment and Urban Renewal: Infrastructure investment and urban renewal are improving connectivity, transport access, and business activity around key growth corridors. Large-scale projects such as metro, airport, road, and precinct redevelopment programs are creating demand for offices, retail spaces, mixed-use assets, and logistics-linked commercial properties. These developments also attract private investment and support higher leasing activity in revitalized urban locations.

Market Restraints

- Hybrid Work and Elevated Office Vacancy Creating Structural Demand Uncertainty for Office Commercial Real Estate: Hybrid work and elevated office vacancy are creating uncertainty around long-term office space demand. Many companies are downsizing, adopting flexible leases, or delaying expansion decisions, which weakens absorption in traditional office assets. This puts pressure on landlords to offer incentives, upgrade buildings, and reposition older office spaces to retain tenants.

- High Interest Rates and Capitalization Rate Pressure: High interest rates and capitalization rate pressure are increasing borrowing costs and reducing investor appetite for new acquisitions and developments. Higher cap rates can lower asset valuations, making refinancing, project feasibility, and transaction activity more challenging. This particularly affects office and retail assets where leasing uncertainty already pressures return.

Market Opportunities

- Net Zero Retrofit Wave Creating Commercial Building Upgrade Investment Opportunity: Net-zero retrofit activity is creating an opportunity as landlords upgrade older buildings with energy-efficient systems, smart controls, solar integration, and low-carbon materials. Rising tenant preference for sustainable spaces and ESG-aligned leasing is increasing demand for green-certified commercial assets. This supports higher asset value, stronger occupancy, and new investment opportunities in building modernization.

- Build-to-Rent and Mixed-Use Precinct Development Creating New Commercial Real Estate Asset Classes: Build-to-rent and mixed-use precinct development is combining residential, retail, office, hospitality, and community spaces within integrated developments. These projects generate demand for supporting commercial assets such as retail stores, coworking spaces, healthcare, fitness, and convenience services. As urban populations grow, this trend is encouraging developers and investors to create diversified, income-generating commercial precincts in major cities.

Market Challenges

- Office-to-Residential Conversion Complexity and Planning Risk: Office-to-residential conversion complexity and planning risk are challenging, as many older office buildings require major structural, safety, zoning, and compliance upgrades before they can be repurposed. Lengthy approval processes, high retrofit costs, design limitations, and uncertainty around project feasibility can delay redevelopment. This makes it harder for landlords to quickly reposition vacant office assets into alternative income-generating uses.

- FIRB Restrictions and National Security Review Adding Transaction Complexity for Foreign Capital: Foreign Investment Review Board (FIRB) restrictions and national security reviews are increasing approval requirements for foreign investors in strategic assets such as logistics hubs, data centres, ports, and critical infrastructure-linked properties. Longer review timelines and compliance checks can delay transactions, raise due diligence costs, and create uncertainty around deal completion. This may slow foreign capital deployment in sensitive commercial real estate segments.

