Australia Firearms Market Size, Share, Trends and Forecast by Type, Technology, Operation, End Use, and Region, 2026-2034

Australia Firearms Market Summary:

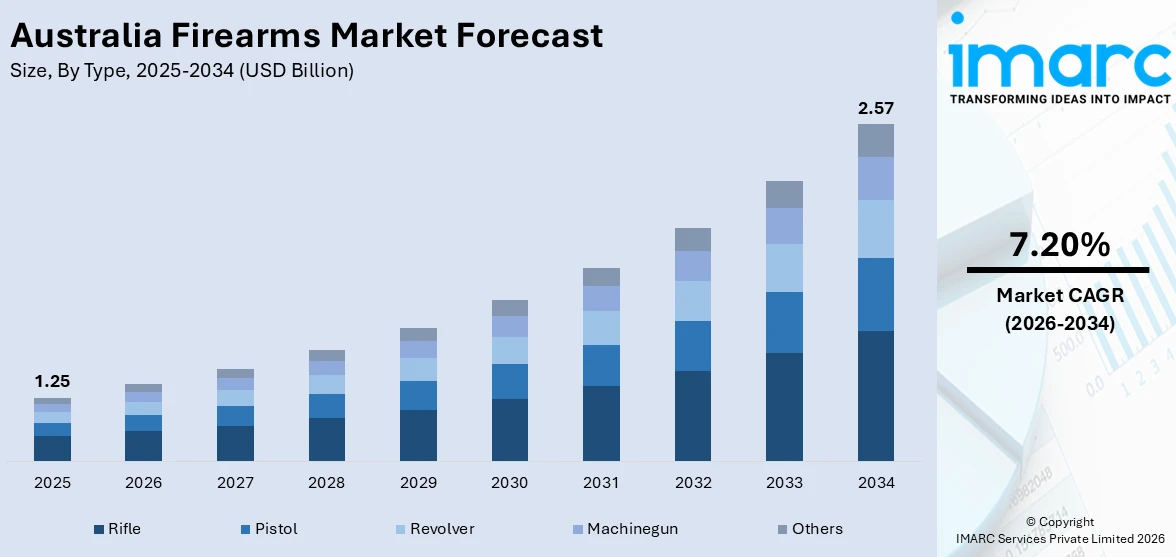

The Australia firearms market size was valued at USD 1.25 Billion in 2025 and is projected to reach USD 2.57 Billion by 2034, growing at a compound annual growth rate of 7.20% from 2026-2034.

The market is driven by a strong outdoor sporting culture, consistent demand from agricultural and pest management operations, and escalating government investment in defense modernization. Growing participation in licensed hunting and competitive shooting disciplines continues to fuel demand across regulated firearm categories, while advancing military procurement strategies stimulate institutional purchasing. Rising national security imperatives further accelerate spending on modern firearm platforms across defense forces, collectively reinforcing momentum across the Australia firearms market share.

Key Takeaways and Insights:

- By Type: Rifle dominates the market with a share of 46.8% in 2025, driven by widespread use in sport shooting, hunting activities, and strong consumer preference for precision firearms.

- By Technology: Unguided leads the market with a share of 97.2% in 2025, owing to lower cost, simpler operation, and broad accessibility across recreational and professional user segments.

- By Operation: Manual represents the largest segment with a market share of 49.7% in 2025, driven by affordability, regulatory ease, and strong adoption among recreational shooters and hunting communities.

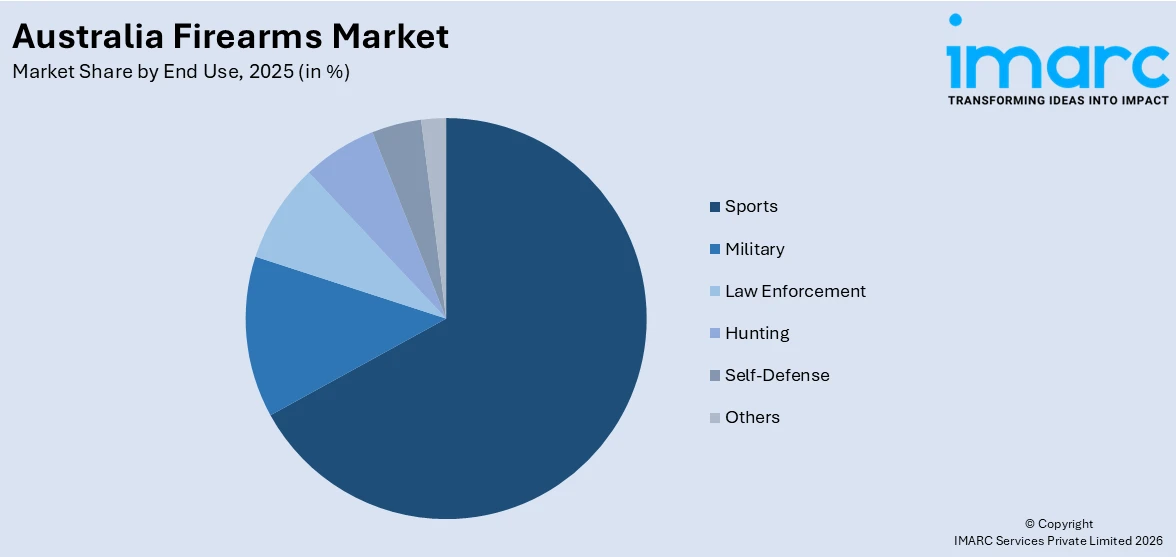

- By End Use: Sports dominates the market with a share of 66.4% in 2025, owing to rising participation in competitive shooting, organized sporting events, and growing recreational firearm culture.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 34.2% in 2025, driven by high population concentration, established sporting clubs, and strong retail infrastructure.

- Key Players: The market exhibits a moderately competitive landscape, with established domestic and international manufacturers competing on product innovation, regulatory compliance, pricing strategies, and distribution network strength across sporting, hunting, and recreational end-use segments.

To get more information on this market Request Sample

The Australia firearms market operates across a complex and multifaceted demand landscape shaped by regulatory, cultural, and strategic forces. Rural communities maintain a foundational reliance on firearms for livestock protection and the control of invasive feral species that threaten agricultural output and ecological balance. Urban and regional sporting communities, organized through established shooting federations and licensed clubs, sustain consistent demand for performance-oriented platforms across a range of competitive and recreational disciplines. According to reports, Thales Australia officially opened a new advanced manufacturing facility at its Lithgow Arms site in New South Wales to support the precision manufacture and testing of next-generation weapon systems for the Australian Defence Force. At the institutional level, the Australian defence force's ongoing capability modernization program, supported by a long-term commitment to increased defense expenditure, creates a structurally significant demand channel that extends well beyond the civilian market and reinforces the ecosystem serving suppliers, importers, and manufacturers operating in this space.

Australia Firearms Market Trends:

Rising Preference for Modular and Customizable Precision Rifle Platforms

A prominent trend reshaping the Australia firearms market is the growing preference among licensed civilian owners for modular precision rifle systems that allow for personalized configuration. Competitive sport shooters and field hunters are increasingly seeking bolt-action platforms with interchangeable caliber options, adjustable stock assemblies, and broad compatibility with aftermarket accessories. As per sources, in January 2026, the Australian Department of Home Affairs reported that more than 4 million registered firearms and about 929,741 firearm licences were recorded nationwide, reflecting continued participation in regulated shooting and hunting activities. This shift reflects the maturation of Australia's shooting sports culture, where participants are moving beyond entry-level equipment toward purpose-built solutions that support specific disciplines.

Growing Integration of Advanced Optics and Tactical Accessories

A significant trend across the Australia firearms market is the increasing adoption of sophisticated optical sighting systems and tactical accessories by both civilian sport shooters and law enforcement agencies. Licensed sporting and hunting users are investing in variable-magnification scopes, illuminated reticle systems, and mounting solutions that enhance target acquisition and accuracy at extended distances. In April 2024, the Australian Government committed about $161.3 million over four years to establish a National Firearms Register that will provide police with near real-time nationwide data on firearms, owners, and licences to improve enforcement and safety coordination. Law enforcement bodies are similarly upgrading issued firearms with compatibility-focused accessory solutions that improve operational effectiveness.

Strengthening Focus on Sovereign Defence Manufacturing and Local Supply Chains

A defining structural trend within the Australia firearms market is the accelerating policy emphasis on building a sovereign defence industrial base capable of supporting domestic small arms production and supply chain resilience. Government strategies have placed priority on enabling local firms to participate in the manufacture, assembly, and sustainment of military firearm platforms and associated systems. According to reports, the Australian Criminal Intelligence Commission estimated that around 200,000 illicit firearms remain in circulation across Australia, including approximately 190,000 long-arms and 10,000 handguns, highlighting the continued focus of law-enforcement and regulatory agencies on firearm monitoring and control initiatives. This is encouraging partnerships between established international defence suppliers and Australian industrial partners, fostering technology transfer and indigenous capability development.

Market Outlook 2026-2034:

The Australia firearms market is poised for consistent and sustained growth across the forecast period, supported by a convergence of expanding national defence investment, a resilient civilian sporting and agricultural demand base, and the progressive development of sovereign defence manufacturing capacity. Increasing participation in licensed shooting disciplines, combined with deepening institutional procurement driven by military modernization priorities, will continue to broaden the market's revenue foundations. Regulatory evolution and strategic security imperatives are expected to further shape product demand and market structure throughout the outlook period. The market generated a revenue of USD 1.25 Billion in 2025 and is projected to reach a revenue of USD 2.57 Billion by 2034, growing at a compound annual growth rate of 7.20% from 2026-2034.

Australia Firearms Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Type |

Rifle |

46.8% |

|

Technology |

Unguided |

97.2% |

|

Operation |

Manual |

49.7% |

|

End Use |

Sports |

66.4% |

|

Region |

Australia Capital Territory & New South Wales |

34.2% |

Type Insights:

- Pistol

- Revolver

- Rifle

- Machinegun

- Others

Rifle dominates with a market share of 46.8% of the total Australia firearms market in 2025.

Rifle holds the largest share of the Australia firearms market, reflecting its unmatched versatility across the diverse range of licensed applications that define civilian and institutional demand in the country. Bolt-action and lever-action rifle configurations occupy a privileged position within Australia's regulatory framework, as they represent the most broadly accessible platform class available to licensed civilian owners. This regulatory alignment, combined with the rifle's suitability for sport shooting, competitive marksmanship, and field use, cements its dominance.

Demand for rifles continues to evolve as licensed users seek increasingly specialized configurations suited to their specific disciplines. The growing popularity of precision long-range shooting has accelerated interest in higher-specification platforms featuring adjustable stock assemblies, enhanced barrel profiles, and modular components that allow for personalized setup. Manufacturers serving the Australian market have responded by expanding product lines that balance technical performance with regulatory compliance, reinforcing the segment's position as the most commercially active and product-diverse category within the broader firearms market landscape.

Technology Insights:

- Guided

- Unguided

Unguided leads with a share of 97.2% of the total Australia firearms market in 2025.

Unguided holds the commanding position across the Australia firearms market, a reflection of the foundational role that conventional firearm platforms play across civilian, law enforcement, and military demand channels. For licensed civilian owners engaged in sporting, hunting, and agricultural applications, unguided configurations offer mechanical reliability, operational simplicity, and cost-effective performance that satisfies the requirements of everyday use. Their broad compatibility with accessories, optics, and maintenance solutions further entrenches their position as the default technology choice across all end-use categories operating within Australia's regulatory framework.

Within institutional procurement channels, unguided platforms continue to serve as the primary equipment standard for law enforcement agencies and conventional military units. The established supply infrastructure supporting unguided firearms, including authorized dealer networks, certified service providers, and domestic distributors, ensures consistent product availability and after-sales support across all regions. As the civilian and institutional segments expand in parallel, the unguided category benefits from both organic demand growth and the deepening of the commercial ecosystem that surrounds its procurement, distribution, and ongoing maintenance across the Australian market.

Operation Insights:

- Automatic

- Semi-Automatic

- Manual

Manual exhibits a clear dominance with a 49.7% share of the total Australia firearms market in 2025.

Manual leads the Australia firearms market, a dominance that is structurally reinforced by the country's national regulatory framework governing civilian firearm ownership. Bolt-action and lever-action configurations represent the most widely permitted classes for licensed private owners, making manual-action platforms the natural default for the civilian sporting and agricultural segments. For rural landholders engaged in pest control and for competitive shooters participating in licensed disciplines, manual firearms deliver reliable field performance within the boundaries of permissible ownership, establishing this category as the most commercially significant operation type in the civilian market.

The enduring strength of the manual segment is further supported by the broad range of quality platforms available through authorized domestic retailers and licensed importers serving the Australian market. Established manufacturers have consistently invested in refining manual-action designs to meet the expectations of experienced users who prioritize accuracy, trigger quality, and long-term mechanical durability. As participation in precision shooting disciplines grows and rural demand remains stable, the manual segment continues to attract both first-time licensed buyers seeking an entry point into ownership and experienced shooters investing in upgraded configurations tailored to their specific sporting or practical requirements.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Military

- Law Enforcement

- Sports

- Hunting

- Self-Defense

- Others

Sports leads with a market share of 66.4% of the total Australia firearms market in 2025.

Sports represents the largest demand category within the Australia firearms market, underpinned by a well-organized ecosystem of registered shooting clubs, licensed competition venues, and structured participation programs that collectively sustain a broad and growing base of active firearm users. As per sources, the Sporting Shooters’ Association of Australia (SSAA) reported a membership base of more than 220,000 licensed firearm owners and sport shooters nationwide, making it one of the largest organised communities for competitive shooting and sporting firearm participation in Australia.

As participants advance within their respective disciplines, purchasing behavior shifts toward higher-specification platforms and premium accessories that deliver improved performance. This dynamic progression supports a layered demand structure in which both new entrants and experienced competitors contribute to market revenue at different price points. The expansion of national and state-level competition calendars, combined with growing visibility of shooting sports within the broader recreational landscape, continues to attract new license holders into organized sporting frameworks, reinforcing the segment's role as the primary growth engine of the civilian firearms market.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales dominates with a market share of 34.2% of the total Australia firearms market in 2025.

Australia Capital Territory & New South Wales form the largest regional market within the Australia firearms market, supported by the highest concentration of licensed firearm holders and registered shooting infrastructure in the country. New South Wales hosts an extensive network of authorized dealers, sporting ranges, and affiliated clubs that collectively generate consistent retail and aftermarket activity across both metropolitan and regional areas. The depth of the state's sporting shooting community, combined with strong rural demand from agricultural regions across the state's interior, provides this regional cluster with a broad and diversified demand base.

Australia Capital Territory & New South Wales contributes an institutional dimension to this regional market through the concentration of federal defence establishments and government agencies in the Canberra metropolitan area. Defence-linked procurement activity channeled through institutional buyers in the region reinforces the cluster's overall revenue significance beyond what civilian demand alone would generate. The combination of high licensed civilian ownership density, well-developed retail and service infrastructure, and meaningful institutional procurement component distinguishes as the most commercially active and structurally diverse regional market across the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Australia Firearms Market Growing?

Expanding Participation in Licensed Shooting Sports and Recreational Activities

Australia's organized shooting sports ecosystem continues to serve as a foundational demand driver for the firearms market. A well-established network of registered clubs, licensed ranges, and structured training programs sustains growing participation across competitive and recreational disciplines. In 2024, an Australian Sports Commission review found that approximately 27,000 Australians aged 15 and over participated in shooting sports at least once, highlighting broad engagement in formal and casual disciplines. As more licensed individuals engage with precision, field, and clay target formats, demand for performance-oriented platforms and specialized accessories rises correspondingly.

Sustained Agricultural and Rural Demand for Pest and Feral Animal Control

Across Australia's extensive pastoral and cropping regions, firearms remain indispensable tools for managing invasive feral species that threaten livestock, crops, and native ecosystems. State licensing frameworks formally recognize pest control as a legitimate ownership purpose, embedding this demand within a regulated and structurally stable channel. Rural landholders consistently require reliable, field-appropriate firearm platforms suited to the practical demands of property management. This utilitarian requirement operates independently of sporting trends, providing the market with a geographically distributed and persistently active demand source throughout rural and regional Australia.

Escalating National Defence Investment and Australian Defence Force Modernization

Australia's commitment to significantly increasing defence expenditure over the coming decade is creating a structurally important demand channel for military-grade firearm platforms and small arms systems. The Australian defence force's capability modernization agenda prioritizes infantry equipment upgrades and procurement of advanced platforms aligned with evolving regional security requirements. In the 2024–25 defence budget, the government allocated a record A$55.7 billion for national defence spending, including funding for new military acquisitions and capability upgrades across the ADF. Long-term defence budgeting provides forward procurement visibility that supports sustained institutional purchasing activity.

Market Restraints:

What Challenges the Australia Firearms Market is Facing?

Expanding Participation in Licensed Shooting Sports and Recreational Activities

Australia's organized shooting sports ecosystem serves as a foundational demand driver, sustained by a well-established network of registered clubs, licensed ranges, and structured training programs. Growing participation across competitive and recreational disciplines elevates demand for performance-oriented platforms and specialized accessories. This cultural engagement creates a durable and self-reinforcing civilian demand base that supports consistent market activity across the forecast period.

Sustained Agricultural and Rural Demand for Pest and Feral Animal Control

Across Australia's extensive pastoral and cropping regions, firearms remain indispensable tools for managing invasive feral species that threaten livestock, crops, and native ecosystems. State licensing frameworks formally recognize pest control as a legitimate ownership purpose, embedding this demand within a regulated and stable channel. This utilitarian requirement operates independently of sporting trends, providing the market with a persistently active and geographically distributed rural demand source.

Escalating National Defence Investment and Australian Defence Force Modernization

Australia's long-term commitment to increasing defence expenditure is creating a structurally significant demand channel for military-grade firearm platforms and small arms systems. The Australian Defence Force's capability modernization agenda prioritizes infantry equipment upgrades aligned with evolving regional security requirements. Sustained government investment reinforces the institutional segment and creates downstream opportunities for domestic manufacturers and authorized suppliers participating in expanding defence procurement programs.

Competitive Landscape:

The Australia firearms market features a moderately competitive landscape characterized by a combination of established domestic distributors, internationally licensed importers, and defence-aligned supply chain participants. Competition is shaped primarily by regulatory compliance expertise, product portfolio depth, established dealer networks, and specialization across civilian sporting, law enforcement, and military procurement channels. Institutional buyers serving defence and law enforcement requirements favor suppliers with demonstrated experience in government contracting and sustained supply capacity. In the civilian segment, brand credibility, accessory compatibility, and the quality of after-sales service and technical support are the primary factors influencing purchasing decisions among licensed firearm owners and sporting users.

Recent Developments:

- In April 2025, the Australian Defence Force began fielding the new F9 Sidearm Weapon System, a modular 9 mm pistol based on the SIG Sauer P320 X‑Carry Pro. Supplied by NIOA, it replaces the Browning Mk3 under the AUD 500 million LAND 300 Lethality Program, enhancing small arms capabilities across Army, Navy, and Air Force units.

Australia Firearms Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Pistol, Revolver, Rifle, Machinegun, Others |

| Technologies Covered | Guided, Unguided |

| Operations Covered | Automatic, Semi-Automatic, Manual |

| End Uses Covered | Military, Law Enforcement, Sports, Hunting, Self-Defense, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Firearms Market Report

The Australia firearms market size was valued at USD 1.25 Billion in 2025

The Australia firearms market is expected to grow at a compound annual growth rate of 7.20% from 2026-2034 to reach USD 2.57 Billion by 2034.

Rifle holds the largest share of the Australia firearms market, driven by its widespread use across sport shooting, competitive marksmanship, and rural pest management operations, along with its alignment with civilian licensing provisions that make it the most broadly accessible and commonly owned firearm category.

Key factors driving the Australia firearms market include a deeply rooted outdoor sporting and recreational shooting culture, consistent utilitarian demand from agricultural and pest management operations across rural regions, and a sustained expansion of national defence expenditure directed toward modernizing Australian defence force small arms capabilities and procurement capacity.

Major challenges facing the Australia firearms market include stringent and evolving regulatory frameworks that constrain civilian access to certain firearm categories, vulnerability to policy-driven buyback programs and supply disruptions triggered by public safety developments, and ongoing pressure from illicit firearm activity that intensifies scrutiny on the legitimate licensed market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)