Australia Electric Vehicle (EV) Charging Market Size, Share, Trends and Forecast by Charging Station Type, Vehicle Type, Installation Type, Charging Level, Connector Type, Application and Region, 2026-2034

Australia Electric Vehicle (EV) Charging Market Size, Share, Trends & Forecast (2026-2034)

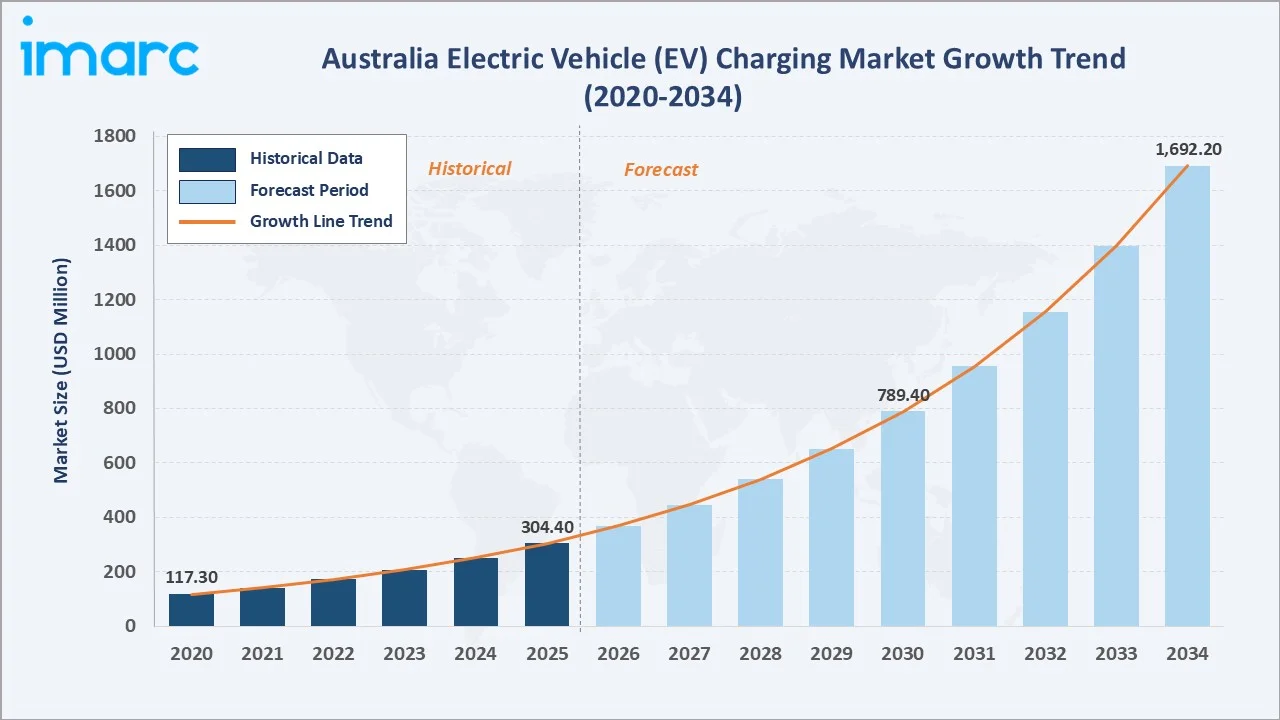

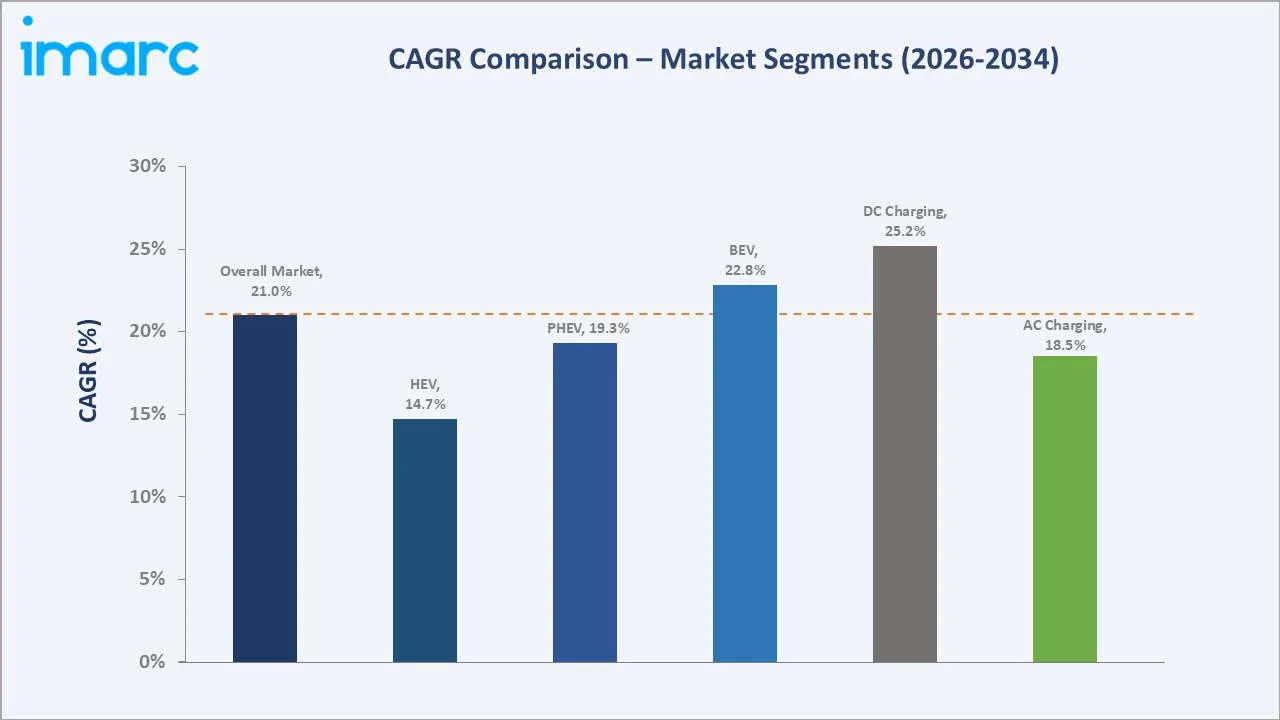

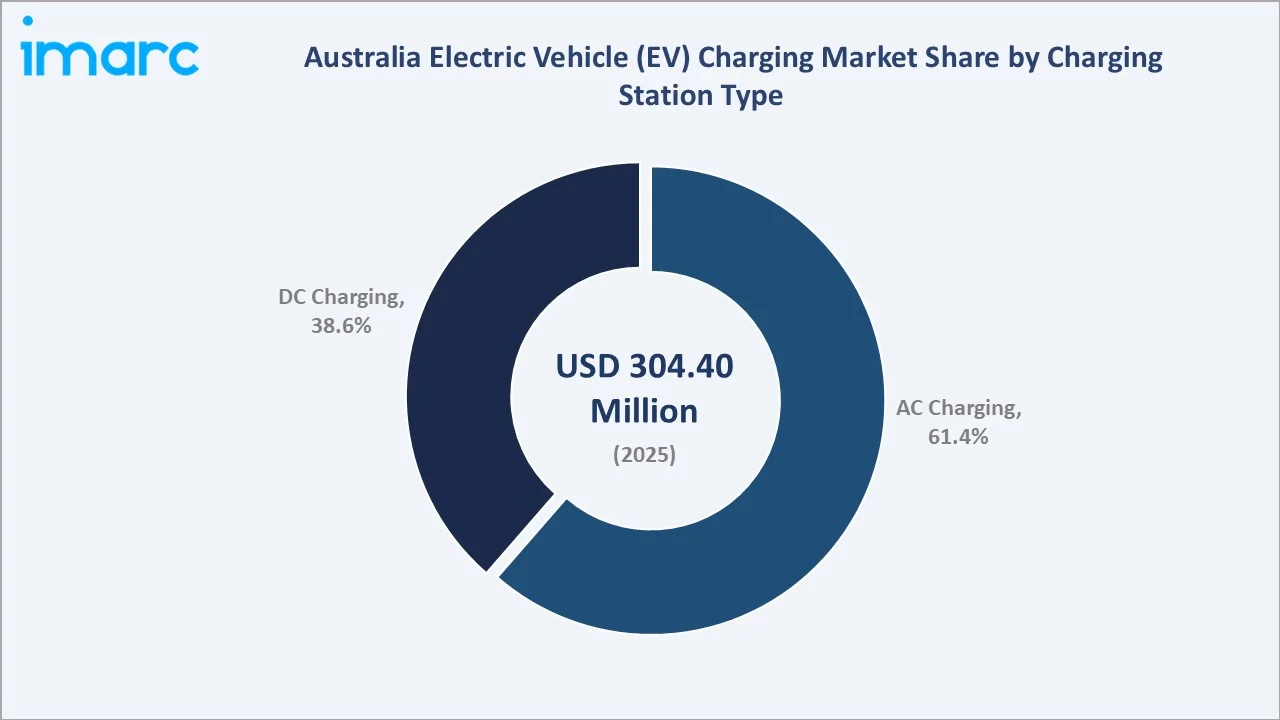

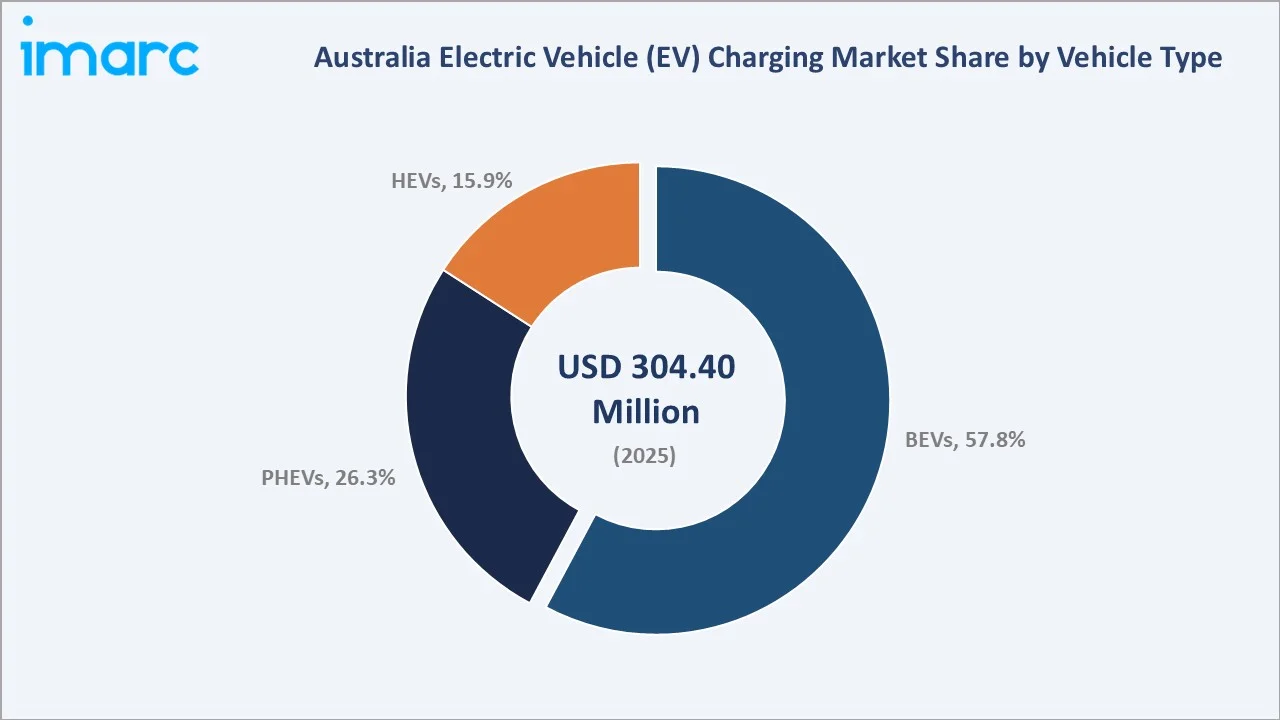

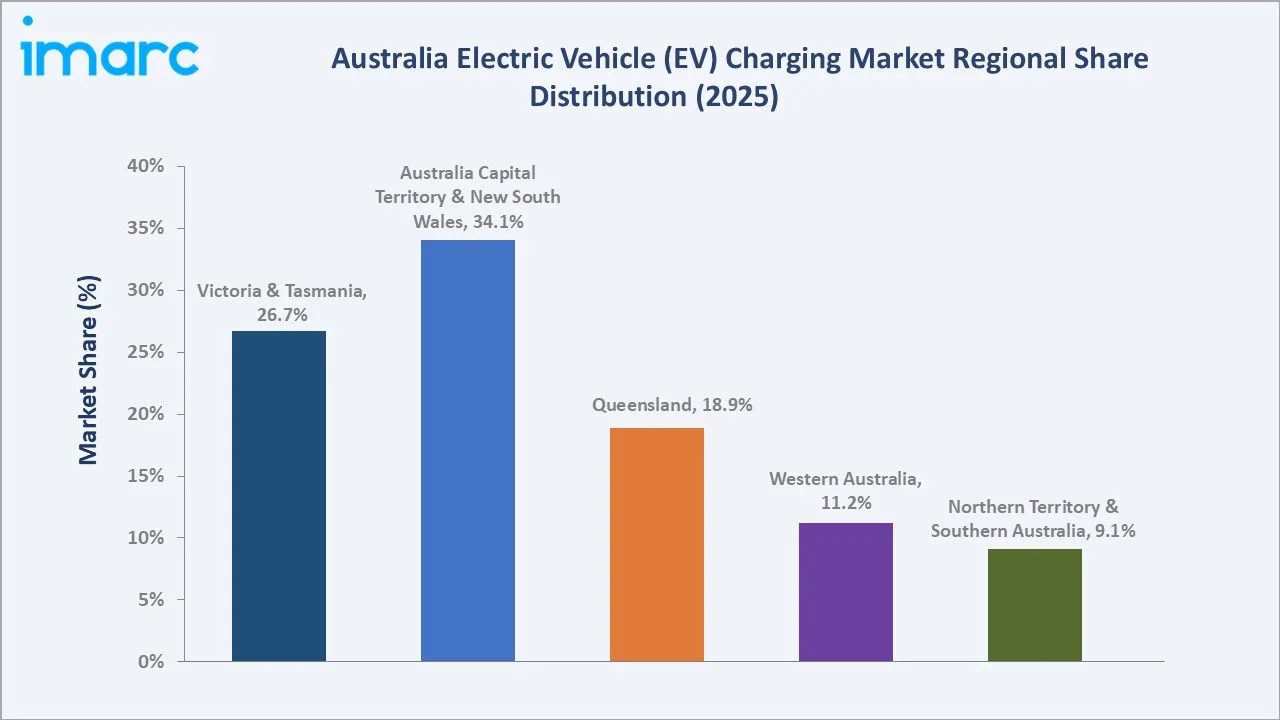

The Australia electric vehicle (EV) charging market reached USD 304.4 Million in 2025. It is projected to reach USD 1,692.2 Million by 2034, exhibiting a CAGR of 21.00% during 2026-2034. AC Charging holds the dominant share at 61.4% (2025), while Battery Electric Vehicles (BEV) lead at 57.8%. ACT & New South Wales is the leading region, contributing 34.1% of the national market share. Strong government support through the New Vehicle Efficiency Standard (NVES), rapid infrastructure expansion, and growing fleet electrification are key growth drivers.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 304.4 Million |

|

Forecast Market Size (2034) |

USD 1,692.2 Million |

|

CAGR (2026-2034) |

21.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Market Size (2020) |

USD 117.3 Million |

|

Market Size (2030) |

USD 789.4 Million |

|

Dominant Charging Type |

AC Charging (61.4%, 2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle (57.8%, 2025) |

|

Leading Region |

ACT & New South Wales (34.1%, 2025) |

Australia's EV charging market expanded from USD 117.3 Million in 2020 to USD 304.4 Million in 2025. The market is anchored at USD 789.4 Million in 2030, and is forecast to reach USD 1,692.2 Million by 2034. This exceptional 21% CAGR reflects the convergence of policy support, rising EV penetration, and private capital inflows into charging infrastructure. Australia's unique geographic and climatic conditions have also pushed innovation in climate-resilient, solar-powered, and highway-grade charging solutions.

To get more information on this market, Request Sample

