Australia Digital Health Market Size, Share, Trends and Forecast by Type, Component, and Region, 2026-2034

Australia Digital Health Market Size and Share:

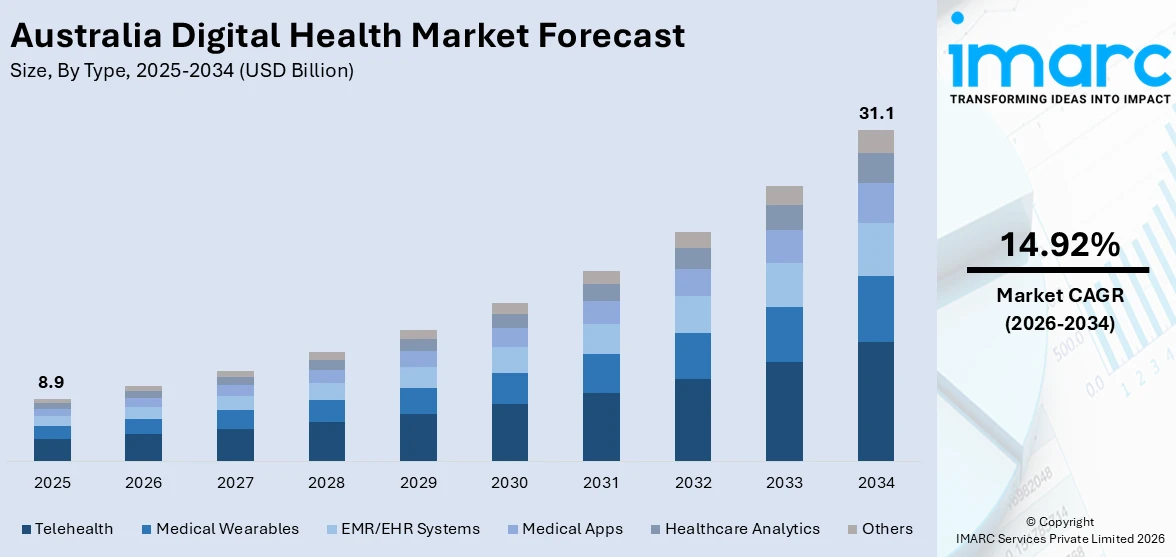

The Australia digital health market size was valued at USD 8.9 Billion in 2025. Looking forward, the market is expected to reach USD 31.1 Billion by 2034, exhibiting a CAGR of 14.92% from 2026-2034. The Australia digital health market share is expanding, driven by the implementation of favorable government regulations, heightened usage of telemedicine among patients, increasing advanced healthcare information technology (IT) infrastructure, and rising need for personalized medical treatment options to get better patient outcomes.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 8.9 Billion |

| Market Forecast in 2034 | USD 31.1 Billion |

| Market Growth Rate 2026-2034 | 14.92% |

Currently, the increasing adoption of telehealth services among the masses is propelling the growth of the Australian market. Several infectious diseases have acted as catalysts for the high adoption of telehealth due to the need for providers and patients to find alternative safe and convenient options that can replace in-person consultation. Government subsidies for telehealth consultations are also driving its utilization. Telehealth platforms are changing the delivery model of healthcare due to convenience and accessibility. The process of virtual consultation allows patients to be in touch with health providers while at home, reducing time and cost associated with travel. Telehealth is instrumental in addressing geographic disparities in healthcare access, especially among rural and indigenous communities. Sustained demand for telehealth services is expanding the Australia digital health market share.

To get more information on this market Request Sample

There is an increased adoption of mobile health (mHealth) applications and wearable devices in Australia due to growing emphasis on preventive care and personal health management. mHealth applications enable users to monitor aspects of their health, such as physical activity, nutrition, mental health, and chronic disease management. Such applications often work with wearable devices, like fitness trackers and smartwatches, providing real-time insights and personalized recommendations about the users' health. Wearable devices are gaining traction, not only among the athletic individuals but also among patients that are suffering from chronic diseases, which include diabetes and CVDs.

Key Trends of Australia Digital Health Market:

Growth of Telehealth Services

Telehealth services have increased significantly in Australia as a result of government support and increasing patient demand. In particular, telehealth has been very effective in countering healthcare disparities in rural and remote areas, which often lack access to health care providers and specialists. Virtual consultations made possible by telehealth eliminate the need for traveling long distances, thereby cutting costs and time taken to receive care. This has been particularly impactful for Indigenous communities and those managing chronic conditions, allowing for timely and continuous care. Telehealth has also been highly effective in mental health services, with virtual consultations providing accessibility and privacy, encouraging more patients to seek support. The integration of advanced technologies such as artificial intelligence (AI), wearable devices, and data analytics is further enhancing the capabilities of telehealth in Australia. Wearables allow the real-time monitoring of health metrics, and AI tools will ensure higher diagnostic accuracy and patient engagement. According to the IMARC Group, Australia telemedicine is expected to reach USD 2501.53 million by 2032.

Adoption of Electronic Health Records (EHR)

Another major trend emerging in the digital health area of Australia is the use of electronic health records or EHR. The overall process of managing patient records has become easier with EHR, and healthcare services are able to access valuable medical information in real time. This minimizes opportunities for medical errors, has positive impacts on patients' conditions, and facilitates easier coordination among care providers. EHR systems are also improving preventive care by enabling healthcare professionals to monitor patient history and predict potential health risks. EHR adoption is expected to grow further with government backing and increased awareness about data-driven healthcare, becoming an integral part of clinical workflows and decision-making. In 2024, the Royal Australian College of GPs asked the Federal Government to overhaul My Health Record so that it becomes appropriate for purpose for patents and GPs. This was due to the fact that 31% of GPs were reported to rarely or never use it following a countrywide survey.

Expansion of Mobile Health (mHealth) Solutions

According to the Australia digital health market analysis, mobile health, or mHealth, solutions are growing rapidly in the region, providing patients with greater access to healthcare services through mobile applications. These include appointment scheduling, chronic disease management, mental health support, and fitness tracking applications. mHealth is empowering individuals to take a more active interest in their health by encouraging self-care and patient engagement. More health professionals are increasingly employing these mHealth platforms by following patients remotely and even on real-time communication in patients to further improve outcomes regarding treatment. Furthermore, based on Australian Institute of Digital Health, the number of smartphone users in Australia will grow by 3.7 million to 23.6 million by the year 2026. Therefore, with an increase in users of smartphones in daily lives, mHealth solutions are bound to go up thereby triggering novelty and Australia digital health market growth.

Growth Drivers of Australia Digital Health Market:

National Infrastructure and Platforms of Government

A very powerful driver of Australian digital health expansion arises from national-scale infrastructure developed and administered by federal agencies, such as the Australian Digital Health Agency and its rollout of My Health Record (MHR). MHR is an Australian, opt-out electronic health record system at national scale tightly interlinked with Medicare profiles and personal healthcare identifiers, widely taken up in GPs, pharmacies, and hospitals. The My Health Record platform facilitates secure digital discharge summaries, test results, immunisation records, and prescriptions, allowing interoperability between heterogeneous providers. New systems like Provider Connect Australia also facilitate streamlined workforce data between Medicare, pharmacy, and hospital systems. These reforms empower digital health providers with a common mandate and infrastructure. They also provide clarity in policy frameworks and enable secure messaging, standard clinical terminology, and patient-centric access. With government strategic support and improvements paid for through successive budgets to modernise digital health systems, Australia provides a secure and stable context which reinforces trust, interoperability, and adoption between providers and patients.

Integration of Private Sector and Health Insurance Innovation

The second major force behind the Australia digital health market demand is growing integration of private health insurers, technology businesses, and healthcare providers to provide end-to-end digital care solutions. Australia's public-private mixed healthcare system enables the insurers to directly contribute to innovation, especially in prevention and management of chronic diseases. Top health funds are investing in digital platforms that provide tele-consultations, health coaching, integration with wearable devices, and AI-based risk assessments for their members. This is also supplemented by the increasing employer-sponsored wellness programs and digital-first clinics combining insurance with app-based services. A mark of distinction within the region is the permissiveness of the Australian regulatory environment for insurer-initiated health tech pilots, which leaves space for nimble service models. Furthermore, competition between private insurers favors the uptake of differentiated digital applications that enhance patient outcomes and retention. Such sector-wide cooperation, supported by an active tech ecosystem and a responsive policy environment, is serving to amplify digital health services well beyond traditional clinical environments.

Local Innovation Ecosystem and AI‑Enabled Preventive Care

Australia's fast-changing local health tech innovation ecosystem characteristically fuels digital health development by interweaving academic research capabilities, government innovation programs, and new commercial entrants. Australian cities and universities are hotbeds for AI‑based diagnostics, wearable health technologies, and future models of imaging. Consumer‑focused startups, in the meantime, are using AI diagnostics and personalised preventive health checks with a view to changing the paradigm from reactive to predictive care. At the same time, dominant telecom and technology players collaborate closely with public systems to provide virtual care technologies and clinical software. This fusion of home-bred innovation and robust industry-government partnership is quintessentially Australian. Parallel initiatives integrating local hospital record information with cloud analytics to enable cutting-edge research are in development, presenting platforms specific to the region. These localized innovation pipelines, combined with digital health strategy grants, commercialization programs, and university-industry collaborations, increase both the availability of digital solutions and their uptake across varying healthcare settings.

Opportunities of Australia Digital Health Market:

Growth in Personalized and Preventive Digital Care

Australia's digital health industry is ready for lift-off in personalised and preventive care, where data and AI have tremendous potential. With high incidence of conditions like diabetes, cardiovascular disease, and obesity, demand is increasing for those tools that enable the management of health proactively rather than reactively. Australia's healthcare system, with the blending of public (Medicare) and private care, provides a dynamic platform for new digital models to be tested and scaled. Insurers and startups are increasingly leveraging wearables data, genetic tests, and lifestyle data to provide consumers with personalized health advice, which is revolutionizing conventional care pathways. Moreover, mobile health app and remote monitoring device acceptance among locals provides an opportunity for further investment in digital coaching, medication adherence apps, and early detection platforms. The extensive rural and regional regions of Australia create a further opportunity for preventive digital solutions to enhance self-management and early intervention where healthcare access is not available. This special situation makes Australia a laboratory for scalable, personalized digital care technologies.

Inclusion of Indigenous and Remote Health with Digital Tools

Australia's digital health sector has enormous unfulfilled potential in bridging the long-standing healthcare gaps that have long been a challenge for Aboriginal and Torres Strait Islander populations and those who live in remote areas. Because of geographic and socioeconomic limitations, these groups often experience difficulties in receiving timely, culturally relevant medical treatment. Digital health technologies, especially mobile-first systems and telehealth models, are proving to be a viable means of bridging these gaps. The opportunity is not just to provide services remotely, but to co-design culturally grounded and community-led solutions. There is increasing interest in implementing indigenous-owned health tech solutions, language-accessible mental health platforms, and telepsychiatry networks specific to remote communities. Government funding and health workforce schemes are increasingly focusing on this sector, providing a rich terrain for innovators to deliver enduring value. In contrast to other parts of the world, Australia's reconciliation agenda and focus on indigenous wellbeing present a singular, society-led opportunity to leverage digital health as an agent of equity and empowerment.

Interoperability and Data Integration for National Health Outcomes

Another key opportunity in Australia's digital health sector is the development of interoperable systems and real-time data integration across care providers. While Australia is already gaining advantages from platforms such as My Health Record, the next level of opportunity exists to link data from hospitals, GPs, allied health services, private insurers, pharmacies, and even aged care facilities into coherent, actionable systems. This would facilitate a more comprehensive understanding of patient trajectories and population trends at a level, informing improved decision-making in clinical and policy contexts. Australia's healthcare industry is increasingly appreciating the potential benefits of health informatics, predictive analytics, and cloud-stored electronic medical records facilitating coordinated care. Only in Australia is there existing national infrastructure to enable such connectivity, such as standardized patient identifiers and health information exchange protocols. As more private and public organizations come together on secure data-sharing collaborations, the potential to create a genuine integrated, outcomes-oriented digital health ecosystem becomes more realizable and beneficial.

Challenges of Australia Digital Health Market:

Fragmentation of Health Systems and Data Silos

Fragmentation across healthcare systems and ongoing data silos are among the biggest challenges confronting Australia's digital health industry. Even with a national digital platform such as My Health Record, most public and private healthcare providers remain on separate systems with differing degrees of digital maturity. This fragmentation is particularly acute between state and territory health departments, each of which has its own hospital networks, IT systems, and procurement systems. Consequently, smooth exchange of patient data continues to be challenging, especially in the case of cross-jurisdictional care or changeover between public and private systems. This fragmentation prevents the use of integrated digital health solutions that need steady, real-time data streams to effectively work. Secondly, older people's care and allied health services tend to be excluded from usual data-sharing arrangements, making it more challenging to provide integrated patient care. The solution to this problem demands more stringent national interoperability standards as well as intensified federal-state coordination, something that is particularly challenging in Australia's federated health system.

Digital Divide and Unequal Access to Technology

The vast expanse of Australia and its socio-economic variability pose a particular challenge to universal access to digital health solutions. Remote and rural groups, and especially Indigenous communities, usually do not have the stable internet networks or digital competence to be able to take advantage of telehealth, mobile health applications, or virtual consultations. Whereas urban communities have swiftly embraced digital solutions, citizens in more remote areas are confronted with less bandwidth, fewer devices connected, and less trust for unknown technologies. Moreover, non-English-speaking communities and older Australians may find it difficult to use complex digital interfaces, thus being excluded from services ever more delivered online. This digital divide has the potential to generate a two-tiered healthcare system, one digitally enabled and the other behind. While there are regional connectivity efforts being made, the issue is firmly embedded in larger differences in education levels, infrastructure, and access to healthcare. For digital health to produce equitable results in Australia, it needs to be supported by adapted help systems, community outreach, and culturally appropriate design, especially for those who have been traditionally underserved by the mainstream system.

Privacy, Security, and Public Trust Concerns

Sustaining public confidence in digital health platforms is a continued problem across the Australian experience, especially in regard to data privacy and cybersecurity. The implementation of My Health Record, though of national importance, was greeted early with resistance in part because of privacy issues when the system was initially opt-out instead of opt-in. Most Australians were wary of the risks of accessing centralised health data without adequate protective measures or misuse by third parties. Cybersecurity breaches in both private and public sectors that followed have further energized worries regarding sensitive health information storage, handling, and security. This conservative climate keeps consumers and even some healthcare professionals reluctant to adopt fully digital systems, especially those with AI or third-party software integration. Australia's regulatory framework is changing, with new data-sharing rules and greater protections forthcoming, but public trust needs to be earned through openness, accountability, and clarity on an ongoing basis. Without trust, digital health tool adoption may continue to lag unevenly across pivotal populations.

Australia Digital Health Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the Australia digital health market, along with forecasts at the country and regional levels from 2026-2034. The market has been categorized based on type and component.

Analysis by Type:

- Telehealth

- Medical Wearables

- EMR/EHR Systems

- Medical Apps

- Healthcare Analytics

- Others

Telehealth is considered a major segment in the digital health market, which includes virtual consultations, remote patient monitoring, and telemedicine platforms. This segment has recorded rapid growth due to growing demand for accessible healthcare services, especially in rural and underserved regions. Telehealth solutions would thus allow patients to visit through video calls, telecall, or secure message about their health condition while bridging geographical barriers for hospital visits. The telemedicine segment has grown hugely within Australia. It is encouraged by subsidies set by the government from Medicare Benefits Schedule (MBS) and also its applications of advanced technologies including use of AI in diagnosing and monitoring.

The medical wearables segment is growing fast as people and healthcare providers look to monitor health in real-time and take preventive care. It includes products such as fitness trackers, smartwatches, and medical-specific wearables for heart rate monitoring, blood pressure monitoring, glucose level monitoring, and other vital signs. The wearables are highly beneficial for the management of chronic diseases like diabetes, cardiovascular diseases, and respiratory diseases, which are provided with constant health data and early intervention.

The EMR/EHR systems segment plays a significant role in the digital health market by centralizing patient health information for streamlined access and improved care coordination. These systems enable healthcare providers to document, share, and analyze patient data in real time, thus allowing them to make better decisions and reduce medical errors. In Australia, the government-led My Health Record initiative has been a significant driver of EHR adoption, providing a nationwide platform for electronic health data storage and sharing.

Medical applications, also known as mHealth apps, are highly dynamic within the digital health market. Some of their uses include fitness and wellness tracking; chronic diseases management; mental health; medication compliance; telemedicine. Such medical applications support individuals in assuming a participatory role in health through informed, contextual, goal-related, or reminder-based guidance. Penetration of smart phones within Australia, preventive care seeking among consumers, and increasingly being exposed to mental illness-related concerns promote the usage of medical applications.

Healthcare analytics is a rapidly evolving and impactful segment that enables health service providers to obtain actionable insights from significant volumes of patient data. In this category come predictive analytics, population health management, and clinical decision support systems - helping to optimize care outcomes and costs while reducing resource consumption. The health analytics market is also beginning to gain prominence in Australia with organizations looking forward to using their data better and efficiently to make decisions.

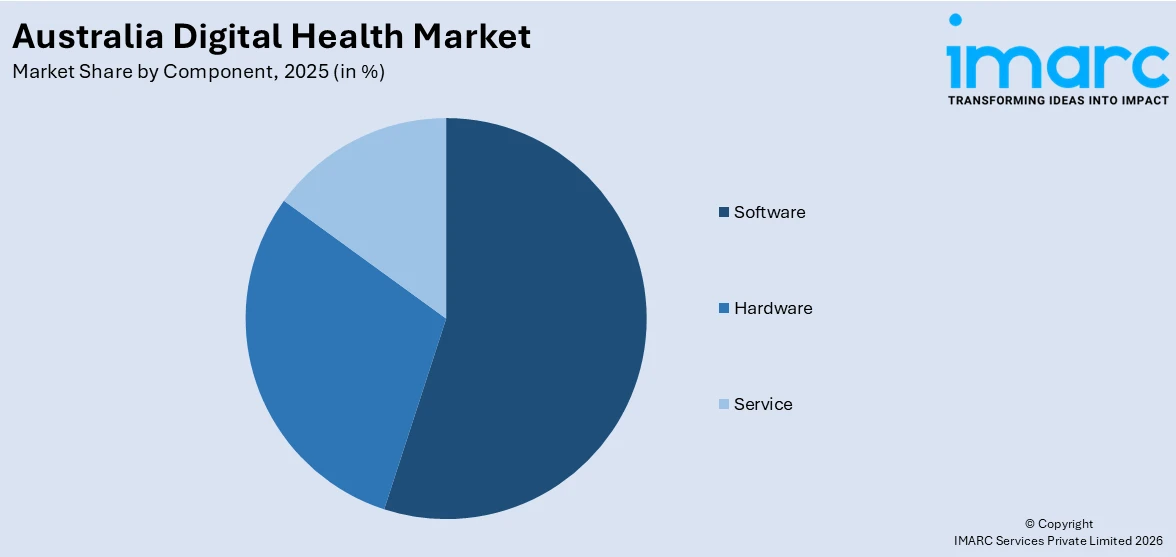

Analysis by Component:

Access the comprehensive market breakdown Request Sample

- Software

- Hardware

- Service

The software segment is a core component of the digital health market, encompassing applications, platforms, and systems that power telehealth, electronic medical records (EMR/EHR), medical apps, and healthcare analytics. Software solutions enable data integration, patient-provider communication, and advanced analytics, forming the backbone of digital health services. In Australia, the demand for interoperable and cloud-based software solutions is growing as healthcare organizations strive to enhance efficiency, comply with regulations, and improve patient outcomes.

The hardware segment includes devices and physical infrastructure that support digital health technologies, such as wearable devices, remote monitoring systems, telehealth equipment, and data storage hardware. This segment is driven by the rising adoption of connected medical devices that enable real-time health monitoring and seamless data transmission. In Australia, the demand for wearable devices such as fitness trackers, smartwatches, and specialized health monitors is growing as consumers focus on preventive care and chronic disease management.

The services segment encompasses a wide range of offerings, including implementation, integration, training, maintenance, and ongoing support for digital health solutions. This segment is critical to the adoption and effective use of software and hardware technologies in healthcare. In Australia, the services market is expanding as healthcare organizations increasingly seek third-party expertise for the deployment of telehealth platforms, EHR systems, and analytics tools.

Regional Analysis:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The Australian Capital Territory (ACT) and New South Wales (NSW) represent a significant portion of the digital health market, driven by the region’s dense population, advanced healthcare infrastructure, and high concentration of healthcare facilities. Sydney, as a financial and technological hub, is home to many digital health startups, research institutions, and innovation centers that are driving the adoption of advanced healthcare technologies such as telehealth, AI-powered diagnostics, and electronic health records (EHR). Government support, including funding for regional telehealth programs, has further boosted digital health adoption in rural parts of NSW.

Victoria and Tasmania are key regions in the Australian digital health market, with Victoria leading in healthcare innovation and research. Melbourne, in particular, is a center for digital health advancements, housing numerous health-tech companies, academic institutions, and technology accelerators.

Queensland is a growing market for digital health, driven by the state’s diverse geography, which includes urban centers like Brisbane and a vast network of rural and remote communities. Telehealth adoption has been particularly robust in Queensland, addressing the challenges of delivering healthcare to isolated areas where physical access to medical facilities is limited. The state has invested heavily in digital infrastructure, such as telehealth platforms and electronic health records, to bridge gaps in healthcare access.

The Northern Territory and South Australia represent unique opportunities for digital health expansion, given their relatively sparse populations and significant healthcare challenges in remote and Indigenous communities. Telehealth is a cornerstone of healthcare delivery in these regions, enabling remote consultations and virtual monitoring for patients in isolated areas. Government-funded programs are pivotal in promoting digital health initiatives, particularly for addressing chronic disease management and improving Indigenous health outcomes.

Western Australia, the largest state by land area, faces unique challenges in providing healthcare due to its vast and sparsely populated geography. Digital health technologies, particularly telehealth and remote monitoring systems, play a critical role in overcoming these barriers. The state government has heavily invested in telehealth infrastructure to connect patients in remote regions with specialists based in urban centers like Perth.

Competitive Landscape:

Prominent players are heavily investing in research and development (R&D) to create innovative digital health solutions. By prioritizing R&D, companies are not only enhancing their product offerings but also addressing critical healthcare challenges like interoperability, data security, and chronic disease management. In 2024, The Hunter New England and Central Coast Primary Health Network (HNECC PHN) is developing digital health innovation in rural Australia with the introduction of the country’s first Gen 2 SiSU Mini Health Station at Glen Innes in Timbs Pharmacy. Moreover, telehealth remains a cornerstone of the digital health market in Australia, and companies are intensifying their focus on this segment. Many players are also tailoring their telehealth offerings to meet the needs of specific demographics, such as rural communities or mental health patients, thereby expanding their market reach. The emphasis on user-friendly interfaces, high-quality video streaming, and seamless integration with EHR systems has become a priority for companies looking to capture a larger share of the telehealth market.

The report provides a comprehensive analysis of the competitive landscape in the Australia digital health market with detailed profiles of all major companies.

Latest News and Developments:

- November 2024: Monash University’s Faculty of Information Technology (IT) created a strategic partnership with Apollo Hospitals to improve digital health research and solutions across both India and Australia.

- September 2024: The Department of Health and Aged Care announced the launch of a telehealth service for aged care residents as part of reform actions in the aged care industry. It recently launched an ender request for a supplier or a group of suppliers of a telehealth solution for delivering virtual nursing services to 30 unnamed residential aged care homes in Australia.

- November 2024: MedAdvisor Solutions launch a brand-new telehealth functionality available on its app. The launch supports the heightened requirement of patients and pharmacies throughout Australia.

- August 2024: DDM Health launched a novel digital health platform in Australia after getting a REDI Fellowship in 2023.

Australia Digital Health Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Telehealth, Medical Wearables, EMR/EHR Systems, Medical Apps, Healthcare Analytics, Others |

| Components Covered | Software, Hardware, Service |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, Australia digital health market forecasts, and dynamics of the market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the Australia digital health market.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia digital health industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Digital Health Market Report

Digital health market involves the use of digital technologies, such as telehealth, mHealth, EMR/EHR systems, and healthcare analytics, to enhance healthcare delivery, patient engagement, and operational efficiency. Applications include virtual consultations, chronic disease management, and real-time health monitoring.

The Australia market was valued at USD 8.9 Billion in 2025.

The Australia digital health market is projected to exhibit a CAGR of 14.92% during 2026-2034.

The Australia digital health market is expected to reach a value of USD 31.1 Billion by 2034.

The Australia digital health market trends include growing adoption of AI-powered diagnostics, expansion of telehealth services, increased focus on personalized and preventive care, and rising integration of electronic health records across systems. Public-private partnerships and rural health innovations also shape the evolving landscape of digital healthcare delivery in the country.

Key drivers of the Australia digital health market include strong government support, nationwide platforms like My Health Record, rising demand for telehealth, innovation in AI and wearable tech, and increased private sector investment. The need for remote care access across rural areas also fuels digital health adoption and infrastructure development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade