Australia Concrete Market Size, Share, Trends and Forecast by Concrete Type, Application, End Use Industry, and Region, 2026-2034

Australia Concrete Market Overview:

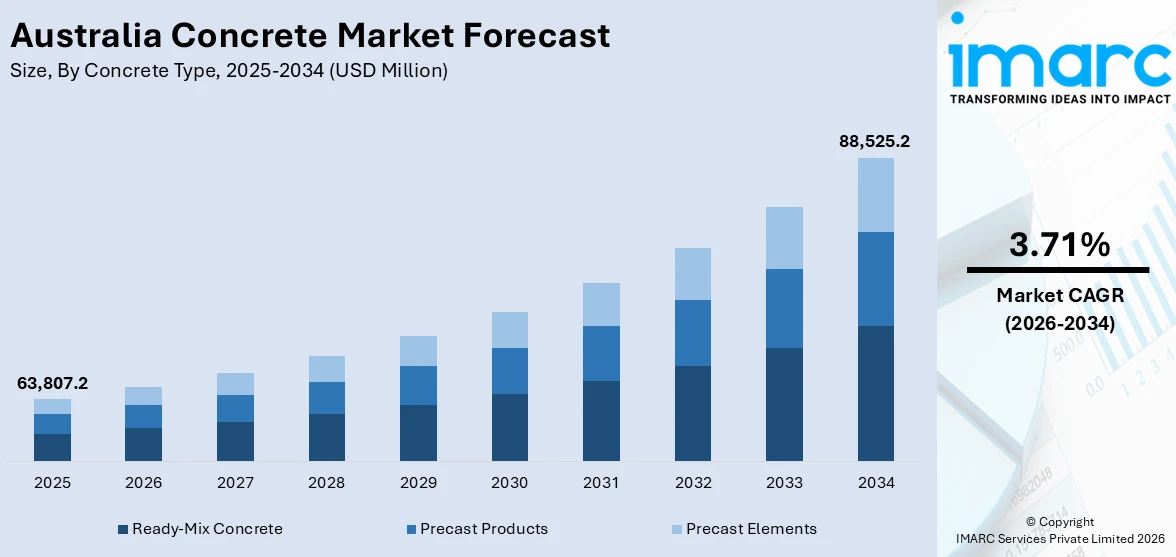

The Australia concrete market size reached USD 63,807.2 Million in 2025. Looking forward, the market is expected to reach USD 88,525.2 Million by 2034, exhibiting a growth rate (CAGR) of 3.71% during 2026-2034. The market is driven by federally backed infrastructure investments requiring high-performance concrete in transport, utilities, and energy projects. National climate goals and certification frameworks are accelerating the adoption of low-carbon materials and recycled aggregates within concrete production. Urban densification and zoning reform are increasing the volume of high-rise residential and commercial builds across major cities, further augmenting the Australia concrete market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 63,807.2 Million |

| Market Forecast in 2034 | USD 88,525.2 Million |

| Market Growth Rate 2026-2034 | 3.71% |

Key Trends of Australia Concrete Market:

Nationwide Infrastructure Upgrades and Public Transport Expansion

Australia’s government continues to prioritize large-scale infrastructure projects to support urban population growth, improve connectivity, and stimulate long-term economic resilience. Initiatives such as the Inland Rail, Western Sydney Airport, Melbourne Metro Tunnel, and Bruce Highway upgrades require extensive concrete applications for tunnels, bridges, highways, and transport interchanges. These projects demand materials with high compressive strength, low permeability, and long service life to withstand dynamic loads and environmental exposure. The federal and state governments have collectively committed billions under infrastructure stimulus and forward capital works programs, placing concrete as a foundational material across transport, energy, and social infrastructure. In addition, regional development in Queensland, New South Wales, and Victoria includes freight terminals, water treatment facilities, and renewable energy sites, further expanding the scope of concrete usage. The Australian Infrastructure Plan and state-based strategies reinforce long-term investment flows into public works, placing significant emphasis on material performance standards and on-time delivery. On April 2, 2024, Laing O'Rourke became the first construction company in Australia to set carbon limits for the concrete products it procures, including those purchased through subcontractors, marking a significant step toward sustainability. The company plans to cap carbon emissions from concrete used in both public and private infrastructure projects, aiming to reduce demand for high-emissions concrete, which currently contributes to around 95% of its overall Scope 3 emissions. Laing O'Rourke has also defined ‘low carbon concrete,’ setting specific carbon dioxide limits per cubic meter based on concrete strength grades, establishing a clearer and more consistent standard for the Australian market. These priorities have intensified demand for advanced concrete formulations, prefabricated systems, and automated batching techniques that meet strict technical, logistical, and regulatory requirements, which is a leading catalyst of the Australia concrete market growth.

To get more information on this market Request Sample

Residential and Commercial Construction Driven by Urban Consolidation

Major cities such as Sydney, Melbourne, Brisbane, and Perth are experiencing intensified demand for high-density residential and mixed-use developments driven by urban consolidation strategies. Government rezoning initiatives, paired with rising migration and population density, have catalyzed construction in inner and middle suburbs where vertical expansion is preferred. Concrete is essential to these developments, particularly in mid- and high-rise structures where fire resistance, load-bearing capacity, and acoustic insulation are critical performance parameters. Additionally, the financial sector’s increased funding for build-to-rent, institutional residential, and social housing is accelerating project pipelines that rely heavily on concrete’s durability and cost-efficiency. Precast panels, post-tensioned slabs, and formwork systems are also gaining popularity, improving site efficiency and quality control across constrained urban lots. As the construction sector responds to labor shortages, regulatory scrutiny, and sustainability criteria, the use of ready-mix and high-strength concrete enables consistency, speed, and compliance. Furthermore, with the growing demand for housing in areas facing labor shortages, technologies like 3D concrete printing (3DCP) offer a promising solution. 3DCP can reduce labor costs by 50–80% through automation, while accelerating construction timelines—allowing structures like a 210 m² house to be printed in as little as 70 hours. With cost savings of up to 78% compared to traditional methods and 63% savings on formwork, 3DCP can play a crucial role in addressing Australia’s housing demand, especially in remote areas or those with high construction needs.

Growth Drivers of Australia Concrete Market:

Government Infrastructure Investment and Policy Support

Federal and state governments across Australia continue to channel substantial capital into infrastructure development programs aimed at economic stimulation and regional connectivity enhancement. Major projects, including the Inland Rail network, Western Sydney Airport precinct, and Melbourne Metro Tunnel are anchored by multi-year budgetary commitments that guarantee sustained concrete procurement volumes. These infrastructure initiatives encompass transport corridors, energy transmission systems, water management facilities, and social infrastructure assets that collectively represent billions in construction value. Government procurement frameworks increasingly stipulate compliance with Australian Standards for concrete performance, requiring manufacturers to deliver materials meeting stringent strength classifications, durability ratings, and environmental criteria. Policy mechanisms such as Infrastructure Australia's Priority List and state-level capital works programs provide visibility into project pipelines extending through the forecast period. Additionally, government stimulus packages targeting regional development have expanded concrete demand beyond metropolitan centers into rural and remote construction zones. This policy-driven infrastructure momentum creates predictable demand cycles for both ready-mix and precast concrete suppliers, supporting capital investment in production capacity and logistics networks, thereby enhancing the Australia concrete market analysis and overall growth trajectory.

Sustainability Mandates and Low-Carbon Concrete Adoption

Environmental regulations and corporate sustainability commitments are fundamentally reshaping concrete production and procurement practices across Australia. The Australian Government's commitment to achieving net-zero emissions by 2050 has cascaded into sector-specific decarbonization roadmaps that directly impact cement and concrete manufacturers. Regulatory frameworks now encourage or mandate reductions in embodied carbon through increased use of supplementary cementitious materials including fly ash, ground granulated blast furnace slag, and recycled aggregates. Infrastructure clients, particularly government agencies and institutional developers, are incorporating carbon intensity thresholds into tender specifications and contract requirements. This regulatory and commercial pressure has accelerated industry adoption of alternative binder systems, optimized mix designs, and carbon capture technologies. Major concrete suppliers have responded by developing low-carbon product lines, obtaining environmental product declarations, and pursuing third-party sustainability certifications. The integration of circular economy principles, including the reuse of returned concrete, demolition waste recycling, and industrial by-product valorization, is becoming standard practice among leading market participants. These sustainability imperatives are driving innovation in concrete chemistry and production processes while simultaneously creating competitive differentiation opportunities for suppliers demonstrating measurable environmental performance improvements, positively influencing the Australia concrete market demand.

Technological Innovation and Prefabrication Solutions

The Australian construction industry is experiencing rapid adoption of advanced manufacturing technologies and prefabrication methodologies that are transforming concrete utilization patterns. Prefabricated concrete elements, including façade panels, floor systems, building modules, and structural components, offer significant advantages in construction speed, quality consistency, and on-site safety compared to traditional cast-in-place methods. These prefabrication benefits align particularly well with Australia's construction sector challenges, including skilled labor shortages, stringent safety regulations, and increasing project complexity. Manufacturers have invested in automated batching systems, digital quality control platforms, and building information modeling integration to optimize production efficiency and reduce material waste. Emerging technologies such as 3D concrete printing are progressing from research applications to commercial pilot projects, demonstrating potential for cost reduction and design flexibility. Automated concrete placement systems, sensor-embedded smart concrete, and self-healing concrete formulations represent additional innovation frontiers gaining traction in Australian infrastructure and building projects. The construction technology ecosystem, comprising equipment manufacturers, software providers, and research institutions, continues to develop solutions that enhance concrete performance while addressing labor productivity constraints. This technological evolution is enabling new application possibilities and market segments while simultaneously improving the economic competitiveness of concrete relative to alternative construction materials, supporting a robust market for future growth.

Australia Concrete Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on concrete type, application, and end use industry.

Concrete Type Insights:

- Ready-Mix Concrete

- Transit Mix Concrete

- Central Mix Concrete

- Shrink Mix Concrete

- Precast Products

- Paving Stones and Slabs

- Bricks

- AAC Blocks

- Others

- Precast Elements

- Facade

- Floor

- Building blocks

- Pipe

- Others

The report has provided a detailed breakup and analysis of the market based on the concrete type. This includes ready-mix concrete (transit mix concrete, central mix concrete, and shrink mix concrete), precast products (paving stones and slabs, bricks, AAC blocks, and others), and precast elements (facade, floor, building blocks, pipe, and others).

Application Insights:

Access the comprehensive market breakdown Request Sample

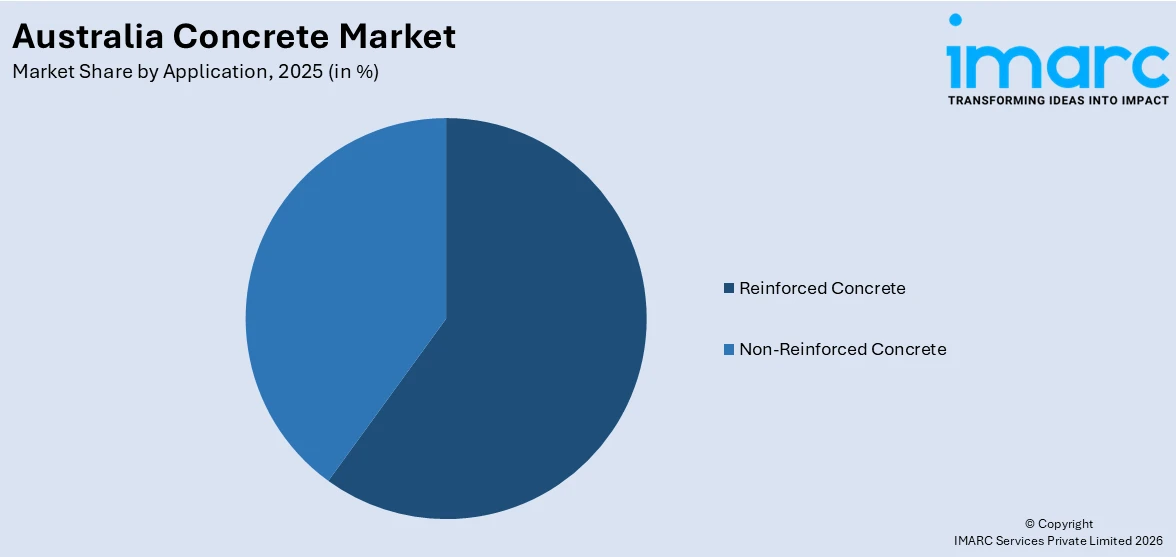

- Reinforced Concrete

- Non-Reinforced Concrete

The report has provided a detailed breakup and analysis of the market based on the application. This includes reinforced concrete and non-reinforced concrete.

End Use Industry Insights:

- Roads and Highways

- Tunnels

- Residential Buildings

- Non-Residential Buildings

- Dams and Power Plants

- Mining

- Others

The report has provided a detailed breakup and analysis of the market based on the end use industry. This includes roads and highways, tunnels, residential buildings, non-residential buildings, dams and power plants, mining, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all major regional markets. This includes Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Concrete Market News:

- On May 15, 2025, Boral Limited announced the acquisition of the newly built Wallan Concrete plant located in Melbourne’s northern growth corridor, enhancing its ability to supply high-demand areas with integrated concrete services. The site features modern batching infrastructure and supports strategic expansion into infrastructure and housing developments.

- On April 16, 2025, Heidelberg Materials announced its acquisition of Midway Concrete’s ready-mix operations in Melbourne and Geelong, reinforcing its vertically integrated model and expanding access to sustainable products. With four new plants added, this move enhances the company’s regional dominance and product portfolio.

Australia Concrete Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Concrete Types Covered |

|

| Applications Covered | Reinforced Concrete, Non-Reinforced Concrete |

| End Use Industries Covered | Roads and Highways, Tunnels, Residential Buildings, Non-Residential Buildings, Dams and Power Plants, Mining, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia concrete market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia concrete market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia concrete industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Concrete Market Report

The concrete market in Australia was valued at USD 63,807.2 Million in 2025.

The concrete market in Australia is projected to exhibit a CAGR of 3.71% during 2026-2034, reaching a value of USD 88,525.2 Million by 2034.

The concrete market in Australia is driven by increasing construction activities in residential, commercial, and infrastructure sectors. Government investments in infrastructure development and urbanization projects significantly boost demand. The focus on sustainable and eco-friendly construction practices encourages the use of green concrete technologies. Additionally, rising population growth and industrial expansion fuel the need for durable and high-performance concrete materials, supporting market growth and innovation across the country.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)