Australia's high-power public charging locations grew by 90% year-on-year, reaching 1,059 sites with 1,849 individual chargers as of mid-2024 (Electric Vehicle Council). The EV Council also confirmed 22% infrastructure growth in H1 2025 alone. BEVs at 57.8% dominate the vehicle mix, growing at the fastest rate as zero-emission regulations tighten. DC Charging, while smaller at 38.6%, grows faster than AC at ~25% CAGR through 2034, supported by highway fast-charging corridors and commercial fleet depot installations.

Executive Summary

Australia's EV charging market reached USD 304.4 Million in 2025 and represents one of Asia-Pacific's most dynamic EV infrastructure markets. The charging ecosystem encompasses AC and DC charging stations, smart network software, grid integration services, and fleet charging platforms deployed across residential, commercial, and public highway corridors. The market is projected to reach USD 1,692.2 Million by 2034, driven by a 21.00% CAGR over the forecast period.

The federal government's New Vehicle Efficiency Standard (NVES), provides a comprehensive policy framework to accelerate EV uptake and charging infrastructure deployment. “Driving the Nation Fund” allocated AUD 39.3 million to install 117 EV chargers on key highway routes. At the state level, NSW, Victoria, and Queensland have deployed tailored incentive programs covering rebates, zero-emissions roadmaps, and fast-charging corridor grants.

AC Charging leads at 61.4% market share, anchored by residential and workplace installations. DC Charging at 38.6% is the faster-growing category. BEVs at 57.8% dominate vehicle demand. ACT & New South Wales leads regionally at 34.1%, supported by its large urban population and government-led charging mandates for new developments.

Key Market Insights

|

Insight |

Data |

|

Dominant Charging Type |

AC Charging - 61.4% share (2025) |

|

Dominant Vehicle Type |

Battery Electric Vehicle (BEV) - 57.8% (2025) |

|

Leading Region |

ACT & New South Wales - 34.1% (2025) |

|

Fastest Growing Segment |

DC Charging (~25.2% CAGR, 2026-2034) |

|

Top Companies |

Tesla Inc., Australian Motoring Services (AMS), Evie Networks, and JOLT |

|

Market Opportunity |

V2G technology, solar-powered stations, regional corridor buildout |

Key Analytical Observations Supporting The Above Data:

- AC Charging at 61.4%: AC chargers dominate due to lower installation costs, compatibility with Level 1 and Level 2 home and workplace setups, and high suitability for overnight residential charging. Over 70% of EV owners in Australia primarily charge at home, sustaining AC infrastructure's share advantage.

- BEV at 57.8%: BEVs lead due to stronger government incentives, greater model availability across passenger and commercial segments, and lower total cost of ownership compared to PHEVs and HEVs. BEV sales surged 157% in 2023 year-on-year (Electric Vehicle Council), sustaining dominant demand for high-power DC and Level 2 AC infrastructure.

- ACT & NSW at 34.1%: New South Wales alone had 200+ public EV charging stations as of 2024, the most of any state. NSW's updated 2021 EV Strategy targets 50% of new car sales as BEVs by 2030 and mandates expanded kerbside charging networks.

- DC Charging fastest growing (~25.2% CAGR): Ultra-fast DC charging is being prioritized for national highway corridors and commercial fleet depots. The NRMA-government partnership is building over 100 highway DC charging stations at 150 km intervals across Australia.

- V2G & Solar: Vehicle-to-Grid pilot projects in the ACT are demonstrating bi-directional energy flows, and Queensland and Western Australia are leading solar canopy-integrated charging deployments, reflecting Australia's world-leading rooftop solar penetration of over 30% of households.

Australia EV Charging Market Overview

Australia's EV charging market encompasses the manufacture, installation, operation, and software management of electric vehicle charging infrastructure. This includes AC wall boxes, DC fast chargers, ultra-fast highway dispensers, portable charging units, and smart network platforms deployed across residential, commercial, industrial, and public highway locations.

The ecosystem integrates charging hardware manufacturers, software and network operators, energy retailers, EV OEMs, government bodies, fleet operators, and end consumers. The New Vehicle Efficiency Standard (NVES), effective from 2025, is a landmark regulatory catalyst that will accelerate EV model supply and directly increase charging infrastructure demand across all segments and geographies.

