Australia Drones Market Size, Share, Trends and Forecast by Type, Component, Payload, Point of Sale, End Use Industry, and Region, 2026-2034

Australia Drones Market Summary:

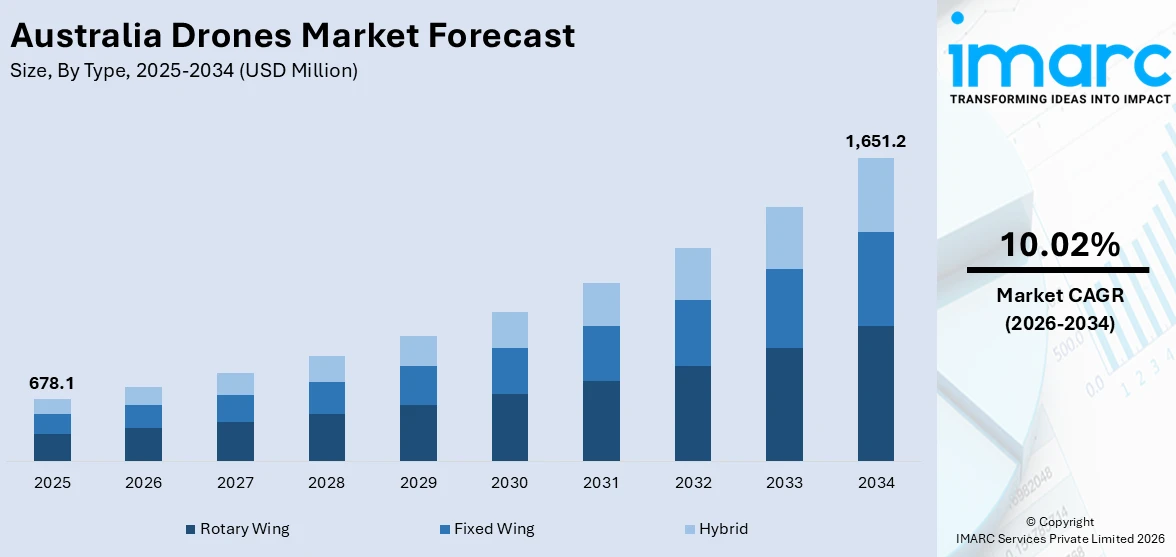

The Australia drones market size was valued at USD 678.1 Million in 2025 and is projected to reach USD 1,651.2 Million by 2034, growing at a compound annual growth rate of 10.02% from 2026-2034.

The market is experiencing robust expansion driven by increasing adoption of unmanned aerial vehicles across agriculture, defense, construction, and logistics sectors. Government investments in drone technology for military modernization and border security are creating strong demand. Advancements in autonomous navigation, AI-powered analytics, and improved payload capabilities are enhancing operational efficiency across industries. Supportive regulatory developments, expanding commercial applications in precision farming and infrastructure inspection, and growing interest in drone delivery services are further strengthening adoption and contributing to Australia drones market share.

Key Takeaways and Insights:

- By Type: Rotary wing dominates the market with a share of 56.3% in 2025, driven by their versatility in vertical takeoff, hovering capabilities, and suitability for diverse commercial and defense applications.

- By Component: Hardware leads the market with a share of 44.2% in 2025, reflecting sustained demand for airframes, sensors, cameras, propulsion systems, and navigation equipment across industrial and military sectors.

- By Payload: <25 kilograms hold the largest share at 52.4% in 2025, supported by widespread use of lightweight drones for surveying, photography, crop monitoring, and small-scale delivery operations.

- By Point of Sale: Original equipment manufacturers (OEMs) represent the largest segment with a 62.7% share in 2025, as end users prefer complete integrated drone systems with manufacturer warranties and technical support.

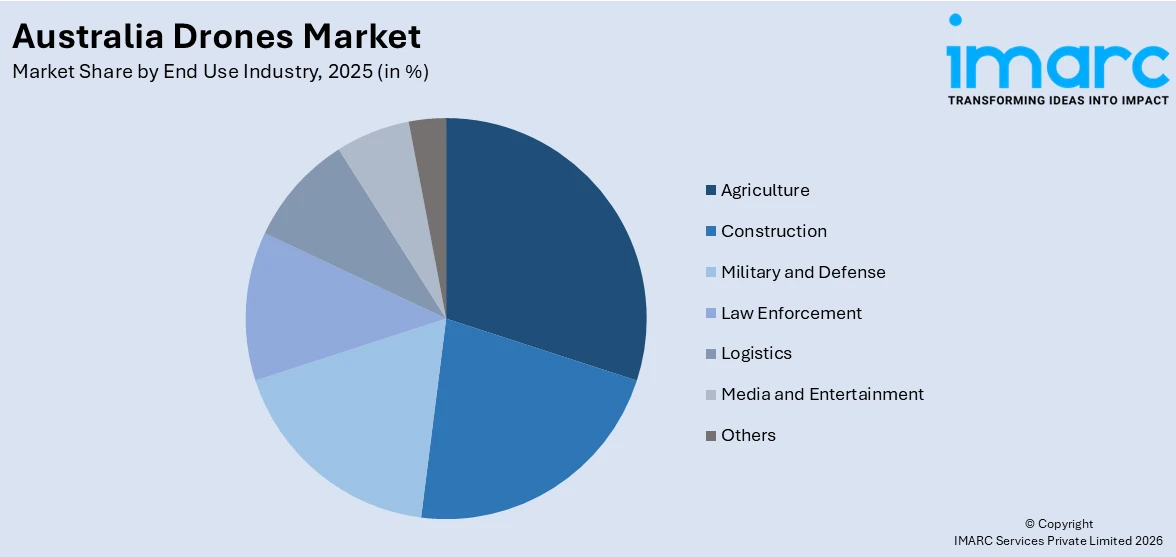

- By End Use Industry: Agriculture accounts for the largest share at 24.5% in 2025, driven by growing precision farming adoption for crop monitoring, pest detection, and targeted spraying across Australia’s vast farmlands.

- By Region: Queensland leads the market with a 26.8% share in 2025, supported by its thriving agricultural sector, favorable geography for drone operations, and growing adoption in mining and tourism industries.

- Key Players: The Australia drones market features a competitive landscape with both global manufacturers and domestic companies driving innovation in hardware, software, and counter-drone solutions to strengthen their market positions.

To get more information on this market Request Sample

The drones market in Australia is progressing with increasing use of unmanned aerial systems in the operations of government agencies, industry, and military forces. One of the factors that influence the growth of the drones market in Australia is the increasing investment in drone technology in the country’s defense and precision agriculture industry. In June 2024, the Australian government announced an investment of AUD 13.5 million in federal funding as part of Round 2 of the Emerging Aviation Technology Partnerships initiative. This investment is targeted at supporting research in advanced beyond visual line of sight drone operations, electric aircraft charging systems, and cargo drone technology. Regulatory developments, increasing use of drone analytics technology, and growing use cases are creating a conducive environment for the use of drones in different industry segments.

Australia Drones Market Trends:

Integration of Artificial intelligence (AI) and Machine Learning (ML) in Drone Operations

In addition, AI and ML technologies are being integrated into drones in the country to improve data processing, autonomous navigation, and analytics capabilities. For example, in 2025, Teledyne FLIR OEM and SYPAQ Systems announced the unveiling of the CorvoX small unmanned aerial system (SUAS), representing a significant leap in advancing the country’s sovereign defense capabilities. The newly unveiled drone was designed as part of the Australian Defence Force (ADF) DEF129 SUAS initiative for ground infantry operations. The newly unveiled drone comes equipped with Teledyne FLIR’s Boson thermal Infrared (IR) camera, providing unmatched situational awareness in challenging environments. The technologies allow drones to carry out complex operations with accuracy, thus contributing to the development of the country’s drones market in the construction, mining, and infrastructure sectors.

Expansion of Commercial Drone Delivery Services

The drone delivery services are gaining traction as companies are investing in last-mile delivery solutions and aerial transport services. For example, in July 2024, Wing partnered with DoorDash, expanding its services in Melbourne by launching the drone delivery service from Eastland Shopping Centre, allowing 250,000 people living in Melbourne’s eastern suburbs to benefit from the service. The improvements in the navigation system of drones have helped transport goods safely, meeting the growing demand of consumers for faster delivery services in the country.

Advancement of Beyond Visual Line of Sight (BVLOS) Operations

Regulatory structures for BVLOS drone operations are in development, and this has created new opportunities for the application of drones in commercial and industrial activities. For instance, in October 2025, the Civil Aviation Safety Authority initiated a 12-month trial, which introduced four new broad area BVLOS approval options for small drones under 25 kilograms. This has helped qualified operators self-assess and approve their operational areas, reducing approval times for these activities.

Market Outlook 2026-2034:

Australia’s drones market is positioned for sustained growth, underpinned by rising defense investments, expanding commercial applications, and evolving regulatory support. The market generated a revenue of USD 678.1 Million in 2025 and is projected to reach a revenue of USD 1,651.2 Million by 2034, growing at a compound annual growth rate of 10.02% from 2026-2034. Increasing adoption of autonomous technologies, advancements in AI-powered drone analytics, and expanding BVLOS operations are expected to drive higher revenue streams and foster a more competitive, mature, and innovative drone landscape across the country.

Australia Drones Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Rotary Wing |

56.3% |

|

Component |

Hardware |

44.2% |

|

Payload |

<25 Kilograms |

52.4% |

|

Point of Sale |

Original Equipment Manufacturers |

62.7% |

|

End Use Industry |

Agriculture |

24.5% |

|

Region |

Queensland |

26.8% |

Type Insights:

- Fixed Wing

- Rotary Wing

- Hybrid

Rotary wing segment leads the market with a revenue share of 56.3% of the total Australia drones market in 2025.

Rotary wing drones, including quadcopters and multirotor systems, are the most widely adopted type in Australia due to their exceptional maneuverability, vertical takeoff and landing capabilities, and ability to hover with precision. These attributes make them ideal for a broad range of applications spanning aerial photography, infrastructure inspection, environmental monitoring, and emergency response operations. Their versatility enables effective data collection in tight and confined spaces where fixed wing designs face operational limitations.

The segment’s dominance is further supported by ongoing technological advancements and expanding commercial use cases. Apart from this, key market players are launching a cutting-edge rotary wing drone specifically designed for environmental monitoring applications in Australia. Growing adoption across agriculture for crop surveillance and in construction for site management, combined with increasing integration of advanced sensors and cameras, is reinforcing the rotary wing segment’s leading position in the market.

Component Insights:

- Hardware

- Software

- Accessories

Hardware dominates the market with a share of 44.2% of the total Australia drones market in 2025.

The hardware segment encompasses airframes, propulsion systems, sensors, cameras, batteries, navigation modules, and communication equipment that form the core of drone platforms. Demand for hardware is sustained by new drone deployments across commercial, agricultural, defense, and industrial sectors, where end users require reliable and high-performance physical components to support increasingly complex missions. Continuous investment in improved battery life, sensor accuracy, and payload capacity is expanding the operational envelope of drone hardware.

The segment benefits from Australia’s growing emphasis on sovereign manufacturing capabilities and defense modernization. For instance, the Australian Defence Force acquired more than AUD 1.5 million worth of Australian-manufactured drones in August 2025 under the Sovereign UAS Challenge, reflecting the government’s commitment to developing domestic drone hardware production. This focus on locally produced hardware, combined with rising commercial procurement, continues to anchor the hardware segment’s market leadership.

Payload Insights:

- <25 Kilograms

- 25-170 Kilograms

- >170 Kilograms

<25 kilograms is the largest segment, accounting for 52.4% of the total Australia drones market in 2025.

Lightweight drones with payloads under 25 kilograms represent the most widely utilized category in Australia, favored for their portability, ease of deployment, and compliance with existing regulatory frameworks. These drones serve a diverse range of applications including agricultural crop monitoring, real estate photography, infrastructure inspection, and environmental surveying. Their lower operational costs and simplified licensing requirements make them accessible to both small operators and large enterprises.

Regulatory developments are further strengthening this segment’s growth trajectory. In October 2025, CASA’s new BVLOS trial pathways were specifically designed for small drones under 25 kilograms, enabling qualified operators to conduct long-range missions with streamlined approvals. This regulatory facilitation, combined with advancing miniaturized sensor technologies and improved battery endurance, is broadening the operational scope and commercial viability of sub-25 kilogram drones across Australian industries.

Point of Sale Insights:

- Original Equipment Manufacturers (OEM)

- Aftermarket

Original equipment manufacturers (OEMs) hold the largest share at 62.7% of the total Australia drones market in 2025.

Original Equipment Manufacturers (OEMs) dominate the point of sale landscape in the Australia drones market, accounting for the largest share due to their direct control over product design, technology integration, and distribution channels. OEMs cater to a wide range of end users including defense, agriculture, mining, and infrastructure, offering advanced drones with integrated software, sensors, and analytics capabilities. Their strong presence is supported by government contracts, enterprise demand, and increasing adoption of high-performance drones for commercial applications such as surveying, mapping, and surveillance. OEMs also benefit from brand trust, compliance with aviation regulations, and the ability to provide end-to-end solutions, including maintenance and training services, which strengthens their market position.

The aftermarket segment, while smaller in comparison, plays a crucial supporting role by addressing demand for spare parts, repairs, upgrades, and accessories. Growth in this segment is driven by the rising installed base of drones across industries and the need for regular maintenance to ensure operational efficiency and safety compliance. Aftermarket providers offer cost-effective solutions that extend drone lifecycle and enhance performance, particularly for small and medium enterprises seeking budget-friendly alternatives. Increasing customization requirements and demand for specialized components such as batteries, cameras, and propellers further contribute to the steady expansion of the aftermarket segment.

End Use Industry Insights:

Access the comprehensive market breakdown Request Sample

- Construction

- Agriculture

- Military and Defense

- Law Enforcement

- Logistics

- Media and Entertainment

- Others

Agriculture accounts for the highest revenue share of 24.5% of the total Australia drones market in 2025.

Agriculture accounts for the highest revenue share in the market, driven by the country’s large-scale farming operations and increasing focus on precision agriculture. Farmers are rapidly adopting drones to monitor crop health, optimize irrigation, and improve yield efficiency, particularly in regions facing water scarcity and climate variability. Drones equipped with multispectral and thermal sensors enable real-time data collection, helping farmers detect issues such as pest infestations, nutrient deficiencies, and soil variability at an early stage. This data-driven approach supports informed decision-making and reduces input costs related to fertilizers and pesticides.

The use of drones for crop spraying and seeding is also gaining traction, as it allows faster coverage of vast agricultural land with improved accuracy and reduced labor dependency. In Australia, where labor shortages and rising operational costs are ongoing concerns, drones offer a practical and scalable solution. Government support for agri-tech adoption and advancements in drone technology further strengthen their use in farming practices. While other industries such as construction, defense, and logistics are expanding their use of drones for surveying, surveillance, and delivery applications, agriculture continues to lead due to its consistent and high-volume demand. The integration of drones with farm management systems is expected to sustain this dominance.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Queensland dominates the Australia drones market with a 26.8% share in 2025.

Queensland dominates the Australia drones market, supported by its expansive geography, strong presence of agriculture, mining, and infrastructure sectors, and increasing adoption of advanced technologies. The state’s large agricultural base drives significant demand for drones in precision farming, crop monitoring, and land management. Farmers in Queensland are increasingly using drones to improve productivity and manage vast farmlands efficiently, contributing to higher adoption rates compared to other regions. The mining industry, a key economic pillar in Queensland, further accelerates drone usage for applications such as site surveying, inspection, and safety monitoring.

Drones enable faster data collection in remote and hazardous locations, reducing operational risks and costs. Additionally, infrastructure development projects across the state, including roads, railways, and urban expansion, are creating strong demand for aerial mapping and surveying solutions. Queensland also benefits from favorable weather conditions that support year-round drone operations, unlike some southern regions with more variable climates. Growing investments in smart technologies and increasing awareness among enterprises about the efficiency gains offered by drones continue to strengthen regional demand.

Market Dynamics:

Growth Drivers:

Why is the Australia Drones Market Growing?

Increasing Government Investment in Defense Drone Technology

The Australian government is substantially expanding its investment in drone technology for military and defense applications, creating a powerful growth catalyst for the broader drones market. Under the leadership of Prime Minister Anthony Albanese, Australia has committed to spending over AUD 10 billion on drone capabilities over the coming decade, with AUD 4.3 billion specifically earmarked for uncrewed aerial platforms and AUD 690 million dedicated to acquiring tactical drone systems for the Army. These investments reflect Australia’s strategic imperative to modernize its defense capabilities in response to evolving regional security dynamics.

Rising Adoption of Drones in Agriculture and Precision Farming

Australia’s agriculture sector is emerging as a major growth driver for the drones market as farmers increasingly adopt precision farming technologies to enhance productivity and reduce operational costs. The country’s vast and geographically diverse farmland, combined with a declining rural workforce, has made drone-based solutions essential for efficient crop management. Drones equipped with advanced sensors enable real-time monitoring of crop health, soil conditions, and irrigation needs, facilitating data-driven decision-making that optimizes resource utilization.

Supportive Regulatory Framework and BVLOS Advancements

Australia’s Civil Aviation Safety Authority has been proactive in developing regulatory frameworks that facilitate commercial drone operations, serving as a significant enabler for market expansion. The regulatory landscape is evolving to accommodate increasingly complex drone missions, including beyond visual line of sight operations that are critical for long-range inspections, agricultural applications, and logistics services. This regulatory progression is reducing operational barriers and encouraging broader industry adoption of drone technologies.

Market Restraints:

What Challenges the Australia Drones Market is Facing?

Regulatory Complexity and Airspace Management Constraints

Despite evolving regulatory frameworks, navigating drone licensing requirements, operational restrictions, and airspace management rules remains complex, particularly for small and medium-sized enterprises. Strict compliance with CASA guidelines and the need for multiple approvals for different operational scenarios can slow adoption and increase the cost of entry for new operators, limiting broader market penetration.

Privacy Concerns and Community Opposition

The growing presence of drones in populated areas has raised significant privacy and noise concerns among communities. Opposition from residents regarding surveillance capabilities, noise disturbance, and safety risks associated with drone operations, particularly in suburban delivery and law enforcement applications, can impede expansion into urban environments and constrain the commercial scalability of certain drone services.

Skilled Workforce Shortages and Training Gaps

As drone applications become increasingly sophisticated, the demand for skilled operators, data analysts, and maintenance technicians continues to outpace available supply. The shortage of qualified personnel in drone operation, programming, and maintenance creates bottlenecks in scaling commercial and industrial drone services, particularly in regional and remote areas where technical expertise is limited.

Competitive Landscape:

The Australia drones market is characterized by a dynamic competitive environment featuring global technology leaders alongside innovative domestic companies. Market participants are focusing on expanding product portfolios, enhancing autonomous capabilities, and strengthening software-driven analytics platforms to differentiate their offerings. Competition is intensified by government emphasis on sovereign manufacturing and local industry support, encouraging Australian companies to develop world-class drone solutions. Strategic partnerships, defense contracts, technology licensing agreements, and investments in research and development are key strategies employed by market players to capture market share and capitalize on the country’s growing demand for advanced drone solutions.

Recent Developments:

- In November 2025, Australian global military communications leader DTC, part of Codan, has commenced local production of its newest advanced drone radio technology; this system is now acknowledged as Ukraine’s choice for drone communications. The BluSDR-6 had its official launch at MiLCIS 2025 in Canberra, with attendance from Ukraine’s Ambassador to Australia Vasyl Myroshnychenko, as well as representatives from the defence industry and government. Created by Codan's DTC division, these radios have turned into an essential support for Ukraine’s frontline unmanned systems, ensuring connectivity in GPS-denied environments and amidst ongoing Russian electronic warfare assaults.

- In August 2025, DroneShield, a leading Australian firm specializing in AI-driven counter-drone and electronic warfare technologies, is excited to declare its position as Platinum Sponsor of the 2025 Tiny Whoop Australian Championships, the top micro drone racing competition in Australia. The Championships are scheduled for 13–14 September 2025 at the Deakin Football Club in Canberra. The event receives backing from Jesse Perkins, the creator of the Tiny Whoop product and brand, whose groundbreaking work in 2015 brought micro-FPV drone racing to the masses and ignited a worldwide phenomenon.

- In March 2025: Australian aerospace company Drone Forge and Airbus have agreed to a Letter of Intent (LOI) to work together on the deployment and operational integration of the Flexrotor unmanned aerial system. This accord, which encompasses the procurement of Flexrotor systems, represents an essential milestone in revolutionizing uncrewed aviation with innovative solutions and technologies designed for tactical operations.

Australia Drones Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fixed Wing, Rotary Wing, Hybrid |

| Components Covered | Hardware, Software, Accessories |

| Payloads Covered | <25 Kilograms, 25-170 Kilograms, >170 Kilograms |

| Point of Sales Covered | Original Equipment Manufacturers (OEM), Aftermarket |

| End Use Industries Covered | Construction, Agriculture, Military and Defense, Law Enforcement, Logistics, Media and Entertainment, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Drones Market Report

The Australia drones market size was valued at USD 678.1 Million in 2025.

The market is expected to grow at a compound annual growth rate of 10.02% from 2026-2034 to reach USD 1,651.2 Million by 2034.

Rotary wing drones, holding the largest revenue share of 56.3% in 2025, lead the Australia drones market due to their versatility, hovering capabilities, and wide adoption across agriculture, construction, defense, and commercial applications.

Key factors driving the Australia drones market include increasing government defense investments, rising adoption of precision agriculture technologies, expanding commercial drone applications, supportive regulatory developments, advancements in AI and autonomous navigation, and growing demand for drone delivery services.

Major challenges include regulatory complexity and airspace management constraints, privacy concerns and community opposition in populated areas, skilled workforce shortages, cybersecurity vulnerabilities, and the high costs of advanced drone systems for smaller operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade