Australia Energy Efficient HVAC Systems Market Size, Share, Trends and Forecast by Product, Application, and Region, 2026-2034

Australia Energy Efficient HVAC Systems Market Summary:

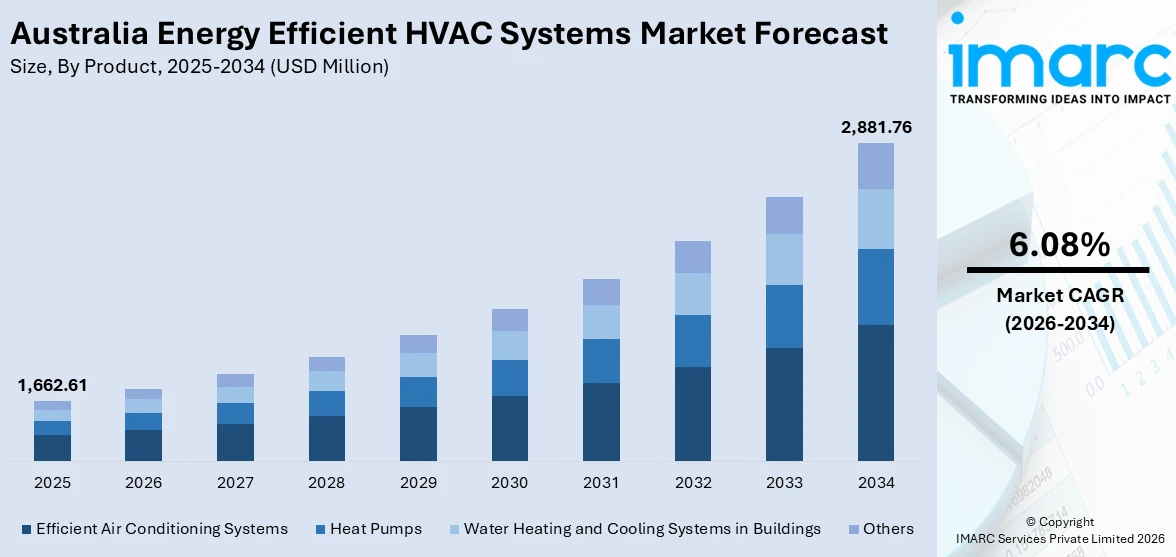

The Australia energy efficient HVAC systems market size was valued at USD 1,662.61 Million in 2025 and is projected to reach USD 2,881.76 Million by 2034, growing at a compound annual growth rate of 6.08% from 2026-2034.

The Australia energy efficient HVAC systems market is gaining strong momentum as escalating electricity tariffs, tightening building energy codes, and growing sustainability commitments drive widespread adoption of high-performance climate control technologies. Increasing preference for inverter-based, smart-connected, and electrified systems across residential, commercial, and institutional buildings is reshaping procurement patterns. The combination of government incentive programs, net-zero building goals, and expanding renewable energy integration continues to reinforce the Australia energy efficient HVAC systems market share.

Key Takeaways and Insights:

- By Product: Efficient air conditioning systems dominate the market with a share of 44.2% in 2025, driven by Australia's warm climate, widespread residential cooling needs, and strong consumer preference for inverter-based, energy-rated split and ducted systems.

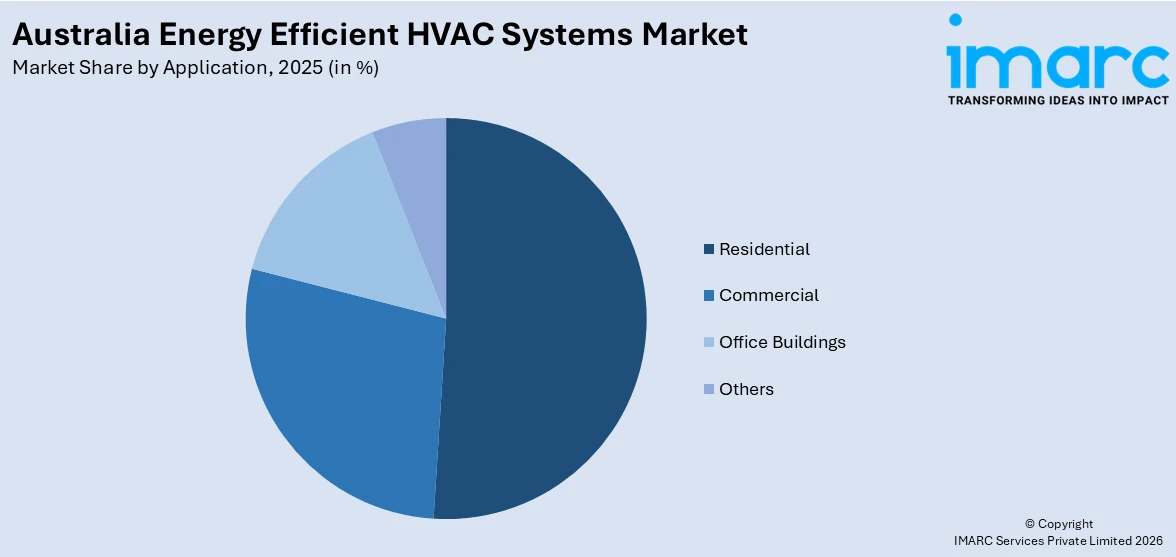

- By Application: Residential leads the market with a share of 50.6% in 2025, reflecting increasing homeowner investment in energy-efficient climate control, government rebate schemes, and the rapid uptake of reverse-cycle air conditioners and heat pumps.

- By Region: Australia Capital Territory & New South Wales represents the largest segment with a market share of 34.1% in 2025, underpinned by Sydney's dense commercial building stock, strong construction activity, high urban population, and early adoption of NABERS-compliant HVAC upgrades.

- Key Players: The Australia energy efficient HVAC systems market is highly competitive, with global manufacturers and specialist contractors competing on inverter technology, smart connectivity, green refrigerant compliance, and NABERS energy rating performance across residential and commercial segments.

To get more information on this market Request Sample

The Australia energy efficient HVAC systems market is advancing rapidly as the built environment sector aligns with national decarbonisation and energy productivity targets. HVAC systems represent a major share of energy consumption in commercial buildings in Australia, making energy efficiency a critical focus within green building strategies and driving increased adoption of high-performance, sustainable HVAC solutions. Sustainability certifications like NABERS, Green Star, and NatHERS are driving the adoption of high-efficiency HVAC systems in new constructions and retrofits. Additionally, evolving state-level regulations promoting energy-efficient and all-electric buildings are further accelerating demand for compliant and sustainable HVAC solutions. The federal government's AUD 10 million investment to expand the NABERS program further signals a sustained policy push toward energy-optimised building performance, elevating demand for premium, high-efficiency HVAC installations.

Australia Energy Efficient HVAC Systems Market Trends:

Rising Integration of Smart, AI-Driven HVAC Technologies

Australian building operators and property developers are increasingly adopting IoT-enabled HVAC systems capable of real-time performance monitoring, automated energy management, and predictive maintenance. AI-powered control platforms enable HVAC networks to optimise zone-level temperature settings, reduce peak load demand, and integrate with building management systems. Publicly funded smart city initiatives in cities such as Adelaide and Brisbane have further catalysed the deployment of AI-driven climate control across mixed-use developments, supporting the Australia energy efficient HVAC systems market growth.

Accelerating Electrification and All-Electric Building Mandates

The transition away from gas-based heating is reshaping HVAC procurement across Australia, as federal and state governments advance electrification policies and building code reforms. In June 2025, Victoria announced that from January 2027 all new homes and most commercial buildings would be required to be all-electric, making reverse-cycle air conditioners the standard heating solution. This regulatory shift, supported by initiatives from the Clean Energy Finance Corporation promoting household energy upgrades, is driving increased replacement demand and encouraging innovation in energy-efficient HVAC technologies, as consumers and businesses transition toward more sustainable and compliant systems.

Growing Synergy Between Rooftop Solar and HVAC Systems

Australia's exceptional solar resource and high rooftop photovoltaic penetration are creating strong commercial logic for solar-coupled HVAC systems. With cumulative rooftop solar installations reaching 25.5 GW by end-2024 and New South Wales alone deploying 952 MW of new rooftop capacity in the first half of 2024 according to the Clean Energy Council, property owners are increasingly pairing solar generation with high-efficiency reverse-cycle systems and heat pumps. This synergy reduces net energy costs, supports grid-responsive HVAC operation, and aligns with sustainability ratings sought by both residential and commercial owners.

Market Outlook 2026-2034:

The Australia energy efficient HVAC systems market is well-positioned for sustained expansion over the forecast period, supported by converging policy, technology, and demographic tailwinds. Stricter building codes, expanding green certification requirements, and deepening renewable energy integration will sustain demand across residential and commercial applications. Urban densification, growing multi-unit residential construction, and strong investment in commercial infrastructure are expected to generate consistent installation volumes. Additionally, ongoing advancements in smart HVAC controls and energy management systems are expected to enhance efficiency and accelerate adoption across both new builds and retrofit projects. The market generated a revenue of USD 1,662.61 Million in 2025 and is projected to reach a revenue of USD 2,881.76 Million by 2034, growing at a compound annual growth rate of 6.08% from 2026-2034.

Australia Energy Efficient HVAC Systems Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product |

Efficient Air Conditioning Systems |

44.2% |

|

Application |

Residential |

50.6% |

|

Region |

Australia Capital Territory & New South Wales |

34.1% |

Product Insights:

- Heat Pumps

- Water Heating and Cooling Systems in Buildings

- Efficient Air Conditioning Systems

- Others

Efficient air conditioning systems dominate the market with a share of 44.2% of the total Australia energy efficient HVAC systems market in 2025.

Efficient air conditioning systems hold a commanding position within the Australia energy efficient HVAC systems market, underpinned by the country's warm to hot climate across much of its territory and the longstanding consumer preference for split-system and ducted air conditioning. Modern inverter-driven units deliver significantly higher seasonal energy efficiency ratios compared to conventional fixed-speed compressors, enabling substantial reductions in electricity consumption while maintaining precise temperature control. Stringent Minimum Energy Performance Standards mandated by the Australian Government and the expansion of the NatHERS energy rating framework have incentivised both manufacturers and households to prioritise high-efficiency models.

Commercial and industrial adoption of high-efficiency air conditioning systems has also gained momentum, as building owners and corporate tenants seek to reduce energy overheads and improve NABERS Energy ratings. Chiller upgrades, variable refrigerant flow systems, and demand-controlled ventilation installations are increasingly common in office retrofits and large mixed-use developments. Facility managers in sectors such as healthcare, retail, and education are accelerating equipment replacement cycles to capture long-term operational savings and meet evolving lease sustainability requirements, driving volume demand for high-performance centrally cooled air conditioning solutions across metropolitan and suburban commercial precincts.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Residential

- Commercial

- Office Buildings

- Others

Residential represent the largest share of 50.6% of the total Australia energy efficient HVAC systems market in 2025.

The residential segment commands the majority share of the Australia energy efficient HVAC systems market, reflecting the widespread adoption of reverse-cycle air conditioners, heat pumps, and high-efficiency ducted systems across Australian households. Rising homeownership rates, expanding multi-unit dwelling construction, and increasing household energy cost awareness are collectively driving investment in premium climate control solutions. Federal and state rebate programs, including the Nationwide House Energy Rating Scheme incentives and the Victoria Energy Upgrades program, have lowered the financial barriers to upgrading older, inefficient systems. In addition, the growing penetration of rooftop solar among Australian households is creating strong demand for solar-compatible HVAC technologies that optimise self-consumption of onsite renewable generation.

The residential application has been further strengthened by tightening building energy codes that now incorporate minimum HVAC efficiency requirements for new homes and significant renovations. Victoria's introduction of 7-star energy efficiency standards in May 2024, which include mandatory performance provisions for fixed heating and cooling appliances, exemplifies the regulatory tailwinds supporting premium residential HVAC adoption. Retrofit activity in the existing housing stock is also gaining pace as electricity price increases make the operational savings from high-efficiency systems increasingly compelling for homeowners, particularly in the more climate-variable southern states.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represent the highest revenue share with 34.1% of the total Australia energy efficient HVAC systems market in 2025.

The Australian Capital Territory and New South Wales account for the highest revenue share in the energy-efficient HVAC systems market due to their strong concentration of commercial infrastructure and high-value urban developments. Cities such as Sydney and Canberra host a dense mix of office buildings, retail complexes, government facilities, and institutional spaces that require advanced climate control systems. These environments prioritize energy efficiency to manage operational costs and meet sustainability targets, driving consistent demand for high-performance HVAC solutions.

Additionally, both regions benefit from stringent building regulations and widespread adoption of green certification frameworks, which actively promote the use of energy-efficient technologies in construction and retrofitting projects. High levels of urbanization, premium real estate development, and strong investment in smart infrastructure further accelerate HVAC system upgrades. The presence of a well-established service ecosystem, skilled workforce, and access to advanced technologies also supports faster implementation and maintenance, reinforcing the regions’ leading position in the overall market.

Market Dynamics:

Growth Drivers:

Why is the Australia Energy Efficient HVAC Systems Market Growing?

Stringent National Building Energy Codes and Green Certification Standards

Australia’s robust building performance standards are a major driver of energy-efficient HVAC adoption across both new construction and retrofit projects. Regulatory frameworks such as the National Construction Code are increasingly guiding developers toward high-performance climate control systems through stricter efficiency and electrification requirements. At the same time, rating programs like NABERS have become influential benchmarks in the commercial property sector, shaping tenant preferences and leasing decisions. These frameworks create strong financial and compliance incentives for building owners to upgrade HVAC systems, reinforcing the importance of energy performance in Australia’s built environment.

Rising Electricity Costs and the Case for Operational Energy Savings

The advantage of high and increasing electricity rates in Australia is rendering the case of operational cost in the context of energy-efficient HVAC systems a strong one for households as well as businesses. With electricity prices currently being high in Australia, the price difference between the traditional fixed-speed systems or resistance-based systems and high-efficiency inverter-powered systems has increased, so that energy-efficient HVAC systems have become cost-effective. Such transition is shortening payback periods and promoting the rapid implementation of premium systems. Simultaneously, government-supported programs targeting household energy upgrades are facilitating the reduction of financial obstacles and increasing the rates of uptake of efficient heating and cooling technology in residential segments further.

Surging Residential and Commercial Construction Activity

Australia's sustained construction boom is generating strong baseline demand for energy-efficient HVAC installations across both residential and commercial segments. The Australian Bureau of Statistics reported that the value of new residential construction reached USD 7.14 billion in January 2024, a year-on-year increase of 19.4%, while non-residential building value rose 12.4% to USD 4.92 billion over the same period. Multi-unit residential developments, which are expanding across urban and near-urban corridors in New South Wales, Victoria, and Queensland, require commercial-style energy-efficient climate control systems that comply with updated NatHERS and Section J standards. Large-scale infrastructure projects, including hospital redevelopments, airport expansions, and transport interchanges, are also mandating integrated, high-efficiency HVAC systems as part of their sustainability and operational specifications, generating sustained contract volumes for specialist HVAC contractors.

Market Restraints:

What Challenges the Australia Energy Efficient HVAC Systems Market is Facing?

High Upfront Capital Investment Requirements

Despite delivering meaningful long-term operational savings, energy-efficient HVAC systems carry significantly higher purchase and installation costs relative to conventional alternatives. For residential consumers, the combined cost of a high-efficiency unit, installation labour, electrical upgrades, and potential ductwork modifications can represent a substantial barrier, particularly in the absence of accessible financing or expanded subsidy coverage. Commercial operators face even greater capital exposure in large-scale retrofit projects involving chiller replacements, variable refrigerant flow installations, and building automation integrations, slowing decision cycles in cost-sensitive occupier and landlord segments.

Shortage of Qualified HVAC Technicians and Specialist Installers

Australia's HVAC industry is facing a growing skills deficit, with insufficient numbers of technicians certified to install, commission, and maintain the latest generation of smart, hybrid, and solar-integrated HVAC systems. This shortage is particularly acute in rural and regional areas where training infrastructure is limited, leaving buildings in remote communities underserved and potentially delaying the uptake of modern, efficient systems. As the market transitions toward more technologically complex products, including AI-enabled controls and low-GWP refrigerant platforms, the demand for specialised expertise is expected to outpace the current labour supply.

Supply Chain Volatility and Component Availability Challenges

The energy-efficient HVAC sector is susceptible to supply chain disruptions affecting key imported components including inverter boards, compressors, refrigerants, and electronic control modules. Pricing volatility, extended lead times, and periodic shortages of specific components can delay project timelines for both residential and commercial installations. These disruptions can erode contractor margins, deter speculative retrofits, and create uncertainty for developers trying to meet building certification deadlines, introducing a degree of market unpredictability that is difficult to mitigate without stronger domestic manufacturing or more diversified supply chains.

Competitive Landscape:

The Australia energy efficient HVAC systems market features a competitive mix of global manufacturers, specialist distributors, and large-scale mechanical contractors. Market participants are differentiating through inverter technology performance, compliance with NABERS and Green Star standards, low global warming potential refrigerant platforms, and smart building integration capabilities. Product innovation is focused on high-SEER-rated air conditioners, advanced heat pump systems, and AI-enabled building management interfaces. Strategic acquisitions, distributor partnerships, and investments in research and development (R&D) centres are intensifying as key players position themselves to capture growth across residential, commercial, and public infrastructure segments amid expanding regulatory requirements.

Recent Developments:

- In April 2025, Next Cycle launched in Australia, introducing Maxa's advanced R290 inverter heat pump range for residential, commercial, and industrial applications. The product line spans capacities from 6kW to 356kW, utilises the ultra-low global warming potential R290 refrigerant, and is designed to address growing demand for electrified, high-efficiency heating and cooling solutions under Australia's tightening building energy codes.

- In January 2025, Sojitz Corporation acquired a 70% stake in Climatech Group Holdings via its Australian subsidiary Ellis Air, consolidating combined annual sales of JPY 45 billion (AUD 450 million) across both companies. The acquisition positions Sojitz as a leading HVAC contractor in Australia and aligns with rising demand for energy-efficient systems under NABERS standards, as well as the anticipated surge in commercial HVAC infrastructure requirements ahead of the Brisbane 2032 Olympics.

Australia Energy Efficient HVAC Systems Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Heat Pumps, Water Heating and Cooling Systems in Buildings, Efficient Air Conditioning Systems, Others |

| Applications Covered | Residential, Commercial, Office Buildings, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Energy Efficient HVAC Systems Market Report

The Australia energy efficient HVAC systems market size was valued at USD 1,662.61 Million in 2025.

The Australia energy efficient HVAC systems market is expected to grow at a compound annual growth rate of 6.08% from 2026-2034 to reach USD 2,881.76 Million by 2034.

Efficient air conditioning systems held the largest revenue share of 44.2% in 2025, driven by Australia's hot climate, widespread residential and commercial cooling demand, and strong uptake of high-efficiency inverter-based split and ducted air conditioning systems.

Key factors driving the Australia energy efficient HVAC systems market include stringent national building energy codes, tightening NABERS and Green Star certification standards, rising electricity tariffs, government rebate programs, accelerating electrification mandates, and surging residential and commercial construction activity.

Major challenges include high upfront capital investment requirements for residential and commercial upgrades, a growing shortage of certified technicians able to install and maintain advanced smart and hybrid HVAC systems, and supply chain volatility affecting the availability and pricing of key imported components, collectively slowing the pace of adoption in cost-sensitive and regionally remote segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)