Australia Craft Beer Market Size, Share, Trends and Forecast by Product Type, Age Group, Distribution Channel, and Region, 2026-2034

Australia Craft Beer Market Summary:

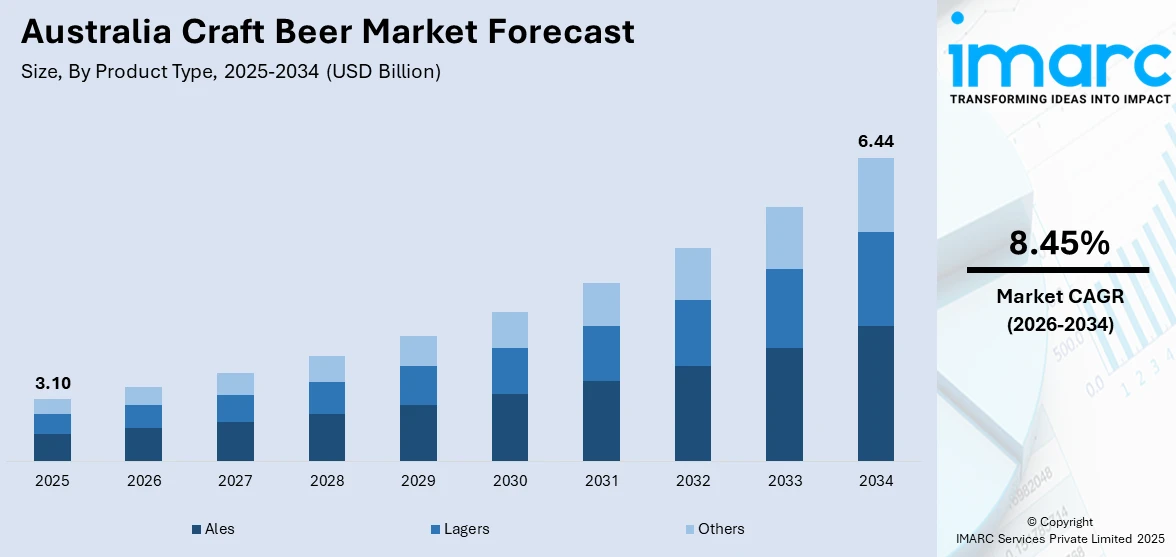

The Australia craft beer market size was valued at USD 3.10 Billion in 2025 and is projected to reach USD 6.44 Billion by 2034, growing at a compound annual growth rate of 8.45% from 2026-2034. The Australia craft beer market is witnessing substantial expansion as consumer preferences shift toward premium, locally brewed beverages that emphasize quality, authenticity, and unique flavor profiles. Growing interest in artisanal products, coupled with the proliferation of microbreweries across urban and regional areas, is driving sustained market momentum. Favorable demographic trends, particularly among younger consumers seeking distinctive drinking experiences, alongside thriving beer tourism and festival culture, are reinforcing market penetration and elevating Australia craft beer market share.

To get more information on this market Request Sample

Key Takeaways and Insights:

- By Product Type: Ales dominates the market with a share of 48% in 2025, driven by strong consumer preference for pale ales, IPAs, and hazy variants that offer bold flavor profiles and aromatic complexity. The popularity of hop-forward styles among craft enthusiasts continues to reinforce ales as the cornerstone of Australia's craft beer landscape.

- By Age Group: 21–35 years old lead the market with a share of 45% in 2025, reflecting strong engagement from millennials and younger consumers who prioritize quality over quantity and seek authentic, narrative-driven beverage experiences. This demographic's affinity for experiential consumption through taprooms, brewery tours, and craft festivals sustains market growth.

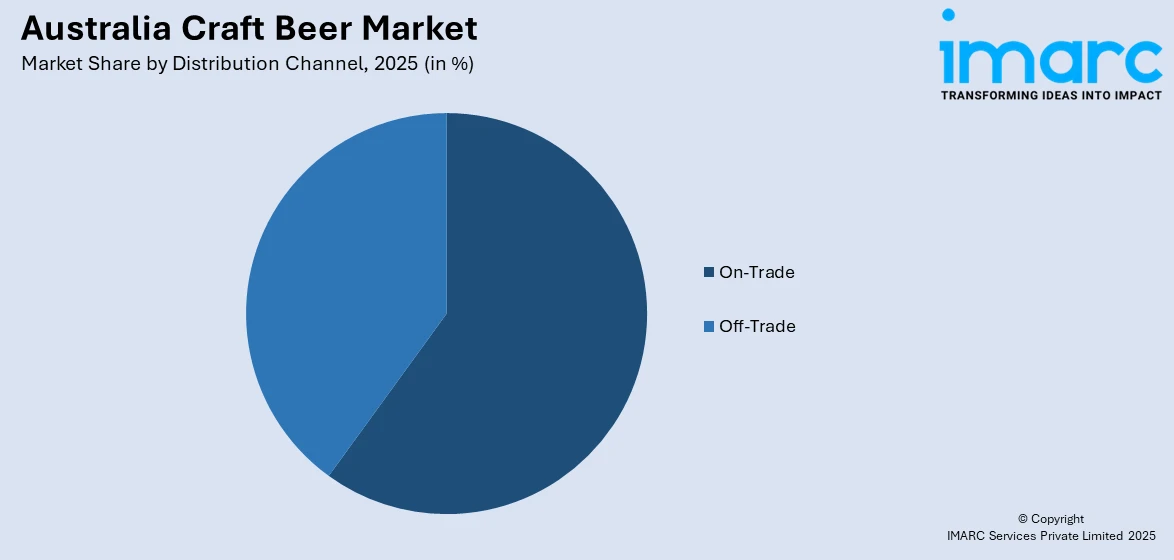

- By Distribution Channel: On-trade holds the largest segment with a market share of 60% in 2025, underpinned by Australia's vibrant hospitality sector where pubs, bars, and restaurants serve as primary venues for craft beer discovery. The social drinking culture and preference for fresh draught experiences drive continued on-premise consumption dominance.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 29% share in 2025, owing to the Sydney and Canberra metropolitan areas' increased population density, concentration of craft breweries, and robust urban demand for high-end beverages.

- Key Players: Key players drive the Australia craft beer market by diversifying product portfolios, investing in innovative brewing techniques, and expanding distribution networks. Their focus on quality ingredients, sustainability initiatives, and strategic partnerships with hospitality venues enhances brand visibility and accelerates consumer adoption across diverse market segments.

The Australia craft beer industry has emerged as a dynamic segment within the broader alcoholic beverages market, characterized by rapid innovation, creative brewing techniques, and strong consumer engagement across urban and regional areas. Independent breweries are increasingly focusing on differentiation through unique flavor profiles, locally sourced ingredients, and sustainability-focused brewing practices that resonate with environmentally conscious consumers seeking authentic beverage experiences. The market benefits from a robust ecosystem of microbreweries, brewpubs, and taprooms that foster direct consumer relationships, encourage brand loyalty, and provide immersive tasting experiences. Strategic partnerships between craft breweries and sports organizations are expanding market reach and enhancing brand visibility among mainstream audiences. Beer festivals and tourism initiatives continue strengthening consumer connections while providing platforms for emerging brewers to showcase their offerings. These developments underscore the market's trajectory toward premiumization, experiential consumption, and community-driven brand building that distinguishes craft offerings from mainstream alternatives.

Australia Craft Beer Market Trends:

Native Australian Ingredients Innovation

Craft breweries across Australia are increasingly engaging in bold experimentation to differentiate their offerings in a competitive market. Many brewers are utilizing native Australian ingredients such as wattleseed, lemon myrtle, and finger lime to develop unique flavor profiles that reflect local terroir and cultural identity. This trend toward indigenous ingredient incorporation extends to fruit infusions and spice blends for seasonal and limited-edition releases, appealing to adventurous consumers seeking authentic Australian brewing experiences and supporting Australia craft beer market growth.

Sports Partnerships Expanding Brand Visibility

Craft beer is gaining deeper exposure through high-visibility sports partnerships that embed brands into community experiences. Regional brewers are leveraging affiliations with Australian Football League teams to boost visibility and exclusivity in match-day environments. In December 2024, the Adelaide Football Club entered a three-year partnership with Coopers Brewery, marking Coopers' first AFL partnership and ensuring exclusive beer availability at Crows events and corporate areas. These alignments signal growing integration of local brewers into mainstream entertainment.

Beer Festivals Strengthening Market Presence

Public festivals are becoming key drivers in boosting the presence of independent brewers and fostering community engagement. These multi-day celebrations serve as launchpads for emerging brewers while reaffirming the relevance of established brands. In October 2024, the 19th Annual Australian Beer Festival took place at the Australian Heritage Hotel in Sydney, showcasing over 40 craft breweries across three days. With increasing turnout and brewer participation each year, festivals are solidifying their role as important platforms for discovery, visibility, and market expansion.

Market Outlook 2026-2034:

The Australia craft beer market outlook remains positive as consumer demand for premium, locally crafted beverages continue expanding across urban and regional markets. Government initiatives supporting the industry, including the two-year freeze on excise indexation for draught beer, are expected to provide relief for brewers and hospitality businesses. The continued proliferation of microbreweries, expanding beer tourism, and strategic partnerships with hospitality venues will sustain growth momentum throughout the forecast period. The market generated a revenue of USD 3.10 Billion in 2025 and is projected to reach a revenue of USD 6.44 Billion by 2034, growing at a compound annual growth rate of 8.45% from 2026-2034.

Australia Craft Beer Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Ales |

48% |

|

Age Group |

21–35 Years Old |

45% |

|

Distribution Channel |

On-Trade |

60% |

|

Region |

Australia Capital Territory & New South Wales |

29% |

Product Type Insights:

- Ales

- Lagers

- Others

Ales dominate with a market share of 48% of the total Australia craft beer market in 2025.

Ales represent the cornerstone of Australia's craft beer landscape, commanding the largest market share due to their diverse flavor profiles and aromatic complexity. Pale beers, India Pale beers (IPAs), hazy ales, and specialized varieties that appeal to daring customers looking for unique flavor experiences are all included in this category. Australian craft brewers have embraced ale production as a platform for innovation, experimenting with hop varieties, yeast strains, and brewing techniques to create signature offerings that differentiate their brands in an increasingly competitive marketplace.

The GABS Hottest 100 Aussie Craft Beers poll for 2024 demonstrated overwhelming ale dominance, with 80 of the top 100 beers falling within the pale and hoppy ale category, including pale ales, XPAs, hazy ales, and various IPA styles. Pale ale remains the most consumed beer style among Australian craft drinkers, with consumers gravitating toward hop-forward offerings that deliver aromatic complexity and bold flavor characteristics that distinguish craft products from mass-produced alternatives.

Age Group Insights:

- 21–35 Years Old

- 40–54 Years Old

- 55 Years and Above

21–35 years old leads with a share of 45% of the total Australia craft beer market in 2025.

Young adult consumers represent the primary demographic driving Australia's craft beer market expansion, significantly shaping overall industry trends and new product development directions. This cohort prioritizes quality over quantity, seeking authentic, narrative-driven products that genuinely reflect their values around craftsmanship, local sourcing, and environmental sustainability. Millennials and younger Gen Z consumers demonstrate strong engagement through brewery visits, taproom experiences, and craft beer festivals, viewing consumption as an experiential activity rather than merely transactional purchasing behavior.

Research indicates that the transition from mainstream to craft beer represents a generational shift with lasting market implications for producers and retailers alike. Young urban professionals in inner-city areas particularly embrace craft beer culture, with concentrations highest in Sydney, Melbourne, and Brisbane metropolitan regions. Industry analysis confirms that Gen Z and Millennials prioritize experiential occasions more than older generations, with significantly higher proportions of their drinking occasions focused on experiences, reinforcing craft beer's appeal through taprooms and festivals.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- On-Trade

- Off-Trade

On-trade exhibits a clear dominance with a 60% share of the total Australia craft beer market in 2025.

The on-trade model refers to the distribution of craft beer through pubs, bars, restaurants, brewpubs, as well as hospitality environments where the consumer is able to access the social profile of craft beer consumption. The on-trade model is advantageously positioned in Australian society as the culture of social beer consumption is highly ingrained, particularly as beer is considered to be associated with social events, group gatherings, as well as sporting events. The fresh character of craft beer can be accessed through the guidance of professionals.

Industry data suggests that draught beer is vastly consumed for business purposes, with pubs, bars, breweries, restaurants, and hotels being key players in drinking craft beer. The rise of the hospitality sector is a key contributor to the dominance of the on-trade market, where microbreweries are increasingly opening own taprooms to directly interact with consumers. The partnership between breweries, especially exclusive rights to pour beer in sporting venues, entertainment parks, etc., also adds to the strength of the on-trade market.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represent the leading segment with a 29% share of the total Australia craft beer market in 2025.

The Australian Capital Territory and New South Wales region leads the craft beer market due to its substantial population base, high concentration of breweries, and strong urban demand for premium beverages. Sydney serves as a major hub for craft beer consumption, hosting numerous microbreweries, specialty bottle shops, and hospitality venues that champion independent brewers. The region's cosmopolitan consumer base demonstrates sophisticated appreciation for craft offerings, driving innovation and premiumization trends across the market.

Survey data confirms that the largest concentrations of craft beer drinkers in Australia are located in New South Wales, Victoria, and Queensland, attributed to higher population density and brewery presence. The NSW Department of Primary Industries actively supports industry development, hosting initiatives such as the November 2024 'Paddock to Pint' workshop at the Orange Agricultural Institute, which introduced farmers and brewers to Mountain Rye perennial grain for beer production applications, demonstrating government commitment to regional craft beer industry growth.

Market Dynamics:

Growth Drivers:

Why is the Australia Craft Beer Market Growing?

Rising Consumer Demand for Premium Locally Brewed Products

Australian consumers are increasingly gravitating toward premium, artisanal beverages that emphasize quality, authenticity, and local provenance over mass-produced alternatives. This shift reflects broader lifestyle changes where consumers prioritize experiences and craftsmanship, viewing craft beer consumption as an expression of personal identity and values. The desire for unique flavor profiles, innovative brewing techniques, and connection to local communities drives sustained demand for independently produced craft offerings. This premiumization trend is reinforced by rising disposable incomes, exposure to global craft beer movements, and growing emphasis on supporting local businesses. The Independent Brewers Association reports that craft breweries contribute approximately AUD 3.53 Billion annually to the national economy, demonstrating the sector's economic significance. Consumers demonstrate willingness to pay premium prices for high-quality products that deliver distinctive taste experiences and authentic brand stories.

Expanding Microbrewery and Brewpub Culture

Increased microbrewery establishments, on the-other-hand, have increased the diversity relating to beer products in the Australian landscape. This is because the presence of microbreweries has proffered consumers unprecedented consumer access to the microbrew world. This suggests the potential contribution that can be offered by microbreweries in the development of regional Australia. This can be done through the creation of employment opportunities, supporting the local agricultural economy, in addition to the potential contribution microbreweries have on beer tourism. In the same vein, the taproom model has the potential advantage of facilitating the development of consumer relationships on the part of microbreweries without relying on consumer access via conventional connections. This is because the government has rolled out the process of issuing licenses for the development of microbreweries.

Strong Engagement from Younger Consumer Demographics

Millennials and Gen Z consumers represent the primary growth engine for Australia's craft beer market, demonstrating strong preferences for authentic, innovative, and experiential beverage offerings. These demographics prioritize quality over quantity, seeking products that align with their values around sustainability, local sourcing, and craftsmanship. Their engagement extends beyond simple consumption to include brewery visits, festival attendance, and active participation in craft beer communities through social media platforms. Research identifies craft beer drinkers as educated, urban consumers who value flavor exploration and local producer support over volume consumption. Young adults aged 18-34 continue visiting pubs, bars, and restaurants more frequently than older demographics despite cost-of-living pressures, indicating strong commitment to experiential consumption. This demographic's influence on market trends ensures continued innovation and premiumization as breweries compete for their attention and loyalty.

Market Restraints:

What Challenges the Australia Craft Beer Market is Facing?

High Excise Tax Burden

Australia's beer tax is one of the highest in the world, and a series of bi-annual increases in line with the Consumer Price Index have resulted in beer taxes at very high levels for packaged beers, contributing to a large percentage of their retail price. Overall, the current beer taxes have placed a huge financial burden on craft beer brewers and have become a major cause for worry for those craft beer brewers whose margins for profits are already low compared to others.

Market Concentration and Distribution Challenges

The Australian beer market is still very consolidated, with two foreign-owned companies holding the majority of the market share due to their comprehensive networks of distribution and venue contracts. The independent brewer finds it very difficult to infiltrate the hospitality premises because of the exclusive tap arrangements entered into by major distributors, thus making it hard to reach consumers through traditional on-premise channels. A market with such a structure inhibits growth opportunities for craft breweries despite overwhelming consumer demand for their products.

Rising Production and Operating Costs

The craft brewing business generally faces rising costs for various factors of production, such as specialty hops, malts, energy, and freight. Notably, the cost-of-living crisis has resulted in a reduction in discretionary spending for premium products, making this a challenging operating environment for breweries. The brewery business has experienced a large number of voluntary administrations and closings over the years, with this issue pointing to the vulnerability of the brewery business to external forces.

Competitive Landscape:

The market structure of the craft beer industry in Australia is considered dynamic, presenting intense competition from the presence of several independent craft breweries operating alongside craft beer brands owned by multinational corporations. For independent breweries, innovation is the core factor differentiating their craft from the rest of the competition, while the bigger breweries utilize their pre-established distribution channels to access the broader consumer market. Strategy has also emerged as another key factor being explored by craft breweries to position their brands more effectively relative to the bigger players in the craft beer industry. Quality accreditation, including recognition of craft breweries through industry awards, has also impacted consumer demand.

Recent Developments:

- In February 2025, the Albanese Labor Government announced a two-year freeze on the excise indexation for draught beer, effective from August 2025. This measure aims to support beer drinkers, brewers, and hospitality businesses amid rising prices and provides relief for the craft beer sector facing sustained taxation pressures.

- In December 2024, Western Australia-based Beerfarm announced plans to commence construction on a new brewery and taphouse in Glenworth Valley on the NSW Central Coast. The development will supply Beerfarm products throughout the East Coast and increase overall production capacity, with Phase One brewing operations expected by mid-2025.

Australia Craft Beer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Ales, Lagers, Others |

| Age Groups Covered | 21–35 Years Old, 40–54 Years Old, 55 Years and Above |

| Distribution Channels Covered | On-Trade, Off-Trade |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Craft Beer Market Report

The Australia craft beer market size was valued at USD 3.10 Billion in 2025.

The Australia craft beer market is expected to grow at a compound annual growth rate of 8.45% from 2026-2034 to reach USD 6.44 Billion by 2034.

Ales dominated the market with a share of 48%, driven by strong consumer preference for pale ales, IPAs, and hazy variants that deliver bold flavor profiles and aromatic complexity appealing to craft beer enthusiasts.

Key factors driving the Australia craft beer market include rising consumer demand for premium locally brewed products, expanding microbrewery culture, strong engagement from younger demographics, and growing beer tourism and festival activities.

Major challenges include high excise tax burden making Australia's beer tax third-highest globally, market concentration with foreign-owned corporations controlling distribution, rising production costs, and limited venue access due to exclusive tap contracts.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade