Australia Data Center Construction Market Size, Share, Trends and Forecast by Construction Type, Data Center Type, Tier Standards, Vertical, and Region, 2026-2034

Australia Data Center Construction Market Size & Forecast 2026-2034

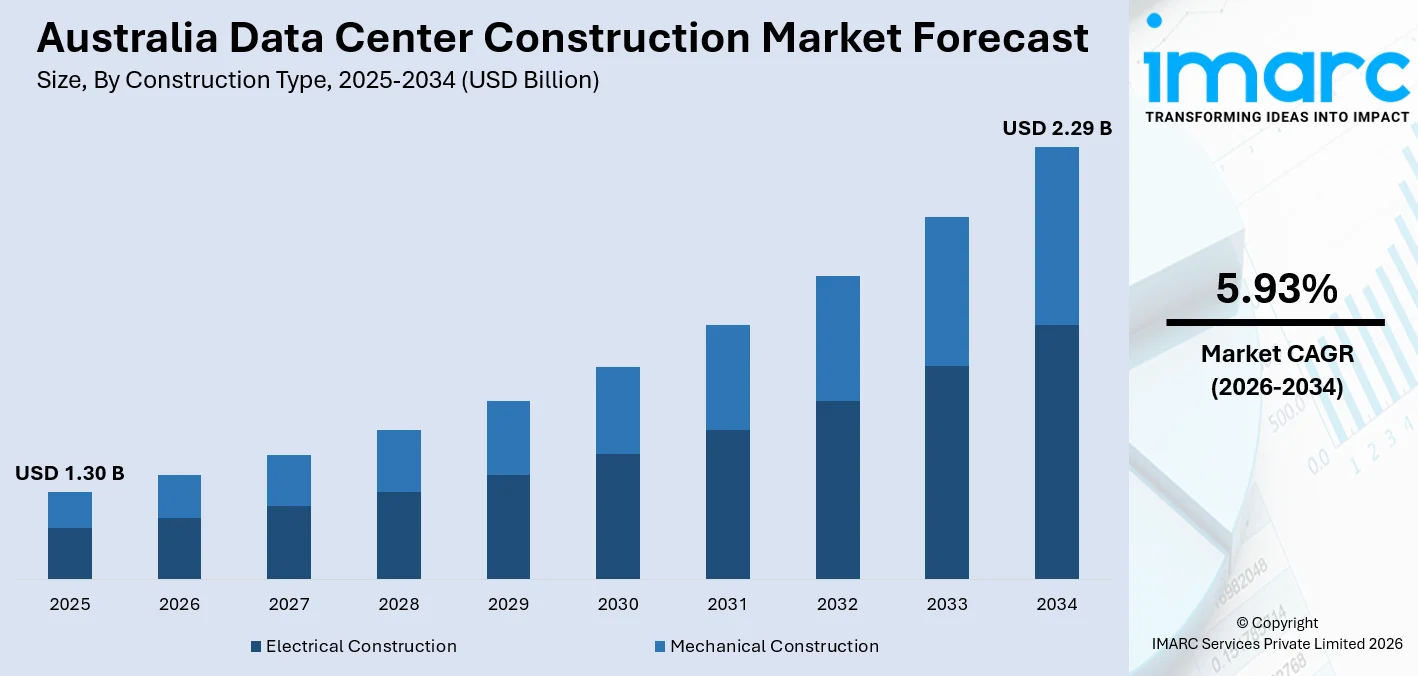

The Australia data center construction market size, valued at USD 1.30 Billion in 2025, is projected to reach USD 2.29 Billion by 2034, growing at a CAGR of 5.93% from 2026-2034. Australia's total occupancy expanded from 37 MW in 2005 to 1.3 GW in 2025, a forty-fold increase, driven by rapid enterprise cloud migration, the surge in AI workloads demanding purpose-built high-density facilities, and landmark hyperscaler commitments. Electrical systems, modular power designs, and liquid-cooling integration are redefining construction economics, while sovereign data requirements and the Security of Critical Infrastructure Act are reinforcing demand for locally built, certified capacity across the Australia data center construction market.

To get more information on this market Request Sample

Australia Data Center Construction Industry Analysis - Key Insights

- Electrical construction commands 55.7% by construction type in 2025- the clear majority, because power infrastructure is where the real money goes. Rack densities pushing from 10 kW toward 100 kW per rack for AI workloads mean UPS systems, high-voltage switchgear, and intelligent PDUs now dominate project budgets before a single cooling unit is specified.

- Large data centers lead at 44.3% by data center type in 2025- driven almost entirely by hyperscaler self-builds and wholesale colocation campuses.

- Tier III holds 46.8% by tier standards in 2025- the rational choice for cloud operators and enterprise tenants alike. Concurrent maintainability without a full fault-tolerance price premium hits the sweet spot between uptime requirements and construction cost, and it is what most of Australia's 145 colocation data centers are built to.

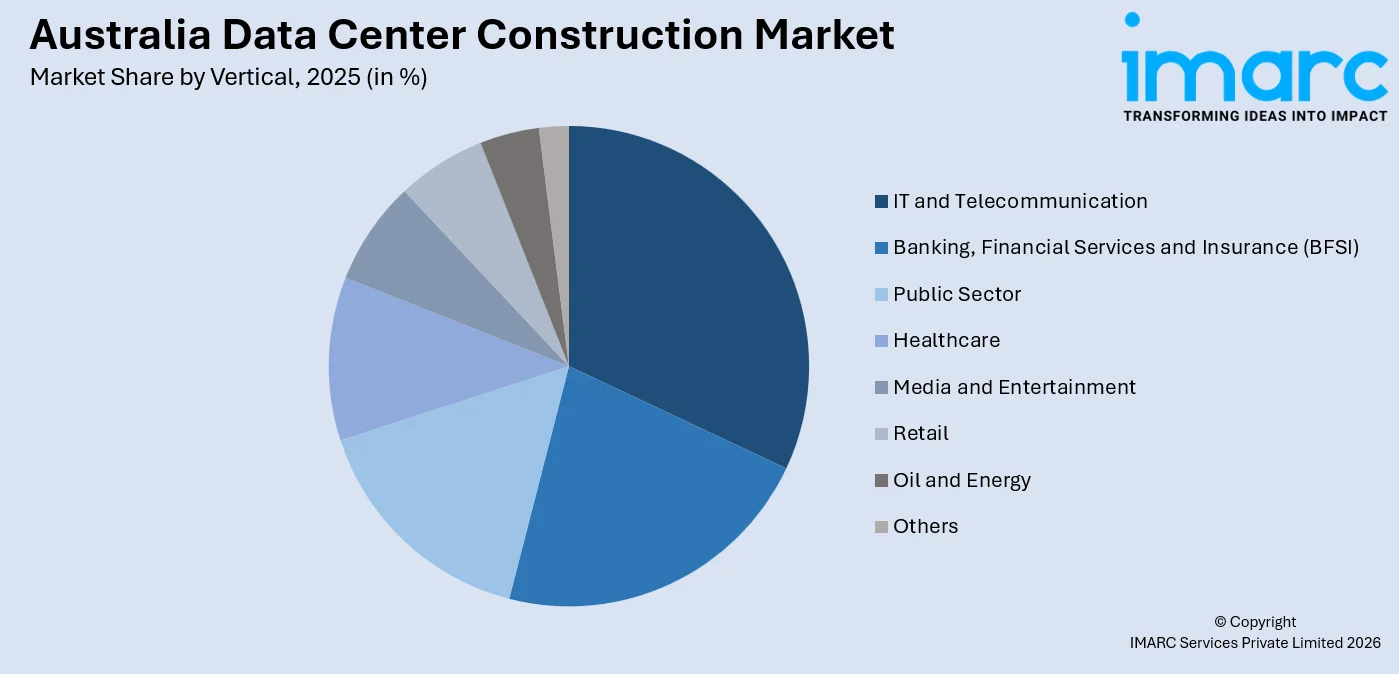

- IT and telecommunication lead vertical at 31.9% in 2025- not surprising given that the three biggest demand sources, AWS, Microsoft Azure, and Google Cloud, all sit in this category. Telcos are also expanding edge nodes to support 5G backhaul and latency-sensitive enterprise applications across metro and regional areas.

- Australia Capital Territory & New South Wales dominates regionally at 37.4% in 2025- the highest geographic concentration, anchored by Sydney's density of hyperscale campuses, subsea cable landings, and the ACT's sovereign government workload facilities.

Australia Data Center Construction Market Trends and Dynamics 2026

Market Trends

AI workloads are fundamentally reshaping what a data center needs to be built like

The shift from conventional enterprise IT toward AI training and inference is hitting construction specifications hard. Rack power densities that once sat at 5-10 kW are now routinely specified at 30-60 kW, requiring electrical infrastructure, bus ducts, UPS arrays, and medium-voltage switchgear to be redesigned from the ground up.

Modular and prefabricated construction methods are becoming the industry standard

Speed-to-market becomes the defining competitive variable, and modular construction is the answer. In January 2024, Delta Electronics installed 12 prefabricated Power Train Units (PTUs) for an Australian hyperscale facility, demonstrating how factory-built, high-efficiency UPS and water-cooled direct expansion units can compress field deployment timelines by months. The Australia data center construction market trends are pointing unambiguously toward prefab power rooms, containerized cooling skids, and modular data halls that let operators expand in incremental phases without idling capital in unoccupied capacity.

Sustainability mandates are driving a complete rethink of cooling and energy architecture

The Australian government's PUE target of 1.3 data centers turned energy efficiency from an aspiration into a construction requirement. Data centers in Australia already consume around 5% of national electricity generation, a figure projected to reach 8% by 2030, which is forcing operators to source renewables before they break ground, not after. Liquid cooling, rear-door heat exchangers, and direct-to-chip cooling are now specification defaults on any facility designed to carry GPU workloads.

- Hyperscaler Self-Build Acceleration: AWS, Microsoft, and Google are bypassing colocation entirely for large campuses, financing dedicated grid spurs and take-or-pay generation.

- SOCI Act Compliance Driving Tier Upgrades: The Security of Critical Infrastructure Act's mandatory risk-management programs for facilities above 25 MW are accelerating Tier III and Tier IV certifications across both government and commercial builds.

- Liquid Cooling Integration at Scale: Immersion cooling and cold-plate systems are transitioning from pilots to standard specifications on new hyperscale halls.

Growth Drivers

Landmark hyperscaler investment commitments are creating a multi-year construction pipeline

The scale of capital flowing into Australian data center construction is without precedent. Amazon is committed to invest AUD 20 billion by 2029 to expand data center infrastructure, the largest technology investment in the nation's history. Microsoft committed AUD 5 billion to expand its local data center footprint from 20 to 29 centers across Sydney, Melbourne, and Canberra. These commitments alone are anchoring a construction pipeline that extends well beyond 2030, directly reinforcing Australia data center construction market growth across electrical, mechanical, and general construction sub-segments.

Enterprise cloud migration is generating sustained, broad-based construction demand

Over 80% of Australian businesses are either already using or planning to migrate to cloud-based platforms within the next two years. Federal technology allocations are generating predictable, recurring demand for data center capacity that extends across BFSI, government, healthcare, and telecommunications verticals. Every enterprise migrating from on-premises infrastructure to cloud or hybrid architecture becomes a demand driver for colocation or hyperscale build-out.

Australia's connectivity infrastructure and sovereign data requirements are creating structural demand

The SOCI Act and government cloud-hosting security requirements are driving agencies to build or lease locally certified, sovereign facilities, a demand channel that CDC Data Centers and Macquarie Data Centers are specifically positioned to serve.

- AI and GPU Infrastructure Demand: Generating AI adoption could contribute up to AUD 600 billion annually to Australia's GDP by 2030, and every dollar of AI infrastructure requires high-density electrical and cooling construction that conventional data halls cannot support.

- Renewable Energy Zone Development: AEMO's Renewable Energy Zone transmission build-outs are improving data center access to clean power sources in regional corridors, enabling operators to meet 100% renewable targets that are now prerequisites for major hyperscaler tenancy agreements.

- Institutional Capital Inflows: Blackstone's AUD 24 billion acquisition of AirTrunk in September 2024 and Partners Group investment up to AUD 1.2 billion to develop GreenSquareDC into a state-of-the-art data center platform in Australia.

Market Restraints

Grid connection delays and power supply constraints: Securing a grid connection for a new data center in Sydney or Melbourne can take as long as two to three years, as transmission projects queue behind long-lead transformer deliveries and substation upgrades that lag well behind site acquisition timelines. Operators with balance-sheet strength can finance dedicated grid spurs or co-locate near grid infrastructure, but mid-tier developers without that capacity face meaningful schedule and financial exposure that can derail project economics entirely.

Land scarcity and planning complexity in major metros: Urban land pricing in western Sydney corridors risen sharply in recent years, eroding returns on speculative builds and making smaller operators increasingly uncompetitive against hyperscalers who can absorb higher land costs within larger project economics.

Construction cost inflation and long-lead equipment shortages: Electrical construction costs are being squeezed from multiple directions simultaneously, copper prices at decade highs are inflating bus-duct and cable costs, IGBT inverter stacks face extended lead times due to semiconductor supply constraints, and a persistent skilled electrician shortage is forcing labour costs upward. The Australian Energy Regulator's reporting on grid capex increases has signalled broader pressure on switchgear and high-voltage cabling procurement across the country, making project cost estimation considerably harder for developers planning multi-phase campuses.

Australia Data Center Construction Market Segmentation Analysis

| Segment | Leading Category | Market Share | Year |

|---|---|---|---|

|

Construction Type |

Electrical Construction |

55.7% |

2025 |

|

Data Center Type |

Large Data Centers |

44.3% |

2025 |

|

Tier Standards |

Tier III |

46.8% |

2025 |

|

Vertical |

IT and Telecommunication |

31.9% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

37.4% |

2025 |

Construction Type Insights

Electrical Construction - 55.7% market share (2025) | Leading Construction Type

Electrical construction dominates the market. Every megawatt of IT load added to the grid requires an equivalent, often larger investment in UPS systems, medium-voltage switchgear, automatic transfer switches, and power distribution units. Modular medium-voltage skids introduced by Siemens in December 2025 aim to reduce field labor, directly addressing both the electrician shortage and schedule pressure.

|

Segment Breakdown Electrical Construction (55.7%) · Mechanical Construction |

Data Center Type Insights

Large Data Centers - 44.3% market share (2025) | Leading Data Center Type

Large data centers, the hyperscale-grade campuses and large-scale colocation facilities that underpin cloud infrastructure dominate Australia's construction activity because that is where virtually all the major capital is going. In December 2025, NEXTDC Limited agreed a MoU with OpenAI, focusing on developing a next-generation hyperscale AI campus and large-scale GPU supercluster at NEXTDC’s S7 site in Eastern Creek, Sydney, leveraging Australia's strong data center infrastructure and its status as a Five Eyes nation.

|

Segment Breakdown Large Data Centers (44.3%) · Enterprise Data Centers · Mid-Size Data Centers |

Tier Standards Insights

Tier III - 46.8% market share (2025) | Leading Tier Standards

Tier III's dominance comes down to a sensible economic calculation: concurrent maintainability without the full fault-tolerance cost premium of Tier IV. For cloud operators and enterprise tenants who need genuine uptime reliability but cannot justify the capital intensity of dual-powered, fully redundant systems on every circuit, Tier III is the specification that wins. There are over 135 operational colocation data centers in Australia, and most are built to Tier III standards.

|

Segment Breakdown Tier III (46.8%) · Tier IV · Tier I and II |

Vertical Insights

Access the comprehensive market breakdown Request Sample

IT and Telecommunication - 31.9% market share (2025) | Leading Vertical

The IT and telecommunications vertical drives the largest share of construction demand because it encompasses the three biggest buyers of new data center capacity in Australia, AWS, Microsoft Azure, and Google Cloud, alongside Telstra and Optus, who are actively building edge infrastructure for 5G and enterprise latency applications. Telstra received approval for its $700 million joint venture with Accenture to speed up its AI transformation in Australia. The project began in April 2025, generating direct data center construction activity.

|

Segment Breakdown IT and Telecommunication (31.9%) · Banking, Financial Services and Insurance (BFSI) · Public Sector · Healthcare · Media and Entertainment · Retail · Oil and Energy · Others |

Regional Insights

Australia Capital Territory & New South Wales - 37.4% market share (2025) | Leading Region

Australia Capital Territory & New South Wales together form the undisputed center of Australian data center construction activity. Sydney, anchored by subsea cable systems including Southern Cross NEXT and Google's Topaz, is the natural interconnection hub for Asia-Pacific traffic. Macquarie Data Centers began construction of the AUD 350 million IC3 Super West data center in Sydney's Macquarie Park in June 2024, with FDC Construction as the main contractor, a purpose-built AI and high-performance computing facility expected to create over 1,200 jobs and expand total IT load to 63 MW on the campus.

|

Metric

|

Details

|

|---|---|

| Market share in 2025 | 37.4% |

| Key Growth Drivers | Hyperscale campus build-out, subsea cable connectivity, ACT sovereign workload demand, Western Sydney 330 kV grid access |

| Outlook | Dominant regional market, construction pipeline through 2034 |

|

Regional Breakdown Australia Capital Territory & New South Wales (37.4%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia · Western Australia |

Victoria & Tasmania:

Melbourne is the fastest-growing data center market in Australia. In June 2025, Australia's top data center-as-a-service provider announced a $2 billion (AUD) investment to develop M4 Melbourne, a next-generation digital campus located at 127 Todd Road, Port Melbourne. Melbourne's cooler climate meaningfully reduces energy-intensive cooling requirements compared to Sydney, improving PUE performance and making the city attractive for operators prioritising the government's 1.3 or lower PUE mandate. Tasmania's low-cost renewable hydropower is generating early-stage interest for future AI training campuses that require 100% clean energy supply.

|

Metric

|

Details

|

|---|---|

| Key Growth Drivers | Pre-committed pipeline, cooler climate PUE advantage, REZ incentives, hyperscale northern corridor demand |

| Outlook | Fastest-growing market, record construction pipeline |

Queensland:

Brisbane is maturing as Australia's third data center market, moving beyond edge deployments toward mid-scale colocation campuses targeting enterprise and government tenants. Brisbane is at a similar stage of maturation. Queensland's growing population base, warm-weather tourism and retail economy, and expanding healthcare sector are creating diversified vertical demand beyond pure hyperscale.

|

Metric

|

Details

|

|---|---|

| Key Growth Drivers | AWS Local Zone expansion, population growth, enterprise colocation demand, government cloud transformation programs |

| Outlook | Emerging third market, accelerating enterprise demand |

Northern Territory & Southern Australia:

South Australia's data center market is anchored by Adelaide's proximity to renewable energy generation, particularly wind and solar, making it an attractive site for operators committed to 100% renewable power purchase agreements. DCI Data Centers' ADL02 campus in Kidman Park demonstrates the investment appetite: a high-security, 100% renewable-powered facility serving both enterprise and government tenants in a market where competition remains limited and land costs are substantially lower than in Sydney or Melbourne. The Northern Territory contributes limited construction volumes currently, but its strategic proximity to undersea cable routes and its role in Australia's defense infrastructure create a long-term optionality case for sovereign data hosting facilities.

|

Metric

|

Details

|

|---|---|

| Key Growth Drivers | Renewable energy access, lower land costs, government data sovereignty requirements, defense infrastructure adjacency |

| Outlook | Niche market with renewable energy construction opportunity |

Western Australia:

Perth is an emerging data center hub, driven by Western Australia's strong economic base in mining and resources, a growing technology sector, and the state's geographic position as the closest Australian capital to Southeast Asia and South Asian cable landing points. Stack Infrastructure's planned multi-megawatt Perth facility is adding capacity to a market that has historically been underserved relative to the state's economic weight.

|

Metric

|

Details

|

|---|---|

| Key Growth Drivers | Microsoft Azure region launch, mining-sector data demand, Southeast Asia cable proximity, Macquarie Data Centers campus construction |

| Outlook | Emerging market with structural cloud-region demand uplift |

Market Outlook 2026-2034

What is the future outlook of the Australia data center construction market?

The Australia data center construction market is expected to sustain steady revenue growth through 2034.

Australia's deployable data center capacity is projected to more than double from 1,350 MW in 2024 to 3,100 MW by 2030, and every megawatt of that expansion requires electrical, mechanical, and general construction spend. The structural demand drivers are firmly in place: hyperscaler commitments extend to 2029 and beyond, enterprise cloud migration is accelerating, and the government's sovereign data hosting requirements are generating a dedicated construction channel that is insulated from cyclical demand softness. Renewable Energy Zone transmission upgrades, AEMO grid-interactive market mechanisms, and maturing modular construction techniques are progressively improving the build economics. The Australia data center construction market trends toward AI-ready, liquid-cooled, Tier III campus development point to a construction market that will sustain its growth trajectory well beyond 2034, with both public and private sector demand converging on higher-density, higher-specification builds.

Australia Data Center Construction Market - Leading Key Players

Australia's data center construction market brings together hyperscale operators, specialist colocation developers, and global engineering and infrastructure firms that compete on build speed, electrical expertise, renewable energy sourcing, and compliance posture.

| Company | Leading Brands | Highlights |

|---|---|---|

|

NextDC Limited |

Colocation, Data Center Migration and Relocation, Edge Data Centers |

Australia’s premier domestic data center provider with multiple Tier III facilities across key cities; also active in design and build for scalable hyperscale infrastructure. |

|

Macquarie Telecom Group |

Macquarie Telecom Data Center Services & Construction Support | Australian carrier‑neutral data center operator delivering custom build projects, colocation, and managed services with a strong local presence. |

|

PEXA Group |

PEXA Data Center Projects |

Focuses on developing data center infrastructure in Australia, supporting enterprise and government digital transformation needs. |

Some of the other key market players in Australia data center construction market are Telstra, Multiplex (Australia), Amazon, Microsoft, BESIX Watpac, etc.

Latest Development & News

- In December 2025, NEXTDC Limited signed a Memorandum of Understanding (MoU) with OpenAI, allowing Australia to become a regional infrastructure partner under the Open AI for Countries program. The MoU outlines a collaboration between OpenAI and NEXTDC to plan, develop, and operate a next-generation hyperscale AI campus and a large-scale GPU supercluster at NEXTDC's S7 site in Eastern Creek, Sydney.

- In November 2025, Firmus Technologies Pty Ltd. secured $327 million in funding, which includes contributions from Nvidia Corp. and Ellerston Capital, a Sydney-based fund. With this investment, Firmus is valued at $3.9 billion. The company stated that the funds will be used for an infrastructure project called Project Southgate, which aims to build 1.8 gigawatts of data center capacity in Australia by 2028.

- In October 2024, HMC Capital announced major steps to create a global digital infrastructure platform, which will include the DigiCo Infrastructure REIT (DigiCo REIT), aimed to be listed on the ASX, along with a new institutional Unlisted Fund. HMC reached an agreement to acquire 100% of Global Switch Australia for $1.937 billion, a strategic 26MW colocation data center located in Sydney CBD, offering significant growth potential through an extensive development pipeline.

Australia Data Center Construction Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Construction Types Covered | Electrical Construction, Mechanical Construction |

| Data Center Types Covered | Mid-Size Data Centers, Enterprise Data Centers, Large Data Centers |

| Tier Standards Covered | Tier I and II, Tier III, Tier IV |

| Verticals Covered | Public Sector, Oil and Energy, Media and Entertainment, IT and Telecommunication, Banking, Financial Services and Insurance (BFSI), Healthcare, Retail, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia data center construction market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Australia data center construction market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia data center construction industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Data Center Construction Market Report

The Australia data center construction market was valued at USD 1.30 Billion in 2025.

The Australia data center construction market is anticipated to reach a value of USD 2.29 Billion by 2034.

Electrical construction dominates the market with a share of 55.7% in 2025. Power infrastructure, including UPS systems, medium-voltage switchgear, intelligent PDUs, and high-voltage bus ducts, accounts for the majority of project spend as rack densities climb and GPU workloads, with Sydney construction costs reflecting the electrical intensity of these builds.

Large data centers dominate the market with a share of 44.3% in 2025. Hyperscale self-build campuses and large-scale colocation developments from NEXTDC, AirTrunk, and Stack Infrastructure are driving a multi-year construction cycle, which favor purpose-built, large-scale facilities over incremental leasing.

Tier III dominates the market with a share of 46.8% in 2025. Concurrent maintainability without the full cost penalty of Tier IV makes Tier III the specification of choice for cloud operators and enterprise tenants. It is the standard to which most of Australia's 145 operational colocation data centers are built and the primary certification target for new-build facilities entering the market.

IT and telecommunication dominates the market with a share of 31.9% in 2025. Hyperscale cloud providers AWS, Microsoft Azure, and Google Cloud, alongside Telstra and Optus expanding 5G edge infrastructure, collectively represent the largest and most consistent source of new construction demand, supported by Australia's rapidly growing IT services market.

Australia Capital Territory & New South Wales currently leads the market, accounting for a share of 37.4%. Sydney, a natural hub for hyperscale campus development, with 72% of new supply under construction already pre-committed by tenants.

Some of the major players in the market include NextDC Limited, Macquarie Telecom Group, PEXA Group, Telstra, Multiplex (Australia), Amazon, Microsoft, BESIX Watpac, etc.

Key emerging trends include accelerating liquid cooling integration across hyperscale builds as GPU rack densities exceed 80 kW, modular prefabricated construction compressing delivery timelines by up to 30%, SOCI Act compliance driving Tier III and Tier IV certification upgrades, hyperscaler self-build programs bypassing colocation entirely for large campuses, and edge node construction expanding beyond Sydney and Melbourne into Brisbane, Perth, and Adelaide.

The market faces grid connection delays of up to 30 months in major metros as transmission projects queue behind long-lead transformer deliveries, land scarcity and planning restrictions in Sydney and Melbourne that are pushing developers toward costlier brownfield conversions, construction cost inflation driven by elevated copper prices and semiconductor lead time extensions for IGBT components, and a persistent shortage of qualified electrical engineers and HVAC specialists that is inflating labour costs and extending build timelines across the national construction pipeline.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)