Market Dynamics

To evaluate market opportunities, Request Sample

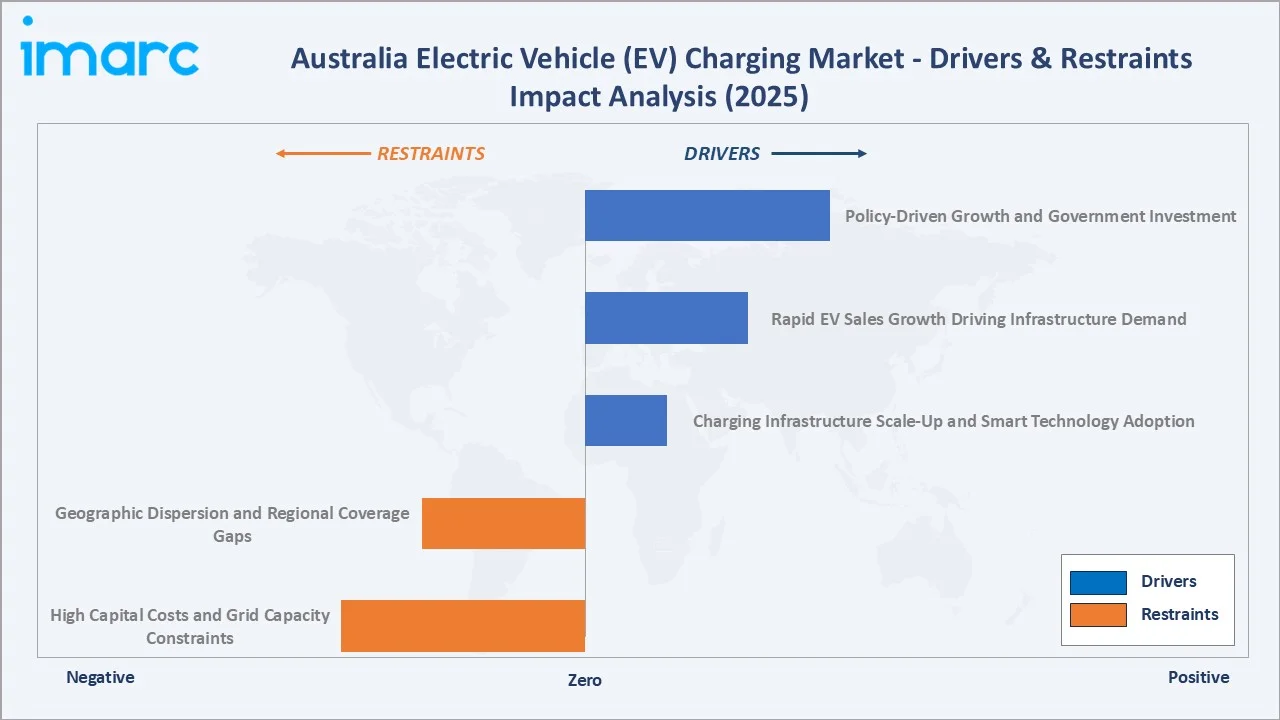

Market Drivers

- Policy-Driven Growth and Government Investment: Australia's federal and state governments have established a comprehensive policy framework driving EV charging market expansion. The New Vehicle Efficiency Standard (NVES) provided a dedicated roadmap. Government’s “Driving the Nation Fund” allocated AUD 39.3 million to deploy 117 EV chargers on key highway routes (energy.gov.au, 2025). NSW's EV Strategy targets 50% BEV new-car-sales share by 2030. These policy levers collectively de-risk private investment and stimulate demand.

- Rapid EV Sales Growth Driving Infrastructure Demand: Australia recorded 114,283 EV sales in 2024, a 16.1% increase year-on-year, with EVs representing 9.5% of new car sales by September 2024 (Electric Vehicle Council). This rapid fleet growth directly creates demand for public, residential, and commercial charging infrastructure, accelerating market revenues.

- Charging Infrastructure Scale-Up and Smart Technology Adoption: High-power public charging locations grew 90% year-on-year to 1,059 sites with 1,849 chargers by mid-2024 (Electric Vehicle Council). Australia's charging infrastructure grew a further 22% in H1 2025. Smart charging technologies including Vehicle-to-Grid (V2G) pilots, app-based booking platforms, IoT-enabled load management, and solar-integrated stations are expanding the addressable market beyond hardware to software and energy services.

- Fleet Electrification and Corporate Sustainability Mandates: Large logistics, utilities, government, and mining fleets are committing to EV transitions, driving demand for depot, workplace, and renewable-powered charging solutions. Charging-as-a-Service (CaaS) models are enabling organizations to adopt EV charging without upfront capital expenditure. Major retailers including Bunnings and Officeworks are partnering with charging operators for nationwide site rollouts, creating high-visibility commercial charging hubs.

Market Restraints

- Geographic Dispersion and Regional Coverage Gaps: Australia's vast geography creates significant challenges in achieving uniform charging coverage. Remote and regional areas face high infrastructure costs per charger due to low traffic density and long distances between population centers. Deloitte Australia's January 2024 report identified insufficient regional infrastructure as a primary barrier to accelerating EV adoption beyond urban areas.

- High Capital Costs and Grid Capacity Constraints: Ultra-fast DC charging installations require significant upfront capital investment. Grid augmentation costs in areas with limited electricity distribution capacity add further barriers. AusNet's EV integration strategy identifies a 3% increase in peak operational demand by 2031 from EV charging alone, requiring AUD 120 million in network augmentation (AusNet EV Strategy, 2025).

Market Opportunities

- Renewable Energy Integration and V2G Systems: Australia's world-leading rooftop solar penetration exceeding 30% of households creates unique opportunity for solar-powered charging stations, battery-backed microgrids, and V2G energy systems. Queensland and Western Australia are active deployment zones for solar canopy charging. V2G pilot programs in the ACT are demonstrating commercial viability for bi-directional energy services, creating new revenue streams for charging operators and energy retailers.

- Regional and Tourism Corridor Expansion: Government-funded destination charging grants are enabling councils, wineries, national parks, and regional motels to install EV chargers. This creates a tourism-integrated charging network across iconic routes. NSW and Tasmania received government-backed grants for tourism-linked EV charging installations. Strategic deployments along the Great Ocean Road, Kimberley corridor, and Nullarbor Plain will expand the charging footprint substantially through 2034.

Market Challenges

- Interoperability and Standardization: Australia's EV charging market encompasses multiple connector standards including CCS, CHAdeMO, Type 1, Type 2, and Tesla Supercharger. Lack of full interoperability across networks creates consumer friction and slows adoption. Government-led standardization initiatives under the NVES are working to address this, but implementation is gradual.

- Skilled Workforce Shortage: The rapid expansion of charging infrastructure requires licensed electricians, EV technicians, and software engineers with specialized skills. The Australian Government's AUD 325 million TAFE Centres of Excellence initiative addresses this through vocational training programs for EV and clean-tech sectors. However, workforce shortfalls remain a near-term bottleneck for deployment velocity.

Emerging Market Trends

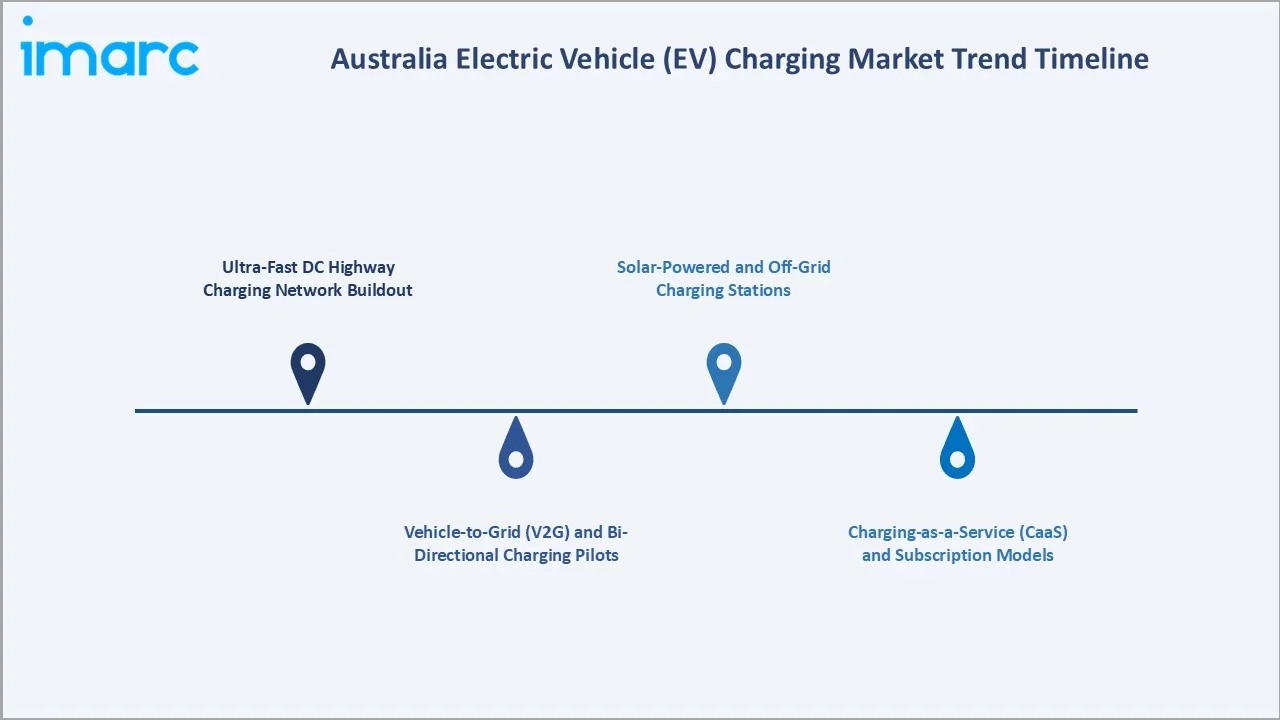

1. Ultra-Fast DC Highway Charging Network Buildout

The federal government's partnership with NRMA to install 100+ DC charging stations on key highway routes at 150 km intervals is establishing a national EV backbone network. The Driving the Nation Fund's DRIVEN grants stream added further public chargers from late 2025. This trend is rapidly reducing range anxiety and unlocking long-distance EV travel across Australia.

2. Vehicle-to-Grid (V2G) and Bi-Directional Charging Pilots

Australia's rooftop solar leadership positions it as a global frontrunner in V2G technology adoption. ACT government-backed V2G trials are allowing EVs to feed electricity back into homes and the grid during peak demand periods. As V2G matures, charging operators and energy retailers are developing integrated energy-transport business models that could fundamentally reshape grid management and EV infrastructure economics.

3. Solar-Powered and Off-Grid Charging Stations

Solar canopy EV charging stations are proliferating in Queensland and Western Australia, harnessing Australia's exceptional solar resource to provide clean, off-grid charging. These installations deploy co-located battery storage for 24-hour availability, providing reliability in locations with limited grid access. This trend is commercially critical for regional tourism corridor deployments and mining sector applications.

4. Charging-as-a-Service (CaaS) and Subscription Models

Corporate and fleet operators are increasingly adopting Charging-as-a-Service models, which eliminate upfront capital expenditure and shift to operational expense-based charging infrastructure. CaaS providers offer bundled hardware, installation, software, maintenance, and energy management under multi-year contracts. This model is accelerating fleet electrification across logistics, retail, government, and resources sectors, creating predictable recurring revenue for infrastructure providers.

5. Smart Grid Integration and Dynamic Load Management

Smart charging platforms using IoT sensors, real-time pricing signals, and demand-response controls are enabling EV charging infrastructure to actively participate in grid management. Network providers including Chargefox and Evie Networks offer end-to-end platforms integrating booking, load management, dynamic pricing, and operator analytics. As EV penetration approaches 10% of new sales, grid-smart charging becomes operationally essential for network stability.

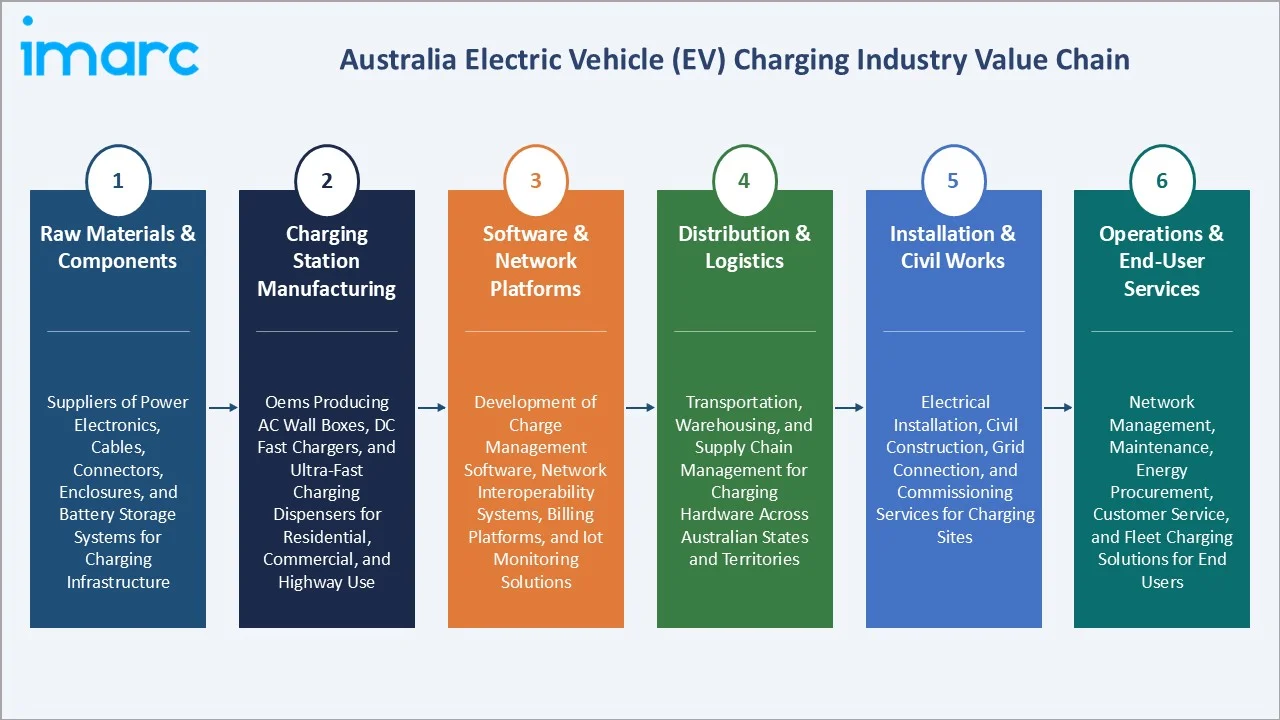

Industry Value Chain Analysis

Australia's EV charging value chain integrates raw material supply, component manufacturing, charging hardware production, software and network development, installation and service delivery, and end-user operations and monitoring.

|

Stage |

Key Participants |

|

Raw Materials & Components |

Suppliers of power electronics, cables, connectors, enclosures, and battery storage systems for charging infrastructure |

|

Charging Station Manufacturing |

OEMs producing AC wall boxes, DC fast chargers, and ultra-fast charging dispensers for residential, commercial, and highway use |

|

Software & Network Platforms |

Development of charge management software, network interoperability systems, billing platforms, and IoT monitoring solutions |

|

Distribution & Logistics |

Transportation, warehousing, and supply chain management for charging hardware across Australian states and territories |

|

Installation & Civil Works |

Electrical installation, civil construction, grid connection, and commissioning services for charging sites |

|

Operations & End-User Services |

Network management, maintenance, energy procurement, customer service, and fleet charging solutions for end users |

The installation and civil works stage represents the most commercially competitive phase of Australia's EV charging value chain, particularly in regional highway corridor buildouts where site complexity and grid connection costs are highest. The operations and end-user services stage is the value chain's fastest-growing recurring revenue tier.

Technology Landscape in the Australia EV Charging Industry

AC Charging Technology (Level 1 & Level 2)

AC charging technology supports Level 1 (2.4 kW) and Level 2 (7-22 kW) installations at residential and commercial locations. Smart AC chargers now integrate Wi-Fi, OCPP (Open Charge Point Protocol) compliance, dynamic load balancing, and app-based scheduling. Over 70% of EV charging events in Australia occur at home through AC infrastructure (Electric Vehicle Council, 2024). Level 2 smart chargers are being mandated in new residential developments in NSW and Victoria.

DC Fast Charging Technology (Level 3)

DC fast charging (50-350 kW) enables rapid highway and commercial fleet charging. Ultra-fast chargers from manufacturers including Tritium DCFC (now under Exicom ownership) are capable of delivering 80% charge in 20-30 minutes. Australia's extreme ambient temperature environment (above 40°C in summer) has driven innovations in thermal management, including isolated satellite dispensers with shaded electronics enclosures that improve uptime and reliability in outback and regional locations.

Vehicle-to-Grid (V2G) and Smart Grid Technology

V2G technology enables bi-directional power flow between EVs and the grid. ACT government-backed V2G pilot projects are demonstrating commercial viability, enabling EVs to act as distributed energy storage. Australia's high rooftop solar penetration of over 30% of households (Clean Energy Council, 2025) creates a structurally advantaged environment for V2G integration and solar-storage-charging combined systems.

Charging Network Software and IoT Platforms

Cloud-based charge management platforms using OCPP 2.0.1, smart metering, RFID authentication, real-time session data, and dynamic pricing APIs are the operational backbone of commercial charging networks. Chargefox and Evie Networks are Australia's leading network software operators, providing national interoperability and seamless roaming for EV drivers across multiple operator networks. IoT-enabled predictive maintenance is reducing station downtime and improving asset utilization rates.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Charging Station Type |

AC Charging |

61.4% |

2025 |

|

Vehicle Type |

Battery Electric Vehicle (BEV) |

57.8% |

2025 |

|

Installation Type |

🔒 |

🔒 |

2025 |

|

Charging Level |

🔒 |

🔒 |

2025 |

|

Connector Type |

🔒 |

🔒 |

2025 |

|

Application |

🔒 |

🔒 |

2025 |

|

Region |

ACT & New South Wales |

34.1% |

2025 |

By Charging Station Type

AC Charging leads at 61.4% (2025). The AC charging segment encompasses all Level 1 and Level 2 charging infrastructure deployed at residential, workplace, retail, and public locations. AC chargers represent the largest installed base in Australia due to their lower cost, ease of installation in existing buildings, and suitability for overnight and extended-dwell charging. The residential charging segment accounts for the majority of AC charging demand, with smart Level 2 chargers becoming the standard specification for new EV owner installations. AC charging's ~18.5% CAGR reflects continued residential and workplace expansion alongside mandated EV-ready building codes in major states.

To access detailed market analysis, Request Sample

DC Charging at 38.6% represents the highway fast-charging and commercial fleet depot segment. DC chargers operate at 50-350 kW, enabling rapid charging for time-sensitive use cases including long-distance travel, taxi and ride-share fleets, and logistics depot turnaround. DC Charging is the faster-growing segment at ~25.2% CAGR through 2034, driven by the national highway DC network buildout under the Driving the Nation Fund, ultra-fast charger deployment at major retail sites, and fleet electrification acceleration in logistics and resources sectors.

By Vehicle Type

Battery Electric Vehicles (BEVs) lead at 57.8% (2025). BEVs are the fastest-growing vehicle category in Australia, with BEV-specific sales reaching 47,145 units in the first half of 2025 alone. BEVs require the most intensive charging infrastructure given their full reliance on electric power, driving disproportionate demand for both Level 2 home chargers and DC public fast chargers. Government incentive programs in NSW, Victoria, and Queensland have historically been targeted at BEVs, further accelerating BEV adoption and its share of charging demand.

Plug-in Hybrid Electric Vehicles (PHEVs) at 26.3% reflect a significant fleet of dual-fuel vehicles that use public and residential AC Level 1 and Level 2 charging for partial electric-mode range. PHEV users generate lower charging revenue per vehicle than BEVs due to shorter charging sessions. Hybrid Electric Vehicles (HEVs) at 15.9% include self-charging hybrids that use regenerative braking and internal combustion engines, with minimal external charging infrastructure demand, primarily using AC Level 1 chargers.

Regional Market Insights

|

Region |

Share (2025) |

Key EV Charging Market Drivers & Characteristics |

|

ACT & New South Wales |

34.1% |

Largest state by EV charging demand. NSW EV Strategy mandates 50% BEV share in new car sales by 2030 and kerbside charging expansion. |

|

Victoria & Tasmania |

26.7% |

Victoria's large manufacturing base and Melbourne's high-density urban environment drive residential and commercial charging demand. |

|

Queensland |

18.9% |

Queensland had 192 public EV charging stations as of 2024, and leads in solar-powered charging deployments. Strong growth in tourism corridor EV infrastructure along coastal and outback routes. Growing fleet electrification in resources and logistics sectors. |

|

Western Australia |

11.2% |

Benefits from state government EV incentives and remote mining sector demand for reliable off-grid charging solutions. Solar-battery-EV charging systems are commercially deployed in remote mining sites and regional tourism destinations. |

|

NT & Southern Australia |

9.1% |

Strategically important for outback highway corridor charging enabling cross-continental EV travel. South Australia's defense manufacturing sector and emerging hydrogen-linked EV infrastructure are long-term growth drivers. |

ACT & New South Wales' combined 34.1% leadership reflects the region's urban EV density, proactive policy environment, and highest concentration of public charging infrastructure. Victoria & Tasmania at 26.7% is underpinned by Melbourne's large EV owner base and Victoria's progressive EV Uptake Strategy. Queensland at 18.9% is the fastest-growing region, driven by solar-EV integration and tourism corridor buildout. Western Australia's 11.2% reflects mining sector demand and state-level EV incentive expansion. NT & South Australia at 9.1% represents the most strategically underserved regions with highest growth potential through highway corridor and defense sector investment.

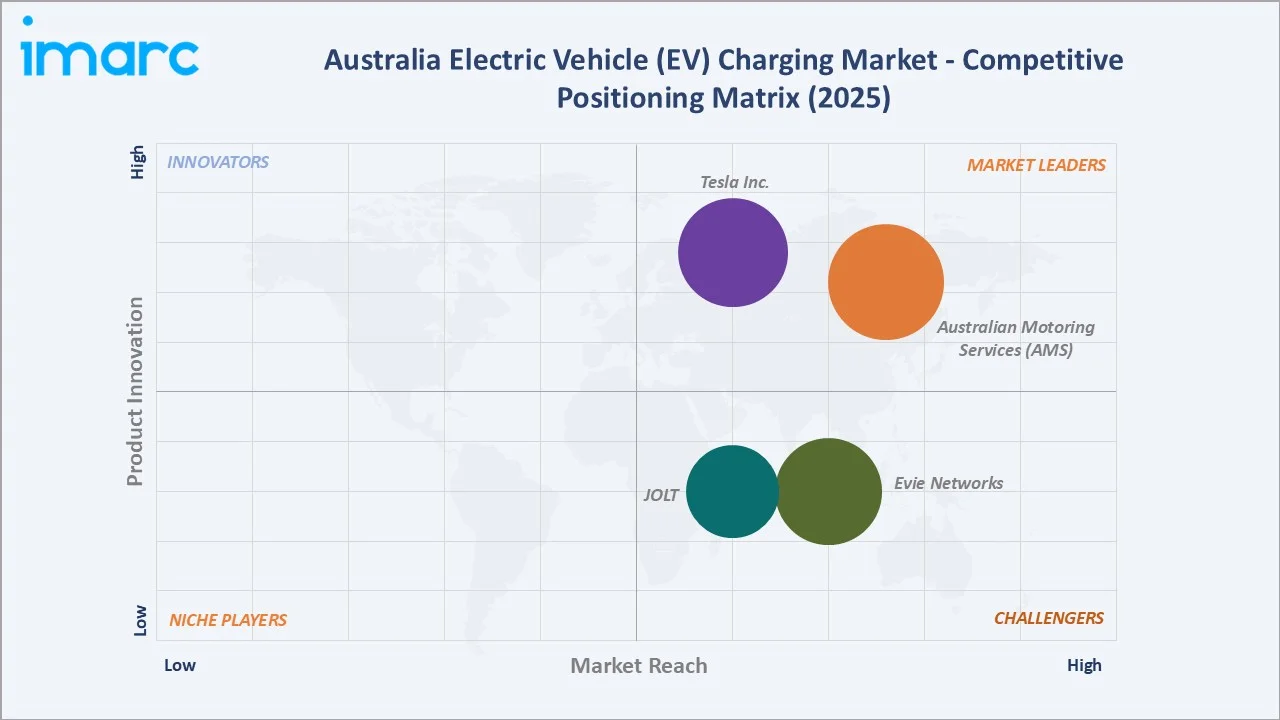

Competitive Landscape

Australia's EV charging market is moderately concentrated. Tesla leads through its proprietary Supercharger network and market-leading BEV installed base. Australian Motoring Services (Chargefox) and Evie Networks are the dominant public network operators with national footprints. The market is characterized by increasing public-private partnerships, with government-backed programs co-funding network expansion across highway, retail, and tourism corridor segments.

|

Company Name |

Brand / Network |

Market Position |

Core Strength |

|

|

Tesla Supercharger/ Tesla Destination Charging |

Leader |

Alleviates "range anxiety" for cross-country driving, utilizes an online, no-haggle pricing structure, proprietary charging network. |

|

|

Chargefox |

Leader |

Australia's largest public EV charging network by locations, with end-to-end app-based management platform. |

|

|

Evie Networks |

Strong Challenger |

Government-backed national highway DC fast-charging network operator focused on highway corridor coverage. |

|

JOLT |

JOLT Charge |

Strong Challenger |

Free 7 kWh/day advertising-funded charging model |

Key Company Profiles

Tesla Inc.

Tesla Inc. operates Australia's most recognized EV charging network through its proprietary Supercharger infrastructure. The company provides end-to-end EV and charging solutions across passenger vehicles and energy storage.

- Key Products: Tesla Supercharger/ Tesla Destination Charging

- Recent Developments: In August 2025, Tesla opened country’s largest electric car charging station in NSW with 20 stalls. The new Superchargers are Tesla's latest V4 design, capable of supplying power at up to 300kW.

- Strategic Focus: Expanding Supercharger density in urban areas and highway corridors, growing non-Tesla EV charging revenue, and integrating Powerwall home energy storage with EV charging for V2G-ready residential installations.

Australian Motoring Services (AMS)

AMS, which operates Chargefox, is Australia's largest public EV charging network operator, providing ultra-rapid, fast DC, and AC Level 2 charging infrastructure across Australia. The company operates an end-to-end digital platform for charging session management, payment, and network monitoring.

- Key Products: Ultra-rapid DC charging stations (up to 350 kW), fast DC chargers (50 kW), AC Level 2 chargers, and the Chargefox app-based charging management platform.

- Recent Developments: In April 2026, Chargefox partnered with bp pulse to integrate its network of approximately 300 EV charging plugs into the Chargefox app. The partnership enables Chargefox app users and RFID card holders to locate, access, and pay for charging sessions across bp pulse's national footprint.

- Strategic Focus: Maintaining national coverage leadership through highway and retail site expansion, enhancing app-based interoperability, and developing fleet charging solutions for corporate clients.

Market Concentration Analysis

Australia's EV charging market displays moderate concentration at the public network operator tier. Tesla holds the largest single-brand charging asset base through its Supercharger network. Australian Motoring Services (Chargefox) and Evie Networks collectively anchor the independent public charging segment.

Fragmentation is higher in the residential and commercial AC charging segments, where multiple hardware vendors, electricians, and aggregators compete. The market is consolidating at the software and network platform tier, with Australian Motoring Services (Chargefox) and Evie Networks expanding interoperability to absorb smaller network operators. New entrants from energy retail (AGL, Origin), telecommunications, and automotive sectors are increasing competitive intensity in the 2026-2028 period.

Investment & Growth Opportunities

Highest Growth Segments

DC fast charging (~25.2% CAGR) is the highest-growth hardware segment, driven by national highway network buildout and commercial fleet depot demand. V2G-integrated charging systems represent the fastest-emerging technology category. Queensland and Western Australia regional markets are growing above the national average through solar-EV integration and mining sector fleet electrification. Commercial AC Level 2 charging for corporate campuses and retail destinations is a high-volume recurring revenue opportunity with minimal technology risk.

Emerging Investment Opportunities

- V2G Technology Platform Development: Australia's structural solar and policy advantage positions V2G technology commercialization as a first-mover opportunity. Companies establishing bi-directional charging hardware and energy management software before the 2027-2029 V2G commercialization phase will capture structurally advantaged recurring revenue from energy arbitrage and grid services above hardware margins.

- Regional Tourism Corridor Charging: Government destination charging grants are co-funding the capital investment required for regional tourism corridor deployments, creating low-risk infrastructure opportunities at iconic Australian routes. These deployments generate both charging revenue and value-added service revenue through integrated hospitality and tourism partnerships.

- Fleet Charging-as-a-Service: CaaS contract models for logistics, retail, mining, and government fleet operators provide predictable multi-year revenue streams. Growing corporate sustainability mandates and fleet electrification timelines in 2026-2030 create a structural demand pipeline.

Future Market Outlook (2026-2034)

Australia's EV charging market is projected to grow from USD 304.4 Million in 2025 to USD 1,692.2 Million by 2034, delivering a 21.00% CAGR over the forecast period. The market's anchor value of USD 789.4 Million in 2030 represents a critical inflection, where EV market penetration will exceed 30% of new car sales (Deloitte Australia, 2024 projection) and national highway DC charging coverage will be substantially complete.

Three structural forces define growth with high confidence through 2034. First, the New Vehicle Efficiency Standard (NVES) effective from 2025 is compelling increased EV model supply, creating a sustained step-change in EV adoption rates. Second, V2G technology commercialization from 2027 onwards will transform EV charging from infrastructure cost to grid asset, creating new revenue models and accelerating private sector investment. Third, state and federal charging mandates for new buildings and transport corridors will create demand certainty for AC and DC infrastructure providers across residential, commercial, and public segments.

BEV dominance at 57.8% will increase further as HEV and PHEV shares decline relative to falling BEV battery costs and expanding BEV model ranges. DC fast charging's share of market revenue will grow from 38.6% in 2025 toward 50% by 2034 as highway and commercial fleet demand scales. ACT & NSW will maintain regional leadership, but Queensland and Western Australia will outgrow the national average through renewable energy-integrated charging deployments and resources sector fleet electrification.

Research Methodology

Primary Research

Primary research comprised structured interviews and consultations with 40+ industry stakeholders including EV charging network operators, equipment manufacturers, fleet managers, government energy policy advisors, and automotive industry specialists. Fieldwork was conducted in 2025 across key Australian states.

Secondary Research

Secondary research encompassed the National Electric Vehicle Strategy Annual Update (DCCEEW, 2024-25), Driving the Nation Fund program documentation (dcceew.gov.au), NSW EV Strategy (nsw.gov.au, 2025), Electric Vehicle Council infrastructure reports, AusNet EV Strategy (2025), Deloitte Australia EV Charging report (January 2024), roadgenius.com EV statistics data, ARENA project database, VFACTS sales data, and company annual reports. Over 60 secondary sources were reviewed.

Forecasting Models

Market revenue forecasts were developed using a bottom-up deployment model integrating EV fleet size projections, charging session frequency by vehicle type, average revenue per charging session, and hardware installation volume multiplied by average unit pricing. Historical period (2020-2025) data was calibrated against EV Council deployment statistics and government infrastructure mapping data. Forecast period (2026-2034) models incorporate policy scenario analysis for NVES impact, V2G adoption probability, and regional deployment acceleration timelines.

Australia Electric Vehicle Charging Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Charging Station Types Covered | AC Charging, DC Charging |

| Vehicle Types Covered | Battery Electric Vehicle (BEV), Plug-in Hybrid Electric Vehicle (PHEV), Hybrid Electric Vehicle (HEV) |

| Installation Types Covered | Portable Charger, Fixed Charger |

| Charging Levels Covered | Level 1, Level 2, Level 3 |

| Connector Types Covered | Combines Charging Station (CCS), CHAdeMO, Type-1 (SAE J1772), Tesla Supercharger, Type-2 (IEC 62196-2), Others |

| Applications Covered | Residential, Commercial |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Tesla Inc., Australian Motoring Services (AMS), Evie Networks, JOLT, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia electric vehicle charging market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia electric vehicle charging market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia electric vehicle charging industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Electric Vehicle (EV) Charging Market Report

Australia's EV charging market reached USD 304.4 Million in 2025, driven by strong government policy support, rapid EV adoption, and expanding public and private charging infrastructure across all states.

Australia's EV charging market exhibits a CAGR of 21.00% during 2026-2034, reaching USD 1,692.2 Million by 2034, one of the highest EV charging CAGRs in the Asia-Pacific region.

AC Charging leads at 61.4% market share in 2025, anchored by widespread residential and workplace Level 2 charging installations across New South Wales, Victoria, and Queensland.

Australia's EV charging market is projected to reach USD 789.4 Million by 2030, driven by national highway DC network completion, V2G pilot commercialization, and BEV share exceeding 30% of new car sales.

Battery Electric Vehicles (BEV) lead at 57.8% in 2025. BEV sales reached 47,145 units in H1 2025 alone, sustaining dominant demand for both residential AC and public DC charging infrastructure.

ACT & New South Wales leads with 34.1% market share in 2025. NSW had 294 public EV charging stations as of 2024 - the most of any Australian state. The ACT leads nationally in EV sales penetration at 25.1%.

Leading companies include Tesla Inc., Australian Motoring Services (AMS), Evie Networks, and JOLT, among others competing across hardware, network operations, and software.

Key programs include the National Electric Vehicle Strategy (DCCEEW), Driving the Nation Fund (AUD 39.3M for highway chargers), DRIVEN grants stream (USD 20M for public chargers), and state-level rebate and fast-charging corridor programs in NSW, Victoria, and Queensland.

DC fast charging grows at ~25% CAGR driven by the NRMA-government highway network (100+ stations at 150 km intervals), commercial fleet depot charging demand, and ultra-fast 350 kW installations at major retail sites.

Australia's EV charging market was valued at USD 117.3 Million in 2020, growing to USD 304.4 Million by 2025, representing a 159% increase over the five-year historical period as EV adoption accelerated.

Top opportunities include V2G technology platforms, regional tourism corridor charging infrastructure, fleet Charging-as-a-Service (CaaS) contracts, solar-battery-EV integrated systems, and ultra-fast DC highway network expansion.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade