Australia Ferrous Scrap Recycling Market Size, Share, Trends and Forecast by Type, Application, End User, and Region, 2026-2034

Australia Ferrous Scrap Recycling Market Overview:

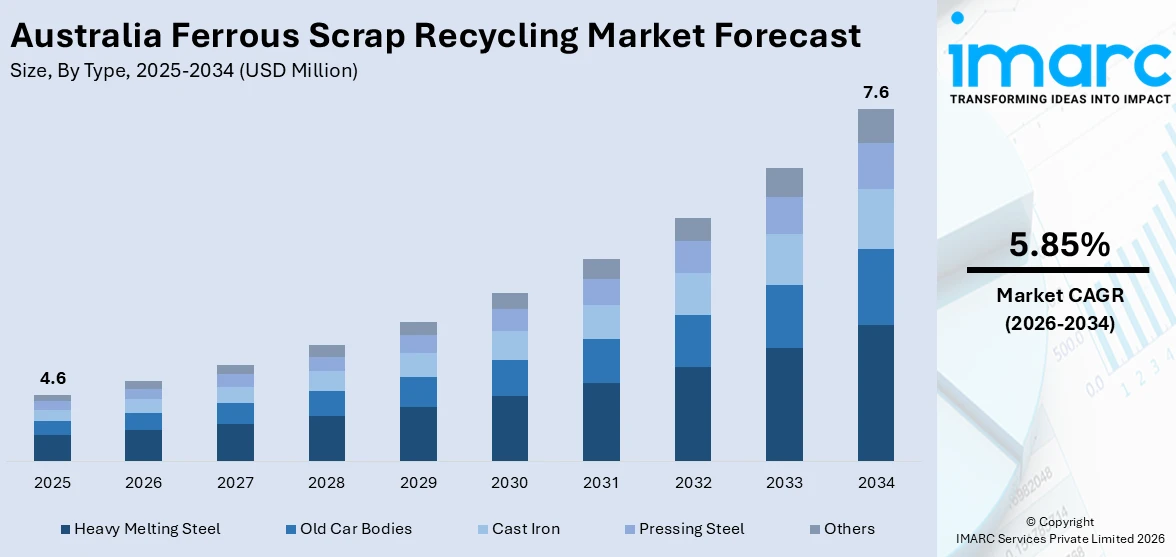

The Australia ferrous scrap recycling market size reached USD 4.6 Million in 2025. Looking forward, the market is expected to reach USD 7.6 Million by 2034, exhibiting a growth rate (CAGR) of 5.85% during 2026-2034. The market is driven by increasing demand for sustainable steel production, particularly through electric arc furnace (EAF) technology which relies heavily on recycled ferrous scrap. In addition to this, government policies supporting decarbonization and waste export restrictions are further encouraging domestic processing and utilization of scrap materials. Additionally, growing activity in the construction and manufacturing sectors is intensifying the demand, further augmenting the Australia ferrous scrap recycling market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 4.6 Million |

| Market Forecast in 2034 | USD 7.6 Million |

| Market Growth Rate 2026-2034 | 5.85% |

Key Trends of Australia Ferrous Scrap Recycling Market:

Increasing Domestic Steel Production and Demand for Scrap-Based Feedstock

A significant trend influencing the market is the growing emphasis on domestic steel production utilizing scrap-based electric arc furnace (EAF) technology. On February 24, 2025, under the Future Made in Australia Innovation Fund, the Australian government unveiled a USD 500 Million investment plan to support the domestic production of steel. The fund will award merit-based grants for manufacturing possibilities, such as projects focused on developing new capabilities in wind tower steel fabrication and adjacent industries. As traditional blast furnace operations give way to more sustainable alternatives, domestic steelmakers are increasing their reliance on recycled ferrous scrap as a primary raw material. Moreover, the government's support for decarbonizing heavy industries through grants and emissions targets is accelerating the adoption of EAF technology, which uses up to 100% of scrap in steelmaking processes. In addition to this, steel manufacturers are making strategic investments in scrap-fed furnaces, which is creating a surge in demand for high-quality recycled scrap domestically. This shift is also driving improvements in scrap sorting, processing, and quality control systems at recycling facilities. Furthermore, as construction and manufacturing sectors rebound post-COVID-19, the need for cost-effective and eco-friendly steel feedstock is reinforcing the requirement for recycled ferrous scrap. Consequently, major players are repositioning themselves as key suppliers to a revitalized domestic steel industry.

To get more information on this market Request Sample

Regulatory and Environmental Pressures Driving Circular Economy Integration

The Australia ferrous scrap recycling market growth is increasingly influenced by regulatory and environmental frameworks that prioritize circular economy principles. According to the New South Wales Government report published in November 2024, Greater Sydney is on the verge of a trash disaster. Without action, landfill capacity is expected to be exhausted by 2030. Therefore, policies aimed at reducing landfill reliance, increasing resource recovery, and lowering carbon emissions are increasing, which is prompting both public and private stakeholders to rethink operational models. Apart from this, the federal government's ban on unprocessed waste exports has forced recycling operators to invest in domestic processing capabilities, including metal shredders, magnetic separators, and advanced sensor-based sorters. Furthermore, environmental compliance standards enforced by the Environment Protection Authorities (EPAs) across states require recyclers to manage air emissions, noise, and hazardous residues more rigorously. Simultaneously, infrastructure funding schemes and green procurement guidelines incentivize recycled content in public construction projects, enhancing the value proposition of recycled ferrous products. These regulatory dynamics are compliance-based and are reshaping the market's strategic focus toward sustainability, transparency, and lifecycle-based material management. As a result, ferrous scrap recyclers are aligning more closely with environmental, social, and governance (ESG) benchmarks to secure long-term viability.

Growth Drivers of Australia Ferrous Scrap Recycling Market:

Increasing Demand for Electric Arc Furnace (EAF) Steelmaking and Local Sourcing

One of the driving forces of the expansion of Australia's ferrous scrap recycling industry is the steel industry's increasing trend toward electric arc furnace (EAF) production, while traditional dependence on blast furnaces wanes. This shift puts increasing pressure on domestic ferrous scrap supply since EAFs are more reliant on recycled metals than virgin ore. By adopting this model, Australia enhances its industrial independence and decreases dependence on imports. Major steel plants close to industry centers like Port Kembla and Whyalla have begun using more quantities of recycled scrap for melting and refining, encouraging recyclers to increase collection, sorting, and processing activities. These plants are making investments in cutting-edge sensor-based sorting and magnetically assisted separation technology to improve ferrous scrap quality. The outcome is a lean supply chain that reconciles scrap availability with EAF steelmaking requirements, enabling local manufacturers to access a more stable, locally based raw material, providing both supply stability and lower transport footprint across Australia's large geography.

Circular Economy Initiatives and Landfill Reduction Policies

Increasing commitment to circular economy values and more stringent environmental regulation play a big part in driving growth in the Australia ferrous scrap recycling market demand. While municipal landfills approach capacity in core metropolitan areas such as Greater Sydney, Melbourne, and Perth, policymakers and local councils increasingly promote metal waste diversion into recycling channels. There is pressure on stakeholders ranging from building demolition companies to manufacturing plants to recycle or sort ferrous metal in-house, instead of landfill disposal or export as mixed waste. This regulatory landscape is encouraging a spike in investments for contemporary recycling plants throughout states, each with cutting-edge material recovery systems to make sure effective separation and reusing of ferrous scrap. Auto shredder residue separation, electromagnet-based sorting, and mechanized conveyor systems are being used to raise recovery percentages. This systemic policy matching with environmental need serves to transform ferrous scrap into a commodity resource while also minimizing waste and creating green employment opportunities for urban and regional Australia.

Infrastructure Projects and Regional Industry Partnership

Another strong impetus according to the Australia ferrous scrap recycling market analysis, is found in its robust development pipeline for infrastructure and increasing partnerships between recyclers and construction or mining industries. Mass infrastructure projects focusing on bridges, rail expansions, and urban renewal, increase the demand for cost-effective yet environmentally friendly materials. Recyclable ferrous materials have become more desirable to use in reinforced steel products and construction hardware, prompting recyclers to cultivate closer relationships with local fabricators. In mining areas like the Outback and Pilbara, where steel is vital for site establishment and upkeep, local recyclers are in league with mining companies to provide recycled scrap material that meets operating needs. Such arrangements tend to incorporate logistics arrangements that capitalize on proximity to regional ports, allowing cost-effective transportation between recycling facilities and heavy industry areas. Furthermore, working with the local councils and recycling companies allows municipal waste metal e.g., retired assets and obsolete machinery, to be gleaned, processed, and recycled back into infrastructure applications. This coordinated, regionally focused strategy allows ferrous scrap recycling to not just be a tool for waste minimization but rather a pillar within the material circulation system in Australia, contributing to both urban and regional development.

Opportunities of Australia Ferrous Scrap Recycling Market:

Integrated Supply Chains and Regional Manufacturing Hubs

Australia's ferrous scrap recycling industry is particularly well-placed to supply the nation's growing regional manufacturing clusters with near-source, high-quality recycled feedstock. Plants in large industrial hubs like Port Kembla, Whyalla, and Brisbane's outer suburbs provide the best opportunity for scrap recyclers to establish vertically integrated supply chains. Through association with regional steel fabricators and secondary producers, recycling operators can align logistics to transport materials economically and with short transit time. This strategy simplifies operations and enhances resilience in distant and coastal manufacturing operations, where conventional raw materials would otherwise need to be imported from abroad. In addition, recyclers can supply customized feedstock grades to individual industries, whether prefabricated rail parts, agribusiness equipment, or ship repairs, enhancing regional value chains. By utilizing location advantage, recyclers can lower the cost of logistics, deliver on a just-in-time basis, and retain more of the downstream value creation from Australian producers, enhancing circularity in regional economies.

Infrastructure Renewal and Green Construction Advantage

Australia's expansive government public infrastructure projects, ranging from upgradation of rails to suburban housing and inner-city regeneration, present a prime opportunity for ferrous scrap recyclers to provide sustainably produced materials. With mounting concern about green building credentials, government departments and developers alike are now more amenable to integrating recycled metals into building structures, rebar, and reinforcing. Recyclers who serve markets such as the Outback's mining communities and coastal cities with high-speed rail or water projects can market locally recycled ferrous products as green alternatives to virgin steel. These opportunities enable recycling companies to become more than just waste managers but also key players in sustainable infrastructure construction. They can also take advantage of municipal green procurement policies through displaying recycled content and reduced embodied carbon. With increasing awareness of carbon footprint and compliance requirements, ferrous scrap recyclers can position their products in alignment with the sustainability objectives of public works, thus making their business more market-relevant to both rural and urban infrastructure projects.

Innovation Partnerships and Diversified Product Development

A rich field of opportunity for Australia's ferrous scrap recycling industry is the arena of innovation and product diversification through collaboration with research institutions and industry leaders. Universities and government-supported research laboratories in Victoria, New South Wales, and Queensland are researching emerging recycling technologies, like sensor-aided sorting, metal alloy separation, and effective decontamination systems. Access to these institutions allows recycling businesses to test new processing technologies, commercialize specialty products, and produce specialty alloy combinations for new end applications such as custom automobile components or heat-resistant devices. Industrial partnerships with car assembly factories, renewable energy system installers, and heavy equipment makers can result in co-development of tailored ferrous materials that meet precise performance specifications. Such initiatives provide avenues to higher-value streams of revenue, above typical scrap commodity sales. Recyclers can also draw on circular economy research funds and financing incentives, which enable them to experiment with technology such as bio-adaptive adhesives or composite scrap blends. By transforming themselves from commodity processors into solution-based suppliers, ferrous recyclers can become more competitive and positioning themselves as innovators within the larger Australian recycling ecosystem.

Government Support for Australia Ferrous Scrap Recycling Market:

State and Federal Policies Promoting Local Recycling Infrastructure

Australian governments, both federal and state, have begun to recognize the strategic value of domestic recycling infrastructure, especially in the ferrous scrap industry. Major manufacturing and industrial centers such as Whyalla in South Australia and Port Kembla in New South Wales have been at the center of policy and investment incentive strategies to create new scrap-processing plants. Government authorities are providing grants, tax abatements, or land-lease concessions to recyclers who install new processing facilities or upgrade equipment locally, solidifying the circular economy in local economies. The government initiatives also spur the adoption of technologies like magnetic separation, shredder residue systems, and enclosed processing systems by recyclers to comply with increasingly stringent environmental standards. In fact, public support closes the gap between rural or regional scrappers and metropolitan processing capacity, promoting industrial resilience as it also eliminates reliance on waste export. By promoting growth and technological upgrading in selected recycling areas, Australia's public institutions are establishing foundations for longer-term, geographically dispersed ferrous scrap recycling capacity.

Recycled Content Mandates and Green Procurement Drives

Another strong reflection of government backing appears through procurement policies with preferences for recycled content used in infrastructure and building projects. In Australia's capital cities and regional shires, governments have started to include requirements, or at least strong preferences, for ferrous materials containing certified recycled content. This is particularly evident on large-scale public works such as rail expansions, bridge replacements, and local road upgrades. Reforms to public-sector procurement aim to lower embodied carbon by enabling the use of recycled metals. Local councils in states like Victoria and Queensland have even introduced trial programs mandating a minimum proportion of publicly commissioned construction comprising recycled steel or ferrous materials. Such requirements establish assured channels of demand for ferrous recyclers and convey to private companies that recycled-origin materials are both viable and preferable. In the long term, such procurement commitment builds supplier confidence, fosters enlargement of recycling business, and spurs more meaningful collaboration between governments and local recyclers for a more circular, locally resilient material economy.

Regulatory Streamlining and Skills Development Support

Australian governments are also making strides on regulatory harmonization and skills capacity-building to facilitate ferrous scrap recycling. Awakening to the fact that varied licensing or environmental laws from state to state can hinder growth, national task forces are harmonizing requirements for approvals of recycling facilities, transportation permits, and pollution controls. Simplifying these decreases administrative complexity and allows recyclers to expand across borders more easily and predictably. Also, authorities in Western Australia and Tasmania are testing training schemes, frequently in conjunction with technical schools and industry associations, to provide workers with skills in new sorting technologies, safety procedures in metal handling, and environmental regulation. These schemes are particularly targeted at the needs of smaller recyclers or those in regional locations, where formal training tends to be less available. Through investment in both workforce upskilling and regulatory clarity, government programs are making the sector more resilient in its ability to support operational expansion and technology take-up, along with promoting rural employment and industry modernization throughout Australia.

Challenges of Australia Ferrous Scrap Recycling Market:

Geographic Dispersion and Logistics Challenges

The vast geographic extent of Australia, with its depopulated interior and faraway industrial centers, poses the main challenge to the effectiveness of ferrous scrap recycling activities. It involves significant logistical challenges to move heavy metal products from rural terminals to seashore processing facilities, or the reverse. The Outback, Pilbara, and Bowen Basin are remote mining areas that produce excesses of scrap metal due to equipment dismantling, but do not have close-by recycling facilities. It is this imbalance between scrap generation and available processing facilities that pushes up the costs and makes planning more difficult. Equally, urban recyclers in Melbourne, Sydney, or Perth encounter congestion, restricted access areas, and infrastructural limitations affecting efficient scrap flow. Such geographic and infrastructural issues increase operational costs and lower the competitiveness of recycled feedstock against imported virgin materials. Defeat of these challenges necessitates strategic investment in local collection depots, optimal transport routes, and small-scale processing capacity near scrap sources, albeit the size of the nation makes such deployment expensive and complicated.

Industry Fragmentation and Constrained Resources

The other major challenge is the industry's fragmented structure, comprising a concentration of small, frequently family-owned operations with some medium-sized enterprises. These companies often face shortages of capital, restricted access to high-end processing technology, and shortages in expanding operations to accommodate increasing supply. Independent recyclers do not have the same capital flexibility as integrated metal groups to purchase state-of-the-art sorting equipment, sensor-based separation equipment, or regular maintenance. This leaves them unable to generate higher-grade scrap material for use in specialized applications, i.e., electric arc furnace feed or construction-grade rebar. Additionally, the volatility of supply resulting from changing volumes of scrap due to local economic conditions, hindering these operators from being able to predict demand and preserve investment confidence. Lacking structural consolidation, shared infrastructure, or cooperative structures, the fragmented environment prevents the industry from modernizing, having uniform quality, and being competitive against more dominant, better-financed rivals.

Regulatory Complexities and Market Uncertainties

Dealing with the changing regulatory landscape is an ongoing issue for ferrous scrap recyclers throughout Australia. Differing environmental requirements, licensing, and waste management rules can be applied by each state and territory. For instance, urban councils can apply strict noise, dust, and pollutant emission regulations, requiring high compliance costs and administrative burdens. In contrast, rural areas could lack clarity or enforcement uniformity, subjecting operators growing across jurisdictions to uncertainty. In addition, global market volatility and regulatory changes influence scrap export dynamics, as some of the ferrous metal gathered is usually headed for foreign buyers. Shifts in trade policy or export quotas can stimulate abrupt demand changes, subjecting recyclers to market fluctuation risk. In the domestic arena, public procurement policy regarding recycled content could differ by state or project, resulting in mixed demand signals. These multiple layers of regulatory and market risks undermine long-term investment choice and strategic decision-making. Solving this problem would need more aligned national systems, procurement clarity, and more transparent regulatory routes.

Australia Ferrous Scrap Recycling Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type, application, and end user.

Type Insights:

- Heavy Melting Steel

- Old Car Bodies

- Cast Iron

- Pressing Steel

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes heavy melting steel, old car bodies, cast iron, pressing steel, and others.

Application Insights:

Access the comprehensive market breakdown Request Sample

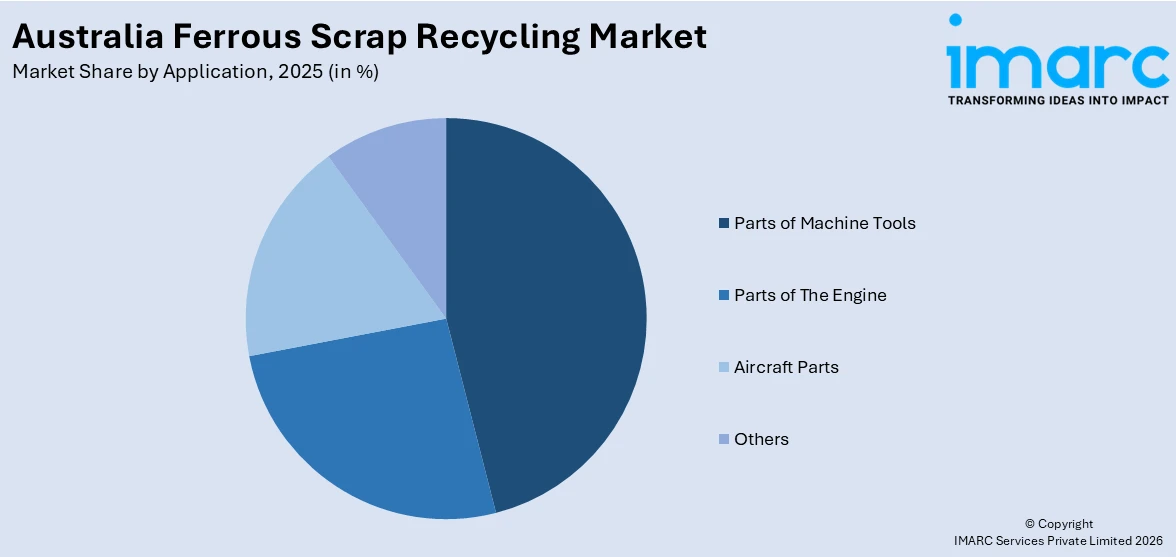

- Parts of Machine Tools

- Parts of The Engine

- Aircraft Parts

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes parts of machine tools, parts of the engine, aircraft parts, and others.

End User Insights:

- Construction

- Automotive

- Shipbuilding

- Equipment Manufacturing

- Consumer Appliances

- Others

The report has provided a detailed breakup and analysis of the market based on the end user. This includes construction, automotive, shipbuilding, equipment manufacturing, consumer appliances, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Ferrous Scrap Recycling Market News:

- In January 2025, ICD, a recycling firm from Sheffield, announced the establishment of a new plant in Canning Vale, Western Australia, aimed at recovering and processing essential minerals and valuable metals. The metals will be marketed as specialty alloys to industrial clients in Australia, Japan, Korea, and Southeast Asia. Australia possesses abundant critical minerals, yet it has restricted capability to extract them from scrap metal. This will alter in 2025.

- In August 2025, Sims Ltd., a Sydney-based company specializing in metals and electronics recycling with worldwide operations, announced that it has signed a nonbinding memorandum of understanding (MOU) to create a scrap supply and services agreement with the proprietors of the planned Alter Steel mill in Australia. Sims announces it has entered into the MOU with Equest Steel Pty. Ltd. has named its planned recycled-content electric arc furnace (EAF) steel rebar mill Alter Steel. The mill is set to be constructed in Pinkenba, located in Queensland, Australia.

- In April 2024, the Australian Steel Institute (ASI) presented a proposal to the Australian Senate aimed at prohibiting the export of unprocessed steel scrap from Australia. According to a note reviewed by Kallanish, the waste reduction and recycling policies aim to maximize waste management and promote a circular economy in the nation, as steel scrap is reported by ASI to be a sovereign, rare, and increasingly valuable resource. Unprocessed steel scrap consists of automotive components and household appliances mixed with plastics and other items that are prohibited from export, according to the document.

Australia Ferrous Scrap Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Heavy Melting Steel, Old Car Bodies, Cast Iron, Pressing Steel, Others |

| Applications Covered | Parts of Machine Tools, Parts of The Engine, Aircraft Parts, Others |

| End Users Covered | Construction, Automotive, Shipbuilding, Equipment Manufacturing, Consumer Appliances, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia ferrous scrap recycling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia ferrous scrap recycling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia ferrous scrap recycling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Ferrous Scrap Recycling Market Report

The Australia ferrous scrap recycling market was valued at USD 4.6 Million in 2025.

The Australia ferrous scrap recycling market is projected to exhibit a CAGR of 5.85% during 2026-2034.

The Australia ferrous scrap recycling market is expected to reach a value of USD 7.6 Million by 2034.

The Australia ferrous scrap recycling market is witnessing trends such as increased adoption of advanced sorting technologies, rising domestic consumption due to infrastructure growth, and stronger regional recycling networks. There is s also a noticeable shift toward sustainability, with recyclers aligning operations to meet green construction demands and environmental compliance standards nationwide.

The Australia ferrous scrap recycling market is driven by the transition to electric arc furnace steelmaking, increasing focus on circular economy practices, and rising infrastructure development. Local sourcing of recycled metals and supportive environmental regulations further encourage domestic processing, aligning with sustainability goals and reducing reliance on imported raw materials.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)