Australia Fertility Services Market Size, Share, Trends and Forecast by Cause of Infertility, Procedure, Service, End User, and Region, 2026-2034

Australia Fertility Services Market Overview:

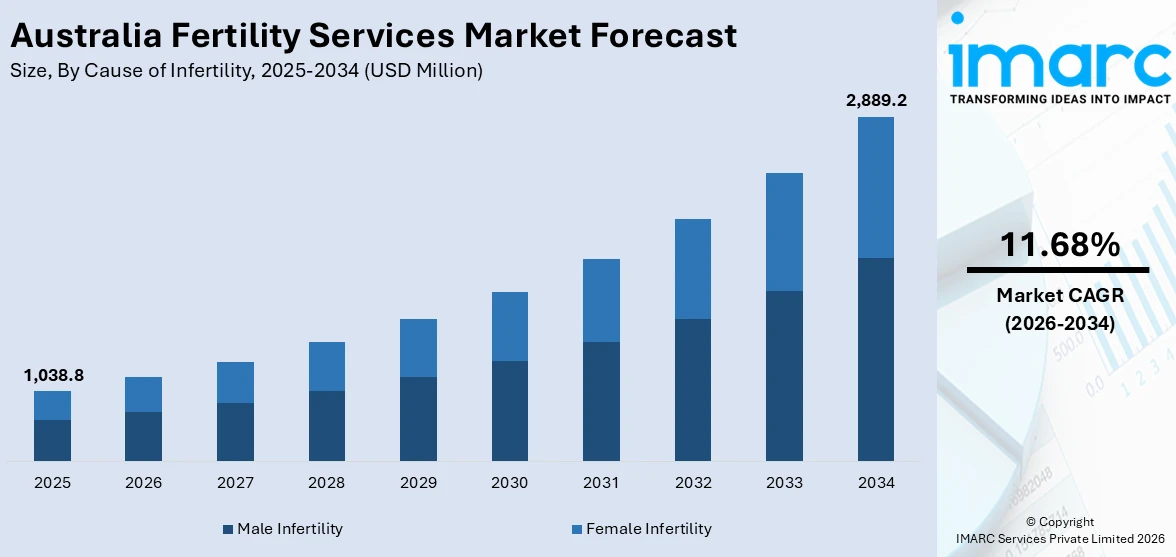

The Australia fertility services market size reached USD 1,038.8 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 2,889.2 Million by 2034, exhibiting a growth rate (CAGR) of 11.68% during 2026-2034. Rising demand driven by delayed parenthood, increased infertility diagnoses, broader awareness, technological advances like genetic screening, and growing adoption of fertility preservation highlight the sector’s momentum. These drivers, combined with expanding accessibility and supportive healthcare initiatives, are some of the factors contributing to Australia fertility services market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1,038.8 Million |

| Market Forecast in 2034 | USD 2,889.2 Million |

| Market Growth Rate 2026-2034 | 11.68% |

Australia Fertility Services Market Trends:

Expanding Access to Reproductive Healthcare

The fertility services market in Australia is seeing growth as affordability and access to reproductive treatments improve. Broader availability of advanced contraceptives, targeted therapies for conditions like endometriosis, and wider use of hormone-based support for IVF are reshaping patient care pathways. These developments reduce cost barriers, encouraging more individuals to pursue family planning and fertility treatments earlier. The market is also benefiting from increased demand for specialized clinics that can deliver comprehensive reproductive care. With supportive healthcare policies and rising awareness of treatment options, providers are expected to see higher patient volumes, stronger adoption of innovative therapies, and a more inclusive approach to reproductive health across the country. These factors are intensifying the Australia fertility services market growth. For example, in March 2025, the Australian Government expanded Pharmaceutical Benefits Scheme listings to make contraception, endometriosis treatments, and IVF medications more accessible. The new listings include Slinda (progestogen-only contraceptive), Ryeqo (endometriosis), and broader access to Pergoveris (IVF hormone therapy).

To get more information on this market Request Sample

Public Support for Fertility Care

Fertility services in Queensland are being reshaped through new public funding that improves access for residents affected by serious illnesses such as cancer. The initiative directs resources toward subsidized assisted reproductive technology within public hospitals, reducing financial strain for patients who often face additional medical costs. Alongside clinical support, counselling services are being integrated to address the emotional and psychological challenges linked to treatment. This approach not only broadens access to fertility care but also emphasizes patient well-being through combined medical and emotional support. The policy shift is expected to strengthen demand for fertility services in the state, foster equitable access across income groups, and set a precedent for integrating reproductive care into broader public health planning. For instance, in March 2024, Queensland’s government unveiled a public funding package to expand fertility treatment access for residents who have faced serious illnesses like cancer. The initiative allocates funds for subsidized assisted reproductive technology in public hospitals and includes counselling services to support those undergoing treatment.

Australia Fertility Services Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on cause of infertility, procedure, service, and end user.

Cause of Infertility Insights:

- Male Infertility

- Female Infertility

The report has provided a detailed breakup and analysis of the market based on the cause of infertility. This includes male infertility and female infertility.

Procedure Insights:

- In Vitro Fertilization with Intracytoplasmic Sperm Injection (IVF with ICSI)

- Surrogacy

- In Vitro Fertilization Without Intracytoplasmic Sperm Injection (IVF without ICSI)

- Intrauterine Insemination (IUI)

- Others

The report has provided a detailed breakup and analysis of the market based on the procedure. This includes in vitro fertilization with intracytoplasmic sperm injection (IVF with ICSI), surrogacy, in vitro fertilization without intracytoplasmic sperm injection (IVF without ICSI), intrauterine insemination (IUI), and others.

Service Insights:

- Fresh Non-Donor

- Frozen Non-Donor

- Egg and Embryo Banking

- Fresh Donor

- Frozen Donor

The report has provided a detailed breakup and analysis of the market based on the service. This includes fresh non-donor, frozen non-donor, egg and embryo banking, fresh donor, and frozen donor.

End User Insights:

Access the comprehensive market breakdown Request Sample

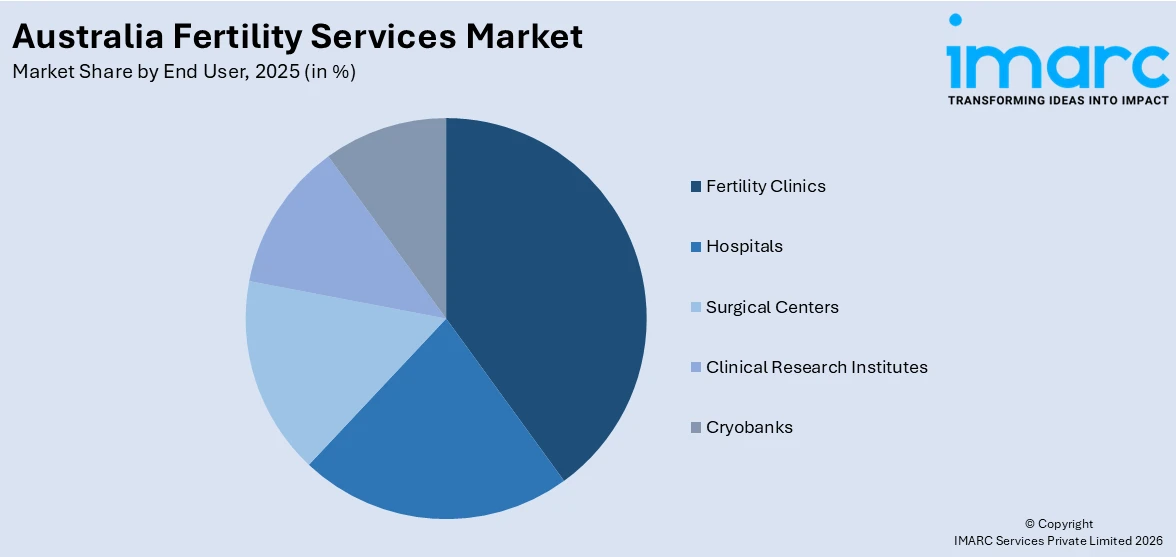

- Fertility Clinics

- Hospitals

- Surgical Centers

- Clinical Research Institutes

- Cryobanks

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes fertility clinics, hospitals, surgical centers, clinical research institutes, and cryobanks.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Fertility Services Market News:

- In April 2025, the Victorian government marked a milestone as over 150 babies were born through Australia’s first free public fertility program. The initiative also operates through satellite clinics across regional areas and is supported by the first public egg and sperm bank at the Royal Women’s Hospital.

Australia Fertility Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Cause of Infertilities Covered | Male Infertility, Female Infertility |

| Procedures Covered | In Vitro Fertilization with Intracytoplasmic Sperm Injection (IVF with ICSI), Surrogacy, In Vitro Fertilization Without Intracytoplasmic Sperm Injection (IVF without ICSI), Intrauterine Insemination (IUI), Others |

| Services Covered | Fresh Non-Donor, Frozen Non-Donor, Egg and Embryo Banking, Fresh Donor, Frozen Donor |

| End Users Covered | Fertility Clinics, Hospitals, Surgical Centers, Clinical Research Institutes, Cryobanks |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia fertility services market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia fertility services market on the basis of cause of infertility?

- What is the breakup of the Australia fertility services market on the basis of procedure?

- What is the breakup of the Australia fertility services market on the basis of service?

- What is the breakup of the Australia fertility services market on the basis of end user?

- What is the breakup of the Australia fertility services market on the basis of region?

- What are the various stages in the value chain of the Australia fertility services market?

- What are the key driving factors and challenges in the Australia fertility services market?

- What is the structure of the Australia fertility services market and who are the key players?

- What is the degree of competition in the Australia fertility services market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia fertility services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia fertility services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia fertility services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)