Emerging Market Trends

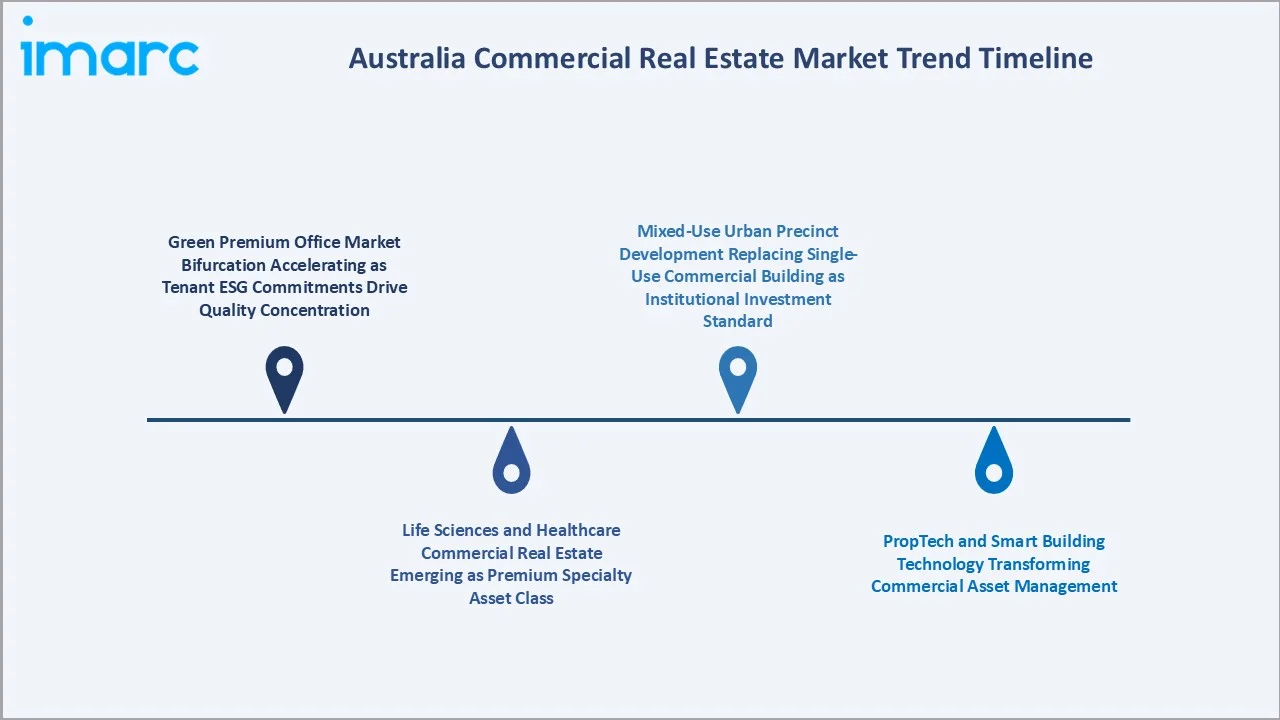

1. Green Premium Office Market Bifurcation Accelerating as Tenant ESG Commitments Drive Quality Concentration

Green premium office market bifurcation is emerging as tenants with ESG commitments increasingly prefer high-quality, energy-efficient, and sustainability-certified office buildings. This is concentrating demand in premium-grade green assets, while older and less efficient buildings face higher vacancy and weaker leasing appeal. As a result, landlords are investing in upgrades, certifications, and net-zero retrofits to remain competitive.

2. Life Sciences and Healthcare Commercial Real Estate Emerging as Premium Specialty Asset Class

Life sciences and healthcare commercial real estate is emerging as a premium specialty asset class in Australia as demand grows for laboratories, medical offices, research facilities, hospitals, and healthcare-linked mixed-use spaces. Rising healthcare spending, biotechnology activity, ageing population needs, and university-industry research collaboration are supporting specialized property demand. These assets often attract stable tenants, long leases, and higher-quality infrastructure requirements, making them increasingly attractive to developers and institutional investors. In June 2024, Kurraba Group launched Australia’s commercial life sciences Campus, a $490 million development in the heart of Sydney’s emerging health and innovation precinct.

3. PropTech and Smart Building Technology Transforming Commercial Asset Management

PropTech and smart building technology are emerging as landlords use IoT sensors, automation, digital twins, and data analytics to improve asset performance. These tools help monitor energy use, occupancy, maintenance needs, air quality, and tenant experience in real time. As tenants seek efficient, sustainable, and flexible spaces, smart building systems are becoming important for reducing operating costs, supporting ESG targets, and improving commercial property value.

4. Mixed-Use Urban Precinct Development Replacing Single-Use Commercial Building as Institutional Investment Standard

Mixed-use urban precinct development is emerging as institutional investors increasingly prefer integrated assets combining office, retail, residential, hospitality, and community spaces. These precincts create diversified revenue streams and stronger tenant demand compared with single-use commercial buildings. Rising urbanization, lifestyle-focused development, and demand for walkable business districts are encouraging developers to build multi-functional commercial hubs across major Australian cities.

Industry Value Chain Analysis

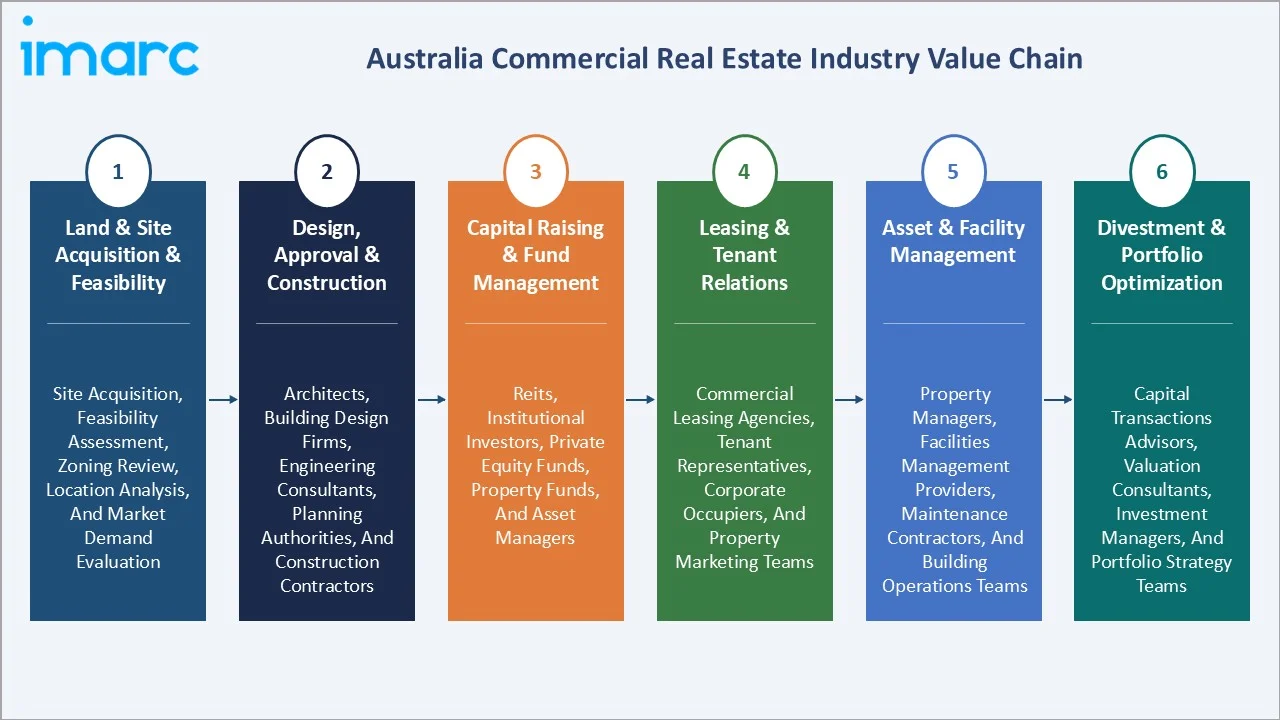

The Australia commercial real estate value chain integrates land and site acquisition and feasibility, design approval and construction, capital raising and fund management, leasing and tenant relations, asset and facility management, and divestment and portfolio optimization. The value chain in Australian commercial real estate is distinctive for its high degree of institutional vertical integration. This integrated model creates commercial efficiency and competitive advantages.

|

Stage |

Key Participants |

|

Land & Site Acquisition & Feasibility |

Site acquisition, feasibility assessment, zoning review, location analysis, and market demand evaluation |

|

Design, Approval & Construction |

Architects, building design firms, engineering consultants, planning authorities, and construction contractors |

|

Capital Raising & Fund Management |

REITs, institutional investors, private equity funds, property funds, and asset managers |

|

Leasing & Tenant Relations |

Commercial leasing agencies, tenant representatives, corporate occupiers, and property marketing teams |

|

Asset & Facility Management |

Property managers, facilities management providers, maintenance contractors, and building operations teams |

|

Divestment & Portfolio Optimization |

Capital transactions advisors, valuation consultants, investment managers, and portfolio strategy teams |

The divestment and portfolio optimization tier creates the capital recycling that enables ongoing commercial real estate value chain activity, by divesting mature, stabilised assets at lower capitalization rates into wholesale investor demand, REITs and developers, free capital for new development and value-add acquisition at higher potential returns.

Technology Landscape in the Australia Commercial Real Estate Industry

Building Management Systems and Smart Building Technology

Building management systems and smart building technology are enabling real-time control of lighting, HVAC, energy use, security, and occupancy across commercial assets. These systems help landlords reduce operating costs, improve tenant comfort, support ESG targets, and enhance building performance. As demand rises for efficient, sustainable, and connected workplaces, BMS and smart building platforms are becoming core technologies in premium commercial properties. In March 2026, Blue IoT announced the release of its Encompass Blue AI Edition. This new platform aims to enhance building intelligence by integrating advanced AI capabilities. It consolidates IoT networks and building management systems into a single ecosystem.

Property Management and Leasing Technology

Property management and leasing technology digitizes lease administration, tenant communication, rent collection, maintenance tracking, and occupancy management. These platforms help landlords improve operational efficiency, reduce manual processes, and enhance tenant experience across office, retail, and mixed-use assets. Integration with analytics, CRM tools, and asset performance systems is making leasing decisions more data-driven and efficient.

Investment and Fund Management Technology

Investment and fund management technology is digitizing portfolio tracking, asset valuation, capital allocation, investor reporting, and fund performance analysis. These platforms help REITs, institutional investors, and asset managers make faster, data-driven decisions across office, retail, industrial, and mixed-use assets. Integration with market analytics, risk modelling, ESG reporting, and transaction management tools is improving transparency, efficiency, and portfolio optimization.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Rental |

58.6% |

2025 |

|

End Use |

Offices |

36.9% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

34.2% |

2025 |

By Type

Rental leads at 58.6% market share (2025). Rental income encompasses all income-generating commercial real estate tenancy relationships such as office leases, retail leases, hotel management agreements and leases, and leisure and specialty commercial leases.

To access detailed market analysis, Request Sample

Sales at 41.4% encompasses commercial investment transactions. Sales transaction volumes are influenced by interest rates, capitalization rate sentiment, and institutional portfolio strategy cycles, creating more volatility in the sales segment than the recurring rental income segment.

By End Use

Offices lead at 36.9% market share (2025). The office end use encompasses all professional, corporate, government, and technology office accommodation across CBD and metropolitan office markets, creating the largest single end-use category through the combination of prime rental value and transaction volume.

Retail at 27.8% encompasses major regional shopping centres, sub-regional retail, supermarket-anchored convenience retail, CBD retail precincts, and specialty retail formats. Leisure at 18.6% grows fastest at ~6.2% CAGR through hotel, entertainment, tourism attractions, and mixed-use leisure commercial development. Others at 16.7% includes healthcare facilities, education, car parks, data centres, service stations, and specialty commercial properties.

Regional Market Insights

|

Region |

Share (2025) |

Key Commercial Real Estate Market Drivers & Characteristics |

|

Australia Capital Territory & New South Wales |

34.2% |

Supported by strong office demand, government presence, financial services activity, institutional investment, and mixed-use commercial development. |

|

Victoria & Tasmania |

23.7% |

Supported by corporate occupiers, retail activity, healthcare facilities, education-linked assets, and Melbourne’s role as a major business and commercial property hub. |

|

Queensland |

17.9% |

Driven by population growth, infrastructure investment, tourism-linked assets, retail expansion, and rising demand for office and mixed-use spaces. |

|

Northern Territory & Southern Australia |

10.6% |

Benefits from government activity, defense-linked demand, industrial services, regional business hubs, and commercial assets serving resource and agricultural sectors. |

|

Western Australia |

13.6% |

Shaped by mining, energy, resources, and export-linked business activity, creating demand for office, retail, industrial, and service-based commercial properties. |

ACT and NSW at 34.2% leads through Sydney CBD's premium office and retail market, combined with Canberra's stable government-backed commercial property demand. Victoria and Tasmania at 23.7% reflects Melbourne's diversified commercial base despite the elevated office vacancy from the hybrid work structural impact.

Queensland at 17.9% is the fastest growing of the major state commercial markets, driven by office tightening and South-East Queensland population growth. Western Australia at 13.6% reflects a resources-cycle-correlated CBD office market and growing mining services commercial demand. NT and SA at 10.6% is anchored by defence industry commercial growth.

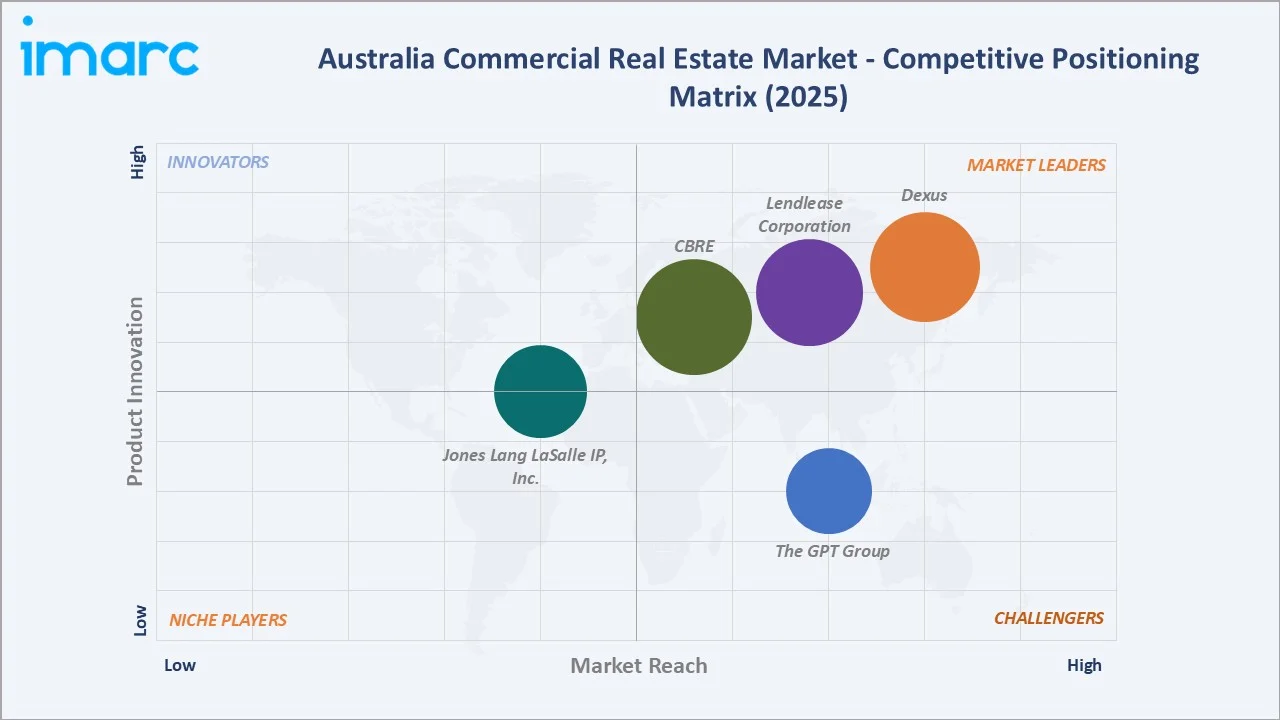

Competitive Landscape

The Australian commercial real estate competitive landscape is structured across three primary competitive domains: REIT and fund managers owning and managing commercial assets; commercial real estate services firms advising owners, occupiers, and investors; and specialist sector players targeting specific commercial property categories.

|

Company Name |

Key Portfolio |

Market Position |

Core Strength |

|

Dexus |

100 Mount Street, 123 Albert Street, 25 Martin Place, 385 Bourke Street, 2 & 4 Dawn Fraser Avenue |

Market Leader |

With decades of experience in real estate and infrastructure investment, funds management, asset management, and development, Dexus has built a strong track record of delivering value for investors. |

|

Lendlease Corporation |

Melbourne Quarter, Barangaroo South, NSW, Blue & William, NSW, Sydney Place, NSW, Victoria Harbour, VIC, Brisbane Showgrounds, QLD, Melbourne Connect, VIC |

Market Leader |

Lendlease is an Australia-centric, market-leading real estate business |

|

The GPT Group |

Charlestown Square, Dapto Mall, Macarthur Square, Macquarie Centre, Marrickville Metro, Melbourne Central Tower, Queen & Collins, TWO PARK |

Strong Challenger |

The GPT Group is one of Australia’s leading real estate investment managers, with a diverse portfolio of high-quality retail, office, logistics and student accommodation assets. |

|

CBRE |

1 Midland Square, 520 Collins Street, 16 Scott Street, 17-23 Nissan Drive, 116-53-57 Esplanade, 78 Waterloo Road, |

Market Leader |

CBRE builds real estate solutions of the future to help clients, professionals and business partners realise their potential. |

|

Jones Lang LaSalle IP, Inc. |

2 KENDALL STREET, 18 - 20 BRUCE STREET, 101 MORAY STREET, 41-45 RICKARD ROAD, 50 BELMORE STREET, BRISBANE TECHNOLOGY PARK |

Established Player |

JLL's innovative, intelligent and sustainable approach includes AI-driven solutions that help illuminate a brighter way forward. |

The competitive landscape is being reshaped by global capital entering Australian commercial real estate through both direct acquisition and platform investment.

Key Company Profiles

Dexus

Dexus is Australia's largest fully-integrated real estate group, with office, industrial, healthcare, and retail assets across owned and managed portfolios.

- Key Portfolio: 100 Mount Street, 123 Albert Street, 25 Martin Place, 385 Bourke Street, 2 & 4 Dawn Fraser Avenue.

- Recent Developments: In December 2025, Dexus launched a new fund series, with its fund set to acquire a 25% stake in a Brisbane shopping centre, named Westfield Chermside, for A$683 million.

- Strategic Focus: To expand and optimize high-quality office, retail, industrial, and mixed-use assets through active funds management, sustainable development, and investor-focused asset management.

Lendlease Corporation

Lendlease Corporation is Australia-centric, integrated commercial real estate developer-constructor-investment managers, with operations across development, construction, and investment management that provide complete commercial real estate value chain capability from concept to divestment.

- Key Portfolio: Melbourne Quarter, Barangaroo South, NSW, Blue & William, NSW, Sydney Place, NSW, Victoria Harbour, VIC, Brisbane Showgrounds, QLD, Melbourne Connect, VIC.

- Strategic Focus: To deliver sustainable urban regeneration, mixed-use precincts, and investment-led commercial assets while strengthening its Australia-focused development and funds management platform.

Market Concentration Analysis

The Australian commercial real estate market exhibits moderate concentration at the institutional ownership level and high fragmentation at the private and SME ownership level. The top listed and unlisted commercial real estate managers collectively manage an estimated AUD 500-600 Billion in Australian commercial real estate, representing 30-40% of the total estimated commercial real estate stock value across all categories.

Market concentration is increasing in the REIT and fund management sector as scale advantages in fund management create powerful incentives for concentration. This concentration trend creates competitive barriers for smaller commercial real estate fund managers, unable to offer the breadth of fund products that institutional investors increasingly require from their commercial property fund manager relationships.

Investment & Growth Opportunities

Highest Growth Segments

Leisure commercial end use (~6.2% CAGR), rental type (~6.0% CAGR), healthcare and life sciences commercial (~8-12% CAGR from growing base), Queensland commercial market (~7-8% CAGR through Olympics catalyst), premium green-rated office rental income (~8-10% CAGR within premium sub-market), and build-to-rent commercial real estate (~25-30% CAGR from near-zero base) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Life sciences commercial real estate is Australia's most compelling emerging commercial property investment opportunity. The intersection of university research excellence, government biomedical investment, and pharmaceutical company R&D investment is creating sustained demand for laboratory, clinical trial, and research commercial accommodation at rental premiums 30-60% above conventional office.

Investment Themes

- Net zero retrofit investment opportunity across Australia's secondary commercial office stock: Australia's secondary commercial office stock of approximately 40-50 million sqm represents the largest single addressable commercial real estate investment opportunity of the 2026-2034 period.

- Life sciences and healthcare commercial real estate development for demographic-driven stable growth: Australia's ageing population creates structural, non-cyclical demand growth for healthcare commercial real estate across all categories - hospitals, day surgery, GP and specialist medical centres, diagnostic imaging, rehabilitation, aged care, and pharmaceutical distribution.

Future Market Outlook (2026-2034)

The Australia commercial real estate market is projected to grow from USD 12.65 Billion in 2025 to USD 21.23 Billion by 2034, delivering a 5.74% CAGR over the forecast period. The market's anchor value of USD 16.73 Billion in 2030 represents an Australian commercial real estate industry at an inflection point. Three structural forces define Australian commercial real estate market growth through 2034. Population growth provides the most reliable foundation. The sustainability imperative creates investment demand. The superannuation growth tailwind provides the capital supply.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including Head of Research Directors; Commercial Leasing Directors; Fund Management Executives; Commercial Development Directors; Sustainability Directors; and senior commercial real estate economists.

Secondary Research

Secondary research encompassed CBRE Australia Office Market Reports Q4 2025; JLL Australia Office Market Overview; Australia Commercial Market Snapshot; Property Council of Australia office market data and Australian Property Digest; Australian Real Estate Annual Property Index; JLL Australia Capital Markets Research; Green Building Council of Australia Green Star Certified Projects Register; Annual Reports; individual company investor presentations and market updates. Over 65 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a combination of commercial real estate income modelling calibrated against Australian Property Annual Index historical income and capital return data, and forward-looking modelling incorporating RBA cash rate forecast, building supply pipeline from PCA commercial property vacancy surveys, population growth from ABS demographic projections, and superannuation fund commercial real estate allocation projections from Association of Superannuation Funds of Australia (ASFA) data. CAGR forecasts by segment calibrated against consensus commercial real estate market forecasts from Real Estate Advisory.

Australia Commercial Real Estate Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Rental, Sales |

| End Uses Covered | Offices, Retail, Leisure, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| COmpanies Covered | Dexus, Lendlease Corporation, The GPT Group, CBRE, Jones Lang LaSalle IP, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia commercial real estate market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia commercial real estate market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia commercial real estate industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Commercial Real Estate Market Report

The Australia commercial real estate market reached USD 12.65 Billion in 2025, driven by premium green-rated office rental growth in Sydney and Brisbane CBDs, retail centre recovery through food and experience remixing programs, leisure and hotel commercial real estate post-COVID recovery, Australia's migration-driven population growth sustaining commercial space demand, and the growing superannuation pool providing institutional capital for commercial real estate investment at above-historical-average volumes.

The market grows at 5.74% CAGR during 2026-2034, reaching USD 21.23 Billion by 2034. Growth reflects population-driven commercial space demand, green building premium creating sustained office rental growth in premium sub-market, healthcare commercial real estate emerging as mainstream institutional asset class, and Build-to-Rent commercial sector scaling from pioneer to established institutional investment category.

Rental leads at 58.6% through the income-yield orientation of Australia's institutional commercial real estate ownership. Rental also grows fastest at ~6.0% CAGR, driven by Sydney CBD and Brisbane CBD premium office rental growth, retail centre rental recovery through experience remixing, and hotel and leisure rental income post-COVID recovery.

Offices lead at 36.9% through Sydney CBD and Melbourne CBD premium office rental concentration.

ACT and New South Wales lead at 34.2% through Sydney CBD's premium office and retail market, combined with Canberra's stable government office accommodation demand.

Leading companies include Dexus, Lendlease Corporation, The GPT Group, CBRE, and Jones Lang LaSalle IP, Inc., among others.

The market is projected to reach approximately USD 16.73 Billion by 2030, with Brisbane CBD emerging as Australia's tightest major office market through Olympics investment, Sydney CBD premium office vacancy sustaining below 5% driving 6-10% annual rental growth in premium sub-market, Melbourne CBD office market stabilising at 12-14% vacancy as conversion and hybrid work stabilization occur, healthcare commercial growth, and Build-to-Rent scaling.

Build-to-Rent (BTR), purpose-built, institutionally owned rental apartments managed as commercial real estate, is Australia's newest and fastest-growing commercial property asset class, growing from near-zero to 30,000+ apartments in the development pipeline.

Three priority opportunities: net zero commercial office retrofit; Brisbane CBD pre-Olympics positioning; and life sciences commercial real estate development at biomedical precincts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)