Australia Energy Storage Market Size, Share, Trends and Forecast by Type, End User, and Region, 2026-2034

Australia Energy Storage Market Size, Share, Trends & Forecast (2026-2034)

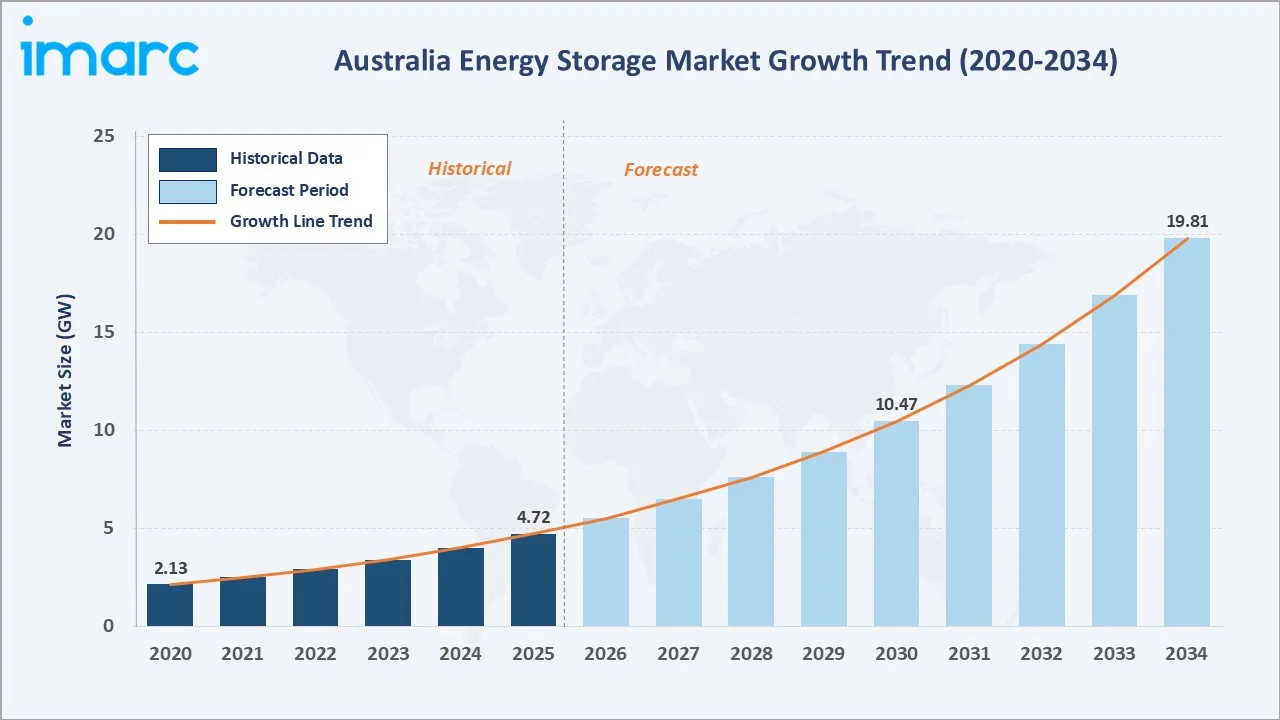

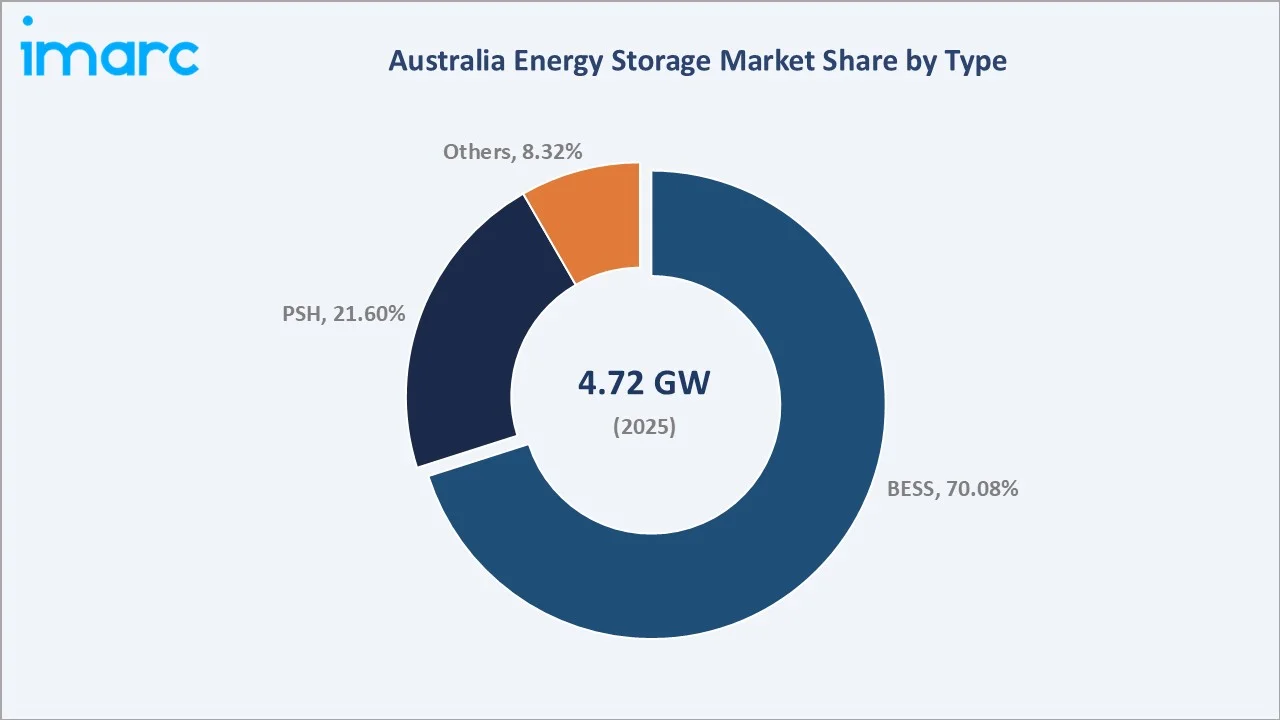

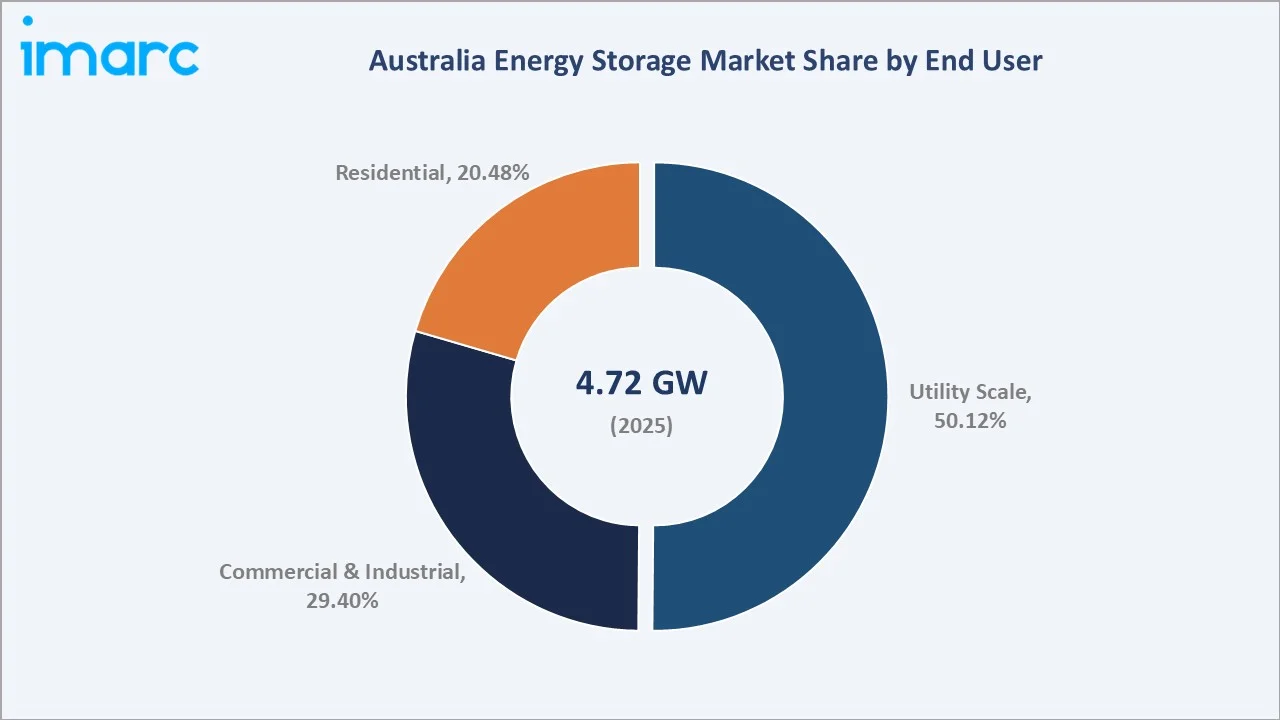

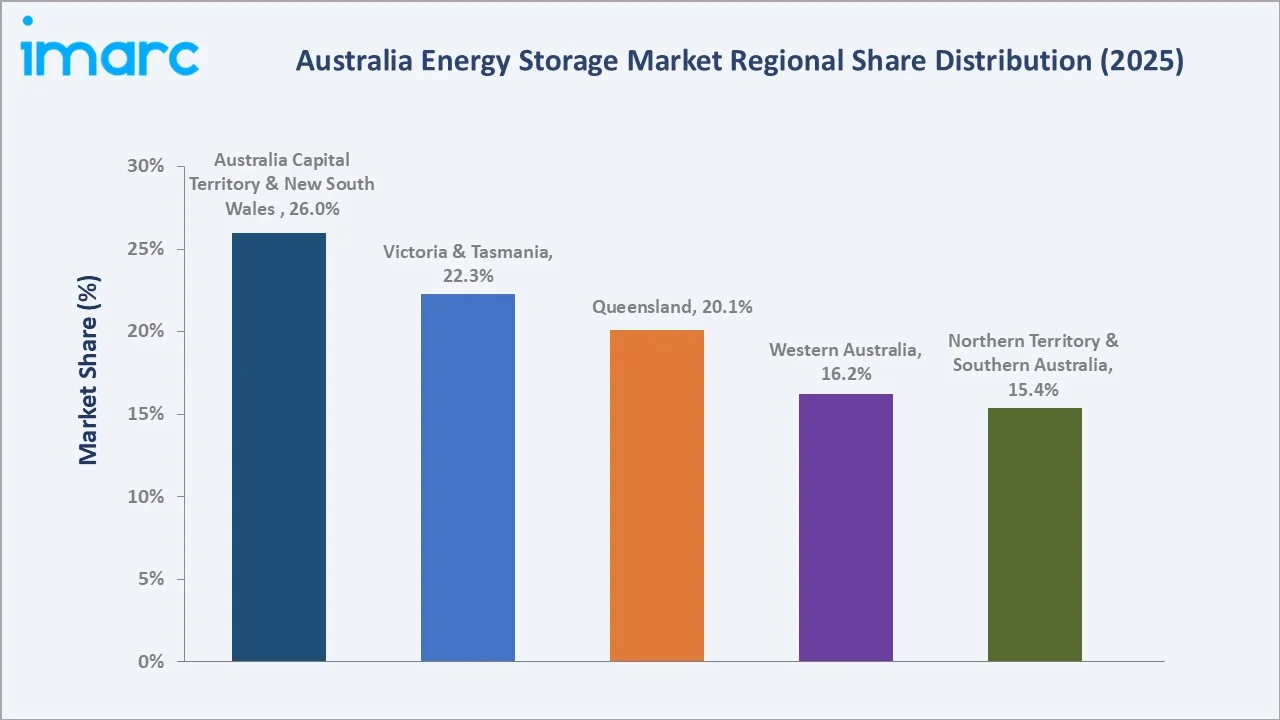

The Australia energy storage market reached 4.72 GW in 2025 and is projected to reach 19.81 GW by 2034, growing at a CAGR of 17.28% during 2026-2034. The market is driven by the growing demand for renewable energy integration, government incentives for clean energy solutions, and the need for grid stability and reliability, particularly with the transition towards solar and wind power. The Australian Government’s expansion of the national target of the Capacity Investment Scheme (CIS) from 82% renewable electricity by 2030 to 100% by 2030 is driving the market by increasing the demand for efficient storage solutions to support the integration of renewable energy into the grid. Battery Energy Storage Systems (BESS) dominate at 70.08% type share. Utility scale leads the end-user at 50.12%. Australia Capital Territory & New South Wales command 26.0% of the market capacity.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

4.72 GW |

|

Forecast Market Size (2034) |

19.81 GW |

|

CAGR (2026-2034) |

17.28% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Storage Type |

BESS (70.08%, 2025) |

|

Largest End User |

Utility Scale (50.12%, 2025) |

|

Leading Region |

ACT & New South Wales (26.0%, 2025) |

The market expanded from 2.13 GW in 2020 to 4.72 GW in 2025, anchored at 10.47 GW in 2030, and forecast to reach 19.81 GW by 2034. South Australia's successful integration of variable renewable energy, supported by BESS that high-renewable grids are technically and economically viable with adequate storage.

To get more information on this market, Request Sample

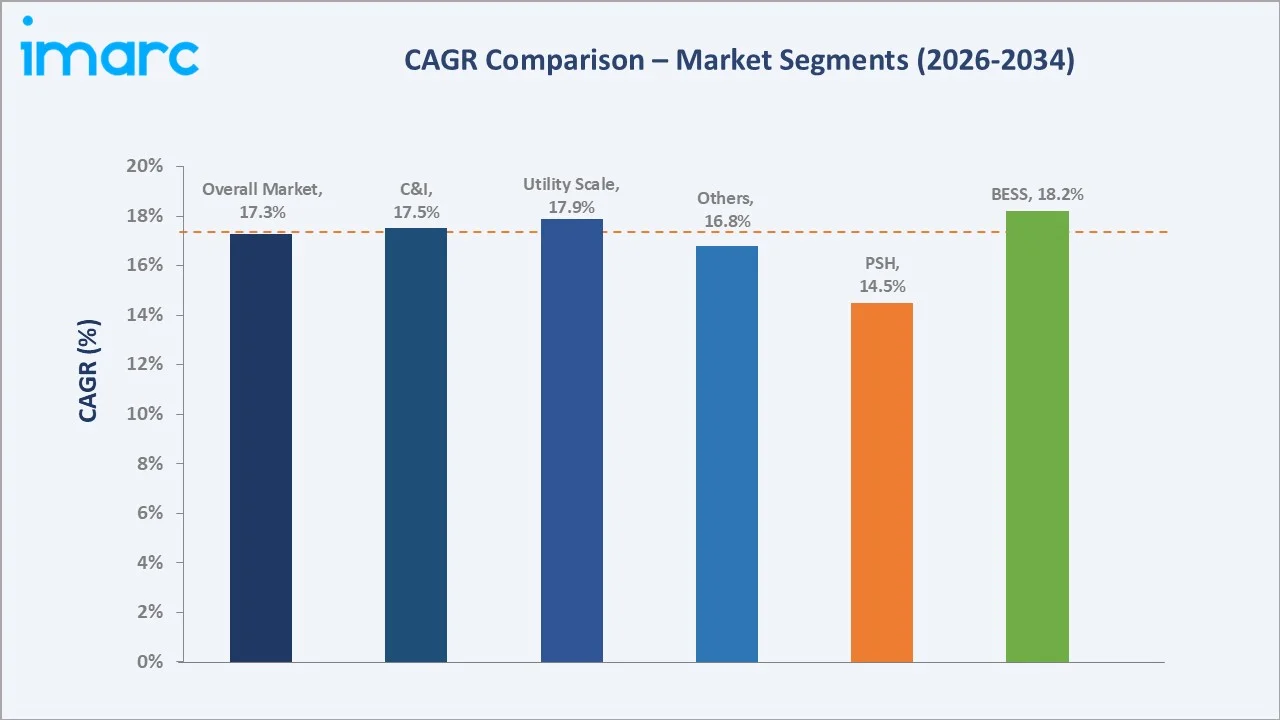

BESS grows fastest at ~18.2% CAGR (2026-2034), driven by declining lithium iron phosphate (LFP) cell costs, short-notice BESS dispatch advantage versus slower-responding thermal units, and Australia's unique combination of world-class solar irradiance, making solar and BESS increasingly the lowest-cost new electricity source. Utility scale end-user grows at ~17.9% CAGR, outpacing residential and commercial and industrial (C&I), as grid-scale BESS projects attract institutional capital.

Executive Summary

The Australia energy storage market reached 4.72 GW in 2025, making Australia one of the world's fastest-growing energy storage markets in absolute capacity addition terms. The 2024 Integrated System Plan (ISP) forecasts the need for 36 GW/522 GWh of storage capacity in 2034-35, rising to 56 GW/660 GWh of storage capacity in 2049-50. The market is projected to reach 19.81 GW by 2034 at 17.28% CAGR.

BESS dominates at 70.08% (2025), driven by faster deployment timelines, declining LFP battery costs and emergency reserve market mechanisms that provide BESS operators with attractive revenue streams independent of energy arbitrage. Utility scale at 50.12% leads end-user as 300-850 MW projects deploy to replace retiring coal generation capacity. Australia Capital Territory & New South Wales at 26.0% leads regionally, anchored by the transmission investment roadmap.

Key Market Insights

|

Insight |

Data |

|

Dominant Storage Type |

BESS - 70.08% share (2025) |

|

Largest End User |

Utility Scale - 50.12% share (2025) |

|

Dominant Region |

Australia Capital Territory & New South Wales - 26.0% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- BESS at 70.08% reflecting deployment speed, cost, and market design advantages: Battery energy storage systems deploy in 12-18 months versus 8-10 years for PSH, aligning with Australia's urgent need to replace retiring coal capacity.

- Utility scale at 50.12% driven by coal retirement and renewable energy zone (REZ) co-location requirements: The ISP’s Optimal Development Path through the NEM’s transition to a net-zero future has an annualised capital cost of $122 billion to 2050, with utility storage as the primary grid stability mechanism replacing dispatchable coal.

- Australia Capital Territory & New South Wales at 26.0% anchored by grid-scale BESS landmark projects and transmission investment: NSW coordinates $32 billion of investment in REZs to deliver at least 12 GW of renewable energy by 2030, with storage integration at every major new transmission node.

Australia Energy Storage Market Overview

The Australia energy storage market encompasses all grid-connected and behind-the-meter energy storage installations, including Battery Energy Storage Systems (BESS), Pumped-storage Hydroelectricity (PSH), flow batteries, compressed air energy storage, and emerging long-duration storage technologies.

The ecosystem integrates battery cell manufacturers, BESS system integrators, PSH developers, federal funding bodies, market operators, state transmission networks, and end-user segments spanning utility retailers, industrial corporations, and residential solar storage households. Macroeconomic factors include strong government support through renewable energy targets and incentives, rising energy costs, the push for energy security, and increasing investments in clean energy technologies as part of the country's transition to a low-carbon economy.

Market Dynamics

To evaluate market opportunities, Request Sample

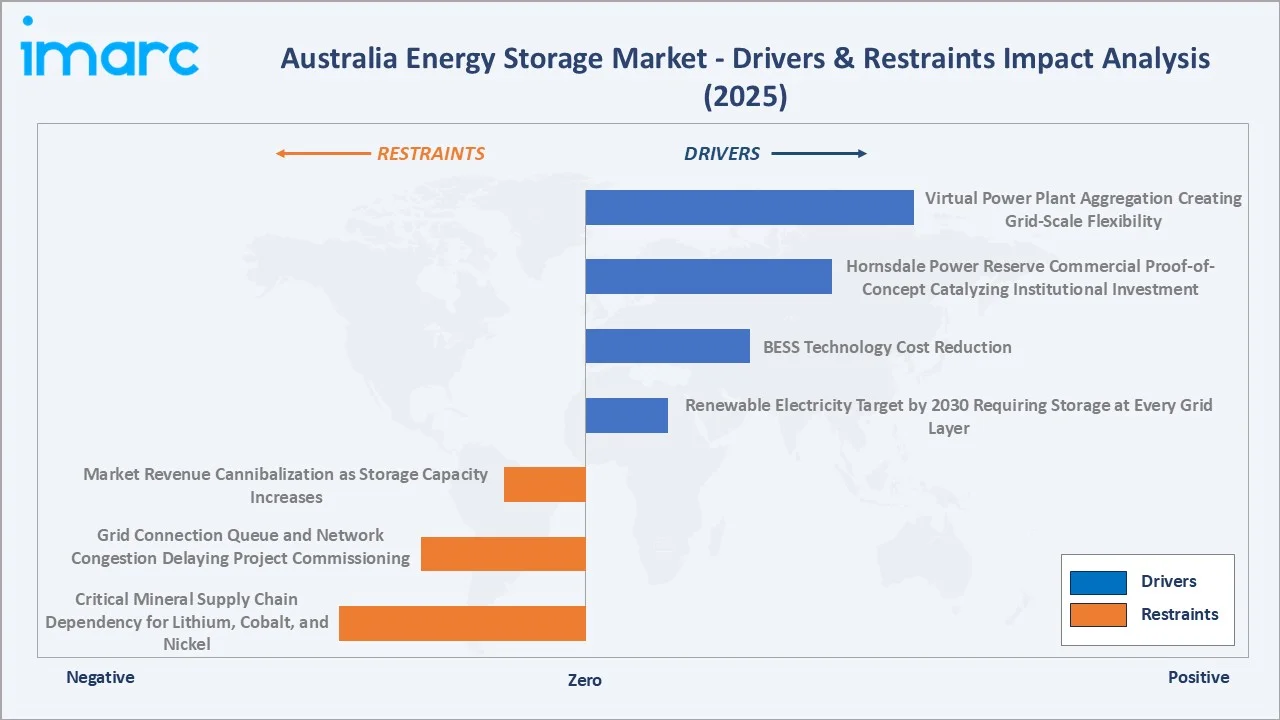

Market Drivers

- Renewable Electricity Target by 2030 Requiring Storage at Every Grid Layer: Australia's expansion of the national target of the Capacity Investment Scheme (CIS) from 82% renewable electricity by 2030 to 100% by 2030 and accelerate the staged closure of coal plants before 31 December 2030, in the National Electricity Market (NEM) and the South West Interconnected System (SWIS) is continuously accelerating the market growth.

- BESS Technology Cost Reduction: LFP battery cell price reduction, making utility BESS economically competitive with peaking gas turbines at equivalent service duration. This cost trajectory makes new solar+2-hour BESS the lowest-cost new electricity source across all Australian electricity zones, displacing new gas generation as the marginal investment benchmark.

- Hornsdale Power Reserve Commercial Proof-of-Concept Catalyzing Institutional Investment: The Hornsdale Power Reserve, the world’s first large-scale battery, plays a crucial role in providing grid support services. The initial 100 MW/129 MWh capacity was completed in November 2017. In its first two years of operation, it demonstrated the advantages of grid-scale batteries in the National Electricity Market, saving South Australian consumers more than $150 million.

Market Restraints

- Critical Mineral Supply Chain Dependency for Lithium, Cobalt, and Nickel: Australia's energy storage market faces a structural dependency on critical mineral supply chains where Australian mining provides raw materials, but battery cell manufacturing value-add occurs predominantly in other regions.

- Grid Connection Queue and Network Congestion Delaying Project Commissioning: Grid connection queues and network congestion are delaying project commissioning, increasing wait times for connecting new energy storage systems to the grid, and creating bottlenecks that slow down the transition to renewable energy and energy storage infrastructure.

Market Opportunities

- Long-Duration Energy Storage Commercialization Creating New Storage Market: Beyond current BESS (2-4 hour) and PSH (6-24 hour), emerging long-duration energy storage (LDES) technologies are approaching commercial deployment at costs compatible with Australia's grid requirements for seasonal and weekly energy shifting.

- Virtual Power Plant Aggregation Creating Grid-Scale Flexibility from Residential Assets: Australia's rooftop solar households represent 3-5 GW of distributed storage potential when paired with home battery systems. If Australia's solar homes install battery storage and join VPPs, the aggregate capacity would equal multiple utility-scale BESS projects at zero grid infrastructure cost.

Market Challenges

- Market Revenue Cannibalization as Storage Capacity Increases: As more BESS capacity enters the markets, the very grid services that make BESS economically attractive become less valuable as market saturation compresses revenue.

- Fire Safety and Community Acceptance Challenges for Large BESS Projects: Large-scale lithium-ion BESS installations face increasing community and regulatory scrutiny following international incidents. Australian states have implemented enhanced BESS fire safety standards that increase project costs, creating additional project development costs and approval timeline extensions.

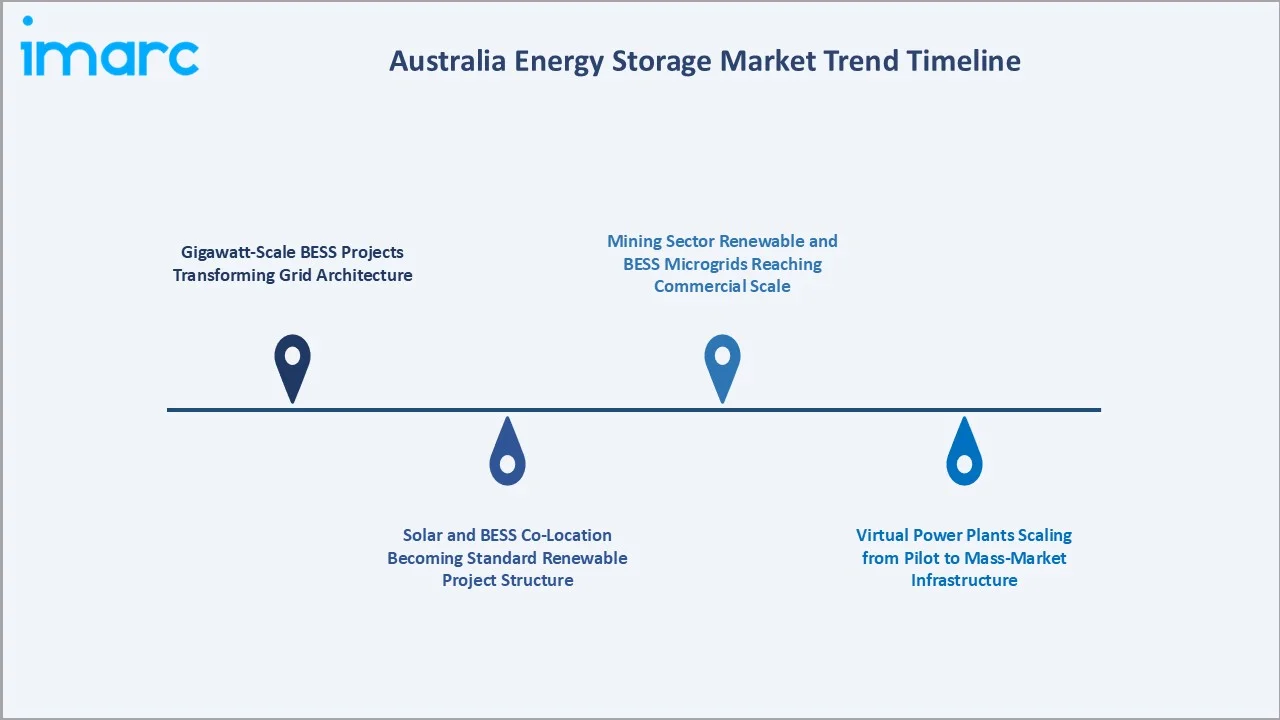

Emerging Market Trends

1. Gigawatt-Scale BESS Projects Transforming Grid Architecture

Gigawatt-scale Battery Energy Storage System (BESS) projects are transforming grid architecture in Australia by providing large-scale storage solutions that enhance grid stability, enable greater integration of renewable energy, and reduce reliance on traditional fossil fuel-based power generation, positioning BESS as a key player in modernizing the national energy infrastructure.

2. Solar and BESS Co-Location Becoming Standard Renewable Project Structure

The co-location of Solar and Battery Energy Storage Systems (BESS) is becoming a standard renewable project structure in Australia as it enhances energy reliability, optimizes the use of renewable power, and allows for better energy management by storing excess solar energy for use during peak demand periods, thus improving grid stability and efficiency.

3. Virtual Power Plants Scaling from Pilot to Mass-Market Infrastructure

Virtual Power Plants (VPPs) are scaling from pilot projects to mass-market infrastructure in Australia by aggregating distributed energy resources like residential solar panels and battery storage, enabling more efficient energy dispatch, enhancing grid flexibility, and supporting the transition to a renewable energy future, while reducing reliance on traditional power plants.

4. Mining Sector Renewable and BESS Microgrids Reaching Commercial Scale

Mining sector renewable energy and Battery Energy Storage System (BESS) microgrids are reaching commercial scale in Australia as mining companies increasingly adopt off-grid, self-sufficient energy solutions to reduce costs, lower carbon emissions, and ensure reliable power supply in remote locations, driving the growth of sustainable energy practices in the industry.

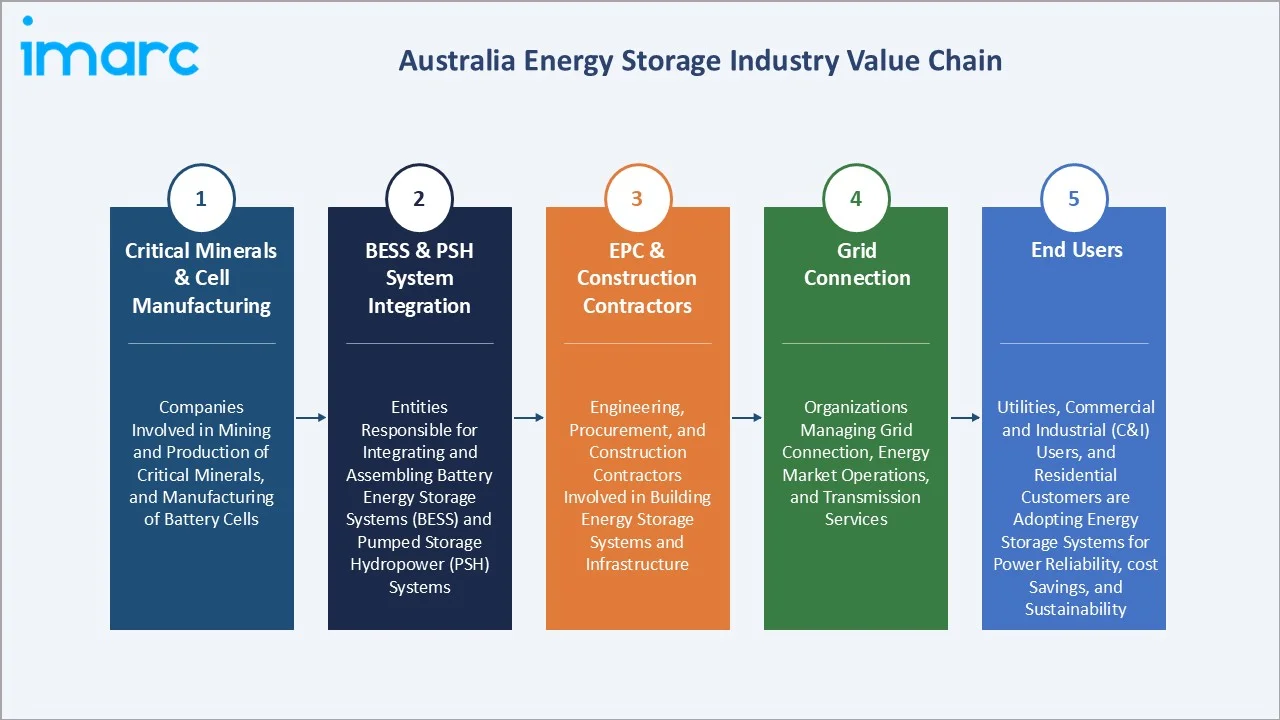

Industry Value Chain Analysis

The Australia energy storage value chain integrates critical mineral mining, international battery cell manufacturing, system integration and EPC construction, federal and state government funding, grid registration and market participation, and end-user operation spanning utility, commercial and industrial, and residential applications. Storage project developers capture 15-25% project development margins; BESS integrators earn 8-15% on supply contracts; grid operators earn recurring dispatch revenues.

|

Stage |

Key Participants |

|

Critical Minerals & Cell Manufacturing |

Companies involved in mining and production of critical minerals, and manufacturing of battery cells |

|

BESS & PSH System Integration |

Entities responsible for integrating and assembling Battery Energy Storage Systems (BESS) and Pumped Storage Hydropower (PSH) systems |

|

EPC & Construction Contractors |

Engineering, procurement, and construction contractors involved in building energy storage systems and infrastructure |

|

Grid Connection |

Organizations managing grid connection, energy market operations, and transmission services |

|

End Users |

Utilities, commercial and industrial (C&I) users, and residential customers are adopting energy storage systems for power reliability, cost savings, and sustainability |

The federal funding ecosystem is the value chain's most strategically critical tier for new entrant project developers, as government co-funding de-risks project economics sufficiently to attract institutional infrastructure capital.

Technology Landscape in the Australia Energy Storage Industry

Lithium Iron Phosphate (LFP) Battery Dominance and Cost Trajectory

The dominance of Lithium Iron Phosphate (LFP) batteries, driven by their cost efficiency, long lifespan, and enhanced safety, is shaping the technology landscape by making large-scale storage solutions more affordable and accessible. LFP batteries’ decreasing cost trajectory supports the widespread adoption of energy storage systems, enabling faster integration of renewable energy, increasing grid stability, and driving the growth of both residential and commercial storage projects.

Pumped-Storage Hydroelectricity Engineering and Snowy 2.0

Snowy 2.0’s 2,200 megawatt (MW) capacity is capable of supplying enough energy to power 3 million homes for a week, equivalent to approximately 23 million home batteries. According to the Australian Energy Market Operator, the National Electricity Market (NEM) will need around 649 gigawatt hours (GWh) of dispatchable energy storage to achieve net zero by 2050. Snowy 2.0 will contribute over half of this, offering the grid an impressive 350 GWh of energy storage.

BESS Power Electronics and Grid Forming Inverter Technology

BESS power electronics and grid-forming inverter technology are enhancing the stability, reliability, and flexibility of energy storage systems. These advanced technologies allow BESS to seamlessly integrate with the grid, enabling them to provide critical services like voltage control, frequency regulation, and backup power. Grid-forming inverters enable BESS to operate autonomously and stabilize the grid during periods of low or no generation from traditional power plants, playing a key role in the transition to a more resilient and renewable-powered grid.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Type | Battery Energy Storage System (BESS) | 70.08% | 2025 |

| End User | Utility Scale | 50.12% | 2025 |

| Region | Australia Capital Territory & New South Wales | 26.0% | 2025 |

By Type

Battery Energy Storage System (BESS) leads at 70.08% capacity share (2025). This encompasses utility-scale BESS, commercial BESS, and residential BESS. BESS grows at ~18.2% CAGR (2026-2034) as LFP cost reductions and AEMO market rule reforms improve BESS revenue stack predictability.

To access detailed market analysis, Request Sample

Pumped-storage Hydroelectricity (PSH) at 21.6% represents existing hydro pumped-storage capacity. PSH grows at ~14.5% CAGR as Snowy 2.0 phases come online. Others at 8.32% encompasses thermal storage, pilot projects, vanadium flow batteries, and flywheels, growing as emerging technologies reach commercial deployment thresholds.

By End User

Utility scale leads at 50.12%. The utility-scale ability to provide large-scale, cost-effective energy storage solutions that support grid stability, integrate renewable energy, and enhance the reliability of the National Electricity Market (NEM). Utility-scale projects, such as Snowy 2.0, can store significant amounts of energy, enabling utilities to manage fluctuations in renewable generation and meet peak demand efficiently. This large-scale capability makes the utility sector the primary driver of energy storage adoption and growth in Australia.

Commercial and industrial at 29.4% is driven by mine-site microgrids, large commercial solar and storage, industrial demand response, and commercial and industrial behind-the-meter peak shaving. C&I grows at ~17.5% CAGR as grid demand charges and rising energy prices improve C&I BESS business cases. Residential at 20.48% benefits from high Australian residential solar penetration, creating a natural paired-storage market.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers & Characteristics |

|

Australia Capital Territory & New South Wales |

26.0% |

Major projects targeting large-scale energy storage and grid integration, with strong government support and infrastructure investment. |

|

Victoria & Tasmania |

22.3% |

Ongoing large-scale energy storage projects, including pumped hydro storage, support regional grid stability and renewables integration. |

|

Queensland |

20.1% |

Growing investment in large-scale energy storage systems, pumped hydro, and decentralized energy solutions to support resource extraction areas. |

|

Western Australia |

16.2% |

Focus on off-grid and microgrid energy storage, community-based storage systems, and integrating renewable energy solutions in remote areas. |

|

Northern Territory & South Australia |

15.4% |

Strong commitment to energy storage with grid-connected and regional projects supporting renewable energy integration and local grid stability. |

Australia Capital Territory & New South Wales’s 26.0% dominance reflects the state's combination of the NEM's largest electricity load, most ambitious storage procurement pipeline, and strategic grid investment. NSW coordinates $32 billion of investment in REZs to deliver at least 12 GW of renewable energy by 2030.

Victoria and Tasmania's 22.3% are anchored by the Victorian Big Battery. Queensland's 20.1% features a BESS procurement pipeline and the combination of solar, wind, and PSH. Western Australia's 16.2% grid creates unique storage dynamics with remote community BESS deployments.

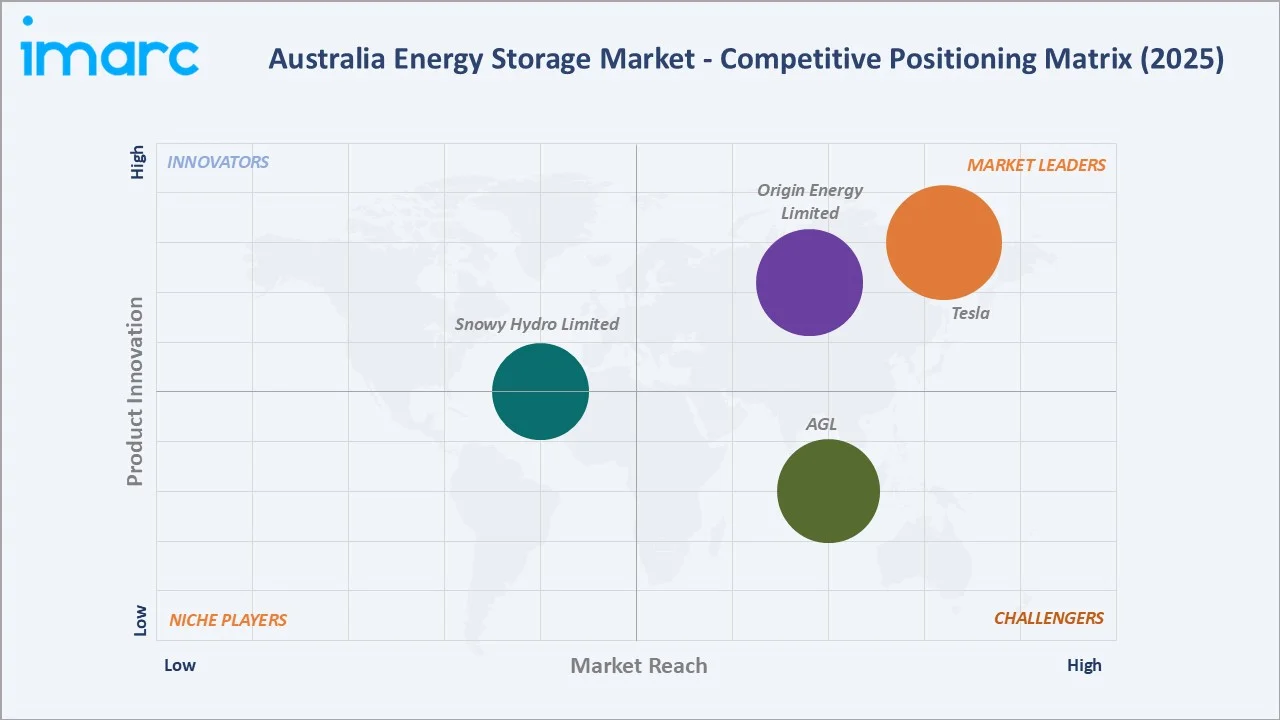

Competitive Landscape

The Australia energy storage market exhibits moderate concentration at the utility BESS supply level and high fragmentation at the project development level, where 50+ entities hold BESS project development rights. Battery supply concentration reflects global manufacturing dominance rather than Australian market-specific dynamics, while project development fragmentation reflects Australia's favorable regulatory framework, attracting diverse institutional and strategic investors.

|

Company Name |

Products |

Market Position |

Core Strength |

|

Tesla |

Megapack, Powerwall |

Market Leader |

Powerwall is a compact home battery that stores energy generated by solar or from the grid. Megapack is a powerful, integrated battery system that provides clean, reliable, cost-effective energy storage to help stabilize the grid and prevent outages. |

|

AGL |

Broken Hill Battery, Tomago Battery, Liddell Battery |

Strong Challenger |

AGL operates the largest private electricity generation portfolio in Australia. AGL opened a 250 MW / 250 MWh grid-scale battery at Torrens Island in Adelaide in August 2023. |

|

Snowy Hydro Limited |

Snowy 2.0 |

Established Player |

Snowy 2.0’s 2,200 megawatt (MW) capacity will deliver enough energy to power 3 million homes for a week, equivalent to about 23 million home batteries. |

|

Origin Energy Limited |

Eraring Power Station battery, Mortlake Power Station battery, Darling Downs Power Station battery, Templers Creek battery |

Leader |

Origin Energy's priority renewable energy project is the Yanco Delta wind farm in NSW, and also building large-scale battery energy storage systems at Eraring and Mortlake power stations. |

The competitive landscape is bifurcating between vertically integrated energy retailers pursuing BESS as a coal-replacement strategy and pure-play BESS developers that own and operate storage assets, selling services into NEM spot and ancillary service markets.

Key Company Profiles

Tesla

Tesla is the defining company of Australia's energy storage market with Powerwall and Megapack energy products.

- Product Portfolio: Megapack and Powerwall

- Recent Developments: In September 2024, Tesla officially launched the first deliveries of Powerwall 3 in Australia.

- Strategic Focus: Megapack as the standard utility BESS product for Australia's giga-scale deployment phase.

AGL

AGL is one of Australia's largest energy companies and a major energy storage developer. The company operates the largest private electricity generation portfolio in Australia and is building on its history as one of Australia’s leading private investors in the construction of renewable energy projects.

- Product Portfolio: Broken Hill Battery, Tomago Battery, Liddell Battery.

- Recent Developments: In July 2025, Fluence Energy, Inc. was selected by AGL to deliver the 500 MW / 2000 MWh Tomago Battery Energy Storage System (BESS) in Newcastle, New South Wales, Australia. Moreover, AGL opened a 250 MW / 250 MWh grid-scale battery at Torrens Island in Adelaide in August 2023.

- Strategic Focus: BESS conversion leveraging existing grid connections and community acceptance.

Market Concentration Analysis

Australia's energy storage market exhibits a bifurcated concentration structure: high concentration in BESS technology supply, contrasted with moderate fragmentation in project development, and high concentration in PSH development. The technology supply concentration reflects global battery manufacturing dynamics rather than Australian market-specific factors.

Energy retailer BESS concentration is moderate, with AGL and Snowy Hydro (retail) together representing approximately 60% of Australia's utility electricity generation fleet, providing natural advantages for BESS integration into existing retailer dispatch portfolios. Independent BESS developers represent the competitive counterweight, bringing pure-play project development expertise and international institutional capital.

Investment & Growth Opportunities

Fastest Growing Segments

BESS utility scale (~18.2% CAGR), residential BESS via VPP aggregation (~17.5% CAGR), C&I mine-site renewable and storage (~17.5% CAGR), long-duration storage pilot-to-commercial (~25%+ CAGR from small base), and co-located solar and BESS (~20%+ CAGR) represent Australia's highest-growth storage investment vectors.

Emerging Market Opportunities

Australia's solar households represent the world's largest untapped residential storage market. If state government rebate programs are extended and replicated in NSW, the residential BESS market could add 2-3 GW of distributed storage capacity by 2030 from this single demographic segment.

Investment Themes

- Critical minerals to battery manufacturing value chain development: Australia exports a global lithium supply but captures less than 5% of battery manufacturing value. Investment in Australian cathode active material (CAM) processing, cell manufacturing, and battery pack assembly creates diversified exposure to Australia's energy storage supply chain beyond project development.

- Virtual Power Plant platform development: Australia's solar homes and growing home battery penetration create a distributed storage aggregation opportunity. VPP platforms that aggregate residential storage into NEM-registered dispatchable resources at negligible marginal cost versus utility BESS represent the highest-margin energy storage business model in the Australian market.

Future Market Outlook (2026-2034)

The Australia energy storage market is projected to grow from 4.72 GW in 2025 to 19.81 GW by 2034, delivering a 17.28% CAGR over the forecast period. The market's anchor value of 10.47 GW in 2030 represents a pivotal transition point. The 2030 milestone transforms Australia from a market proving BESS viability to one demonstrating full renewable electricity reliability with diversified storage portfolios.

Three structural forces define the Australia energy storage market's trajectory with exceptional certainty through 2034: coal retirement creating dispatchable capacity that the NEM must replace with storage-backed renewable energy, an irreversible, policy-mandated replacement wave that provides guaranteed demand for energy storage independent of technology cost curves or policy discretion; BESS technology cost reductions, making new solar and 4-hour BESS the lowest-cost electricity source across all Australian states and eliminating the need for policy support for most utility BESS projects; and Snowy 2.0's completion providing the long-duration storage backbone that allows Australia's NEM to operate reliably on variable renewable energy across all weather scenarios.

Research Methodology

Primary Research

Primary research comprised structured interviews with 70+ industry stakeholders (2025), including AEMO grid planning and market operations staff; CEFC and ARENA project managers overseeing committed storage funding; utility BESS project developers; Tesla Australia commercial team; state transmission network service providers; BHP and Rio Tinto energy procurement executives managing mine-site BESS; and residential battery installer aggregators for SA, VIC, and QLD VPP programs.

Secondary Research

Secondary research encompassed AEMO Integrated System Plan 2024, AEMO Generation Information, ARENA and CEFC project databases and annual reports 2024, Clean Energy Council Australian Battery Storage Report 2024, Climate Change Authority Renewable Energy Target analysis, state government energy plans, BNEF Australia Energy Storage Outlook 2025, and company investor presentations and project announcement data. Over 130 secondary sources were reviewed.

Forecasting Models

Market capacity forecasts were developed using bottom-up project pipeline modeling incorporating AEMO's committed and anticipated generation information, state government storage procurement commitments, Capacity Investment Scheme contracted capacity, Snowy 2.0 commissioning milestone projections, residential solar and storage adoption rate models calibrated against state rebate program take-up data, and C&I mine-site storage project announced pipelines. Key inputs include AEMO ISP 2024 storage capacity requirements by year, CEFC and ARENA contracted project commissioning schedules, LFP battery cost trajectories from BNEF, and coal retirement timelines from AEMO's 2024 Electricity Statement of Opportunities.

Australia Energy Storage Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | GW |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Battery Energy Storage System (BESS), Pumped-storage Hydroelectricity (PSH), Others |

| End Users Covered | Residential, Commercial and Industrial, Utility Scale |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Tesla, AGL, Snowy Hydro Limited, Origin Energy Limited, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Energy Storage Market Report

The Australia energy storage market reached 4.72 GW in 2025, driven by BESS dominance at 70.08%, utility solar and storage REZ co-location requirements, and residential solar homes representing the highest per-capita solar and storage rate.

The market grows at 17.28% CAGR during 2026-2034, reaching 19.81 GW by 2034, driven by Australia's renewable electricity target, coal retirements requiring storage replacement, BESS cost reductions, and Snowy 2.0's PSH commissioning.

BESS leads at 70.08% due to 12-18 month deployment speed versus 8-10 years for PSH, AEMO's multi-revenue market structure enabling BESS to optimize across energy and emergency reserve simultaneously, and LFP cost reductions.

Utility scale leads at 50.12%, driven by coal retirement replacement requirements and Capacity Investment Scheme contracted revenues providing project finance certainty.

ACT and New South Wales leads at 26.0%, anchored by the Waratah Super Battery (AUD 32 Billion transmission investment roadmap.

Leading companies include Tesla, AGL, Snowy Hydro Limited, and Origin Energy Limited, among others.

The market is projected to reach approximately 10.47 GW by 2030, with Snowy 2.0's first phases, giga-scale BESS projects operational, residential VPP aggregation, and renewable electricity achieved under AEMO market conditions.

Snowy 2.0 is the pumped-storage hydro expansion of Australia's Snowy Mountains scheme, the world's largest new PSH project under construction. Snowy 2.0’s 2,200 megawatt (MW) capacity will deliver enough energy to power 3 million homes for a week, equivalent to about 23 million home batteries.

BESS deploys in 12-18 months versus 8-10 years for PSH; LFP cost reductions are making 4-hour BESS economically competitive for all peak-demand applications where PSH traditionally competed; BESS can be co-located with solar at REZ sites more flexibly than PSH, requiring specific topographic conditions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)