Australia Data Center Market Size, Share, Trends and Forecast by Component, Type, Enterprise Size, End User, and Region, 2026-2034

Australia Data Center Market Size, Share, Trends & Forecast (2026-2034)

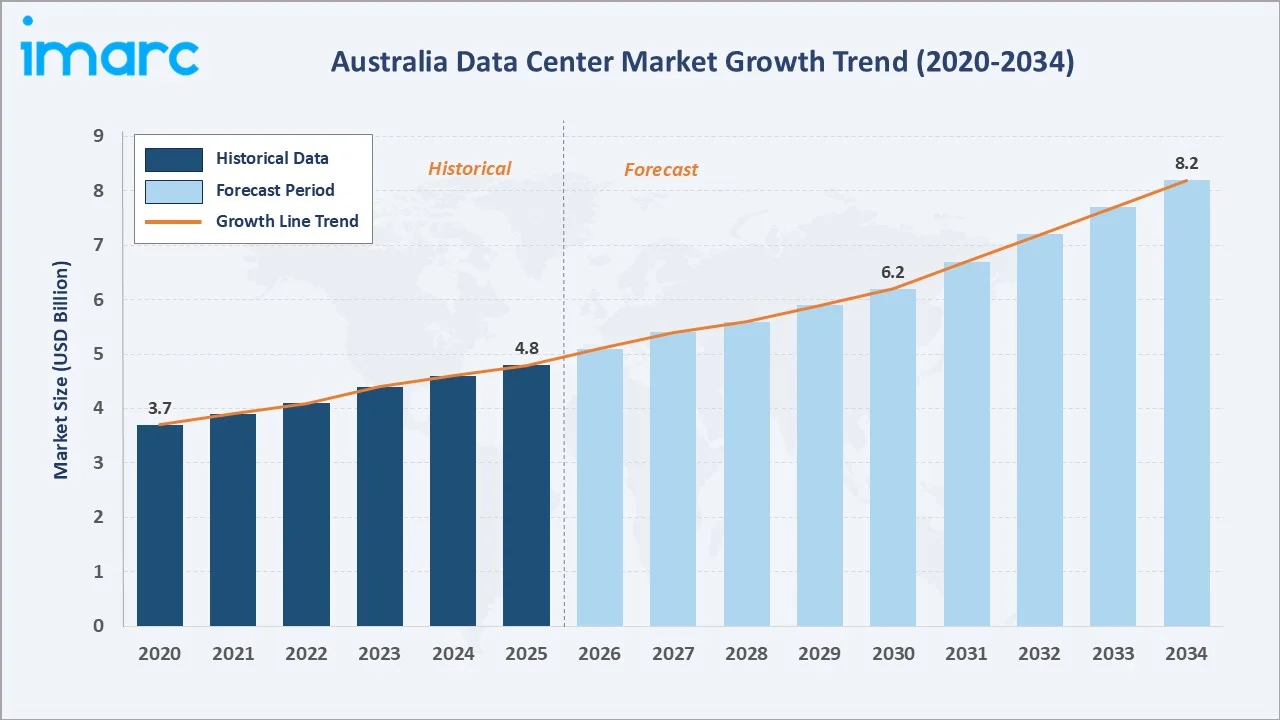

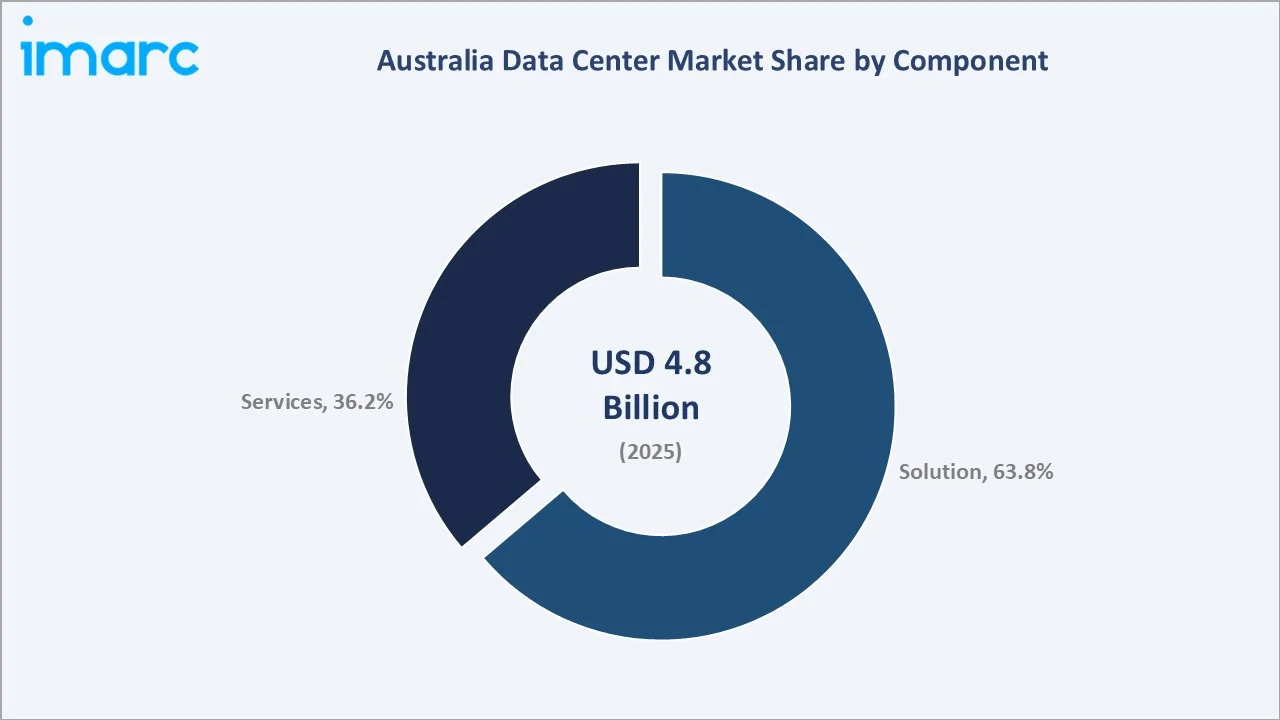

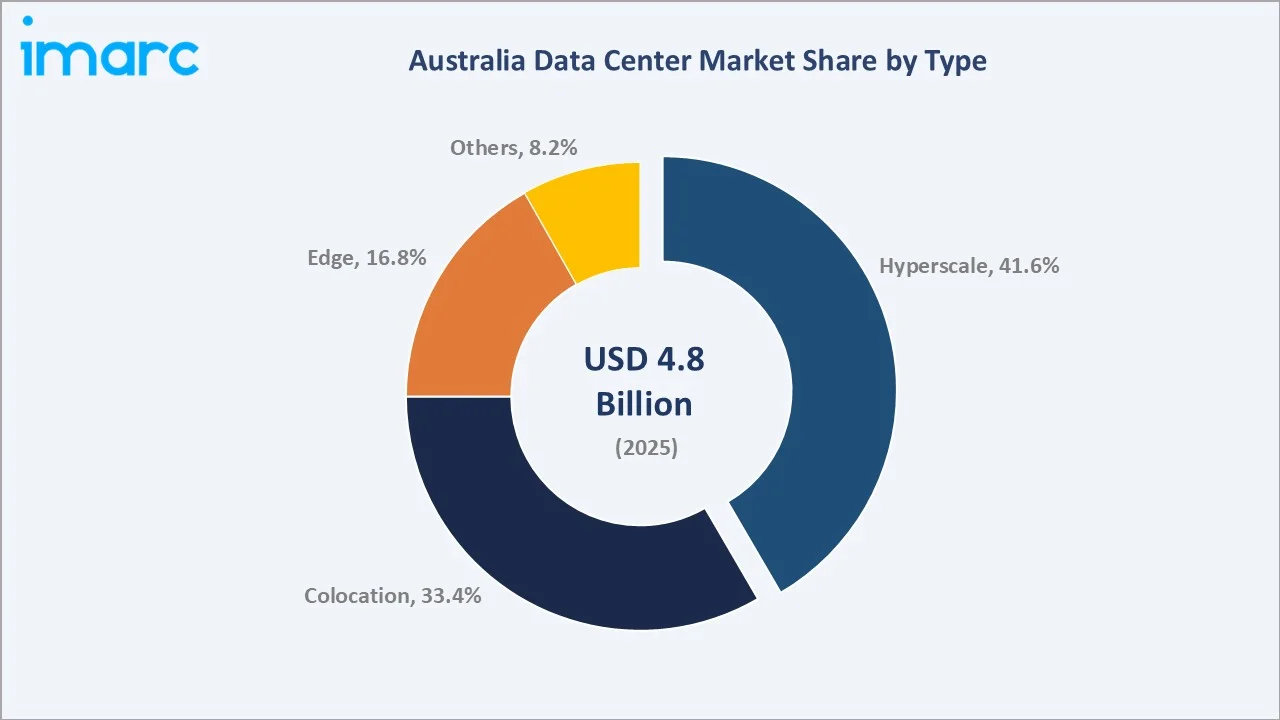

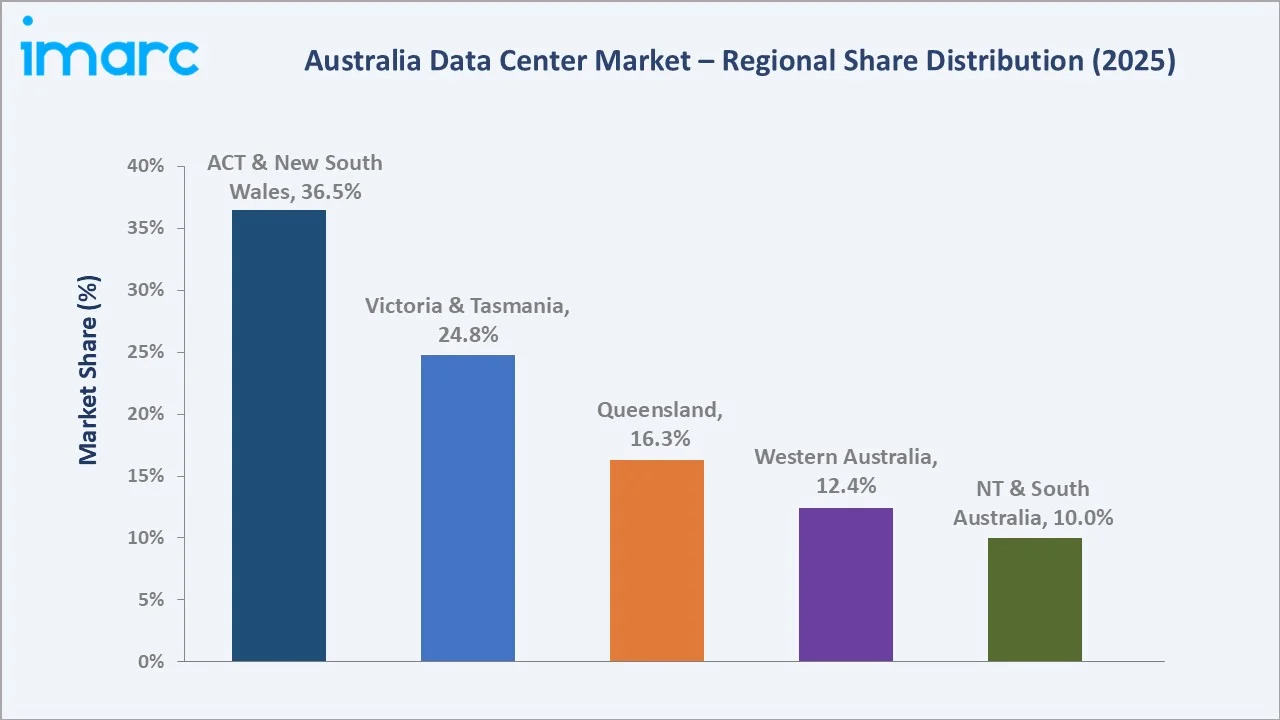

The Australia data center market size was valued at USD 4.8 Billion in 2025 and is projected to reach USD 8.2 Billion by 2034, exhibiting a CAGR of 5.47% during the forecast period 2026-2034. Surging cloud adoption, AI and high-performance computing workloads, 5G network rollout, and government digital sovereignty mandates are key growth enablers. Solution leads component share at 63.8% in 2025, while Hyperscale dominates the type segment at 41.6%. Australian Capital Territory and New South Wales account for 36.5% of national revenue in 2025, anchored by Sydney as the primary east-coast cloud availability zone.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.8 Billion |

|

Forecast Market Size (2034) |

USD 8.2 Billion |

|

CAGR (2026-2034) |

5.47% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Australia Capital Territory & New South Wales (36.5% share, 2025) |

|

Fastest Growing Region |

Queensland (CAGR ~6.8%) |

|

Leading Component |

Solution (63.8%, 2025) |

|

Leading Type |

Hyperscale (41.6%, 2025) |

The chart below tracks the Australia data center market trajectory from 2020 through 2034, contrasting a steady historical expansion base against a sustained forecast curve powered by hyperscale capacity build-out, AI workload demand, and enterprise cloud migration.

To get more information on this market, Request Sample

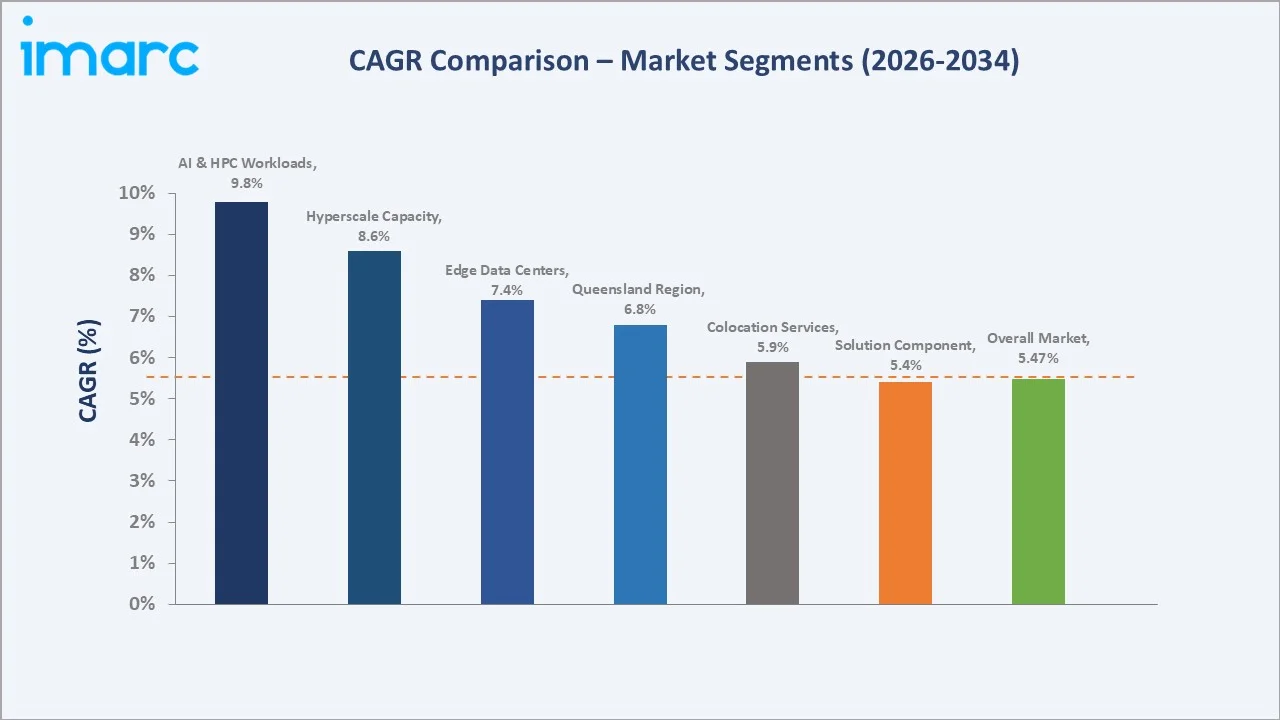

Segment-level CAGR comparisons highlight AI and HPC workloads along with hyperscale capacity as the two fastest-growing sub-categories within the Australia data center industry analysis through 2034.

Executive Summary

The Australia data center market is undergoing rapid expansion driven by the convergence of cloud computing, artificial intelligence, and digital sovereignty mandates. Valued at USD 4.8 Billion in 2025, the market is forecast to reach USD 8.2 Billion by 2034 at a CAGR of 5.47%. AirTrunk's AUD 24 Billion acquisition by Blackstone in 2024 underscored the scale of investor appetite for Australian hyperscale capacity.

Solution commands the dominant component share at 63.8% in 2025, supported by demand for server, storage, and network hardware across hyperscale and colocation deployments. Services follow at 36.2%, lifted by managed hosting, consulting, and integration revenues. Within type, Hyperscale leads at 41.6% in 2025, reflecting AWS, Microsoft Azure, and Google Cloud regional expansion.

Australian Capital Territory and New South Wales dominate with a 36.5% share in 2025, led by Sydney's position as the country's largest cloud availability zone. Victoria and Tasmania holds 24.8% and Queensland 16.3%, both shaped by rapid enterprise cloud migration and emerging edge computing deployments supporting regional digital services.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Solution - 63.8% share (2025) |

|

Leading Type |

Hyperscale - 41.6% share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 36.5% revenue share (2025) |

|

Second Region |

Victoria & Tasmania - 24.8% revenue share (2025) |

|

Top Companies |

NEXTDC Ltd., AirTrunk Operating Pty Ltd, Equinix Inc., Digital Realty, CDC Data Centres Pty Ltd, Macquarie Technology Group, DigiCo Infrastructure REIT, Vocus Group, DCI Data Centers, and Iron Mountain, Inc. |

Key Analytical Observations Supporting the Above Data Points:

- Solution accounted for 63.8% share in 2025, underpinned by rising hardware capex for GPU servers, storage arrays, and networking gear, with NVIDIA H100 and H200 GPU deployments accelerating across Australian hyperscale sites.

- Hyperscale led type segment at 41.6% in 2025, driven by AWS Sydney, Azure Australia East, and Google Cloud Sydney regional expansion projects with significant announced capex through 2027.

- Australia Capital Territory & New South Wales dominance of 36.5% in 2025 reflects Sydney's role as the Asia-Pacific primary interconnect hub, supported by multiple subsea cable landings and federal government IRAP-certified facilities.

- Victoria and Tasmania held 24.8% in 2025, driven by Melbourne's growing tier-1 cloud availability zone status and Tasmania's cool-climate green data center appeal.

Australia Data Center Market Overview

Data centers are purpose-built facilities housing computing, storage, and networking infrastructure that power cloud services, enterprise applications, and digital platforms. Major categories include hyperscale facilities operated by cloud providers, colocation facilities serving enterprise tenants, and edge sites enabling low-latency compute near end users.

Applications span public cloud services, enterprise hybrid IT, financial services, healthcare, government digital platforms, and content delivery networks. Macroeconomic drivers include Australia’s rapidly expanding digital economy, rapid 5G subscriber growth exceeding 13 Million connections, and the Federal Government's Data and Digital Government Strategy extending to 2030.

Market Dynamics

To evaluate market opportunities, Request Sample

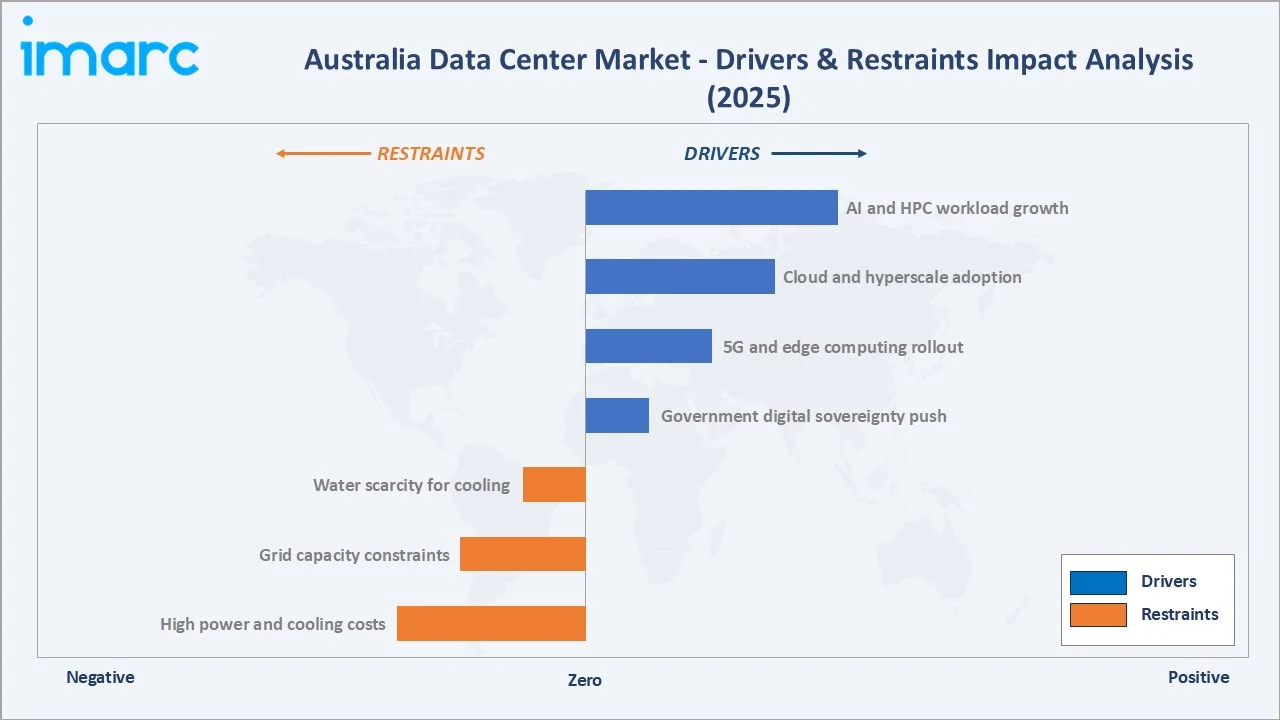

Market Drivers

Structural demand is anchored in AI, cloud, and digital sovereignty. These three forces jointly explain why the market has expanded from USD 3.7 Billion in 2020 to USD 4.8 Billion in 2025.

- AI and HPC workload growth: Generative AI deployments in 2024-2025 have created a surge in GPU-intensive compute demand, with NEXTDC and AirTrunk announcing dedicated AI-ready capacity exceeding 500 MW across NSW and VIC sites.

- Cloud and hyperscale adoption: Australian public cloud spending crossed AUD 23 Billion in 2024, driving AWS, Microsoft Azure, and Google Cloud to expand regional availability zones, creating sustained hyperscale capacity demand.

- 5G and edge computing rollout: Telstra, Optus, and TPG Telecom deployed over 12,000 new 5G base stations in 2024, lifting edge data center demand for low-latency content delivery and IoT applications.

- Government digital sovereignty push: The Federal Government's Hosting Certification Framework and IRAP-assessed facility requirements are channeling public-sector workloads to sovereign Australian data centers, supporting CDC and NEXTDC growth.

Market Restraints

- High power and cooling costs: Australian commercial electricity prices averaged AUD 280 per MWh in 2024, pressuring data center operating margins and forcing accelerated renewable energy procurement.

- Grid capacity constraints: NSW and Victoria grid connection queues for multi-megawatt data center loads have extended to 36-48 months, slowing hyperscale capacity expansion timelines.

- Water scarcity for cooling: Sydney and Melbourne experienced reduced water allocations in 2023-2024, prompting operators to shift toward air-cooled and liquid immersion cooling designs.

Market Opportunities

- AI-ready data center facilities: High-density GPU deployments require 30-50 kW per rack versus 8-12 kW for traditional workloads, creating premium-priced capacity. For example, NEXTDC’s S3 Sydney facility supports high-density AI workloads.

- Green and renewable-powered facilities: Australia's abundant solar and wind resources enable operators to reach 100% renewable targets, with NEXTDC and Macquarie Data Centres advancing renewable integration and PPA adoption.

- Regional and edge deployments: Queensland, Western Australia, and South Australia offer underpenetrated opportunities for edge data centers serving mining, agriculture, and regional government customers.

Market Challenges

- Talent shortage: Australian data center operators reported a 22% vacancy rate for senior mechanical, electrical, and cybersecurity engineers in 2024, slowing facility build-out and commissioning.

- Regulatory compliance complexity: Critical Infrastructure Act amendments, IRAP requirements, and the Consumer Data Right create overlapping compliance obligations that increase operational costs.

- Land availability: Suitable industrial land near Sydney, Melbourne, and Brisbane with grid and fiber access has become scarce, driving site acquisition costs up by 35-45% from 2022 levels.

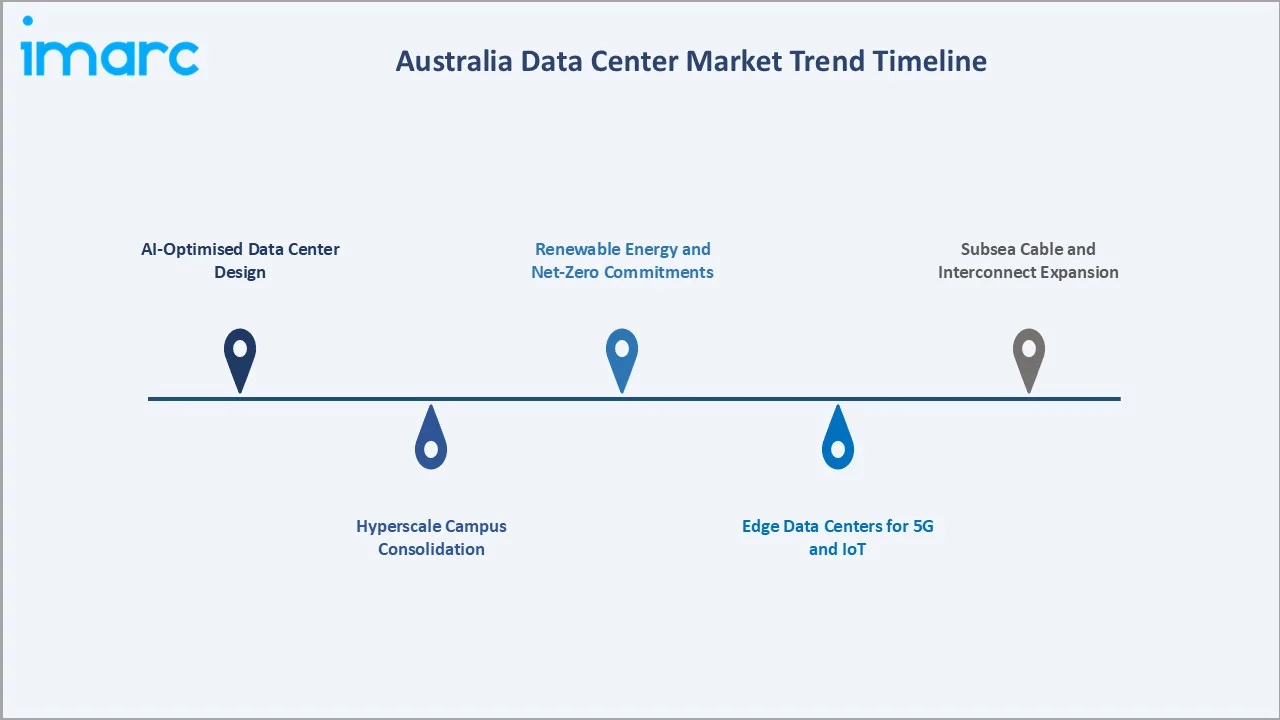

Emerging Market Trends

Five trend vectors are reshaping the competitive logic of the Australian data center market through 2034, from AI-driven capacity design to sustainability-linked facility architecture.

1. AI-Optimised Data Center Design

Operators are redesigning facilities for GPU-dense AI workloads, with direct-to-chip liquid cooling, 132 kV high-voltage feeds, and AI-specific rack architectures becoming standard in new builds commissioned from 2024 onwards.

2. Hyperscale Campus Consolidation

Single-site campuses now exceed 150-300 MW in planned capacity. AirTrunk's SYD1 and SYD2 (150+ MW) campuses and NEXTDC's S3 Sydney facility represent a decisive shift from discrete buildings to integrated hyperscale campuses.

3. Renewable Energy and Net-Zero Commitments

Leading operators, including Microsoft Azure Australia, NEXTDC, and CDC have committed to 100% renewable energy operations, supported by multi-year power purchase agreements with Australian solar and wind developers covering hundreds of megawatts of capacity.

4. Edge Data Centers for 5G and IoT

Telstra, Optus, and regional operators are deploying smaller-footprint edge facilities near population centres to serve 5G, IoT, and content delivery workloads requiring sub-5 millisecond latency.

5. Subsea Cable and Interconnect Expansion

New Indigo, Hawaiki Nui, and Echo subsea cables are landing in Sydney and Perth, reinforcing Australia's role as an Asia-Pacific data interconnect hub and stimulating carrier-neutral colocation demand.

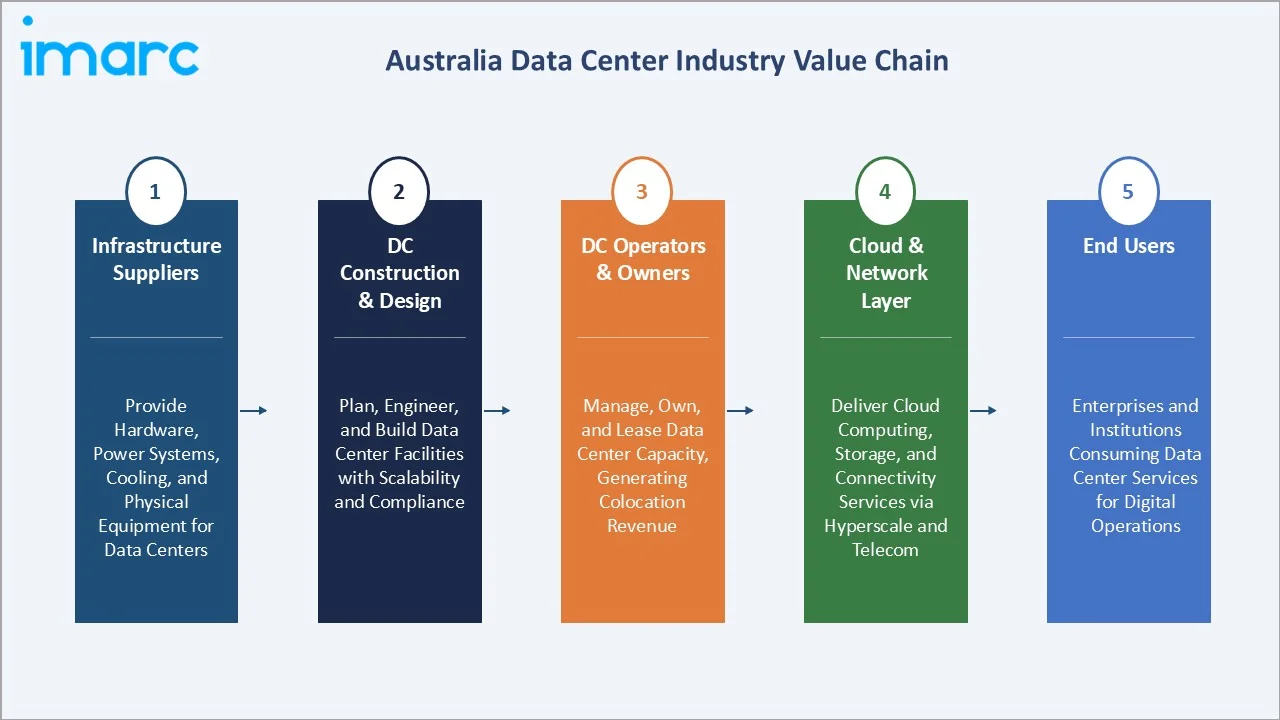

Industry Value Chain Analysis

The Australia data center value chain spans five integrated stages, each with distinct margin profiles, capex intensity, and innovation dynamics.

|

Stage |

Key Players / Examples |

|

Infrastructure Suppliers |

Provide hardware, power systems, cooling, and physical equipment enabling data center operations. |

|

DC Construction & Design |

Plan, engineer, and build data center facilities with scalability, efficiency, and compliance standards. |

|

DC Operators & Owners |

Manage, own, and lease data center capacity, generating revenue through colocation and services. |

|

Cloud & Network Layer |

Deliver cloud computing, storage, and connectivity services via hyperscale and telecom providers. |

|

End Users |

Enterprises and institutions are consuming data center services for digital operations, applications, and data storage. |

DC operators and hyperscale cloud providers capture the highest margins, driven by long-term customer contracts and recurring colocation revenues. Infrastructure suppliers benefit from large capex cycles tied to hyperscale build-out.

Technology Landscape in the Australia Data Center Industry

Power and Cooling Innovation

Operators are deploying direct liquid cooling and immersion cooling systems to handle 50-80 kW per rack densities. In 2024, In March 2024, NEXTDC acquired S6 Sydney in Artarmon, Australia's first purpose-built AI Factory, featuring advanced liquid-cooling capabilities for GPU-intensive workloads.

Renewable Energy and Storage

Battery energy storage systems and on-site solar are being co-located with data center campuses. For instance, 95.8% of the electricity used in CDC data centres was matched with renewable energy certificates, offered to all customers through our Renewable Energy Program.

Software-Defined Infrastructure

AI-driven DCIM platforms are enabling predictive maintenance, capacity optimisation, and dynamic workload placement. Vertiv and Schneider Electric are leading the deployment of these platforms across major Australian operators.

Automation and Robotics

Automated cable management, robotic facility inspection, and AI-enabled security are replacing manual operations. In December 2025, data center giants including AirTrunk, AWS, CDC, Microsoft, NEXTDC, and Equinix launched Data Centres Australia, a new peak body to coordinate AI infrastructure, energy automation, and workforce development across the sector.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Solution |

63.8% |

2025 |

|

Type |

Hyperscale |

41.6% |

2025 |

|

Enterprise Size |

Large Enterprises |

69.3% |

2025 |

|

End User |

IT and Telecom |

38.7% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

36.5% |

2025 |

By Component

Solution commands a 63.8% majority share in 2025, reflecting capex-heavy hardware spending across servers, storage, networking, and power infrastructure. The segment benefits from Australia's hyperscale expansion wave and enterprise hardware refresh cycles.

To access detailed market analysis, Request Sample

Services captured 36.2% in 2025, driven by managed hosting, consulting, deployment, integration, and ongoing maintenance revenues. Enterprise customers increasingly outsource colocation management and cloud migration services to specialist providers, including Kyndryl, DXC, and Accenture.

By Type

Hyperscale leads at 41.6% in 2025, reflecting the rapid expansion of AWS, Microsoft Azure, and Google Cloud regional capacity alongside AirTrunk and NEXTDC's dedicated hyperscale builds for third-party cloud customers.

Colocation holds 33.4% in 2025, supported by enterprise and government hybrid cloud adoption and the need for carrier-neutral interconnection. Edge represents 16.8%, the fastest-growing sub-segment, lifted by 5G rollout and IoT demand. Others (8.2%) include captive corporate facilities and specialised HPC installations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Australia Capital Territory & New South Wales |

36.5% |

Sydney cloud hub, subsea cable landings, federal IRAP facilities, hyperscale capex |

|

Victoria & Tasmania |

24.8% |

Melbourne cloud zone expansion, Tasmania cool-climate green DCs, enterprise demand |

|

Queensland |

16.3% |

Brisbane data hub, edge DC growth, mining/energy digital transformation |

|

Western Australia |

12.4% |

Perth subsea cable landing, resources-sector demand, and emerging cloud region |

|

Northern Territory & South Australia |

10.0% |

Adelaide defence industry, Northern Territory regional edge facilities |

Australian Capital Territory and New South Wales command a 36.5% national revenue share in 2025, the most dominant regional position in the Australian data center market. Sydney accounts for around 60% of Australia’s total built-out data centre capacity, driven by its role as the Asia-Pacific primary cloud availability zone and subsea cable interconnect hub.

Canberra's federal government ecosystem drives IRAP-certified demand, with CDC operating the largest sovereign government hosting footprint. Melbourne's position as Australia's second-largest cloud zone, alongside Tasmania's cool-climate renewable advantage, supports the 24.8% share held by Victoria and Tasmania in 2025.

Queensland, at 16.3% in 2025, is anchored by Brisbane's growing tier-2 data hub status, supported by mining sector digital transformation and regional edge facility deployments. Western Australia at 12.4%, benefits from Perth's position as the country's western subsea cable landing point serving Asia and Africa traffic.

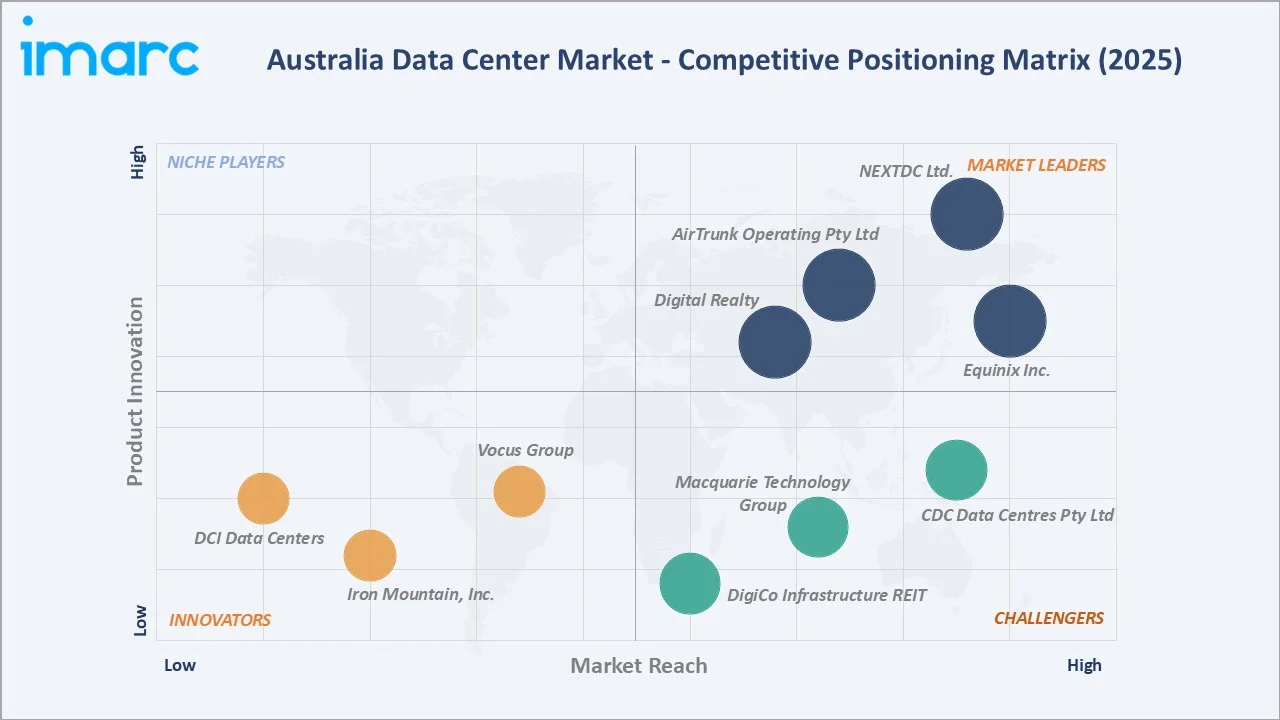

Competitive Landscape

|

Company Name |

Key Brand / Facility |

Position |

Core Strength |

|

NEXTDC Ltd. |

S1-S6 Sydney, M1-M3 Melbourne |

Leader |

ASX-listed, national footprint |

|

AirTrunk Operating Pty Ltd |

SYD1/2, MEL1/2 |

Leader |

Hyperscale campuses, Blackstone-backed |

|

Equinix Inc. |

SY1-SY9, ME1-ME5, PE1-PE3 |

Leader |

Global interconnect platform |

|

Digital Realty |

SYD10, SYD11, MEL11 |

Leader |

Global hyperscale colocation |

|

CDC Data Centres Pty Ltd |

CDC Hume, Eastern Creek |

Challenger |

Federal government sovereign DC |

|

Macquarie Technology Group |

IC1-IC3 Sydney, IC4 Canberra |

Challenger |

Government and enterprise focus |

|

DigiCo Infrastructure REIT |

Sydney Data Center |

Challenger |

Carrier-neutral interconnect |

|

Vocus Group |

Vocus Data Center Solutions |

Emerging |

Telco-adjacent edge DC |

|

DCI Data Centers |

DCI Data Centers |

Emerging |

Regional and edge facilities |

|

Iron Mountain, Inc. |

Iron Mountain Data Centers |

Emerging |

Enterprise colocation niche |

The competitive landscape shows moderate consolidation at the top tier, with NEXTDC, AirTrunk, Equinix, and Digital Realty collectively holding an estimated 60-65% of national market revenue in 2025. AirTrunk's AUD 24 Billion acquisition by Blackstone in September 2024 marked the largest data center transaction in Australian history.

Key Company Profiles

NEXTDC Ltd

NEXTDC is Australia's largest ASX-listed data center operator, headquartered in Brisbane with a national footprint covering Sydney, Melbourne, Brisbane, Perth, Adelaide, and Canberra.

- Product & Facility Portfolio: S1-S6 Sydney campuses, M1-M3 Melbourne facilities, B1-B2 Brisbane sites, plus AXON high-performance compute platform, and ONEDC cloud-native interconnect services.

- Recent Developments: In March 2024, NEXTDC acquired and rebranded a facility in Artarmon as S6 Sydney, Australia's first data centre designed exclusively as an AI Factory, delivering 13.5MW of initial capacity. Additionally, NEXTDC has committed to net-zero operations and has signed PPAs totalling 255MW across APAC.

- Strategic Focus: NEXTDC is prioritising AI-ready capacity expansion, renewable energy procurement, and strategic hyperscale customer wins, while maintaining leadership in federal government IRAP-certified sovereign hosting.

AirTrunk Operating Pty Ltd

AirTrunk is Asia-Pacific's largest hyperscale data center specialist, with headquarters in Sydney and campus operations across Australia, Japan, Singapore, Hong Kong, and Malaysia.

- Product & Facility Portfolio: SYD1 and SYD2 hyperscale campuses in Sydney (over 320 MW combined), MEL1 and MEL2 Melbourne facilities, PER1 in Perth, and an expanded AI-optimised campus pipeline across Asia-Pacific.

- Recent Developments: In September 2024, Blackstone announced an agreement to acquire AirTrunk in an AUD 24 Billion transaction.

- Strategic Focus: AirTrunk is focused on hyperscale AI-ready capacity, long-term agreements with AWS, Microsoft, and Google Cloud, and renewable energy procurement to meet customer net-zero targets across the Asia-Pacific footprint.

Equinix Inc.

Equinix is the Australian subsidiary of the global interconnect and colocation leader, operating 12 International Business Exchange (IBX) facilities across Sydney, Melbourne, Perth, and Brisbane.

- Product & Facility Portfolio: SY1-SY9 Sydney IBX sites, ME1-ME2 Melbourne, PE1-PE2 Perth, and the Equinix Fabric software-defined interconnect platform enabling private connections to AWS, Azure, Google Cloud, and Oracle Cloud.

- Recent Developments: In June 2024, Equinix invested AU$240 million to expand its SY5 Sydney and ME2 Melbourne IBX facilities with 4,175 additional cabinets to support AI and high-density workloads, while also rolling out direct-to-chip liquid cooling across its Australian platform.

- Strategic Focus: Equinix is focused on carrier-neutral interconnect leadership, hyperscale cloud adjacency, and enterprise hybrid cloud enablement through its xScale and Fabric platforms across the Australian market.

Market Concentration Analysis

The Australia data center market exhibits high concentration at the top tier, with NEXTDC, AirTrunk, Equinix, Digital Realty, and CDC collectively accounting for approximately 65-72% of national revenue in 2025. The remaining share is distributed across mid-tier and emerging operators.

Consolidation trends accelerated in 2024: Blackstone's AirTrunk acquisition reinforced hyperscale scale as the dominant competitive moat, while NEXTDC's continued ASX-listed growth highlights the capital intensity required for national expansion.

Fragmentation is visible in the edge and regional segment, where over 15 operators, including Vocus, DCI, and telco-adjacent providers, compete for 5G-driven and regional demand. Future consolidation is expected as hyperscale economics dominate the national market.

Investment & Growth Opportunities

Fastest-Growing Segments

AI and HPC workloads are the highest-growth sub-category, driven by GPU-intensive generative AI and enterprise ML adoption. Hyperscale capacity expansion follows at 8.6% CAGR, supported by AWS, Azure, and Google Cloud regional builds.

Emerging Market Expansion

Queensland's data center market is expanding steadily, underpinned by Brisbane's tier-2 hub growth and edge facility deployments. Western Australia benefits from subsea cable landings and resources-sector digitalisation.

Venture & Strategic Investment Trends

Notable 2024-2025 transactions include Blackstone's AUD 24 Billion AirTrunk acquisition, NEXTDC's $1.3 Billion capital investment in in Sydney and Melbourne data centres, and Microsoft's A$25 Billion Australia AI infrastructure commitment. Private equity interest in Australian data center assets remains exceptionally strong.

Future Market Outlook (2026-2034)

The Australia data center market is projected to expand from USD 4.8 Billion in 2025 to USD 8.2 Billion by 2034 at a CAGR of 5.47%, a value expansion underpinned by AI workloads, cloud adoption, and 5G-driven edge computing through the forecast period.

Three technology discontinuities will reshape the competitive landscape through 2034. First, AI-optimised data centers with liquid cooling and 100+ kW rack densities will displace traditional designs across hyperscale builds. Second, edge data centers will emerge as a distinct sub-market with significant growth potential.

Third, renewable energy and battery storage integration will become mandatory for hyperscale customers, with 100% renewable operations becoming the baseline procurement requirement by 2030. Digital sovereignty and data residency mandates will continue driving domestic capacity expansion.

Research Methodology

Primary Research

Primary research encompassed over 50 structured interviews conducted in 2024-2025 with stakeholders, including senior executives at Australian data center operators, hyperscale cloud providers, enterprise IT directors, federal government digital strategy leads, and institutional investors in digital infrastructure.

Secondary Research

Secondary sources include Australian Bureau of Statistics data, Department of Home Affairs Critical Infrastructure publications, IRAP assessment frameworks, ACCC telecommunications market reports, AWS/Azure/Google Cloud regional announcements, NEXTDC and AirTrunk annual reports, and industry press, including iTnews and Datacenter Dynamics.

Forecasting Models

Market sizing combined top-down and bottom-up approaches, incorporating installed MW capacity, colocation revenue per kW, hyperscale capex commitments, and historical cloud adoption rates. Scenario analysis tested base, optimistic, and conservative cases around AI workload growth and renewable energy transition timelines.

Australia Data Center Market Report Scope

|

Attribute |

Details |

|

Market Size (2025) |

USD 4.8 Billion |

|

Forecast (2034) |

USD 8.2 Billion |

|

CAGR (2026-2034) |

5.47% |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Segmentation |

By Component, By Type, By Region |

|

Regional Analysis |

ACT & NSW, Victoria & Tasmania, Queensland, Western Australia, NT & South Australia |

|

Key Companies |

NEXTDC Ltd., AirTrunk Operating Pty Ltd, Equinix Inc., Digital Realty, CDC Data Centres Pty Ltd, Macquarie Technology Group, DigiCo Infrastructure REIT, Vocus Group, DCI Data Centers, Iron Mountain, Inc., etc. |

|

Report Format |

PDF, Excel |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia data center market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Australia data center market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia data center industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Data Center Market Report

The Australia data center market was valued at USD 4.8 Billion in 2025, supported by cloud adoption, AI workload demand, and expanding hyperscale capacity across Sydney and Melbourne.

The market is projected to reach USD 8.2 Billion by 2034, growing at a CAGR of 5.47% during 2026-2034, driven by hyperscale expansion, AI workloads, and edge computing rollout.

Solution leads with a 63.8% share in 2025, driven by hardware capex across servers, storage, networking, and power infrastructure supporting hyperscale and colocation expansion nationally.

Hyperscale dominates with a 41.6% share in 2025, supported by AWS, Microsoft Azure, and Google Cloud regional expansion alongside AirTrunk and NEXTDC dedicated hyperscale campuses.

Australian Capital Territory and New South Wales leads with a 36.5% share in 2025, driven by Sydney's cloud hub status, subsea cable landings, and federal government IRAP-certified facilities.

Key drivers include AI and HPC workload growth, cloud hyperscale adoption, 5G and edge computing rollout, government digital sovereignty push, and rising enterprise digital transformation spending.

AI and HPC workloads are growing fastest at approximately 9.8% CAGR, followed by hyperscale capacity at 8.6% CAGR, driven by GPU-intensive generative AI adoption and cloud expansion.

Leading companies include NEXTDC Ltd., AirTrunk Operating Pty Ltd, Equinix Inc., Digital Realty, CDC Data Centres Pty Ltd, Macquarie Technology Group, DigiCo Infrastructure REIT, Vocus Group, DCI Data Centers, and Iron Mountain, Inc.

Blackstone's AUD 24 Billion acquisition of AirTrunk in 2024 was Australia's largest data center transaction, accelerating hyperscale capacity investment and validating private equity interest in the sector.

AI workloads are driving demand for GPU-dense facilities with liquid cooling and 50-100 kW per rack densities, with operators investing in dedicated AI-ready capacity across Sydney and Melbourne.

Green data centers are expanding rapidly, with NEXTDC, CDC, and AirTrunk signing multi-year renewable PPAs exceeding 500 MW combined capacity to meet customer net-zero commitments by 2030.

Sydney, Melbourne, and Canberra remain tier-1 hubs, while Brisbane, Perth, and Adelaide are emerging as tier-2 hubs supported by subsea cables, 5G rollout, and regional enterprise demand.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade