Australia Dairy Alternatives Market Size, Share, Trends and Forecast by Product Type, Source, Formulation, Nutrient, Distribution Channel, and Region, 2026-2034

Australia Dairy Alternatives Market Size and Trends:

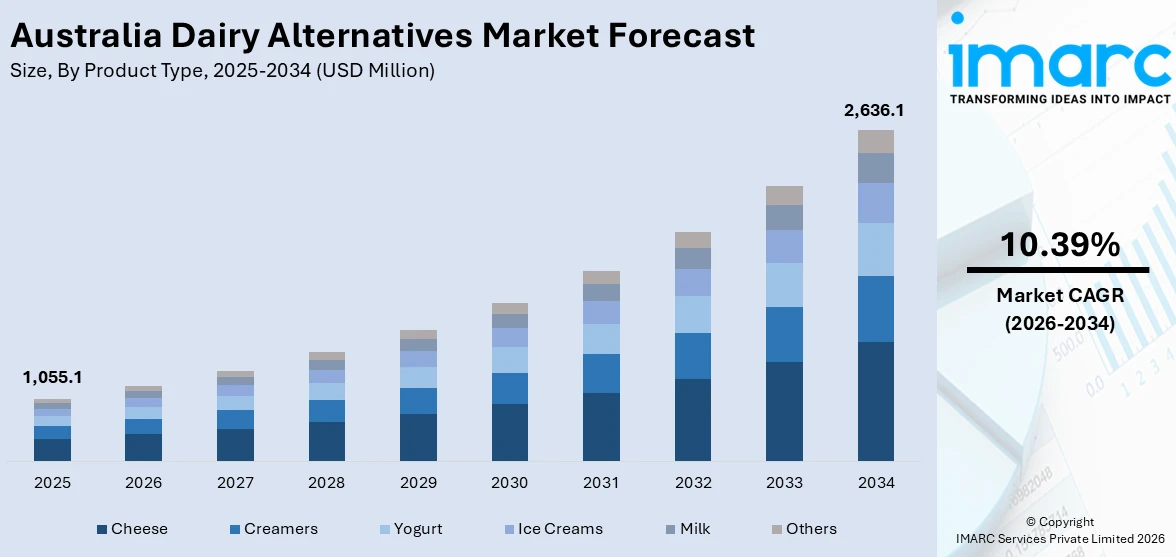

The Australia dairy alternatives market size reached USD 1,055.1 Million in 2025. Looking forward, the market is projected to reach USD 2,636.1 Million by 2034, exhibiting a growth rate (CAGR) of 10.39% during 2026-2034. The market is experiencing rapid growth, stimulated by growing health awareness, higher lactose intolerance, and enhanced popularity of plant-based diets. Soy, almond, oat, and other non-dairy milk types are gaining preference among consumers as they have their perceived health and environmental benefits. Food manufacturers are also widening product lines to keep pace with changing tastes, enhancing demand across channels of food retail and foodservice, and thereby fortifying the Australia dairy alternatives share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,055.1 Million |

| Market Forecast in 2034 | USD 2,636.1 Million |

| Market Growth Rate 2026-2034 | 10.39% |

Key Trends of Australia Dairy Alternatives Market:

Growing Consumer Trend Toward Plant-Based Dairy Alternatives

Australian consumers have increasingly turned to plant-based dairy alternatives because of increasing health awareness and environmental concerns regarding dairy farming. Increasing numbers of individuals are turning to plant-based diets like veganism and flexitarianism, which emphasize minimizing or avoiding animal-based foods. Dairy alternatives like oat, almond, soy, and coconut-based products have emerged as the preferred option for those looking for lactose-free, low-cholesterol, and vegan-friendly alternatives. For example, in July 2024, Sanitarium introduced its PLANTWELL line of superfood-based plant milks in Australia, such as high-protein soy, cholesterol-lowering oat, and immune-boosting almond milk, providing health benefits and targeted nutrients. Furthermore, this shift in consumers is driving the growth of Australia's dairy alternatives market, with plant-based milk and cheese sales increasing consistently. The market growth is also driven by consumer demand for products that meet health and environmental objectives. The future outlook of the Australia dairy alternatives market is optimistic, with market share projected to grow as additional products are created to meet a variety of consumer tastes, such as better flavor and texture.

To get more information on this market Request Sample

Dairy Alternative Product Innovation Advances

The Australian market for dairy alternatives is growing very fast owing to the ongoing innovation in products. Manufacturers are introducing new products that respond to changing tastes and dietary requirements in Australia. For instance, in May 2024, Brownes Dairy introduced its alternative dairy range (oat, almond, and soy) in selected cafes, restaurants, and retailers. This is after three years of R&D, addressing the need for high-quality alternatives. Moreover, oat milk and almond milk plant-based milk alternatives are gaining popularity because of their creaminess and nutritional value, whereas dairy-free cheese is being redesigned to better melt and taste. Besides, fresh categories of new products such as dairy-free yogurts, ice creams, and creams are evolving to accommodate growing demand for plant-based alternatives. Not only do these emerging technologies enhance the palatability and texture of milk substitutes, but also improve nutritional value through fortification to supplement critical nutrients and minerals like vitamin D and calcium. Australia dairy alternatives market share is, therefore, increasing due to these developing technologies. With these developments, the market growth is likely to persist as consumers seek increasingly versatile and palatable plant-based alternatives.

Sustainability and Ethical Consumerism Driving Demand for Dairy Alternatives

Increased concern for sustainability and ethical consumerism is impacting the growth of Australia's dairy alternatives market strongly. With fears related to climate change, deforestation, and animal cruelty, increasingly consumers are adopting plant-based dairy alternatives as a greener and more humane option. The ecological cost of conventional dairy production, with significant water use and greenhouse emissions, has stimulated interest in the production of fewer-resource, plant-based alternatives to these products with associated lower levels of waste. They provide an ecologically superior method of increasing dairy product supplies as demand expands. The push for sustainability, along with increased concerns over the environmental impacts of livestock farming, has led to Australia dairy alternatives market growth. The Australia dairy alternatives proportion within the food and beverage industry as a whole is expected to grow as Australians become more conscious about making ethical and environmentally friendly options.

Growth Drivers of Australia Dairy Alternatives Market:

Rise in Lactose Intolerance and Dairy Allergies

A notable segment of the Australian population deals with lactose intolerance or dairy allergies, leading to a surge in demand for dairy alternative products. This trend is further fueled by increasing consumer awareness about the symptoms and long-term consequences of lactose sensitivity. Plant-based options like almond, soy, and oat milk provide acceptable substitutes that do not sacrifice taste or nutritional benefits. These alternatives have been widely integrated into daily diets, particularly in urban settings. As consumers look for convenient and safe options, brands are broadening their ranges to meet this health-centric demand. The rise of medical endorsements and the influence of wellness advocates promoting dairy-free options are also driving this transformation in the market, enhancing Australia dairy alternatives market demand.

Ethical and Environmental Awareness

Australian consumers are becoming more motivated by ethical considerations and sustainability when choosing food. The ecological footprint of conventional dairy farming including greenhouse gas emissions, water consumption, and land degradation has led many individuals to switch to dairy alternatives. Additionally, heightened awareness surrounding animal welfare and cruelty-free practices is steering consumers towards plant-based products. This movement is especially pronounced among younger age groups, who emphasize eco-friendly consumption. Brands that emphasize transparent sourcing, cruelty-free certifications, and reduced environmental impacts are gaining popularity. As the conversation around sustainability intensifies, the dairy alternatives market continues to benefit from values-driven purchasing habits, positioning it as a responsible and progressive sector in the Australia dairy alternatives market.

Expanded Retail Presence and Strategic Brand Marketing

The increased retail presence of dairy alternatives in mainstream supermarkets, cafés, and online sites is significantly enhancing their adoption in Australia. Leading companies are introducing innovative plant-based products and employing engaging marketing strategies focused on health, taste, and sustainability. Collaborations with influencers, digital marketing campaigns, and attractive packaging are all contributing to heightened consumer awareness and trust. Furthermore, promotional activities and product sampling in stores encourage trial and encourage repeat purchases. As both convenience and accessibility improve, consumers are progressively incorporating dairy alternatives into their shopping routines. According to Australia dairy alternatives market analysis, this broader retail presence and brand-focused outreach are strengthening consumer demand.

Opportunities of Australia Dairy Alternatives Market:

Expansion into Foodservice and Hospitality

The Australian dairy alternatives market is experiencing significant growth driven by the foodservice and hospitality industries. Cafés, quick-service restaurants, and casual dining establishments are increasingly catering to shifting dietary preferences, resulting in growing demand for dairy-free options like almond, oat, and soy milk. Many dining venues now include plant-based milk as a standard offering, influenced by consumer desires for inclusivity and health-driven choices. This transformation presents an opportunity for suppliers to establish B2B partnerships with foodservice entities and broaden distribution beyond traditional retail. Moreover, the rising prevalence of vegan menus and specialized dessert offerings within hospitality settings further enhances market expansion. Strategic collaborations and co-branding efforts may support manufacturers in gaining traction within this rapidly changing segment of the Australian dairy alternatives market.

Private Label and Niche Branding Growth

The trajectory of the Australian dairy alternatives market is being significantly influenced by retailers and emerging startups through the growth of private-label products and niche branding approaches. Supermarkets are launching competitively priced store brands, increasing accessibility for mass consumers seeking dairy-free options. At the same time, niche startups are focusing on specific consumer groups such as those looking for keto-friendly, allergen-free, or organic alternatives garnering interest among health-conscious shoppers. This dual approach encourages innovation and variety while heightening competition within the market. Tailored branding, transparent labeling, and diversified ingredient sourcing enable smaller players to cultivate loyal customer bases. Such advancements are contributing to a thriving ecosystem of unique offerings in the Australian dairy alternatives market.

Functional and Fortified Offerings

Due to escalating health awareness, the Australian dairy alternatives market is progressively leaning towards functional and fortified products. Consumers are looking for plant-based milk and yogurt enriched with nutrients such as protein, calcium, vitamins B12 and D, and gut-healthy probiotics. These added benefits address nutritional deficiencies typically filled by dairy, positioning alternatives as not just substitutes but as superior choices for health-focused individuals. Functional claims such as “supports immunity,” “bone health,” or “high in omega-3” are becoming compelling selling points. Brands that prioritize research and development to create these types of formulations are likely to gain a competitive advantage. This trend reflects a larger movement towards preventive health and performance-oriented nutrition within the Australian dairy alternatives market.

Challenges of Australia Dairy Alternatives Market:

High Price Point Compared to Traditional Dairy

A significant challenge in the Australian dairy alternatives market is the comparatively high cost of plant-based products against conventional dairy. The premium pricing stems from factors such as high raw material costs, specialized processing methods, and lower production scales. This situation poses a barrier to price-sensitive consumers, particularly in budget-conscious households. While increasing demand and economies of scale might eventually reduce prices, current affordability concerns may limit market growth to health-focused or affluent consumer groups. Brands should consider options like value packs, promotional pricing, or mid-tier product offerings to enhance accessibility. Striking a balance between quality, cost, and market positioning is essential for achieving broader acceptance within the Australian dairy alternatives market.

Taste and Texture Limitations

Despite advancements in food technology, the challenge of mimicking the flavor, creaminess, and mouthfeel of traditional dairy products persists for many dairy alternatives. Some consumers feel that plant-based milk, cheese, or yogurt do not provide the rich taste and texture they expect. This sensory shortfall may hinder repeat purchases, especially among mainstream or flexitarian consumers who are accustomed to dairy. As competition grows, taste and texture will be critical factors for differentiation. Ongoing research and development, enhanced emulsification methods, and innovative ingredient combinations could help bridge this gap. Until then, consumer satisfaction may vary, affecting overall retention in the dynamic Australian dairy alternatives market.

Supply Chain Constraints for Key Ingredients

The Australian dairy alternatives market is significantly dependent on imported ingredients such as almonds, soybeans, and oats, which makes the sector susceptible to international supply chain interruptions. Elements like climate change, geopolitical issues, and fluctuating global commodity prices can impact both the availability and cost of raw materials. Furthermore, logistics challenges or tariffs may lead to bottlenecks, particularly for brands lacking diversified sourcing approaches. These supply limitations can result in price volatility, affecting both manufacturers and consumers. Local sourcing efforts, contract farming, and ingredient diversification present potential solutions, albeit requiring long-term planning and investment. Effectively addressing these challenges is vital for ensuring supply stability and maintaining competitiveness in the market.

Australia Dairy Alternatives Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product type, source, formulation, nutrient, and distribution channel.

Product Type Insights:

- Cheese

- Creamers

- Yogurt

- Ice Creams

- Milk

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes cheese, creamers, yogurt, ice creams, milk, and others.

Source Insights:

- Almond

- Soy

- Oats

- Hemp

- Coconut

- Rice

- Others

A detailed breakup and analysis of the market based on the source have also been provided in the report. This includes almond, soy, oats, hemp, coconut, rice, and others.

Formulation Insights:

- Plain

- Sweetened

- Unsweetened

- Flavored

- Sweetened

- Unsweetened

The report has provided a detailed breakup and analysis of the market based on the formulation. This includes plain (sweetened and unsweetened) and flavored (sweetened and unsweetened).

Nutrient Insights:

- Protein

- Starch

- Vitamin

- Others

A detailed breakup and analysis of the market based on the nutrient have also been provided in the report. This includes protein, starch, vitamin, and others.

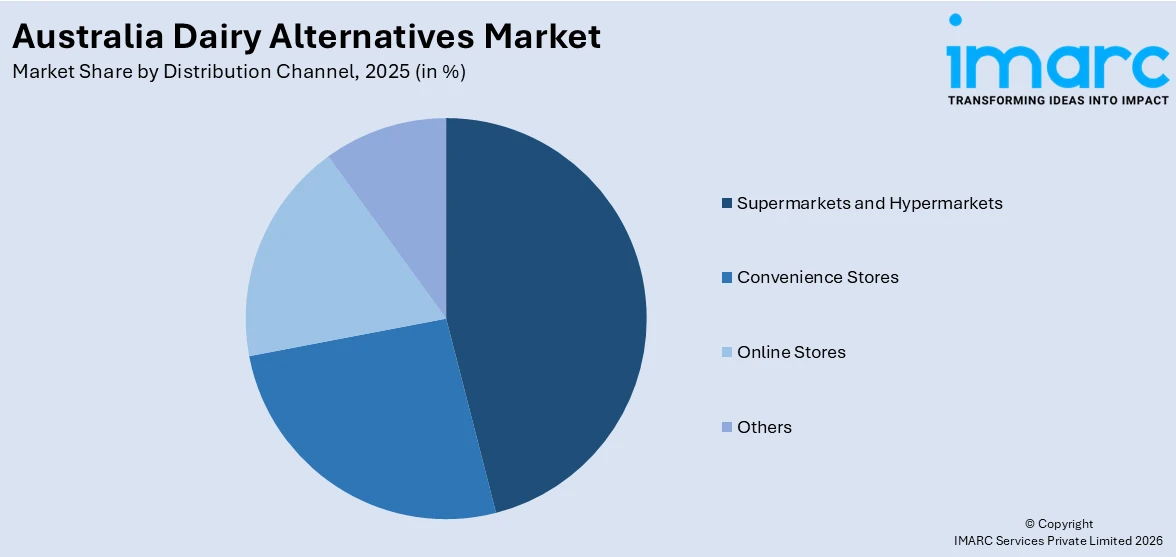

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Convenience Stores

- Online Stores

- Others

The report has provided a detailed breakup and analysis of the market based on the distribution channel. This includes supermarkets and hypermarkets, convenience stores, online stores, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Dairy Alternatives Market News:

- In September 2024, Oatly introduced three new oat drink flavors in Australia—Full, Light, and Low Sugar—to meet the increasing demand for plant-based beverages. The beverages are stocked at Woolworths, providing customers with a variety of options perfect for coffee, baking, and cereals, emphasizing taste, nutrition, and sustainability.

- In April 2024, Dare Iced Coffee has launched two new dairy-free variants, Double Espresso and Mocha, after strong consumer demand. The products are now on shelves at independent supermarkets, Coles, and Woolworths, meeting the growing demand for dairy-free in the iced coffee category of the Australian market.

Australia Dairy Alternatives Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Cheese, Creamers, Yogurt, Ice Creams, Milk, Others |

| Sources Covered | Almond, Soy, Oats, Hemp, Coconut, Rice, Others |

| Formulations Covered |

|

| Nutrients Covered | Protein, Starch, Vitamin, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Convenience Stores, Online Stores, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia dairy alternatives market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia dairy alternatives market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia dairy alternatives industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Dairy Alternatives Market Report

The dairy alternatives market in Australia was valued at USD 1,055.1 Million in 2025.

The Australia dairy alternatives market is projected to exhibit a compound annual growth rate (CAGR) of 10.39% during 2026-2034.

The Australia dairy alternatives market is expected to reach a value of USD 2,636.1 Million by 2034.

The Australia dairy alternatives market is witnessing trends such as innovation in plant-based product formulations, increased demand for barista-style non-dairy milk, and the rise of oat and pea-based offerings. Clean-label preferences and premium packaging are also influencing consumer choices across multiple retail segments.

Key growth drivers include rising health consciousness, increasing vegan and flexitarian lifestyles, and strong retail support through expanded shelf space. Government-backed sustainability initiatives and growing food intolerances among consumers are further accelerating the shift toward dairy-free beverages and food products across the Australian market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)