Australia E-Wallet Market Size, Share, Trends and Forecast by Type, Ownership, Technology, Vertical, and Region, 2026-2034

Australia E-Wallet Market Overview:

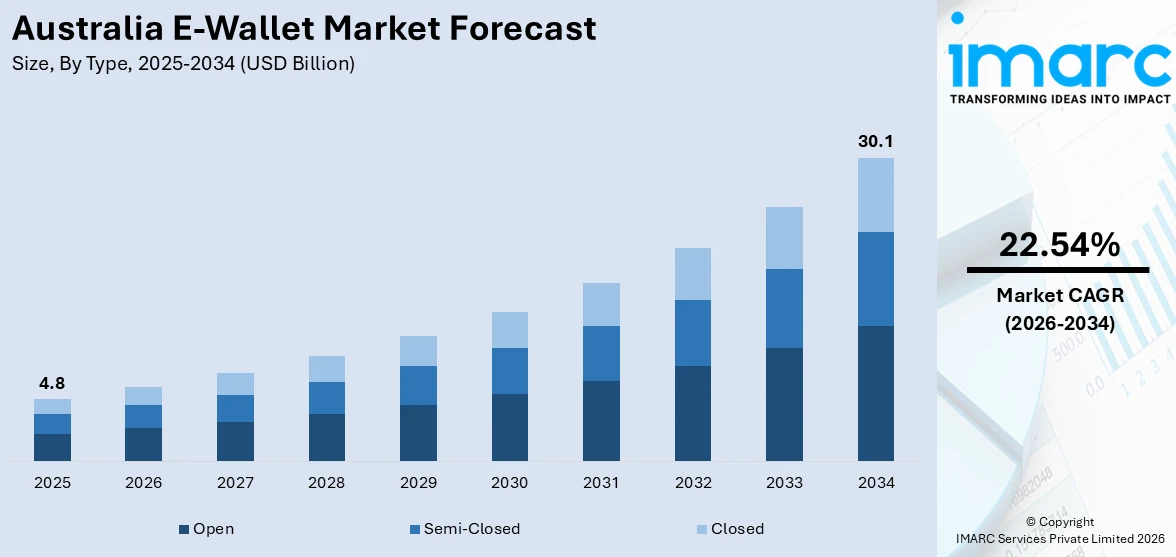

The Australia e-wallet market size reached USD 4.8 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 30.1 Billion by 2034, exhibiting a growth rate (CAGR) of 22.54% during 2026-2034. The market is propelled by accelerating digital payment usage, enhanced security features, and increased service integration. As habits of consumers trend toward convenience and contactless payments, the industry is poised for consistent growth across a range of daily financial activities.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 4.8 Billion |

| Market Forecast in 2034 | USD 30.1 Billion |

| Market Growth Rate 2026-2034 | 22.54% |

Australia E-Wallet Market Trends:

Integration of E-Wallets into Daily Services

One of the major trends influencing the Australian digital payments environment is the rise in embedding e-wallets into daily services like transport, eating out, bill payment, and entertainment. Consumer preference for convenience is fueling this trend, where users can control various facets of their financial lives through one digital platform. For instance, in May 2024, Shaype and ANNA Money released Australia's first AI-driven business finance "super app" for SMEs, combining business banking, tax, expenses, and company setup into a single streamlined platform for Pty Ltd businesses. Moreover, with secure interfaces and advanced APIs, e-wallets are facilitating smooth payments across an increasingly broad spectrum of public and private services. Mobile technology's combination with financial functionality is rendering digital wallets a requirement for everyday actions. This merger is also having an impact on merchant ecosystems, which are being modified to enable digital-first payment habits. The trend enables higher frequency of interaction, leading to user retention and satisfaction. As these platforms develop further into integrated financial instruments, Australia e-wallet market growth will continue to improve considerably, solidifying the industry's place in the overall digital economy.

To get more information on this market Request Sample

Biometric and Device-Based Authentication Enhancement

Device and biometric-based authentication is surfacing as an urgent trend in the e-wallets landscape in Australia. In the face of increasing consumer apprehension around cybersecurity, users are seeking solutions that provide secure yet seamless entry to digital wallets. Device-based, facial recognition, and fingerprint-scanning-based authentication is taking precedence over legacy passwords and PIN-based authentication, with increased security and efficiency of entry. These authentication protocols secure sensitive financial information and enhance the overall user experience, building consumer trust and adoption. Furthermore, the widespread use of smartphones with biometric sensors has made it highly accessible across all demographics. With regulatory standards improving to accommodate these technologies, e-wallet platforms are investing in strong identity verification systems. This focus on security via innovation is making digital wallets more attractive in urban and rural areas alike. Therefore, Australia e-wallet market share is improving as trust and accessibility keep increasing. For example, in April 2024, Waave introduced its biometrically secured Waave Wallet in Australia, with a real-time, account-to-account payment that features biometric authentication, targeted at minimizing fraud and removing card fees for users.

Increase in Contactless and Offline Transaction Facilities

One of the most significant trends in Australia's e-wallet space is the development of contactless and offline transaction capabilities. Customers are ever more looking for quick, easy payment solutions that do not completely depend on being online all the time. Offline capabilities in e-wallets allow for payments even in places with no or low signal, improving flexibility in varying contexts. At the same time, the demand for contactless payments remains on an upward trend based on its speed, safety, and convenience, especially in post-pandemic retail environments. This two-pronged growth caters to the requirement for resilience and continuity in transactions. Advancements in technology in the form of tokenization and secure near-field communication (NFC) are facilitating this transformation, making offline and contactless payments both efficient and secure. The capacity to transact across different conditions broadens e-wallets' appeal across different customer bases and geographies. Consequently, Australia e-wallet market outlook is set to witness consistent advancement, fueled by pragmatic innovation and openness.

Australia E-Wallet Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region level for 2026-2034. Our report has categorized the market based on type, ownership, technology, and vertical.

Type Insights:

- Open

- Semi-Closed

- Closed

The report has provided a detailed breakup and analysis of the market based on the type. This includes open, semi-closed, and closed.

Ownership Insights:

- Banks

- Telecom Companies

- Device Manufacturers

- Tech Companies

A detailed breakup and analysis of the market based on the ownership have also been provided in the report. This includes banks, telecom companies, device manufacturers, and tech companies.

Technology Insights:

- Near Field Communication

- Optical/QR Code

- Digital Only

- Text-Based

The report has provided a detailed breakup and analysis of the market based on the technology. This includes near field communication, optical/QR code, digital only, and text-based.

Vertical Insights:

Access the comprehensive market breakdown Request Sample

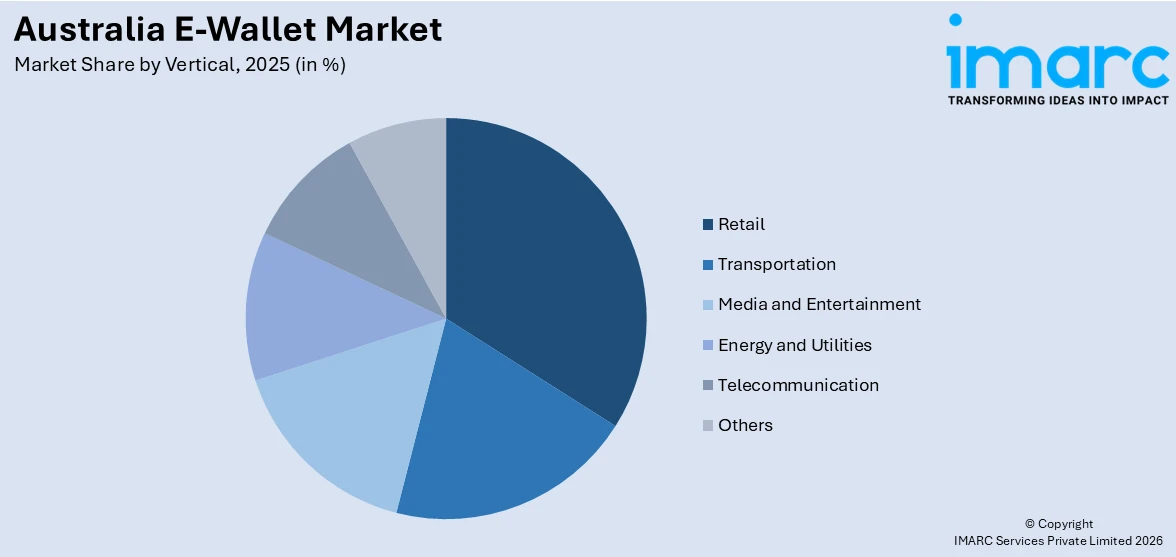

- Retail

- Transportation

- Media and Entertainment

- Energy and Utilities

- Telecommunication

- Others

A detailed breakup and analysis of the market based on the vertical have also been provided in the report. This includes retail, transportation, media and entertainment, energy and utilities, telecommunication, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia E-Wallet Market News:

- In March 2025, Australian Payments Plus aligned with Google in bringing the eftpos capability and Least Cost Routing (LCR) to Google Wallet. This enables merchants to route payments through the cheaper eftpos network. ANZ and Suncorp Bank have brought eftpos multi-network debit cards to life, with other issuers following later in 2025.

- In August 2024, Easy Crypto released its intuitive cryptocurrency wallet for first-time investors in Australia, making it easy to buy, exchange, and hold crypto assets, with robust security features, designed to meet the increasing demand for investment in digital currencies among ordinary Australians.

Australia E-Wallet Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Open, Semi-Closed, Closed |

| Ownerships Covered | Banks, Telecom Companies, Device Manufacturers, Tech Companies |

| Technologies Covered | Near Field Communication, Optical/QR Code, Digital Only, Text-Based |

| Verticals Covered | Retail, Transportation, Media and Entertainment, Energy and Utilities, Telecommunication, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia e-wallet market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia e-wallet market on the basis of type?

- What is the breakup of the Australia e-wallet market on the basis of ownership?

- What is the breakup of the Australia e-wallet market on the basis of technology?

- What is the breakup of the Australia e-wallet market on the basis of vertical?

- What is the breakup of the Australia e-wallet market on the basis of region?

- What are the various stages in the value chain of the Australia e-wallet market?

- What are the key driving factors and challenges in the Australia e-wallet?

- What is the structure of the Australia e-wallet market and who are the key players?

- What is the degree of competition in the Australia e-wallet market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia e-wallet market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia e-wallet market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia e-wallet industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)