Australia Cybersecurity Market Size, Share, Trends and Forecast by Component, Deployment Type, User Type, Industry Vertical, and Region, 2026-2034

Australia Cybersecurity Market Size, Share, Trends & Forecast (2026-2034)

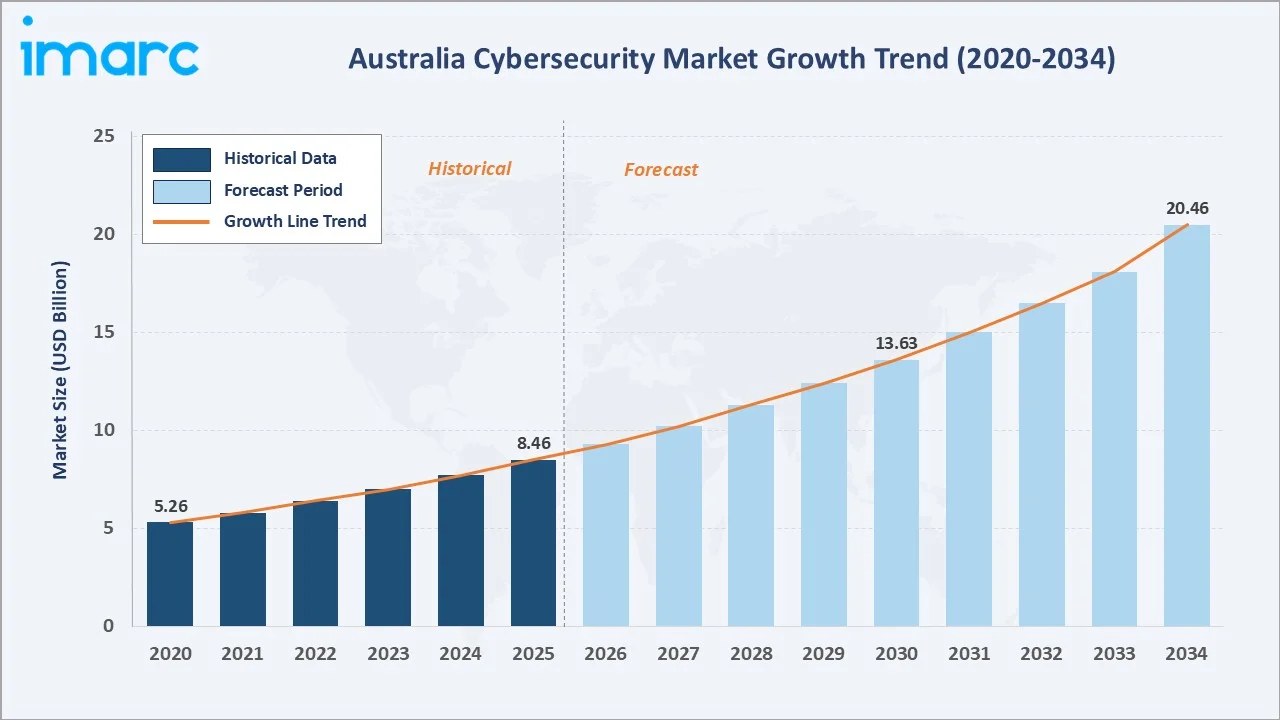

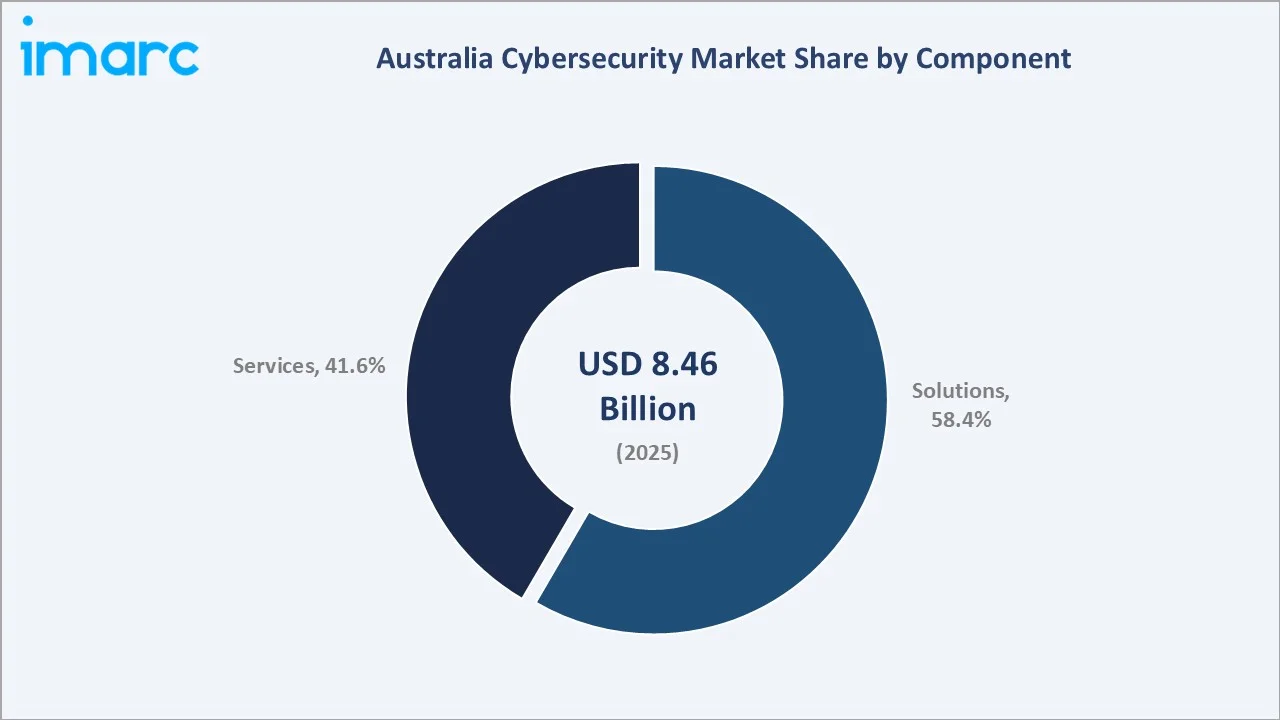

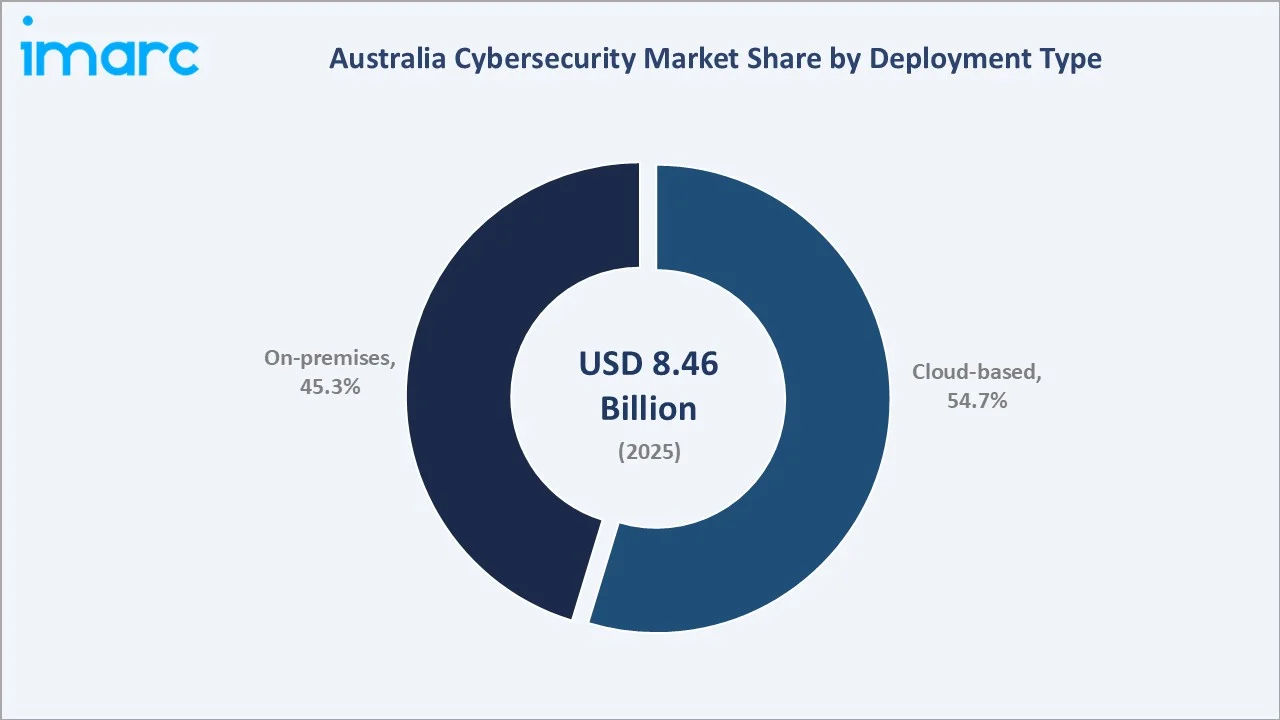

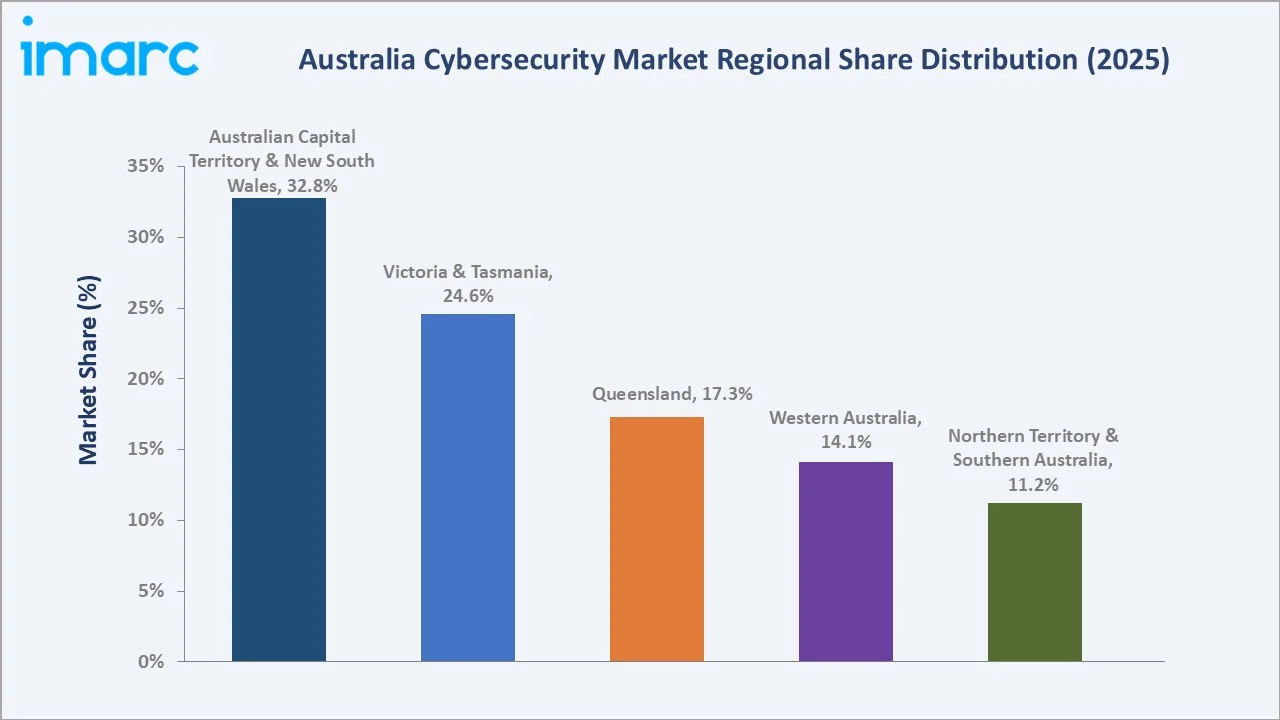

The Australia cybersecurity market reached USD 8.46 Billion in 2025 and is projected to reach USD 20.46 Billion by 2034, growing at a CAGR of 10.00% during 2026-2034. As of August 2025, employment among Database and Systems Administrators and ICT Security Specialists reached around 70,900, increasing by 3,300 compared with the previous year in Australia. The workforce is expected to expand by 14.2% from May 2024 to 2029, significantly outpacing the national employment growth average of 6.6%. This rising employment demand is driving the Australia cybersecurity market by increasing investment in security tools, managed services, threat detection platforms, and workforce training. Solutions dominate at 58.4%. Cloud-based deployment leads at 54.7%. Australia Capital Territory & New South Wales command 32.8% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.46 Billion |

|

Forecast Market Size (2034) |

USD 20.46 Billion |

|

CAGR (2026-2034) |

10.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Component |

Solutions (58.4%, 2025) |

|

Dominant Deployment |

Cloud-based (54.7%, 2025) |

|

Leading Region |

Australia Capital Territory & New South Wales (32.8%, 2025) |

The market expanded from USD 5.26 Billion in 2020 to USD 8.46 Billion in 2025, anchored at USD 13.63 Billion in 2030, and forecast to reach USD 20.46 Billion by 2034. The data breaches created a watershed moment for Australian cybersecurity investment, triggering the Government's accelerated cybersecurity reform agenda, the mandatory reporting expansion under the Privacy Act, and board-level cybersecurity governance elevation across all major Australian organisations.

To get more information on this market, Request Sample

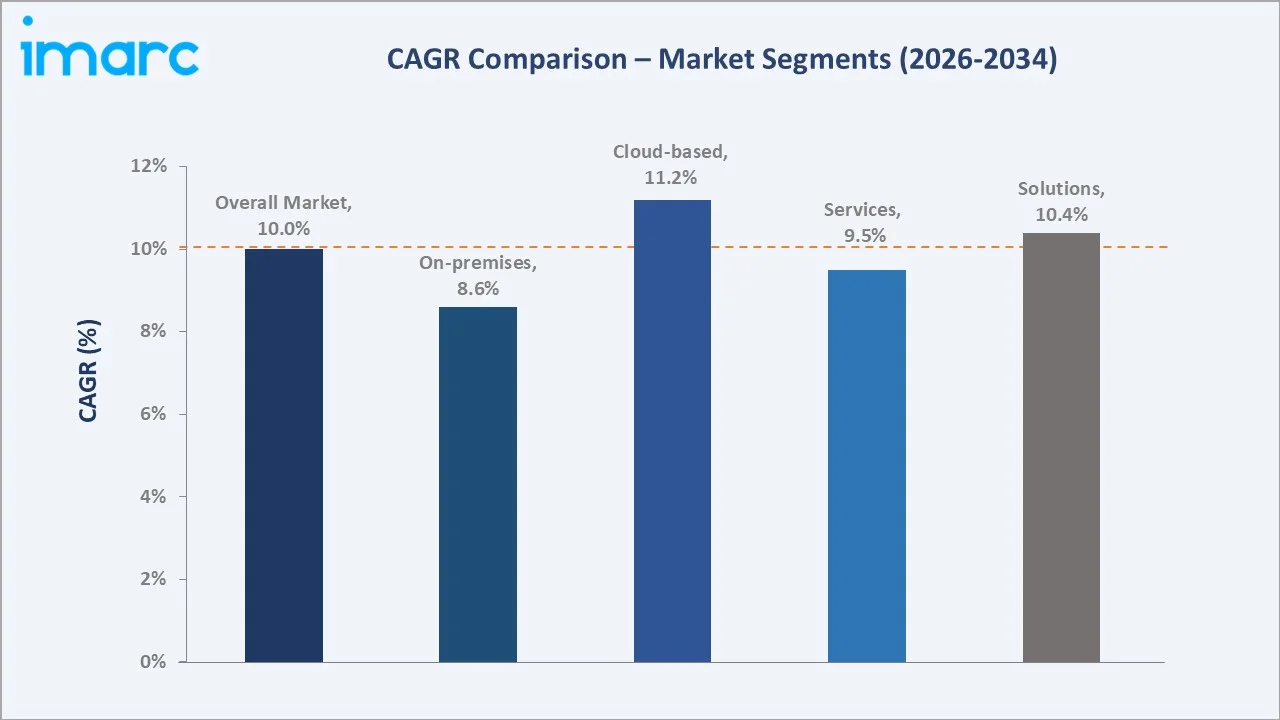

Solutions grow fastest at ~10.4% CAGR driven by XDR (Extended Detection and Response), SASE (Secure Access Service Edge), cloud security posture management (CSPM), and AI-powered threat detection platforms that are progressively replacing point-product security tools across Australian enterprises. Cloud-based deployment grows fastest at ~11.2% CAGR as Australian government agencies adopt IRAP-assessed cloud security services and enterprises accelerate hybrid multi-cloud adoption, requiring cloud-native security platforms.

Executive Summary

The Australia cybersecurity market reached USD 8.46 Billion in 2025, ranking Australia as one of the Asia-Pacific region's largest cybersecurity markets, and one of the world's top cybersecurity markets by absolute spending. The market is projected to reach USD 20.46 Billion by 2034.

Solutions at 58.4% dominate through the deployment of endpoint detection and response (EDR), network security platforms, identity and access management (IAM), data loss prevention (DLP), and cloud security platforms across Australian enterprise, government, and critical infrastructure sectors. Cloud-based deployment at 54.7% reflects the adoption inflection point where more than half of Australian cybersecurity is now delivered as cloud or SaaS services. ACT and NSW lead regionally at 32.8%, through federal government and financial services concentration.

Key Market Insights

|

Insight |

Data |

|

Dominant Component |

Solutions - 58.4% share (2025) |

|

Dominant Deployment |

Cloud-based - 54.7% market share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 32.8% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Solutions at 58.4%: The solutions segment dominates the market as organizations increasingly deploy security platforms, threat detection systems, identity access management, encryption, and endpoint protection tools to safeguard digital infrastructure. Rising cyber risks, cloud adoption, and compliance requirements are further driving demand for advanced cybersecurity solutions across enterprises and government agencies.

- Cloud-based at 54.7%: The cloud-based segment dominates the market as businesses increasingly shift workloads, applications, and data to cloud environments, creating strong demand for scalable cloud security, threat monitoring, access control, and data protection solutions. Growing adoption of hybrid work, SaaS platforms, and cloud infrastructure further strengthens the need for flexible and cost-efficient cybersecurity deployment.

- ACT and NSW at 32.8%: Australian Capital Territory & New South Wales dominate the market due to the strong concentration of federal government agencies, defense operations, financial institutions, technology firms, and large enterprises. High spending on data protection, digital government services, cloud security, and critical infrastructure protection further supports cybersecurity demand in the region.

Australia Cybersecurity Market Overview

The Australia cybersecurity market encompasses the procurement, deployment, and management of cybersecurity solutions and services across all sectors of the Australian economy, from federal and state government to financial services, healthcare, critical infrastructure, resources, and SME. The market is defined by Australia's specific threat environment, regulatory framework, and the unique demands of Australia's geographic position.

The ecosystem integrates cybersecurity technology vendors with Australian-headquartered providers, carrier-based security providers, defence and intelligence specialist providers, managed service providers, system integrators, and the government's own cyber capability. Macroeconomic factors include rapid digitalization, rising cloud and data center investments, expanding e-commerce and fintech activity, and growing dependence on digital public services.

Market Dynamics

To evaluate market opportunities, Request Sample

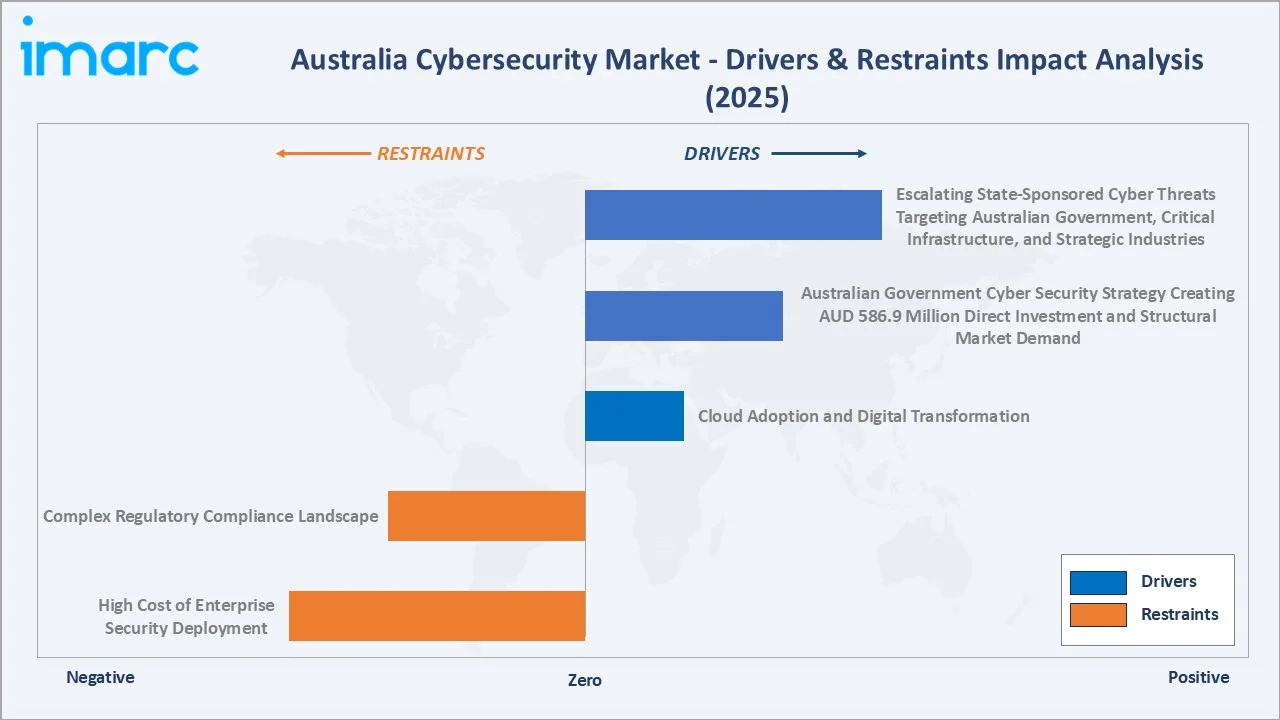

Market Drivers

- Escalating State-Sponsored Cyber Threats Targeting Australian Government, Critical Infrastructure, and Strategic Industries: In FY2024-25, Australian Signals Directorate’s Australian Cyber Security Centre (ASD’s ACSC) received over 42,500 calls to the Australian Cyber Security Hotline, a 16% increase from the previous year. These escalating cyber threats are driving the market by increasing demand for advanced threat intelligence, zero-trust security, endpoint detection, and incident response solutions. Government agencies, defense networks, energy utilities, telecom operators, and financial institutions are investing more heavily to protect sensitive data and critical infrastructure.

- Australian Government Cyber Security Strategy Creating AUD 586.9 Million Direct Investment and Structural Market Demand: The Australian Government focus to commit A$586.9 million to the Cyber Security Strategy out to 2030, articulating the goal of making Australia the world's most cyber-secure country by 2030. The Strategy's mandatory standards for smart devices and director liability reforms create compliance-driven demand that extends cybersecurity investment to previously underspending organisations.

- Cloud Adoption and Digital Transformation: Cloud adoption and digital transformation are driving the market as businesses migrate applications, workloads, and customer data to cloud platforms, increasing the need for cloud security, identity management, encryption, and threat monitoring. The rise of hybrid work, digital banking, e-commerce, and connected enterprise systems is expanding the cyber risk surface. As a result, organizations are investing in scalable cybersecurity solutions to protect digital assets, ensure compliance, and maintain business continuity.

Market Restraints

- High Cost of Enterprise Security Deployment: The high cost of enterprise security deployment is hampering as advanced tools, skilled professionals, integration, compliance, and continuous monitoring, which require significant investment. Small and medium-sized businesses often delay or limit cybersecurity adoption due to budget constraints. High implementation and maintenance costs also make it difficult for organizations to upgrade legacy systems or deploy comprehensive, multi-layered security frameworks.

- Complex Regulatory Compliance Landscape: Complex regulatory compliance is hampering the market as organizations must align with multiple privacy, data protection, critical infrastructure, and sector-specific security requirements. This increases compliance costs, documentation burden, audit pressure, and the need for specialized legal and cybersecurity expertise. For smaller firms, regulatory complexity can slow cybersecurity adoption, delay implementation, and make security investments more difficult to scale.

Market Opportunities

- Cyber Partnership Creating Sovereign Capability Investment and Tri-National Security Collaboration: Cyber partnerships strengthening sovereign security capabilities, local technology development, and advanced cyber defense infrastructure. Tri-national collaboration, particularly through defense and intelligence alliances, is encouraging investment in secure communications, threat intelligence, workforce development, and critical infrastructure protection. These partnerships also support domestic cybersecurity vendors by opening opportunities in government, defense, and strategic industry contracts.

- AI-Driven Security Operations Transforming SOC Capabilities Across Australian Enterprise: AI-driven security operations help enterprises improve threat detection, incident response, and real-time monitoring across complex IT environments. AI-enabled SOC platforms can reduce alert fatigue, automate routine security tasks, and identify suspicious activity faster than traditional systems. As cyber threats become more sophisticated, Australian organizations are expected to invest more in AI-powered analytics, automated response tools, and managed detection services.

Market Challenges

- Supply Chain Cybersecurity Risk Creating Third-Party Risk Management Complexity: Supply chain cybersecurity risk is challenging as organizations increasingly depend on third-party vendors, cloud providers, software partners, and outsourced service providers. A security weakness in any external partner can expose sensitive data, disrupt operations, or compromise critical systems. This makes vendor risk assessment, continuous monitoring, compliance checks, and incident coordination more complex and costly for Australian enterprises.

- Ransomware and Business Email Compromise Sustained Financial Losses Requiring Response Capability Investment: Ransomware and business email compromise causing sustained financial losses, operational disruption, data theft, and reputational damage across businesses and public institutions. These attacks force organizations to invest heavily in backup systems, email security, endpoint protection, cyber insurance, incident response, and recovery planning. However, the rising cost and complexity of response capabilities can strain security budgets, especially for SMEs.

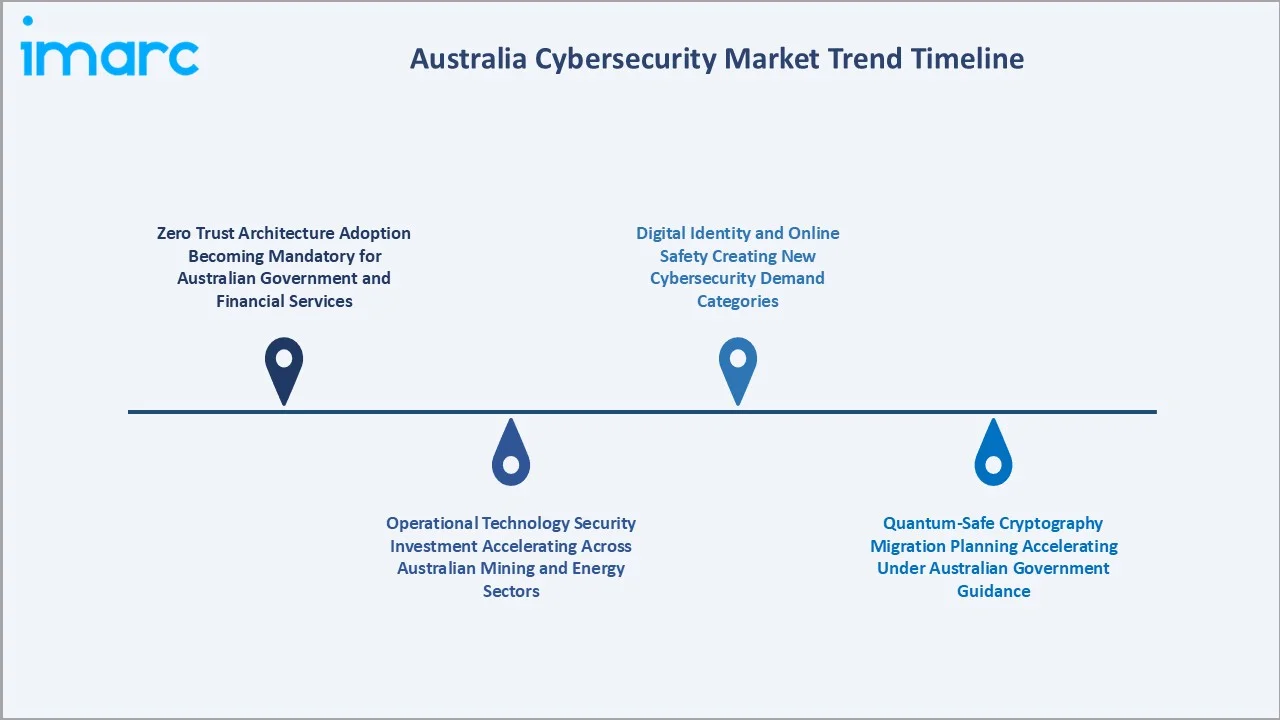

Emerging Market Trends

1. Zero Trust Architecture Adoption Becoming Mandatory for Australian Government and Financial Services

Zero Trust Architecture is emerging as government agencies and financial institutions move away from perimeter-based security models. Rising cloud adoption, remote access, identity-based attacks, and sensitive data exposure are pushing organizations to verify every user, device, and application before granting access. This is increasing demand for identity and access management, multi-factor authentication, endpoint security, micro-segmentation, and continuous monitoring solutions.

2. Operational Technology Security Investment Accelerating Across Australian Mining and Energy Sectors

Operational technology security investment is emerging as mining and energy companies strengthen protection for industrial control systems, connected assets, and remote operational sites. By the end of 2029, Microsoft plans to invest A$25 billion in Australia’s digital infrastructure, while also strengthening national cyber defence capabilities and workforce training initiatives. The investment will expand Microsoft’s Azure AI supercomputing and cloud capacity in Australia, support collaboration with the Australian AI Safety Institute, extend the Microsoft-ASD Cyber-Shield to more government agencies, enhance national resilience efforts with the Department of Home Affairs, and provide AI-ready skills training to three million Australians.

3. Quantum-Safe Cryptography Migration Planning Accelerating Under Australian Government Guidance

Quantum-safe cryptography migration is emerging as government guidance encourages organizations to prepare for future quantum computing risks. Public agencies, financial institutions, telecom operators, and critical infrastructure firms are beginning to assess vulnerable encryption systems and plan upgrades to post-quantum cryptographic standards. This is driving demand for cryptographic asset discovery, risk assessment, secure key management, and long-term data protection solutions.

4. Digital Identity and Online Safety Creating New Cybersecurity Demand Categories

Digital identity and online safety are emerging as government and enterprises strengthen user verification, fraud prevention, and secure access to digital services. Rising use of digital IDs, online banking, e-government platforms, and child/user safety frameworks is creating demand for identity proofing, authentication, privacy protection, content security, and anti-fraud solutions. This is expanding cybersecurity spending beyond traditional network protection into trust, safety, and secure digital participation.

Industry Value Chain Analysis

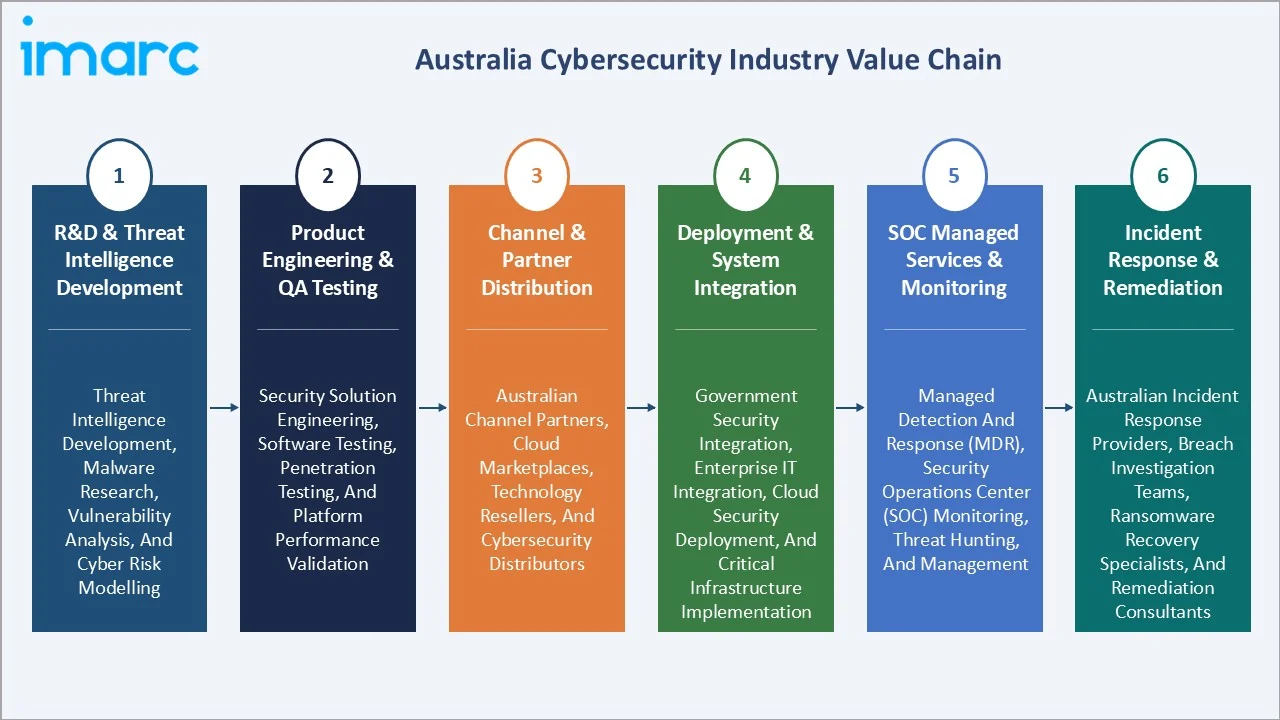

The Australia cybersecurity value chain integrates R&D and threat intelligence development, product engineering and quality assurance testing, channel and partner distribution, deployment and system integration, SOC managed services and monitoring, and incident response and remediation. The value chain's commercial structure reflects Australia's position as a market that primarily consumes imported security technology while adding local value through system integration, managed services, and specialist Australian sovereign capability.

|

Stage |

Key Participants |

|

R&D & Threat Intelligence Development |

Threat intelligence development, malware research, vulnerability analysis, and cyber risk modelling |

|

Product Engineering & QA Testing |

Security solution engineering, software testing, penetration testing, and platform performance validation |

|

Channel & Partner Distribution |

Australian channel partners, cloud marketplaces, technology resellers, and cybersecurity distributors |

|

Deployment & System Integration |

Government security integration, enterprise IT integration, cloud security deployment, and critical infrastructure implementation |

|

SOC Managed Services & Monitoring |

Managed Detection and Response (MDR), Security Operations Center (SOC) monitoring, threat hunting, and management |

|

Incident Response & Remediation |

Australian incident response providers, breach investigation teams, ransomware recovery specialists, and remediation consultants |

The incident response and remediation tier represents the most commercially urgent value chain component. The mandatory incident reporting timelines have accelerated demand for incident response retainer agreements that are now standard procurement practice.

Technology Landscape in the Australia Cybersecurity Industry

Endpoint Detection and Response and Extended Detection and Response

Endpoint Detection and Response (EDR) and Extended Detection and Response (XDR) are enabling faster detection, investigation, and response across endpoints, networks, cloud workloads, and user activity. As ransomware, phishing, and advanced persistent threats increase, enterprises are adopting EDR/XDR platforms to improve visibility and reduce response time. These tools are also supporting AI-led threat analytics, automated incident response, and integrated SOC operations across Australian organizations.

SIEM and Security Operations Center Technology

SIEM and security operations center technologies are centralizing threat detection, log management, and real-time monitoring across enterprise IT environments. As cyberattacks become more frequent and complex, Australian organizations are adopting SIEM platforms and SOC capabilities to improve visibility, compliance, and incident response. In May 2026, Infosys launched its Global Security Operations Center (GSOC) in Australia, based at its North Sydney office, expanding cybersecurity service delivery across Australia and New Zealand.

Cloud Security Posture Management and Cloud-Native Security

Cloud security posture management and cloud-native security are shaping the market as enterprises move workloads, applications, and sensitive data into multi-cloud and hybrid environments. These tools help identify misconfigurations, compliance gaps, identity risks, and exposed assets before they lead to breaches. Rising cloud adoption across government, BFSI, healthcare, and critical infrastructure is driving demand for automated cloud monitoring, workload protection, container security, and continuous risk management. In April 2024, Aqua Security launched the SaaS version of its Aqua Cloud Security Platform for the Australia region, enabling customers to access cloud-native security with local data sovereignty, stronger platform protection, and flexible deployment. The platform helps organizations prevent cloud-native attacks before they occur and stop active threats in real time.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solutions |

58.4% |

2025 |

|

Deployment Type |

Cloud-based |

54.7% |

2025 |

|

User Type |

🔒 |

🔒 |

2025 |

|

Industry Vertical |

🔒 |

🔒 |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

32.8% |

2025 |

By Component

Solutions lead at 58.4% market share (2025). Solutions encompass the full range of cybersecurity technology platforms deployed across Australian organisations: network security, endpoint security, identity security, cloud security, data security, application security, SIEM and security analytics, and OT/ICS security.

To access detailed market analysis, Request Sample

Services at 41.6% encompasses managed security services, professional services, and incident response services. Services' substantial share reflects Australia's cybersecurity skills shortage, driving managed service adoption.

By Deployment Type

Cloud-based leads at 54.7% market share (2025). Cloud-based deployment encompasses SaaS security platforms, cloud-delivered security services, and security tools deployed within cloud environments.

On-premises at 45.3% remains significant for classified government networks, core banking and payment infrastructure, OT/ICS security, and on-premises SIEM for organisations with legacy investments requiring multi-year migration periods.

Regional Market Insights

|

Region |

Share (2025) |

Key Cybersecurity Market Drivers & Characteristics |

|

Australian Capital Territory & New South Wales |

32.8% |

Driven by strong government, defense, financial services, cloud, and enterprise security demand. |

|

Victoria & Tasmania |

24.6% |

Supported by Melbourne’s financial, corporate, healthcare, and technology ecosystem, driving demand for data protection and managed security services. |

|

Queensland |

17.3% |

Driven by its diversified economy, expanding digital infrastructure, public sector modernization, and growing protection needs across healthcare, education, and utilities. |

|

Northern Territory & Southern Australia |

11.2% |

Benefits from defense activity, critical infrastructure protection, space and advanced technology initiatives, and rising sovereign cyber capability investment. |

|

Western Australia |

14.1% |

Western Australia’s cybersecurity demand is strongly linked to mining, resources, energy, and industrial operations, where security, remote asset protection, and operational resilience are key priorities. |

ACT and NSW at 32.8% is the market's dominant region through federal government technology investment and Sydney's financial services concentration. Victoria and Tasmania, at 24.6%, reflect Melbourne's financial, utilities, and manufacturing security investment alongside Victoria's state digital government initiatives.

Queensland, at 17.3%, is growing through healthcare digitisation and Queensland's resources sector. Western Australia, at 14.1%, reflects the mining sector's extensive OT/ICS security investment driven by the digital transformation of remote mining operations. NT and South Australia, at 11.2%, are anchored by defence capability, national security infrastructure, and South Australia's defence industrial base.

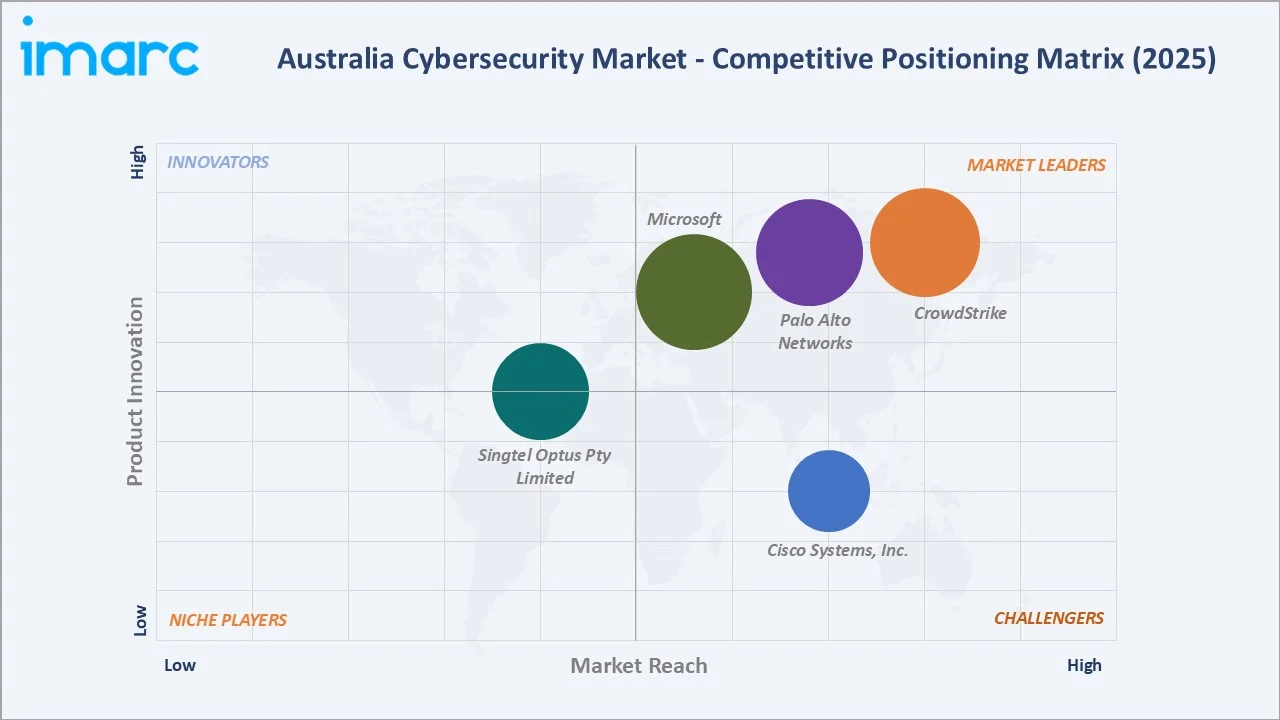

Competitive Landscape

The Australian cybersecurity competitive landscape is structured around three tiers: global technology leaders with IRAP-assessed platforms and dedicated Australian offices, carrier and managed service providers with Australian network infrastructure creating unique delivery advantages, and defence and sovereign capability specialists with government clearances.

|

Company Name |

Key Platforms |

Market Position |

Core Strength |

|

CrowdStrike |

Endpoint Security, Charlotte AI, Falcon platform |

Market Leader |

CrowdStrike helps protect customers from modern cyber threats by securing key risk areas, including endpoints, cloud workloads, identity systems, and data, enabling organizations to stay ahead of attackers and prevent breaches. |

|

Palo Alto Networks |

Idira, Strata, Cortex |

Market Leader |

Palo Alto Networks’ revenue benefits from its cybersecurity platforms, as they enable faster partner integration and support the deployment of new applications, technologies, and data streams. |

|

Microsoft |

Microsoft Defender, Microsoft Sentinel, Microsoft Entra, Microsoft Purview |

Market Leader |

Microsoft Security solutions are designed around Zero Trust principles, helping organizations tackle modern security challenges with confidence. |

|

Cisco Systems, Inc. |

Cisco Hypershield, Cisco Duo, Cisco XDR, Cisco Secure Access (SSE) |

Strong Challenger |

Cisco is collaborating with leading Australian universities to identify common cyber threats and develop practical security solutions for critical infrastructure operators. |

|

Singtel Optus Pty Limited |

Optus |

Established Player |

Optus partners with cybersecurity leaders and works closely with industry stakeholders to stay ahead of evolving threats and strengthen collective cyber protection capabilities |

The competitive landscape's defining dynamic is IRAP assessment status as a government procurement differentiator. The time and cost of IRAP assessment create a competitive moat for assessed vendors that deters new market entrants.

Key Company Profiles

CrowdStrike

CrowdStrike is the dominant endpoint security and platform vendor in the Australian cybersecurity market. The company helps protect customers from modern cyber threats by securing key risk areas, including endpoints, cloud workloads, identity systems, and data, enabling organizations to stay ahead of attackers and prevent breaches.

- Platforms: Endpoint Security, Charlotte AI, Falcon platform.

- Recent Developments: In May 2025, CrowdStrike and Australia’s Academic and Research Network (AARNet) expanded their partnership to offer CrowdStrike Falcon Complete Next-Gen MDR as a managed service for Australia’s research and education sector. The service will deliver round-the-clock managed detection and response, using CrowdStrike’s Falcon Complete for Service Providers platform and AARNet’s delivery capabilities to protect institutions from advanced cyber threats.

- Strategic Focus: To expand AI-powered endpoint, identity, cloud, and managed detection and response solutions across enterprises, education, government, and critical infrastructure sectors.

Palo Alto Networks

Palo Alto Networks is the Australia cybersecurity market's broadest enterprise platform vendor. Palo Alto Networks' three-platform strategy, Strata (network security), Idira, and Cortex (AI-driven security operations), positions the company as a key player.

- Platforms: Idira, Strata, Cortex.

- Recent Developments: In May 2026, Palo Alto Networks launched Idira, a next-generation identity security platform designed to discover, manage, and govern all types of identities, removing silos that leave organizations vulnerable. The platform enhances capabilities for existing CyberArk customers and the wider industry by offering modern privileged access management (PAM) with agentic functionality, enabling organizations to apply dynamic privilege controls across human, machine, and agentic identities.

- Strategic Focus: To strengthen cloud, network, AI-driven, and security solutions for enterprises, government, and critical infrastructure operators.

Market Concentration Analysis

The Australian cybersecurity market is moderately concentrated, with the top 5 vendors collectively holding an estimated 45-55% of total market revenue. Microsoft's unique position as both a dominant productivity platform and security platform creates an installed base advantage no pure-play cybersecurity vendor can match. Concentration is highest in endpoint security and government SIEM.

Market concentration is declining in the services segment, where Australia's managed security market supports 50+ independent MSSPs and a deep consulting firm ecosystem. Australian MSSP market consolidation has been occurring through M&A. Market concentration dynamics are reshaping as vendor platform consolidation progressively reduces the viability of independent point-product security vendors in the Australian enterprise market.

Investment & Growth Opportunities

Highest Growth Segments

Cloud-based deployment (~11.2% CAGR), solutions component (~10.4% CAGR), OT/ICS security for mining and energy (~15-18% CAGR from growing base), AI-native security operations platforms (~20-25% CAGR in AI SOC segment), healthcare SOCI Act compliance security (~15-20% CAGR following November 2023 SOCI Act expansion), and Australian sovereign cybersecurity capability development (~15%+ CAGR through government strategy investment) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Australia's SME cybersecurity market represents the largest underserved segment, with Australian SMEs, of which the majority lack meaningful cybersecurity investment. The government-funded programs are seeding SME security awareness, but the commercially accessible managed security product for Australian SMEs is a growing addressable segment that providers like emerging fintech-style SME security companies are developing.

Investment Themes

- Quantum-safe cryptography migration services for Australian financial services and government: The advisory on quantum-safe cryptography migration and standard finalisation has initiated the first commercial procurement cycle for quantum-safe cryptography assessment and migration services. Australian banks and superannuation funds collectively managing AUD 3.5+ Trillion in assets are prioritising quantum-safe cryptographic migration as a 5-10 year program starting with cryptographic inventory, migration completion, and infrastructure readiness for post-quantum algorithms.

- Cyber capability investment through Australian sovereign defence industry: Australian defence industry companies with existing security clearances and registration are positioned for cyber capability development contracts. The technology transfer provisions allowing Australian companies to access US and UK classified cybersecurity technology for domestic development create a pathway for Australian sovereign cybersecurity capability that could generate exportable products to partners, creating commercial value beyond Australian domestic market procurement.

Future Market Outlook (2026-2034)

The Australia cybersecurity market is projected to grow from USD 8.46 Billion in 2025 to USD 20.46 Billion by 2034, delivering a 10.00% CAGR over the forecast period. The market's anchor value of USD 13.63 Billion in 2030 represents an Australian cybersecurity industry at a maturation inflection point. Australia's aspiration to be the world's most cyber-secure country by 2030, articulated in the 2023-2030 Cyber Security Strategy, will not be fully achieved by 2030, but will have established Australia as demonstrably among the top-5 most cyber-secure nations globally based on the measurable improvements in compliance rates, critical infrastructure resilience, and cybercrime reporting outcomes.

Three structural forces define Australian cybersecurity market growth through 2034. The geopolitical force creates a permanent national security imperative for cybersecurity investment that is above and beyond purely commercial risk management. The regulatory ratchet creates an iterative compliance demand escalator that sustainably increases minimum cybersecurity investment across Australian organisations. The technology opportunity that creates substantial commercial opportunities for vendors aligned with Australian regulatory and national security requirements.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025), including APAC Regional Directors; Australian Country Managers; Security Practice Partners; SOC Operations Directors; CISO-level executives; ASD-affiliated cybersecurity policy advisors; and ACSC Cyber Uplift program coordinators from the Australian Cyber Security Center.

Secondary Research

Secondary research encompassed ASD ACSC Annual Cyber Threat Report 2023-24; 2023-2030 Australian Cyber Security Strategy; Australian Bureau of Statistics ABS Digital Economy Indicators 2024; AIIA (Australian Information Industry Association) Tech Council cybersecurity industry data; Australia IT Security Market forecast data; individual vendor annual reports. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using top-down national IT security spend modelling combined with bottom-up segment models by component and deployment type. Key inputs include Essential Eight compliance mandates creating minimum security procurement floors for the government sector, critical infrastructure compliance investment modelling for newly regulated sectors, AUKUS program annual cybersecurity investment estimates from Defence funding commitments, and technology refresh cycle timing for quantum-safe cryptography migration.

Australia Cybersecurity Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Types Covered | Cloud-based, On-premises |

| User Types Covered | Large Enterprises, Small and Medium Enterprises |

| Industry Verticals Covered | IT and Telecom, Retail, BFSI, Healthcare, Defense/Government, Manufacturing, Energy, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | CrowdStrike, Palo Alto Networks, Microsoft, Cisco Systems, Inc., Singtel Optus Pty Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia cybersecurity market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia cybersecurity market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia cybersecurity industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Cybersecurity Market Report

The Australia cybersecurity market reached USD 8.46 Billion in 2025, making it one of the Asia-Pacific region's largest cybersecurity markets. Growth is driven by the 2023-2030 Australian Cyber Security Strategy's AUD 586.9 Million government investment, critical infrastructure compliance mandates, escalating state-sponsored threats documented by ASD, cloud adoption accelerating cloud-native security investment, and the breaches catalysing board-level cybersecurity investment elevation across all major Australian organisations.

The market grows at 10.00% CAGR during 2026-2034, reaching USD 20.46 Billion by 2034. The 10% CAGR reflects the compound of regulatory-driven compliance investment, escalating threat environment requiring continuous security capability uplift, AI-native security operations platform adoption creating technology refresh cycles.

Solutions lead at 58.4% through EDR/XDR platforms, SIEM, cloud security, and data security tools driven by compliance requirements. Solutions also grow fastest at ~10.4% CAGR.

Cloud-based leads at 54.7% reflecting certification enabling government cloud security adoption, enterprise cloud migration creating cloud-native security requirements, and SaaS security platform vendor transitions.

ACT and New South Wales lead at 32.8% through federal government cybersecurity investment and Sydney's financial services concentration.

Leading companies include CrowdStrike, Palo Alto Networks, Microsoft, Cisco Systems, Inc., and Singtel Optus Pty Limited, among others.

The market is projected to reach approximately USD 13.63 Billion by 2030, with AI-native SOC becoming standard at Australian enterprises, healthcare compliance investment reaching full scale, cyber capability at program scale, post-quantum cryptography migration planning completing design phase, and the Australian Cyber Security Act mandating smart device minimum security standards, creating a consumer IoT security market.

AI is transforming Australian SOC operations through three primary mechanisms: alert triage automation, threat detection improvement, and automated response orchestration. Banking SOCs are in active AI-enhanced SOC transformation programs.

Three priority opportunities: healthcare SOCI Act compliance, post-quantum cryptography migration services for Australian financial services, and AI-native SOC platform migration from Splunk to cloud-native SIEM.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)